fiat s.p.a. financial statements - fca group · carlo barel di sant’albano ... (pursuant to...

TRANSCRIPT

FIAT S.p.A. Financial Statements (pursuant to Article 2506-ter of the Civil Code) at 30 June 2010

CONTENTS BOARD OF DIRECTORS AND AUDITORS

FIAT S.P.A. FINANCIAL STATEMENTS AT 30 JUNE 2010 (pursuant to Article 2506-ter of the Civil Code) Income statement ……………………………………………………………….……………………………………………….….. 2 Statement of comprehensive income................................................................................................................................. 2 Statement of financial position……………………………………………………………………………………………………… 3 Statement of cash flows……………………………………………………………………………………………………….…….. 4 Statement of changes in equity………………………………………………………………………………………….…………. 5 Notes…………………………………………………………………………………………………………………………….…….. 6

AUDITOR’S REVIEW REPORT ON THE HALF-YEAR CONDENSED SEPARATE FINANCIAL STATEMENTS FOR THE SIX-MONTH PERIOD ENDED JUNE 30, 2010 (PURSUANT TO ARTICLE 2506-TER OF THE CIVIL CODE)……………. 31

This document has been translated into English for the convenience of international readers. The original Italian document should be considered the authoritative version. This Report is available at www.fiatgroup.com

Fiat S.p.A. Registered Office: 250 Via Nizza, Turin, ITALY

Share Capital: €6,377,262,975

Turin Companies Register/Tax Code: 00469580013

BOARD OF DIRECTORS AND AUDITORS

BOARD OF DIRECTORS

Chairman John Elkann (1) (*)

Chief Executive Officer Sergio Marchionne

Directors Andrea Agnelli Carlo Barel di Sant’Albano Roland Berger (3) Tiberto Brandolini d’Adda René Carron Luca Cordero di Montezemolo (**) Luca Garavoglia (1) (3) Gian Maria Gros-Pietro (1) (2) Virgilio Marrone Vittorio Mincato (2) Pasquale Pistorio Ratan Tata Mario Zibetti (2) (3)

Secretary Franzo Grande Stevens

BOARD OF STATUTORY AUDITORS

Regular Auditors Riccardo Perotta – Chairman Giuseppe Camosci Piero Locatelli

Alternate Auditors Lucio Pasquini Fabrizio Mosca Stefano Orlando

INDEPENDENT AUDITORS Deloitte & Touche S.p.A.

(*) Appointed Chairman on 21 April 2010

(**) Resigned as Chairman on 21 April 2010, but remains a member of the Board

(1) Member of the Nominating, Corporate Governance and Sustainability Committee

(2) Member of the Internal Control Committee

(3) Member of the Compensation Committee

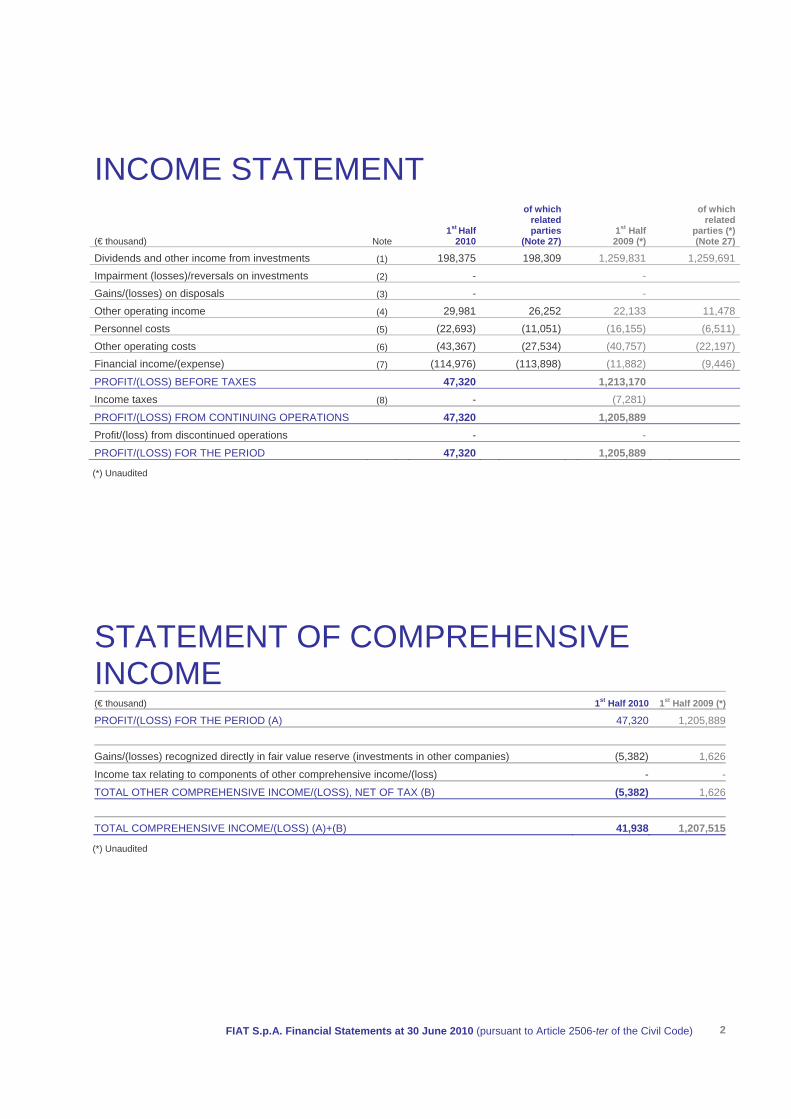

INCOME STATEMENT

(€ thousand) Note 1st Half

2010

of which related parties

(Note 27) 1st Half 2009 (*)

of which related

parties (*) (Note 27)

Dividends and other income from investments (1) 198,375 198,309 1,259,831 1,259,691Impairment (losses)/reversals on investments (2) - - Gains/(losses) on disposals (3) - - Other operating income (4) 29,981 26,252 22,133 11,478Personnel costs (5) (22,693) (11,051) (16,155) (6,511)Other operating costs (6) (43,367) (27,534) (40,757) (22,197)Financial income/(expense) (7) (114,976) (113,898) (11,882) (9,446)

PROFIT/(LOSS) BEFORE TAXES 47,320 1,213,170 Income taxes (8) - (7,281) PROFIT/(LOSS) FROM CONTINUING OPERATIONS 47,320 1,205,889 Profit/(loss) from discontinued operations - - PROFIT/(LOSS) FOR THE PERIOD 47,320 1,205,889

(*) Unaudited

STATEMENT OF COMPREHENSIVE INCOME (€ thousand) 1st Half 2010 1st Half 2009 (*)

PROFIT/(LOSS) FOR THE PERIOD (A) 47,320 1,205,889

Gains/(losses) recognized directly in fair value reserve (investments in other companies) (5,382) 1,626

Income tax relating to components of other comprehensive income/(loss) - -

TOTAL OTHER COMPREHENSIVE INCOME/(LOSS), NET OF TAX (B) (5,382) 1,626

TOTAL COMPREHENSIVE INCOME/(LOSS) (A)+(B) 41,938 1,207,515

(*) Unaudited

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 2

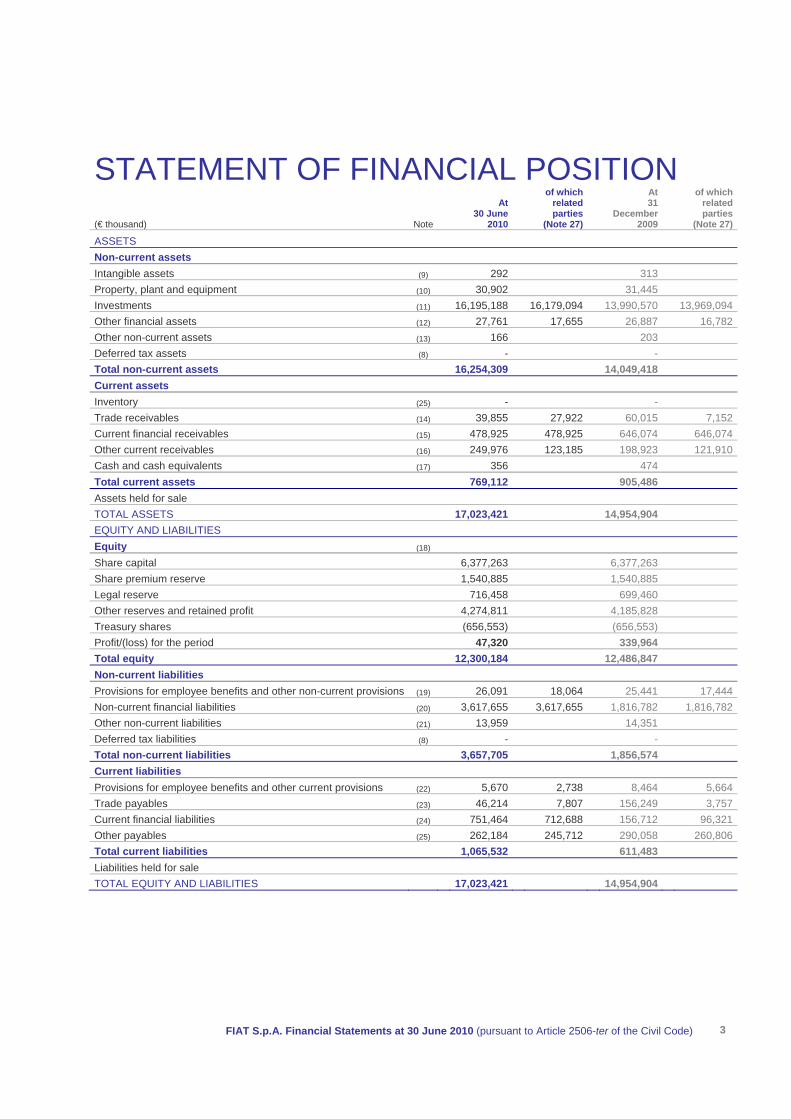

STATEMENT OF FINANCIAL POSITION

(€ thousand) Note

At 30 June

2010

of which related parties

(Note 27)

At 31

December 2009

of which related parties

(Note 27)

ASSETS Non-current assets Intangible assets (9) 292 313 Property, plant and equipment (10) 30,902 31,445 Investments (11) 16,195,188 16,179,094 13,990,570 13,969,094Other financial assets (12) 27,761 17,655 26,887 16,782Other non-current assets (13) 166 203 Deferred tax assets (8) - - Total non-current assets 16,254,309 14,049,418 Current assets Inventory (25) - - Trade receivables (14) 39,855 27,922 60,015 7,152Current financial receivables (15) 478,925 478,925 646,074 646,074Other current receivables (16) 249,976 123,185 198,923 121,910Cash and cash equivalents (17) 356 474 Total current assets 769,112 905,486 Assets held for sale TOTAL ASSETS 17,023,421 14,954,904 EQUITY AND LIABILITIES Equity (18) Share capital 6,377,263 6,377,263 Share premium reserve 1,540,885 1,540,885 Legal reserve 716,458 699,460 Other reserves and retained profit 4,274,811 4,185,828 Treasury shares (656,553) (656,553) Profit/(loss) for the period 47,320 339,964 Total equity 12,300,184 12,486,847 Non-current liabilities Provisions for employee benefits and other non-current provisions (19) 26,091 18,064 25,441 17,444Non-current financial liabilities (20) 3,617,655 3,617,655 1,816,782 1,816,782Other non-current liabilities (21) 13,959 14,351 Deferred tax liabilities (8) - - Total non-current liabilities 3,657,705 1,856,574 Current liabilities Provisions for employee benefits and other current provisions (22) 5,670 2,738 8,464 5,664Trade payables (23) 46,214 7,807 156,249 3,757Current financial liabilities (24) 751,464 712,688 156,712 96,321Other payables (25) 262,184 245,712 290,058 260,806Total current liabilities 1,065,532 611,483 Liabilities held for sale TOTAL EQUITY AND LIABILITIES 17,023,421 14,954,904

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 3

STATEMENT OF CASH FLOWS (€ thousand)

1st Half 2010

of which related parties

1st Half 2009 (*)

of whichrelated

parties (*)

A) CASH AND CASH EQUIVALENTS AT BEGINNING OF THE PERIOD 474 495B) CASH FROM/(USED IN) OPERATING ACTIVITIES:

Profit/(loss) for the period 47,320 1,205,889 Amortization and depreciation 841 872 Non-cash cost of stock option plans 8,518 8,518 4,343 2,924 Impairment losses/(reversals) on investments - - Fair value adjustment to equity swaps on Fiat shares 35,863 35,863 (53,122) (53,122) Losses/(gains) on disposals - - Change in provisions for employee benefits and other provisions (2,144) (2,306) (126) 1,255 Change in deferred taxes - (5,858) Change in working capital (169,157) (33,089) (314,544) (172,872) TOTAL (78,759) 837,454C) CASH FROM/(USED IN) INVESTING ACTIVITIES:

Investment relating to: Recapitalization of subsidiaries (2,209,932) (2,209,932) (5,000) (5,000) Acquisitions (68) (68) - Reductions in investments resulting from:

Capital reductions and distributions of reserves by subsidiaries - - Proceeds from disposals - - Other (investments)/disposals, net (1,151) (128)

TOTAL (2,211,151) (5,128)D) CASH FROM/(USED IN) FINANCING ACTIVITIES:

Change in current financial assets 148,636 148,636 (983,547) (983,547) Change in non-current financial liabilities 1,800,873 1,800,873 - Change in current financial liabilities 577,402 616,367 176,065 (91,194) Increase in share capital - - Purchase of own shares - - Sale of own shares - - Dividends paid (237,119) (66,935) (24,773) TOTAL 2,289,792 (832,255) E) TOTAL CHANGE IN CASH AND CASH EQUIVALENTS (118) 71F) CASH AND CASH EQUIVALENTS AT END OF THE PERIOD 356 566

(*) Unaudited

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 4

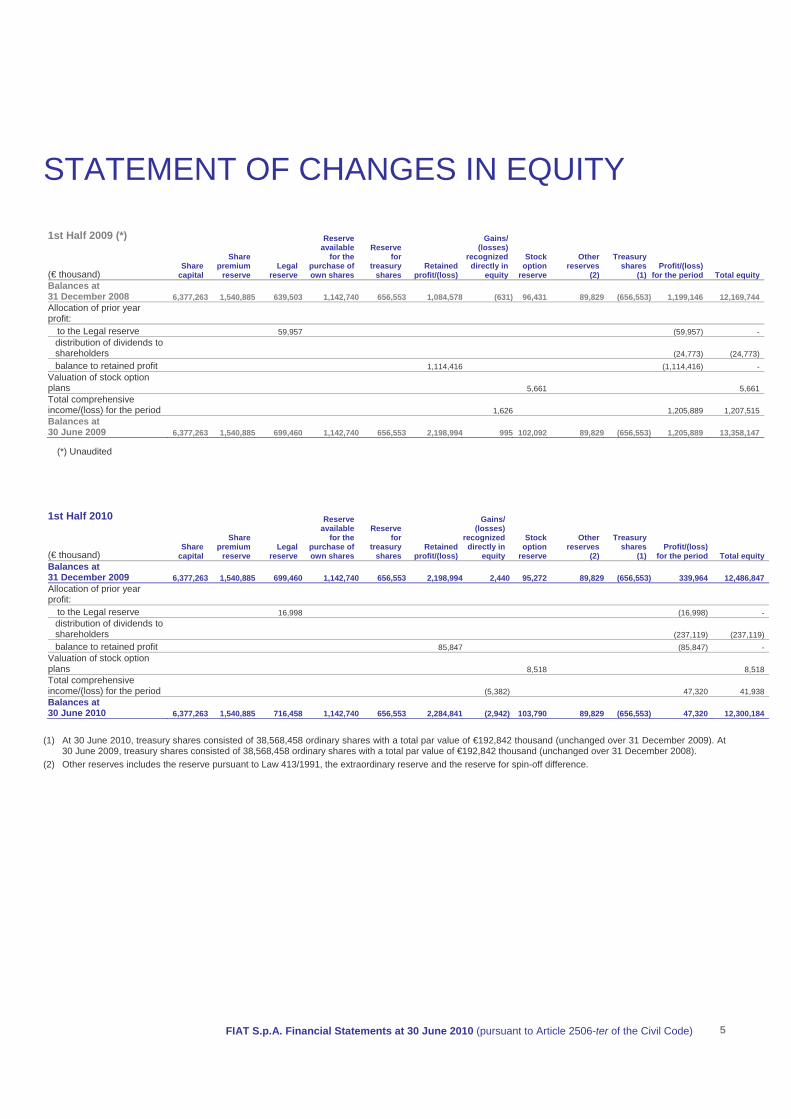

STATEMENT OF CHANGES IN EQUITY 1st Half 2009 (*) (€ thousand)

Share capital

Share premium

reserve Legal

reserve

Reserve available

for the purchase of own shares

Reserve for

treasury shares

Retained profit/(loss)

Gains/ (losses)

recognized directly in

equity

Stock option

reserve

Other reserves

(2)

Treasury shares

(1) Profit/(loss)

for the period Total equity Balances at 31 December 2008 6,377,263 1,540,885 639,503 1,142,740 656,553 1,084,578 (631) 96,431 89,829 (656,553) 1,199,146 12,169,744 Allocation of prior year profit:

to the Legal reserve 59,957 (59,957) - distribution of dividends to shareholders (24,773) (24,773) balance to retained profit 1,114,416 (1,114,416) -

Valuation of stock option plans 5,661 5,661 Total comprehensive income/(loss) for the period 1,626 1,205,889 1,207,515 Balances at 30 June 2009 6,377,263 1,540,885 699,460 1,142,740 656,553 2,198,994 995 102,092 89,829 (656,553) 1,205,889 13,358,147

(*) Unaudited

1st Half 2010 (€ thousand)

Share capital

Share premium

reserve Legal

reserve

Reserve available

for the purchase of own shares

Reserve for

treasury shares

Retained profit/(loss)

Gains/ (losses)

recognized directly in

equity

Stock option

reserve

Other reserves

(2)

Treasury shares

(1) Profit/(loss)

for the period Total equity Balances at 31 December 2009 6,377,263 1,540,885 699,460 1,142,740 656,553 2,198,994 2,440 95,272 89,829 (656,553) 339,964 12,486,847 Allocation of prior year profit:

to the Legal reserve 16,998 (16,998) - distribution of dividends to shareholders (237,119) (237,119) balance to retained profit 85,847 (85,847) -

Valuation of stock option plans 8,518 8,518 Total comprehensive income/(loss) for the period (5,382) 47,320 41,938 Balances at 30 June 2010 6,377,263 1,540,885 716,458 1,142,740 656,553 2,284,841 (2,942) 103,790 89,829 (656,553) 47,320 12,300,184

(1) At 30 June 2010, treasury shares consisted of 38,568,458 ordinary shares with a total par value of €192,842 thousand (unchanged over 31 December 2009). At 30 June 2009, treasury shares consisted of 38,568,458 ordinary shares with a total par value of €192,842 thousand (unchanged over 31 December 2008).

(2) Other reserves includes the reserve pursuant to Law 413/1991, the extraordinary reserve and the reserve for spin-off difference.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 5

NOTES SIGNIFICANT ACCOUNTING POLICIES

Basis of preparation The Fiat S.p.A. Financial Statements at 30 June 2010 have been prepared pursuant to the requirements of Articles 2506-ter and 2501-quater of the Civil Code for the purposes of the partial and proportional demerger of Fiat S.p.A. to Fiat Industrial S.p.A.

This document has been prepared in accordance with the International Financial Reporting Standards ( “IFRS”) issued by the International Accounting Standards Board (“IASB”) and adopted by the European Union. Use of the term IFRS also includes the International Accounting Standards (“IAS”) remaining in effect, as well as all interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”), formerly the Standing Interpretations Committee (“SIC”).

For the Financial Statements at 30 June 2010, prepared in accordance with IAS 34 - Interim Financial Reporting, the accounting principles applied are consistent with those used for the Statutory Financial Statements at 31 December 2009.

Preparation of the interim financial statements requires management to make estimates and assumptions that affect the amounts reported for revenues and expenses, assets and liabilities and the disclosure of contingent assets and liabilities at the interim reporting date. If, in the future, such estimates and assumptions, which are based on management's best judgment, deviate from the actual circumstances, the original estimates and assumptions will be modified as appropriate in the period in which those circumstances change. For a detailed description of the most significant valuation methods used by Fiat S.p.A., please refer to the section entitled "Use of Estimates" in the Statutory Financial Statements at 31 December 2009.

Additionally, some valuations, particularly those of a more complex nature, such as the determination of potential impairment or reversal of impairment losses on non-current assets, are generally only carried out in full during preparation of the annual financial statements when all of the necessary information is available, except where there are indications of impairment or where a previously recognized impairment is no longer applicable, in which case an immediate assessment of the potential impairment or reversal of impairment is required. Similarly, actuarial valuations required for the determination of employee benefit provisions are also usually only carried out during preparation of the annual financial statements.

Recognition of income taxes is based on the best estimate of the weighted average tax rate expected for the full financial year. Fiat S.p.A. and the majority of its Italian subsidiaries have elected to take part in the domestic tax consolidation program pursuant to Articles 117/129 of Presidential Decree 917/1986 (the Italian income tax act). That election was made for an initial three-year period beginning in 2004 (subsequently renewed in 2007 for a further three-year period). The election was renewed again in 2010 for a further minimum three-year period. Fiat S.p.A. acts as the consolidating company and calculates a single taxable base for the group of companies taking part, thereby enabling benefits to be realized from the offsetting of taxable income and tax losses in a single tax return. Each company participating in the consolidation transfers its taxable income or tax loss to the consolidating company. Fiat S.p.A. recognizes receivables from companies contributing taxable income equivalent to the amount of corporate income tax (IRES) payable on their behalf. Conversely, if a company contributes a tax loss to consolidation group, Fiat S.p.A. recognizes a payable to that company equivalent to the amount of the loss actually set off at group level. Please note that the effects of the above procedure for 2010 are not reflected in the Interim Financial Statements, but will be calculated for the annual financial statements at 31 December 2010, when the necessary information is available.

For the purposes of comparison, the statements of income, comprehensive income, cash flows and changes in equity for the six months ended 30 June 2010 also provide data for the same period in 2009, for which there was no requirement to prepare interim financial statements. Data for the first six months of 2009 reflect transactions pertaining to the period, but no adjustments deriving from complex valuations (such as impairments tests on equity investments) have been recognized, as no such valuations were undertaken for the first six months of 2009 given that preparation of interim financial statements was not required. Furthermore, no retrospective valuation of the recoverable amount of investments held at 30 June 2009 was carried out for the purposes of preparing these Financial Statements, as this would have required forward-looking estimates conducted at that time and such retrospective valuations would in any event have been irrelevant to the purpose for which the Financial Statements at 30 June 2010 have been prepared.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 6

Format of the financial statements For the annual financial statements and the interim financial statements at 30 June 2010, the presentation of Fiat S.p.A.’s Income Statement is based on the nature of its revenues and expenses, given the specific activities carried out. The Consolidated Income Statement, however, is classified according to function, which is considered more representative of the internal reporting format used for management of the business sectors and is in line with international practice for the automotive sector. For the Statement of Financial Position, Fiat S.p.A. has elected a “current and non-current” classification for assets and liabilities. A mixed format has, however, been adopted for presentation of the Consolidated Statement of Financial Position, as provided under IAS 1, with assets only being classified between current and non-current. This election was made in view of the fact that the Consolidated Statement of Financial Position includes the activities of both industrial and financial services companies. In the consolidated financial statements, the portfolios of the financial services companies are included under current assets, as they are expected be realized within their normal operating cycle. However, the financial services companies only obtain part of their funding directly from the market. The remaining funding is received from the Group’s treasury companies (included in industrial activities), which provide funding to both industrial companies and financial services companies as required.

Although the distribution of the financial services activities within the Group has no impact on the presentation of liabilities for Fiat S.p.A., a presentation in the Consolidated Statement of Financial Position that distinguishes between current and non-current financial liabilities would not be meaningful.

The Statement of Cash Flows is presented using the indirect method.

Finally, in accordance with the requirements of Consob Resolution 15519 of 27 July 2006, the format adopted for presentation of the Statements of Income, Financial Position and Cash Flows included in the Interim Financial Statements at 30 June 2010 includes an itemized presentation of significant related party transactions.

Accounting principles, amendments and interpretations adopted from 1 January 2010 The Company adopted the following standards, amendments and interpretations from 1 January 2010.

IFRS 3 (2008) – Business Combinations The main changes to IFRS 3 concern: the accounting treatment of step acquisitions; the option between measuring non-controlling interests acquired through a partial acquisition either as their proportionate interest in the net identifiable assets or at fair value; the recognition of acquisition-related costs as an expense in the income statement; the recognition and measurement at fair value at the acquisition date of any contingent consideration included in the arrangements.

The standard now requires the recognition of acquisition-related costs in the separate income statement of the company in the period in which they are incurred. Under the previous version of the standard, by contrast, such costs were included in the purchase cost of the interest acquired.

Adoption of this standard in the first half of 2010 did not, however, result in any accounting impacts as no acquisition-related costs were recognized for the period.

Standards, amendments and interpretations effective from 1 January 2010 but not applicable to the Company The following amendments, improvements and interpretations also become effective from 1 January 2010. They relate to issues that were not applicable to the Company at the date of these interim financial statements, but which may have an impact on the accounting treatment of future transactions or arrangements:

Improvement to IFRS 5 – Non-current Assets Held for Sale and Discontinued Operations. Amendments to IAS 28 – Investments in Associates and IAS 31 – Interests in Joint Ventures consequential to

the amendment to IAS 27. Improvements to IAS/IFRS (2009). Amendments to IFRS 2 – Share based Payment: Group Cash-settled Share-based Payment Transactions. nIFRIC 17 – Distributions of Non-cash Assets to Ow ers. IFRIC 18 – Transfers of Assets from Customers. Amendment to IAS 39 – Financial Instruments: Recognition and Measurement: Eligible Hedged items.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 7

Accounting principles, amendments and interpretations not yet applicable and not early adopted by the Company On 8 October 2009, the IASB issued an amendment to IAS 32 – Financial Instruments: Presentation, Classification of Rights Issues to address the accounting for rights issues (rights, options or warrants) that are denominated in a currency other than the functional currency of the issuer. Previously such rights issues were accounted for as derivative liabilities. However, the amendment requires that, provided certain conditions are met, such rights issues are classified as equity regardless of the currency in which the exercise price is denominated. The amendment is applicable retrospectively from 1 January 2011. Adoption of this amendment is not expected to lead to any impacts on the Company’s financial statements.

On 4 November 2009, the IASB issued a revised version of IAS 24 - Related Party Disclosures that simplifies the disclosure requirements for government-related entities and clarifies the definition of a related party. The revised standard is effective for annual periods beginning on or after 1 January 2011. The revised standard had not yet been endorsed by the European Union at the date of these interim financial statements.

On 12 November 2009, the IASB issued IFRS 9 – Financial Instruments which addresses the classification and measurement of financial assets, having an effective date for mandatory adoption of 1 January 2013. The new standard represents the completion of the first part of a project to replace IAS 39. The new standard uses a single approach to determine whether a financial asset is measured at amortized cost or fair value, replacing the many different rules in IAS 39. The approach in IFRS 9 is based on how an entity manages its financial instruments and the contractual cash flow characteristics of the financial assets. IFRS 9 also requires a single impairment method to be used. The new standard had not yet been endorsed by the European Union at the date of these interim financial statements.

On 26 November 2009, the IASB issued a minor amendment to IFRIC 14 - Prepayments of a Minimum Funding Requirement. The amendment applies when an entity is subject to minimum funding requirements and makes an early payment of contributions to cover those requirements. The amendment permits an entity to treat the benefit of such early payment as an asset. Adoption of the amendment is mandatory from 1 January 2011. The amendment had not yet been endorsed by the European Union at the date of these interim financial statements.

On 26 November 2009, IFRIC issued the interpretation IFRIC 19 – Extinguishing Financial Liabilities with Equity Instruments that provides guidance on how to account for the extinguishment of a financial liability through the issue of equity instruments. The interpretation clarifies that when an entity renegotiates the terms of a financial liability with its creditor and the creditor agrees to accept the entity’s shares or other equity instruments to settle the financial liability fully or partially, then the entity’s equity instruments issued to a creditor are part of the consideration paid to extinguish the financial liability and are measured at their fair value. The difference between the carrying amount of the financial liability extinguished and initial measurement of the equity instruments issued is recognized in the profit or loss for the period. Adoption of the interpretation is mandatory from 1 January 2011. The interpretation had not yet been endorsed by the European Union at the date of these interim financial statements.

On 6 May 2010 the IASB issued a set of amendments to IFRSs (“Improvements to IFRSs”) that are applicable from 1 January 2011; set out below are those that may lead to changes in the presentation, recognition or measurement of items in the financial statements, excluding those that only relate to changes in terminology or editorial changes having a limited accounting effect and those that affect standards or interpretations that are not applicable to the Company.

IFRS 1 – First-time Adoption of International Financial Reporting Standards: this amendment clarifies that if an entity has to measure its assets at fair value due to a special event such as an IPO or a privatization in accordance with local law, the revalued amount may also be used in preparation of the IFRS financial statements even if the company had already determined the fair value of assets and liabilities existing at the date of transition to IFRSs. IFRS 3 (2008) – Business Combinations: this amendment clarifies that the components of non-controlling interests

that do not entitle their holders to a proportionate share of the entity’s net assets must be measured at fair value or as required by the applicable accounting standards. For example, stock options granted to employees must be measured in accordance with the requirements of IFRS 2 in the case of a business combination, while the equity portion of a convertible debt instrument must be measured in accordance with IAS 32. In addition, the Board goes into further detail on the question of share-based payment plans that are replaced as part of a business combination by adding specific guidance to clarify the accounting treatment. IFRS 7 – Financial Instruments: Disclosures: this amendment emphasizes the interaction between the qualitative

and quantitative disclosures required by the standard concerning the nature and extent of risks arising from financial instruments. This should assist users of financial statements to link related disclosures and hence form an overall picture of the nature and extent of risks arising from financial statements. In addition, the disclosure requirement concerning financial assets that are past due or impaired but whose terms have been renegotiated, and that relating to the fair value of collateral, have been eliminated.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 8

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 9

IAS 1 – Presentation of Financial Statements: The amendment requires reconciliation in the changes of each component of equity to be presented in the notes or in the primary statements. IAS 34 – Interim Financial Reporting: By using a series of examples certain clarifications are provided concerning

the additional disclosures that must be provided in interim financial reports. At the date of these interim financial statements, the competent bodies of the European Union had not yet completed the endorsement process for the above improvements.

COMPOSITION AND PRINCIPAL CHANGES

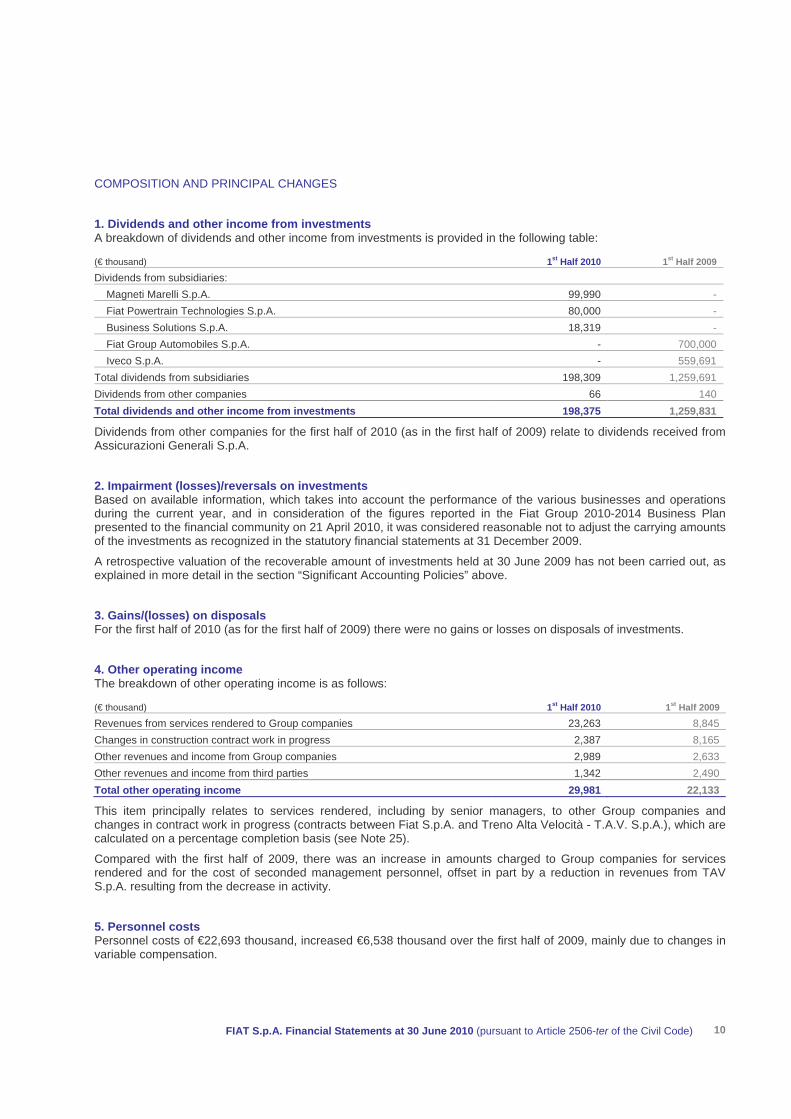

1. Dividends and other income from investments A breakdown of dividends and other income from investments is provided in the following table:

(€ thousand) 1st Half 2010 1st Half 2009

Dividends from subsidiaries: Magneti Marelli S.p.A. 99,990 - Fiat Powertrain Technologies S.p.A. 80,000 - Business Solutions S.p.A. 18,319 - Fiat Group Automobiles S.p.A. - 700,000 Iveco S.p.A. - 559,691 Total dividends from subsidiaries 198,309 1,259,691 Dividends from other companies 66 140 Total dividends and other income from investments 198,375 1,259,831

Dividends from other companies for the first half of 2010 (as in the first half of 2009) relate to dividends received from Assicurazioni Generali S.p.A.

2. Impairment (losses)/reversals on investments Based on available information, which takes into account the performance of the various businesses and operations during the current year, and in consideration of the figures reported in the Fiat Group 2010-2014 Business Plan presented to the financial community on 21 April 2010, it was considered reasonable not to adjust the carrying amounts of the investments as recognized in the statutory financial statements at 31 December 2009.

A retrospective valuation of the recoverable amount of investments held at 30 June 2009 has not been carried out, as explained in more detail in the section “Significant Accounting Policies” above.

3. Gains/(losses) on disposals For the first half of 2010 (as for the first half of 2009) there were no gains or losses on disposals of investments.

4. Other operating income The breakdown of other operating income is as follows:

(€ thousand) 1st Half 2010 1st Half 2009

Revenues from services rendered to Group companies 23,263 8,845 Changes in construction contract work in progress 2,387 8,165 Other revenues and income from Group companies 2,989 2,633 Other revenues and income from third parties 1,342 2,490 Total other operating income 29,981 22,133

This item principally relates to services rendered, including by senior managers, to other Group companies and changes in contract work in progress (contracts between Fiat S.p.A. and Treno Alta Velocità - T.A.V. S.p.A.), which are calculated on a percentage completion basis (see Note 25).

Compared with the first half of 2009, there was an increase in amounts charged to Group companies for services rendered and for the cost of seconded management personnel, offset in part by a reduction in revenues from TAV S.p.A. resulting from the decrease in activity.

5. Personnel costs Personnel costs of €22,693 thousand, increased €6,538 thousand over the first half of 2009, mainly due to changes in variable compensation.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 10

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 11

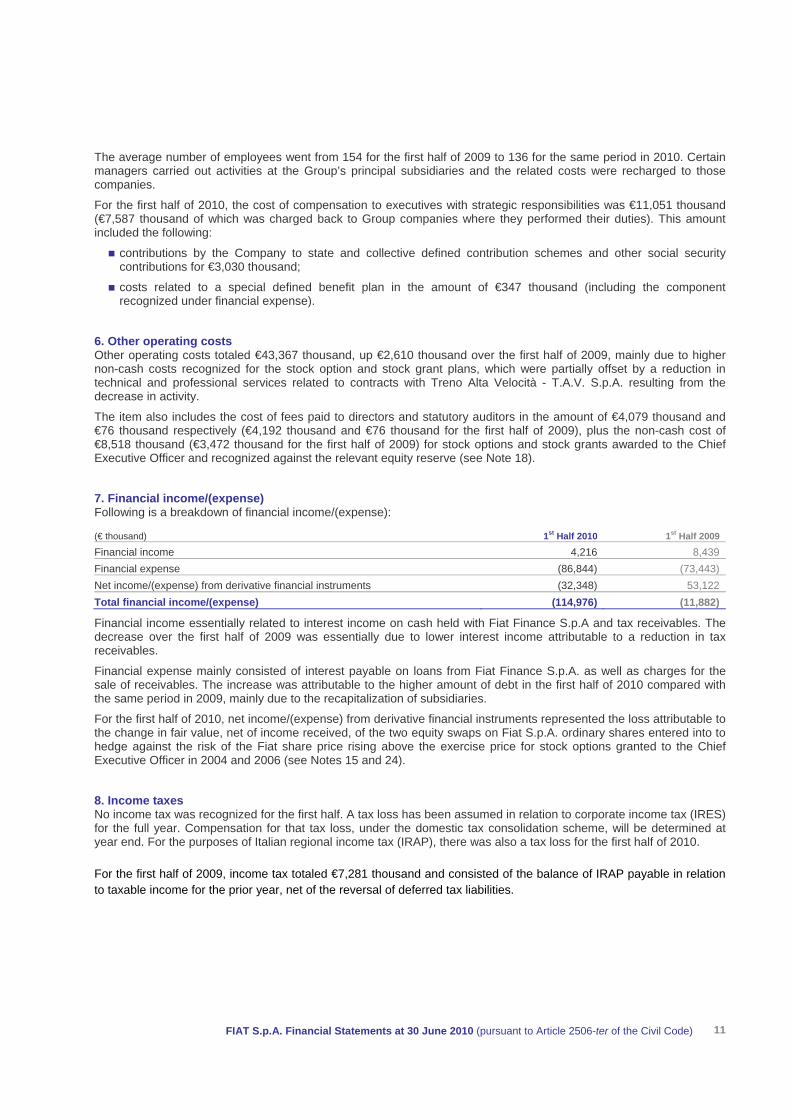

The average number of employees went from 154 for the first half of 2009 to 136 for the same period in 2010. Certain managers carried out activities at the Group’s principal subsidiaries and the related costs were recharged to those companies.

For the first half of 2010, the cost of compensation to executives with strategic responsibilities was €11,051 thousand (€7,587 thousand of which was charged back to Group companies where they performed their duties). This amount included the following:

contributions by the Company to state and collective defined contribution schemes and other social security contributions for €3,030 thousand;

costs related to a special defined benefit plan in the amount of €347 thousand (including the component recognized under financial expense).

6. Other operating costs Other operating costs totaled €43,367 thousand, up €2,610 thousand over the first half of 2009, mainly due to higher non-cash costs recognized for the stock option and stock grant plans, which were partially offset by a reduction in technical and professional services related to contracts with Treno Alta Velocità - T.A.V. S.p.A. resulting from the decrease in activity.

The item also includes the cost of fees paid to directors and statutory auditors in the amount of €4,079 thousand and €76 thousand respectively (€4,192 thousand and €76 thousand for the first half of 2009), plus the non-cash cost of €8,518 thousand (€3,472 thousand for the first half of 2009) for stock options and stock grants awarded to the Chief Executive Officer and recognized against the relevant equity reserve (see Note 18).

7. Financial income/(expense) Following is a breakdown of financial income/(expense):

(€ thousand) 1st Half 2010 1st Half 2009

Financial income 4,216 8,439 Financial expense (86,844) (73,443) Net income/(expense) from derivative financial instruments (32,348) 53,122 Total financial income/(expense) (114,976) (11,882)

Financial income essentially related to interest income on cash held with Fiat Finance S.p.A and tax receivables. The decrease over the first half of 2009 was essentially due to lower interest income attributable to a reduction in tax receivables.

Financial expense mainly consisted of interest payable on loans from Fiat Finance S.p.A. as well as charges for the sale of receivables. The increase was attributable to the higher amount of debt in the first half of 2010 compared with the same period in 2009, mainly due to the recapitalization of subsidiaries.

For the first half of 2010, net income/(expense) from derivative financial instruments represented the loss attributable to the change in fair value, net of income received, of the two equity swaps on Fiat S.p.A. ordinary shares entered into to hedge against the risk of the Fiat share price rising above the exercise price for stock options granted to the Chief Executive Officer in 2004 and 2006 (see Notes 15 and 24).

8. Income taxes No income tax was recognized for the first half. A tax loss has been assumed in relation to corporate income tax (IRES) for the full year. Compensation for that tax loss, under the domestic tax consolidation scheme, will be determined at year end. For the purposes of Italian regional income tax (IRAP), there was also a tax loss for the first half of 2010.

For the first half of 2009, income tax totaled €7,281 thousand and consisted of the balance of IRAP payable in relation to taxable income for the prior year, net of the reversal of deferred tax liabilities.

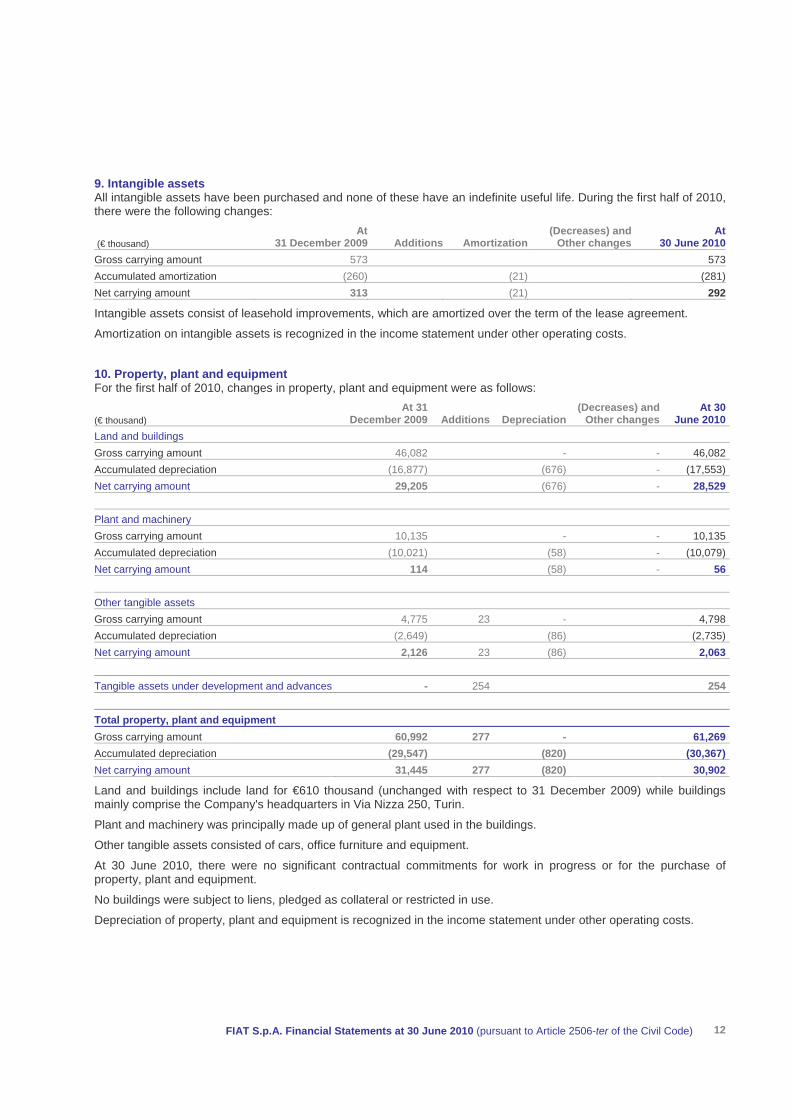

9. Intangible assets All intangible assets have been purchased and none of these have an indefinite useful life. During the first half of 2010, there were the following changes:

(€ thousand) At

31 December 2009 Additions Amortization(Decreases) and

Other changesAt

30 June 2010Gross carrying amount 573 573Accumulated amortization (260) (21) (281)Net carrying amount 313 (21) 292

Intangible assets consist of leasehold improvements, which are amortized over the term of the lease agreement.

Amortization on intangible assets is recognized in the income statement under other operating costs.

10. Property, plant and equipment For the first half of 2010, changes in property, plant and equipment were as follows:

(€ thousand) At 31

December 2009 Additions Depreciation (Decreases) and

Other changesAt 30

June 2010Land and buildings Gross carrying amount 46,082 - - 46,082Accumulated depreciation (16,877) (676) - (17,553)Net carrying amount 29,205 (676) - 28,529 Plant and machinery Gross carrying amount 10,135 - - 10,135Accumulated depreciation (10,021) (58) - (10,079)Net carrying amount 114 (58) - 56 Other tangible assets Gross carrying amount 4,775 23 - 4,798Accumulated depreciation (2,649) (86) (2,735)Net carrying amount 2,126 23 (86) 2,063 Tangible assets under development and advances - 254 254 Total property, plant and equipment Gross carrying amount 60,992 277 - 61,269Accumulated depreciation (29,547) (820) (30,367)Net carrying amount 31,445 277 (820) 30,902

Land and buildings include land for €610 thousand (unchanged with respect to 31 December 2009) while buildings mainly comprise the Company's headquarters in Via Nizza 250, Turin.

Plant and machinery was principally made up of general plant used in the buildings.

Other tangible assets consisted of cars, office furniture and equipment.

At 30 June 2010, there were no significant contractual commitments for work in progress or for the purchase of property, plant and equipment.

No buildings were subject to liens, pledged as collateral or restricted in use.

Depreciation of property, plant and equipment is recognized in the income statement under other operating costs.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 12

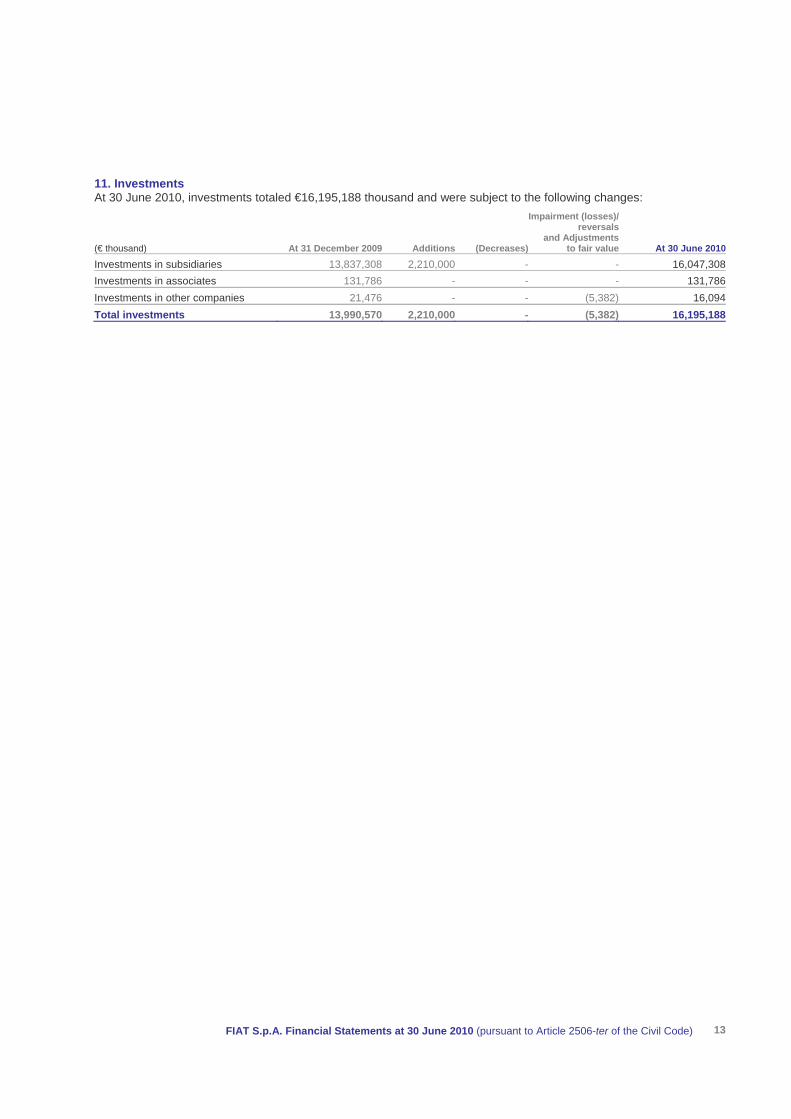

11. Investments At 30 June 2010, investments totaled €16,195,188 thousand and were subject to the following changes:

(€ thousand) At 31 December 2009 Additions (Decreases)

Impairment (losses)/reversals

and Adjustments to fair value At 30 June 2010

Investments in subsidiaries 13,837,308 2,210,000 - - 16,047,308Investments in associates 131,786 - - - 131,786Investments in other companies 21,476 - - (5,382) 16,094Total investments 13,990,570 2,210,000 - (5,382) 16,195,188

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 13

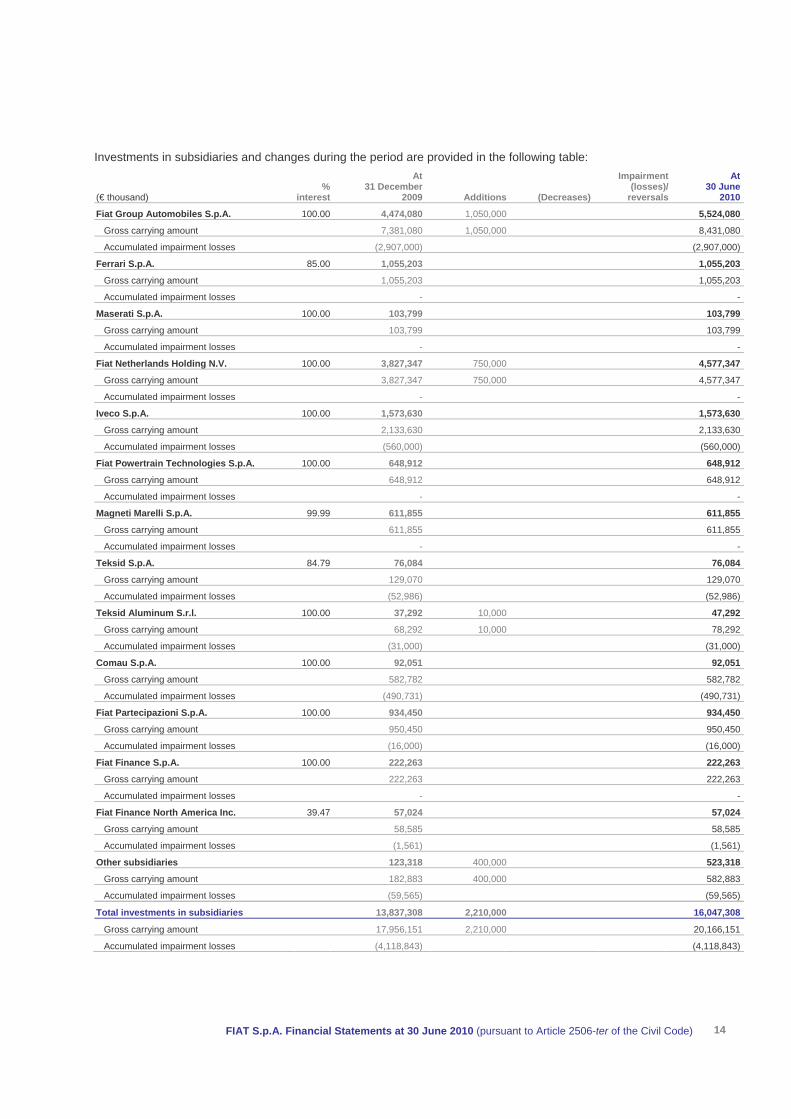

Investments in subsidiaries and changes during the period are provided in the following table:

(€ thousand) %

interest

At 31 December

2009 Additions (Decreases)

Impairment (losses)/

reversals

At 30 June

2010

Fiat Group Automobiles S.p.A. 100.00 4,474,080 1,050,000 5,524,080

Gross carrying amount 7,381,080 1,050,000 8,431,080

Accumulated impairment losses (2,907,000) (2,907,000)

Ferrari S.p.A. 85.00 1,055,203 1,055,203

Gross carrying amount 1,055,203 1,055,203

Accumulated impairment losses - -

Maserati S.p.A. 100.00 103,799 103,799

Gross carrying amount 103,799 103,799

Accumulated impairment losses - -

Fiat Netherlands Holding N.V. 100.00 3,827,347 750,000 4,577,347

Gross carrying amount 3,827,347 750,000 4,577,347

Accumulated impairment losses - -

Iveco S.p.A. 100.00 1,573,630 1,573,630

Gross carrying amount 2,133,630 2,133,630

Accumulated impairment losses (560,000) (560,000)

Fiat Powertrain Technologies S.p.A. 100.00 648,912 648,912

Gross carrying amount 648,912 648,912

Accumulated impairment losses - -

Magneti Marelli S.p.A. 99.99 611,855 611,855

Gross carrying amount 611,855 611,855

Accumulated impairment losses - -

Teksid S.p.A. 84.79 76,084 76,084

Gross carrying amount 129,070 129,070

Accumulated impairment losses (52,986) (52,986)

Teksid Aluminum S.r.l. 100.00 37,292 10,000 47,292

Gross carrying amount 68,292 10,000 78,292

Accumulated impairment losses (31,000) (31,000)

Comau S.p.A. 100.00 92,051 92,051

Gross carrying amount 582,782 582,782

Accumulated impairment losses (490,731) (490,731)

Fiat Partecipazioni S.p.A. 100.00 934,450 934,450

Gross carrying amount 950,450 950,450

Accumulated impairment losses (16,000) (16,000)

Fiat Finance S.p.A. 100.00 222,263 222,263

Gross carrying amount 222,263 222,263

Accumulated impairment losses - -

Fiat Finance North America Inc. 39.47 57,024 57,024

Gross carrying amount 58,585 58,585

Accumulated impairment losses (1,561) (1,561)

Other subsidiaries 123,318 400,000 523,318

Gross carrying amount 182,883 400,000 582,883

Accumulated impairment losses (59,565) (59,565)

Total investments in subsidiaries 13,837,308 2,210,000 16,047,308

Gross carrying amount 17,956,151 2,210,000 20,166,151

Accumulated impairment losses (4,118,843) (4,118,843)

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 14

Changes to investments in subsidiaries during the first half of 2010 included capital contributions of €1,050 million to Fiat Group Automobiles S.p.A., €750 million to Fiat Netherlands Holding N.V. and €10 million to Teksid Aluminum S.r.l. to strengthen the capital structure of these subsidiaries.

Also of note in the first half of 2010 was the purchase from Fiat Partecipazioni S.p.A. and subsequent capital increase of the subsidiaries Nuove Iniziative Finanziarie Cinque S.p.A. and Nuova Immobiliare Nove S.p.A. (both currently inactive), in the amount of €200 million and €100 million respectively, and the incorporation of the subsidiary Fiat Industrial Finance S.p.A., also capitalized in the amount of €100 million. These transactions are linked to the envisaged demerger from Fiat S.p.A. to Fiat Industrial S.p.A. of shareholdings representing the capital goods businesses (agricultural and construction equipment, trucks and commercial vehicles, and the industrial & marine activities of the FPT Powertrain Technologies Sector).

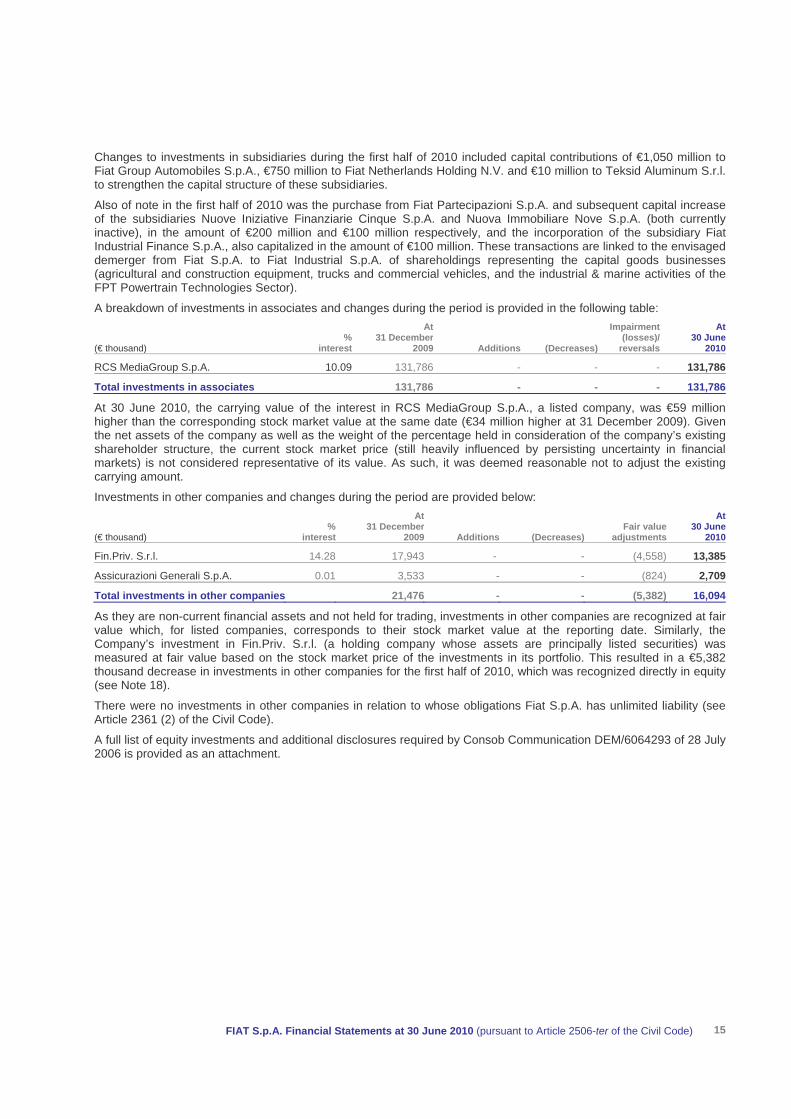

A breakdown of investments in associates and changes during the period is provided in the following table:

(€ thousand) %

interest

At31 December

2009 Additions (Decreases)

Impairment (losses)/

reversals

At30 June

2010

RCS MediaGroup S.p.A. 10.09 131,786 - - - 131,786

Total investments in associates 131,786 - - - 131,786

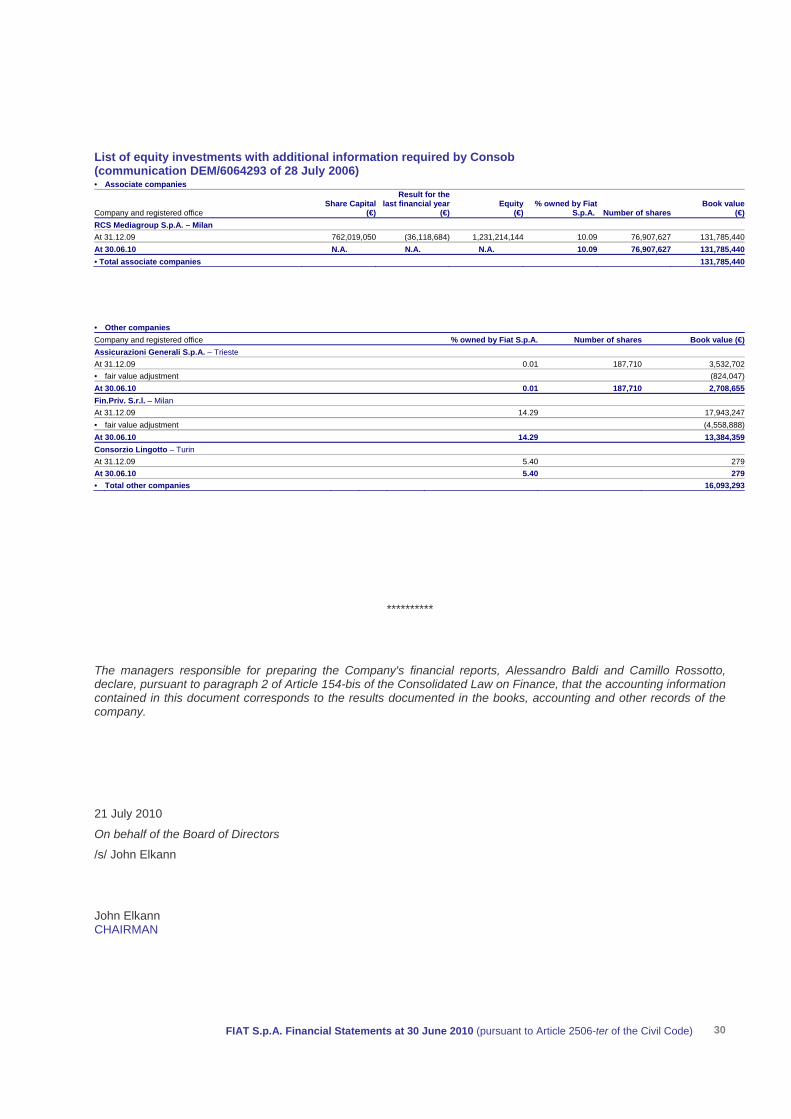

At 30 June 2010, the carrying value of the interest in RCS MediaGroup S.p.A., a listed company, was €59 million higher than the corresponding stock market value at the same date (€34 million higher at 31 December 2009). Given the net assets of the company as well as the weight of the percentage held in consideration of the company’s existing shareholder structure, the current stock market price (still heavily influenced by persisting uncertainty in financial markets) is not considered representative of its value. As such, it was deemed reasonable not to adjust the existing carrying amount.

Investments in other companies and changes during the period are provided below:

(€ thousand) %

interest

At31 December

2009 Additions (Decreases)Fair value

adjustments

At30 June

2010

Fin.Priv. S.r.l. 14.28 17,943 - - (4,558) 13,385

Assicurazioni Generali S.p.A. 0.01 3,533 - - (824) 2,709

Total investments in other companies 21,476 - - (5,382) 16,094

As they are non-current financial assets and not held for trading, investments in other companies are recognized at fair value which, for listed companies, corresponds to their stock market value at the reporting date. Similarly, the Company’s investment in Fin.Priv. S.r.l. (a holding company whose assets are principally listed securities) was measured at fair value based on the stock market price of the investments in its portfolio. This resulted in a €5,382 thousand decrease in investments in other companies for the first half of 2010, which was recognized directly in equity (see Note 18).

There were no investments in other companies in relation to whose obligations Fiat S.p.A. has unlimited liability (see Article 2361 (2) of the Civil Code).

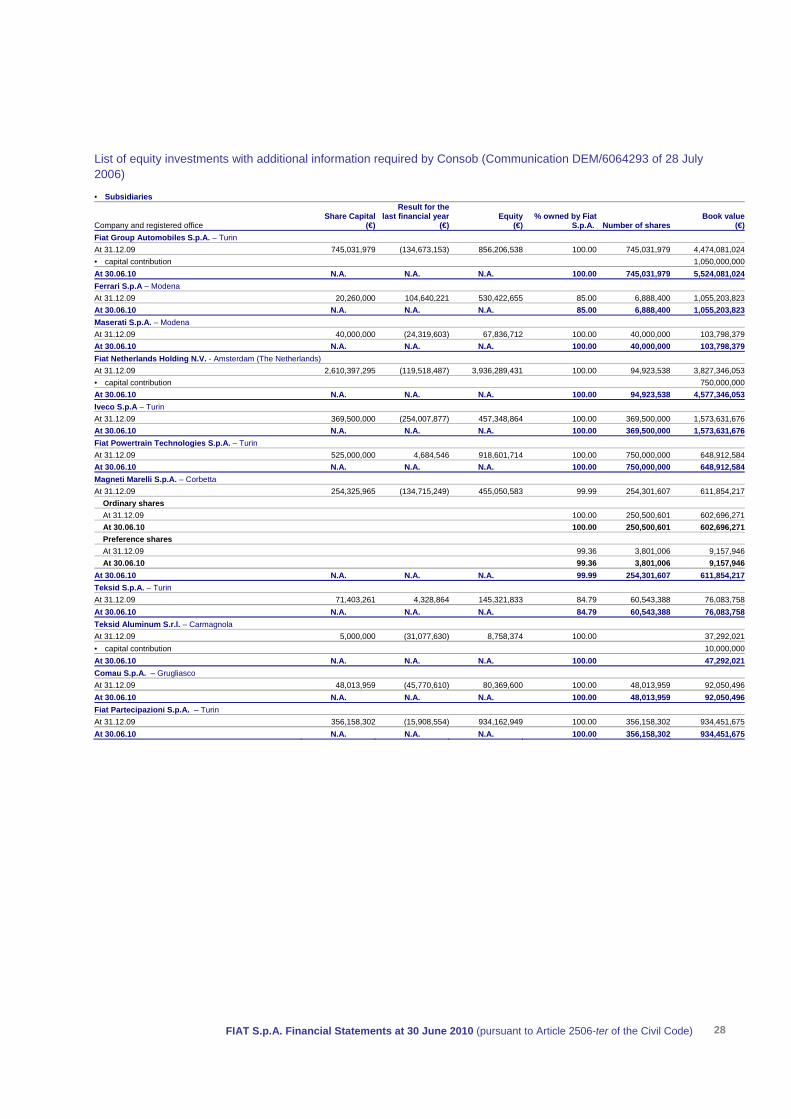

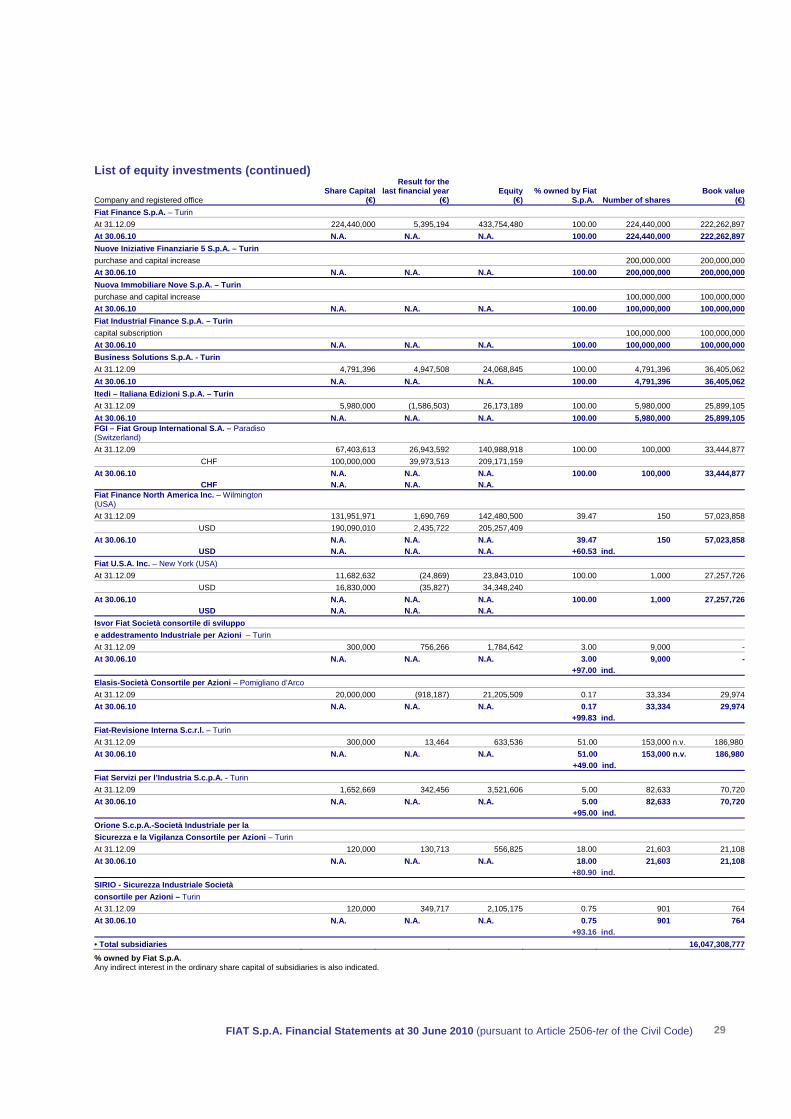

A full list of equity investments and additional disclosures required by Consob Communication DEM/6064293 of 28 July 2006 is provided as an attachment.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 15

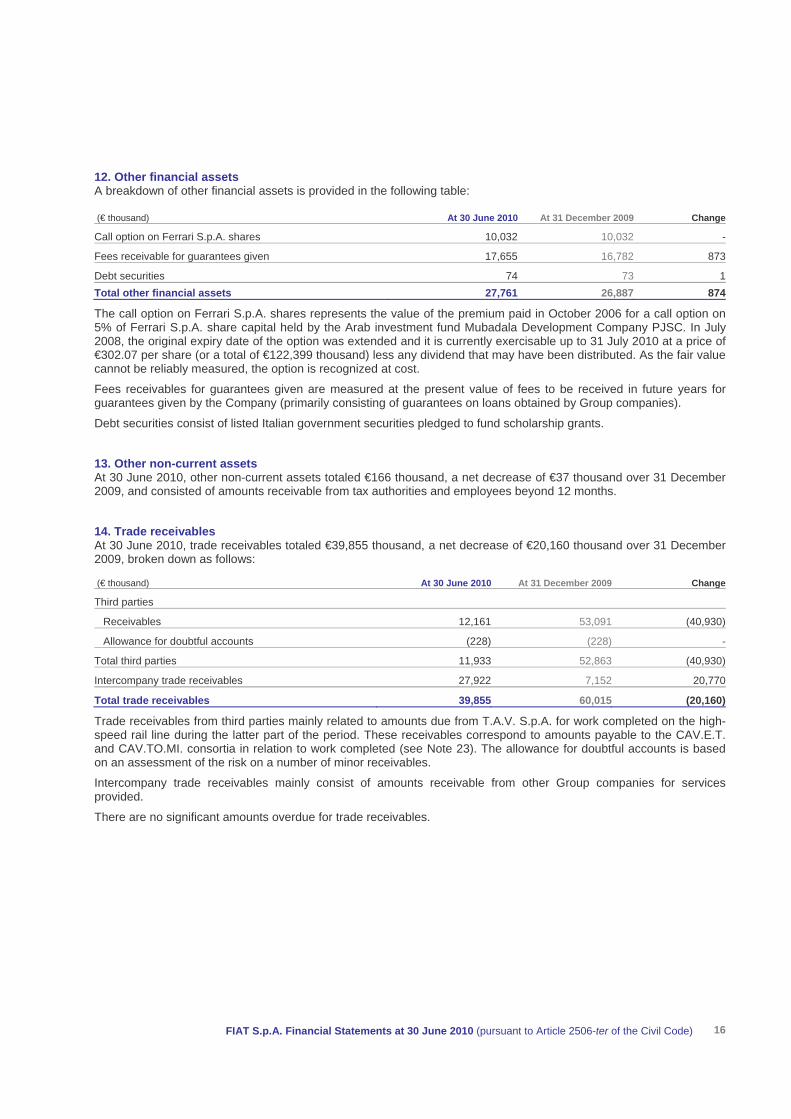

12. Other financial assets A breakdown of other financial assets is provided in the following table:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Call option on Ferrari S.p.A. shares 10,032 10,032 -

Fees receivable for guarantees given 17,655 16,782 873

Debt securities 74 73 1Total other financial assets 27,761 26,887 874

The call option on Ferrari S.p.A. shares represents the value of the premium paid in October 2006 for a call option on 5% of Ferrari S.p.A. share capital held by the Arab investment fund Mubadala Development Company PJSC. In July 2008, the original expiry date of the option was extended and it is currently exercisable up to 31 July 2010 at a price of €302.07 per share (or a total of €122,399 thousand) less any dividend that may have been distributed. As the fair value cannot be reliably measured, the option is recognized at cost.

Fees receivables for guarantees given are measured at the present value of fees to be received in future years for guarantees given by the Company (primarily consisting of guarantees on loans obtained by Group companies).

Debt securities consist of listed Italian government securities pledged to fund scholarship grants.

13. Other non-current assets At 30 June 2010, other non-current assets totaled €166 thousand, a net decrease of €37 thousand over 31 December 2009, and consisted of amounts receivable from tax authorities and employees beyond 12 months.

14. Trade receivables At 30 June 2010, trade receivables totaled €39,855 thousand, a net decrease of €20,160 thousand over 31 December 2009, broken down as follows:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Third parties

Receivables 12,161 53,091 (40,930)

Allowance for doubtful accounts (228) (228) -

Total third parties 11,933 52,863 (40,930)

Intercompany trade receivables 27,922 7,152 20,770

Total trade receivables 39,855 60,015 (20,160)

Trade receivables from third parties mainly related to amounts due from T.A.V. S.p.A. for work completed on the high-speed rail line during the latter part of the period. These receivables correspond to amounts payable to the CAV.E.T. and CAV.TO.MI. consortia in relation to work completed (see Note 23). The allowance for doubtful accounts is based on an assessment of the risk on a number of minor receivables.

Intercompany trade receivables mainly consist of amounts receivable from other Group companies for services provided.

There are no significant amounts overdue for trade receivables.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 16

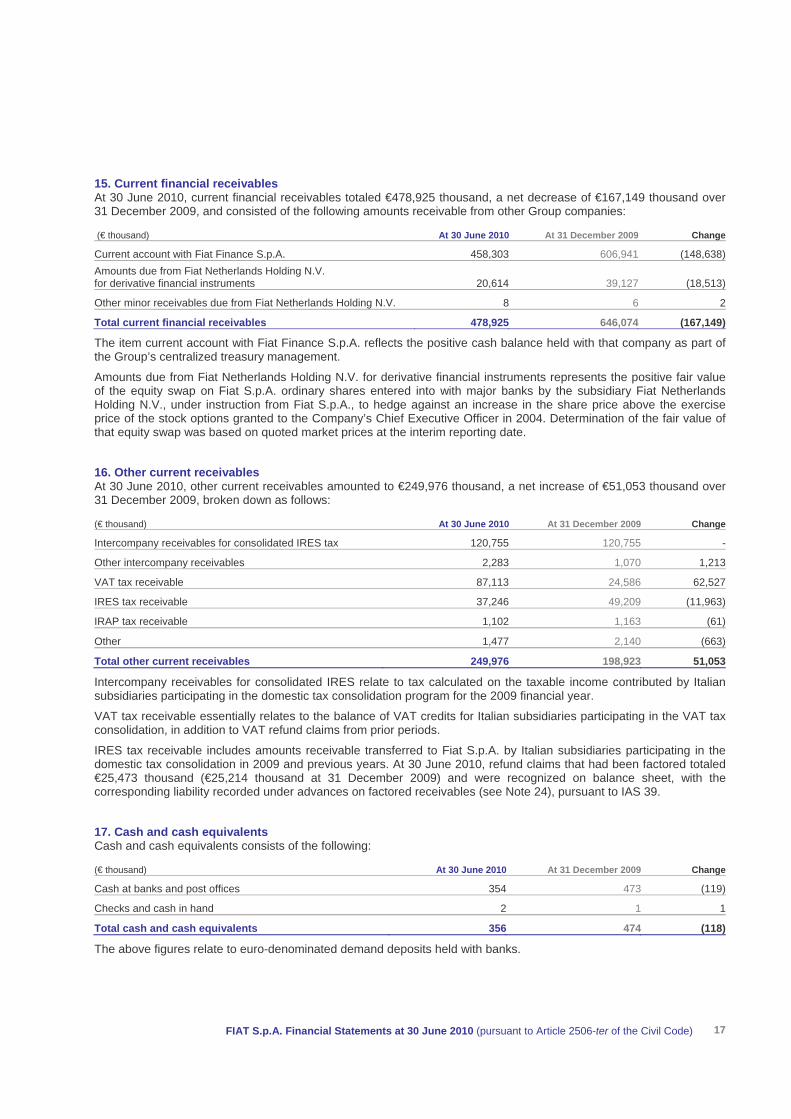

15. Current financial receivables At 30 June 2010, current financial receivables totaled €478,925 thousand, a net decrease of €167,149 thousand over 31 December 2009, and consisted of the following amounts receivable from other Group companies:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Current account with Fiat Finance S.p.A. 458,303 606,941 (148,638)Amounts due from Fiat Netherlands Holding N.V. for derivative financial instruments 20,614 39,127 (18,513)

Other minor receivables due from Fiat Netherlands Holding N.V. 8 6 2

Total current financial receivables 478,925 646,074 (167,149)

The item current account with Fiat Finance S.p.A. reflects the positive cash balance held with that company as part of the Group’s centralized treasury management.

Amounts due from Fiat Netherlands Holding N.V. for derivative financial instruments represents the positive fair value of the equity swap on Fiat S.p.A. ordinary shares entered into with major banks by the subsidiary Fiat Netherlands Holding N.V., under instruction from Fiat S.p.A., to hedge against an increase in the share price above the exercise price of the stock options granted to the Company’s Chief Executive Officer in 2004. Determination of the fair value of that equity swap was based on quoted market prices at the interim reporting date.

16. Other current receivables At 30 June 2010, other current receivables amounted to €249,976 thousand, a net increase of €51,053 thousand over 31 December 2009, broken down as follows:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Intercompany receivables for consolidated IRES tax 120,755 120,755 -

Other intercompany receivables 2,283 1,070 1,213

VAT tax receivable 87,113 24,586 62,527

IRES tax receivable 37,246 49,209 (11,963)

IRAP tax receivable 1,102 1,163 (61)

Other 1,477 2,140 (663)

Total other current receivables 249,976 198,923 51,053

Intercompany receivables for consolidated IRES relate to tax calculated on the taxable income contributed by Italian subsidiaries participating in the domestic tax consolidation program for the 2009 financial year.

VAT tax receivable essentially relates to the balance of VAT credits for Italian subsidiaries participating in the VAT tax consolidation, in addition to VAT refund claims from prior periods.

IRES tax receivable includes amounts receivable transferred to Fiat S.p.A. by Italian subsidiaries participating in the domestic tax consolidation in 2009 and previous years. At 30 June 2010, refund claims that had been factored totaled €25,473 thousand (€25,214 thousand at 31 December 2009) and were recognized on balance sheet, with the corresponding liability recorded under advances on factored receivables (see Note 24), pursuant to IAS 39.

17. Cash and cash equivalents Cash and cash equivalents consists of the following:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Cash at banks and post offices 354 473 (119)

Checks and cash in hand 2 1 1

Total cash and cash equivalents 356 474 (118)

The above figures relate to euro-denominated demand deposits held with banks.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 17

18. Equity At 30 June 2010, equity totaled €12,300,184 thousand, a €186,663 thousand decrease over 31 December 2009, primarily attributable to dividend distributions totaling €237,119 thousand (€0.17 per ordinary share, €0.31 per preference share and €0.325 per savings share), net of profit for the period of €47,320 thousand.

Share capital At 30 June 2010, share capital totaled €6,377,263 thousand (fully paid) and consisted of the following:

(no. of shares) At 30 June 2010 At 31 December 2009

Shares issued and fully paid-up

Ordinary shares 1,092,247,485 1,092,247,485

Preference shares 103,292,310 103,292,310

Savings shares 79,912,800 79,912,800

Total shares issued 1,275,452,595 1,275,452,595

All issued shares have a par value of €5.00 each.

For more detailed information on the share capital of Fiat S.p.A., refer to Note 19 of the Statutory Financial Statements at 31 December 2009.

Share premium reserve At 30 June 2010, this reserve totaled €1,540,885 thousand and was unchanged from 31 December 2009.

Legal reserve At 30 June 2010, this reserve totaled €716,458 thousand, an increase of €16,998 thousand over 31 December 2009 following allocation of profit for the prior year, as approved by Shareholders on 26 March 2010.

Reserve available for the purchase of own shares This reserve was created through a transfer from the retained profit/(loss) reserve, following authorization of the share buy-back program (the "Program") by Shareholders on 5 April 2007 and subsequently renewed on 31 March 2008. Pursuant to that Program, purchases were carried out on regulated markets in accordance with the following conditions:

the Program was to expire on 30 September 2009 or, in any event, once a maximum purchase amount of €1.8 billion (including the value of Fiat S.p.A. shares already held by the Company) or a number of shares equivalent to 10% of share capital had been reached;

the maximum purchase price could not exceed the reference price reported by the Stock Exchange on the date before the purchase was made by more than 10%;

for each share class, the maximum number of shares purchased daily could not exceed 20% of the total daily trading volume.

Although this share buy-back program has been placed on hold, in order to maintain the necessary operating flexibility over an adequate time period, at the General Meeting of 26 March 2010 Shareholders renewed their authorization for the purchase and disposal of own shares, including transactions carried out through subsidiary companies, at the same time revoking the authorization given in the General Meeting of 27 March 2009, to the extent not already exercised. The new authorization is for the purchase of a maximum number of shares, for all three classes combined, not to exceed 10% of share capital or a purchase value of €1.8 billion, inclusive of the €656.6 million in Fiat shares already held by the Company.

At 21 July 2010, the total number of ordinary shares purchased since the beginning of the Program was 37.27 million, for a total invested amount of €665 million.

The reserve for the purchase of own shares totaled €1,142,740 thousand at 30 June 2010, unchanged from 31 December 2009.

As mentioned above, the resolution passed by Shareholders on 26 March 2010 revoked the existing authorization for share buy-backs to the extent not already exercised, equivalent to €1,142,740 thousand, and, at the same time, renewed the authorization to make share buy-backs for a maximum of €1.8 billion, which, in consideration of the reserves already utilized for share buy-backs at that date (i.e., 38,568,458 shares having a book value of €656,553 thousand), resulted in an available reserve of €1,142,740 thousand, unchanged at 30 June 2010 as no purchases had been made subsequent to the resolution being passed.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 18

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 19

Reserve for treasury shares This reserve amounted to €656,553 thousand at 30 June 2010, unchanged from 31 December 2009.

This reserve is subject to certain restrictions imposed by law (Article 2357-ter of the Civil Code). Changes in the reserve represent increases - through transfers from the reserve available for the purchase of own shares - for own shares purchased and decreases for own shares sold.

Retained profit/(loss) At 30 June 2010, retained profit totaled €2,284,841 thousand, an increase of €85,847 thousand over 31 December 2009, following allocation of the prior year's profit, after dividends and allocations to the legal reserve, as approved by Shareholders on 26 March 2010.

Gains/(losses) recognized directly in equity This reserve includes gains and losses recognized directly in equity and in particular those arising from fair value adjustments on investments in other companies, as described previously (see Note 11).

At 30 June 2010, this reserve was a negative €2,942 thousand, representing a decrease of €5,382 thousand over 31 December 2009 attributable to fair value adjustments on the investments in Fin.Priv. S.r.l. and Assicurazioni Generali S.p.A.

Stock option reserve At 30 June 2010, the stock option reserve totaled €103,790 thousand, an increase of €8,518 thousand over 31 December 2009, offsetting the cost recognized in the income statement for the first half of 2010 in relation to stock option and stock grant plans for the Chief Executive Officer based on Fiat S.p.A. shares (see Note 6).

Other reserves At 30 June 2010, other reserves totaled €89,829 thousand and were unchanged from 31 December 2009. This amount includes:

Reserves pursuant to Law 413/1991: a total of €22,591 thousand corresponding to the compulsory revaluation of property (net of substitute tax) pursuant to Law 413 of 30 December 1991 and allocated to a specific reserve, as required by the Law.

Extraordinary reserve: a total of €28,044 thousand corresponding to the value approved by Shareholders on 11 May 2004.

Reserve for Spin-off difference: a total of €39,194 thousand and includes the positive difference arising from the spin-off executed by Fiat Partecipazioni S.p.A. on 29 December 2008.

Treasury shares At 30 June 2010, the book value of treasury shares held was €656,553 thousand and related to 38,568,458 ordinary shares (average book value of €17.023 per share) representing 3.02% of share capital and having a total par value of €192,842 thousand. The amount was unchanged over 31 December 2009, as no Fiat shares were bought or sold during the first half of 2010.

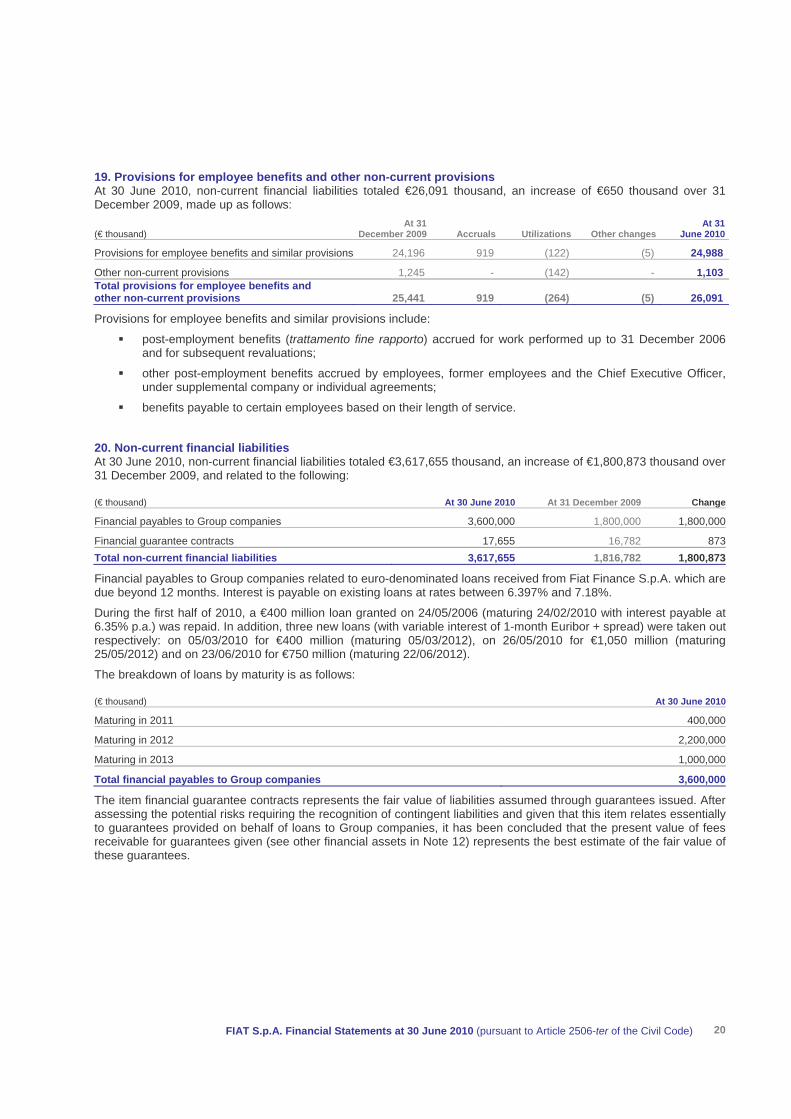

19. Provisions for employee benefits and other non-current provisions At 30 June 2010, non-current financial liabilities totaled €26,091 thousand, an increase of €650 thousand over 31 December 2009, made up as follows:

(€ thousand) At 31

December 2009 Accruals Utilizations Other changesAt 31

June 2010

Provisions for employee benefits and similar provisions 24,196 919 (122) (5) 24,988

Other non-current provisions 1,245 - (142) - 1,103Total provisions for employee benefits and other non-current provisions 25,441 919 (264) (5) 26,091

Provisions for employee benefits and similar provisions include:

post-employment benefits (trattamento fine rapporto) accrued for work performed up to 31 December 2006 and for subsequent revaluations;

other post-employment benefits accrued by employees, former employees and the Chief Executive Officer, under supplemental company or individual agreements;

benefits payable to certain employees based on their length of service.

20. Non-current financial liabilities At 30 June 2010, non-current financial liabilities totaled €3,617,655 thousand, an increase of €1,800,873 thousand over 31 December 2009, and related to the following:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Financial payables to Group companies 3,600,000 1,800,000 1,800,000

Financial guarantee contracts 17,655 16,782 873Total non-current financial liabilities 3,617,655 1,816,782 1,800,873

Financial payables to Group companies related to euro-denominated loans received from Fiat Finance S.p.A. which are due beyond 12 months. Interest is payable on existing loans at rates between 6.397% and 7.18%.

During the first half of 2010, a €400 million loan granted on 24/05/2006 (maturing 24/02/2010 with interest payable at 6.35% p.a.) was repaid. In addition, three new loans (with variable interest of 1-month Euribor + spread) were taken out respectively: on 05/03/2010 for €400 million (maturing 05/03/2012), on 26/05/2010 for €1,050 million (maturing 25/05/2012) and on 23/06/2010 for €750 million (maturing 22/06/2012).

The breakdown of loans by maturity is as follows:

(€ thousand) At 30 June 2010

Maturing in 2011 400,000

Maturing in 2012 2,200,000

Maturing in 2013 1,000,000

Total financial payables to Group companies 3,600,000

The item financial guarantee contracts represents the fair value of liabilities assumed through guarantees issued. After assessing the potential risks requiring the recognition of contingent liabilities and given that this item relates essentially to guarantees provided on behalf of loans to Group companies, it has been concluded that the present value of fees receivable for guarantees given (see other financial assets in Note 12) represents the best estimate of the fair value of these guarantees.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 20

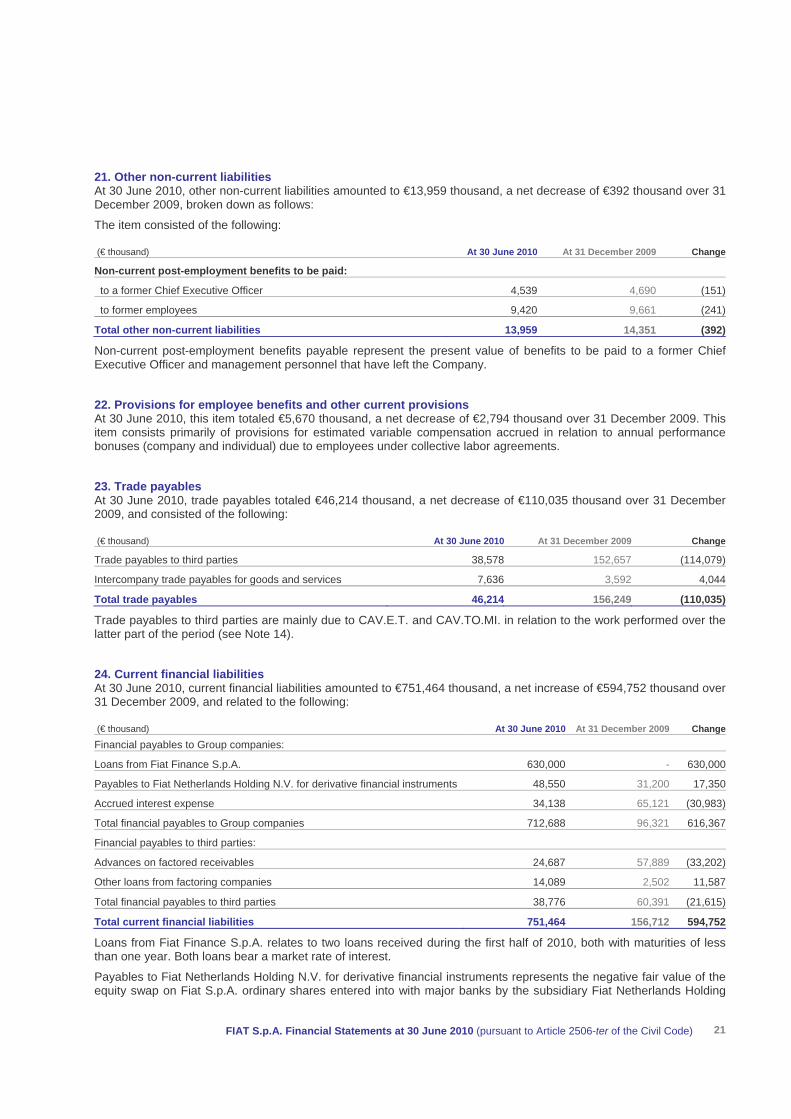

21. Other non-current liabilities At 30 June 2010, other non-current liabilities amounted to €13,959 thousand, a net decrease of €392 thousand over 31 December 2009, broken down as follows:

The item consisted of the following:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Non-current post-employment benefits to be paid:

to a former Chief Executive Officer 4,539 4,690 (151)

to former employees 9,420 9,661 (241)

Total other non-current liabilities 13,959 14,351 (392)

Non-current post-employment benefits payable represent the present value of benefits to be paid to a former Chief Executive Officer and management personnel that have left the Company.

22. Provisions for employee benefits and other current provisions At 30 June 2010, this item totaled €5,670 thousand, a net decrease of €2,794 thousand over 31 December 2009. This item consists primarily of provisions for estimated variable compensation accrued in relation to annual performance bonuses (company and individual) due to employees under collective labor agreements.

23. Trade payables At 30 June 2010, trade payables totaled €46,214 thousand, a net decrease of €110,035 thousand over 31 December 2009, and consisted of the following:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Trade payables to third parties 38,578 152,657 (114,079)

Intercompany trade payables for goods and services 7,636 3,592 4,044

Total trade payables 46,214 156,249 (110,035)

Trade payables to third parties are mainly due to CAV.E.T. and CAV.TO.MI. in relation to the work performed over the latter part of the period (see Note 14).

24. Current financial liabilities At 30 June 2010, current financial liabilities amounted to €751,464 thousand, a net increase of €594,752 thousand over 31 December 2009, and related to the following:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Financial payables to Group companies:

Loans from Fiat Finance S.p.A. 630,000 - 630,000

Payables to Fiat Netherlands Holding N.V. for derivative financial instruments 48,550 31,200 17,350

Accrued interest expense 34,138 65,121 (30,983)

Total financial payables to Group companies 712,688 96,321 616,367

Financial payables to third parties:

Advances on factored receivables 24,687 57,889 (33,202)

Other loans from factoring companies 14,089 2,502 11,587

Total financial payables to third parties 38,776 60,391 (21,615)

Total current financial liabilities 751,464 156,712 594,752

Loans from Fiat Finance S.p.A. relates to two loans received during the first half of 2010, both with maturities of less than one year. Both loans bear a market rate of interest.

Payables to Fiat Netherlands Holding N.V. for derivative financial instruments represents the negative fair value of the equity swap on Fiat S.p.A. ordinary shares entered into with major banks by the subsidiary Fiat Netherlands Holding

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 21

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 22

N.V., under instruction from Fiat S.p.A., to hedge against the risk of an increase in the Fiat share price above the exercise price of the stock options granted to the Company’s Chief Executive Officer in 2006. Determination of the fair value of that equity swap was based on quoted market prices at the interim reporting date.

Advances on factored receivables relates to advances on IRES receivables (see Note 16).

The item other loans from factoring companies relates to the residual liability for advances on receivables which had already been repaid at the interim reporting date.

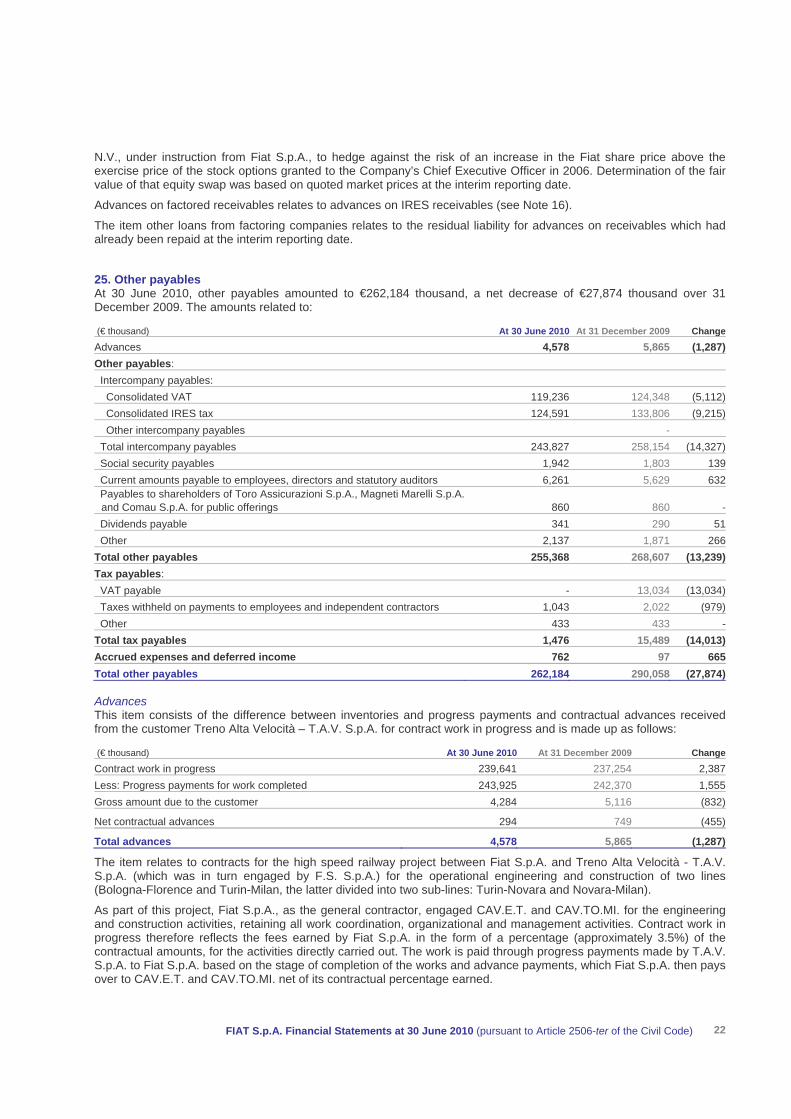

25. Other payables At 30 June 2010, other payables amounted to €262,184 thousand, a net decrease of €27,874 thousand over 31 December 2009. The amounts related to:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Advances 4,578 5,865 (1,287)Other payables: Intercompany payables: Consolidated VAT 119,236 124,348 (5,112) Consolidated IRES tax 124,591 133,806 (9,215) Other intercompany payables - Total intercompany payables 243,827 258,154 (14,327) Social security payables 1,942 1,803 139 Current amounts payable to employees, directors and statutory auditors 6,261 5,629 632 Payables to shareholders of Toro Assicurazioni S.p.A., Magneti Marelli S.p.A.

and Comau S.p.A. for public offerings 860 860 - Dividends payable 341 290 51 Other 2,137 1,871 266Total other payables 255,368 268,607 (13,239)Tax payables: VAT payable - 13,034 (13,034) Taxes withheld on payments to employees and independent contractors 1,043 2,022 (979) Other 433 433 -Total tax payables 1,476 15,489 (14,013)Accrued expenses and deferred income 762 97 665Total other payables 262,184 290,058 (27,874)

Advances This item consists of the difference between inventories and progress payments and contractual advances received from the customer Treno Alta Velocità – T.A.V. S.p.A. for contract work in progress and is made up as follows:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Contract work in progress 239,641 237,254 2,387Less: Progress payments for work completed 243,925 242,370 1,555Gross amount due to the customer 4,284 5,116 (832)

Net contractual advances 294 749 (455)

Total advances 4,578 5,865 (1,287)

The item relates to contracts for the high speed railway project between Fiat S.p.A. and Treno Alta Velocità - T.A.V. S.p.A. (which was in turn engaged by F.S. S.p.A.) for the operational engineering and construction of two lines (Bologna-Florence and Turin-Milan, the latter divided into two sub-lines: Turin-Novara and Novara-Milan).

As part of this project, Fiat S.p.A., as the general contractor, engaged CAV.E.T. and CAV.TO.MI. for the engineering and construction activities, retaining all work coordination, organizational and management activities. Contract work in progress therefore reflects the fees earned by Fiat S.p.A. in the form of a percentage (approximately 3.5%) of the contractual amounts, for the activities directly carried out. The work is paid through progress payments made by T.A.V. S.p.A. to Fiat S.p.A. based on the stage of completion of the works and advance payments, which Fiat S.p.A. then pays over to CAV.E.T. and CAV.TO.MI. net of its contractual percentage earned.

Contract work in progress is measured on the basis of the stage of completion in relation to the sales price, which in this case is the consideration contractually agreed for the activities directly carried out by Fiat S.p.A. Changes in contract work in progress have been recognized in the income statement under the item other operating income (see Note 4). When the lines are contractually completed, the final contractual revenue for the activities directly carried out will be recognized in the income statement under other operating income, net of any decrease in inventories. At the same time, the accounts for inventories and amounts classified as advances will be closed.

In this regard, it should be noted that the Secondary Final Test Certificate relating to completion of the residual work was signed at year-end 2009 and work on the Turin-Novara line was therefore recognized as completed from an accounting perspective. The Bologna-Florence and Novara-Milan lines were also formally handed over to T.A.V. S.p.A. during 2009 and the high-speed lines were opened for commercial use (following technical approval by the Testing Commission). However, ancillary work and cleanup were still ongoing at 30 June 2010 (as was also the case at 31 December 2009) and contractual obligations for final approval of the work (Final Test Certificates) and the release of bank guarantees were still incomplete. Therefore, from an accounting perspective, these projects remained open.

At 30 June 2010, Fiat S.p.A. had a total of €970 million in bank and insurace guarantees outstanding to T.A.V. S.p.A. against contractual advances received, performance and the release of amounts withheld pending completion. Pursuant to the agreements entered into with the aforementioned consortia and institutions issuing the guarantees, €935 million of the total represents a direct liability of the consortia towards the issuing banks and insurance companies, without the joint responsibility of Fiat S.p.A.

Tax payables and other payables An explanation of the principal components is provided below.

At 30 June 2010, intercompany payables for consolidated VAT of €119,236 thousand (€124,348 thousand at 31 December 2009) related to VAT credit of Italian subsidiaries transferred to Fiat S.p.A. as part of the VAT consolidation regime.

At 30 June 2010, intercompany payables for consolidated IRES of €124,591 thousand (€133,806 thousand at 31 December 2009), related to the compensation payable for tax losses contributed by Italian subsidiaries to the domestic tax consolidation for 2009, in addition to IRES credits of Italian subsidiaries transferred to Fiat S.p.A. under the tax consolidation program.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 23

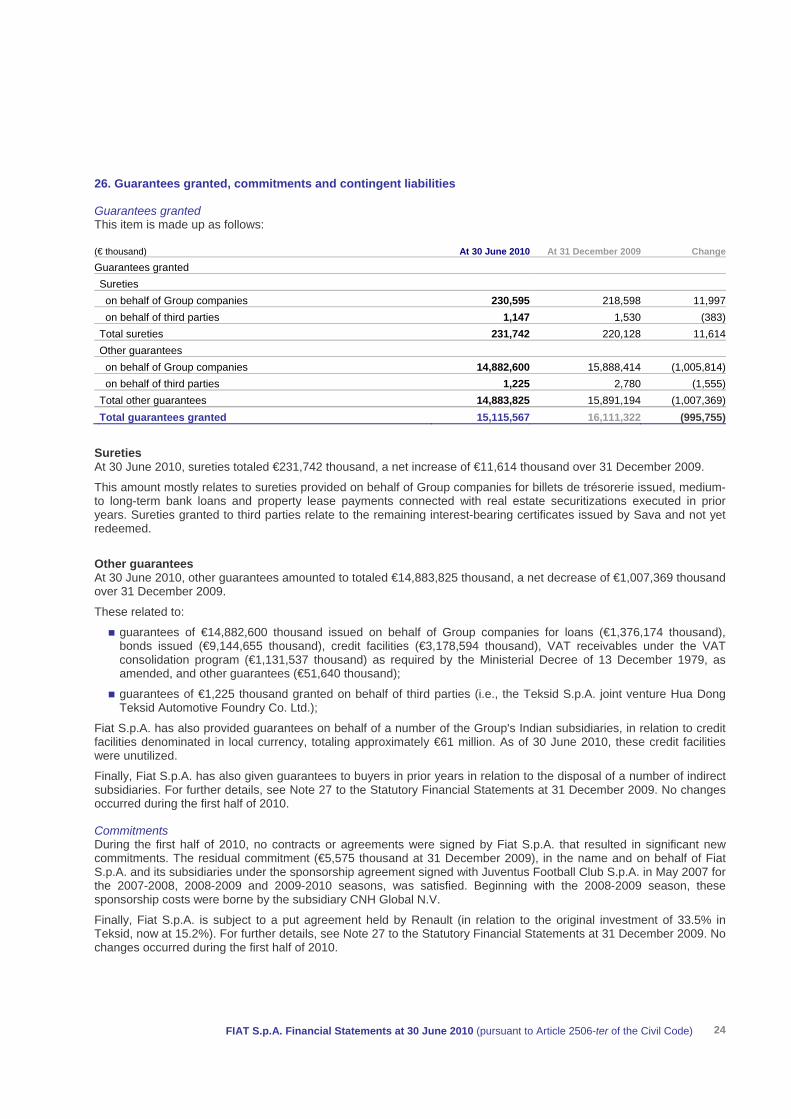

26. Guarantees granted, commitments and contingent liabilities

Guarantees granted This item is made up as follows:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Guarantees granted Sureties on behalf of Group companies 230,595 218,598 11,997 on behalf of third parties 1,147 1,530 (383) Total sureties 231,742 220,128 11,614 Other guarantees on behalf of Group companies 14,882,600 15,888,414 (1,005,814) on behalf of third parties 1,225 2,780 (1,555) Total other guarantees 14,883,825 15,891,194 (1,007,369) Total guarantees granted 15,115,567 16,111,322 (995,755)

Sureties At 30 June 2010, sureties totaled €231,742 thousand, a net increase of €11,614 thousand over 31 December 2009.

This amount mostly relates to sureties provided on behalf of Group companies for billets de trésorerie issued, medium- to long-term bank loans and property lease payments connected with real estate securitizations executed in prior years. Sureties granted to third parties relate to the remaining interest-bearing certificates issued by Sava and not yet redeemed.

Other guarantees At 30 June 2010, other guarantees amounted to totaled €14,883,825 thousand, a net decrease of €1,007,369 thousand over 31 December 2009.

These related to:

guarantees of €14,882,600 thousand issued on behalf of Group companies for loans (€1,376,174 thousand), bonds issued (€9,144,655 thousand), credit facilities (€3,178,594 thousand), VAT receivables under the VAT consolidation program (€1,131,537 thousand) as required by the Ministerial Decree of 13 December 1979, as amended, and other guarantees (€51,640 thousand);

guarantees of €1,225 thousand granted on behalf of third parties (i.e., the Teksid S.p.A. joint venture Hua Dong Teksid Automotive Foundry Co. Ltd.);

Fiat S.p.A. has also provided guarantees on behalf of a number of the Group's Indian subsidiaries, in relation to credit facilities denominated in local currency, totaling approximately €61 million. As of 30 June 2010, these credit facilities were unutilized.

Finally, Fiat S.p.A. has also given guarantees to buyers in prior years in relation to the disposal of a number of indirect subsidiaries. For further details, see Note 27 to the Statutory Financial Statements at 31 December 2009. No changes occurred during the first half of 2010.

Commitments During the first half of 2010, no contracts or agreements were signed by Fiat S.p.A. that resulted in significant new commitments. The residual commitment (€5,575 thousand at 31 December 2009), in the name and on behalf of Fiat S.p.A. and its subsidiaries under the sponsorship agreement signed with Juventus Football Club S.p.A. in May 2007 for the 2007-2008, 2008-2009 and 2009-2010 seasons, was satisfied. Beginning with the 2008-2009 season, these sponsorship costs were borne by the subsidiary CNH Global N.V.

Finally, Fiat S.p.A. is subject to a put agreement held by Renault (in relation to the original investment of 33.5% in Teksid, now at 15.2%). For further details, see Note 27 to the Statutory Financial Statements at 31 December 2009. No changes occurred during the first half of 2010.

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 24

Legal actions and disputes Fiat S.p.A. is involved in various disputes and legal actions. However, resolution of these disputes is not expected to result in any significant liabilities that have not already been provided for. For further details, see Note 27 to the Statutory Financial Statements at 31 December 2009. No changes occurred during the first half of 2010.

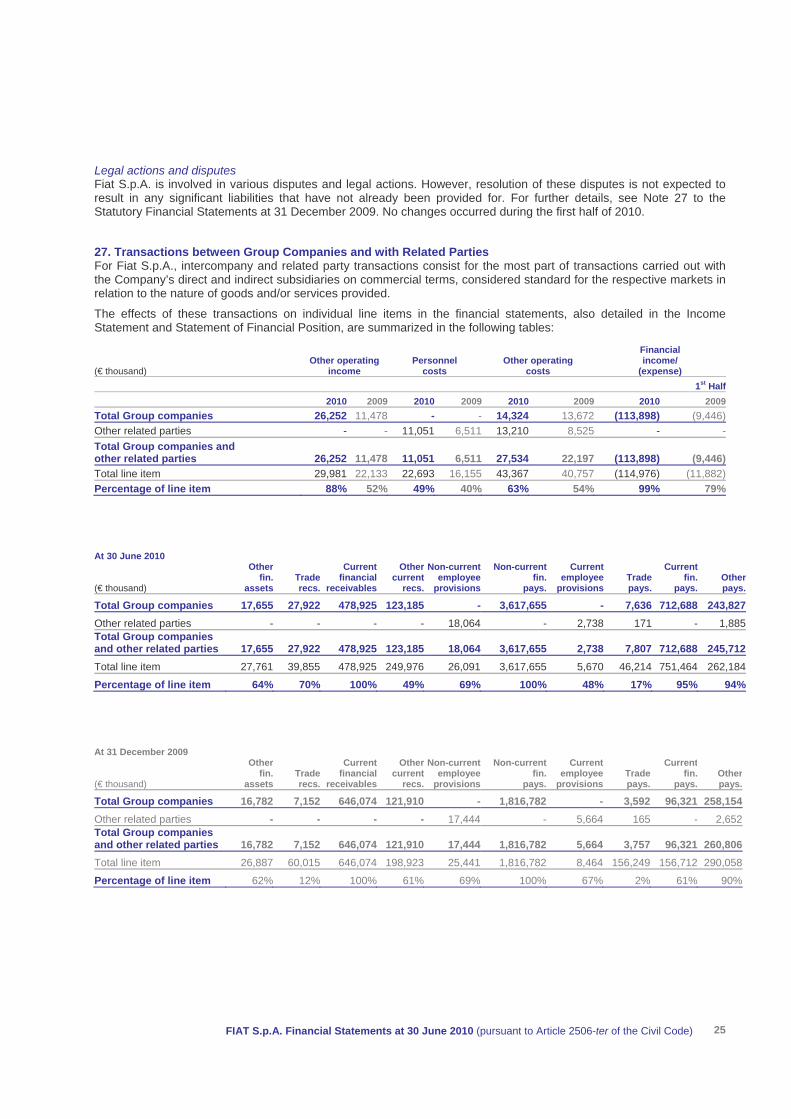

27. Transactions between Group Companies and with Related Parties For Fiat S.p.A., intercompany and related party transactions consist for the most part of transactions carried out with the Company’s direct and indirect subsidiaries on commercial terms, considered standard for the respective markets in relation to the nature of goods and/or services provided.

The effects of these transactions on individual line items in the financial statements, also detailed in the Income Statement and Statement of Financial Position, are summarized in the following tables:

(€ thousand) Other operating

income Personnel

costs Other operating

costs

Financial income/

(expense) 1st Half

2010 2009 2010 2009 2010 2009 2010 2009Total Group companies 26,252 11,478 - - 14,324 13,672 (113,898) (9,446)Other related parties - - 11,051 6,511 13,210 8,525 - -Total Group companies and other related parties 26,252 11,478 11,051 6,511 27,534 22,197 (113,898) (9,446)Total line item 29,981 22,133 22,693 16,155 43,367 40,757 (114,976) (11,882)Percentage of line item 88% 52% 49% 40% 63% 54% 99% 79%

At 30 June 2010 (€ thousand)

Otherfin.

assets Traderecs.

Current financial

receivables

Othercurrent

recs.

Non-currentemployee

provisions

Non-currentfin.

pays.

Current employee

provisions Tradepays.

Currentfin.

pays. Otherpays.

Total Group companies 17,655 27,922 478,925 123,185 - 3,617,655 - 7,636 712,688 243,827Other related parties - - - - 18,064 - 2,738 171 - 1,885Total Group companies and other related parties 17,655 27,922 478,925 123,185 18,064 3,617,655 2,738 7,807 712,688 245,712Total line item 27,761 39,855 478,925 249,976 26,091 3,617,655 5,670 46,214 751,464 262,184

Percentage of line item 64% 70% 100% 49% 69% 100% 48% 17% 95% 94%

At 31 December 2009 (€ thousand)

Otherfin.

assets Traderecs.

Current financial

receivables

Othercurrent

recs.

Non-currentemployee

provisions

Non-currentfin.

pays.

Current employee

provisionsTradepays.

Currentfin.

pays.Otherpays.

Total Group companies 16,782 7,152 646,074 121,910 - 1,816,782 - 3,592 96,321 258,154Other related parties - - - - 17,444 - 5,664 165 - 2,652Total Group companies and other related parties 16,782 7,152 646,074 121,910 17,444 1,816,782 5,664 3,757 96,321 260,806Total line item 26,887 60,015 646,074 198,923 25,441 1,816,782 8,464 156,249 156,712 290,058

Percentage of line item 62% 12% 100% 61% 69% 100% 67% 2% 61% 90%

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 25

The most significant transactions undertaken between Fiat S.p.A. and Group companies in the first half of 2010, summarized in the above tables, related to:

services provided by Fiat S.p.A. and senior managers at various Group companies (Fiat Group Automobiles S.p.A., Iveco S.p.A., Magneti Marelli S.p.A., Ferrari S.p.A., Fiat Powertrain Technologies S.p.A., Fiat Group Purchasing S.r.l., Teksid S.p.A., Comau S.p.A. and other minor companies);

lease of buildings or office space (Fiat Finance S.p.A., Fiat Group Marketing & Corporate Communication S.p.A., Fiat Partecipazioni S.p.A. and other minor companies) and the recovery of directors' fees and expenses;

provision of sureties and other guarantees (see Note 26) on bonds and billets de trésorerie (Fiat Finance and Trade Ltd S.A., Fiat Finance North America Inc. and Fiat Finance Canada Ltd.), bank loans and credit facilities (Fiat Finance and Trade Ltd S.A., Fiat Finance S.p.A., Banco CNH Capital S.A., CNH Global N.V., Fiat Finance Canada Ltd., Fiat Automoveis S.A.- FIASA and other minor companies), property lease payments (Fiat Group Automobiles S.p.A. and its subsidiaries) and to tax authorities for VAT credits;

management of current accounts, obtaining short- and medium-term loans and consulting/assistance on financial matters (Fiat Finance S.p.A.);

management of derivative instruments and contracts (Fiat Netherlands Holding N.V., see Notes 15 and 24);

purchase of administrative, tax, corporate consultancy and services as well as related IT systems (Fiat Services S.p.A. and Fiat I.T.E.M. S.p.A.), public relations services (Fiat Group Marketing & Corporate Communication S.p.A.), personnel and other management services (Fiat Servizi per l’Industria S.c.p.A.), security services (Orione S.c.p.A. and Sirio S.c.p.A.), inspection and internal audit services (Fiat-Revisione Interna S.c.r.l.), vehicle leases (Leasys S.p.A.) maintenance and property services (Fiat Partecipazioni S.p.A.).

During the first half of 2010, intercompany transactions also related to management of investments in subsidiaries, whose effects on the Company’s earnings and financial position, as described above, consisted of the:

receipt of dividends from investees (see Note 1);

subscription to capital increases of Fiat Group Automobiles S.p.A. in the amount of €1,050 million, Fiat Netherlands Holding N.V. in the amount of €750 million and Teksid Aluminum S.r.l. in the amount of €10 million (see Note 11);

purchase from Fiat Partecipazioni S.p.A. and subsequent capital increase of the subsidiaries Nuove Iniziative Finanziarie 5 S.p.A. and Nuova Immobiliare Nove S.p.A. (currently inactive), in the amount of €200 million and €100 million respectively, and the incorporation of the subsidiary Fiat Industrial Finance S.p.A., also capitalized in the amount of €100 million (see Note 11).

During the first half of 2010, transactions with related parties, as defined by IAS 24, that did not involve direct or indirect subsidiaries are presented in the tables above under “Other related parties”. The details of these transactions were as follows:

expenses for services rendered by Soiem S.p.A. (€35 thousand);

professional and advisory services and the activities of secretary to the Board of Directors and its sub-committees provided to Fiat S.p.A. by Franzo Grande Stevens for fees of €500 thousand;

Fiat S.p.A. directors' and statutory auditors’ fees as well as the compensation component arising from stock option and stock grant plans for the Chief Executive Officer based on Fiat S.p.A. shares (see Note 6);

compensation due to Fiat S.p.A. executives with strategic responsibilities (see Note 5).

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 26

FIAT S.p.A. Financial Statements at 30 June 2010 (pursuant to Article 2506-ter of the Civil Code) 27

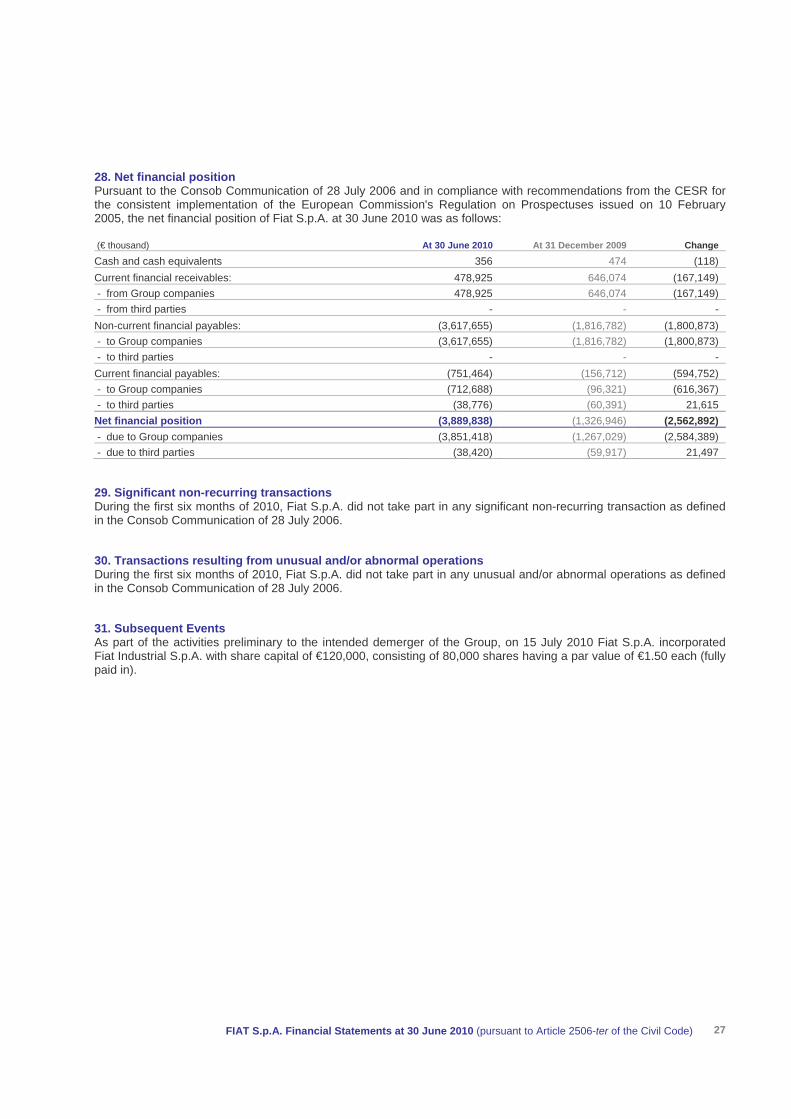

28. Net financial position Pursuant to the Consob Communication of 28 July 2006 and in compliance with recommendations from the CESR for the consistent implementation of the European Commission's Regulation on Prospectuses issued on 10 February 2005, the net financial position of Fiat S.p.A. at 30 June 2010 was as follows:

(€ thousand) At 30 June 2010 At 31 December 2009 Change

Cash and cash equivalents 356 474 (118) Current financial receivables: 478,925 646,074 (167,149) - from Group companies 478,925 646,074 (167,149) - from third parties - - - Non-current financial payables: (3,617,655) (1,816,782) (1,800,873) - to Group companies (3,617,655) (1,816,782) (1,800,873) - to third parties - - - Current financial payables: (751,464) (156,712) (594,752) - to Group companies (712,688) (96,321) (616,367) - to third parties (38,776) (60,391) 21,615 Net financial position (3,889,838) (1,326,946) (2,562,892) - due to Group companies (3,851,418) (1,267,029) (2,584,389) - due to third parties (38,420) (59,917) 21,497

29. Significant non-recurring transactions During the first six months of 2010, Fiat S.p.A. did not take part in any significant non-recurring transaction as defined in the Consob Communication of 28 July 2006.

30. Transactions resulting from unusual and/or abnormal operations During the first six months of 2010, Fiat S.p.A. did not take part in any unusual and/or abnormal operations as defined in the Consob Communication of 28 July 2006.

31. Subsequent Events As part of the activities preliminary to the intended demerger of the Group, on 15 July 2010 Fiat S.p.A. incorporated Fiat Industrial S.p.A. with share capital of €120,000, consisting of 80,000 shares having a par value of €1.50 each (fully paid in).