董監事暨重要職員責任保險對企業信用評等之...

TRANSCRIPT

75

臺大管理論叢 2017/12第 27 卷第 4 期 75-104DOI:10.6226/NTUMR.2017.APR.A102-067

董監事暨重要職員責任保險對企業信用評等之影響

The Effect of Directors’ and Officers’ Liability Insurance on Firms’ Credit Ratings

摘 要

本文旨在以債權人的觀點,針對 2008年至 2011年在臺灣證券交易所及櫃檯買賣中心交易之上市(櫃)公司為研究樣本,探討上市(櫃)公司購買董監事暨重要職員責任保險(簡稱 D&O保險)是否會影響債權人對企業信用風險的認知,而債權人對企業信用風險的認知係以信用評量機構發布的評等來衡量。整體而言,實證結果穩健地支持相對於未購買 D&O保險的公司,有購買 D&O保險的公司,其信用評等較佳;然而進一步針對有購買D&O保險的公司,探討其投保金額與信用評等之關聯性時,實證結果則發現,當公司依自身之特質及所面臨的風險投保適度的金額(即正常投保金額),將可獲得較佳的信用評等;但當公司投保金額超過公司自身特質及風險所需之保險金額(即超額投保金額)愈大時,反而使債權人認為董監事與管理階層的道德風險會增加,因而導致給予較差的信用評等。

【關鍵字】 董監事暨重要職員責任保險、信用評等、投保金額

Abstract

This paper explores the effect of directors’ and officers’ liability insurance (D&O insurance hereafter) on the firms’ credit ratings, which serve as a proxy for firms’ credit risk perceived by the creditors. We construct a sample from the firms listed on both the Taiwan Stock Exchange (TWSE) and GreTai Securities Market (GTSM) from 2008 to 2011. The evidence shows that firms with D&O insurance have better credit ratings than those without D&O insurance. Further results show that D&O insurance coverage also impacts firms’ credit ratings. If the firm purchases the appropriate (normal) D&O insurance coverage that suits the firm’s specific characteristics and risk, it tends to have a superior credit rating. However, if the firm purchases excess (abnormal) D&O insurance coverage that is more than the firm’s needs, it tends to have an inferior credit rating, a fact that likely stems from opportunistic behaviors from the directors and managers at the expense of creditors.【Keywords】directors’ and officers’ liability insurance, credit rating, insurance coverage

廖秀梅 /銘傳大學會計學系副教授Hsiu-Mei Liao, Associate Professor, Department of Accounting, Ming Chuan University

湯麗芬 /致理科技大學會計資訊系副教授Li-Fen Tang, Associate Professor, Department of Accounting Information, Chihlee University of

Technology

李建然 /國立臺北大學會計學系教授Jan-Zan Lee, Professor, Department of Accountancy, National Taipei UniversityReceived, 2013/10, Final revision received 2015/4

董監事暨重要職員責任保險對企業信用評等之影響

76

壹、前言

近年來臺灣證券主管機關為了提升對上市(櫃)公司外部投資人權益的保障,鼓

勵上市(櫃)公司購買董監事及重要職員責任保險(Directors’ and Officers’ Liability Insurance,以下簡稱 D&O保險)1。雖然 D&O保險對董監事及重要職員因疏忽而造成外部投資人損失的補償提供若干的保障,但同時也可能因將董監事及重要職員部分

風險移轉給保險公司,產生道德危機 (Moral Hazard) 的風險,進而提高外部投資人的風險。由於債務融資為企業重要籌措資金管道之一,債權人亦是重要的外部投資人之

一,信用評量機構主要針對企業信用風險及債務履約能力進行評估,其所發佈企業信

用評等高低除了會影響債務融資的可能性與資金成本外,其對股票市場的影響亦不可

忽視 2,故以信用評量機構角度衡量債權人對企業信用風險的認知有其重要性。因此,

本文以債權人的觀點,探討上市(櫃)公司投保 D&O保險是否會影響債權人對企業信用風險的認知,而債權人對企業信用風險的認知係以信用評量機構的評等來衡量。

公司治理機制的主要目的之一為提升企業經營績效與公司價值,並保障各利害關

係人之權益,而董監事及管理階層則是公司治理成效是否發揮的主要關鍵因素。企業

購買 D&O保險可有效降低董監事及管理階層所面對的法律責任及訴訟風險,然而,過去文獻對於 D&O保險對公司治理成效的影響則有正、反兩面不同的論述;前者認為購買 D&O保險的公司除了增加保險公司對投保公司在公司治理及經營情況上之間接監督外,也會促進董監事之間相互監督,並且較能吸引優秀或具聲譽的獨立董事及

管理階層參與經營,進而強化公司治理的機制,增加各利害關係人權益的保障 (Bhagat, Brickley, and Coles, 1987; Priest, 1987; Holderness, 1990; Forker, 1992; Daniels and Hutton, 1993; Brook and Rao, 1994; Hampel, 1998)。而後者則認為 D&O保險將潛在部分訴訟風險移轉給保險公司,反而會使董監事與管理階層比較不會全力投入在公司經

營及監督,增加道德危機的風險,進而降低公司治理的成效,損害各利害關係人的權

益 (Gutierrez, 2003; Baker and Griffith, 2007)。雖然歐美國家實施 D&O保險制度行之有年,但過去因 D&O保險並非公開揭露

之資訊(如美國),使得相關研究並不多見,且多集中在有要求公司揭露 D&O保險資訊的國家為主(如英國及加拿大)。例如,有部分研究以加拿大公司為研究對象,

探討 D&O保險金額與 IPO長期股票績效、盈餘穩健性或自願揭露品質之關聯性

1 臺灣目前雖未強制要求公司一定要購買 D&O保險,但於 2003年修訂「上市上櫃公司治理實務守則」中,鼓勵公司為董監事及重要職員購買責任保險。

2 例如:國際信用評量機構穆迪 (Moody’s) 2012年將夏普 (Sharp) 短期債券調降至最低級,立刻造成夏普公司股價重挫;而標準普爾 (Standard & Poor’s) 2011年 8月 5日將美國主權信用評等由最高級 AAA降一級至 AA+,更造成全球股市重挫,並掀起全球金融風暴。

臺大管理論叢 第27卷第4期

77

(Chalmers, Dann, and Harford, 2002; Chung and Wynn, 2008; Wynn, 2008),研究結果發現 D&O保險金額與上市後三年之股票報酬呈顯著負相關 (Chalmers et al., 2002);與公司盈餘的穩健性亦呈顯著負相關 (Chung and Wynn, 2008),而且超額之 D&O保險,會造成公司比較不願意揭露傳遞壞消息之盈餘預測 (Wynn, 2008)。換言之,這些研究的實證結果似乎意味著 D&O保險雖然降低了董監事及管理階層之法律責任,卻可能提高董監事及管理階層投機的誘因,因此可能不利於公司的長期股票績效與盈餘品質。

債權人是企業重要的利害關係人之一,然而,尚未有文獻探討公司購買 D&O保險及其投保金額是否會影響債權人對企業信用風險的認知。由於信用評量機構為一個

專業債信評量者,且發佈債信評等會影響企業的融資成本,因此本文係透過檢視公司

購買 D&O保險及其投保金額與信用評等的關聯性,藉以瞭解 D&O保險對債權人企業信用風險認知的影響。過去文獻發現,公司治理機制之良窳會影響企業信用風險的

評等(Ashbaugh-Skaife, Collins, and LaFond, 2006; Alali, Anandarajan, and Jiang, 2012; 林宛瑩、許崇源、戚務君與陳宜伶,2009)。然而,誠如前述,D&O保險對於公司治理的成效可能有正反兩面的影響。換言之,如果公司購買 D&O保險可以強化董事會功能,將有效提升經營績效與公司價值,減少違約的機率,而且還有保險公司的賠

償作為保障,故可增加債權人權益的保障,則公司購買 D&O保險將有助於信用評量機構給予較佳的信用評等。但相反地,若購買 D&O保險會增加董監事與管理階層道德危機的風險,將提高了管理階層傷害債權人權益的可能性 3 (Jensen and Meckling, 1976),則公司購買 D&O保險將導致信用評量機構給予較差的信用評等。因此,為了釐清購買 D&O保險對於公司信用評等所造成的影響,本文以 2008年

至 2011年臺灣上市(櫃)公司為研究樣本,探討公司購買 D&O保險是否會影響債權人對企業信用風險的認知。整體而言,實證結果支持相對於未購買D&O保險的公司,有購買D&O保險的公司,其信用評等較佳;然而進一步針對有購買D&O保險的公司,探討其投保金額與信用評等之關聯性時,實證結果則發現,當公司依自身之特質及所

面臨的風險投保適度的金額(即正常投保金額),將可獲得較佳的信用評等;但當公

司投保金額超過公司自身特質及風險所需之保險金額(即超額投保金額)愈大時,反

而使債權人認為董監事與管理階層的道德風險會增加,因而導致給予較差的信用評等。

本文研究結果有下列研究貢獻,首先,由於許多國家 D&O保險並非公開揭露之資訊,使得相關研究並不充分,而且目前少有文獻從債權人的角度,探討 D&O保險,因此,本文為探討 D&O保險對債權人企業信用風險認知影響的首篇研究,本文研究

3 例如:管理階層為了自利行為,投資高風險的計畫或買回庫藏股等,而影響企業未來現金流量,使債權人承受較不對等風險,損害債權人權益(林宛瑩等,2009)。

董監事暨重要職員責任保險對企業信用評等之影響

78

結果除了可彌補 D&O保險相關文獻的不足外,並提供相關信用評等文獻的增額貢獻。其次,過去文獻對於 D&O保險對公司治理成效的影響並無定論 (Bhagat et al., 1987; Priest, 1987; Holderness, 1990; Forker, 1992; Daniels and Hutton, 1993; Brook and Rao, 1994; Hampel, 1998; Gutierrez, 2003; Baker and Griffith, 2007; Chalmers et al., 2002; Chung and Wynn, 2008; Wynn, 2008),本文之結果隱含著探討 D&O保險對公司治理成效的影響不能僅從有無投保 D&O保險著眼,應進一步探討 D&O保險金額適當性對公司治理成效的影響。最後,本文結果亦可提供證券主管機關作為推行 D&O保險之參考依據,以及能提供外部債權人評估 D&O保險及其金額對信用評等影響之參考。本文後續結構說明如下:第貳節闡述研究假說建立之相關文獻;第參節為研究設

計說明;第肆節為彙整實證結果與分析;第伍節則為結論。

貳、研究假說之建立

公司治理機制的主要目的之一為提升企業經營績效與公司價值,並保障各利害關

係人的權益。過去文獻發現公司治理機制之良窳會影響企業信用評等(Ashbaugh-Skaife et al., 2006; 林宛瑩等,2009;Alali et al., 2012),而董監事及管理階層則是公司治理成效是否發揮的關鍵因素。企業購買 D&O保險可有效降低董監事及管理階層所面對的法律責任,然而卻也可能誘發董監事及管理階層的道德危機,由於過去文獻

對於 D&O保險對公司治理成效的影響有正、反兩面不同的看法,因此,D&O保險對企業信用風險的影響亦有下列兩種不同看法。

首先,由於 D&O保險會降低董監事及管理階層部分的法律風險,導致董監事及管理階層增加道德危機的風險 (Gutierrez, 2003; Baker and Griffith, 2007),進而提高管理階層傷害債權人權益的風險。過去文獻發現,D&O保險因董監事及管理階層產生道德危機而對公司治理有負面影響的實證證據,例如:公司治理差的公司,有較多空

間從事投機行為,較可能去購買 D&O保險 (Boyer and Delvaux-Derome, 2002),而且投保 D&O保險額度較高 (Core, 2000);Chalmers et al. (2002) 亦發現 IPO股票被高估的公司比較可能購買高額的 D&O保險,而且 D&O保險金額與三年後的 IPO股票報酬呈顯著負相關;Chung and Wynn (2008) 則發現當公司購買愈多的 D&O保險,公司盈餘報導會愈不保守。因此,從管理階層投機行為的觀點而言,公司購買 D&O保險會增加管理階層的自利行為,並降低董監事監督的動機與成效,進而使公司發生財務危

機,提高違約的機率,將導致信用評量機構給予較差的信用評等。

另一方面,由於 D&O保險將會使得保險公司監督投保公司營運及財務結構之狀況,以作為核保之基礎,企業為降低保費,愈會健全公司治理機制及財務結構 (Holderness, 1990; Baker and Griffith, 2007; 陳彩稚與龐嘉慧,2008),以降低訴訟風險,企業可能因而獲得較佳的信用評等。其次,由於購買 D&O保險的公司比較容易

臺大管理論叢 第27卷第4期

79

延攬優秀或具聲譽之獨立董事及管理階層,而且獨立董事需具備專業能力及獨立性,

決策較能客觀以及發揮監督的功能,故購買 D&O保險的公司較能提升經營績效與公司價值(Bhagat et al., 1987; Holderness, 1990; Daniels and Hutton, 1993; 陳彩稚與龐嘉慧,2008;陳彩稚與張瑞益,2011),減少違約的機率,保障債權人權益。過去文獻也發現獨立董事席次比率較高之公司,可降低債務融資成本 (Bhojraj and Sengupta, 2003)、提升債信評等 (Ashbaugh-Skaife et al., 2006) 以及降低信用風險(林宛瑩等,2009)。此外,亦有學者主張雖然 D&O保險移轉部分訴訟風險予保險公司,但董監事及管理階層仍須負擔部分求償金額,道德危機應能被有效的抑制,反而是公司投保

D&O保險後,造成其他利害關係人對訴訟預期的價值提高,進而增加訴訟的機率,故投保 D&O保險的公司為了減少訴訟的機率,反而可能減少投機行為 (Bhagat et al., 1987; Gutierrez, 2003; Baker and Griffith, 2007)4,並提高盈餘保守性(許文馨與林玟君,

2013),故公司購買 D&O保險將會降低信用風險。最後,當董監事及管理階層因錯誤或疏失行為而傷害債權人權益時,因有保險公司的賠償保障,使得債權人認為投保

D&O保險公司的信用風險會較低。因此,綜合上述之理由,公司購買 D&O保險會降低信用風險,將有助於信用評量機構給予較佳的信用評等。綜合前述分析可以發現,

D&O保險對於企業信用風險的影響存在著正反兩方的論述,因此,本文不預期公司購買 D&O保險對於信用評等的影響方向,僅探討兩者是否具有關聯性。故本文提出研究假說 1(以對立假說的方式表達):H1:在其他條件不變之下,購買D&O保險會影響公司的信用評等。

此外,投保金額的多寡與未來投資者損害受償金額及對董監事(管理階層)的保

障息息相關,當 D&O保險投保金額愈高,則董監事及管理階層應承擔之法律責任及訴訟風險移轉至保險公司的部分將愈大,因此,本文進一步探討 D&O保險投保金額對信用評等的影響(假說 2)。一般而言,公司考量投保金額時,除了考量公司特質及所面臨的訴訟風險外,也可能考量投機行為所帶來額外的訴訟風險而進行超額投

保,故 D&O投保金額可進一步區分為正常 D&O投保金額 (Normal D&O Insurance Coverage) 及超額 D&O投保金額 (Abnormal D&O Insurance Coverage);前者指的是能反映公司特性及風險下的預期 D&O投保金額;後者則為實際 D&O投保金額與正常D&O投保金額間的差異數(即超額投保)。若公司根據自身特性及風險下為董監事及管理階層投保正常的 D&O保險金額,將可為董監事及管理階層之責任風險提供適

4 此種論述如同 Dye (1993) 推論因大型會計師事務所較有能力賠償,因而財務報表使用者愈會控告大型會計師事務所,大型會計師事務所為避免較高的訴訟風險,愈會維持較佳的審計品質。

董監事暨重要職員責任保險對企業信用評等之影響

80

度保障,並延攬優秀的董監事及管理階層參與經營,而且由於董監事及管理階層仍須

負擔部分求償金額,因而誘發道德危機的可能性較小。因此,本文預期有購買 D&O保險的公司,正常的 D&O投保金額將可促使董監事及管理階層積極監督其他董監事及管理階層的行為,因而提升公司治理的效能,降低企業的信用風險,因此信用評量

機構將給予較佳的信用評等(即假說 2a)。然而,從過去文獻發現,D&O保險對公司治理有負面影響的原因係來自 D&O保險所誘發之道德危機,Wynn (2008) 認為當董監事與管理階層進行投機的誘因與機會愈大,超額 D&O投保金額愈大,藉以移轉投機行為所帶來增額的法律責任,其實證結果發現超額投保金額愈大的公司,自願揭露

盈餘品質會愈差。因此,本文預期有購買 D&O保險的公司,超額投保金額愈大,債權人反而會認為董監事與管理階層自利行為會更為嚴重,因而增加企業的信用風險,

進而導致信用評量機構給予公司較差的信用評等(即假說 2b)。綜合上述分析,針對D&O保險投保金額對信用評等的影響,本文建立之研究假說 2a及 2b如下:H2a:有購買 D&O保險的公司,正常投保金額將導致公司獲得較佳的信用評等。

H2b:有購買 D&O保險的公司,超額投保金額將導致公司獲得較差的信用評等。

參、研究設計

一、實證模型與變數衡量

由於臺灣主管機關並未強制上市(櫃)公司購買 D&O保險,故本文先針對全部樣本,測試公司是否購買 D&O保險與信用評等的關聯性(假說 1),接著再針對有購買 D&O保險的樣本,進一步探討投保金額對信用評等的影響(假說 2),本文實證模型分別為下列式 (1) 及式 (2)。測試假說 1(針對全部樣本)

TCRI = a0 + a

1DO + Σφ

kControl Variables

k + (Year Dummies) +

(1) (Industry Dummies) + error

測試假說 2a及 2b(針對有購買 D&O保險之樣本)

TCRI = b0 + b

1NormalDO + b2AbnDO + ΣχkControl Variables

k + (Year Dummies) +

(2) (Industry Dummies) + error

在應變數 (TCRI) 衡量方面,本文以臺灣經濟新報 (Taiwan Economic Journal; TEJ) 所建構之企業信用風險指標 (Taiwan Corporate Credit Risk Index; TCRI) 作為債權人對

臺大管理論叢 第27卷第4期

81

企業信用風險認知的代理變數 5。TEJ將企業的信用風險高低分為 9等,其中 1至 4等為低度風險;5至 6等為中度風險;7至 9為高等風險;D為企業已發生違約或倒帳,為了便於分析,本文將屬於 D等之企業量化為第 10等 6;換言之,TCRI值愈大,代表公司的信用評等愈差。由於信用風險指標係等級上之差異,因此本文以 Order Probit迴歸模型進行估計。在實驗變數的衡量方面,由於臺灣主管機關並未強制上市(櫃)

公司購買 D&O保險,故為了測試公司有無購買 D&O保險是否會造成信用評等的差異(假說 1),本文針對全部樣本,以虛擬變數的方式衡量 D&O保險(若有購買D&O保險,則 DO為 1;反之為 0),本文預期式 (1)中 DO的係數將顯著異於 0(測試假說 1)。此外,D&O投保金額的多寡應與未來投資者損害受償金額及對董監事(管理階

層)的保障息息相關,過去文獻亦發現超額投保金額可以更精確地衡量 D&O保險對董監事與管理階層所衍生之道德危機的影響 (Wynn, 2008)。因此本文進一步針對有購買 D&O保險的樣本,探討正常投保金額及超額投保金額是否會影響公司信用風險,進而影響信用評等。本文參考 D&O保險需求相關文獻 (Holderness, 1990; Core, 1997; O’Sullivan, 2002; Chung and Wynn, 2008; Zou, Wong, Shum, Xiong, and Yan, 2008; 陳彩稚與龐嘉慧,2008),歸納出影響企業D&O保險投保金額的決定因素,包括訴訟風險、公司規模及公司治理三類變數,並建構 D&O保險投保金額模型(式 (3)),估計公司正常投保金額及超額投保金額,而超額投保金額 (AbnDO)則為實際 D&O投保金額與正常 D&O投保金額 (NormalDO)7之差異數,亦即式 (3)之誤差項,並且預期式 (2)中NormalDO的係數將顯著小於 0(測試假說 2a),而 AbnDO的係數將顯著大於 0(測

試假說 2b)。

DO_Amtit = α0 + α

1Betait + α

2ROAit + α

3Levit + α

4Restateit + α

5MBit + α

6GDRit +

α7ECBit + α

8Techit + α

9Stockit + α

10Sizeit + α

11Inddirit + α

12Controlit + (3)

α13Controlownit + α

14Mgtownit + α

15Bonusit + ɛit

5 TCRI係針對所有公開發行公司做為評估對象(排除金融、證券、投資及媒體業),根據財務報表等公開資訊分析並輔以專業人士加以判斷來決定信用指標等級,故其所建立信用風險評等指標較

為客觀,所使用之樣本代表性較強,樣本選擇性的偏誤較小。此外,TCRI被很多銀行作為內部評估貸款人風險之參考,也被分析師作為選股分析的指標之一。

6 TEJ說明其 TCRI的 1-4級約當於 S&P分類中的投資等級,5-10級則可類比於投機等級(參見貨幣觀測與信用風險評等 ,第 46期 , p134)。

7

董監事暨重要職員責任保險對企業信用評等之影響

82

其中,DO_Amt為公司實際 D&O投保金額以淨值平減 8,過去文獻發現,公司訴

訟風險愈大時,風險規避之董監事以及經理人會要求公司購買 D&O保險,並增加保險金額做為風險補償 (Core, 1997; O’Sullivan, 2002)。訴訟風險與公司財務風險、成長機會、海外籌措資金、產業、股東人數等因素有關(Core, 1997; O’Sullivan, 2002; Chung and Wynn, 2008; Zou et al., 2008; 陳彩稚與龐嘉慧,2008)。首先,本文財務風險之代理變數包括系統風險 (Beta)、資產報酬率 (ROA)、負債比率 (Lev)、財務重編的虛擬變數 (Restate)。其次,成長機會較大的企業,面臨訴訟的風險較高,公司愈可能購買 D&O保險,並且可以避免投資不足的問題 (Core, 1997; O’Sullivan, 2002; Zou et al., 2008),本文以市值淨值比 (MB) 作為成長機會之代理變數。由於國外的法律環境與責任比臺灣嚴峻,進行海外募資活動的公司以及以國外銷貨為主的高科技產業,所

面臨的訴訟風險較大(Chung and Wynn, 2008; Chen and Li, 2010; 陳彩稚與龐嘉慧,2008),故預期進行海外募資活動以及電子產業的公司,對 D&O保險的需求較大,本文分別包括是否發行海外有價證券 (GDR與 ECB) 的虛擬變數以及電子業 (Tech) 的虛擬變數。股東人數愈多,面臨股東求償的機率愈大,公司愈可能購買D&O保險(Zou et al., 2008; 陳彩稚與龐嘉慧,2008),故本文以股東人數取對數 (Stock) 納入控制。公司規模愈大,股東可預期賠償損失愈大,發生訴訟的機率也愈高,故對 D&O保險的需求較大 (Core, 1997);但大公司因實質服務效率 (Real-service Efficiencies) 較高及破產成本較低,反而會降低對 D&O保險的需求 (Mayers and Smith, 1990; O’Sullivan, 2002),故本文以總資產取對數 (Size) 納入控制,但不預期影響方向。在公司治理變數方面,獨立董事多為風險規避者,通常較會要求公司購買 D&O保險,且 D&O保險亦可幫助公司延攬優秀獨立董事 (O’Sullivan, 2002; Zou et al., 2008),故本文納入獨立董監事席次比率 (Inddir)。當控制股東控制力或經理人持股愈高時,為追求自身效用最大化,則較會忽略外部股東之利益,故代理成本愈大的公司愈可能去買 D&O保險,增加個人薪酬之保障 (Core, 1997; Zou et al., 2008);但當控制股東控制力或經理人持股愈高時,與外部股東的利益會較一致,反而會降低訴訟風險;而且需分擔保險成本也

會增加,導致 D&O保險的需求會降低 (Core, 1997)。故本文將最終控制席次比率 (Control)、最終控制持股比率 (Controlown) 及經理人持股比率 (Mgtown) 納入控制,但不預期影響方向。D&O保險為董監事總薪酬之一部分,亦即 D&O保險與其他形式薪資互為替代品,故當其他董監事酬勞增加時,則 D&O保險需求會降低 (Core, 1997);但另一方面,董監事酬勞愈高,代表董監事所面臨的責任與風險愈大,對 D&O保險需求愈大(陳彩稚與龐嘉慧,2008),故將董監事酬勞取對數 (Bonus) 納入控制,但

8 D&O投保金額以淨值平減目的係排除公司規模的效果,過去亦有文獻以總資產平減(如Wynn, 2008),故本文在敏感性測試另將 D&O投保金額以總資產平減進行分析。

臺大管理論叢 第27卷第4期

83

不預期影響方向。 最後,本文參考過去文獻,在式 (1) 及式 (2) 中加入影響信用風險之控制變數,包

括股權結構、公司治理特性與財務特性等因素(Ashbaugh-Skaife et al., 2006; Alali et al., 2012; 林宛瑩等,2009)。股權結構包括大股東持股比率 (Block)9、內部人持股比率 (Insiderown)10、機構投資人持股比率 (Instown)11、控制權偏離程度 (Deviation) 及是否為家族企業 (Family)等變數,除了控制權偏離程度 (Deviation)預期係數為正 12外,其他

變數不預期係數方向。公司治理特性包括董事會規模 (Board)、獨立董監事席次比率 (Inddir)、董事長兼任總經理 (Dual)、獨立董監事專業性 (Inddir_Expert)、董事持股質押比率 (Pledge)、總經理及財務主管的異動次數 (CEOturn、CFOturn) 等變數,當公司治理愈佳,企業違約的機率愈低,信用風險會愈低(即 TCRI值會愈小),因此,除了董事會規模 (Board) 不預期係數方向 13外,獨立董監事席次比率 (Inddir)、獨立董監事專業性 (Inddir_Expert) 預期係數為負 14,而董事長兼任總經理 (Dual)、董事持股質押比率 (Pledge)、總經理及財務主管的異動次數 (CEOturn、CFOturn) 預期係數為正 15。財

務特性包括公司規模 (Size)、資產報酬率 (ROA)、負債比率 (Lev)、發生損失 (Loss)、利息保障倍數 (Interest_inten) 與資本密集度 (PPE_inten) 變數。當公司財務愈健全,企業違約的機率愈低,信用風險會愈低,因此,資本密集度 (PPE_inten)、公司規模 (Size)、資產報酬率 (ROA) 與利息保障倍數 (Interest_inten) 預期係數為負,而負債比率 (Lev)、發生損失 (Loss) 預期係數為正。此外,為了控制年度及產業的影響,本文亦在

9 大股東持股比率愈高,愈有誘因監督管理階層 (Oviatt, 1988);然而,大股東仍以股東的立場對管理階層進行監督,其股東角色與債權人仍存在代理問題 (Jensen and Meckling, 1976),故本文不預期大股東持股比率的係數方向。

10 當內部人持股比率愈高時,須承擔企業財富損失的部分也愈大,內部人與外部債權人的利益會趨於一致,代理成本愈小,並致力於企業價值的提升 (Jensen, 1993)。但另一方面也可能造成擁有足夠投票權或影響力保障其職位安全,進行不利於公司價值的行為 (Jensen and Ruback, 1983),故本文不預期內部人持股比率的係數方向。

11 機構投資人因為具備更多專業知識與技術,能在公司治理上扮演積極監督的角色 (Pound, 1988);然而,機構投資人仍以股東的立場對管理階層進行監督,其股東角色與債權人仍存在代理問題(林

宛瑩等,2009),故本文不預期機構投資人持股比率的係數方向。12 控制股東控制權偏離程度愈大,控制股東侵占財富的可能性愈大,企業的價值愈低,企業違約的機率愈大,故債權人要求的債務資金成本會愈大(林宛瑩等,2009),進而降低信用評等。

13 董事會規模過大容易造成董事會功能不彰 (Jensen, 1993),但亦有研究指出,董事會規模大可以容納較多專業領域的專家,決策品質較佳 (Zahra and Pearce, 1989),故本文不預期董事會規模的係數方向。

14 董事會若具有獨立性與專業性,較能發揮監督效果與制定較佳的決策,故發生的違約機率較低,進而提升債信評等(Ashbaugh-Skaife et al., 2006; 林宛瑩等,2009)。

15 董事長兼任總經理或董事持股質押比率愈高,將減弱監督功能,進行自利誘因的動機愈強,因而導致較高的信用風險 (林宛瑩等,2009)。另外,過去研究顯示總經理及財務主管的異動與公司績效不佳有關 (Weisbach, 1988; Farrell and Whidbee, 2003),而公司財務狀況惡化會提高違約機率,降低信用評等(林宛瑩等,2009)。

董監事暨重要職員責任保險對企業信用評等之影響

84

式 (1) 及式 (2) 加入年度 (Year) 及產業 (Industry) 之虛擬變數。茲將詳細的變數說明列示於附錄。

二、樣本選取及資料來源

本研究資料來源為臺灣經濟新報資料庫及公開資訊觀測站。為了加強公司治理相

關資訊揭露,主管機關要求上市(櫃)公司自 2008年開始須揭露有關 D&O保險相關資訊,因此,本文以 2008年至 2011年排除行業性質特殊之金融、保險及證券產業之上市(櫃)公司為研究對象,並刪除資料缺漏不全之觀察值,篩選後最終研究樣本共

計 4,150個觀察值,茲將最終研究樣本與購買 D&O保險樣本各年度分佈情形彙整於表 1。從表 1可以發現,有購買 D&O保險的公司為 2,221個,占全部樣本 53.52%,而且購買 D&O保險的公司家數有逐年成長的趨勢。

表 1 樣本分配年 度 全部樣本(測試 H1) 購買 D&O 保險之樣本 (%)(測試 H2)

2008 930 425 (45.70%)

2009 964 479 (49.69%)

2010 1,021 573 (56.12%)

2011 1,235 744 (60.24%)

合 計 4,150 2,221 (53.52%)

肆、實證結果

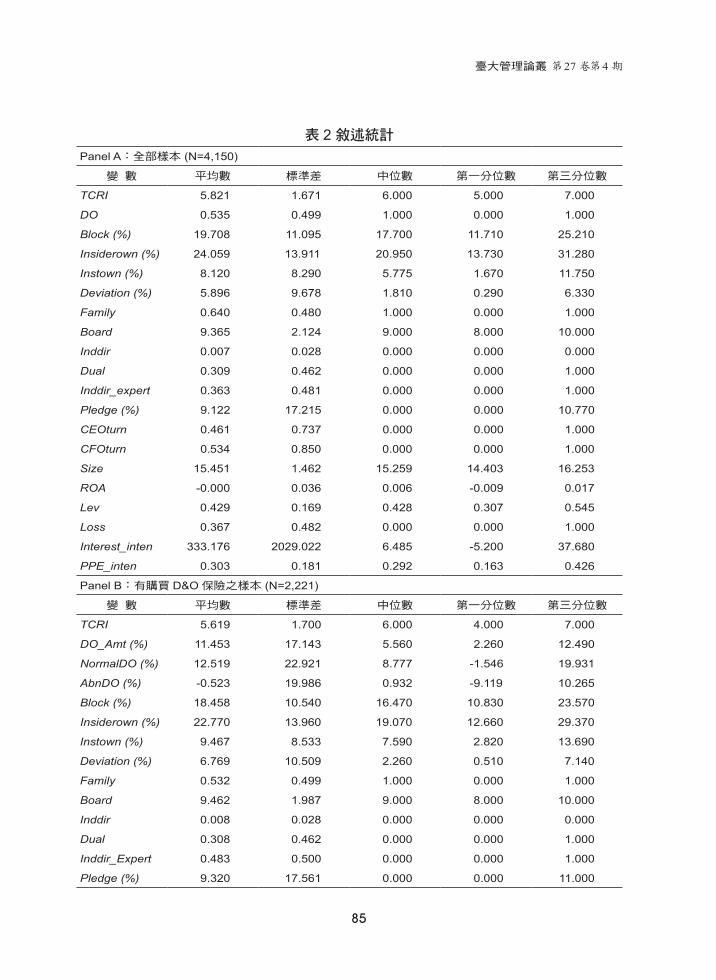

一、敘述性統計

為了控制極端值的影響,本文將自變數中屬連續變數者,其數值大於(小於)第

99 (1) 百分位值之資料做溫賽化 (Winsorize) 處理。表 2列示所有變數之敘述統計量。由表 2可發現,全部樣本 (Panel A) TCRI的平均數(中位數)為 5.821 (6.000),而有購買 D&O保險樣本 (Panel B) TCRI的平均數(中位數)為 5.619 (6.000),顯示上市(櫃)公司屬於中度風險等級占多數 16。購買 D&O保險 (DO) 的平均數為 0.535 (Panel A),顯示有購買 D&O保險的公司占所有研究樣本 53.5%。其次,從 Panel B發現,有購買 D&O保險的公司,其投保 D&O保險金額占淨值 (DO_Amt) 的平均數為11.453%,正常投保 D&O保險金額 (NormalDO) 的平均數為 12.519%,超額投保 D&O保險金額 (AbnDO)的平均數為 -0.523%,顯示平均而言,公司購買 D&O保險金額小於正常D&O投保金額,但其中位數卻為 0.932%,顯示超額投保的公司仍占 50%以上。

16 未列表顯示研究樣本之各等級信用風險指標分布情形為 1至 4等(低度風險)約占 21.23%;5至6等(中度風險)約占 47.56%;7至 10等(高等風險)約占 31.21%。

臺大管理論叢 第27卷第4期

85

表 2 敘述統計Panel A:全部樣本 (N=4,150)

變 數 平均數 標準差 中位數 第一分位數 第三分位數

TCRI 5.821 1.671 6.000 5.000 7.000

DO 0.535 0.499 1.000 0.000 1.000

Block (%) 19.708 11.095 17.700 11.710 25.210

Insiderown (%) 24.059 13.911 20.950 13.730 31.280

Instown (%) 8.120 8.290 5.775 1.670 11.750

Deviation (%) 5.896 9.678 1.810 0.290 6.330

Family 0.640 0.480 1.000 0.000 1.000

Board 9.365 2.124 9.000 8.000 10.000

Inddir 0.007 0.028 0.000 0.000 0.000

Dual 0.309 0.462 0.000 0.000 1.000

Inddir_expert 0.363 0.481 0.000 0.000 1.000

Pledge (%) 9.122 17.215 0.000 0.000 10.770

CEOturn 0.461 0.737 0.000 0.000 1.000

CFOturn 0.534 0.850 0.000 0.000 1.000

Size 15.451 1.462 15.259 14.403 16.253

ROA -0.000 0.036 0.006 -0.009 0.017

Lev 0.429 0.169 0.428 0.307 0.545

Loss 0.367 0.482 0.000 0.000 1.000

Interest_inten 333.176 2029.022 6.485 -5.200 37.680

PPE_inten 0.303 0.181 0.292 0.163 0.426

Panel B:有購買 D&O 保險之樣本 (N=2,221)

變 數 平均數 標準差 中位數 第一分位數 第三分位數

TCRI 5.619 1.700 6.000 4.000 7.000

DO_Amt (%) 11.453 17.143 5.560 2.260 12.490

NormalDO (%) 12.519 22.921 8.777 -1.546 19.931

AbnDO (%) -0.523 19.986 0.932 -9.119 10.265

Block (%) 18.458 10.540 16.470 10.830 23.570

Insiderown (%) 22.770 13.960 19.070 12.660 29.370

Instown (%) 9.467 8.533 7.590 2.820 13.690

Deviation (%) 6.769 10.509 2.260 0.510 7.140

Family 0.532 0.499 1.000 0.000 1.000

Board 9.462 1.987 9.000 8.000 10.000

Inddir 0.008 0.028 0.000 0.000 0.000

Dual 0.308 0.462 0.000 0.000 1.000

Inddir_Expert 0.483 0.500 0.000 0.000 1.000

Pledge (%) 9.320 17.561 0.000 0.000 11.000

董監事暨重要職員責任保險對企業信用評等之影響

86

變 數 平均數 標準差 中位數 第一分位數 第三分位數

CEOturn 0.507 0.754 0.000 0.000 1.000

CFOturn 0.595 0.879 0.000 0.000 1.000

Size 15.633 1.545 15.409 14.521 16.477

ROA -0.001 0.037 0.006 -0.009 0.017

Lev 0.430 0.168 0.431 0.306 0.547

Loss 0.358 0.480 0.000 0.000 1.000

Interest_inten 341.550 2089.712 6.990 -5.880 38.960

PPE_inten 0.288 0.181 0.266 0.143 0.414

註:變數定義詳見附錄。

二、單變量分析

本文進一步將全部樣本區分為有購買 D&O保險 (N = 2,221) 及未購買 D&O保險 (N = 1,929) 兩個子樣本,並比較兩組樣本間各變數的平均數及中位數是否存在顯著差異,結果彙總於表 3。從表 3可以發現,無論是 T檢定或Wilcoxon等級和檢定皆顯示,相較於未購買D&O保險的公司,有購買D&O保險的公司,TCRI較低,信用評等較佳,不過單變量檢測並未將其他控制變數納入考量,因此單變量結果只能作為初步檢測之

參考。此外,單變量檢定亦顯示,相較於未購買 D&O保險的公司,有購買 D&O保險的公司,有較高(或較大)的機構投資人持股比率 (Instown)、控制股東控制權偏離程度 (Deviation)、董事會規模 (Board)、獨立董監事專業性 (Inddir_Expert)、總經理的異動次數 (CEOturn)、財務主管的異動次數 (CFOturn) 及公司規模 (Size);另一方面則有較低的大股東持股比率 (Block)、內部人持股比率 (Insiderown)、屬家族企業 (Family) 及資本密集度 (PPE_inten)。

臺大管理論叢 第27卷第4期

87

表 3 單變量分析

變 數

購買 D&O 保險

(N = 2,221)未購買 D&O 保險

(N = 1,929)T 檢定

Wilcoxon 等級

和檢定

平均數 中位數 平均數 中位數平均數差異

(t 值)

中位數差異

(Z 值)

TCRI 5.619 6.000 6.053 6.000 -0.434 *** 0.000 ***

(-8.409) (-8.25)

Block 18.458 16.470 21.147 18.950 -2.690 *** -2.480 ***

(-7.846) (-8.017)

Insiderown 22.770 19.070 25.543 22.570 -2.773 *** -3.500 ***

(-6.436) (-8.118)

Instown 9.467 7.590 6.569 4.020 2.898 *** 3.570 ***

(11.407) (13.477)

Deviation 6.769 2.260 4.889 1.330 1.880 *** 0.930 ***

(6.270) (8.453)

Family 0.532 1.000 0.766 1.000 -0.234 *** 0.000 ***

(-16.145) (-15.662)

Board 9.462 9.000 9.252 9.000 0.210 *** 0.000 ***

(3.188) (5.811)

Inddir 0.008 0.000 0.007 0.000 0.001 0.000

(0.735) (1.020)

Dual 0.308 0.000 0.311 0.000 -0.002 0.000

(-0.146) (-0.146)

Inddir_Expert 0.483 0.000 0.225 0.000 0.258 *** 0.000 ***

(17.864) (17.217)

Pledge 9.320 0.000 8.894 0.000 0.426 0.000

(0.794) (1.215)

CEOturn 0.507 0.000 0.409 0.000 0.099 *** 0.000 ***

(4.320) (5.020)

CFOturn 0.595 0.000 0.464 0.000 0.131 *** 0.000 ***

(4.959) (5.712)

Size 15.633 15.409 15.242 15.064 0.390 *** 0.345 ***

(8.655) (8.002)

ROA -0.001 0.006 0.000 0.005 -0.001 0.001

(-1.208) (0.536)

Lev 0.430 0.431 0.428 0.422 0.001 0.009

(0.275) (0.439)

董監事暨重要職員責任保險對企業信用評等之影響

88

變 數

購買 D&O 保險

(N = 2,221)未購買 D&O 保險

(N = 1,929)T 檢定

Wilcoxon 等級

和檢定

平均數 中位數 平均數 中位數平均數差異

(t 值)

中位數差異

(Z 值)

Loss 0.358 0.000 0.378 0.000 -0.020 0.000

(-1.365) (-1.365)

Interest_inten 341.550 6.990 323.534 5.530 18.02 1.460

(0.285) (0.777)

PPE_inten 0.288 0.266 0.319 0.311 -0.031 *** -0.045 ***

(-5.528) (-5.814)

註:***、** 及 * 分別代表雙尾 1%、5% 及 10% 的顯著水準,變數定義請參考附錄。

三、多元迴歸分析

首先,為了測試公司有無購買 D&O保險是否會造成信用評等的差異(假說 1),本文將 Order Probit迴歸估計的結果彙總在表 4。從表 4可以發現,DO之係數顯著為負(係數為 -0.092,p值為 0.012),顯示相較於未購買 D&O保險的公司,有購買D&O保險的公司,信用評等機構會給予較低的 TCRI;換言之,實證結果比較支持購買 D&O保險會降低債權人對企業信用風險的認知,而獲得較佳的信用評等。在控制變數方面,本文發現企業信用評等 (TCRI) 與 Insiderown、Instown、Board、Inddir、Inddir_Expert、Size及 ROA呈顯著負相關;而與 Family、Dual、Pledge、CEOturn、CFOturn、Lev、Loss及 PPE_inten呈顯著正相關,此結果大致與過去文獻發現一致

(Ashbaugh-Skaife et al., 2006; 林宛瑩等,2009)。此外,本文進一步針對有購買 D&O保險的樣本,將各公司之 D&O保險投保金

額 (DO_Amt) 拆解成正常 D&O投保金額 (NormalDO) 及超額投保金額 (AbnDO),檢測正常及超額投保金額與信用評等之關聯性。首先,本文參考相關文獻,建構 D&O保險金額需求模型(即式 3),並據以估計 NormalDO及 AbnDO,未列表發現 D&O保險金額需求模型的解釋能力 (Adj. R2) 高達 75.6%,而且大部分影響 D&O保險需求變數 (ROA、Lev、MB、GDR、Stock、Size、Controlown、Bonus) 的係數皆具顯著性,且與預期方向一致,顯示本文所建構 D&O保險金額需求模型可合理估計正常及超額D&O投保金額。

臺大管理論叢 第27卷第4期

89

表 4 D&O保險對信用評等影響之迴歸結果變 數 預期符號 係數 p 值

DO ? -0.092 (0.012)**

Block ? -0.001 (0.729)

Insiderown ? -0.006 (0.000)***

Instown ? -0.012 (0.000)***

Deviation + 0.003 (0.201)

Family ? 0.090 (0.012)**

Board ? -0.034 (0.000)***

Inddir - -2.036 (0.000)***

Dual + 0.138 (0.000)***

Inddir_Expert - -0.173 (0.000)***

Pledge + 0.010 (0.000)***

CEOturn + 0.096 (0.000)***

CFOturn + 0.135 (0.000)***

Size - -0.787 (0.000)***

ROA - -7.211 (0.000)***

Lev + 3.666 (0.000)***

Loss + 0.504 (0.000)***

Interest_inten - 0.000 (0.685)

PPE_inten - 1.414 (0.000)***

Year and Industry dummies Included

Wald χ2 3373.62 (0.000)***

Pseudo R2 0.277

樣本數 4,150

註:***、** 及 * 分別代表雙尾 1%、5% 及 10% 的顯著水準,變數定義請參考附錄。

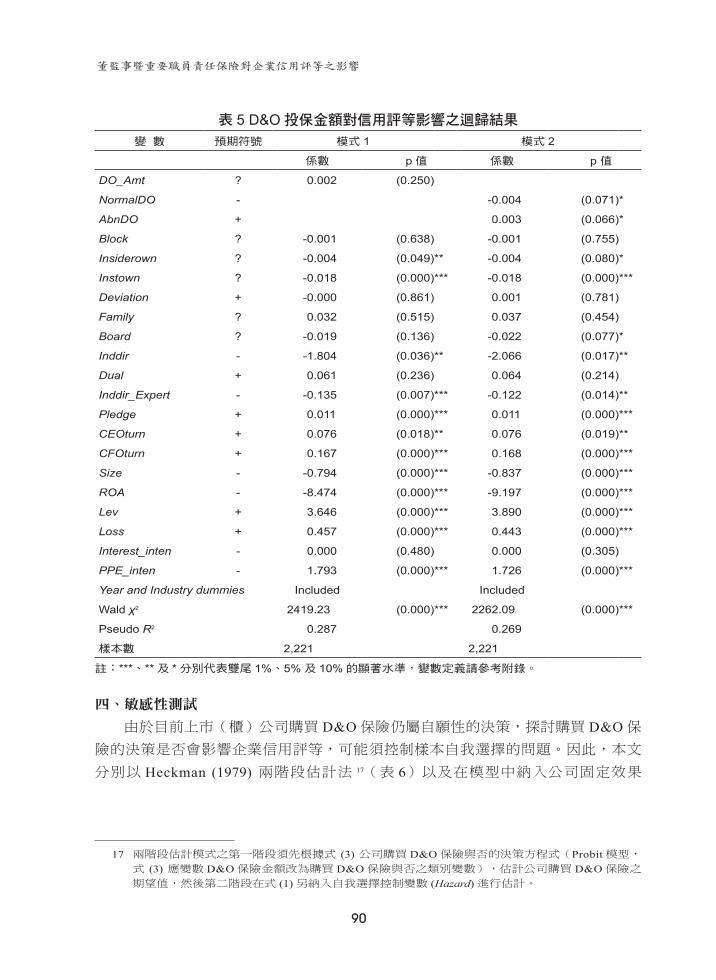

接著,本文分別針對 D&O投保總金額 (DO_Amt)(即模式 1)以及將其拆解成正常投保金額 (NormalDO) 及超額投保金額 (AbnDO)(即模式 2)對信用評等的影響進行估計,並將結果列示在表 5。從模式 1的結果發現 DO_Amt之係數雖為正,但未達顯著水準(係數為 0.002,p值為 0.250);然而模式 2估計結果卻發現 NormalDO之係數顯著為負(係數為 -0.004,p值為 0.071),而AbnDO之係數顯著為正(係數為 0.003,p值為 0.066)。因此,結果顯示當公司依自身之特質及所面臨的風險投保適度的金額(即正常投保金額),將可獲得較佳的信用評等;但當公司投保金額超過公司自身特

質及風險所需之保險金額(即超額投保金額)愈大時,反而使債權人認為董監事與管

理階層的道德風險會增加,因而導致給予較差的信用評等。

董監事暨重要職員責任保險對企業信用評等之影響

90

表 5 D&O投保金額對信用評等影響之迴歸結果變 數 預期符號 模式 1 模式 2

係數 p 值 係數 p 值

DO_Amt ? 0.002 (0.250)

NormalDO - -0.004 (0.071)*

AbnDO + 0.003 (0.066)*

Block ? -0.001 (0.638) -0.001 (0.755)

Insiderown ? -0.004 (0.049)** -0.004 (0.080)*

Instown ? -0.018 (0.000)*** -0.018 (0.000)***

Deviation + -0.000 (0.861) 0.001 (0.781)

Family ? 0.032 (0.515) 0.037 (0.454)

Board ? -0.019 (0.136) -0.022 (0.077)*

Inddir - -1.804 (0.036)** -2.066 (0.017)**

Dual + 0.061 (0.236) 0.064 (0.214)

Inddir_Expert - -0.135 (0.007)*** -0.122 (0.014)**

Pledge + 0.011 (0.000)*** 0.011 (0.000)***

CEOturn + 0.076 (0.018)** 0.076 (0.019)**

CFOturn + 0.167 (0.000)*** 0.168 (0.000)***

Size - -0.794 (0.000)*** -0.837 (0.000)***

ROA - -8.474 (0.000)*** -9.197 (0.000)***

Lev + 3.646 (0.000)*** 3.890 (0.000)***

Loss + 0.457 (0.000)*** 0.443 (0.000)***

Interest_inten - 0.000 (0.480) 0.000 (0.305)

PPE_inten - 1.793 (0.000)*** 1.726 (0.000)***

Year and Industry dummies Included Included

Wald χ2 2419.23 (0.000)*** 2262.09 (0.000)***

Pseudo R2 0.287 0.269

樣本數 2,221 2,221

註:***、** 及 * 分別代表雙尾 1%、5% 及 10% 的顯著水準,變數定義請參考附錄。

四、敏感性測試

由於目前上市(櫃)公司購買 D&O保險仍屬自願性的決策,探討購買 D&O保險的決策是否會影響企業信用評等,可能須控制樣本自我選擇的問題。因此,本文

分別以 Heckman (1979) 兩階段估計法 17(表 6)以及在模型中納入公司固定效果

17 兩階段估計模式之第一階段須先根據式 (3) 公司購買 D&O保險與否的決策方程式(Probit模型,式 (3) 應變數 D&O保險金額改為購買 D&O保險與否之類別變數),估計公司購買 D&O保險之期望值,然後第二階段在式 (1) 另納入自我選擇控制變數 (Hazard) 進行估計。

臺大管理論叢 第27卷第4期

91

表 6 D&O保險對信用評等影響之迴歸結果:採用 Heckman兩階段估計法變 數 預期符號 係數 p 值

信用評等模型

DO ? -1.756 (0.000)***

Block ? -0.006 (0.004)***

Insiderown ? -0.011 (0.000)***

Instown ? -0.008 (0.001)***

Deviation + 0.003 (0.173)

Family ? 0.041 (0.267)

Board ? -0.020 (0.030)**

Inddir - -2.431 (0.000)***

Dual + 0.138 (0.000)***

Inddir_Expert - -0.101 (0.012)**

Pledge + 0.010 (0.000)***

CEOturn + 0.100 (0.000)***

CFOturn + 0.129 (0.000)***

Size - -0.732 (0.000)***

ROA - -8.396 (0.000)***

Lev + 3.771 (0.000)***

Loss + 0.480 (0.000)***

Interest_inten - 0.000 (0.788)

PPE_inten - 1.418 (0.000)***

Hazard ? 1.024 (0.000)***

Year and Industry dummies Included

D&O 保險選擇模型

Beta + 0.062 (0.454)

ROA - -2.615 (0.000)***

Lev + 0.159 (0.249)

Restate + 0.131 (0.312)

MB + 0.089 (0.000)***

GDR + 0.182 (0.122)

ECB + -0.048 (0.622)

Tech + 0.937 (0.009)***

Stock + 0.095 (0.010)***

Size ? 0.105 (0.002)***

Inddir + -0.921 (0.220)

Control ? -0.013 (0.000)***

Controlown ? -0.003 (0.027)**

Mgtown ? 0.031 (0.002)***

Bonus ? 0.130 (0.000)***

Wald χ2 3317.07 (0.000)***

Pseudo R2 0.2281

樣本數 4,150

註:***、** 及 * 分別代表雙尾 1%、5% 及 10% 的顯著水準,變數定義請參考附錄。

董監事暨重要職員責任保險對企業信用評等之影響

92

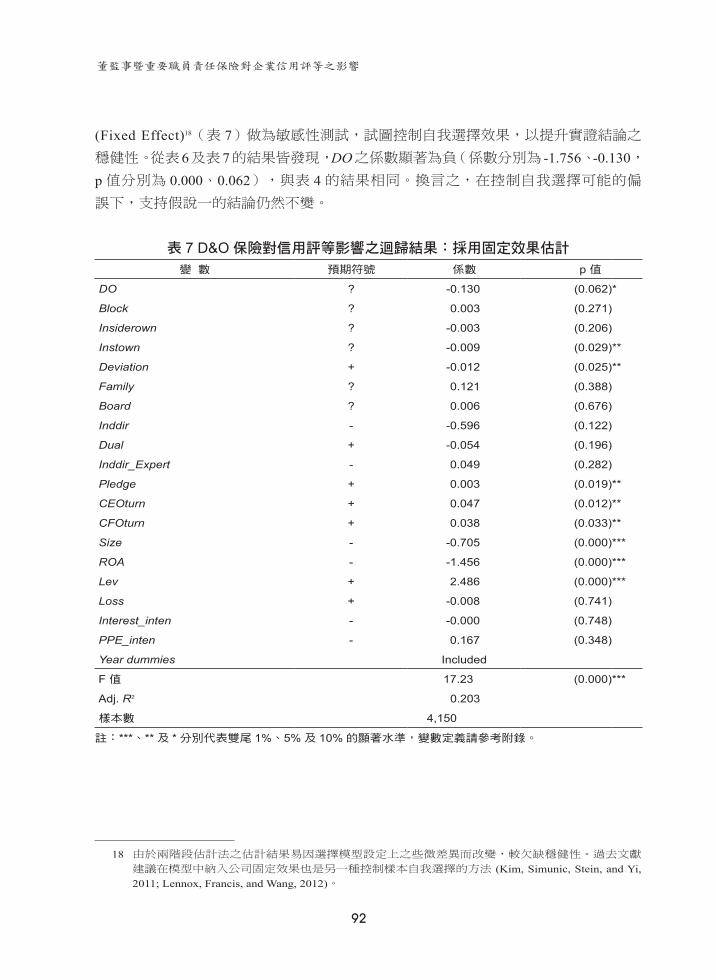

(Fixed Effect)18(表 7)做為敏感性測試,試圖控制自我選擇效果,以提升實證結論之穩健性。從表6及表7的結果皆發現,DO之係數顯著為負(係數分別為 -1.756、-0.130,p值分別為 0.000、0.062),與表 4的結果相同。換言之,在控制自我選擇可能的偏誤下,支持假說一的結論仍然不變。

表 7 D&O保險對信用評等影響之迴歸結果:採用固定效果估計變 數 預期符號 係數 p 值

DO ? -0.130 (0.062)*

Block ? 0.003 (0.271)

Insiderown ? -0.003 (0.206)

Instown ? -0.009 (0.029)**

Deviation + -0.012 (0.025)**

Family ? 0.121 (0.388)

Board ? 0.006 (0.676)

Inddir - -0.596 (0.122)

Dual + -0.054 (0.196)

Inddir_Expert - 0.049 (0.282)

Pledge + 0.003 (0.019)**

CEOturn + 0.047 (0.012)**

CFOturn + 0.038 (0.033)**

Size - -0.705 (0.000)***

ROA - -1.456 (0.000)***

Lev + 2.486 (0.000)***

Loss + -0.008 (0.741)

Interest_inten - -0.000 (0.748)

PPE_inten - 0.167 (0.348)

Year dummies Included

F 值 17.23 (0.000)***

Adj. R2 0.203

樣本數 4,150

註:***、** 及 * 分別代表雙尾 1%、5% 及 10% 的顯著水準,變數定義請參考附錄。

18 由於兩階段估計法之估計結果易因選擇模型設定上之些微差異而改變,較欠缺穩健性。過去文獻建議在模型中納入公司固定效果也是另一種控制樣本自我選擇的方法 (Kim, Simunic, Stein, and Yi, 2011; Lennox, Francis, and Wang, 2012)。

臺大管理論叢 第27卷第4期

93

D&O投保金額以淨值平減主要目的係排除公司規模的效果,過去 D&O相關文獻亦有使用總資產平減(如Wynn, 2008),故本文另以投保金額以總資產平減進行分析,未列表的實證結果發現 NormalDO之係數顯著為負,而 AbnDO之係數顯著為正,故D&O投保金額以總資產平減的結果與 D&O投保金額以淨值平減的結果(表 5)大致相同,本文假說二的實證結論仍然不變。

由於 TCRI第 10級為企業已發生財務危機(違約或倒帳),本文刪除此類型樣本後重複表 4與表 5的分析 19。未列表的結果顯示DO顯著為負,而NormalDO顯著為負,AbnDO顯著為正,換言之,刪除已發生財務危機的樣本後,本文的結論仍然不變。

此外,臺灣經濟新報說明其 TCRI的 1-4級約當於 S&P分類投資等級,5-10級則可類比於投機等級,因此,本文另將 TCRI分成高低兩種等級(TCRI屬於 5-10級者設為 1,其他等級則設為 0),以 Probit模型重複表 4與表 5的分析,未列表的實證結果亦顯示 DO顯著為負,而 NormalDO顯著為負,AbnDO顯著為正,換言之,本文的結論仍然不變。

最後,臺灣經濟新報對上市櫃公司第 t年進行信用風險評估,可能是根據第 t-1年公司財務報表等公開資訊分析,故迴歸式中應變數的期間 (t) 與自變數的期間 (t-1) 應相差一期。因此,本文針對自變數的資料,另以 t-1年的數據取代 t年的數據,重複表4與表 5的分析,未列表的實證結果顯示與表 4及表 5的結果大致相同。綜合上述分析,本文實證證據穩健地支持相對於未購買 D&O保險的公司,有購

買 D&O保險的公司,其信用評等較佳(結果支持假說 1)。然而,為求精確補捉D&O保險與信用評等的關聯性,本文進一步針對有購買 D&O保險的樣本,檢測正常及超額投保金額與信用評等之關聯性。實證結果則發現當公司依自身之特質及所面臨

的風險投保適度的金額(即正常投保金額),將可促使董監事及管理階層積極監督其

他董監事及管理階層的行為,因而提升公司治理的效能,降低企業的信用風險,因此

信用評量機構將給予公司較佳的信用評等(結果支持假說 2a);但當公司投保金額超過公司自身特質及風險所需之保險金額(即超額投保金額)愈大時,債權人反而會認

為董監事與管理階層自利行為會更為嚴重,因而增加企業的信用風險,進而導致信用

評量機構給予公司較差的信用評等(結果支持假說 2b)。

19 由於表 5的結果顯示資料有明顯自我選擇的問題,故本節之敏感性測試於探討有無購買 D&O保險對信用風險評等之影響時,皆以兩階段 Heckman模型控制自我選擇下進行分析。

董監事暨重要職員責任保險對企業信用評等之影響

94

伍、結論

債務融資為企業重要籌措資金管道之一,信用風險評量機構所發佈企業信用評等

高低除了會影響債務融資的可能性與資金成本外,其對股票市場的影響亦不可忽視。

由於 D&O保險可能會影響公司治理的成效,亦會改變公司董監事及管理階層之法律責任,而公司治理成效及監事與管理階層法律責任皆會影響企業的信用風險。因此,

本文從債權人的觀點,探討上市(櫃)公司投保 D&O保險是否會影響債權人對企業信用風險的認知。

整體而言,實證結果穩健地支持相對於未購買 D&O保險的公司,有購買 D&O保險的公司,其信用評等較佳;然而進一步針對有購買 D&O保險的公司,探討其投保金額與信用評等之關聯性時,實證結果則發現,正常投保金額將可獲得較佳的信用

評等;但超額投保金額愈大時,反而使債權人認為董監事與管理階層的道德風險會增

加,因而導致給予較差的信用評等。

本文研究結果除了可彌補 D&O保險相關文獻的不足外,並提供相關信用評等文獻的增額貢獻。此外,本文研究結果對證券市場主管機關、外部債權人及保險公司而

言,各有其重要的政策意涵。首先,在推動 D&O保險政策之餘,仍應注意如何防範公司發生超額投保的情況。其次,對外部債權人而言,固然投保金額愈大,似乎對債

權人的保障愈大,但超額投保卻可能誘發道德危機的行為,進而可能傷害外部債權人

的權益,因此應注意公司D&O投保金額的決策,才能確保D&O保險產生正面的效果。最後,對保險公司而言,雖然各保險公司積極拓展 D&O保險的業務,但仍需注意投保公司超額投保所引發董監事及管理階層道德危機的情況,以避免未來承擔不必要的

風險及損失。

臺大管理論叢 第27卷第4期

95

The Effect of Directors’ and Officers’ Liability Insurance on Firms’ Credit Ratings

SummaryIn recent years, the securities authority in Taiwan has been encouraging the firms listed

in the Taiwanese Stock Exchange (TWSE) and GreTai Securities Market (GTSM) to purchase directors’ and officers’ liability insurance (D&O insurance hereafter). The motivation of this recommendation is to protect the interests of outside investors. The purchase of D&O insurance for directors and officers can compensate outside investors for losses arising from the wrongdoings or negligence of directors or officers. However, D&O insurance also transfers certain legal liabilities to the insurance company, which may increase agency conflicts of debt and managerial opportunism (Moral Hazard); D&O insurance thereby also increases the risk for outside investors.

Debt financing is a primary source of capital for business enterprises, and creditors are also important outside investors. Designated agencies issue credit ratings, which are determined by both the firm’s credit risk and its probability of default. Credit ratings can impact the possibility of debt financing and the cost of debt. This fact has driven us to explore the effect of D&O insurance on firms’ credit ratings, which serves as a proxy for creditors’ perceptions of credit risk.

Prior studies on this subject are lacking. Although European and American countries have implemented the D&O insurance system for many years, the information on D&O insurance is not disclosed. The few D&O insurance studies are mostly concentrated on the countries (e.g., Canada, UK), where D&O insurance information is disclosed upon request. For example, some Canadian studies have explored the association between D&O insurance and IPO (Initial Public Offering) prices, earnings conservatism and voluntary disclosure (Chalmers et al., 2002; Chung and Wynn, 2008; Wynn, 2008). Their findings show that although D&O insurance can lower the directors’ and officers’ legal liabilities, it may also motivate directors and officers to engage in opportunistic earnings management. Thus, D&O insurance may not be conducive to earnings quality and stock performance.

Hsiu-Mei Liao, Associate Professor, Department of Accounting, Ming Chuan University

Li-Fen Tang, Associate Professor, Department of Accounting Information, Chihlee University of Technology

Jan-Zan Lee, Professor, Department of Accountancy, National Taipei University

董監事暨重要職員責任保險對企業信用評等之影響

96

Creditors are also important stakeholders. D&O insurance may also affect creditors’ perceptions of credit risk. Due to the credit rating agencies being professional debt rating institutions, the credit ratings issued by them will affect the cost of debt. So far, no prior studies have investigated the effect of D&O insurance and its coverage on firms’ credit ratings. To better understand these effects, we explore the association between D&O insurance and firms’ credit ratings.

The primary objectives of sound corporate governance are (1) to enhance business performance and corporate value and (2) to protect the interests of all stakeholders. Prior studies have demonstrated that corporate governance impact credit ratings (Ashbaugh-Skaife et al., 2006; Lin et al., 2009; Alali et al., 2012). Directors and managers play critical roles in the efforts to build sound corporate governance systems. The literature exposes two opposing effects of D&O insurance on corporate governance – the monitoring role and managerial opportunism. In other words, D&O insurance also has two opposing effects on firms’ credit risk.

If the purchase of D&O insurance can strengthen the function of the board, business performance will be effectively enhanced. Moreover, this will reduce the probability of default. In other words, D&O insurance can improve a firm’s credit risk (Monitoring Role Effect). In addition, the included compensation of the insurance company as a guarantee allows D&O insurance to further protect the interests of the creditors. Therefore, the protection of the interests of creditors and the improvement in a firm’s credit risk that come with D&O insurance should lead to superior credit ratings issued by credit rating agencies.

On the other hand, if the purchase of D&O insurance increases the risk of moral hazard from the directors and officers, the likelihood of damage at the expense of the creditors also increases (Managerial Opportunism Effect). It follows that the purchase of D&O insurance will lead to inferior credit ratings issued by credit rating agencies. Motivated by these paradoxical effects, we design the following research hypotheses (these hypotheses are stated as alternative hypotheses):H1: D&O insurance is correlated with credit ratings.H2a: For firms with D&O insurance, normal D&O insurance coverage is negatively

associated with credit ratings (superior credit ratings).H2b: For firms with D&O insurance, abnormal D&O insurance coverage is positively

associated with credit ratings (inferior credit ratings).

臺大管理論叢 第27卷第4期

97

We construct a sample from the firms listed on both the TWSE and GTSM from 2008 to 2011. We exclude the finance, insurance and securities sectors. Our data is collected from the financial, stock and corporate governance databases of Taiwan Economic Journal (TEJ hereafter). Our full sample for test H1 contains 4,150 observations after excluding observations with missing value in variables. For test H2, we use a sample of 2,221 observations.

In this study, we first explore the effect of D&O insurance on firms’ credit ratings. We then further explore the effect of D&O insurance coverage on credit ratings only for firms with D&O insurance. We tested H1 and H2 with the following regression models:

Test H1 (full sample)

TCRI = a0 + a

1DO + Σφ

kControl Variables

k + (Year Dummies) +

(1) (Industry Dummies) + error

Test H2 (a sub-sample of firms with D&O insurance)

TCRI = b0 + b

1NormalDO + b2AbnDO + ΣχkControl Variables

k + (Year Dummies) +

(2) (Industry Dummies) + error

For the measurement of the dependent variable, we adopt the Taiwan Corporate Credit Risk Index (TCRI), constructed by the TEJ. TCRI serves as a proxy for creditors’ perceptions of credit risk. TEJ classifies corporate credit risk into nine levels. Levels 1 to 4 represent low risk. Levels 5 to 6 represent medium risk, and levels 7 to 9 represent high risk. “D” refers to firms that have violated agreements or defaulted on their debt payments. To facilitate our analysis, we quantify “D” as level 10. A higher TCRI represents a higher credit risk, an inferior credit rating by the credit rating agency, and vice versa. Because TCRI is an ordinal dependent variable, we employ an ordered probit regression model for estimation.

The independent variable DO is a dummy variable for the full sample. If the firm purchases D&O insurance, its DO is 1; otherwise, its DO is 0. We do not predict the direction of the effect of D&O insurance on credit ratings. We do, however, predict the coefficient of DO to be significantly different from 0 (for test H1).

董監事暨重要職員責任保險對企業信用評等之影響

98

We further explore the effect of normal insurance coverage (NORMAL_DO) and abnormal insurance coverage (AbnDO) on credit ratings for firms with D&O insurance. We predict the direction of NormalDO to be negative and the direction of AbnDO to be positive.

The evidence shows that firms with D&O insurance have better credit ratings than those without D&O insurance (supporting H1). Further results show that D&O insurance coverage also impacts firms’ credit ratings. If the firm purchases the appropriate (normal) D&O insurance coverage that suits the firm’s specific characteristics and risk, it tends to have a superior credit rating (supporting H2a). However, if the firm purchases excess (abnormal) D&O insurance coverage that is more than the firm’s needs , it tends to have an inferior credit rating, a fact that likely stems from opportunistic behaviors from the directors and managers at the expense of creditors (supporting H2b).

Our study offer important contributions to this field. First, our study is the first to investigate the effect of D&O insurance and its coverage on firms’ credit ratings as perceived by creditors, thus filling not only the void in the existing literature on D&O insurance, but also the scarcity of research on credit ratings. Second, we find that the purchase of D&O insurance can reduce credit ratings as perceived by creditors, but only when it is the purchase of excess (abnormal) D&O insurance. These findings imply that future research should further explore the effect of D&O insurance coverage on the effectiveness of corporate governance. Third, the results of this study also can act as a reference to security authorities in the implementation of D&O insurance, a reference to insurance companies in decision-making on D&O insurance, and a reference to creditors in the assessment of the effect of D&O insurance on firms’ credit ratings.

臺大管理論叢 第27卷第4期

99

參考文獻

林宛瑩、許崇源、戚務君與陳宜伶,2009,公司治理與信用風險,臺大管理論叢,19卷 S2期:71-98。(Lin, Wan-Ying, Hsu, Chung-Yuan, Chi, Wu-Chun, and Chen, Yi-Ling. 2009. Corporate governance and credit risk. NTU Management Review, 19 (Supplement-2): 71-98. )

許文馨與林玟君,2013,董監事責任險、債務契約與盈餘保守性,臺大管理論叢,24卷 1期:1-42。(Hsu, Audrey Wen-Hsin, and Lin, Wen-Chun. 2013. Directors' and officers' liability insurance, debt contracting, and earnings conservatism. NTU Management Review, 24 (1): 1-42.)

陳彩稚與張瑞益,2011,公司治理:董監事責任與董事會結構,管理評論,30卷 3期:1-23。(Chen, Tsai-Jyh, and Chang, Jui-I. 2011. Corporate governance: Directors' liability and board structure. Management Review, 30 (3): 1-23.)

陳彩稚與龐嘉慧,2008,董監事暨重要職員責任保險之需求因素分析,臺大管理論叢, 18卷 2期:171-196。(Chen, Tsai-Jyh, and Pang, Chia-Hui. 2008. An analysis of determinants of the corporate demand for directors' and officers' liability insurance. NTU Management Review, 18 (2): 171-196.)

Alali, F., Anandarajan, A., and Jiang, W. 2012. The effects of corporate governance on firms’ credit ratings: Further evidence using governance score in the United States. Accounting & Finance, 52 (2): 291-312. doi: 10.1111/j.1467-629X.2010.00396.x

Ashbaugh-Skaife, H., Collins, D. W., and LaFond, R. 2006. The effects of corporate governance on firms’ credit ratings. Journal of Accounting and Economics, 42 (1-2): 203-243. doi: 10.1016/j.jacceco.2006.02.003

Baker, T., and Griffith, S. J. 2007. The missing monitor in corporate governance: The directors’ and officers’ liability insurer. Georgetown Law Journal, 95 (6): 1795-1842. doi: 10.2139/ssrn.946309

Bhagat, S., Brickley, J. A., and Coles, J. L. 1987. Managerial indemnification and liability insurance: The effect on shareholder wealth. Journal of Risk and Insurance, 54 (4): 721-736. doi: 10.2307/253119

Bhojraj, S., and Sengupta, P. 2003. Effect of corporate governance on bond ratings and yields: The role of institutional investors and outside directors. The Journal of Business, 76 (3): 455-475. doi: 10.1086/344114

Boyer, M. M., and Delvaux-Derome, M. 2002. The demand for directors’ and officers’ insurance in Canada (Working Paper No. 2002s-72). Montreal, Canada: Center for Interuniversity Research and Analysis of Organizations.

董監事暨重要職員責任保險對企業信用評等之影響

100

Brook, Y., and Rao, R. K. S. 1994. Shareholder wealth effects of directors’ liability limitation provisions. The Journal of Financial and Quantitative Analysis, 29 (3): 481-497. doi: 10.2307/2331341

Chalmers, J. M. R., Dann, L. Y., and Harford, J. 2002. Managerial opportunism? Evidence from directors’ and officers’ insurance purchases. The Journal of Finance, 57 (2): 609-636. doi: 10.1111/1540-6261.00436

Chen, T. J., and Li, S. H. 2010. Directors’ & officers’ insurance, corporate governance and firm performance. International Journal of Disclosure and Governance, 7 (3): 244-261. doi: 10.1057/jdg.2010.9

Chung, H. H., and Wynn, J. P. 2008. Managerial legal liability coverage and earnings conservatism. Journal of Accounting and Economics, 46 (1): 135-153. doi: 10.1016/j.jacceco.2008.03.002

Core, J. E. 1997. On the corporate demand for directors’ and officers’ insurance. Journal of Risk and Insurance, 64 (1): 63-87. doi: 10.2307/253912

. 2000. The directors’ and officers’ insurance premium: An outside assessment of the quality of corporate governance. Journal of Law, Economics, and Organization, 16 (2): 449-477. doi: 10.1093/jleo/16.2.449

Daniels, R. J., and Hutton, S. 1993. The capricious cushion: The implications of the directors and insurance liability crisis on Canadian corporate governance. Canadian Business Law Journal, 22 (2): 182-230.

Dye, R. A. 1993. Auditing standards, legal liability, and auditor wealth. Journal of Political Economy, 101 (5): 887-914. doi: 10.1086/261908

Farrell, K. A., and Whidbee, D. A. 2003. Impact of firm performance expectations on CEO turnover and replacement decisions. Journal of Accounting and Economics, 36 (1-3): 165-196. doi: 10.1016/j.jacceco.2003.09.001

Forker, J. J. 1992. Corporate governance and disclosure quality. Accounting and Business Research, 22 (86): 111-124. doi: 10.1080/00014788.1992.9729426

Gutierrez, M. 2003. An economic analysis of corporate directors’ fiduciary duties. The RAND Journal of Economics, 34 (3): 516-535.

Hampel, R. 1998. Committee on Corporate Governance. London, UK: Gee Publishing Ltd.Heckman, J. J. 1979. Sample selection bias as a specification error. Econometrica, 47 (1):

153-162. doi: 10.2307/1912352Holderness, O. G. 1990. Liability insurers as corporate monitors. International Review of

Law and Economics, 10 (2): 115-129. doi: 10.1016/0144-8188(90)90018-O

臺大管理論叢 第27卷第4期

101

Jensen, M. C. 1993. The modern industrial revolution, exit, and the failure of internal control systems. The Journal of Finance, 48 (3): 831-880. doi: 10.2307/2329018

Jensen, M. C., and Meckling, W. H. 1976. Theory of the firm: Managerial behavior, agency cost and ownership structure. Journal of Financial Economics, 3 (4): 305-360. doi: 10.1016/0304-405X(76)90026-X

Jensen, M. C., and Ruback, R. S. 1983. The market for corporate control: The scientific evidence. Journal of Financial Economics, 11 (1-4): 5-50. doi: 10.1016/0304-405X(83)90004-1

Kim, J. B., Simunic, D. A., Stein, M. T., and Yi, C. H. 2011. Voluntary audits and the cost of debt capital for privately held firms: Korean evidence. Contemporary Accounting Research, 28 (2): 585-615. doi: 10.1111/j.1911-3846.2010.01054.x

Lennox, C. S., Francis, J. R., and Wang, Z. 2012. Selection models in accounting research. The Accounting Review, 87 (2): 589-616. doi: 10.2308/accr-10195

Mayers, D., and Smith, C. W. 1990. On the corporate demand for insurance: Evidence from the reinsurance market. The Journal of Business, 63 (1): 19-40.

O’Sullivan, N. 2002. The demand for directors’ and officers’ insurance by large UK companies. European Management Journal, 20 (5): 574-583. doi: 10.1016/S0263-2373(02)00096-8

Oviatt, B. M. 1988. Agency and transaction cost perspectives on the manager-shareholder relationship: Incentives for congruent interests. Academy of Management Review, 13 (2): 214-225. doi: 10.5465/AMR.1988.4306868

Pound, J. 1988. Proxy contests and the efficiency of shareholder oversight. Journal of Financial Economics, 20 (1): 237-265. doi: 10.1016/0304-405X(88)90046-3

Priest, G. L. 1987. The current insurance crisis and modern tort law. Yale Law Journal, 96 (7): 1521-1590. doi: 10.2307/796494

Weisbach, M. S. 1988. Outside directors and CEO turnover. Journal of Financial Economics, 20: 431-460. doi: 10.1016/0304-405X(88)90053-0

Wynn, J. P. 2008. Legal liability coverage and voluntary disclosure. The Accounting Review, 83 (6): 1639-1669. doi: 10.2308/accr.2008.83.6.1639

Zahra, S. A., and Pearce, J. A. 1989. Boards of directors and corporate financial performance: A review and integrative model. Journal of Management, 15 (2): 291-334. doi: 10.1177/014920638901500208

Zou, H., Wong, S., Shum, C., Xiong, J., and Yan, J. 2008. Controlling-minority shareholder incentive conflicts and directors’ and officers’ liability insurance: Evidence from

董監事暨重要職員責任保險對企業信用評等之影響

102

China. Journal of Banking & Finance, 32 (12): 2636-2645. doi: 10.1016/j.jbankfin.2008.05.015

臺大管理論叢 第27卷第4期

103

附錄 變數定義

變 數 定義

TCRITEJ 所建構之企業信用風險指標;數值由 1 到 10。TCRI 值愈大,代表信用評量機

構給予公司的信用評等愈差;

DO 若公司有購買 D&O 保險者設為 1;反之為 0;

DO_AmtD&O 投保金額以淨值平減,主要目的係排除公司規模的效果,本文在敏感性測試另

將 D&O 投保金額以總資產平減進行分析;

NormalDO正常 D&O 投保金額;為按本文所建構的 D&O 保險投保金額模型(式 (3))所估計個

別公司的正常 D&O 投保金額;

AbnDO 超額 D&O 保險金額;為 DO_Amt 減正常 D&O 保險金額;

Block 大股東持股比率;

Insiderown 內部人(董事與經理人)持股比率;

Instown 機構投資人持股比率;

Deviation 控制股東投票權與現金流量權的偏離程度;

Family若公司為家族控制企業(引用 TEJ 公司治理資料庫集團控制型態為單一家族主導)

者設為 1,反之為 0;

Board 董事會規模;

Inddir 獨立董監事席次比率;

Dual 若公司董事長兼任總經理者設為 1,反之為 0;

Inddir_Expert 若公司獨立董監事有在其他公司擔任獨立董監事者設為 1,反之為 0;

Pledge 董事持股質押比率;

CEOturn 3 年內總經理的異動次數;

CFOturn 3 年內財務主管的異動次數;

Size 公司規模,以總資產取自然對數衡量;

ROA 資產報酬率,以淨利除以總資產衡量;

Lev 負債比率,以總負債除以總資產衡量;

Loss 若公司當年度發生淨損者設為 1,反之為 0;

Interest_inten 利息保障倍數,以稅前息前淨利除以利息費用衡量;;

PPE_inten 資本密集度,以固定資產總額除以總資產衡量;

Beta本文採用 TEJ 權益 (Equity) 資料庫以一年資料所計算 Beta 值來衡量系統風險,其公

式如下: ,其中,Ri 為個別證券報酬率,Rm 為市場證券報酬率;

Restate 若公司當年度有重編財務報表者設為 1,反之為 0;

MB 成長機會,以權益市值除以淨值衡量;

GDR 若公司有發行海外存託憑證者設為 1,反之為 0;

ECB 若公司有發行海外公司債者設為 1,反之為 0;

Tech 若公司屬電子業者設為 1,反之為 0;

Stock 股東人數取自然對數;

Control 控制股東(包括最終控制者之個人、未上市公司、基金會)席次比率;

Controlown 控制股東持股比率;

Mgtown 經理人持股比率;

Bonus 董監事酬勞取自然對數。

董監事暨重要職員責任保險對企業信用評等之影響

104

作者簡介廖秀梅

國立臺北大學會計博士,現任銘傳大學會計系副教授,主要研究領域為財務會計、

公司治理與審計。論文曾發表於「Journal of Modern Accounting and Auditing」、「臺大管理論叢」、「經濟論文」、「經濟論文叢刊」、「交大管理學報」、「中華會計

學刊」、「東吳經濟商學學報」、「當代會計」、「風險管理學報」、「會計與公司

治理」等學術期刊。

*湯麗芬國立台北大學會計博士,現任致理科技大學會計資訊系副教授,主要研究領域為

財務會計、資本市場研究、審計。論文曾發表於「經濟論文」、「經濟論文叢刊」、「交

大管理學報」、「當代會計」、「輔大管理評論」等學術期刊。

李建然

國立政治大學會計博士、現任國立台北大學會計系教授,主要研究領域:審計研

究、公司治理、市場基礎研究。論文曾發表於:「會計評論」、「中華會計學刊」、「財

務金融學刊」、「臺大管理論叢」、「經濟論文」、「經濟論文叢刊」、「交大管理

學報」、「中山管理評論」、「管理評論」、「管理與系統」、「人力資源管理學報」、

「輔大管理評論」、「東吳經濟商學學報」、「中國會計評論」、「風險管理學報」、

「當代會計」、「中華管理學報國際學報 (Web Journal of Chinese Management Review)」、「公司治理學刊」、「International Research Journal of Finance and Economics」、「會計審計論叢」等學術期刊。

* E-mail: [email protected]