beazley results2016

TRANSCRIPT

Generic title white

Results for the year ended 31 December 2015

Thursday, 4 February 2016

Disclaimer notice

2

Certain statements made in this presentation, both oral and written, are or may constitute “forward looking statements”with respect to the operation, performance and financial condition of the Company and/or the Group. These forwardlooking statements are not based on historical facts but rather reflect current beliefs and expectations regarding futureevents and results. Such forward looking statements can be identified from words such as “anticipates”, “may”, “will”,“believes”, “expects”, “intends”, “could”, “should”, “estimates”, “predict” and similar expressions in such statements or thenegative thereof, or other variations thereof or comparable terminology. These forward looking statements appear in anumber of places throughout this document and involve significant inherent risks, uncertainties and other factors, known orunknown, which may cause the actual results, performance or achievements of the Company, or industry results, to bematerially different from any future results, performance or achievements expressed or implied by such forward lookingstatements. Given these uncertainties, such forward looking statements should not be read as guarantees of futureperformance or results and no undue reliance should be placed on such forward looking statements. A number of factorscould cause actual results to differ materially from the results discussed in these forward looking statements.The information and opinions contained in this presentation, including any forward looking statements, are provided, andreflect knowledge and information available, as at the date of this presentation and are subject to change withoutnotice. There is no intention, nor is any duty or obligation assumed by the Company, the Group or the Directors tosupplement, amend, update or revise any of the information, including any forward looking statements, contained in thispresentation.All subsequent written and oral forward looking statements attributable to the Company and/or the Group or to personsacting on its behalf are expressly qualified in their entirety by the cautionary statements referred to above and containedelsewhere in this document.

Contents

Overview of 2015 4-8

FinancialsPerformance 10Investments 11-12Reserves 13-14Capital 15-16Proposed new holding company 17

Underwriting review 18-22

Our vision and strategy 23

Outlook for 2016 24

Appendix 25-36

3

Pages

Generic title white

Overview of 2015

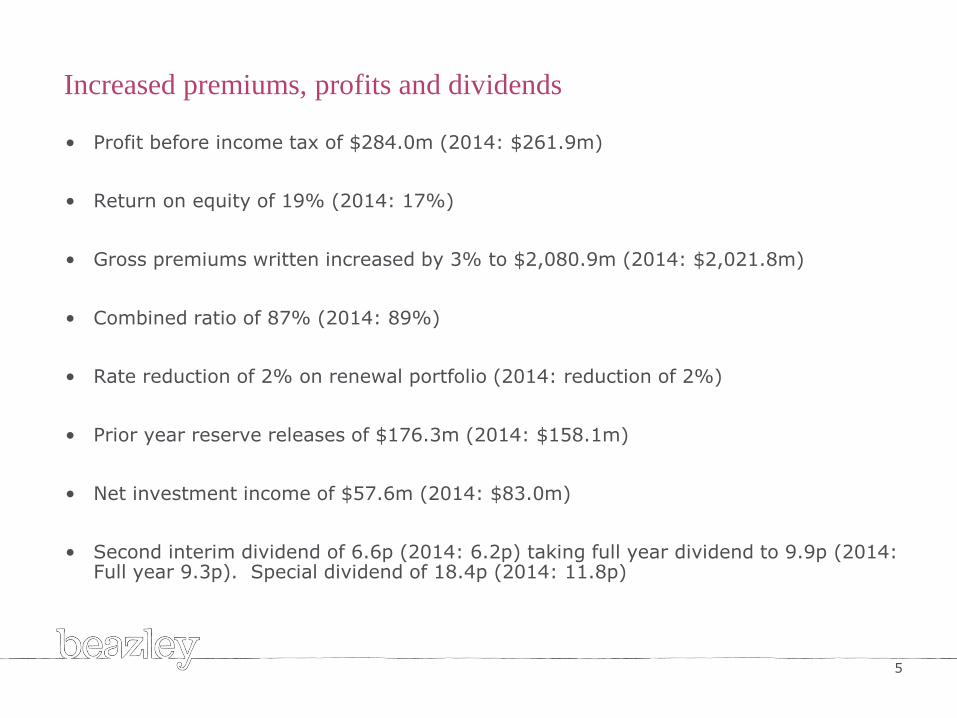

Increased premiums, profits and dividends

• Profit before income tax of $284.0m (2014: $261.9m)

• Return on equity of 19% (2014: 17%)

• Gross premiums written increased by 3% to $2,080.9m (2014: $2,021.8m)

• Combined ratio of 87% (2014: 89%)

• Rate reduction of 2% on renewal portfolio (2014: reduction of 2%)

• Prior year reserve releases of $176.3m (2014: $158.1m)

• Net investment income of $57.6m (2014: $83.0m)

• Second interim dividend of 6.6p (2014: 6.2p) taking full year dividend to 9.9p (2014:Full year 9.3p). Special dividend of 18.4p (2014: 11.8p)

5

• Investment in our teams:

People – ranked in top quartile for employee engagement

We passed the 1,000 employee landmark

We continue to attract talent

• We grew 21% in the US and opened our Los Angeles office

• Started our Korean Re partnership

• Strong balance sheet and active capital management maintained

• Received our Solvency II Internal Model approval from the CBI

• We propose to establish a new UK tax resident group holding company

Continued progress with our strategic initiatives

6

Cover

7

Sustained high performance

1,712.51,895.9 1,970.2 2,021.8 2,080.9

0

500

1,000

1,500

2,000

2,500

2011 2012 2013 2014 2015

Gross premiums written ($m)

62%53%

45% 49% 48%

37%

38%39%

40% 39%

99%91%

84%89% 87%

0%

25%

50%

75%

100%

125%

2011 2012 2013 2014 2015

Combined ratio* (%)

Expense ratio Claims ratio

7.9 8.3 8.8 9.3 9.9

8.4

16.111.8

18.4

0.0

5.0

10.0

15.0

20.0

25.0

30.0

2011 2012 2013 2014 2015

Dividends per share (p)

Special Interim and second interim

6%

19%21%

17%19%

0%

5%

10%

15%

20%

25%

2011 2012 2013 2014 2015

Return on equity (%)

Excellent total shareholder return - TSR 33.5% per annum since 31.12.09

8

Sh

are

ho

lder

retu

rn(%

)

* Average NAV growth (including dividends) over the past 6 years of 17.3%

0%

25%

50%

75%

100%

125%

150%

175%

200%

225%

250%

275%

300%

325%

350%

375%

400%

31 December 2009 31 December 2010 31 December 2011 31 December 2012 31 December 2013 31 December 2014 31 December 2015

NAV target range(RFR +10% p.a. toRFR +15% p.a.)

NAV growth(Including dividends)

TSR growth(1 month average)

Generic title white

Financials

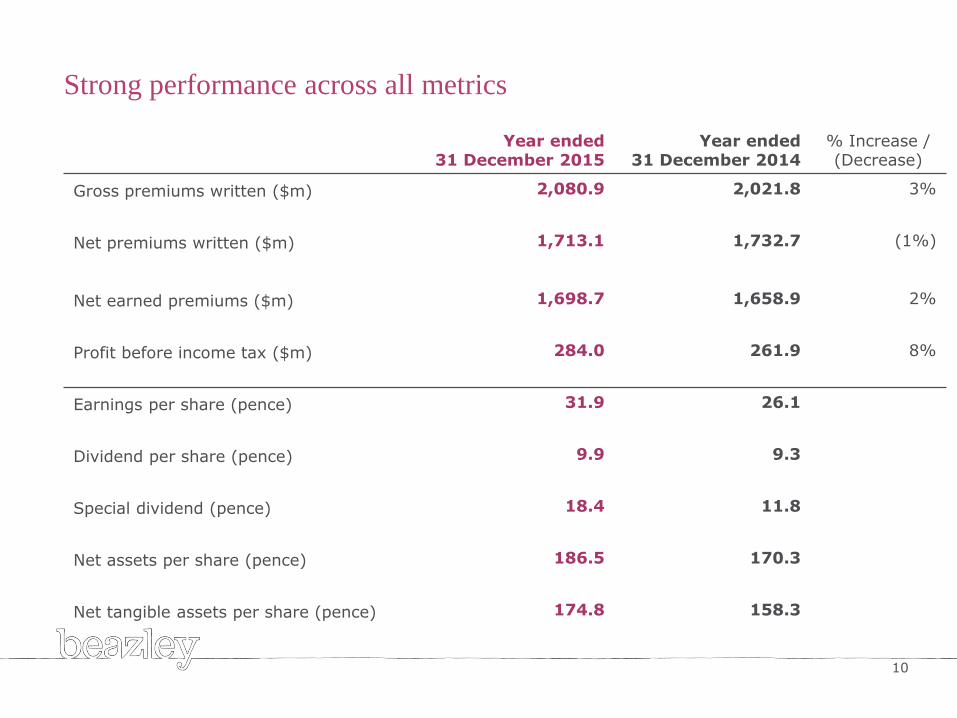

Strong performance across all metrics

Year ended31 December 2015

Year ended31 December 2014

% Increase /(Decrease)

Gross premiums written ($m) 2,080.9 2,021.8 3%

Net premiums written ($m) 1,713.1 1,732.7 (1%)

Net earned premiums ($m) 1,698.7 1,658.9 2%

Profit before income tax ($m) 284.0 261.9 8%

Earnings per share (pence) 31.9 26.1

Dividend per share (pence) 9.9 9.3

Special dividend (pence) 18.4 11.8

Net assets per share (pence) 186.5 170.3

Net tangible assets per share (pence) 174.8 158.3

10

Portfolio delivered 1.3% annualised return

11

In

vestm

en

tre

turn

($

m)

An

nu

ali

sed

In

vestm

en

tR

etu

rn

22.5

36.1

46.843.5

16.8

46.5

43.3

36.2

14.1

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

10

20

30

40

50

60

70

80

90

100

2011 2012 2013 2014 2015

1st half 2nd half Return

Cash and CashEquivalents

15.0%

GovernmentQuasi

Government &Supranational

41.1%

InvestmentGradeCredit27.2%

Other Credit 1.6%

Senior Secured Loans2.5%

Equity Linked funds 3.3%

Hedge Funds(Uncorrelated Strategies)

7.3%

Illiquid Credit Assets 2.0%

Minor changes to portfolio mix

12

31 December 2015 31 December 2014

Cash and CashEquivalents, 8.2%

GovernmentQuasi

GovernmentSupranational

41.6%InvestmentGrade Credit

33.5%

Other Credit, 1.8%

Senior Secured Loans2.3%

Equity Linked funds, 3.3%

Hedge Funds(Uncorrelated Strategies)

8.3%

Illiquid Credit Assets,1.0%

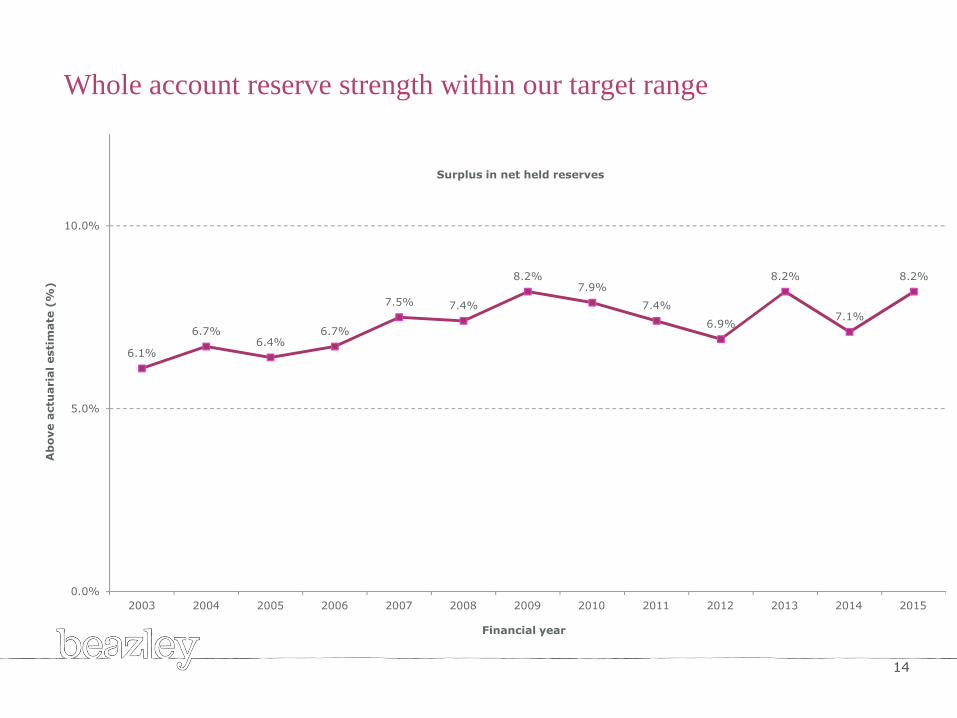

Continued prior year reserve releases

13

Reserv

ere

leases

($

m)

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

11.0%

12.0%

13.0%

14.0%

15.0%

-15

0

15

30

45

60

75

90

105

120

135

150

165

180

195

210

225

2011 2012 2013 2014 2015

Specialty lines Political risks and contingency Life accident and health Marine Property Reinsurance % of NEP

6.1%

6.7%6.4%

6.7%

7.5% 7.4%

8.2%7.9%

7.4%

6.9%

8.2%

7.1%

8.2%

0.0%

5.0%

10.0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Financial year

Surplus in net held reserves

Whole account reserve strength within our target range

14

Ab

ove

actu

ari

alesti

mate

(%

)

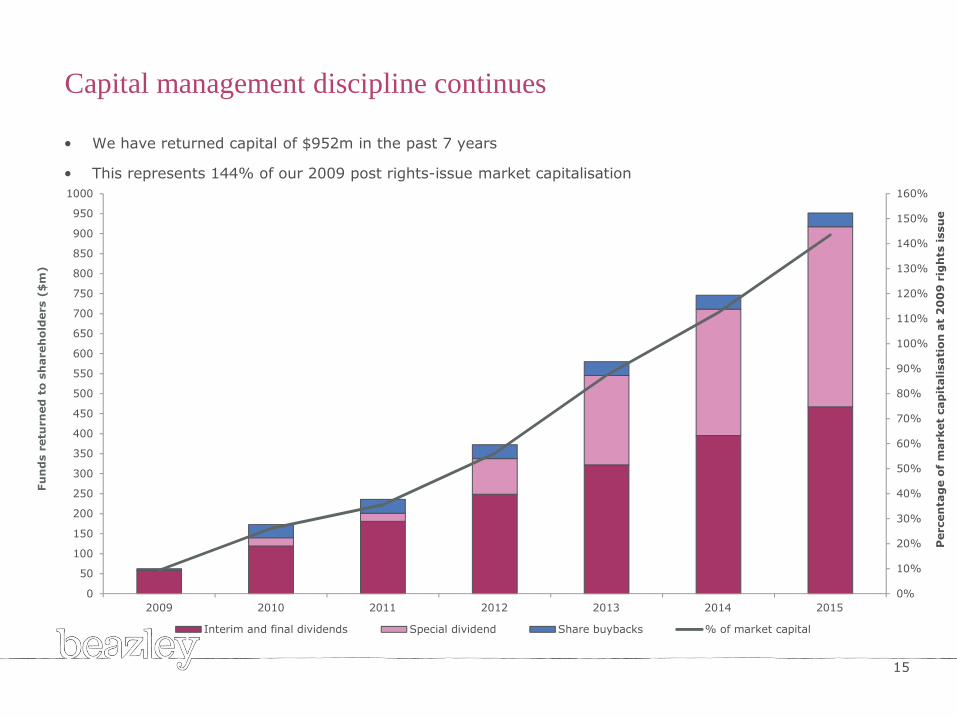

Capital management discipline continues

• We have returned capital of $952m in the past 7 years

• This represents 144% of our 2009 post rights-issue market capitalisation

15

Fu

nd

sre

turn

ed

tosh

are

ho

lders

($

m)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

150%

160%

0

50

100

150

200

250

300

350

400

450

500

550

600

650

700

750

800

850

900

950

1000

2009 2010 2011 2012 2013 2014 2015

Perc

en

tag

eo

fm

ark

et

cap

itali

sati

on

at

20

09

rig

hts

issu

e

Interim and final dividends Special dividend Share buybacks % of market capital

Updated capital position remains strong

16

Year ended31 December 2015

$m

Year ended31 December 2014

$m

Lloyd’s economic capital requirement (ECR) 1,326.9 1,359.0

Capital for US insurance company 107.7 107.7

1,434.6 1,466.7

• Group capital requirement:

• Our funding is made up of our own equity (on a Solvency II basis) plus $247.2m of debtand an undrawn banking facility of $225.0m

• At 31 December 2015 we have surplus capital of 49% of ECR, including Solvency IIadjustments

• We will be paying a special dividend of 18.4p, reducing the surplus to 35%, above ourtarget 15-25% range

Proposed new holding company

17

• Change will allow group management to be from the UK from the end of April

• Timetable is for a shareholder vote in March

• No change to the operating structure, expected profits or tax rates of the group

• Beazley plc will be retained as the name for our top company

Generic title white

Underwriting review

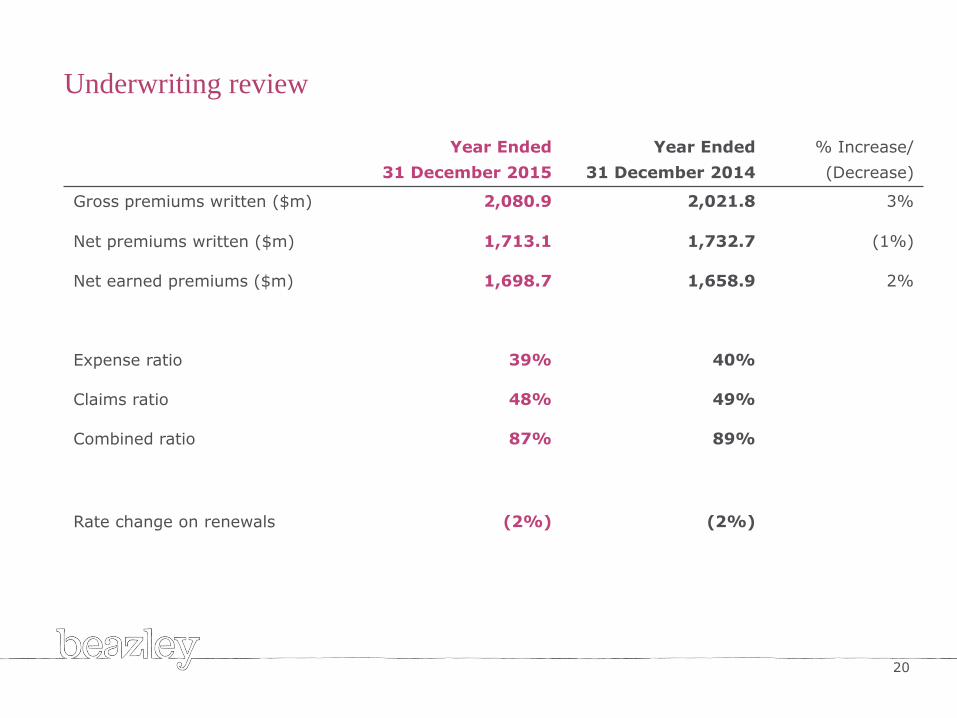

Underwriting review – 2015 achievements

19

• Combined ratio of 87%, with improved combined ratio achieved by all divisions

• Growth in gross premiums written of 3% to $2,080.9m

Specialty lines, our largest division, achieved growth of 13%

21% growth in locally underwritten US premium

• Rate reductions of 2% across portfolio as a whole

• Favourable claims experience including lower than average catastrophe activity

• We continue to reserve consistently, maintaining our surplus over actuarial estimatebetween 5-10%

Underwriting review

Year Ended

31 December 2015

Year Ended

31 December 2014

% Increase/

(Decrease)

Gross premiums written ($m) 2,080.9 2,021.8 3%

Net premiums written ($m) 1,713.1 1,732.7 (1%)

Net earned premiums ($m) 1,698.7 1,658.9 2%

Expense ratio 39% 40%

Claims ratio 48% 49%

Combined ratio 87% 89%

Rate change on renewals (2%) (2%)

20

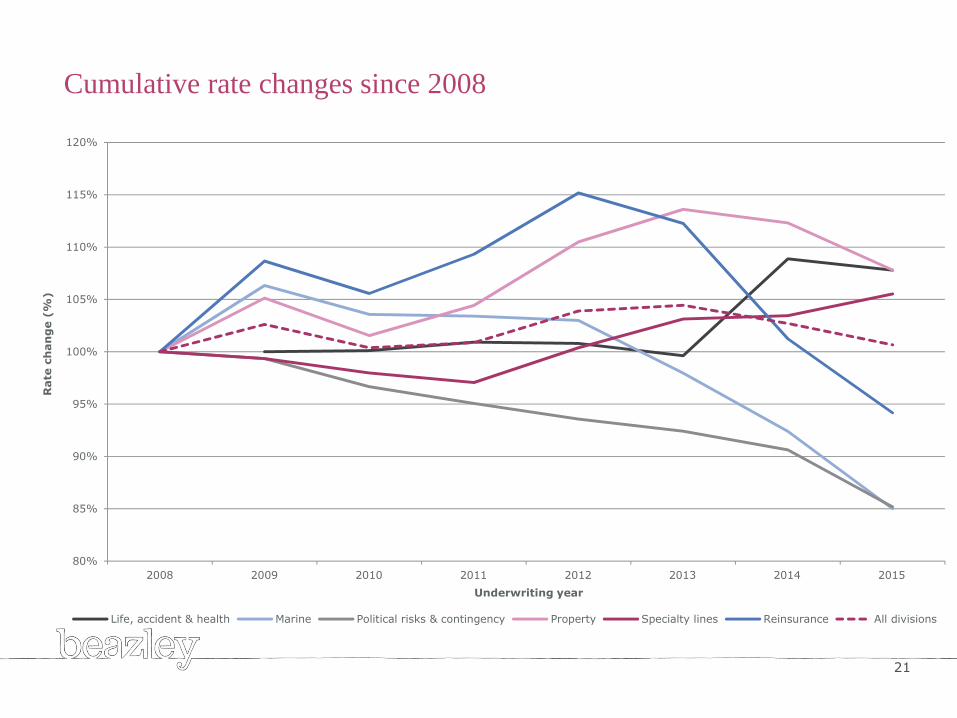

Cumulative rate changes since 2008

Rate

ch

an

ge

(%

)

21

80%

85%

90%

95%

100%

105%

110%

115%

120%

2008 2009 2010 2011 2012 2013 2014 2015

Underwriting year

Life, accident & health Marine Political risks & contingency Property Specialty lines Reinsurance All divisions

2016 underwriting outlook

22

• Competitive market conditions expected to continue

• Well diversified portfolio will allow efficient cycle management

• Disciplined underwriting in areas where competition is greatest

• We see opportunities for moderate growth in 2016

US underwritten premium

US ‘gap protection’ medical cover

Cyber demand continues to increase

Improved distribution channels for SME business

Our vision and strategic priorities

To become, and be recognised as,the highest performing

specialist insurer

Gro

wth

inSM

E

Sale

sand

Serv

ice

Gro

wth

inAsia

Pacific

Gro

wth

inU

S

Innovation

and

Pro

duct

Develo

pm

ent

Gro

wth

inEu

rop

e

23

New in 2015

Outlook for 2016 – our 30th year

• Continue our organic growth strategy

• Premium rates expected to decline across portfolio as a whole

• Continued growth opportunities in US

• Market consolidation offers opportunities to attract talent

• Pursue our refreshed strategic initiatives

• New corporate structure to enable us to run the group from the UK

24

Questions?

Any questions?

Generic title white

Appendix

73%

114%

88%

61%

49%44%

48% 51%

73% 75%

68% 66%60%

44%

29%

14%

0%

20%

40%

60%

80%

100%

120%

140%

1993-1996

1997-2000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Underwriting year

Specialty lines net incurred loss ratio at each development year 6 to latest

6

5

4

3

2

ULR

Specialty lines incurred claims remain in line with expectations

Net ultimate premium $m

27

Net

incu

rred

loss

rati

o(%

)

77 107 52 91 262 313 332 345 419 453 418 434 425 454 476 517

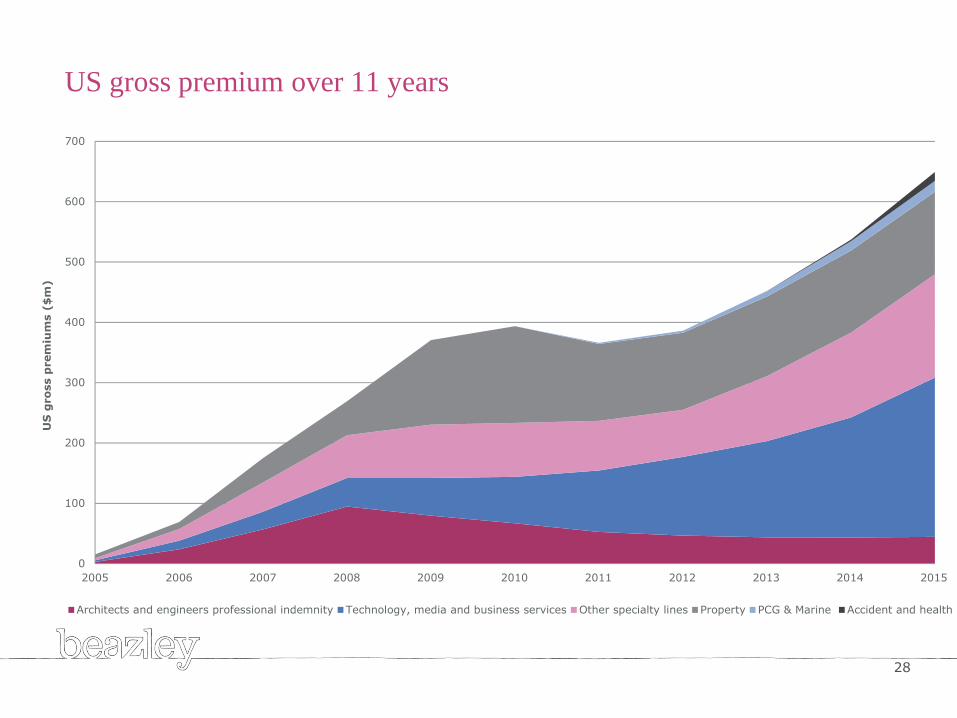

US gross premium over 11 years

28

US

gro

ss

pre

miu

ms

($

m)

0

100

200

300

400

500

600

700

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Architects and engineers professional indemnity Technology, media and business services Other specialty lines Property PCG & Marine Accident and health

Cumulative rate changes since 2001

29

Cu

mu

lati

ve

rate

ch

an

ge

(%

)

50%

100%

150%

200%

250%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Underwriting year

Life, accident & health Marine Political risks & contingency Property Reinsurance Specialty lines All divisions

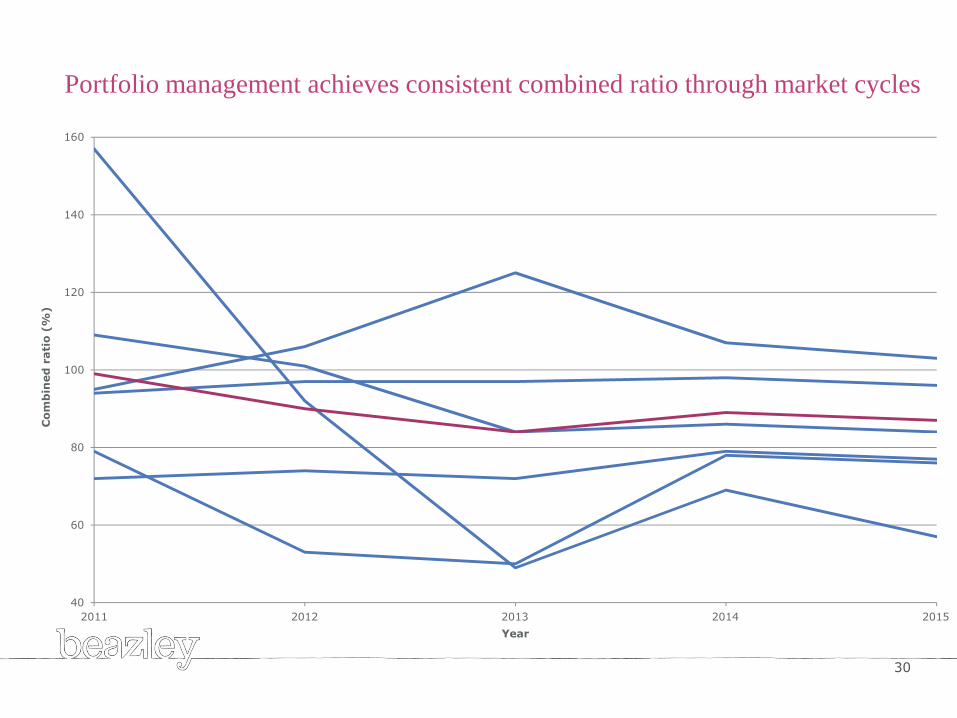

30

Portfolio management achieves consistent combined ratio through market cycles

Co

mb

ined

rati

o(%

)

40

60

80

100

120

140

160

2011 2012 2013 2014 2015

Year

Life accident & health

• Profit of $0.4m

• Combined ratio improved to 103%

(2014: 107%)

Year ended 31 December

2015 2014

Gross premiums written ($m) 119.8 132.2

Net premiums written ($m) 106.6 113.7

Net earned premiums ($m) 110.8 103.0

Claims ratio 58% 60%

Rate change on renewals (1%) 9%

Percentage of business led 68% 68%

31

Marine

• Improved combined ratio of 77%

(2014: 78%)

• Second largest divisional contribution

to group’s profitability in 2015

Year ended 31 December

2015 2014

Gross premiums written ($m) 269.3 325.2

Net premiums written ($m) 239.5 289.9

Net earned premiums ($m) 258.2 282.6

Claims ratio 38% 38%

Rate change on renewals (8%) (6%)

Percentage of business led 46% 43%

32

Political risks and contingency

Year ended 31 December

2015 2014

Gross premiums written ($m) 123.6 123.2

Net premiums written ($m) 105.0 101.2

Net earned premiums ($m) 106.4 96.9

Claims ratio 29% 27%

Rate change on renewals (6%) (2%)

Percentage of business led 68% 70%

33

• Combined ratio of 76% (2014: 78%)

• Net earned premiums increased by

10%

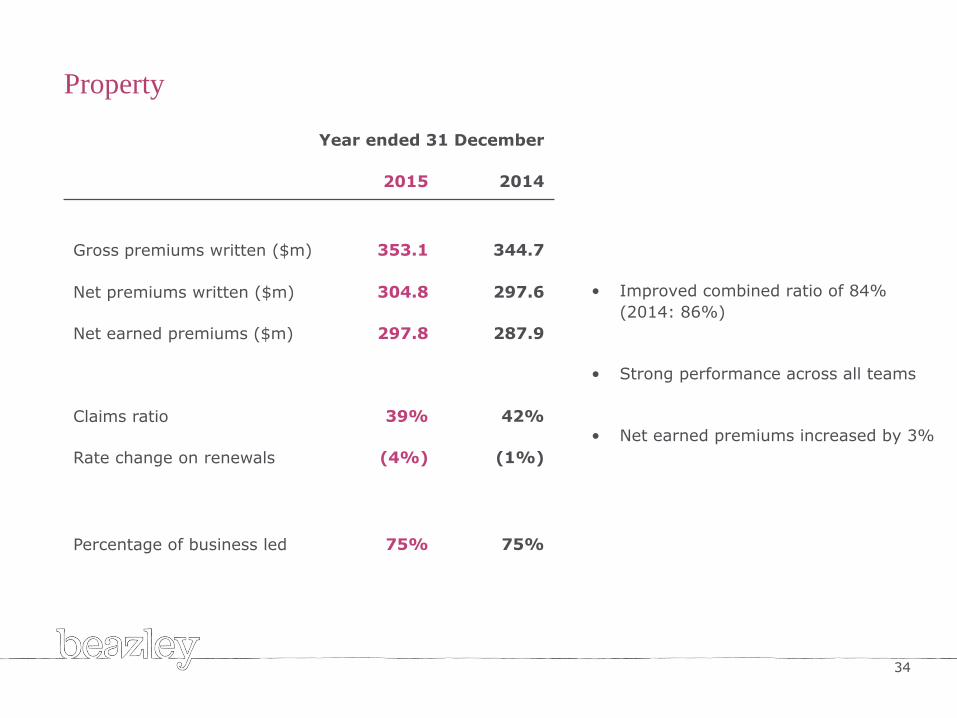

Property

Year ended 31 December

2015 2014

Gross premiums written ($m) 353.1 344.7

Net premiums written ($m) 304.8 297.6

Net earned premiums ($m) 297.8 287.9

Claims ratio 39% 42%

Rate change on renewals (4%) (1%)

Percentage of business led 75% 75%

34

• Improved combined ratio of 84%

(2014: 86%)

• Strong performance across all teams

• Net earned premiums increased by 3%

Reinsurance

• Combined ratio of 57% (2014: 69%)

• Market over supplied with capacity

Year ended 31 December

2015 2014

Gross premiums written ($m) 199.9 200.8

Net premiums written ($m) 132.0 153.8

Net earned premiums ($m) 133.8 160.1

Claims ratio 22% 37%

Rate change on renewals (7%) (10%)

Percentage of business led 40% 39%

35

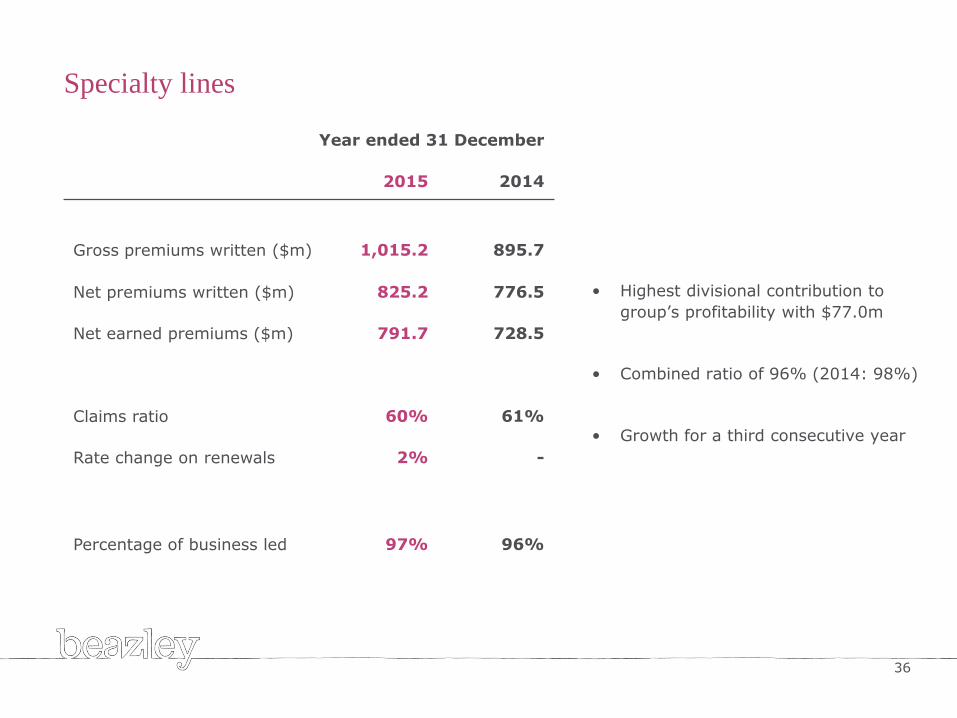

Specialty lines

• Highest divisional contribution to

group’s profitability with $77.0m

• Combined ratio of 96% (2014: 98%)

• Growth for a third consecutive year

Year ended 31 December

2015 2014

Gross premiums written ($m) 1,015.2 895.7

Net premiums written ($m) 825.2 776.5

Net earned premiums ($m) 791.7 728.5

Claims ratio 60% 61%

Rate change on renewals 2% -

Percentage of business led 97% 96%

36