european entertainment imaging industry the new context after the economical crunh - thierry...

TRANSCRIPT

1 : Economic situation

Distribution & Consumption

3 : Second Digital Revolution

New technologies New opportunities

New Financing sources

2 : Source of Finance

New ways of producing & consuming content

New digital services are booming

Reduced Broadcasters advertising revenue

Financial Crisis Credit Crunch

Reduced Broadcasters Contribution to Cinema

Reduced Investisment in new content

Public Money is getting Scarcer

Traditional markets are saturated

MG’s have nearly desappeared

New market context for EI

09.07.11 T. Perronnet / Eamer

-‐ FF independant q 2 worlds :

-‐ a) 5 big countries able to « auto finance » films & invest in productions -‐ b) More than 30 countries needing coproduction to finance their local filmmakers.

q # of financing sources : 15 to 25 is now common.

09.07.11 T. Perronnet / Eamer

40% of FF are Co-produced in EU

Now is all about Loca.on, loca.on, loca.on Ø Tax and rebate incen-ves abound Ø Chasing lower produc-on costs Ø Post forced to chase produc-ons

As a consecquence

-‐ FF independant q 2 worlds :

-‐ a) 5 big countries able to « auto finance » films & invest in productions -‐ b) More than 30 countries needing coproduction to finance their local filmmakers.

q # of financing sources : 15 to 25 is now common. q Much more difficulties to build the budget q Less # of projects q Price pressure stronger than ever q Digital more and more considered as a viable option. q Distributors want to see films finished before buying. q National MG are decreasing q Int’l presales dropping to almost 0 q Technicians more negociable & Producers are taking the power.

09.07.11 T. Perronnet / Eamer

Dramatic changes in Film Financing Structures (The French example)

09.07.11 T. Perronnet / Eamer

Financing source Vol 2008 M€ Vol 2009 M€ Compare %

Broadcasters 349 300 -‐13.8

Producer 336 267 -‐20.6

Distributor 152 121 -‐20.9

Equity / Sofica 35 34 -‐1.2

Video (law 2% net rev) 21.5 5.6 -‐74

Public funds subsid. 96.2 92 -‐4.5

Regional subsid. 32 18.8 -‐18.4

Foreign Co-‐Prod 85 75 -‐11.3

Pre sales ext. 161 13.1 -‐91.9

Total 1260 928 -‐26.3

Dramatic changes in Film Financing Structures (The French example)

09.07.11 T. Perronnet / Eamer

Budgets of films in M€

Number of FF 08 Number of FF in 09 Compare in %

Above 15 18 11 -‐39

10-‐15 17 14 -‐17.6

7-‐10 25 21 -‐16

5-‐7 11 18 +63.6

4-‐5 17 9 -‐47

2-‐4 41 45 +9.7

1-‐2 23 36 +56.5

Below 1 44 28 -‐36.3

total 196 183 -‐7.1

Of which co-‐pro 51 45 -‐11.7

09.07.11 T. Perronnet / Eamer

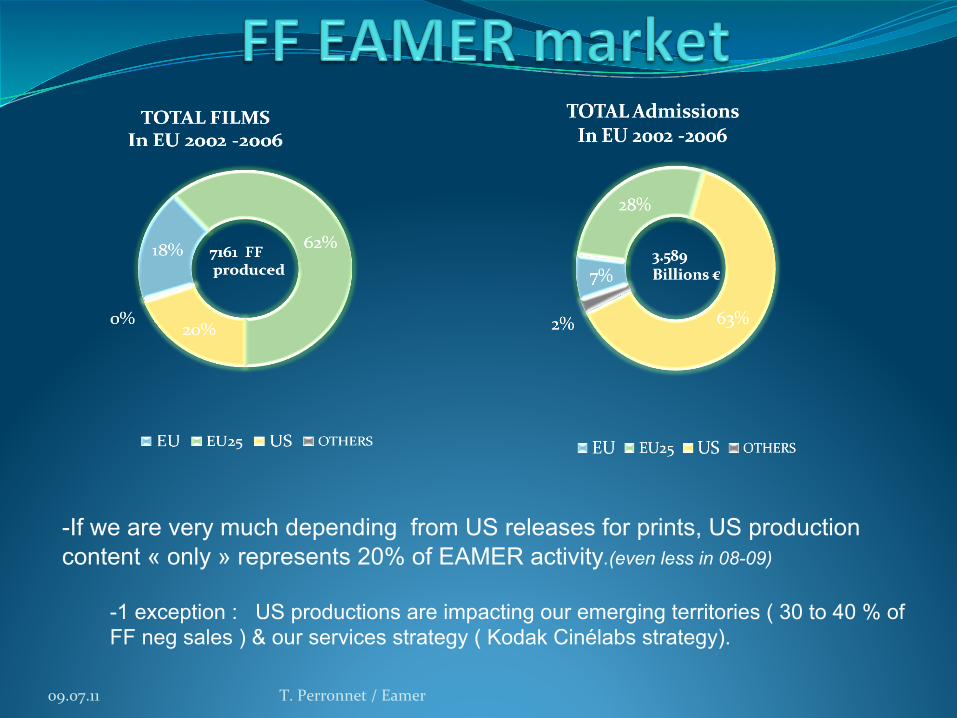

- If we are very much depending from US releases for prints, US production content « only » represents 20% of EAMER activity.(even less in 08-09)

- 1 exception : US productions are impacting our emerging territories ( 30 to 40 % of FF neg sales ) & our services strategy ( Kodak Cinélabs strategy).

-‐ TVC : A soft economy recovery ? Not yet there .

q storyboard seem to re start to circulate a little bit . q Red Hype very slightly slowing down ( -‐> after NAB?) q Communication agencies might integrate TVC producers in the future q Canon & red are approaching Com agencies directly to sell their cameras

09.07.11 T. Perronnet / Eamer

-‐ TV Drama : National content & US content

q S16mm will probably disappeared within 3 years . q 35 2 perf is taking relay in some countries ( FR, UK) q Fuji re attacking this segment since 2010( after having given up in 08 & 09 , our mkt share was above 90%) q Still a reasonable year in 2010 before the arrival of Alexa and Penelope-‐D. q Degraining solutions, package deals & 35 2 perf are the only solutions to defend film TV market.

09.07.11 T. Perronnet / Eamer

19.5 18 15.6 17 14.8 10.8 +1.1 8.9 + 2.5

European Kodak TV Market trend S16mm + 35mm Val ($)

(35 2 or 3 perf is the total EU market)

09.07.11 T. Perronnet / Eamer

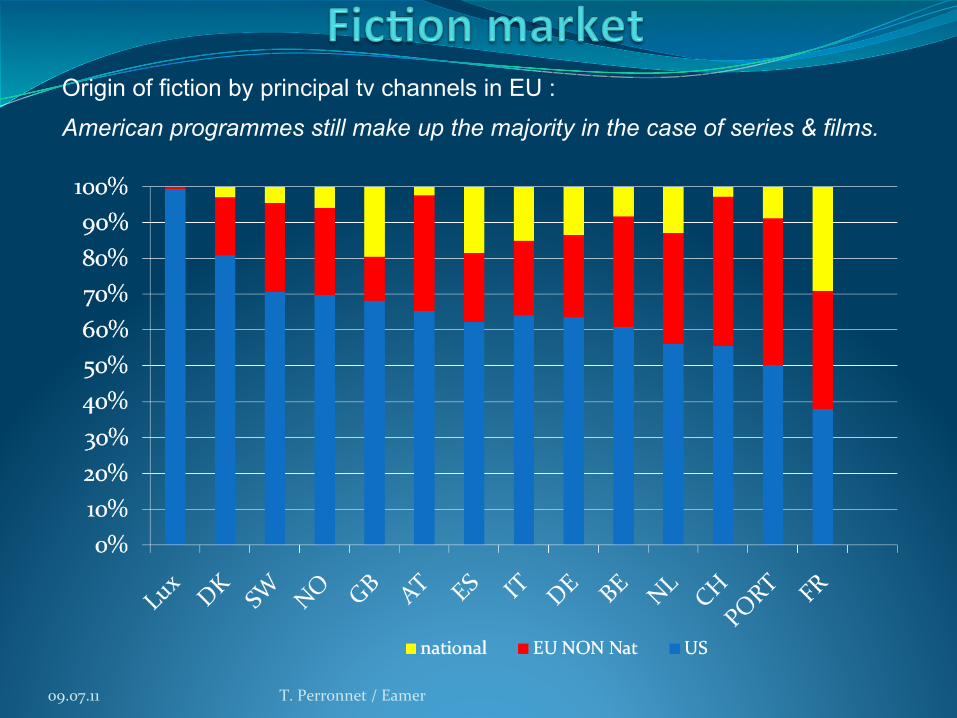

Origin of fiction by principal tv channels in EU :

American programmes still make up the majority in the case of series & films.

-‐ End 2010 / 2011 : No more true allies on the industrial market

1. 100% of camera manufacturers will have a strong digital offer. 2. Post have established a good digital workflow for digital Images

Acquisition and are able to deal with various systems … 3. Gvts are taking the relay of private investors to finance digital

distribution ( Fr, GE) 4. Gvts are financing digital re conversion for film industry (labs) via

training programs (reconversion programs) & financial tax systems to convert these companies to the future.

09.07.11 T. Perronnet / Eamer

Nevertheless -‐ In all , EU states still spend €1.6 Billion a year to support their national film industries , mostly in the form of direct grants or tax incentives

-‐ 3D hype is everywhere with a lot of confusion ( how to do it ? Extra cost for a 3D release ? 3D means automatically digital ,3D TV….)

09.07.11 T. Perronnet / Eamer

The digital revolution will of course mean profound changes for the Cinema industry : => Mutations in distribution, exhibition & productions sectors

But the cost of adaption & economical crisis should play in favour of some technical suppliers on a short term point of view ( 24 months ). 2 majors points to consider

-‐> These important transformations have a high cost in term of new equipment, dev of new business models, development of new ways of producing & distributing. -‐> On the same time, the economic situation makes it difficult for the European industry to meet these costs. ( private companies will have difficulties to follow the necessary investisment in capital & Gvts ( local + EU deficits) might also have difficulties to substitute themselves to private Investors for a while .

=> A slow down in the decrease trends but probably not an increase in volume in 2010

09.07.11 T. Perronnet / Eamer