corporate presentation - indusind · pdf fileenterprise-wide risk management framework for...

TRANSCRIPT

June 2015

Corporate Presentation

hvsv

2

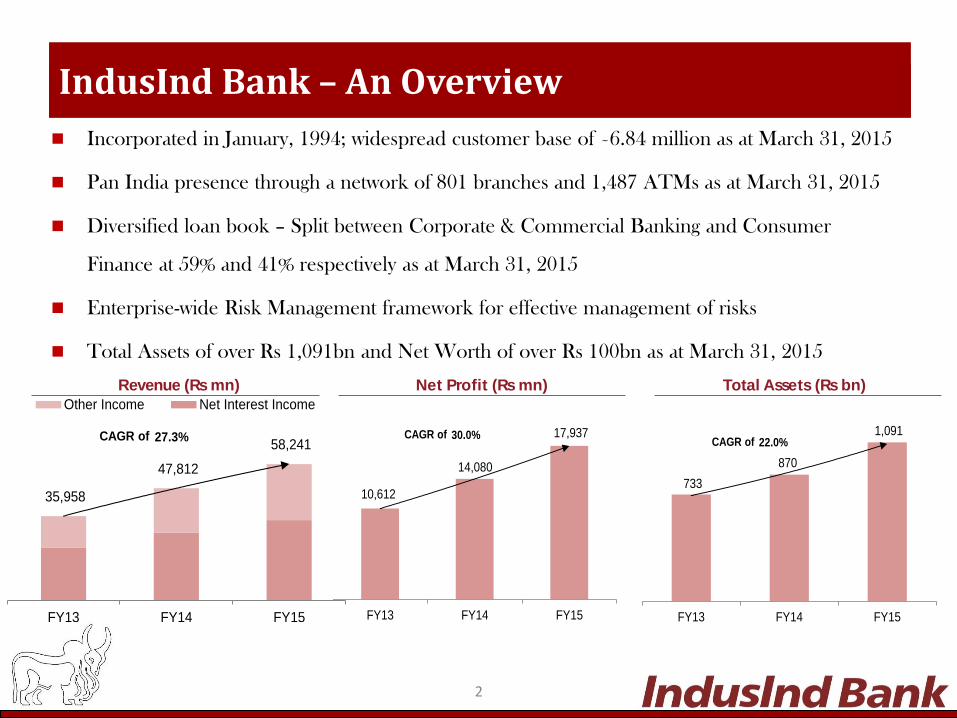

Incorporated in January, 1994; widespread customer base of ~6.84 million as at March 31, 2015

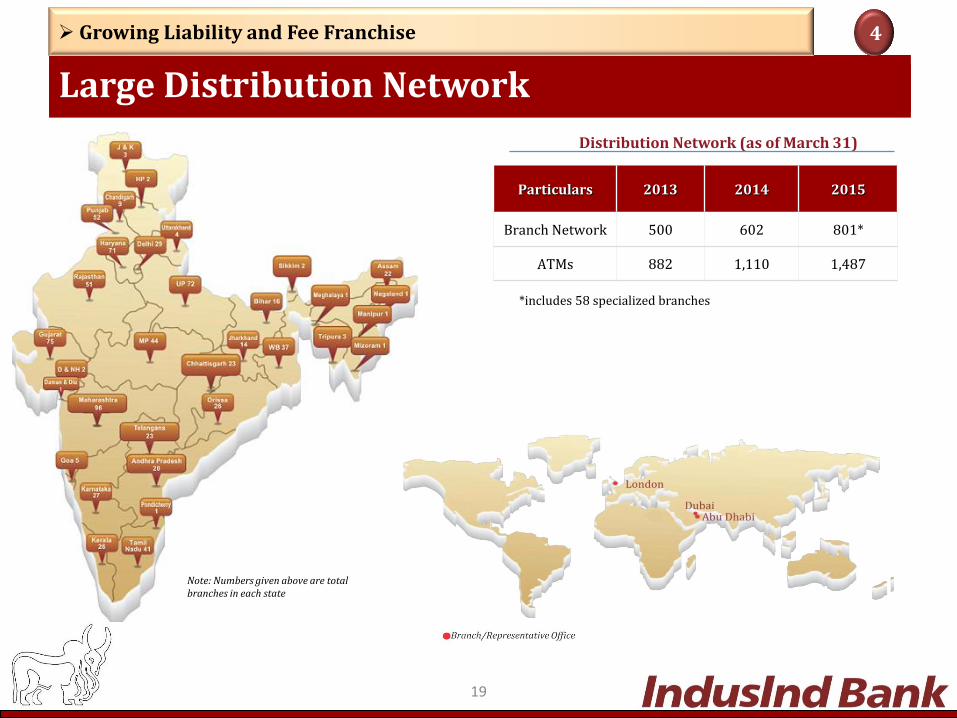

Pan India presence through a network of 801 branches and 1,487 ATMs as at March 31, 2015

Diversified loan book – Split between Corporate & Commercial Banking and Consumer

Finance at 59% and 41% respectively as at March 31, 2015

Enterprise-wide Risk Management framework for effective management of risks

Total Assets of over Rs 1,091bn and Net Worth of over Rs 100bn as at March 31, 2015

IndusInd Bank – An Overview

Revenue (Rs mn) Net Profit (Rs mn) Total Assets (Rs bn)

733

870

1,091

FY13 FY14 FY15

CAGR of 22.0%

10,612

14,080

17,937

FY13 FY14 FY15

CAGR of 30.0%

35,958

47,812

58,241

FY13 FY14 FY15

Other Income Net Interest Income

CAGR of 27.3%

3

Over 20 years of Operating History

New Management team headed by Mr. Romesh Sobti inducted from ABN AMRO Bank NV New Launch/Rollout: Investment Bank, 3rd Party Distribution Platform, Warehouse

Receipt Finance GDR – raised US$ 51.73mn (Jun 2008); QIP – raised Rs 4,803.5 mn (Aug 2009); QIP – raised

Rs 11,727.5 mn (Sept 2010) Tier II Issue – raised Rs 4,200 mn (Mar 2010) Acquired Deutsche Bank’s credit card business Launched Loans Against Property(LAP) and tied-up with HDFC for mortgage origination Innovative product service offering like Choice Money ATM & Check on Cheque Premium Client Segments (Indus Select & Indus Exclusive) introduced Pre-2008

Planning Cycle I: FY09-FY11

Incorporated in 1994; Promoted by a group of Non Resident Indians. Started operations with Rs 1,000 mn capital IPO – raised Rs 1,800 mn (Dec 1997) Tie-ups with exchange houses in Middle East and banks in the United States IndusInd Enterprises & Finance Ltd, an NBFC & one of the promoters of the Bank amalgamated with the Bank Ashok Leyland Finance Ltd, an NBFC merged with the Bank; opened representative office in Dubai Tied up with Aviva Life Insurance and Cholamandalam MS for bancassurance GDR – raised US$ 33.83mn (Mar 2007)

QIP – raised Rs 20,006.4 mn (Dec 2012) New products launched – Prepaid Forex cards,

Tractor financing; Opened – Currency Chests Implemented Finacle 2.0 core banking system Innovations introduced – Instant Redeem, Direct

Connect & Cash On Mobile, My Account My Number

New segments introduced – MFI through Partnership Model; Launched Rural Banking vertical and Govt. Banking vertical

Planning Cycle II: FY12-FY14

ow

4

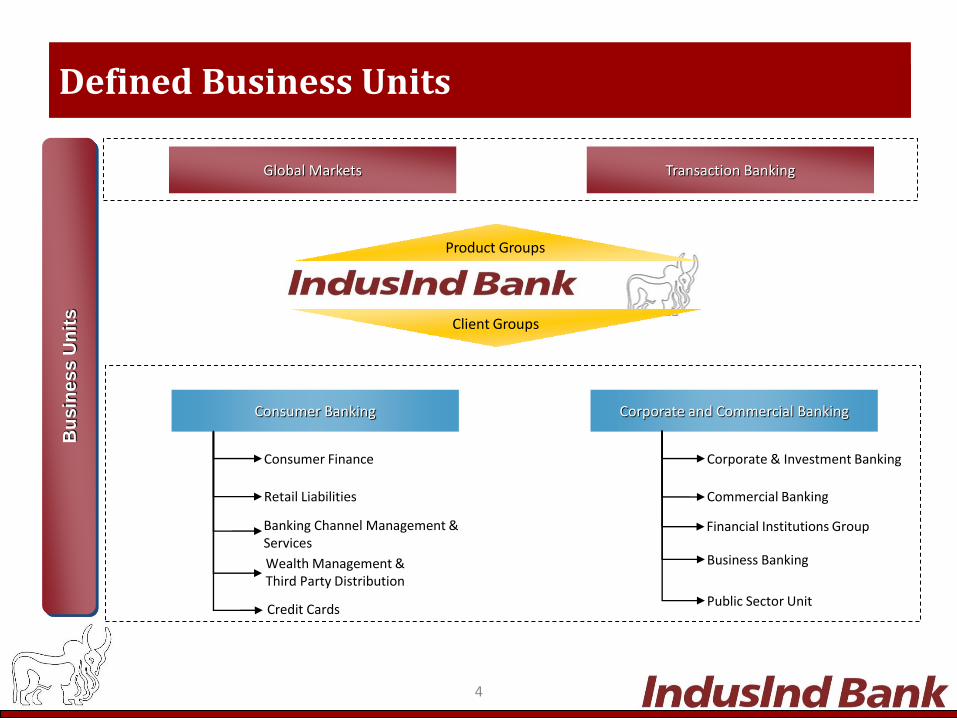

Defined Business Units

Product Groups

Client Groups

Consumer Banking Corporate and Commercial Banking

Consumer Finance

Retail Liabilities

Corporate & Investment Banking

Commercial Banking

Business Banking

Public Sector Unit

Banking Channel Management & Services

Wealth Management & Third Party Distribution

Global Markets Transaction Banking

Bu

sin

ess U

nit

s

Financial Institutions Group

Credit Cards

5

Key Strengths

Universal Banking Offerings

Growing Liability and Fee Franchise

Focused Execution on Risk, Operations and Portfolio

Well Defined Expansion Strategy

History of Technology Refresh and Innovation

Stable Asset Quality

Experienced Management Team

1

2

3

4

5

6

7

6

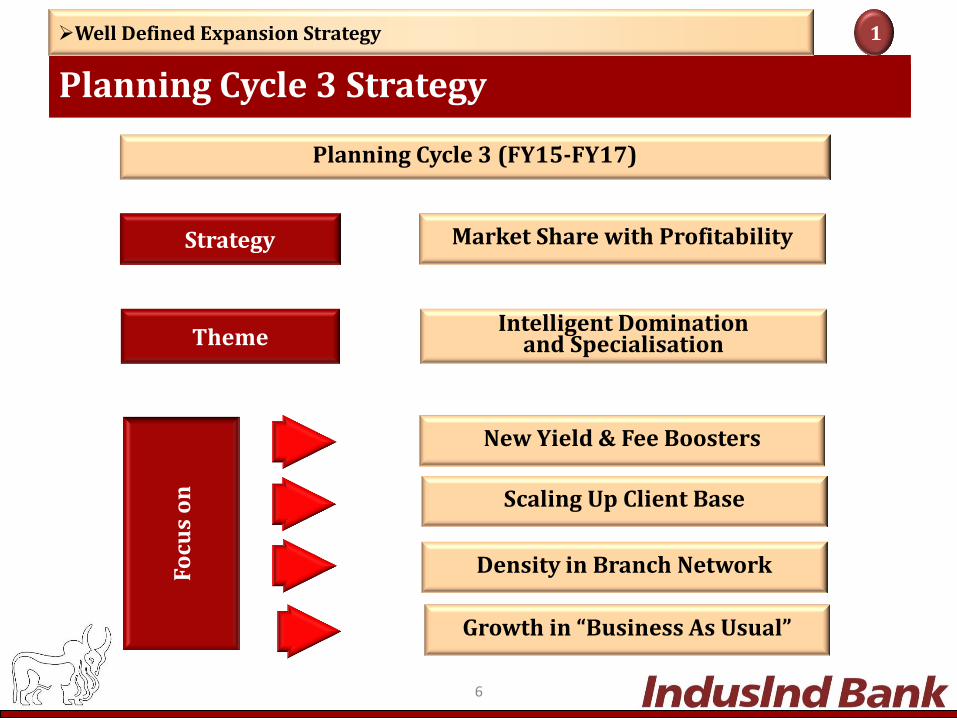

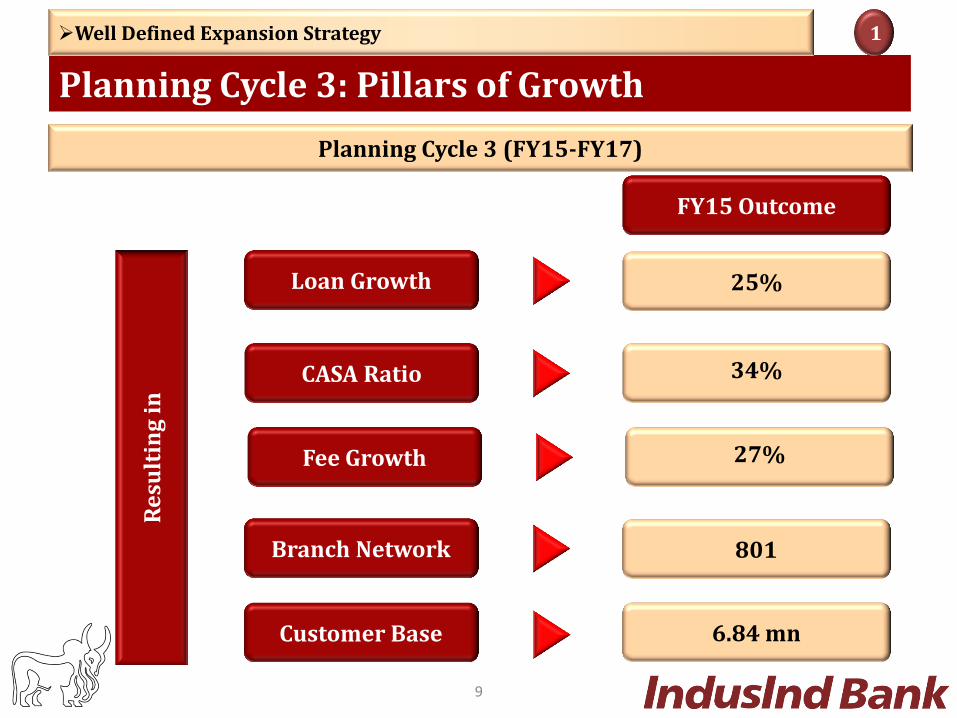

Planning Cycle 3 (FY15-FY17) F

ocu

s o

n

Market Share with Profitability Strategy

Intelligent Domination and Specialisation Theme

New Yield & Fee Boosters

Scaling Up Client Base

Density in Branch Network

Growth in “Business As Usual”

Planning Cycle 3 Strategy

Well Defined Expansion Strategy 1

Planning Cycle 3:Growth Themes

Specialization

in Corporate

Banking

Building a

“High Street”

Brand

Digitization of

Businesses

Rural Banking

Vertical

Focus on

Productivity

Continued

Domination in

Vehicle

Financing

Prioritize

scale in Home

Markets

Well Defined Expansion Strategy 1

7

Tractor Financing Targeting “S” of SME Retail Trade / FX

Retail Assets Ramp Up Real Estate Innovative Customer

Offerings

Front and Back Office

optimization

Full suite of Rural

Products

Retail Assets

Ramp Up

Asset Reconstruction

Planning Cycle 3: Key New Initiatives

Well Defined Expansion Strategy 1

8

CASA Ratio

Branch Network

Customer Base

Loan Growth

34%

801

6.84 mn

25%

Planning Cycle 3 (FY15-FY17) R

esu

ltin

g i

n

Planning Cycle 3: Pillars of Growth

Well Defined Expansion Strategy 1

9

FY15 Outcome

Fee Growth 27%

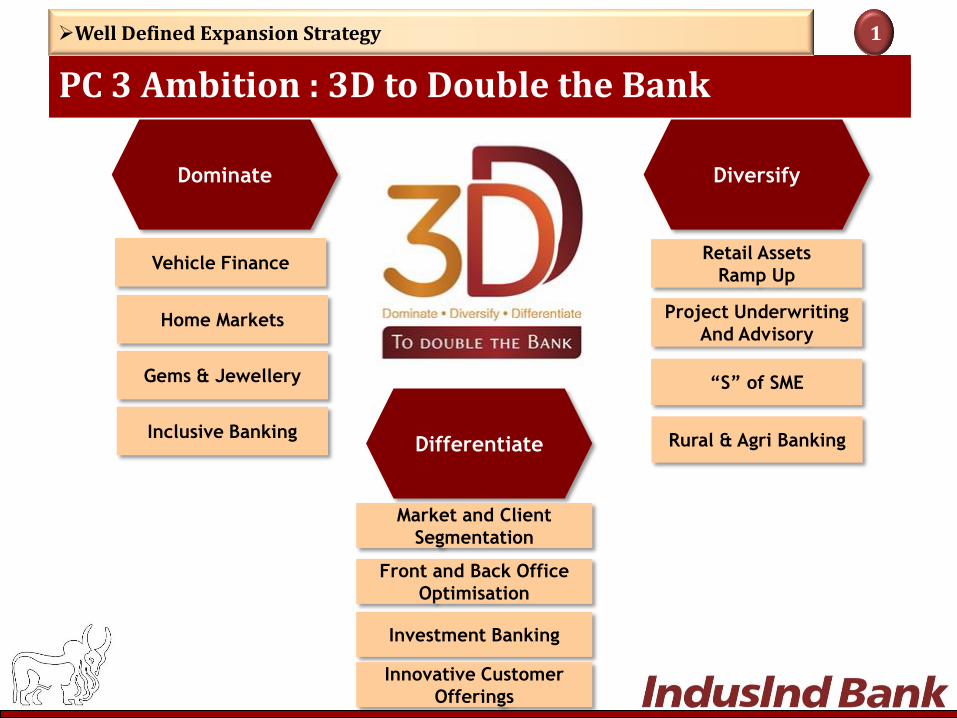

10

Diversify Dominate

Differentiate

Retail Assets

Ramp Up

Project Underwriting

And Advisory

Vehicle Finance

Market and Client

Segmentation

Investment Banking

“S” of SME

Home Markets

Front and Back Office

Optimisation

Gems & Jewellery

Inclusive Banking

Innovative Customer

Offerings

Rural & Agri Banking

PC 3 Ambition : 3D to Double the Bank

Well Defined Expansion Strategy 1

11

Name Designation Occupation / Experience

Mr. R. Seshasayee Part time Non-executive Chairman

Non-Executive Chairman, Infosys; Non-executive Vice Chairman of Ashok Leyland; Past President of the Confederation of Indian Industry

Mr. Romesh Sobti Managing Director & CEO Whole-time Director

Mr. K. Ashok Kini Independent Non-Executive Director

Managing Director (Retired), State Bank of India

Mrs. Kanchan Chitale Independent Non-Executive Director

Practicing Chartered Accountant; MP Chitale & Co

Mr. Vijay Vaid Independent Non-Executive Director

Industrialist and Member of Executive Committee of Automotive Component Manufacturers Association

Mr. T. Anantha Narayanan Additional Independent Non-Executive Director

Executive Director (Retired), Ashok Leyland Ltd.

Mr. Ranbir Singh Butola Additional Independent Non-Executive Director

Ex-Chairman of Indian Oil Corporation Limited

Mr. Y. M. Kale Additional Non-Independent and Non-Executive Director

Past President Institute of Chartered Accountants of India

Board of Directors

Experienced Management Team 2

12

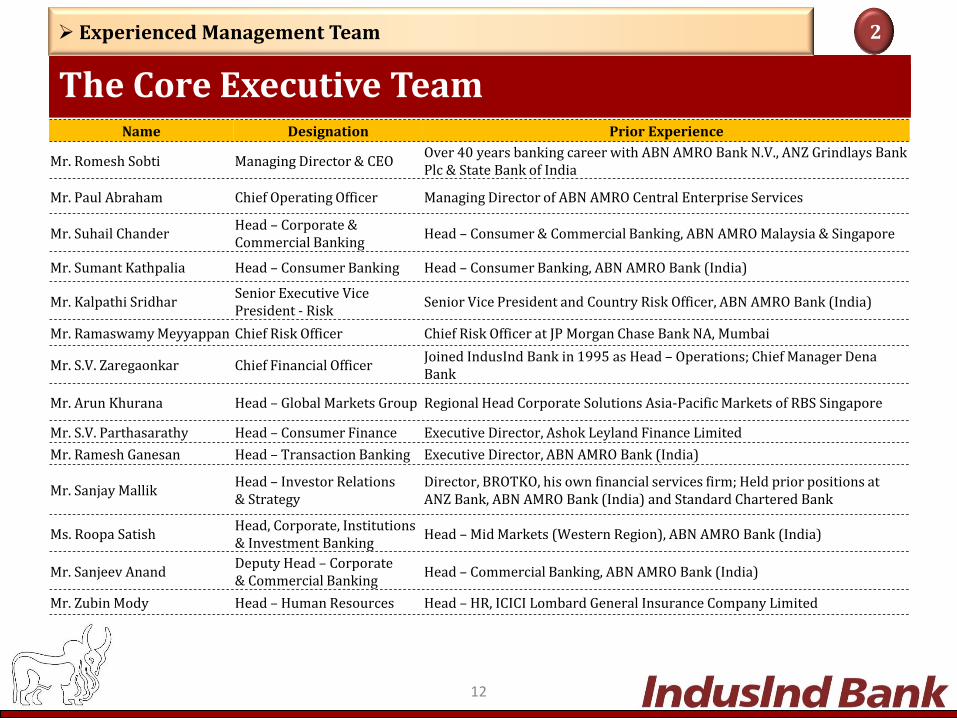

Name Designation Prior Experience

Mr. Romesh Sobti Managing Director & CEO Over 40 years banking career with ABN AMRO Bank N.V., ANZ Grindlays Bank Plc & State Bank of India

Mr. Paul Abraham Chief Operating Officer Managing Director of ABN AMRO Central Enterprise Services

Mr. Suhail Chander Head – Corporate & Commercial Banking

Head – Consumer & Commercial Banking, ABN AMRO Malaysia & Singapore

Mr. Sumant Kathpalia Head – Consumer Banking Head – Consumer Banking, ABN AMRO Bank (India)

Mr. Kalpathi Sridhar Senior Executive Vice President - Risk

Senior Vice President and Country Risk Officer, ABN AMRO Bank (India)

Mr. Ramaswamy Meyyappan Chief Risk Officer Chief Risk Officer at JP Morgan Chase Bank NA, Mumbai

Mr. S.V. Zaregaonkar Chief Financial Officer Joined IndusInd Bank in 1995 as Head – Operations; Chief Manager Dena Bank

Mr. Arun Khurana Head – Global Markets Group Regional Head Corporate Solutions Asia-Pacific Markets of RBS Singapore

Mr. S.V. Parthasarathy Head – Consumer Finance Executive Director, Ashok Leyland Finance Limited

Mr. Ramesh Ganesan Head – Transaction Banking Executive Director, ABN AMRO Bank (India)

Mr. Sanjay Mallik Head – Investor Relations & Strategy

Director, BROTKO, his own financial services firm; Held prior positions at ANZ Bank, ABN AMRO Bank (India) and Standard Chartered Bank

Ms. Roopa Satish Head, Corporate, Institutions & Investment Banking

Head – Mid Markets (Western Region), ABN AMRO Bank (India)

Mr. Sanjeev Anand Deputy Head – Corporate & Commercial Banking

Head – Commercial Banking, ABN AMRO Bank (India)

Mr. Zubin Mody Head – Human Resources Head – HR, ICICI Lombard General Insurance Company Limited

The Core Executive Team

Experienced Management Team 2

13

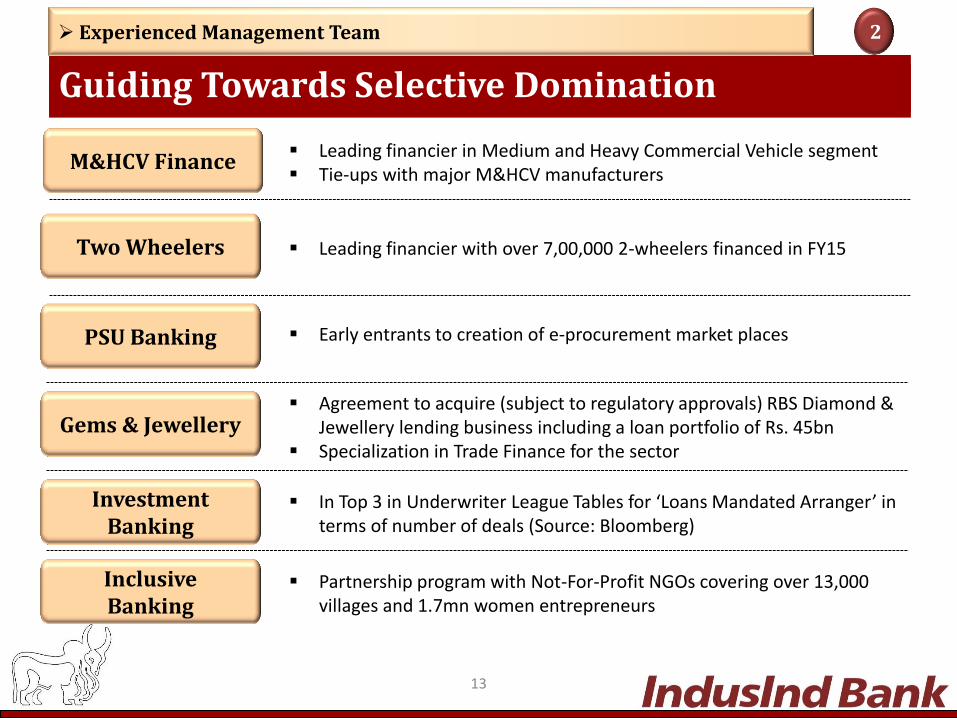

M&HCV Finance

PSU Banking

Gems & Jewellery

Investment Banking

Leading financier in Medium and Heavy Commercial Vehicle segment Tie-ups with major M&HCV manufacturers

Early entrants to creation of e-procurement market places

Agreement to acquire (subject to regulatory approvals) RBS Diamond & Jewellery lending business including a loan portfolio of Rs. 45bn

Specialization in Trade Finance for the sector

In Top 3 in Underwriter League Tables for ‘Loans Mandated Arranger’ in terms of number of deals (Source: Bloomberg)

Inclusive Banking

Partnership program with Not-For-Profit NGOs covering over 13,000 villages and 1.7mn women entrepreneurs

Guiding Towards Selective Domination

Experienced Management Team 2

Two Wheelers Leading financier with over 7,00,000 2-wheelers financed in FY15

14

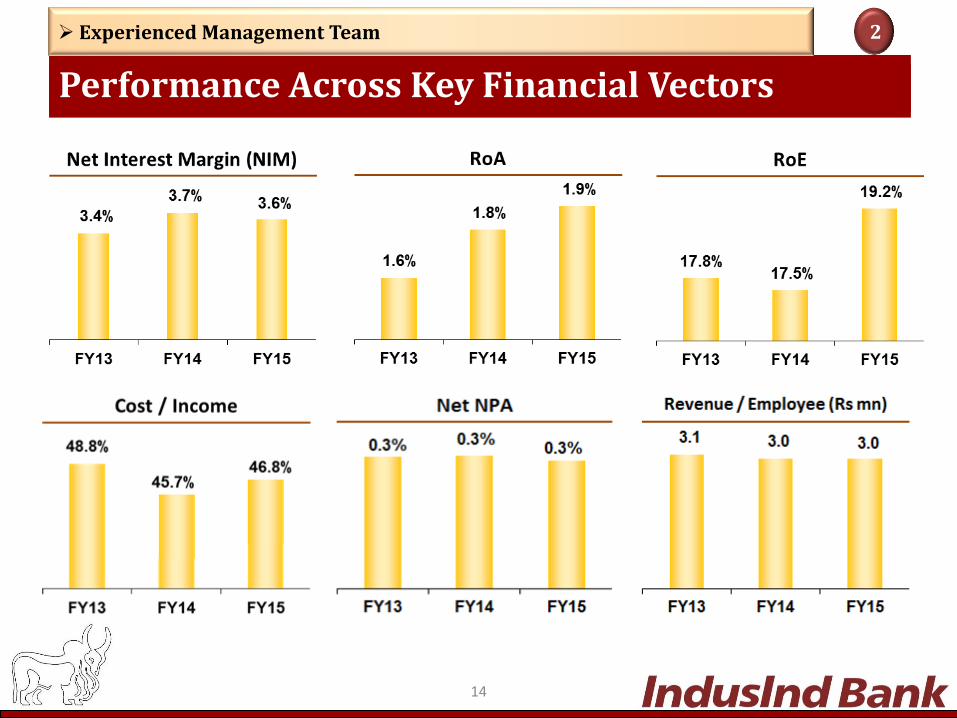

Performance Across Key Financial Vectors

Experienced Management Team 2

15

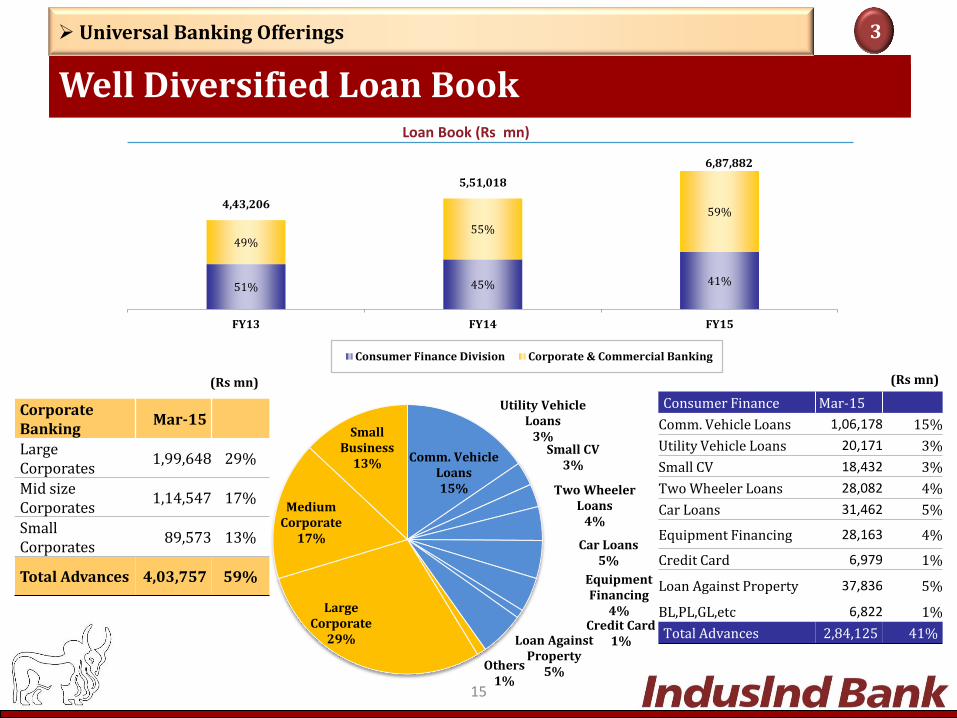

Well Diversified Loan Book

Universal Banking Offerings 3

Corporate Banking

Mar-15

Large Corporates

1,99,648 29%

Mid size Corporates

1,14,547 17%

Small Corporates

89,573 13%

Total Advances 4,03,757 59%

Loan Book (Rs mn)

(Rs mn) (Rs mn)

Consumer Finance Mar-15

Comm. Vehicle Loans 1,06,178 15%

Utility Vehicle Loans 20,171 3%

Small CV 18,432 3%

Two Wheeler Loans 28,082 4%

Car Loans 31,462 5%

Equipment Financing 28,163 4%

Credit Card 6,979 1%

Loan Against Property 37,836 5%

BL,PL,GL,etc 6,822 1%

Total Advances 2,84,125 41%

51% 45% 41%

49% 55%

59% 4,43,206

5,51,018

6,87,882

FY13 FY14 FY15

Consumer Finance Division Corporate & Commercial Banking

Comm. Vehicle Loans 15%

Utility Vehicle Loans

3% Small CV

3%

Two Wheeler Loans

4%

Car Loans 5%

Equipment Financing

4% Credit Card

1% Loan Against Property

5% Others 1%

Large Corporate

29%

Medium Corporate

17%

Small Business

13%

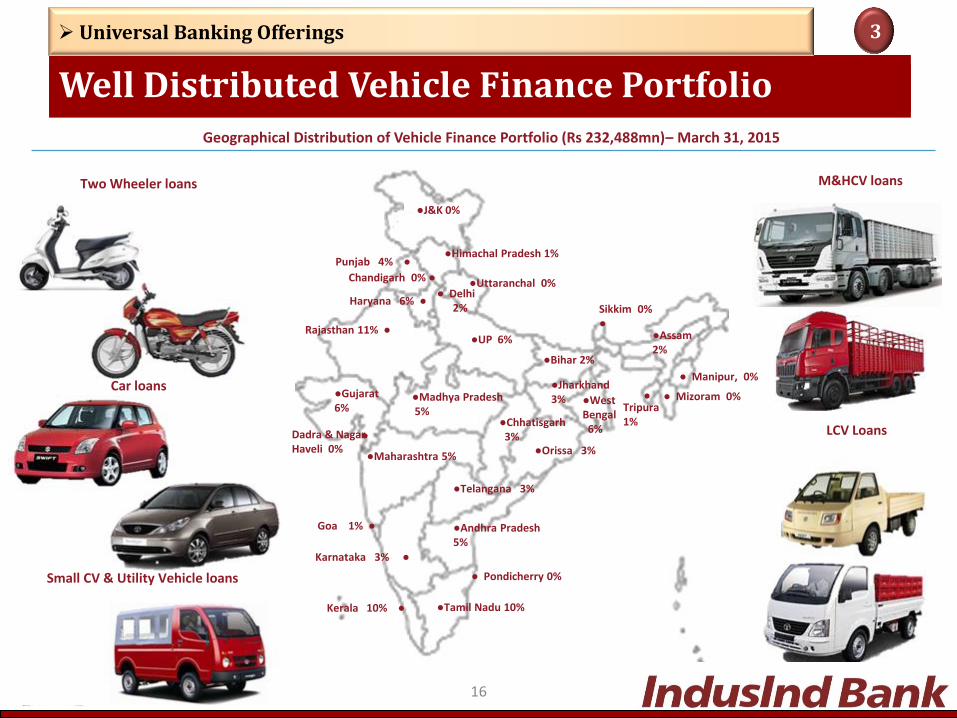

●Andhra Pradesh 5%

●Assam 2%

●Bihar 2%

Chandigarh 0% ●

●Chhatisgarh 3% Dadra & Nagar

Haveli 0%

● Delhi 2%

Goa 1% ●

●Gujarat 6%

Haryana 6% ●

●Himachal Pradesh 1%

●J&K 0%

●Jharkhand 3%

Karnataka 3% ●

Kerala 10% ●

●Madhya Pradesh 5%

●Maharashtra 5%

● Mizoram 0%

●Orissa 3%

● Pondicherry 0%

Punjab 4% ●

Rajasthan 11% ●

●Uttaranchal 0%

●West Bengal 6%

Sikkim 0% ●

●Tamil Nadu 10%

Tripura 1%

●UP 6%

●

●

16

Well Distributed Vehicle Finance Portfolio

Universal Banking Offerings 3

Geographical Distribution of Vehicle Finance Portfolio (Rs 232,488mn)– March 31, 2015

Two Wheeler loans

Car loans

M&HCV loans

Small CV & Utility Vehicle loans

LCV Loans

●Telangana 3%

● Manipur, 0%

17

Distribution of Corporate & Commercial Banking Network Product and Service Offerings

Working Capital Finance

Short Term Finance

Bill Discounting

Export Credit

Term Lending

Buyer’s Credit / Supplier’s Credit

Asset based financing

Lease Rental Discounting

Supply Chain Finance

Warehouse Receipt Finance

Agri Finance

Inclusive Banking

Non Fund Based Services

Value Added Services

Letter of Credit

Bank Guarantees

Forward Contracts / Derivatives

Channel Financing / Associate Financing

Cash Management Services

Corporate Salary Accounts

Liability/ Investment Products

Commodity Finance

Project Finance

Forex / Derivative Desks

Fund Based Services

Comprehensive Corporate and Commercial Banking Offering

Universal Banking Offerings 3

Andhra Pradesh

Assam Bihar

Punjab

Chandigarh

Chhatisgarh

Gujarat

Haryana

Jharkhand

Karnataka

Kerala

Madhya Pradesh

Maharashtra

Orissa

Rajasthan

West Bengal

Tamil Nadu

UP

●

Corporate & Institutions Banking

Public Sector Units

Business Banking Group

Commercial Banking

Goa

Tripura

Nagaland

Meghalaya

Pondicherry

Uttarakhand

HP

Non Fund Based Services

Structured Finance

Debt Syndication

Advisory Services

Investment Banking

Telengana

18

Efficient Distribution and Cross Sell

Universal Banking Offerings 3

19

*includes 58 specialized branches

Particulars 2013 2014 2015

Branch Network 500 602 801*

ATMs 882 1,110 1,487

Distribution Network (as of March 31)

Large Distribution Network

Growing Liability and Fee Franchise 4

Note: Numbers given above are total branches in each state

20

CASA Uptick

Savings Account (SA) Current Account (CA)

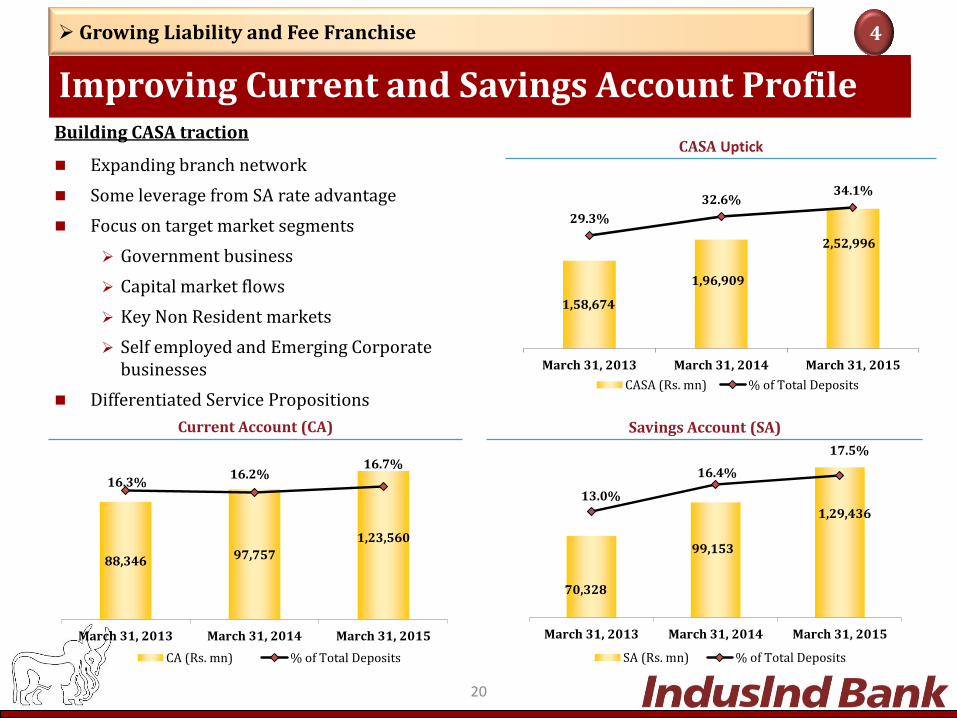

Building CASA traction

Expanding branch network

Some leverage from SA rate advantage

Focus on target market segments

Government business

Capital market flows

Key Non Resident markets

Self employed and Emerging Corporate businesses

Differentiated Service Propositions

Improving Current and Savings Account Profile

Growing Liability and Fee Franchise 4

1,58,674

1,96,909

2,52,996

29.3%

32.6% 34.1%

10%

16%

21%

27%

33%

38%

0

50,000

1,00,000

1,50,000

2,00,000

2,50,000

3,00,000

March 31, 2013 March 31, 2014 March 31, 2015

CASA (Rs. mn) % of Total Deposits

88,346 97,757

1,23,560

16.3% 16.2%

16.7%

5%

7%

9%

11%

13%

15%

17%

0

20,000

40,000

60,000

80,000

1,00,000

March 31, 2013 March 31, 2014 March 31, 2015

CA (Rs. mn) % of Total Deposits

70,328

99,153

1,29,436

13.0%

16.4%

17.5%

0.00%

4.00%

8.00%

12.00%

16.00%

20.00%

1

20,001

40,001

60,001

80,001

1,00,001

1,20,001

1,40,001

March 31, 2013 March 31, 2014 March 31, 2015

SA (Rs. mn) % of Total Deposits

21

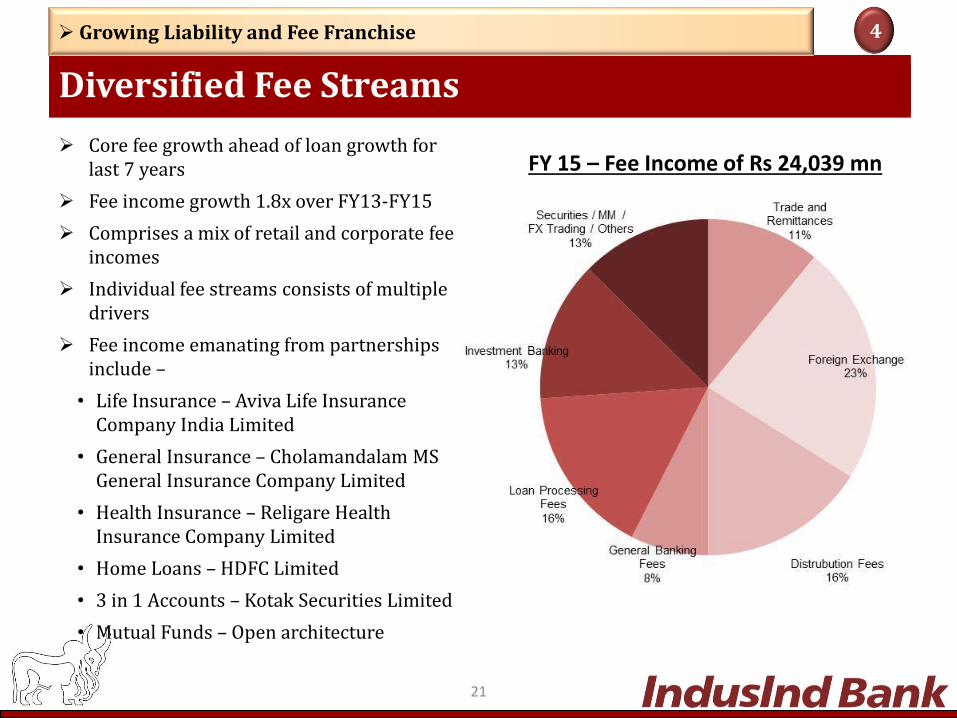

Diversified Fee Streams

Growing Liability and Fee Franchise 4

Core fee growth ahead of loan growth for last 7 years

Fee income growth 1.8x over FY13-FY15

Comprises a mix of retail and corporate fee incomes

Individual fee streams consists of multiple drivers

Fee income emanating from partnerships include –

• Life Insurance – Aviva Life Insurance Company India Limited

• General Insurance – Cholamandalam MS General Insurance Company Limited

• Health Insurance – Religare Health Insurance Company Limited

• Home Loans – HDFC Limited

• 3 in 1 Accounts – Kotak Securities Limited

• Mutual Funds – Open architecture

FY 15 – Fee Income of Rs 24,039 mn

22

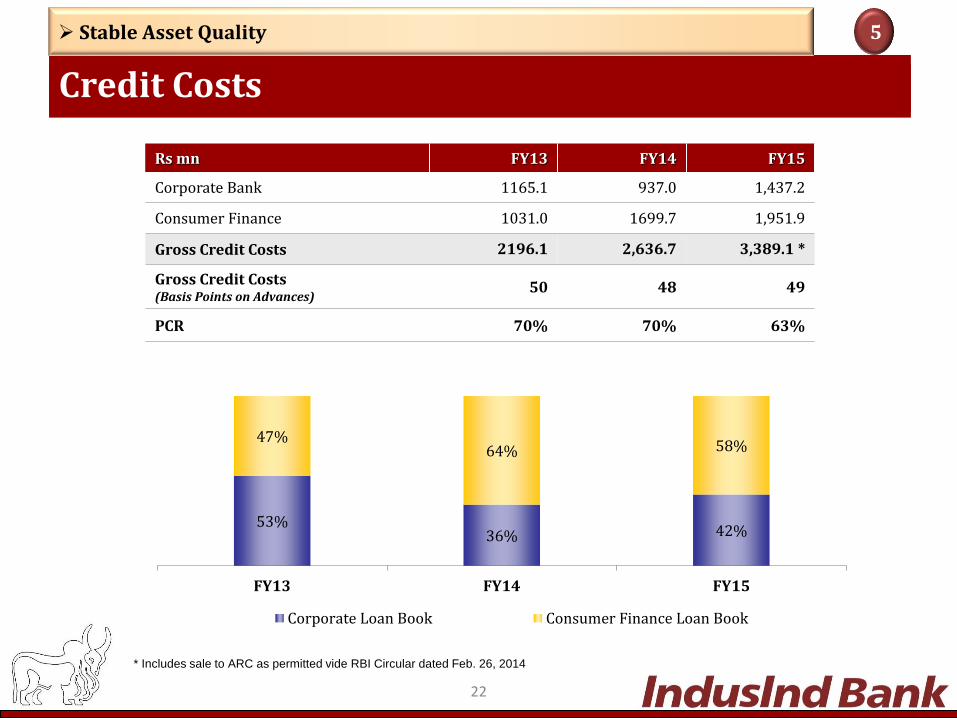

Rs mn FY13 FY14 FY15

Corporate Bank 1165.1 937.0 1,437.2

Consumer Finance 1031.0 1699.7 1,951.9

Gross Credit Costs 2196.1 2,636.7 3,389.1 *

Gross Credit Costs (Basis Points on Advances)

50 48 49

PCR 70% 70% 63%

53% 36% 42%

47% 64% 58%

FY13 FY14 FY15

Corporate Loan Book Consumer Finance Loan Book

Credit Costs

Stable Asset Quality 5

* Includes sale to ARC as permitted vide RBI Circular dated Feb. 26, 2014

23

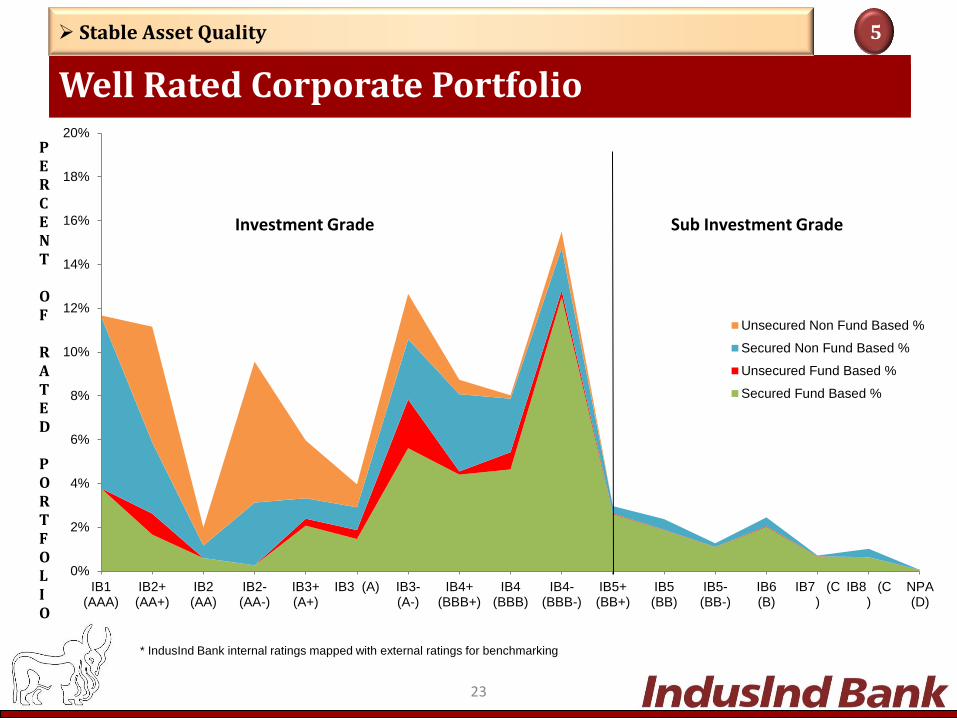

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

IB1(AAA)

IB2+(AA+)

IB2(AA)

IB2-(AA-)

IB3+(A+)

IB3 (A) IB3-(A-)

IB4+(BBB+)

IB4(BBB)

IB4-(BBB-)

IB5+(BB+)

IB5(BB)

IB5-(BB-)

IB6(B)

IB7 (C)

IB8 (C)

NPA(D)

Unsecured Non Fund Based %

Secured Non Fund Based %

Unsecured Fund Based %

Secured Fund Based %

PERCENT OF RATED PORTFOLIO

Investment Grade Sub Investment Grade

Well Rated Corporate Portfolio

Stable Asset Quality 5

* IndusInd Bank internal ratings mapped with external ratings for benchmarking

24

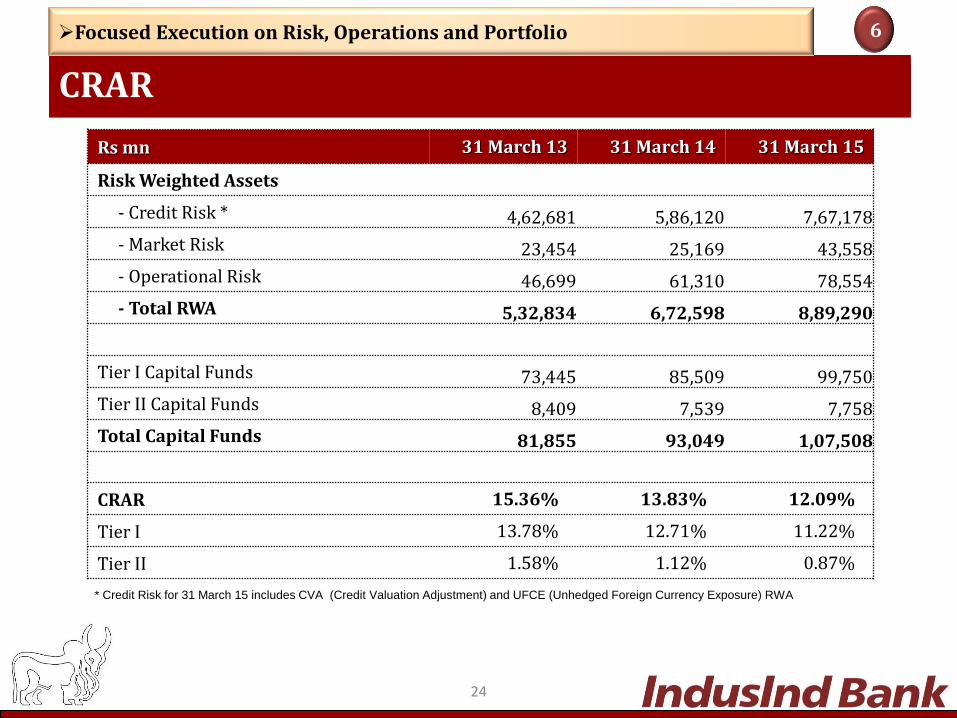

* Credit Risk for 31 March 15 includes CVA (Credit Valuation Adjustment) and UFCE (Unhedged Foreign Currency Exposure) RWA

Rs mn 31 March 13 31 March 14 31 March 15

Risk Weighted Assets

- Credit Risk * 4,62,681 5,86,120 7,67,178

- Market Risk 23,454 25,169 43,558

- Operational Risk 46,699 61,310 78,554

- Total RWA 5,32,834 6,72,598 8,89,290

Tier I Capital Funds 73,445 85,509 99,750

Tier II Capital Funds 8,409 7,539 7,758

Total Capital Funds 81,855 93,049 1,07,508

CRAR 15.36% 13.83% 12.09%

Tier I 13.78% 12.71% 11.22%

Tier II 1.58% 1.12% 0.87%

CRAR

Focused Execution on Risk, Operations and Portfolio 6

25

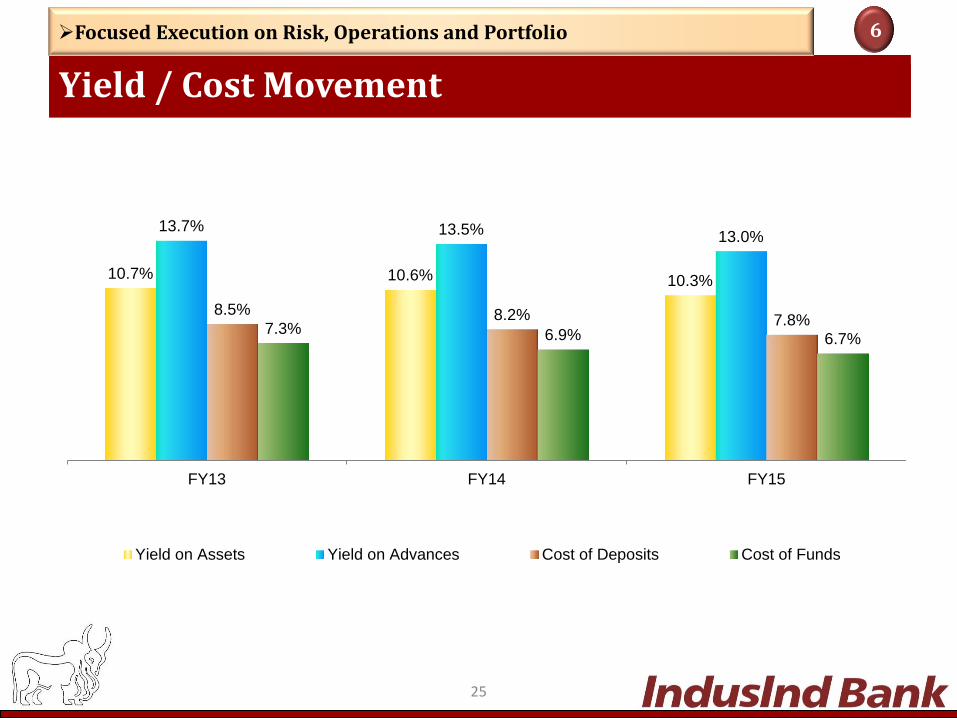

Yield / Cost Movement

Focused Execution on Risk, Operations and Portfolio 6

10.7% 10.6% 10.3%

13.7% 13.5% 13.0%

8.5% 8.2% 7.8% 7.3% 6.9% 6.7%

FY13 FY14 FY15

Yield on Assets Yield on Advances Cost of Deposits Cost of Funds

26

Risk Management Structure in Place

Focused Execution on Risk, Operations and Portfolio 6

Risk Organisation

Credit Approval &

Monitoring

Credit Risk

Management

Market Risk

Management &

ALM

Operational Risk

Management

Financial

Restructuring &

Reconstruction

Credit Quality

Assurance & Loan

Review

Risk and Control

Self Assessment

Key Risk

Indicators (KRIs)

Loss Data

Collection

and

Analysis

Risk Profiling of

branches

Operational Risk

Assessment

Process for New

Products

Risk Events

Reporting

Business

Continuity Plan

Separate group

monitors non

performing loans

Account-wise

monitoring &

recovery

mechanism

Quality check on

entire credit

process

Tracking of credit

rating

Tracking of

portfolio quality

Proactive

Monitoring of Risk

& exposures

Daily valuation

VaR & PV01

Based Limit

Online monitoring

of Risk

sensitivities

Capital Charge

on Market Risk,

CVA Basel III

Liquidity

Standards –

LCR, Liquidity

Ratios

Liquidity Gaps

monitoring – Daily

Duration-based

gap approach

Stress testing for

Liquidity, interest

and foreign

exchange risk

ALM System / Fund

Transfer Pricing

Risk Rating

Models revised

and benchmarked

against external

rating

Basel II & III

implementation

Internal Capital

Adequacy

Assessment

Process (ICAAP)

Stress testing

reinforced

Portfolio

Management &

Credit Quality

Monitoring

reinforced

Credit Risk

values

measurement

reinforced –

PD, LGD, EAD

Credit Appraisal/

Approval process

Credit standards

tightened

Credit Admin

reinforced and

centralised in

hubs

Early warning

signals /

Exceptions

tracking

Enhanced

monitoring

mechanism

27

Standardization

Digitization

Systems

Green Banking

Implemented online solutions for vendor management, invoicing, procurement & travel Image based work flow solution for consumer, trade finance and branch expense

transaction processing

App based sourcing and field investigation launched across India using tabs for Two-Wheeler loans to support faster loan disbursals

Launched multiple technology based initiatives that support client service & engagement

Upgraded key systems in last 3 years (Calypso, Finacle, SAS) Implemented Anti Money Laundering (AML) & Employee Fraud Management (EFM) System Implemented National Information Security architecture

LEED Gold Certification obtained for the first Green Branch launched in Gurgaon Palm Springs Continued investment in green initiatives like virtualization of Servers, Signage timers, Thin

Client Computing, Solar ATMs etc.

Employees Continued focus on cost effective hiring models such as Hire -Train - Deploy Model. Role specific certification programs e.g. IndusPro for RMs, PACE for Vehicle Finance Pan India centralized on-boarding & induction programs for new joiners

Operations - Continuous Process Improvement

Focused Execution on Risk, Operations and Portfolio 6

Centralization

Centralization of processing activities relating to Account reconciliation, Bullion processing, processing of Bank Guarantees, Retail operations

Created independent hubs at Chennai and Mumbai for Trade processing improving turnaround time and business continuity capability

Set-up of Mid Office Group (MOG) for independent and enhanced due diligence & risk analytics

28

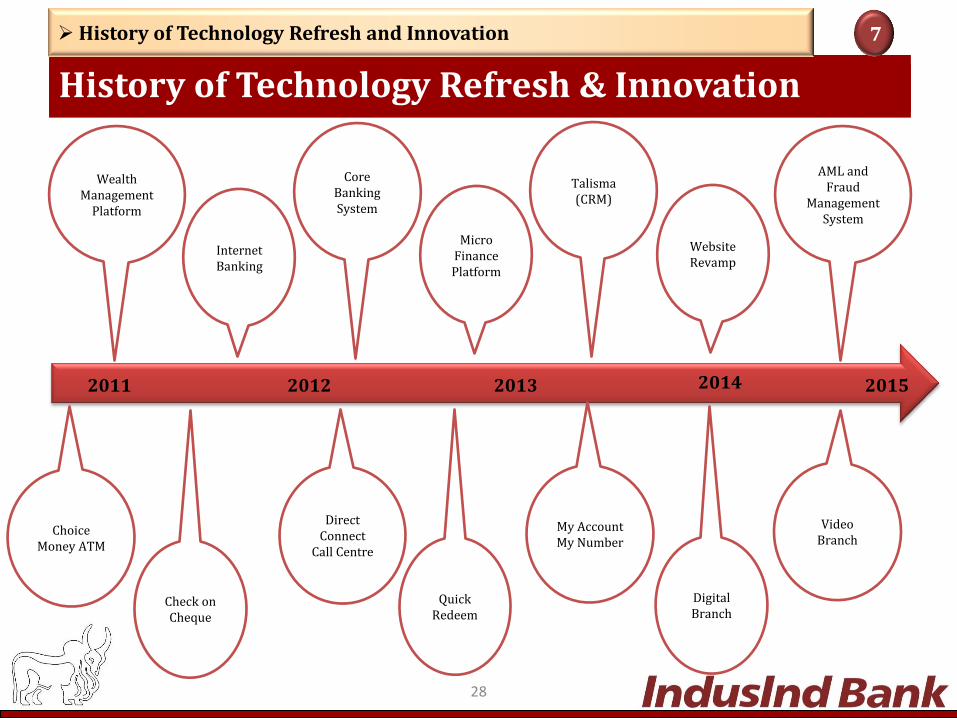

2015 2014 2013 2012 2011

Wealth Management

Platform

Internet Banking

Core Banking System

Micro Finance Platform

Talisma (CRM)

Website Revamp

AML and Fraud

Management System

Choice Money ATM

Check on Cheque

Direct Connect

Call Centre

Quick Redeem

My Account My Number

Digital Branch

Video Branch

History of Technology Refresh & Innovation

History of Technology Refresh and Innovation 7

29

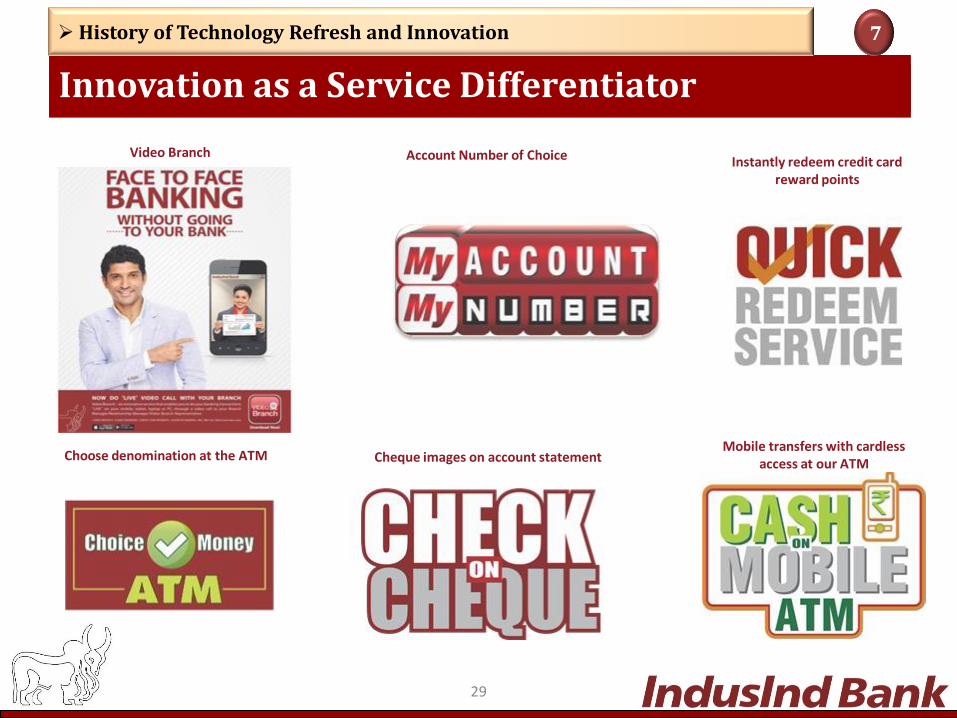

Video Branch

Choose denomination at the ATM

Account Number of Choice Instantly redeem credit card reward points

Cheque images on account statement Mobile transfers with cardless

access at our ATM

Innovation as a Service Differentiator

History of Technology Refresh and Innovation 7

30

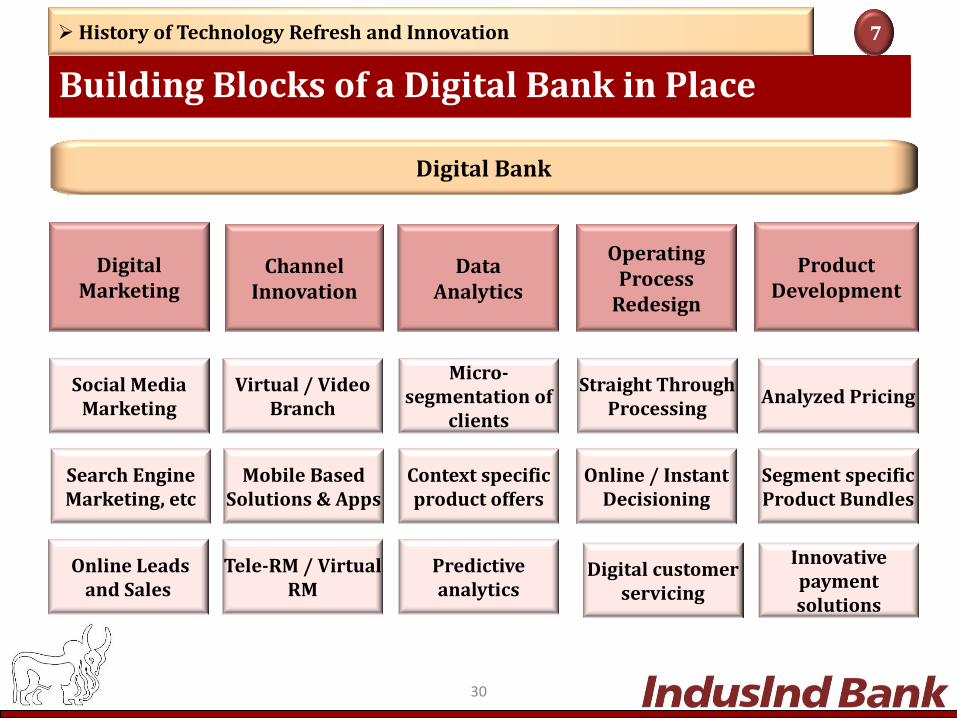

Digital Marketing

Data Analytics

Channel Innovation

Product Development

Operating Process

Redesign

Digital Bank

Social Media Marketing

Search Engine Marketing, etc

Virtual / Video Branch

Mobile Based Solutions & Apps

Micro-segmentation of

clients

Straight Through Processing

Online / Instant Decisioning

Analyzed Pricing

Segment specific Product Bundles

Tele-RM / Virtual RM

Context specific product offers

Predictive analytics

Building Blocks of a Digital Bank in Place

History of Technology Refresh and Innovation 7

Digital customer servicing

Innovative payment solutions

Online Leads and Sales

31

Branch of the Future

History of Technology Refresh and Innovation 7

Financial Performance

33

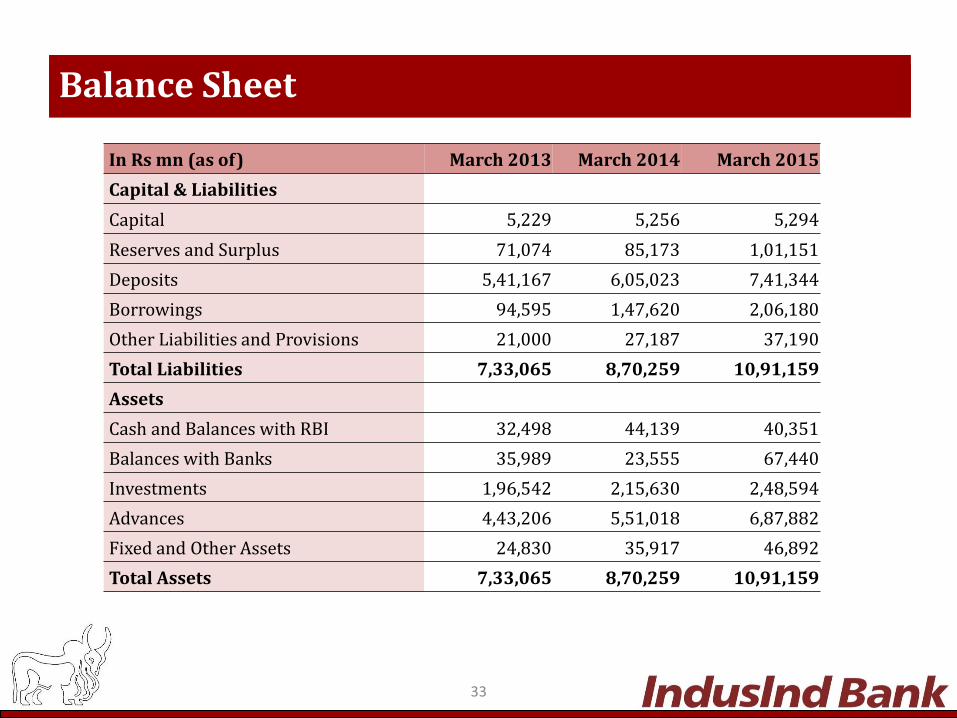

In Rs mn (as of) March 2013 March 2014 March 2015

Capital & Liabilities

Capital 5,229 5,256 5,294

Reserves and Surplus 71,074 85,173 1,01,151

Deposits 5,41,167 6,05,023 7,41,344

Borrowings 94,595 1,47,620 2,06,180

Other Liabilities and Provisions 21,000 27,187 37,190

Total Liabilities 7,33,065 8,70,259 10,91,159

Assets

Cash and Balances with RBI 32,498 44,139 40,351

Balances with Banks 35,989 23,555 67,440

Investments 1,96,542 2,15,630 2,48,594

Advances 4,43,206 5,51,018 6,87,882

Fixed and Other Assets 24,830 35,917 46,892

Total Assets 7,33,065 8,70,259 10,91,159

Balance Sheet

34

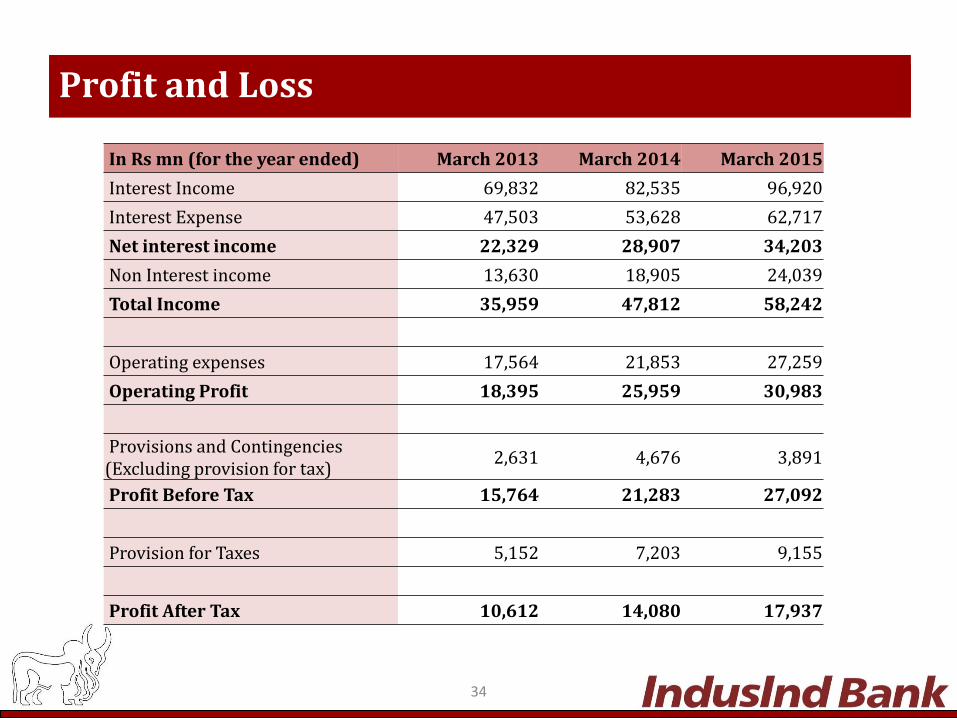

In Rs mn (for the year ended) March 2013 March 2014 March 2015

Interest Income 69,832 82,535 96,920

Interest Expense 47,503 53,628 62,717

Net interest income 22,329 28,907 34,203

Non Interest income 13,630 18,905 24,039

Total Income 35,959 47,812 58,242

Operating expenses 17,564 21,853 27,259

Operating Profit 18,395 25,959 30,983

Provisions and Contingencies (Excluding provision for tax)

2,631 4,676 3,891

Profit Before Tax 15,764 21,283 27,092

Provision for Taxes 5,152 7,203 9,155

Profit After Tax 10,612 14,080 17,937

Profit and Loss

Additional Information

36

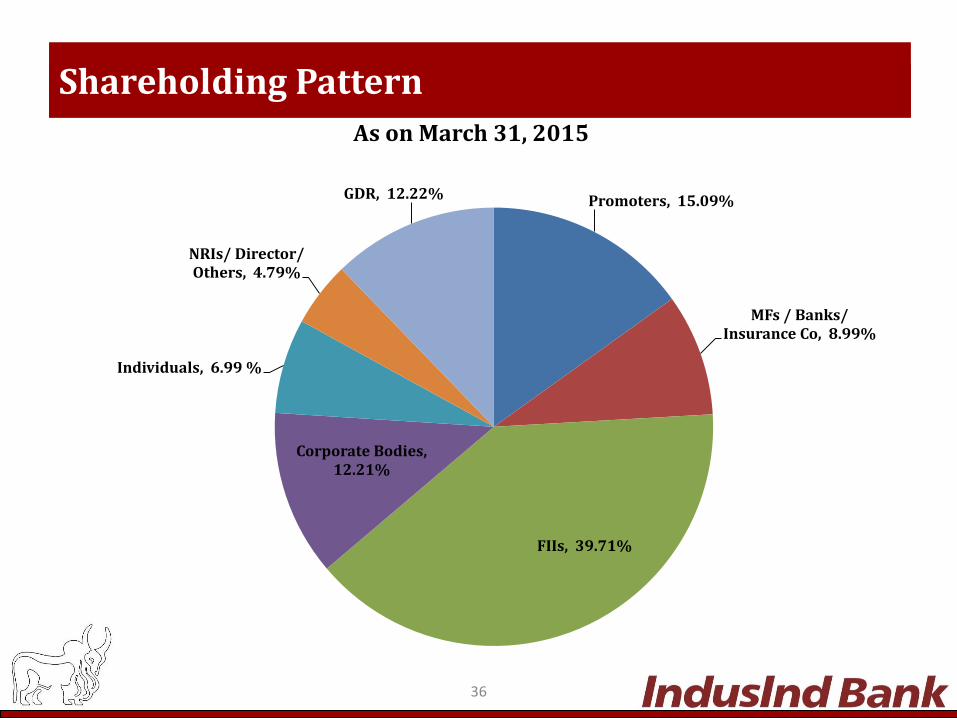

Shareholding Pattern

As on March 31, 2015

Promoters, 15.09%

MFs / Banks/ Insurance Co, 8.99%

FIIs, 39.71%

Corporate Bodies, 12.21%

Individuals, 6.99 %

NRIs/ Director/ Others, 4.79%

GDR, 12.22%

37

Ratings

ICRA AA+ for Lower Tier II subordinate debt program by ICRA

ICRA AA for Upper Tier II bond program by ICRA

CRISIL A1+ for certificate of deposit program by CRISIL

CARE AA+ for Lower Tier II subordinate debt program by CARE

IND A1+ for Short Term Debt Instruments by India Ratings and Research

IND AA+ for Lower Tier II subordinate debt program by India Ratings and Research

IND AA for Upper Tier II bond program by India Ratings and Research

IND AA+ for Senior unsecured bonds program by India Ratings and Research

Awards and Accolades

Business Standard 2015

“Banker of the Year” Mr. Romesh Sobti

Business World 2015

Best Mid-size Bank Fastest Growing Mid- size

Bank

BrandZ Top 50 WPP Plc & Milward Brown

2015

Top 50 Most Valuable Indian Brands

38

Awards and Accolades

Dun & Bradstreet - Polaris Financial – 2013

Best Private Sector Bank - Priority Sector Lending

Asia Trailblazer Awards 2015

Excellence in Service Innovation

BFSI Leadership Summit 2015

Best Branchless Banking

39

40

Disclaimer This presentation has been prepared by IndusInd Bank Limited (the “Bank”) solely for information purposes, without regard to any specific objectives, financial situations or informational needs of any particular person. All information contained has been prepared solely by the Bank. No information contained herein has been independently verified by anyone else. This presentation may not be copied, distributed, redistributed or disseminated, directly or indirectly, in any manner. This presentation does not constitute or form a part of and should not be construed directly or indirectly, as an offer or invitation, to purchase or subscribe for any securities of the Bank by any person in any jurisdiction, including India and the United States. No part of it should form the basis of or be relied upon in connection with any investment decision or any contract or commitment to purchase or subscribe for any securities. Any person placing reliance on the information contained in this presentation or any other communication by the Bank does so at his or her own risk and the Bank shall not be liable for any loss or damage however arising from this presentation, or its contents or otherwise therewith or caused pursuant to any act or omission based on or in reliance upon the information contained herein. No representation or warranty, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information, estimates, projections or opinions contained in this presentation. Such information and opinions are in all events not current after the date of this presentation. Further, past performance is not necessarily indicative of future results. This presentation is not a complete description of the Bank. This presentation may contain statements that constitute forward-looking statements. All forward looking statements are subject to risks, uncertainties and assumptions that could cause actual results to differ materially from those contemplated by the relevant forward-looking statement. Important factors that could cause actual results to differ materially include, among others, future changes or developments in the Bank’s business, its competitive environment and political, economic, legal and social conditions. Given these risks, uncertainties and other factors, viewers of this presentation are cautioned not to place undue reliance on these forward-looking statements. The Bank disclaims any obligation to update these forward-looking statements to reflect future events or developments. Except as otherwise noted, all of the information contained herein is indicative and is based on management information, current plans and estimates in the form as it has been disclosed in this presentation and has not been independently verified. Any opinion, estimate or projection herein constitutes a judgment as of the date of this presentation and there can be no assurance that future results or events will be consistent with any such opinion, estimate or projection. The Bank may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such change or changes. The accuracy of this presentation is not guaranteed, it may be incomplete or condensed and it may not contain all material information concerning the Bank. This presentation is not an offering circular, offer letter, offering document, invitation or solicitation of an offer, a prospectus or an advertisement as defined under the Companies Act, 2013, together with the rules and regulations made thereunder, each as amended, the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended, or any other applicable law in India. Figures for the previous period / year have been regrouped wherever necessary to conform to the current period’s / year’s presentation. Total in some

columns / rows may not agree due to rounding off. Note: All financial numbers in the presentation are from Audited Financials or based on Management estimates.

Thank You