a beer bba - university of chicago law school beer bba university of chicago federal tax conference...

TRANSCRIPT

ABe%erBBAUniversityofChicagoFederalTaxConference

November12,2016

1

Moderator:DavidSchnabel,DavisPolk&WardwellLLPPresenters:

ToddGluth,CooleyLLP

DianaWollman,Cleary,Go%lieb,Steen&HamiltonLLP

Commentators:

BillWilkins,InternalRevenueServiceChiefCounsel

MichaelHirschfeld,CornellLawSchool

Whywehavegatheredheretoday• Goal:UsingtheBBAframework,developanauditandcollecLon

regimeforpartnershipsthatseekstomaximizetwobasic(butambiLous)goals:– Determinethecorrectamountoftaxinaworldwheresomerelevantfacts

mayexistatthepartnershiplevel,otherrelevantfactsmayexistatthepartnerlevel(or,inthecaseofapartnerthatisamemberofaconsolidatedgroup,theconsolidatedgrouplevel),andsLllotherfactsmayexistatthelevelofoneormoreupper-Lerpartnerships.

– ProvidetheIRSwithaneffecLvemechanismtoassessandcollectthatamountoftax.

• Whatwedid:– ReviewedtherichhistoryofpartnershipauditproposalsfromTEFRA

throughBBA.LegislaLveproposalstocollect“partnershipshorWalls”/“imputedunderpayments”fromthepartnershipdatebackto1987.

– DevelopedaproposalthatbuildsonthearchitectureoftheBBAasaplaWormfortoday’sdiscussion.WeareseekingyourreacLonandinput.2

Caveats• ThisProposalismeanttobeaworkingdra_thatwillbenefitfromour

discussiontoday.

• WearewellawarethattheProposalisnotperfectbutwealsocauLonthatwethinkthereisnoperfectsoluLon.

• WethinkthatsomefairnessconcernsareaddressedbygivingtaxpayersadvancenoLceoftherulestheywillbefacingandthusopportunitytocontractualprotectthemselves.– TaxpayerswhocontracttobeinapartnershipcancontractforprotecLons.

• WearenotfocusingtodayonwhichaspectsofthisproposalcouldbeimplementedunderthecurrentstatuteandwhichwouldrequirelegislaLvechanges.

3

Background

4

TEFRARulesSummary

• Partnership-LevelProceedings.Partnershipitemsaddressedinunifiedpartnership-leveladministraLveandjudicialproceedings.

• TMP.IRSinteractswithTMP(whomustbeageneralpartner).

• No7ce,Par7cipa7on&Se;lement.IRCgivespartnersrightstobenoLfiedofaudit,parLcipate,anddissentfromse%lement.

• AdjustmentsFlowThroughtoPartners.Partnership-leveladjustmentspassedthroughtoreviewed-yearpartners;everyone’sreviewed-yearreturngetstoCorrectReturnPosiLon.

• Collec7onfromPartners.IRScomputesamounteveryoneowesandthenmustcollectfromreviewed-yearpartners.

• StatuteofLimita7ons.IRShas3yearsfrompartnership’sfilingdate,whichcanpotenLallybeextendedbyTMP(evenastopartner-level“affecteditems”).

5

TEFRAHadManyProblems• Iden7fica7on&MonitoringofPartners.IdenLfyingand

monitoringpartnerstoprovidenoLce,confirmflowthroughofadjustments,andassessandcollecttax(ordeliverrefunds)canbedaunLng,parLcularlyinwidely-heldpartnerships,Leredpartnerships,andpartnershipswithintereststhatfrequentlychange.

• PartnerPar7cipa7on.CumbersomeintervenLonofnumerouspartnersinproceedings,andwidespreadrightstoiniLateproceedings.ProceduralprotecLonsforpartnerscomplicateauditsandinviteliLgaLon.

• ObstaclestoSe;lement.IRSgenerallyneedsagreementofeverypartnertose%le.

• PartnerRefundClaimsforCorollaryAdjustments.Deficienciesinoneyearfrequentlygiverisetorefundclaimsinlateryears.

• Mul7plicityofSmallPartnerAdjustments.CostsofcollecLngsmallamountsfrom(ordeliveringrefundsto)manypartnerscanbeprohibiLve,eveniftheamountissignificantintheaggregate.

Result:IRSauditsfewlargepartnerships,mostresultinnochangetothepartnership’sreturn,andtheaggregatechangesaresmall. 6

BBABasics• EnactedNovember2015(minortechnicalcorrecLonsin

December2015).– ReplacesTEFRAandELP.

• Appliestopartnershipreturnsfiledfor2018andlateryears.– Partnershipswithlessthan100partners,allindividualsorcorporaLons,

mayelectout.

• Auditisconductedatpartnershiplevel– IndividualpartnershavenostatutoryrighttoreceivenoLce,

parLcipate,ordisagreewithresult.– SinglerepresentaLve,whoneednotbeapartner,interfaceswithIRS.

• Whenauditconcludes,IRScomputesan“imputed

underpayment”thatthepartnershipowestoIRS. – RoughlyequalsunderstatementofincomemulLpliedLmeshighesttax

rateineffectfor“reviewedyear”.– CollecLonfrompartnershipavoidsneedtotrackthroughLersof

partnershipstoulLmatetop-Lerpartners.

7

3MethodstoReduceAmountPartnershipOwestoIRS

1. 6225(c)(2)AmendedReturns:Oneormorepartnersmayelecttofileanamendedreturn(CRP)forreviewedyear.– reducesImputedUnderpaymentthepartnershipowes.

2. 6225(c)(3)/(c)(4)Reduc?on:PartnershipmaytrytoprovetoIRSExamthat“highestrateoftax”isnotappropriateratebaseduponcharacterisLcsofpartners.– reducesImputedUnderpaymentthepartnershipowes.

3. 6226Push-Out:partnershipsends6226noLcetoallreviewed-yearpartnerstellingthemtheymustcomputeCRPandpayIRSdirectly.– partnershipenLrelyoffthehook. 8

ConcernsraisedaboutBBA• Unfair,unfair,unfair.• ConflictswithSubKandothersubstanLvetaxrules– IncludingimposingenLty-leveltaxandtaxingincomeallocabletotax-exempts

• IRScanovercollect,collectfromwrongpersons,anddoubletaxsomepartners.

• Tieredstructuresareespeciallydisadvantagedandfairnesscannotbeachieved.

• IRScanundercollectandhavenomeansofredress

• PartnershiprepresentaLvehastoomuchpower• Well-advisedtaxpayerswillpaylessthantheyshouldand

poorly-advisedtaxpayerswillpaymorethantheyshould.9

Terminology• “sourcepartnership”:partnershipthatisaudited.

• “adjustmentyear”:yearauditconcludes.

• “reviewedyear”:yearthatwasaudited.

• “ImputedUnderpayment”:amountpartnershipowes.

• “6226”/“PushOut”:partnership’selecLontopushpaymentobligaLonouttoreviewed-yearpartners.

• CorrectReturnPosiLon(“CRP”):whatreviewed-yearpartnerswouldhaveowed,andtheirfuture-filedreturnswouldshow,ifreviewed-year1065(andsubsequentreturns)hadbeenconsistentwithauditresults.

10

ProposedChangestotheBBA

11

BigPictureGuidelinesforProposal• StartwiththeBBA,includingpartnershipliabilityconcept.• But,partnershipsandpartnersshouldbeabletogettoCRPif

they(notIRS)arewillingtobeartheadministraLveburdensandcollecLonrisksofdoingso.– ImpossibletodetermineCRPforallpartnersatpartnershiplevelwithout

partnerscomingintoshowtheiraffecteditems.

– Burdenshouldbeonpartnershipsandpartners,nottheIRS,tosecurecooperaLonofunwillingpartnerstogettoCRP.

– AllowpartnerwhocomesintodealdirectlywithIRS,notgothroughPR.

• OurProposaldoesthisby1. StarLngwithpartnershipliability,

2. AllowingpartnerswhowanttogettoCRP(andpaythattoIRSdirectly)todoso(viaPushIn),

3. Reducingthepartnership’sremainingliability,butleavingpartnershipliableforamountnotpaidbyPush-Inpartners.

12

BBABasicFrameworkRetained• IRSauditspartnershipatpartnershiplevel.– One“PartnershipRepresentaLve”representspartnershipinauditandanycourtproceedings.• PRdoesnotneedtobeapartner.

– AdjustmentsdeterminedthroughExam/Appealsusualprocedures.

• Atendofaudit,anImputedUnderpaymentiscomputedandthisisini@allytheamountthesourcepartnershipowestotheIRS.– ButthisImputedUnderpaymentcanbereduced(eventozero)withPushInbypartners. 13

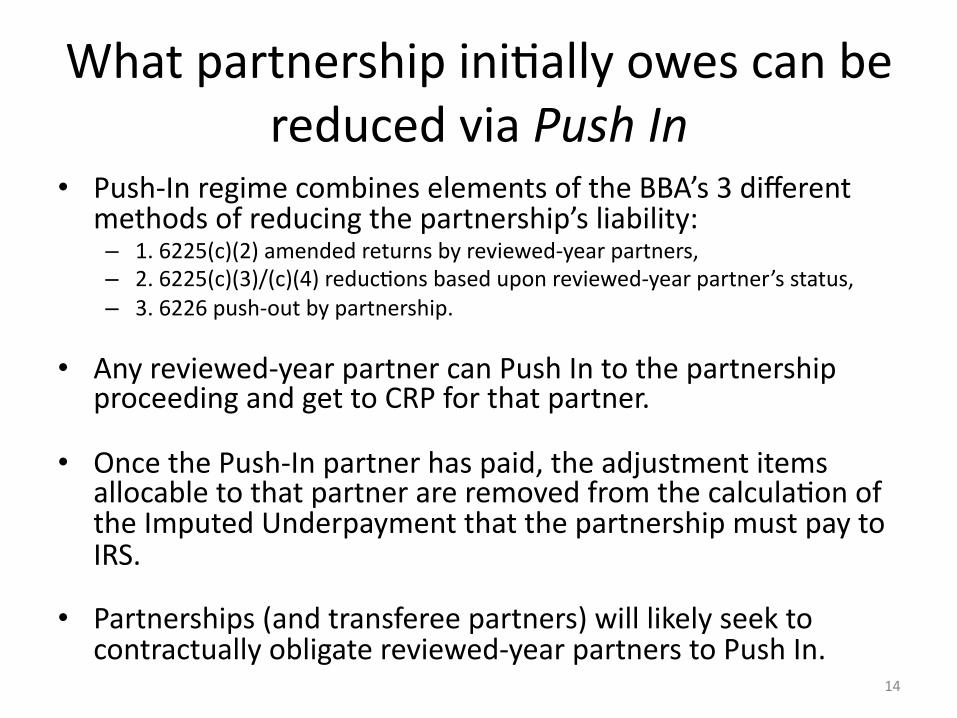

WhatpartnershipiniLallyowescanbereducedviaPushIn

• Push-InregimecombineselementsoftheBBA’s3differentmethodsofreducingthepartnership’sliability:– 1.6225(c)(2)amendedreturnsbyreviewed-yearpartners,– 2.6225(c)(3)/(c)(4)reducLonsbaseduponreviewed-yearpartner’sstatus,– 3.6226push-outbypartnership.

• Anyreviewed-yearpartnercanPushIntothepartnershipproceedingandgettoCRPforthatpartner.

• OncethePush-Inpartnerhaspaid,theadjustmentitemsallocabletothatpartnerareremovedfromthecalculaLonoftheImputedUnderpaymentthatthepartnershipmustpaytoIRS.

• Partnerships(andtransfereepartners)willlikelyseektocontractuallyobligatereviewed-yearpartnerstoPushIn.

14

HowPush-InWorks• Push-InpartnerdealsdirectlywithIRSExam

– Sameteamthatauditspartnership,orseparateteamwithexperLseinsubjectma%erorfamiliaritywiththePush-Inpartner(andcoordinateswithteamforauditedpartnership).

• ProvidesinformaLonsufficienttoestablishCRP– CRP=theamountoftaxesthePush-Inpartnerwouldoweforreviewedyearandall

yearsbetweenreviewedyearandcurrentyeariftheauditadjustmentshadbeenreflectedinthatpartner’sreviewedyearreturn.• Takesintoaccountallchangesintaxa%ributesthatwouldhaveoccurredatboth

partnershipandpartnerlevel(includingpartner-level“affecteditems”).• Takesintoaccountbothincreasesanddecreasesintaxes.• Becausethemechanicsdonotrelyonamendedreturns,PushIndoesnotafford

partnersanotherbiteatunrelateditemsinclosedreturns,itdoesnotrequirethemtorecerLfythecorrectnessofunrelateditemsinpreviouslyfiledreturns,anditmayavoidtheneedtoamendstateandlocalreturns.

• Push-InpartnerpaysthenetaddiLonaltaxesduetoIRSExam.

• AllfuturereturnsforPush-InpartnerpreparedasifCRPiswhatreallyhappened.– Includingpartnershipoutsidebasis,whichgoingforwardreflectsauditadjustments. 15

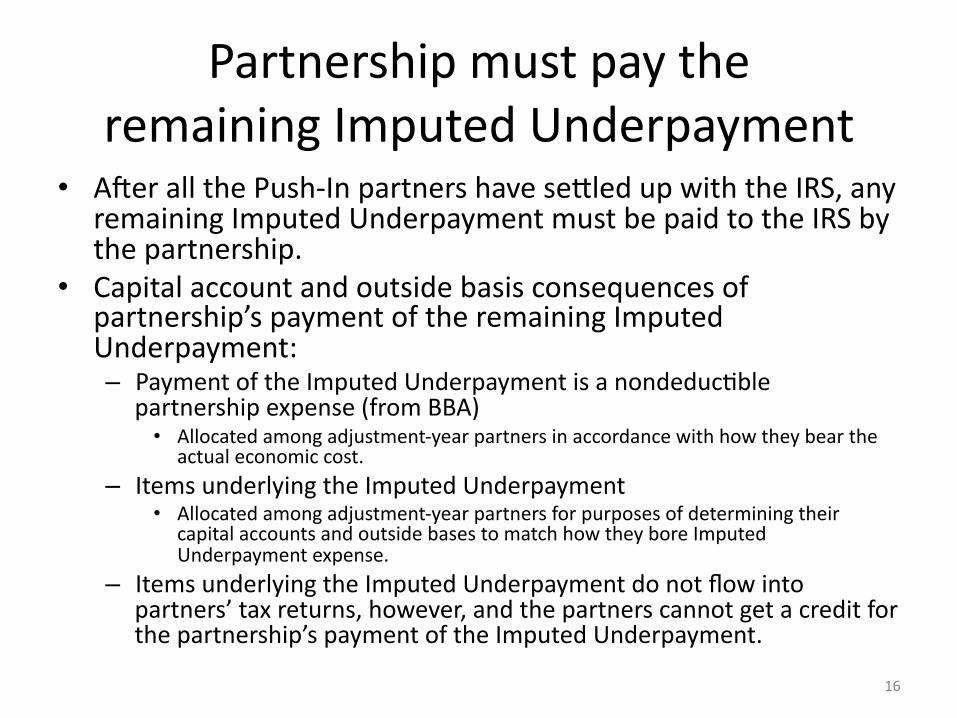

PartnershipmustpaytheremainingImputedUnderpayment

• A_erallthePush-Inpartnershavese%ledupwiththeIRS,anyremainingImputedUnderpaymentmustbepaidtotheIRSbythepartnership.

• Capitalaccountandoutsidebasisconsequencesofpartnership’spaymentoftheremainingImputedUnderpayment:– PaymentoftheImputedUnderpaymentisanondeducLble

partnershipexpense(fromBBA)• Allocatedamongadjustment-yearpartnersinaccordancewithhowtheybearthe

actualeconomiccost.

– ItemsunderlyingtheImputedUnderpayment• Allocatedamongadjustment-yearpartnersforpurposesofdeterminingtheir

capitalaccountsandoutsidebasestomatchhowtheyboreImputedUnderpaymentexpense.

– ItemsunderlyingtheImputedUnderpaymentdonotflowintopartners’taxreturns,however,andthepartnerscannotgetacreditforthepartnership’spaymentoftheImputedUnderpayment.

16

Tieredpartnerships:samerules– Partners’characterisLcscannotbeusedtoreducesource

partnership’sImputedUnderpaymentabsentPushInfromulLmatetop-Lerpartners.

– Apartnerofthesourcepartnershipthatisitselfapartnership

mayPushInandpayitsshareofthesourcepartnership’sImputedUnderpaymentatthehighestrateoftax.– PushInbyanupper-Lerpartnershipshi_saporLonoftheImputed

Underpaymentfromthelower-Lerpartnershiptotheupper-Lerpartnership,butdoesnotreducetheaggregateImputedUnderpayment.

– TheonlywaytoreducetheaggregateImputedUnderpaymentisPushInbytheulLmatetop-Lerpartners.– PushInbytheulLmatetop-LerpartnersrequiresPushInbyeachintervening

partnershiptoestablishthattheallocaLonsateachLerleadinguptotheulLmatepartnerarecorrect,andthatfuture-filedreturnsoftheinterveningpartnershipsappropriatelyreflectthecumulaLveimpactoftheadjustments.

– PaymentofImputedUnderpaymentandreflecLonofrelatedunderlyingauditadjustmentsincapitalaccountsandbasisfloatupthroughtheLers.

17

WhataboutaPush-InpartnerwhowouldbeenLtledtoarefund?

• Examples:– reallocaLons– otheradjustmentsthatincreasededucLons/decreaseincome

– viaimpactonaffecteditemsatpartnerlevel

• AllowPush-Inpartnertoreceiverefundbutonlya_erIRShasreceivedpaymentofenLreImputedUnderpayment(a_erreducLonforPush-Inpartnerswhopaid).

18

PushIncomparedtoPushOut• Similarto6226Push-OutelecLon.

• DifferenceisthatPush-InhappensaspartofExamandoccursbeforepartnershipisabsolvedofobligaLontopay.

• Partnershipisoffthehookonlya_er,andtotheextent,thePush-Inpartnershavethemselvespaid.

• FromperspecLveofreviewed-yearpartners,PushInshouldbebe%er.– Notallpartnersneedtodoit.– Decreasesintaxesandrefundstakenintoaccount.– OccurslivewithExamteamsomaybemoreefficientthanfiling

informaLonwithadjustment-yearreturn.

• PartnershipsmustsecurecooperaLonfromtheirreviewed-yearpartners,andtotheextenttheyfailtodosothepartnershipisliablefortheremainingImputedUnderpayment.

19

IRSabilitytopursueapartnerdirectly• Whattodoaboutpartnership-leveldeterminaLonsthatcannotbe

reflectedinanImputedUnderpaymentbecausetheaddiLonaltaxableincomeisrecognizedonlyatthepartnerlevel?– Examples:disguisedsale,distribuLoninexcessofoutsidebasis,existenceofa

UStradeorbusinessthatmayimpactapartner’snon-partnershipitems,recaptureoccurringatpartner-levelasaresultofapartnershipitem.

• IRScannotseekpaymentfrompartnershipinthesecasesbecausetheseitemsdonotgointocomputaLonofImputedUnderpayment.

• IRSmusthaverighttopursuepartnerdirectly– Eachpartner’sSOLwouldbetolledinrespectofsuchitemsduringBBAaudit.– IRSwouldneedtocommencepartner-levelproceedingtoassessandcollect.

• Open:wouldpartnership-leveldeterminaLonbebindingonpartner?Ifyes,shouldpartnerhaveanyrighttobenoLfiedoforparLcipateinpartnership-levelaudit?

• Note:ifthispartnerPushedIn,wouldneedtodisclosetheseitemsandtheywouldbetakenintoaccountindeterminingthepartner’sCRPandthusamountowedunderPush-In.

20

InsufficientAssets&OtherNon-PaymentSituaLons

• Ifpartnershiphasinsufficientassets(orotherwisedoesnotpayremainingImputedUnderpayment),IRSmayproceedagainstpresentandformerpartnersintheorderandprioritysetoutinthenextslide.

– Ineachcase,IRSissuesnoLceanddemandandif,a_erprescribednumberofdays,paymentisnotreceived,IRSmayproceedtonextLer.

– IRSalsoretainsitsotheravailableremedies,including6901andfraudulentconveyancelaws.

• Warning:thenextslideiscontroversial.21

CollecLonwhenpartnershipdoesn’tpay

– First,fromthe“clawback”partners:• AnypersonwhowasapartneratanyLmeonora_erdatepartnership

receivednoLcefromtheIRSofaudit(includingtax-exempts).• Butonlyuptovalueofnetdistribu@onsreceivedfrompartnershipby

thatpersonduringthatperiod.• Notlimitedbyreferencetoaclawbackpartner’sshareofpartnership

capitalorprofits(orthetaxclawbackpartnerwouldoweifadjustmentwereallocatedtothatclawbackpartner).

• Notabouttheclawbackpartnerowingtax;aboutclawingback,intopartnership,distribuLonsofpartnershipassets.

• Second,fromreviewed-yearpartners(otherthanPush-Inpartners)– ButonlyfortheirproporLonatesharesoftheImputedUnderpayment

baseduponthereviewed-yearpartnershipagreement’sallocaLons.– Personwhowasbothareviewed-yearpartnerandaclawbackpartner

couldbesubjecttobothcollecLonregimes.

22

ShouldPushInbeinaddiLonto,orinlieuof,exisLngregimestomodifyImputedUnderpayment?

• Ideally:Replace6226enLrelywithasinglecomprehensivePush-Inregime• Foreachreviewed-yearpartnerwhoPushesIn,theresultsarethe

sameas6226.• ThedifferenceisPushInreducescollecLonrisksforIRS

• atendofaudit,anyamountnotpaidbyreviewed-yearpartnersmustbepaidbythepartnership

• IRSdoesnotneedtomonitorwhetherithascollectedthroughreviewed-yearpartners’next-filedtaxreturns

– MulLpleregimesdifficultforIRStoadministerandincreaseriskforfisc• AlsomoredifficultformanagersofpartnershipstobalanceconflicLnginterests,andcreatespotenLalforthebe%er-advisedand/ormoreinfluenLalpartnerstosteerthepartnershiptodecisionsthatbenefitthemattheexpenseofothers.

• Realis?cally:retain6226but• Revisesothatsourcepartnership(andpotenLallyanyintervening

partnerships)mustbackstopanyamountnotpaidbythetop-Lerreviewed-yearpartners.

23

ElecLonOut• Retain100-partnerrule(fornow).

– GovernmentdataindicatesthiselecLonwilllikelybeavailabletoalargenumberof(albeitsmall)partnerships.

• ForelecLng-outpartnerships:– IRSmayauditatpartnership-level(likepre-TEFRA)

• ButassessmentandcollecLonrequirepartner-levelproceeding.

– ConsidersomeTEFRA/BBA-likefeatures• ConsistentreporLngabsentnoLcetotheIRS• SOLrules

24

HowisImputedUnderpaymentcomputed?

• A_erauditadjustmentsarefinalized,IRScomputestheiniLalImputedUnderpaymentusingthefollowingrulesderivedfromthe6225ruleswithsomemodificaLons.

25

HowarenegaLveitemsreflectedincompuLngImputedUnderpayment?

• PosiLveandnegaLveitemsforeachaudityeararene%edonlyiftheyareofthesamecharacterandsource.

• NegaLveitemsthatcouldbesubjecttolimitaLonontheiruseatthepartnerlevelarenotne%ed.– Detailsastowhatitemstheseareneedstobeworkedout.

• A_ernepngitemswithinaparLculargroup,netnegaLveitemsareignored.– E.g.,ifnetposiLveOIandnetCL,imputedunderpaymentincludesthenetOIbutignoresthenetCL.

• Reallocateddistributedsharesarenotne%ed– sameas6225(b)(2).

26

HowarechangesincreditsreflectedincompuLngImputedUnderpayment?

• AddiLonalcredits– DecreaseImputedUnderpaymentonlyifalltherulesapplicabletothecredits(includingrecapture)applyatpartnershiplevel.

• ReducLonincredits(includingrecapture)– IncreaseImputedUnderpaymentdollar-for-dollar(evenifthecreditsreportedwouldhavebeensubjecttolimitaLonatthepartnerlevel).

27

Whattaxrateisused?• TakethenetposiLveitemsofeachcharacterandmulLplythemLmesthehighestrateoftaxforanytypeoftaxpayerforincomeofthatcharacterforreviewedyear.– Individualratewouldincludetaxunder1401/1411.

• NoreducLonstothetaxratesusedbasedupona%ributesofpartners.– A%ributesofpartnersrelevantonlyviaPush-In.

28