經濟部推動綠色貿易產 業學程b-2carbon disclosure project (cdp) respect europe business...

TRANSCRIPT

經濟部推動綠色貿易產業學程B-2

www.pwc.com/tw

PwC Taiwan 資誠

1 Starting from GHG protocol 1

2 GHG accounting and reporting principles 11

2.1 Three Scopes of Emissions 12

2.2 Basics of developing a GHG inventory 20

2.3 Which GHGs 26

3 Corporate Value Chain (Scope 3) Accountingand Reporting Standard

31

3.1 What is the Scope 3 standard? 32

3.2 What is the Goal of the Scope 3Standard?

38

Page

簡報大綱簡報大綱

PwC Taiwan 資誠

3.3 Why is the Scope 3 Standard Relevant? 42

4 Identifying Scope 3 Emissions 47

4.1 Category 1: Purchased goods andservices

49

4.2 Category 2: Capital Goods 53

4.3 Category 3 : Fuel- and energy-relatedactivities (not included in Scope 1 orScope 2)

57

4.4 Category 4&9: Transportation andDistribution

61

4.5 Category 5: Waste Generated inOperations

70

Page

簡報大綱簡報大綱

PwC Taiwan 資誠

4.6 Category 6: Business Travel 75

4.7 Category 7: Employee Commuting 81

4.8 Category 8&13: Upstream Leased Assetsand Downstream Leased Assets

85

4.9 Category 10: Processing of Sold Products 90

4.10 Category 11: Use of ProductsSold

94

4.11 Category 12: End-of-LifeTreatment of Sold Products

100

4.12 Category 14: Franchises 104

4.13 Category 15: Investments 108

Page

簡報大綱簡報大綱

PwC Taiwan 資誠

5 Data collection – Primary. Secondary, proxy 115

6 Potential impact of Scope 3 Standard 124

Page

簡報大綱簡報大綱

PwC Taiwan 資誠

Starting from GHG protocolSection 1

PwC Taiwan 資誠

The Main Purpose of GHG Protocol

Enable corporate and governmentmeasurement and managementpractices that lead to a low carboneconomy

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 2

PwC Taiwan 資誠

Basic Framework of the GHG Protocol

• Established concepts of organizational and operational boundaries

• Established options for consolidation methods

• Established carbon accounting principles of Accuracy, Completeness, Consistency,Transparency and Relevance

• Established concepts of Scopes 1, 2 and 3, Scopes 1 and 2 “mandatory”,Scope 3 “optional”

• Enabled corporations to begin reporting carbon emissions (to meet voluntarycommitments or regulatory requirements) under a common, internationallyrecognized framework

• Art, not science – with estimations and many judgment calls tovoluntary reporting

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 3

PwC Taiwan 資誠

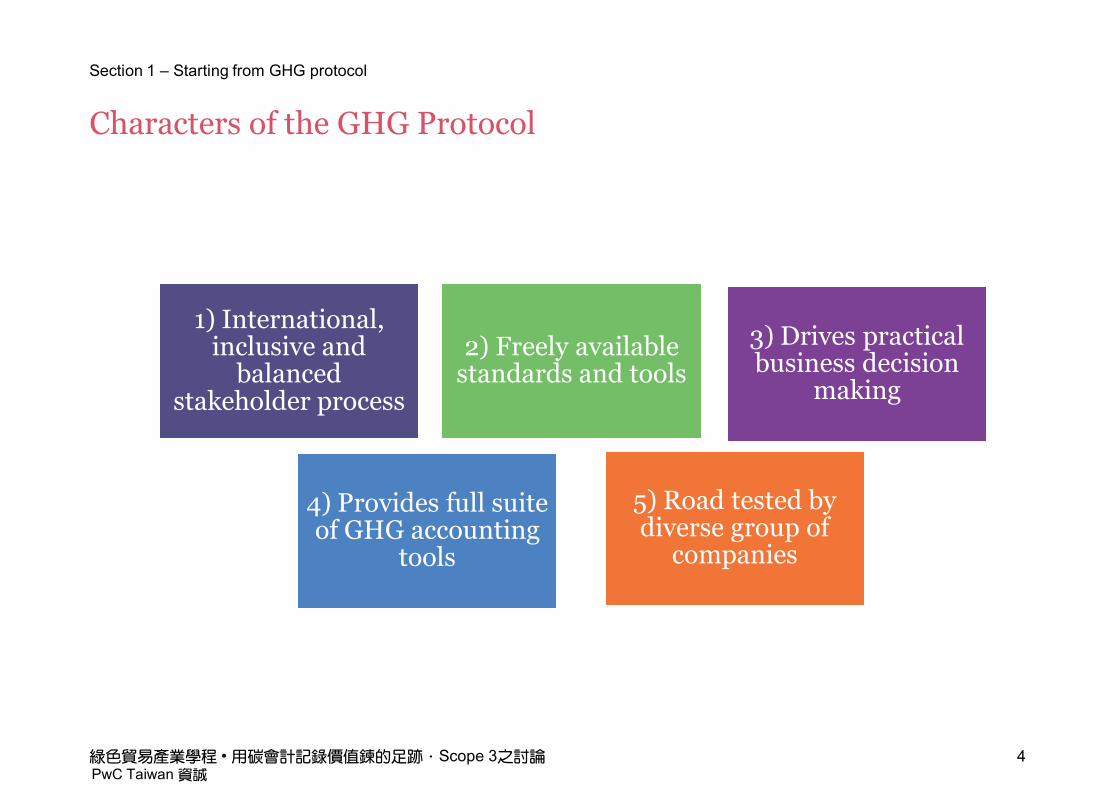

Characters of the GHG Protocol

1) International,inclusive and

balancedstakeholder process

2) Freely availablestandards and tools

3) Drives practicalbusiness decision

making

4) Provides full suiteof GHG accounting

tools

5) Road tested bydiverse group of

companies

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 4

PwC Taiwan 資誠

1) International, inclusive and balanced stakeholder processFoundational framework for many programs

• Launched in 1998, mission is to develop and promote broad adoption ofinternationally accepted GHG accounting and reporting standards for business andorganizations. Significant programs adopting GHG Protocol include:

California Climate Action Registry International Trade Associations (Aluminum,IPIECA, ICFPA, Cement, Iron and Steel)

Carbon Disclosure Project (CDP) Respect Europe Business Leaders Initiative forClimate Change(BLICC)

Chicago Climate Exchange U.K. Emissions Trading System

The Climate Registry U.S. Department of Energy (1605b)

Dow Jones Sustainability Index U.S. EPA Climate Leaders Initiative

E.U. Emissions Trading Scheme U.S. EPA Mandatory GHG Reporting Rule

French REGES Protocol U.S. Executive Order 13514

Global Reporting Initiative Walmart Supplier GHG Innovation Project

ISO 14064 Part 1 World Economic Forum Global GHG Registry

Japanese Ministry of Economy, Trade &Industry

World Wildlife Fund Climate Savers

Mexico GHG Program

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 5

PwC Taiwan 資誠

2) Freely available standards and toolsThe GHG Protocol Family Wheel *

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 6

In Planning

GHGAccounting &Management

(All standards available at www.ghgprotocol.org)

* Sector specific guidance under development

PwC Taiwan 資誠

3) Drives practical business decision makingSelected users of the GHG Protocol

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 7

PwC Taiwan 資誠

3) Drives practical business decision makingBusiness goals served by a GHG inventory

Understand

Emission-relatedrisks

Emission-relatedopportunities

Identify

GHG reductionopportunities

Set reductiontargets and trackperformance

Engage

Suppliers andcustomers

Enhance theworkingrelationship

Report

To stakeholdersand the public

Establishcredibility anddifferentiate yourcompany

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 8

PwC Taiwan 資誠

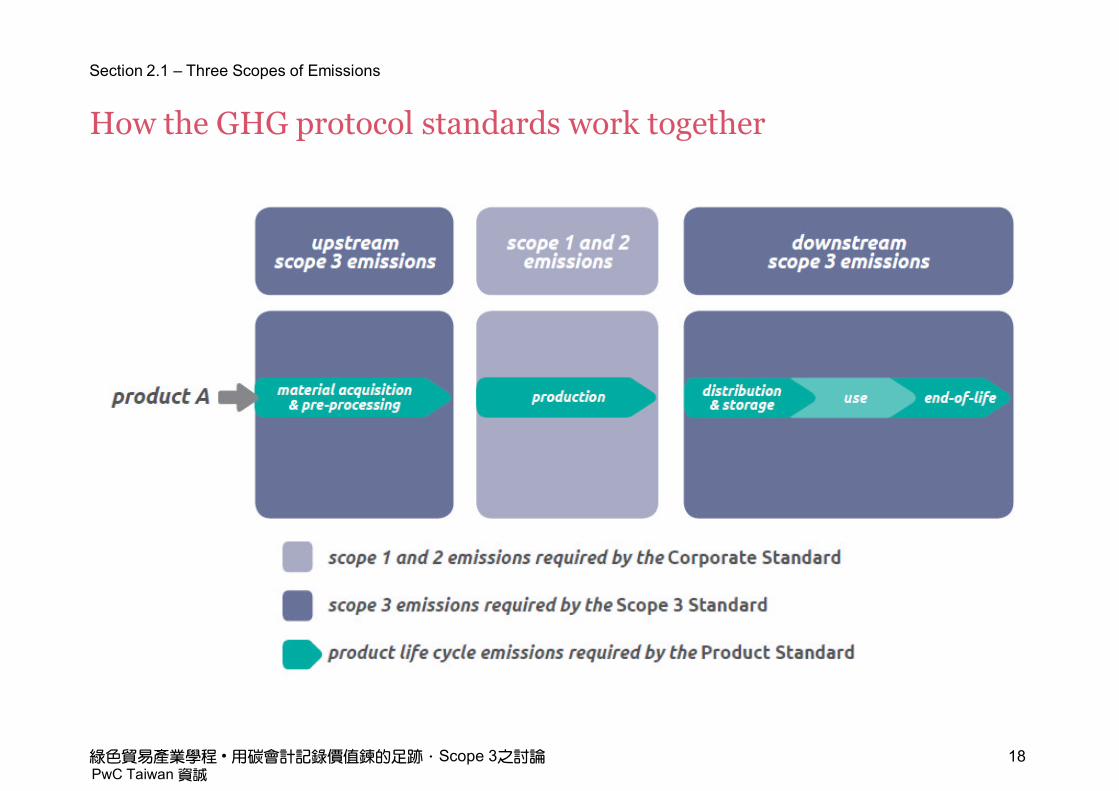

4) Provides full suite of GHG accounting toolsHow the GHG protocol standards work together

* Source: World Resources Institute (WRI) / World Business Council for Sustainable Development Corporate Value Chain (Scope 3)Accounting and Reporting Standard, Supplement to the GHG Protocol Corporate Accounting and Reporting Standard, December 2011

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 9

PwC Taiwan 資誠

5) Road tested by diverse group of companiesScope 3 Standard Road Testing Companies

Companies

3M Company Italcementi Group *

Abengoa Kraft Foods

Acer Inc Levi Strauss & Co. *

Airbus S.A.S National Grid *

AkzoNobel Natura Cosméticos

Alcan Packaging New Belgium Brewing

Autodesk, Inc. Pfizer

Baoshan Iron & Steel CO. LTD Pinchin Environmental Ltd.

BASF SE PricewaterhouseCoopers *

Coca-Cola Erfrischungsgetränke AG Public Service Enterprise Group, Inc.

Deutsche Post DHL* SAP AG

Deutsche Telekom AG Sc Johnson and Son

Eclipse Networks (Pty) Ltd. Siemens *

Ford Motor Company Suzano Pulp and Paper

US GSA Federal Acquisition Service Swire Beverages

Hasbro Inc. UK Highways Agency

Hydro Tasmania Veolia Water

IBM VT Group *

IKEA Webcor Builders

Section 1 – Starting from GHG protocol

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 10

PwC Taiwan 資誠

GHG accounting and reportingprinciples

Section 2

PwC Taiwan 資誠

Three Scopes of EmissionsSection 2.1

PwC Taiwan 資誠

Three scopes of emissions

Emissions type

Direct emissions

Indirect emissions

Scope

Scope 1

Scope 2

Scope 3

Definition

Emissions from operations that areowned or controlled by the reportingcompany

Emissions from the generation ofpurchased or acquired electricity,steam, heating, or cooling consumed bythe reporting company

All indirect emissions (not included inscope 2) that occur in the value chain ofthe reporting company, including bothupstream and downstream emissions

Examples

Emissions from combustion in ownedor controlled boilers, furnaces,vehicles, etc.; emissions fromchemical production in owned orcontrolled process equipment

Use of purchased electricity, steam,heating, or cooling

Production of purchased products,transportation of purchased products,or use of sold products

Note: biogenic emissions shall not be included in scopes, but included and reported separately in the public report

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 13

PwC Taiwan 資誠

Direct and indirect emissions

Direct: emissions from sources owned or controlled by the reporting company

Indirect: emissions that are a consequence of the activities of the reporting companybut occur at sources owned or controlled by another company

Your factoryYour factoryPower plantPower plant(owned by utility company)(owned by utility company)

Maintenance serviceMaintenance service(owned by another company)(owned by another company)

Direct EmissionsIndirect Emissions Indirect Emissions

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 14

PwC Taiwan 資誠

Scope 1 emissions• Direct GHG emissions from sources a company owns or controls

• Examples:

– Generation of electricity, heat, or steam

– Physical or chemical processing

– Transportation of materials, products, waste, and employees

– Fugitive emissions

Your factoryYour factoryPower plantPower plant(owned by utility company)(owned by utility company)

Maintenance serviceMaintenance service(owned by another company)(owned by another company)

Direct EmissionsIndirect Emissions Indirect Emissions

Scope 1Scope 1

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 15

PwC Taiwan 資誠

Scope 2 emissions

• Indirect GHG emissions from generation of purchased or acquired utilitiesconsumed by the reporting company.

• Examples, purchased and/or acquired:

– Electricity

– Heating

– Cooling

– Steam

Your factoryYour factoryPower plantPower plant(owned by utility company)(owned by utility company)

Maintenance serviceMaintenance service(owned by another company)(owned by another company)

Direct EmissionsIndirect Emissions Indirect Emissions

Scope 2Scope 2

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 16

PwC Taiwan 資誠

Scope 3 emissionsDetermining scope by emission source

Raw MaterialProduction

Raw MaterialDistribution

Product

ManufacturingProductDistribution

Retailing &Consumption

DisposalSourceRecycling

Reporting company’s operations

Scope 3Upstream

Scope 3Downstream

Scope 1Owned/Controlled Operations

Scope 2Purchased electricity

• Understood that double counting may occur when different companies claimownership of same emissions or reductions

• Same emissions should never be reported twice under same scope (except S3)

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 17

PwC Taiwan 資誠

How the GHG protocol standards work together

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 18

PwC Taiwan 資誠

Reporting requirements

Report in conformancewith the GHG Protocol

Corporate Standard

Corporate StandardCorporate Standard Corporate Value Chain (Scope 3) StandardCorporate Value Chain (Scope 3) Standard

Report in conformance withthe GHG Protocol Corporate

Standardand Scope 3 Standard

Section 2.1 – Three Scopes of Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 19

PwC Taiwan 資誠

Basics of developing a GHG inventorySection 2.2

PwC Taiwan 資誠

Basics of developing a GHG inventory

• Setting organizationalboundaries

• How many and where areyour facilities locatedacross Taiwan and Globe?What is the impact ofleased spaces?

• At what point do you takeownership of productsfrom suppliers? Do youhave your own distributionfleet?

• Setting operationalboundaries

• Identify the categories ofemissions caused by yourcompany’s activities thatshould be included in theinventory.

Boundaries

• Compile and aggregate data

• Calculate absolute results

• Normalize data

Analyzing

• Identify factorsimpacting selectionof quantificationprotocols.

• Develop GHGEmissions InventoryReport

• Develop summaryreport on keyindicators

• Data Quality/Assurance/ TargetSetting

• Communicate results

Reporting

Section 2.2 – Basics of developing a GHG inventory

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 21

Setting the Boundary

Collecting the Data

PwC Taiwan 資誠

Setting the BoundaryOrganizational boundaries

• A company’s scope 1, scope 2, and scope 3 emissions depend on the chosenOrganizational Boundaries

– Which company operations to include in inventory

– What percentage of each operation to include

30%

75%

0%

0%

100%

100%

100%

100%

100%

Total reported emissions depend on how organizational boundaries are defined

Section 2.2 – Basics of developing a GHG inventory

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 22

PwC Taiwan 資誠

Justifying exclusions: What is relevant

• contribute significantly to the company’s totalanticipated scope 3 emissions.

Size

• potential emissions reductions that could beundertaken or influenced by the company.

Influence

• contribute to the company’s risk exposureRisk

• deemed critical by key stakeholders (e.g., customers,suppliers, investors or civil society)

Stakeholders

• outsourced activities previously performed in-houseOutsourcing

• identified as significant by sector-specific guidanceSector Guidance

• meet any additional criteria developed by thecompany or industry sector

Other

Section 2.2 – Basics of developing a GHG inventory

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 23

PwC Taiwan 資誠

Three consolidation approaches

• Under the equity share approach, a company accounts for GHGemissions from operations according to its share of equity in theoperation. The equity share reflects economic interest,which is the extent of rights a company has to the risks andrewards flowing from an operation.

Equity Share

• Under the financial control approach, a company accounts for100 percent of the GHG emissions over which it hasfinancial control. It does not account for GHG emissions fromoperations in which it owns an interest but does not havefinancial control.

FinancialControl

• Under the operational control approach, a company accountsfor 100 percent of the GHG emissions over which it hasoperational control. It does not account for GHG emissionsfrom operations in which it owns an interest but does not haveoperational control.

OperationalControl

Section 2.2 – Basics of developing a GHG inventory

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 24

PwC Taiwan 資誠

Selecting a consolidation approach

What to consider when choosing a consolidation approach:

• Commercial reality

• Influence over emissions

• Program and regulatory requirements

• Liability and risk management

• Financial accounting

• Management information and performance tracking

• Administrative costs and data access

• Completeness of reporting

Section 2.2 – Basics of developing a GHG inventory

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 25

PwC Taiwan 資誠

Which GHGsSection 2.3

PwC Taiwan 資誠

Sources of Kyoto greenhouse gasses

Greenhouse gas (GHG) Types and source ofsignificant greenhousegases

Activities that contribute toemissions

Carbon dioxide (CO2) Burning of fossil fuels andland-clearing

Electricity generation and use;transport

Methane (CH4) Agricultural activities;emissions from landfills andwastewater treatment;emissions from fossil fuelproduction and mining

Resource consumption;primary production; wastedisposal to landfill

Nitrous oxide (N2O) Burning of fossil fuels andvegetation

Agriculture; cultivating soiland use of nitrogen fertilizers

Hydrofluorocarbons (HFCs) Used in refrigeration and airconditioning

Industrial processes; buildingdesign; refrigeration

Perfluorocarbons (PFCs) Emitted during aluminiumproduction

Manufacturing; resourceconsumption

Sulfur hexafluoride (SF6) Electricity transmission anddistribution

Electricity generation andconsumption

Section 2.3 – Which GHGs

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 27

PwC Taiwan 資誠

Global Warming Potential (GWP) factors

• GWP provides a means of comparing how a given mass of GHG contributes toglobal warming. It provides a scale whereby each gas is compared with the samemass of carbon (remember ‘carbon is key’)

• Radiative forcing impact of one unit of GHG relative to one unit of CO2

• High GWP reflects a higher absorption of infrared & longer atmospheric lifetime

• Units are “carbon dioxide equivalent” (CO2e)

Greenhouse gas Global warming potential

Carbon dioxide (CO2) 1.0 t CO2-e

Methane (CH4) 24 t CO2-e

Nitrous oxide (N2O) 310 t CO2-e

Hydrofluorocarbons (HFCs) 140 to 11,400 t CO2-e

Perfluorocarbons (PFCs) 6,500 to 9,200 t CO2-e

Sulfur hexafluoride (SF6) 23,900 t CO2-e

100 tonnes of CO2 + 1 tonne of CH4 = 121 t CO2-e

i.e. (100 t x 1 CO2-e) + (1 t x 21 CO2-e) = 121 t CO2-e.

• Use mostrecent GWPfactorspublished byIPCC basedon a 100 yeartime horizon

Section 2.3 – Which GHGs

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 28

PwC Taiwan 資誠

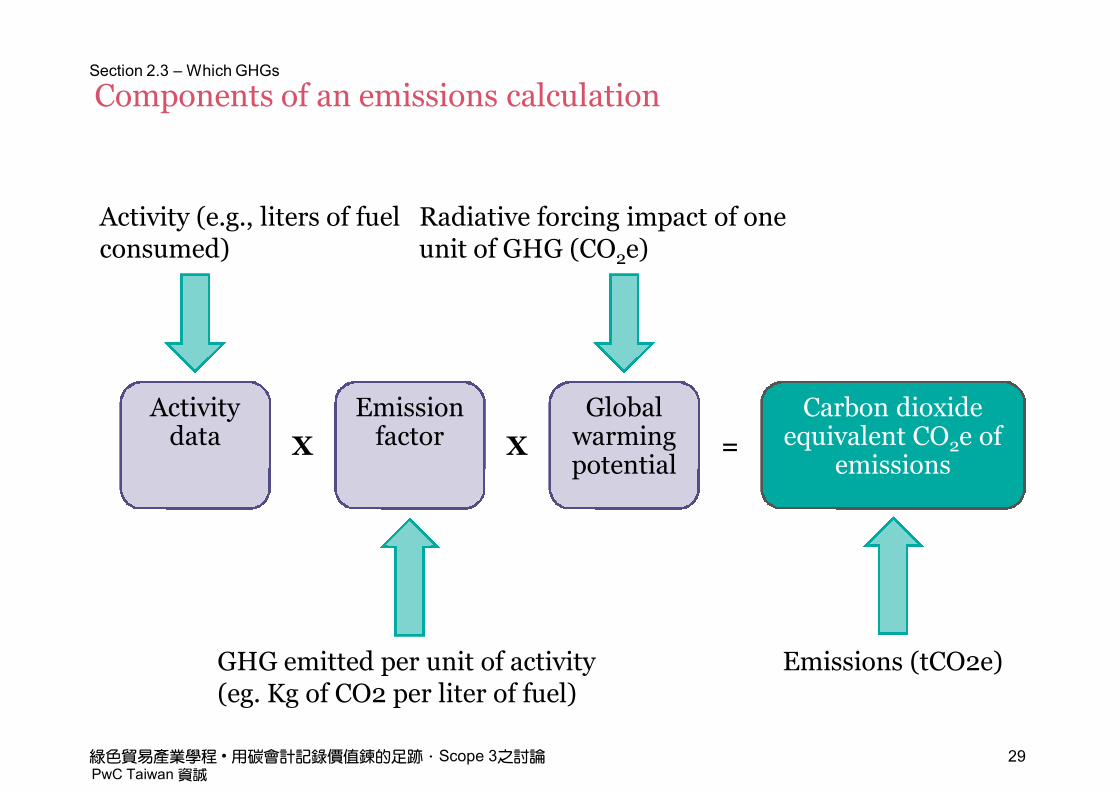

Components of an emissions calculation

Emissions (tCO2e)

Activity (e.g., liters of fuelconsumed)

GHG emitted per unit of activity(eg. Kg of CO2 per liter of fuel)

Radiative forcing impact of oneunit of GHG (CO2e)

X X =

Activitydata

Globalwarmingpotential

Emissionfactor

Carbon dioxideequivalent CO2e of

emissions

Section 2.3 – Which GHGs

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 29

PwC Taiwan 資誠

Example: transportation emissions

GHG emissionsActivity data

100 liters of gas0.23 t CO2e

Supplier activity data

Collect fuel purchaserecords

or miles traveled byvehicles

Find emission factorConsult GHGP

emission factors

Find GWP value

GHG GWP

CO2 1

X X =

GWP valueEmission factor

.0023 tCO2/liter

GHG GWPCO2 1

Section 2.3 – Which GHGs

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 30

PwC Taiwan 資誠

Corporate Value Chain (Scope 3)Accounting and Reporting Standard

Section 3

PwC Taiwan 資誠

What is the Scope 3 standard?Section 3.1

PwC Taiwan 資誠

Scope 3 categories

Upstream ordownstream

Scope 3 category

Upstream Scope 3emissions

1 Purchased goods and services

2 Capital goods

3 Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

4 Upstream transportation and distribution

5 Waste generated in operations

6 Business travel

7 Employee commuting

8 Upstream leased assets

Downstream Scope 3emissions

9 Downstream transportation and distribution

10 Processing of sold products

11 Use of sold products

12 End-of-life treatment of sold products

13 Downstream leased assets

14 Franchises

15 Investments

Section 3.1 – What is the Scope 3 standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 33

PwC Taiwan 資誠

Minimum boundaries

•Each Scope 3 category has a “minimum boundary” in order to standardize theboundaries of each category and to help companies understand which activitiesshould be accounted for.

•The minimum boundaries are intended to ensure that major activities areincluded in the scope 3 inventory, while clarifying that companies need notaccount for the value chain emissions of each entity in its value chain, adinfinitum.

•Companies may include emissions from optional activities within each category.

•Companies may exclude Scope 3 activities included in the minimum boundary ofeach category, provided that any exclusion is disclosed and justified.

Section 3.1 – What is the Scope 3 standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 34

PwC Taiwan 資誠

Time boundaries for Scope 3Section 3.1 – What is the Scope 3 standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 35

PwC Taiwan 資誠

Standards developmentPwC involved throughout process:

•Educated WRI/WBSCD on benefitsof assurance-based standards

•Provided financial support

•Served on the steering committee forthe development of both standards

•Technical Lead for “What Group,”which developed Scope 3requirements

•Revised chapters on assurance basedon feedback from road testing ofstandards

•Supported various clients to “roadtest” assurance to the draft standards

•PwC Canada, Germany, Hong Kong,Italy, UK & US helped to develop thestandards

Section 3.1 – What is the Scope 3 standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 36

PwC Taiwan 資誠

Transformational nature of Scope 3

• Represents a broadening of discussion to what the organization impacts,not just what organization controls

• Can lead to increased revenue, decreased costs, increased margins becauseexpectation of additional information means more organizations reporting moredata to enable more informed decision-making

• Tracking and reporting are leading initiatives – bigger transformationalinitiative is from engaging with suppliers, product developers, and otherstakeholders to reduce impact

Section 3.1 – What is the Scope 3 standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 37

PwC Taiwan 資誠

What is the Goal of the Scope 3Standard?

Section 3.2

PwC Taiwan 資誠

Goals of the Scope 3 Standard

• Primary goal: To support companies to reduce emissions

– Make informed choices about reduction opportunities within their valuechain

– Increase consistency and transparency in value chain GHG accountingand reporting

– To support comparison of one company’s GHG emissions over time

Section 3.2 – What is the Goal of the Scope 3 Standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 39

PwC Taiwan 資誠

Business goals served by a Scope 3 Inventory

Section 3.2 – What is the Goal of the Scope 3 Standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 40

Business goals

Identify and understandrisks and opportunitiesassociated with valuechain emissions

Identify GHG reductionopportunities, setreduction targets, andtrack performance

Engage value chainpartners in GHGmanagement

Enhance stakeholderinformation andcorporate reputationthrough public reporting

Type of risk

Regulatory

Supply chaincosts andreliability

Product andtechnology

Litigation

Reputation

Type of opportunity

Efficiency and costsavings

Drive innovation

Increase sales andcustomer loyalty

Improve stakeholderrelations

Company differentiation

PwC Taiwan 資誠

What the GHG Protocol and Scope 3 Standard should NOT beused for:

• Address avoided emissions

• Support the accounting of GHG emission offsets or claims of carbon neutrality

• Compare two or more companies’ GHG performance

Section 3.2 – What is the Goal of the Scope 3 Standard?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 41

PwC Taiwan 資誠

Why is the Scope 3 Standard Relevant?Section 3.3

PwC Taiwan 資誠

Walmart case study

•In 2/2010, Walmart announced a goal to eliminate 20.0 MMT CO2e of GHGemissions from its global supply chain by 12/2015

•In 6/2011, Walmart reported S1&S2 of 21.4 MMT CO2e and S3 of 42.8k MT CO2eGHG emissions to the Carbon Disclosure Project (CDP)

•Walmart estimates that 95% of itsemissions are in its supply chain, so Walmartcould conceivably be reporting at least anadditional 428.0 MMT CO2e of GHGsfor its Scope 3 supply chain emissions alone,not including all other Scope 3 categories

Total S1 & S2 Scope 1 Scope 2 Scope 3 *

21,404,099 5,922,051 15,482,048 42,841

* Includes Business Travel and Transportation & DistributionScope 3 categories

Scopes 1 + 2 Scope 3

Hypothetical FY12GHG emissions

Section 3.3 – Why is the Scope 3 Standard Relevant?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 43

PwC Taiwan 資誠

Apple case study

http://www.apple.com/environment/ ~98% = Scope 3 emissions

Section 3.3 – Why is the Scope 3 Standard Relevant?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 44

PwC Taiwan 資誠

CDP 2011 S&P 500 Scope 3 case study

• Of 339 S&P 500 companies reportingto CDP and 306 reporting GHGemissions, 214 reported someform of Scope 3 emissions (upfrom 174 in 2010)

• For some PwC clients Scope 3 caneasily dwarf combined Scope 1 and 2GHG emissions currently reported

• Release of Scope 3 Standardrepresents a paradigm shift for carbonreporting and we can provide strategicadvice to clients on how best toaccomplish

Sources: Carbon Disclosure Project S&P 500 2011 Report

S&P 500population

= 500

Respondents toCDP 2011 =

339

Publiclyreported GHG

emissions= 306

Reported someform of Scope 3emissions =

214

Section 3.3 – Why is the Scope 3 Standard Relevant?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 45

PwC Taiwan 資誠

Percent of S&P 500 companies disclosing Scope 3 emissions bysector * 0% 10% 20% 30% 40% 50% 60% 70% 80%

Consumer Discretionary

Consumer Staples

Energy

Financials

Health Care

Industrials

Information Technology

Materials

Telecommunication Services

Utilities

* Source: 2011 Carbon Disclosure Project data

Section 3.3 – Why is the Scope 3 Standard Relevant?

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 46

PwC Taiwan 資誠

Identifying Scope 3 EmissionsSection 4

PwC Taiwan 資誠

Reporting Requirements

Scope 3 reporting requirements:

• Companies shall account for all Scope 3 emissions and disclose and justify exclusions

• Companies shall account for emissions from each Scope 3 category according todefined minimum boundaries.

• Companies shall account for Scope 3 emissions of six priority Kyoto gases (defined inGHG Protocol) of CO2, CH4, N2O, HFCs, PFCs, and SF6, where applicable.

• Companies shall follow the principles of relevance, completeness, accuracy,consistency and transparency when deciding whether to exclude any activities fromthe scope 3 inventory

Companies may exclude categories, but exclusion shall be disclosed and justified

• Some categories are simply not applicable (e.g., a company has no leased assets)

• For some categories:

– lack of data and

– the scope 3 activities are insignificant in size (e.g., employee commuting)

Section 4 – Identifying Scope 3 Emissions

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 48

PwC Taiwan 資誠

Category 1: Purchased goods andservices

Section 4.1

PwC Taiwan 資誠

1. Purchased goods & services:Description

All upstream (i.e., cradle-to-gate) emissions from the production of productspurchased or acquired by the reporting company in the reporting year

Includes extraction, production, & transportation of goods & services purchased oracquired by reporting company in reporting year (excludes categories 2-8)

Products include both goods (tangible products) and services (intangible products)

Section 4.1 – Category 1: Purchased goods and services

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 50

PwC Taiwan 資誠

1. Purchased goods & services:Elements

• Extraction of raw materials

• Agricultural Activities

• Manufacturing, product and processing

• Generation of electricity consumed by upstream activities

• Disposal/treatment of waste generated by upstream activities

• Transportation of materials and products between suppliers

• Any other activities prior to acquisition by the reporting company

• Land use and land-use change

• SuppliersScope 1

emissions of

Section 4.1 – Category 1: Purchased goods and services

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 51

PwC Taiwan 資誠

1. Purchased goods & services:

Minimum boundaries

All upstream (cradle-to-gate) emissions of purchased goods and services. Cradle-to-gateemissions may include:

Extraction of raw materials;

•Agricultural activities;

•Manufacturing, production, and processing;

•Generation of electricity consumed by upstream activities;

•Disposal/treatment of waste generated by upstream activities;

•Land use and land-use change;

•Transportation of materials and products between suppliers;

•Any other activities prior to acquisition by the reporting company

Section 4.1 – Category 1: Purchased goods and services

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 52

PwC Taiwan 資誠

Category 2: Capital GoodsSection 4.2

PwC Taiwan 資誠

2. Capital goods:Description

All upstream (i.e., cradle-to-gate) emissions from the production of capitalgoods purchased or acquired by the reporting company in the reporting year

Emissions from use of capital goods are included in scope 1 or scope 2

Section 4.2 – Category 2: Capital Goods

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 54

PwC Taiwan 資誠

2. Capital goods:Elements

• Final Products that have an extended life and are usedby the company to manufacture the product, provide aservice, or sell, store, and deliver merchandise

• Equipment, machinery, buildings, facilities, andvehicles

• In financial accounting, anything treated as fixed assetsor plant, property

• Suppliers of capital goodsScope 1

emissions of

• Companies should not depreciate, discount, oramortize the emissions

Note:

Section 4.2 – Category 2: Capital Goods

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 55

PwC Taiwan 資誠

2. Capital goods:Minimum boundaries

All upstream (cradle-to-gate) emissions of purchased capital goods.

Section 4.2 – Category 2: Capital Goods

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 56

PwC Taiwan 資誠

Category 3 : Fuel- and energy-relatedactivities (not included in Scope 1 orScope 2)

Section 4.3

PwC Taiwan 資誠

3. Fuel- and energy-related activities:Description

Emissions related to the production of fuels and energy purchased andconsumed by the reporting company in the reporting year that are notincluded in scope 1 or scope 2.

Section 4.3 – Category 3 : Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 58

PwC Taiwan 資誠

3. Fuel- and energy-related activities:Elements

• Upstream emissions of purchased fuels

• Upstream emissions of purchased electricity

• Transmissions & Distribution losses

• Generation of purchased electricity that is sold to end users

• Electric utilities, fuel producersScope 1

emissions of

Section 4.3 – Category 3 : Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 59

PwC Taiwan 資誠

3. Fuel- and energy-related activities:Minimum boundaries

• For upstream emissions of purchased fuels: all upstream (cradle-to-gate)emissions of purchased fuels (from raw material extraction up to the pointof, but excluding combustion)

• For upstream emissions of purchased electricity: all upstream (cradle-to-gate) emissions of purchased fuels (from raw material extraction up to thepoint of, but excluding, combustion by a power generator)

• For T&D losses: all upstream (cradle-to-gate) emissions of energy consumedin a T&D system, including emissions from combustion

• For generation of purchased electricity that is sold to end users: emissionsfrom the generation of purchased energy

Section 4.3 – Category 3 : Fuel- and energy-related activities (not included in Scope 1 or Scope 2)

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 60

PwC Taiwan 資誠

Category 4&9: Transportation andDistribution

Section 4.4

PwC Taiwan 資誠

4/9. Transportation and distribution:Description

Upstream:

1) Transportation and distribution of products purchased by the reportingcompany in the reporting year between a company’s tier 1 suppliers and itsown operations (in vehicles and facilities not owned or controlled by thereporting company)

2) Transportation and distribution services purchased by the reportingcompany in the reporting year, including inbound logistics, outbound logistics(e.g. of sold products), and transportation and distribution between acompany’s own facilities (in vehicles and facilities not owned or controlled bythe reporting company)

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 62

PwC Taiwan 資誠

4/9. Transportation and distribution:Description

Downstream: Transportation and distribution of products sold by thereporting company in the reporting year between the reporting company’soperations and the end consumer (if not paid for by the reporting company),including retail and storage (in vehicles and facilities not owned or controlledby the reporting company)

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 63

PwC Taiwan 資誠

4. Transportation and distribution:Elements

For example:• Air transport• Rail transport• Road transport• Marine transport• Storage in

warehouses anddistributioncenters

• Storage in retailfacilities

• Third-party transportation & distribution of productspurchased by the reporting company in the reportingyear, between a company’s Tier 1 suppliers and itsown operations

• Third-party transportation & distribution servicespurchased by the reporting company in thereporting year including inbound/outboundlogistics

• Third-party transportation and distribution companiesScope 1

emissions of

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 64

PwC Taiwan 資誠

9. Transportation and distribution:Elements

• Transportation company, 3rd party logistics provider,retailer

Scope 1emissions of

Category 9 only includes transportation and distribution-related emissionsthat occur after the reporting company pays to produce and distribute itsproducts (not paid by reporting company)

• Transportation and distribution of sold products

• Warehousing of sold products

• Retail of sold products

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 65

PwC Taiwan 資誠

4/9.Transportation and distribution:Accounting for emissions from T&D activities

Transportation and distribution activity in thevalue chain

Scope and scope 3 category

Transportation and distribution in vehicles andfacilities owned or controlled by the reporting company

Scope 1 (for fuel use) or scope 2 (for electricityuse)

Transportation and distribution in vehicles andfacilities leased by and operated by the reportingcompany (and not already included in scope 1 orscope 2)

Scope 3, category 8 (Upstream leased assets)

Transportation and distribution of purchased products,upstream of the reporting company’s tier 1 suppliers(e.g., transportation between a company’s tier 2 andtier 1 suppliers)

Scope 3, category 1 (Purchased goods andservices), since emissions from transportationare already included in the cradle-to-gateemissions of purchased products. Theseemissions are not required to be reportedseparately from category

Production of vehicles (e.g., ships, trucks, planes)purchased or acquired by the reporting company

Account for the upstream (i.e., cradle-to-gate)emissions associated with manufacturingvehicles in Scope 3, category 2 (Capitalgoods)

Transportation of fuels and energy consumed by thereporting company

Scope 3, category 3 (Fuel- and energy-relatedemissions not included in scope 1 or scope 2

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 66

PwC Taiwan 資誠

4/9.Transportation and distribution:Accounting for emissions from T&D activities

Transportation and distribution activity in thevalue chain

Scope and scope 3 category

Transportation and distribution of productspurchased by the reporting company, between acompany’s tier 1 suppliers and its own operations(in vehicles and facilities not owned or controlledby the reporting company)

Scope 3, category 4 (Upstream transportation anddistribution)

Transportation and distribution services purchasedby the reporting company in the reporting year(either directly or through an intermediary),including inbound logistics, outbound logistics(e.g., of sold products), and transportation anddistribution between a company’s own facilities (invehicles and facilities not owned or controlled bythe reporting company)

Transportation and distribution of products sold bythe reporting company between the reportingcompany’s operations and the end consumer (ifnot paid for by the reporting company), includingretail and storage (in vehicles and facilities notowned or controlled by the reporting company)

Scope 3, category 9 (Downstream transportationand distribution)

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 67

PwC Taiwan 資誠

4/9. Transportation and distribution:Minimum boundaries

The scope 1 and scope 2 emissions of transportation and distribution providersthat occur during use of vehicles and facilities (e.g. from energy use)Optional: The life cycle emissions associated with manufacturing vehicles,facilities, or infrastructure

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 68

PwC Taiwan 資誠

4/9. Transportation and distribution:Case studies

Think: What other types of companies can provide value to customers inthe form of scope 3 emissions reductions by reducing their own scope 1?

Air transport Road transport

Storage of Sold Products Retail of Sold Products

Section 4.4 – Category 4&9: Transportation and Distribution

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 69

PwC Taiwan 資誠

Category 5: Waste Generated inOperations

Section 4.5

PwC Taiwan 資誠

5. Waste generated in operations:Description

Emissions from third-party disposal and treatment of waste that is generatedin the reporting company’s owned or controlled operations in the reportingyear

Section 4.5 – Category 5: Waste Generated in Operations

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 71

PwC Taiwan 資誠

5. Waste generated in operations:Elements

Recycling upstream or downstream: avoid double counting

• Waste/wastewater management companiesScope 1 emissions

of

• Disposal in a landfill

• Disposal in a landfill with landfill-gas-to-energy (LFGTE)

• Recovery for Recycling

• Incineration

• Composting

• Waste-to-Energy (WTE) or Energy-from-Waste (EfW)

• Wastewater Treatment

Section 4.5 – Category 5: Waste Generated in Operations

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 72

PwC Taiwan 資誠

5. Waste generated in operations:Minimum boundaries

The scope 1 and scope 2 emissions of waste management suppliers that occurduring disposal or treatment

Optional: Emissions from transportation of waste

Section 4.5 – Category 5: Waste Generated in Operations

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 73

PwC Taiwan 資誠

5. Waste generated in operations:

Section 4.5 – Category 5: Waste Generated in Operations

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 74

PwC Taiwan 資誠

Category 6: Business TravelSection 4.6

PwC Taiwan 資誠

6. Business travel:Description

Emissions from the transportation of employees for business-relatedactivities in vehicles owned or operated by third parties

Section 4.6 – Category 6: Business Travel

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 76

PwC Taiwan 資誠

6. Business travel:Elements

• Transportation suppliers (e.g. airlines)Scope 1

emissions of

• Air travel

• Rail Travel

• Bus Travel

• Automobile travel (e.g., business travel in rental cars or employee-owned vehicles other than employee commuting to and from work

• Other modes of travel

• Companies may optionally include emissions from businesstravelers staying in hotels

Section 4.6 – Category 6: Business Travel

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 77

PwC Taiwan 資誠

6. Business travel:Minimum boundaries

The scope 1 and scope 2 emissions of transportation carriers that occur duringuse of vehicles (e.g. from energy use)

Optional: The life cycle emissions associated with manufacturing vehicles orinfrastructure

Section 4.6 – Category 6: Business Travel

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 78

PwC Taiwan 資誠

6. Business travel:PwC’s air travel carbon emission calculation

Section 4.6 – Category 6: Business Travel

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 79

PwC Taiwan 資誠

6. Business travel:PwC’s air travel carbon emission calculation

Travelincludes

Section 4.6 – Category 6: Business Travel

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 80

PwC Taiwan 資誠

Category 7: Employee CommutingSection 4.7

PwC Taiwan 資誠

7. Employee commuting:DescriptionTransportation of employees between their homes and their worksites duringthe reporting year (in vehicles not owned or operated by the reportingcompany)

Section 4.7 – Category 7: Employee Commuting

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 82

PwC Taiwan 資誠

7. Employee commuting:Elements

• Upstream because employee commuting is a type of service thatenables company operations

• EmployeesScope 1

emissions of

• Employees commuting to and from work

• May include employee tele-working

Section 4.7 – Category 7: Employee Commuting

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 83

PwC Taiwan 資誠

7. Employee commuting:Minimum boundaries

89

The scope 1 and scope 2 emissions of transportation carriers that occur duringuse of vehicles (e.g. from energy use)

Optional: Emissions from employee teleworking

December2011

Section 4.7 – Category 7: Employee Commuting

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 84

PwC Taiwan 資誠

Category 8&13: Upstream LeasedAssets and Downstream Leased Assets

Section 4.8

PwC Taiwan 資誠

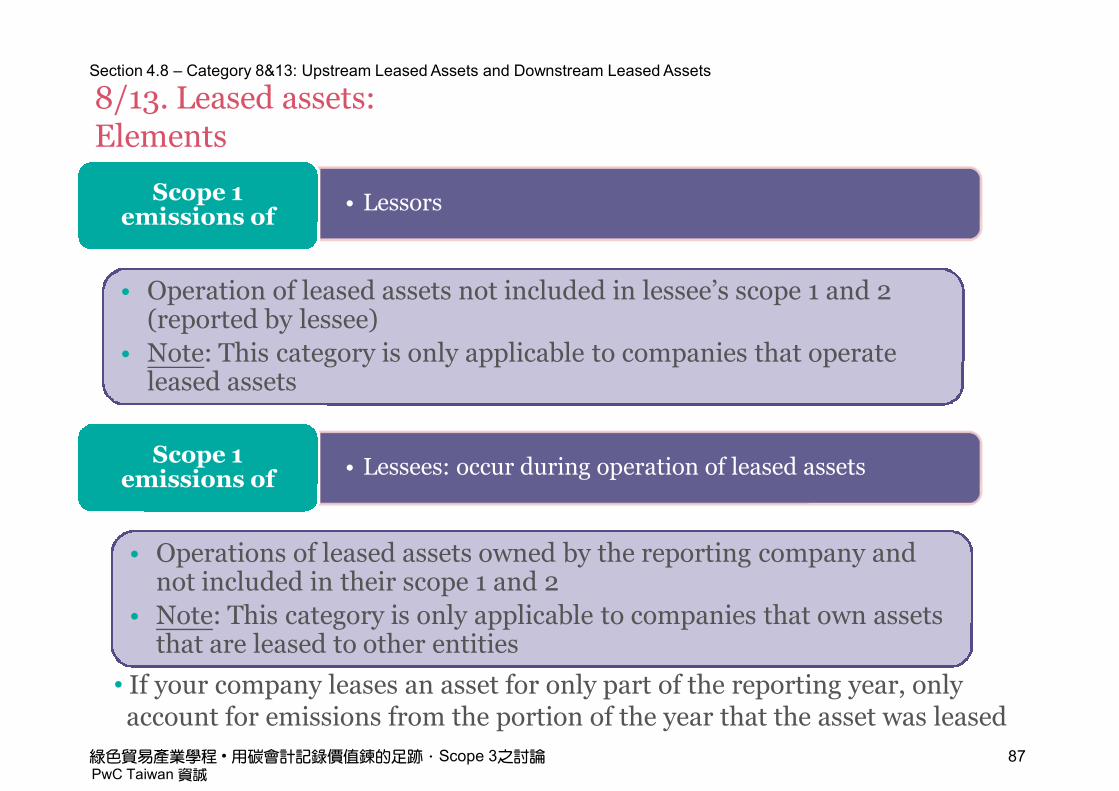

8/13. Leased assets:DescriptionUpstream: Operation of assets leased by the reporting company (lessee) inthe reporting year and not included in scope 1 and scope 2 – reported bylessee

Downstream: Operation of assets owned by the reporting company (lessor)and leased to other entities in the reporting year, not included in scope 1 andscope 2 – reported by lessor

Section 4.8 – Category 8&13: Upstream Leased Assets and Downstream Leased Assets

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 86

PwC Taiwan 資誠

8/13. Leased assets:Elements

• If your company leases an asset for only part of the reporting year, onlyaccount for emissions from the portion of the year that the asset was leased

• LessorsScope 1emissions of

• Operation of leased assets not included in lessee’s scope 1 and 2(reported by lessee)

• Note: This category is only applicable to companies that operateleased assets

• Lessees: occur during operation of leased assetsScope 1

emissions of

• Operations of leased assets owned by the reporting company andnot included in their scope 1 and 2

• Note: This category is only applicable to companies that own assetsthat are leased to other entities

Section 4.8 – Category 8&13: Upstream Leased Assets and Downstream Leased Assets

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 87

PwC Taiwan 資誠

8/13. Leased assets:Minimum boundaries

The scope 1 and scope 2 emissions of lessors that occur during thecompany’s operation of leased assets (e.g. from energy use)

Optional: The life cycle emissions associated with manufacturing orconstructing leased assets

Section 4.8 – Category 8&13: Upstream Leased Assets and Downstream Leased Assets

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 88

PwC Taiwan 資誠

8/13. Leased assets:

Section 4.8 – Category 8&13: Upstream Leased Assets and Downstream Leased Assets

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 89

PwC Taiwan 資誠

Category 10: Processing of SoldProducts

Section 4.9

PwC Taiwan 資誠

10. Processing of sold products:Description

Processing of intermediate products sold in the reporting year bydownstream companies (e.g. manufacturers)

Section 4.9 – Category 10: Processing of Sold Products

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 91

PwC Taiwan 資誠

10. Processing of sold products:Elements

What if my company produces an intermediate product with manypotential downstream applications, each of which has a different GHGemissions profile?

More on this in Chapter 5: Setting the Boundary

• Downstream companies (e.g. manufacturers):emissions that occur during processing (e.g. energyuse)

Scope 1emissions of

• Processing of goods and services sold by the reporting company inthe reporting year

Section 4.9 – Category 10: Processing of Sold Products

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 92

PwC Taiwan 資誠

10. Processing of sold products:Minimum boundaries

The scope 1 and scope 2 emissions of downstream companies that occur duringprocessing (e.g. from energy use)

Section 4.9 – Category 10: Processing of Sold Products

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 93

PwC Taiwan 資誠

Category 11: Use of Products SoldSection 4.10

PwC Taiwan 資誠

11. Use of sold products:Description

Emissions from the use of goods and services sold by the reporting companyin the reporting year by end users

Section 4.10 – Category 11: Use of Products Sold

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 95

PwC Taiwan 資誠

11. Use of sold products:Elements

• CustomersScope 1

emissions of

• Direct Use Phase EmissionsRequired

• Indirect Use Phase EmissionsOptional

• Products that directly consume energy (fuels or electricity duringuse

• Fuels and feedstocks

• Greenhouse gases and products that contain greenhouse gases thatare emitted during use

• Products that indirectly consume energy

Section 4.10 – Category 11: Use of Products Sold

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 96

PwC Taiwan 資誠

11. Use of sold products:Minimum boundaries

The direct use-phase emissions of sold products over their expected lifetime(i.e. the scope 1 and scope 2 emissions of end users that occur from the useof: products that directly consume energy (fuels or electricity) during use;fuels and feedstocks; and GHGs and products that contain for form GHGsthat are emitted during use

Optional: The indirect use-phase emissions of sold products over theirexpected lifetime (i.e. emissions from the use of products that indirectlyconsume energy (fuels or electricity) during use)

Section 4.10 – Category 11: Use of Products Sold

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 97

PwC Taiwan 資誠

11. Use of sold products:Required product types

Product Type Examples

Consumes energy (fuels or electricity) in usephase

Automobiles, aircraft, engines, motors,buildings, appliances, electronics, lighting

Fuels Petroleum products, natural gas, coal, biofuels

Contains GHGs that are emitted during useAerosols, refrigerants, industrial gases, SF6,HFCs, PFCs, fire extinguishers

Other criteria Description

Size They contribute significantly to the company’s total anticipated scope 3 emissions

InfluenceThere are potential emissions reductions that could be undertaken or influencedby the company

RiskThey contribute to the company’s risk exposure (e.g., climate change related riskssuch as financial, regulatory, supply chain, product and technology,compliance/litigation, reputational and physical risks)

StakeholdersThey are deemed critical by key stakeholders (e.g., customers, suppliers, investorsor civil society)

OutsourcingThey are outsourced activities previously performed in-house or activitiesoutsourced by the reporting company that are typically performed in-house byother companies in the reporting company’s sector

Other They meet additional criteria developed by the company or industry sector

Section 4.10 – Category 11: Use of Products Sold

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 98

PwC Taiwan 資誠

11. Use of sold products:Required product types

Type of emissions Product type Examples

Direct use-phase emissions(Required)

Products that directly consumeenergy (fuels or electricity)

duringuse

• Automobiles, aircraft,engines,

motors, power plants,buildings, appliances,electronics, lighting, datacenters, web-based software

Fuels and feedstocks • Petroleum products, naturalgas, coal, biofuels

Greenhouse gases and productsthat contain or form greenhousegases that are emitted duringuse

• CO2, CH4, N2O, HFCs,PFCs,

SF6, refrigeration and air-conditioning equipment,industrial gases, fireextinguishers, fertilizers

Indirect use-phaseemissions(Optional)

Products that indirectlyconsume energy (fuels orelectricity) during use

• Apparel (requires washingand drying), food (requirescooking and refrigeration),pots and pans (requireheating), and soaps anddetergents (require heatedwater)

Section 4.10 – Category 11: Use of Products Sold

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 99

PwC Taiwan 資誠

Category 12: End-of-Life Treatment ofSold Products

Section 4.11

PwC Taiwan 資誠

12. End-of-life treatment of sold products: Description

Waste disposal and treatment of products sold by the reporting company (inthe reporting year) at the end of their life

Section 4.11 – Category 12: End-of-Life Treatment of Sold Products

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 101

PwC Taiwan 資誠

12. End-of-life treatment of sold products: Elements

Requires assumptions about the end-of-life treatment methods used byconsumers

• Waste management companiesScope 1

emissions of

• Waste disposal/treatment of products sold by the reportingcompany (in the reporting year) at the end of their life

Section 4.11 – Category 12: End-of-Life Treatment of Sold Products

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 102

PwC Taiwan 資誠

12. End-of-life treatment of sold products: Minimumboundaries

The scope 1 and scope 2 emissions of waste management companies thatoccur during disposal or treatment of sold products

Section 4.11 – Category 12: End-of-Life Treatment of Sold Products

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 103

PwC Taiwan 資誠

Category 14: FranchisesSection 4.12

PwC Taiwan 資誠

14. Franchises:DescriptionOperation of franchises in the reporting year, not included in scope 1 andscope 2 – reported by franchisor

Section 4.12 – Category 14: Franchises

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 105

PwC Taiwan 資誠

14. Franchises:Elements

• Franchisee: occur during operation of franchisesScope 1

emissions of

• Operation of franchises not included in franchisor’s scope 1 and 2(not reported by franchisor)

• Note: This category is only applicable to companies that ownfranchises

Section 4.12 – Category 14: Franchises

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 106

PwC Taiwan 資誠

14. Franchises:Minimum boundaries

The scope 1 and scope 2 emissions of franchisees that occur duringoperation of franchises (e.g. from energy use)

Optional: The life cycle emissions associated with manufacturing orconstructing franchises

Section 4.12 – Category 14: Franchises

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 107

PwC Taiwan 資誠

Category 15: InvestmentsSection 4.13

PwC Taiwan 資誠

15. Investments:Description

Emissions associated with the reporting company’s investments in thereporting year, not already included in scope 1 or scope 2.

Investments are categorized as a downstream scope 3 category because theprovision of capital or financing is a service provided by the reportingcompany

Section 4.13 – Category 15: Investments

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 109

PwC Taiwan 資誠

15. Investments:Elements

• Company receiving investmentScope 1

emissions of

Primarily for private financial institutions (e.g., commercial banks), butalso relevant to public financial institutions (e.g., multilateral developmentbanks, export credit agencies, etc.)

• Equity investments

• Debt investments

• Project finance

• Managed investments and client services

Section 4.13 – Category 15: Investments

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 110

PwC Taiwan 資誠

15. Investments – Equity investments:Elements

• Company receiving investmentScope 1

emissions of

Includes equity investments in:

• Subsidiaries

• Associate companies

• Joint ventures

• Accounting approach: Account for proportional scope 1 and scope 2emission from the investments that occur in the reporting year

Section 4.13 – Category 15: Investments

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 111

PwC Taiwan 資誠

15. Investments – Debt investments (with known use of proceeds)and project finance:Elements

• Company receiving investmentScope 1

emissions of

Corporate debt holdings including:• Bonds• Convertible bonds prior to conversion• Commercial loans

Only applicable when the use of the investment is known, such as for aparticular power plant. Project Finance includes long term financing ofprojects as equity or debt investor (e.g. infrastructure and industrialprojects)

• Accounting approach: Account for proportional scope 1 and scope 2emissions that occur in the reporting year

• Account for total projected lifetime emissions scope 1 and 2emissions of projects separately from scope 3

Section 4.13 – Category 15: Investments

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 112

PwC Taiwan 資誠

15. Investments:Minimum boundaries

Equity investments•Equity investments made by the reporting company using thecompany’s own capital and balance sheet, including:o Equity investments in subsidiaries (or group companies), where the

reporting company has financial control (typically more than 50percent ownership)

o Equity investments in associate companies (or affiliated companies),where the reporting company has significant influence but notfinancial control (typically 20-50 percent ownership)

o Equity investments in joint ventures (Non-incorporated jointventures/ partnerships/operations), where partners have jointfinancial control

•Equity investments made by the reporting company using thecompany’s own capital and balance sheet, where the reporting companyhas neither financial control nor significant influence over the emittingentity (and typically has less than 20 percent ownership)

Section 4.13 – Category 15: Investments

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 113

PwC Taiwan 資誠

15. Investments:Minimum boundaries

Debt investments (with known use of proceeds)•Corporate debt holdings held in the reporting company’s portfolio,including corporate debt instruments (such as bonds or convertiblebonds prior to conversion) or commercial loans, with known use ofproceeds (i.e. where the use of proceeds is identified as going to aparticular project, such as to build a specific power plant)

Project finance•Long-term financing of projects (e.g. infrastructure and industrialprojects) by the reporting company as either an equity investor (sponsor)or debt investor (financier)

Section 4.13 – Category 15: Investments

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 114

PwC Taiwan 資誠

Data collection – Primary. Secondary,proxy

Section 5

PwC Taiwan 資誠

Data selection

• Choose data sources based on Scope 3 assessment goals

• Companies may use 2 types of data:

– Primary data (e.g., supplier data from specific activities within a company’svalue chain)

– Secondary data (e.g., data not from specific activities in a company’s value chain(industry average) such as EEIO database, financial or proxy data

• Data quality is the key consideration

Primary

• Specific

• Enables performance tracking

• Expands supply chain GHG mgmt

• Allows better tracking of targets

• May be costly

• Perhaps difficult to verify source/quality of data

Secondary

• Fills primary data gaps

• Useful for minor activities

• Cheaper and easier

• Identifies hot spots

• May not represent company’s activities

• Does not reflect suppliers’ operational changes

• Limits ability to track progress

Ad

va

nta

ge

sD

isa

dv

an

tag

es

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 116

PwC Taiwan 資誠

Challenges of collecting Scope 3 data

Reliance on value chainpartners to provide data

Lesser degree of influenceover data collection and

management

Lesser degree of knowledgeabout data types, data

sources, and data quality

Broader need for secondarydata

Broader need for assumptionsand modeling

Tier 1 Supplier

Tier 2 Supplier

ReportingCompany

Tier 2 Supplier

Tier 1 Supplier Tier 2 Supplier

Tier 1 Supplier

Tier 2 Supplier

Tier 2 Supplier

Collecting primary data from Tier 1 and/orTier 2 suppliers

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 117

PwC Taiwan 資誠

Guidance for collecting primary dataChallenge: Large Number of Suppliers

• Target most relevant suppliers based on spend and/or anticipated emissions impact

• Target suppliers where the reporting company has a higher degree of influence

Challenge: Supplier has little/no experience with GHG Inventories

• Target suppliers with prior experience developing GHG inventories

• Identify the correct subject matter expert contact at the company

• Explain the business value of investing in GHG accounting and management

• Request data suppliers already have collected, such as energy use data, rather thanemissions data

• Provide clear instructions and guidance with the data request

• Provide training, support, and follow-up

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 118

PwC Taiwan 資誠

Guidance for collecting primary data

Challenge: Lack of Capacity/Resources for Tracking Data

• Make the data request as simple as possible

• Provide a clear list of data required and where to find data (e.g., utility bills)

• Use an automated online data collection system to streamline data entry

• Consider use of a third party database to collect data

• Coordinate GHG data request with other requests

• Follow up with suppliers

• Use a simple, user-friendly, standardized data template/questionnaire

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 119

PwC Taiwan 資誠

Guidance for collecting primary dataChallenge: Lack of Transparency

• Request documentation on methodology and data sources used, inclusions,exclusions, assumptions, etc.

• Minimize errors by requesting activity data (e.g., kWh electricity used, kg of fuelsused) and calculating GHG emissions separately

• Consider third-party assurance

Challenge: Confidentiality Concerns

• Protect suppliers’ confidential/proprietary information (e.g., through nondisclosureagreements, firewalls, etc.)

• Ask suppliers to obtain third-party assurance rather than submitting detailedactivity data to avoid providing confidential information

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 120

PwC Taiwan 資誠

Collecting secondary data

Companies should:

Prioritize databases and publications that are internationally recognized, provided bynational governments, or peer reviewed

Should use the data quality indicators to select data source

Companies may use proxy data to fill data gaps

•Proxy data can be extrapolated, scaled up, or customized to be morerepresentative of a given activity

• Example of proxy data: An emissions factor exists for Ukraine but not for Moldova.A company uses the electricity factor from Ukraine as a proxy for electricity inMoldova

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 121

PwC Taiwan 資誠

Accounting for avoided emissions

•Do not include in scope 3 inventory (report separately)

•Avoid cherry picking (account for both emissions increases and decreases acrossthe company’s entire product portfolio)

- Be transparent about the methodology

•Report methodology and data sources and assumptions used to allocate avoidedemissions

•Refer to the GHG Protocol for Project Accounting at ghgprotocol.org

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 122

PwC Taiwan 資誠

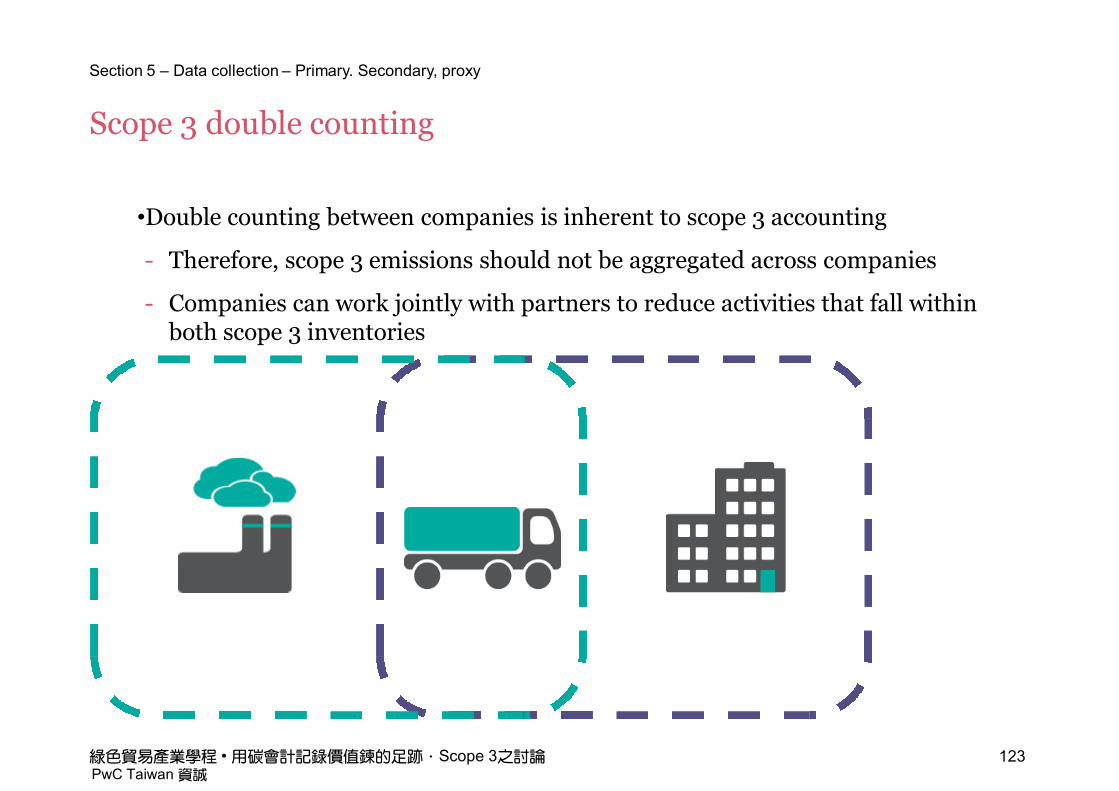

Scope 3 double counting

•Double counting between companies is inherent to scope 3 accounting

- Therefore, scope 3 emissions should not be aggregated across companies

- Companies can work jointly with partners to reduce activities that fall withinboth scope 3 inventories

Section 5 – Data collection – Primary. Secondary, proxy

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 123

PwC Taiwan 資誠

Potential impact of Scope 3 StandardSection 6

PwC Taiwan 資誠

Scope 3 standard – Potential impact

• Represents an increased understanding of what indirect carbonemissions include and how to measure and report them

• Greatly expands what companies will measure, manage, and report beyondtheir own operations

- Represents significant opportunities to influence GHG reductions, reduce cost,and achieve a variety of GHG-related business objectives

- Viewed by many as opportunity to enhance supplier engagement

• A broad range of carbon reduction programs and reporting requirements mayencourage adoption of the new Scope 3 standard, including:

- US Federal (e.g., US EO 13514) and regional carbon reduction schemes

- Ratings efforts by NGOs (e.g., CDP), investors, corporate supply chaininitiatives and other stakeholders

• Over time, customers, investors and other stakeholders may use thisinformation to help them identify less carbon-intensive products

Section 6 – Potential impact of Scope 3 Standard

綠色貿易產業學程 • 用碳會計記錄價值鍊的足跡.Scope 3之討論 125

PwC Taiwan 資誠

Q&A

This publication has been prepared for general guidance on matters of interest only, and doesnot constitute professional advice. You should not act upon the information contained in thispublication without obtaining specific professional advice. No representation or warranty(express or implied) is given as to the accuracy or completeness of the information containedin this publication, and, to the extent permitted by law, PricewaterhouseCoopers Taiwan, itsmembers, employees and agents do not accept or assume any liability, responsibility or dutyof care for any consequences of you or anyone else acting, or refraining to act, in reliance onthe information contained in this publication or for any decision based on it.

© 2012 PricewaterhouseCoopers Taiwan. All rights reserved. In this document, “PwC” refersto PricewaterhouseCoopers Taiwan which is a member firm of PricewaterhouseCoopersInternational Limited, each member firm of which is a separate legal entity.