federal & state tax - step aspects of yachting... · buyer must sign an affidavit regarding...

TRANSCRIPT

FEDERAL & STATE TAX

Considerations For Buying & Ownership Of Yachts

PRESENTED BY: UMBERTO BONAVITA

KEEPING THE FUN IN THE SUN

FLORIDA SALES TAX ON PURCHASE OF YACHTS IN THE U.S.

❑What is a Yacht?

❑“Any vessel which is propelled by sail or machinery in the water which exceeds 32 feet in length, and which weighs less than 300 gross tons.” FS. 326.002(4).

❑Vessels are, in a sense, ordinary goods. The sale of a vessel falls outside federal admiralty jurisdiction and is therefore governed by state law.

RELEVANT PROVISIONS OF FLORIDA LAW

Fla. Admin. Code r. 12A- 1.007

12A-1.007. Aircraft, Boats, Mobile Homes, and Motor Vehicles.

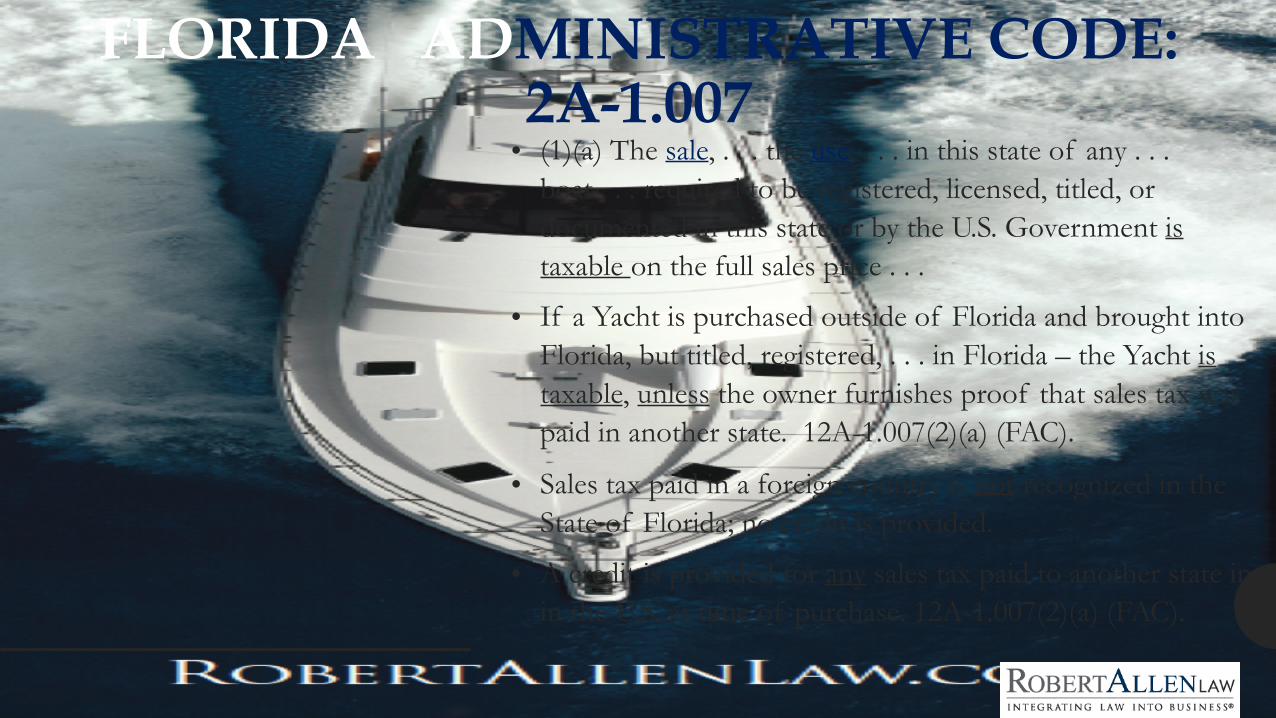

FLORIDA ADMINISTRATIVE CODE: 2A-1.007• (1)(a) The sale, . . . the use, . . . in this state of any . . .

boat . . . required to be registered, licensed, titled, or documented in this state or by the U.S. Government is taxable on the full sales price . . .

• If a Yacht is purchased outside of Florida and brought into Florida, but titled, registered, . . . in Florida – the Yacht is taxable, unless the owner furnishes proof that sales tax was paid in another state. 12A-1.007(2)(a) (FAC).

• Sales tax paid in a foreign country is not recognized in the State of Florida; no credit is provided.

• A credit is provided for any sales tax paid to another state in in the U.S. at time of purchase. 12A-1.007(2)(a) (FAC).

SALES & USE TAX IN FLORIDA

Yachts sold in the State of Florida are generally subject to Florida Sales Tax.

Yachts brought into Florida for use in this state after being purchased elsewhere are subject to the Florida Use Tax.

The state sales and use tax is 6% but the amount is capped for yachts at $18,000 -- only the first $300,000 of the purchase price is taxed. See F.S. 212.05.

1. Dealer Exemption: If the yacht is being purchased exclusively for resale or bareboat chartering:

The buyer can register as a dealer and issue a resale certificate to the selling broker.

The Florida Department of Revenue (“FDOR”) treats the purchase of a yacht for resale or bareboat charter as a tax-exempt wholesale transaction.

HOW DOES A YACHT BUYER LAWFULLY AVOID PAYING FLORIDA SALES OR USE TAX?

HOW DOES A YACHT BUYER LAWFULLY AVOID PAYING FLORIDA SALES OR USE TAX?

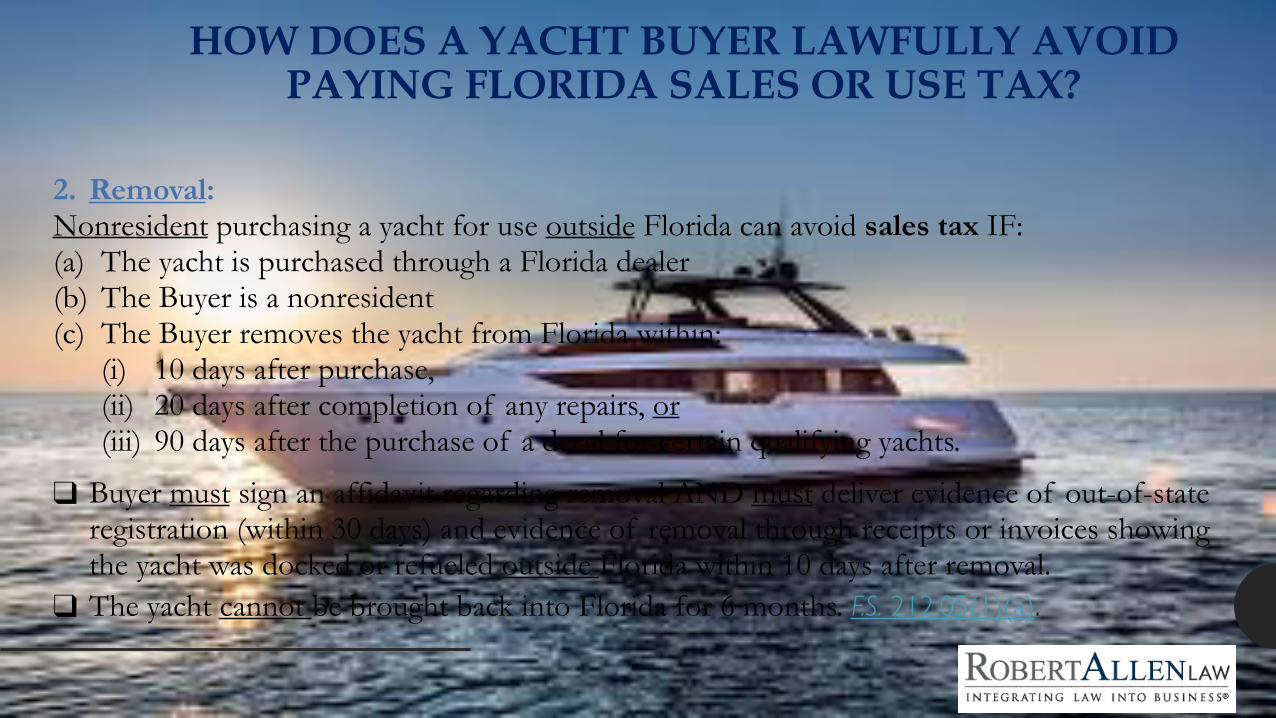

2. Removal: Nonresident purchasing a yacht for use outside Florida can avoid sales tax IF: (a) The yacht is purchased through a Florida dealer (b) The Buyer is a nonresident (c) The Buyer removes the yacht from Florida within:

(i) 10 days after purchase, (ii) 20 days after completion of any repairs, or (iii) 90 days after the purchase of a decal for certain qualifying yachts.

❑ Buyer must sign an affidavit regarding removal AND must deliver evidence of out-of-state registration (within 30 days) and evidence of removal through receipts or invoices showing the yacht was docked or refueled outside Florida within 10 days after removal.

❑ The yacht cannot be brought back into Florida for 6 months. F.S. 212.05(1)(a).

HOW DOES A YACHT BUYER LAWFULLY AVOID PAYING FLORIDA SALES OR USE TAX?

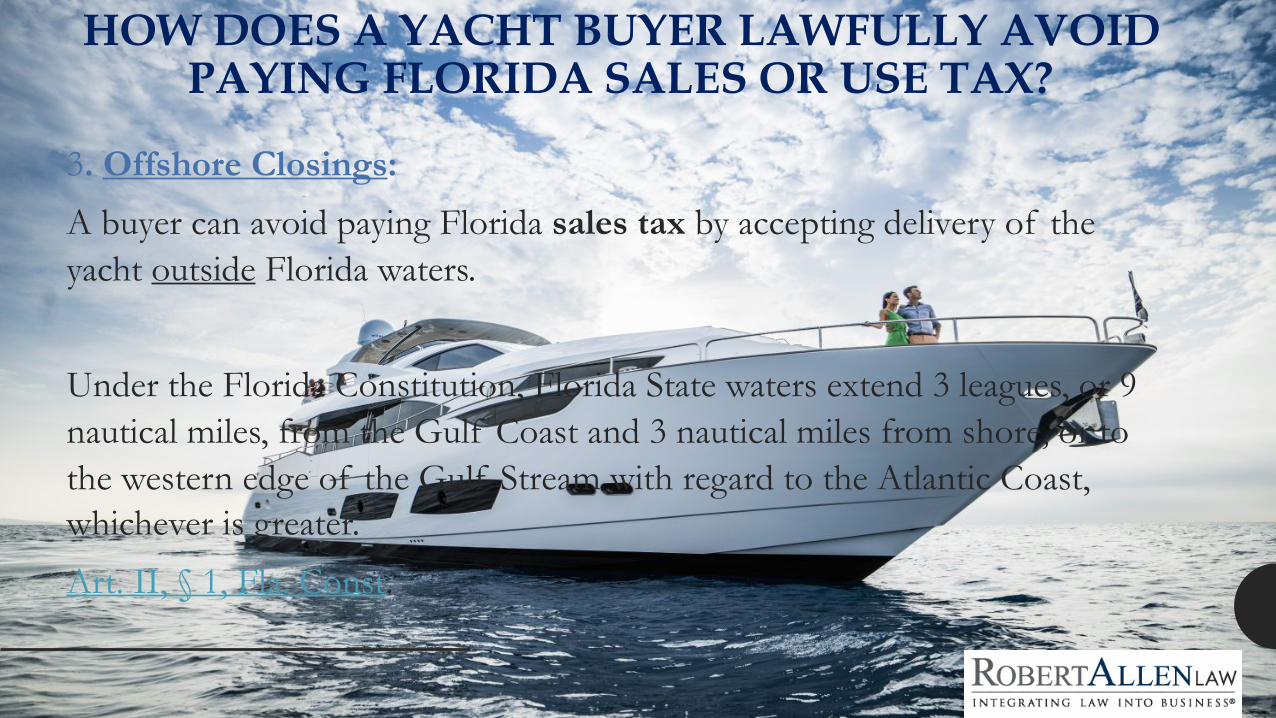

3. Offshore Closings: A buyer can avoid paying Florida sales tax by accepting delivery of the yacht outside Florida waters.

Under the Florida Constitution, Florida State waters extend 3 leagues, or 9 nautical miles, from the Gulf Coast and 3 nautical miles from shore, or to the western edge of the Gulf Stream with regard to the Atlantic Coast, whichever is greater.

Art. II, § 1, Fla. Const.

HOW TO CONDUCT AN OFFSHORE CLOSING?

oIf the yacht is not duty-paid:

➢ The buyer can take delivery in international waters – more than 12 nautical miles from shore or in The Bahamas.

oBUT, if the yacht is duty-paid, or U.S.-built and never exported:

➢The buyer may prefer to keep the yacht's duty-paid or non-exported status by avoiding an “exportation” of the yacht. The sale of a yacht in the territorial waters of another country is deemed an exportation of the yacht.

19 C.F.R. § 101.1.

3/12 CLOSINGS

To avoid exporting the Yacht at time of purchase • Buyer can accept delivery of the yacht within U.S. waters,

BUT outside Florida waters. Called “three-twelve” closings- delivery occurs between 3 & 12 nautical miles from shore. • Allows Buyer to: – Purchase the Yacht in U.S waters, no need to export the vessel and

jeopardize its duty-paid status

– Be exempt from having to pay the Florida sales tax.

HOW TO DOCUMENT OFFSHORE CLOSINGS

❑Parties will sign a protocol of delivery and acceptance onboard the Yacht to evidence the transfer of title from the seller to the buyer.

❑The protocol should include spaces to record the latitude and longitude where signing takes place and there should be proof of date and time of closing.

FLORIDA USE TAX

❑Even if a buyer avoids paying Sales tax, the buyer may still have to pay Florida Use tax.

❑Use tax is also payable at the rate of 6%, up to a maximum of $18,000, on the use of a yacht in the State of Florida.

F.S. 212.05.

EXEMPTIONS FROM FL USE TAX:

1. Dealer Exemption: Buyers may avoid paying use tax, by registering as a dealer and operating the yacht only for bareboat charter.

2. Temporary Visits by Non-Residents: Nonresidents who own no property and do no business in Florida may bring yachts into Florida for up to 90 consecutive days or 183 days in any 12 month period. Fla. Admin. Code Rule 12A-1.007(9)(b).

• FDOR will not attempt to collect use tax on a foreign yacht cruising in U.S. waters under a cruising license, provided the yacht is not offered for sale or charter.

YACHTS SITUATED IN THE US SUBJECT TO U.S. ESTATE TAX

Resident: individual who is domiciled in the US

Nonresident: individual who is not domiciled in the US

U.S. ESTATE TAX❖A person is considered to be domiciled in the U.S. for estate tax

purposes if he lives in the U.S., even for a brief period of time, and has no present intention of later leaving. Determining domicile for US estate purposes is different than determining US income tax residence.

❖You may be a resident for income tax purposes, but not US domiciled for estate tax purposes. An intention to change domicile will not generate such a change unless accompanied by actual removal; intent to leave is not sufficient.

DOMICILE AND ESTATE TAX• A nonresident alien: someone who, at the time of death, had his domicile outside of the U.S.

A U.S. on a nonimmigrant visa can be considered a resident, for estate purposes, if they want to remain in the U.S. even if visa does not allow permanent residence.

• To determination of a person’s “domicile” courts rely upon the intent of the individual, to make the determination courts will consider the following factors:

– Visas and/or work permits, – Location of business and property interests – Family immigration history

– Residential property, – Individual testimony

– Motivation

– Duration of stays in the U.S. – Community group affiliations

DETERMINING ESTATE TAX AMOUNT

➢The value of the nonresident alien’s gross estate is based on the fair market value of the decedent’s estate at the date of death.

➢“Fair market value” is the price at which the estate property would change hands between a willing buyer and seller.

➢Nonresident alien estates of more than $60,000 in U.S. gross assets must file a federal estate tax return.

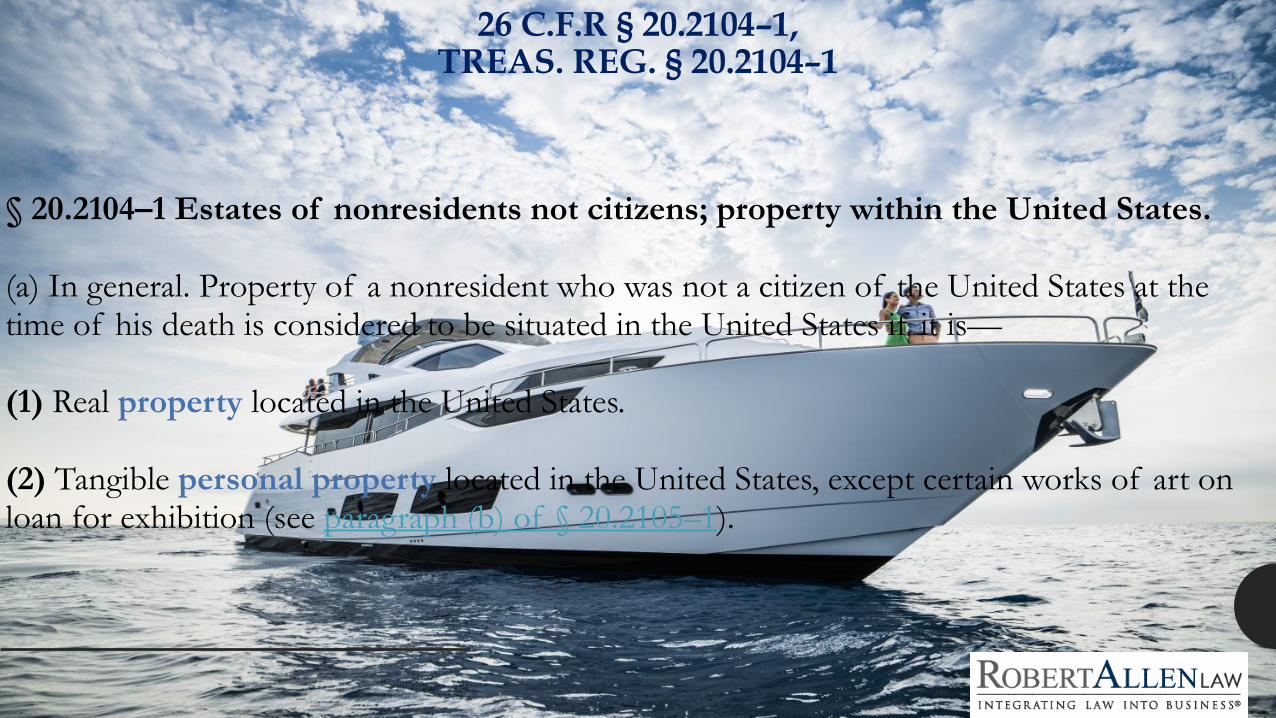

26 C.F.R § 20.2104–1, TREAS. REG. § 20.2104–1

§ 20.2104–1 Estates of nonresidents not citizens; property within the United States. (a) In general. Property of a nonresident who was not a citizen of the United States at the time of his death is considered to be situated in the United States if it is—

(1) Real property located in the United States. (2) Tangible personal property located in the United States, except certain works of art on loan for exhibition (see paragraph (b) of § 20.2105–1).

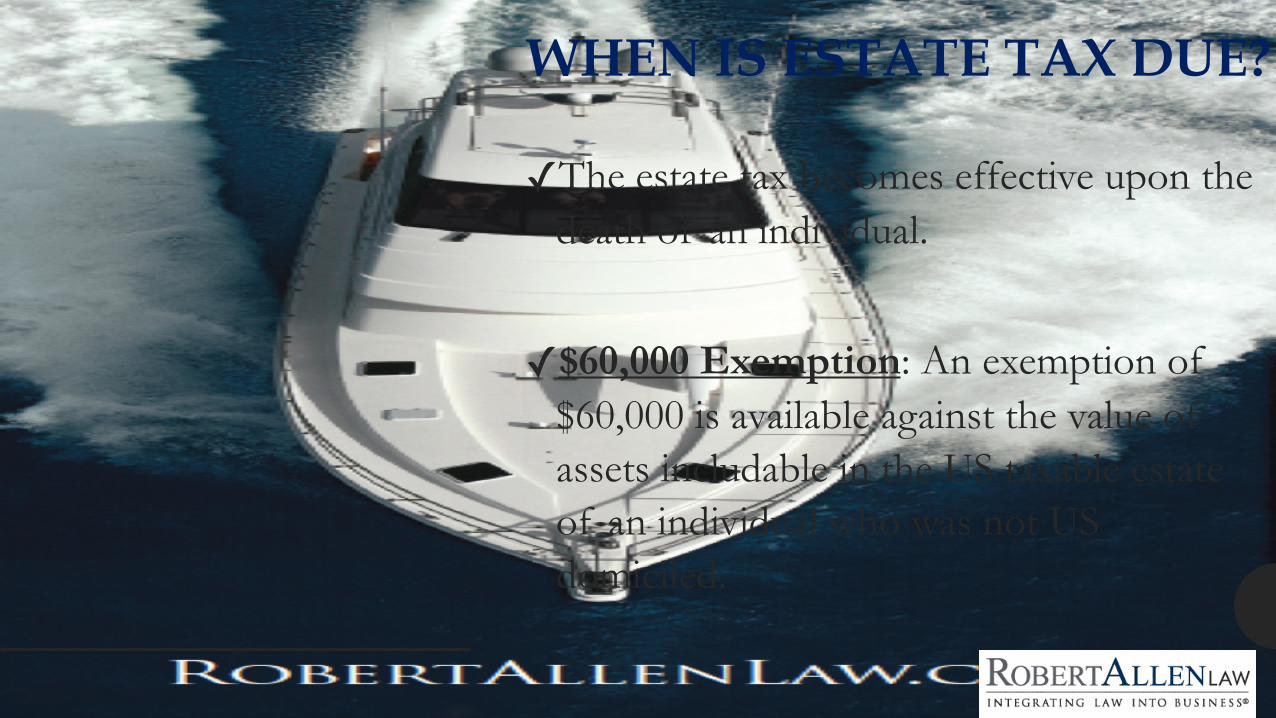

WHEN IS ESTATE TAX DUE?

✓The estate tax becomes effective upon the death of an individual.

✓$60,000 Exemption: An exemption of $60,000 is available against the value of assets includable in the US taxable estate of an individual who was not US domiciled.

HOW IS ESTATE TAX CALCULATED? Value of Taxable Estate Tentative Tax

$250,000-$500,000 $70,800 + 34% of excess over $250,000

$500,000 -$750,000 $155,800 + 37% of excess over $500,000

$750,000 -$1,000,000 $248,300 + 39% of excess over $750,000

Over $1,000,000 $345,800 + 40% of excess over $1,000,000

PLAN AHEAD: ESTATE PLANNING

❖Any asset protection plan should seek to minimize or eliminate any U.S. wealth transfer or estate tax. The imposition of wealth transfer taxes depends on domicile, the type of property, and the situs of the property. If an individual is domiciled in the U.S., all of his property is subject to U.S. estate tax.

❖In addition, certain property located in the U.S. will be subject to U.S. estate tax.

DOMICILE & LOCATION OF PROPERTY

• “A person acquires domicile in a place by living there, for even a brief period of time, with no definite present intention of later removing therefrom.” The determination of domicile is a multi-factored test.

• In order to avoid imposition of the U.S. estate tax, the property of a nonresident alien should have a situs or deemed situs outside of the United States.

WHERE IS THE YACHT?

• To be subject to U.S. estate tax, a nonresident alien's interest in Yacht must be includable in the estate if he were a U.S. citizen or resident and the property must have a situs or deemed situs in the United States.

• The situs of property is crucial in determining whether U.S. wealth transfer taxes will be imposed on nonresident aliens. Tangible personal property located in the United States has a U.S. situs and is subject to estate tax.

COLLECTION & ENFORCEMENT OF ESTATE TAXES

❑The executor of a non-domicillary’s estate is personally liable to the US Government for US estate taxes owed.

❑The executor must file an estate tax return (IRS Form 706 NA) showing the amounts of estate taxes owed.

❑Return must be filed within 9 months after death. ❑If not paid, the U.S. Government can seize the property of the estate or

the executor without obtaining a court order to pay for the outstanding estate taxes.

PROTECTING AGAINST ESTATE TAX

• The situs of property often controls its estate taxation, U.S. estate taxes can be avoided by:

1. Establishing the situs of property outside the United States or 2. By owning assets whose deemed situs is outside the United States. *There are numerous rules governing the situs of property.

• One asset that has a deemed situs outside the United States is stock in a foreign corporation.

OWNING YACHT THROUGH CORPORATE ENTITY

• For estate tax purposes, shares of a foreign corporation are treated as foreign situs property; shares of a U.S. corporation are treated as U.S. situs property.

• Transferring title of U.S. tangible personal property to a foreign corporation can transform such property into intangible property that is deemed to be non-U.S. property and, consequently, not subject to U.S. estate tax.

• The key is for the foreign corporation to be treated, for U.S. tax purposes, as a corporation, otherwise risk not working.

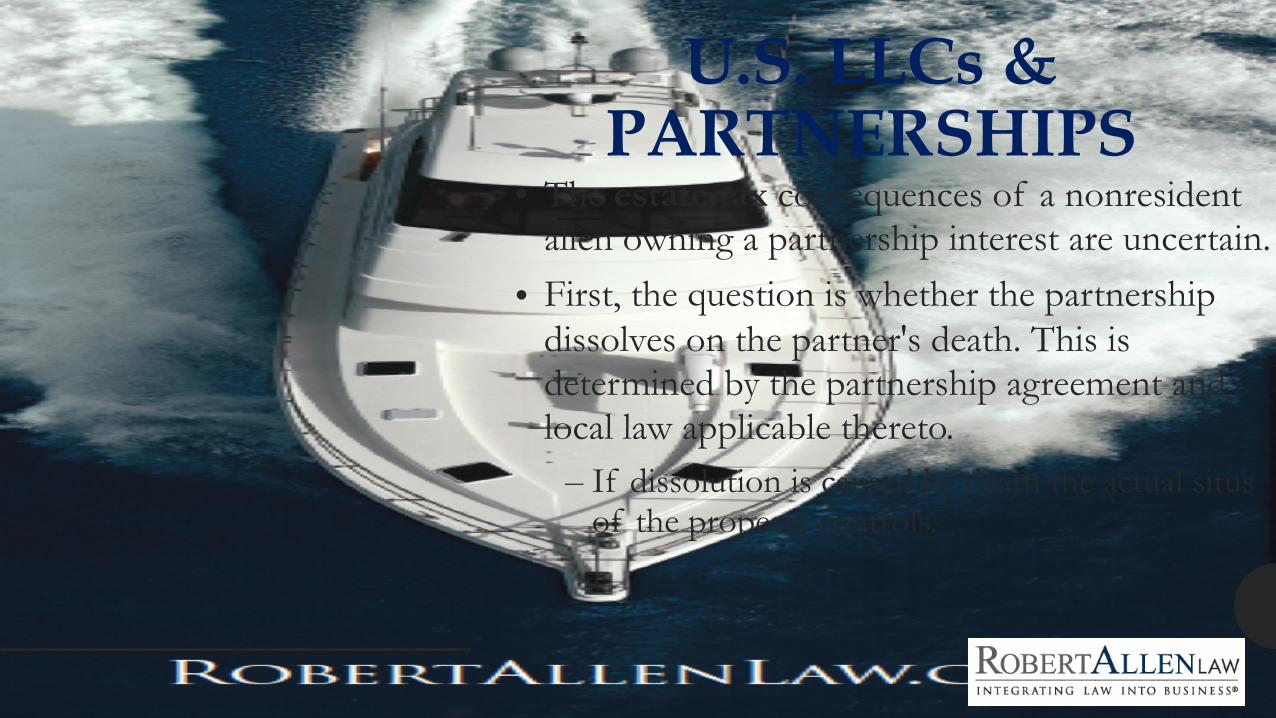

U.S. LLCs & PARTNERSHIPS

• The estate tax consequences of a nonresident alien owning a partnership interest are uncertain.

• First, the question is whether the partnership dissolves on the partner's death. This is determined by the partnership agreement and local law applicable thereto.

– If dissolution is caused by death the actual situs of the property controls.

USING PARTNERSHIPS TO SHIELD AGAINST US ESTATE TAX LIABILITY• If the partnership does not dissolve on the death of one of its partners,

the U.S. estate tax is imposed if the partnership has a deemed situs in the United States. The partnership interest would not be subject to estate tax, however, if the partnership has a foreign situs.

• Under U.S. common law, the situs of a partnership interest is the taxpayer's domicile. In Blodgett v. Silberman, the U.S. Supreme Court employed the common-law maxim of mobilia sequuntur personam to hold that assets of the partnership were deemed situated at the decedent's last domicile.

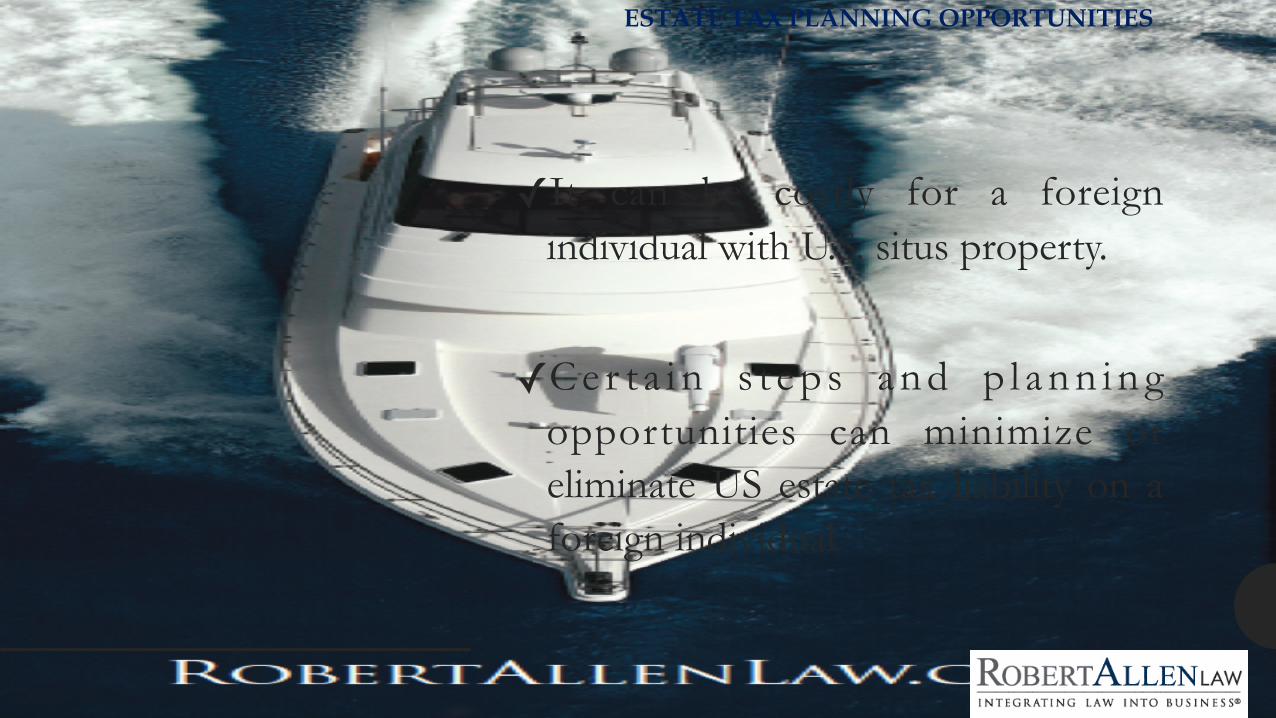

ESTATE TAX PLANNING OPPORTUNITIES

✓It can be costly for a foreign individual with U.S. situs property.

✓C e r t a i n s t e p s a n d p l a n n i n g opportunities can minimize or eliminate US estate tax liability on a foreign individual.

ESTATE PLANNING TOOLS

• Restructuring and owning Yachts so that they are not U.S. situs property.

• Transferring Yachts into certain legal entities (e.g., utilizing certain common law or civil law trusts).

• Operating U.S. yacht ownership businesses entities directly or indirectly through foreign corporations or other legal entities.

• Obtaining certain U.S. loans or other debt to reduce the taxable value of the estate.

presented by: ROBERT ALLEN LAW

Umberto Bonavita

1441 Brickell Avenue, Suite 1400

Miami, FL 33131

Tel. (305) 372. 3300 [email protected]

www.robertallenlaw.com