front row seatfilecache.drivetheweb.com/mr5cnw_flintenergy/69866/a… · · 2013-02-04north...

TRANSCRIPT

ANNUAL MEETING OF SHAREHOLDERSMetropolitan CentreC l Alb tCalgary, AlbertaMay 5, 2011

Your investment in Flint gives you a

t ti l l i FRONT ROW SEAT

at every unconventional energy play in North America

1

Annual Meeting of Shareholders

Agenda

gMay 5, 2011

Agenda• Call Meeting to Order Scrutineer’s Report• Election of Directors• Tabling of the December 31, 2010 Financial Statements• Appointment of Auditors• Other Matters• Adjournment

Management Presentation W J Bill Li d

2

• W. J. Bill Lingard President and Chief Executive Officer

Nominees for Directors of the Corporation

•••

••

•••

• •

3

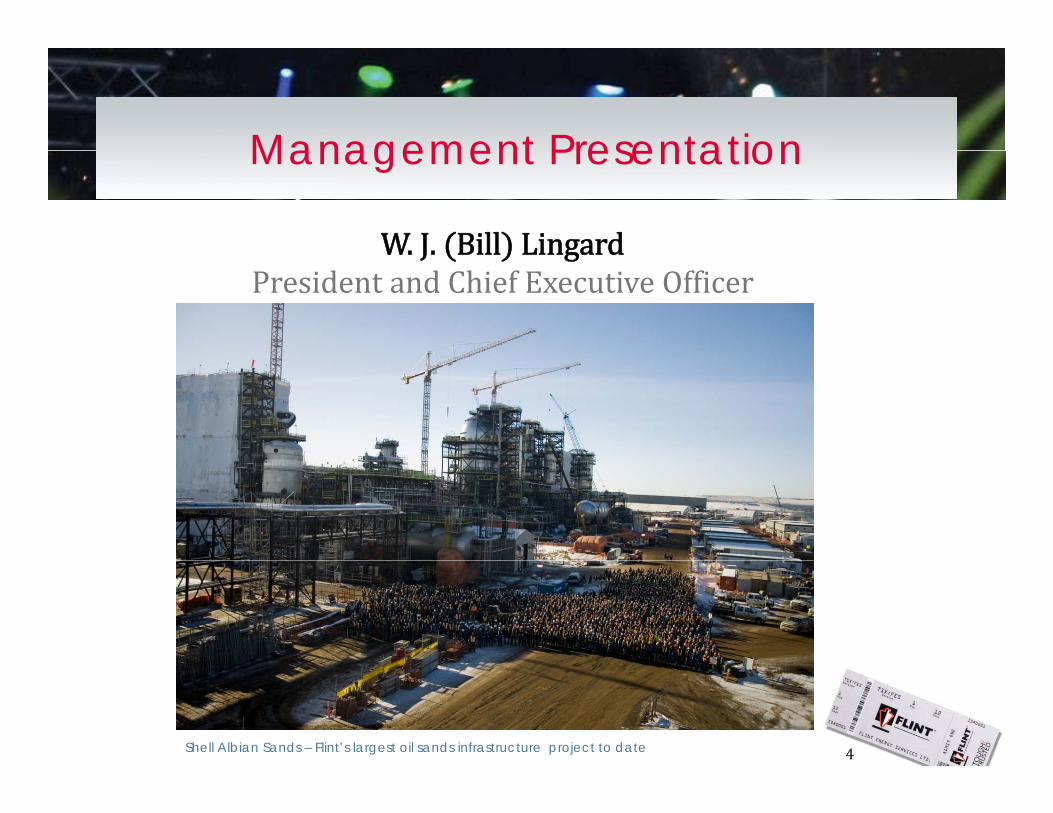

Management PresentationManagement Presentation

W. J. Bill LingardW. J. Bill LingardPresident and Chief Executive Officer

4Shell Albian Sands – Flint’s largest oil sands infrastructure project to date

Forward Looking Information StatementForward-Looking Information Statement

This presentation contains forward‐looking statements concerning the Company’s projected operating results and anticipated capital expenditure trends and drilling activity in the oil and gas industry. Actual events or results may differ materially from those reflected in the Company’s forward‐looking statements due to a

b f i k i i d h f ff i h C ’ b inumber of risks, uncertainties and other factors affecting the Company’s business and the oil and gas industry generally. These risk factors include, but are not limited to risks and uncertainties described d h h di “Ri k F ” d l h i h C ’ A lunder the heading “Risk Factors” and elsewhere in the Company’s Annual

Information Form for the year ended December 31, 2010, and other documents filed with Canadian provincial securities authorities, which are available to the public at wwwsedarcompublic at www.sedar.com. Unless otherwise indicated, all financial information in this presentation is in Canadian dollars and in accordance with Canadian generally accepted accounting principles

5

principles.

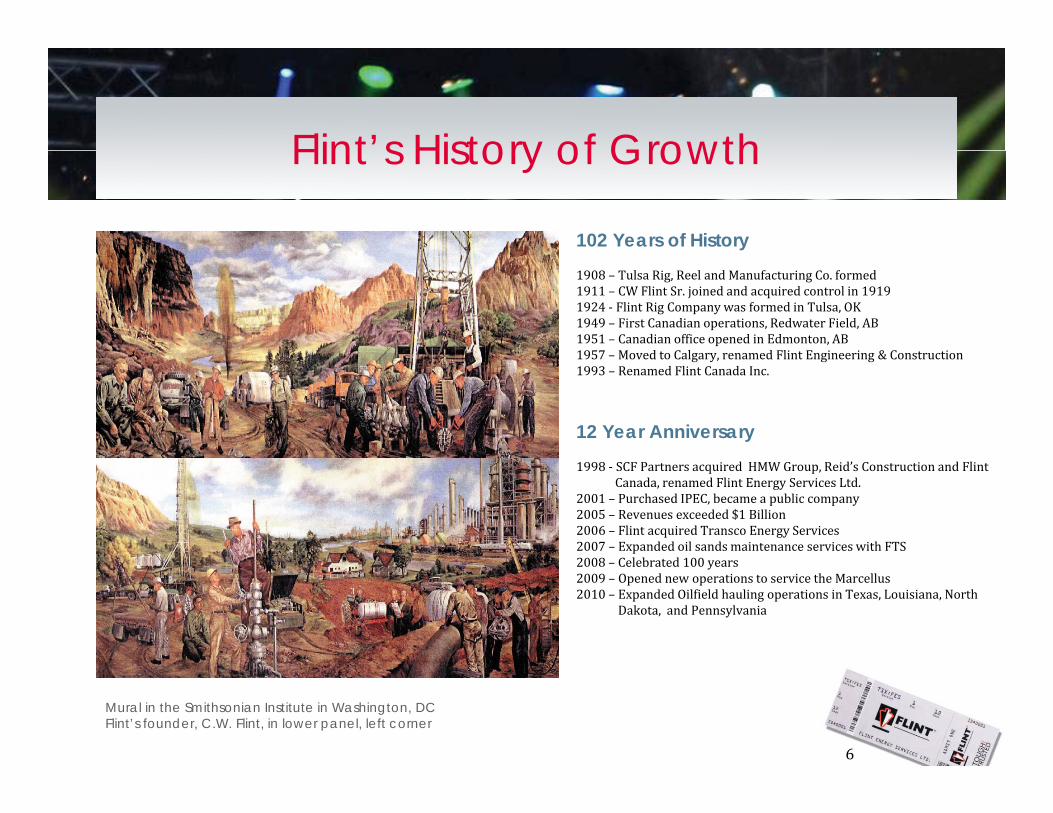

Flint’s History of GrowthFlint s History of Growth

102 Years of History1908 – Tulsa Rig, Reel and Manufacturing Co. formed 1911 – CW Flint Sr. joined and acquired control in 19191924 ‐ Flint Rig Company was formed in Tulsa, OK 1949 – First Canadian operations, Redwater Field, AB1951 – Canadian office opened in Edmonton, AB1957 – Moved to Calgary renamed Flint Engineering & Construction1957 – Moved to Calgary, renamed Flint Engineering & Construction1993 – Renamed Flint Canada Inc.

12 Year Anniversary1998 ‐ SCF Partners acquired HMW Group, Reid’s Construction and Flint

Canada, renamed Flint Energy Services Ltd.2001 – Purchased IPEC, became a public company 2005 – Revenues exceeded $1 Billion2006 – Flint acquired Transco Energy Services2007 – Expanded oil sands maintenance services with FTS 2008 Celebrated 100 years2008 – Celebrated 100 years 2009 – Opened new operations to service the Marcellus2010 – Expanded Oilfield hauling operations in Texas, Louisiana, North

Dakota, and Pennsylvania

6

Mural in the Smithsonian Institute in Washington, DC Flint’s founder, C.W. Flint, in lower panel, left corner

Flint’s Strategy - “Build it then Maintain it”Trading and Financial Indicatorsit”Trading and Financial Indicators

$19 99 $11 00 FES Sh P i (Hi h/L )$19.99 - $11.00 FES Share Price (High/Low)(high 2/22/11, low 5/21/10)

45.8 Million Basic Shares Outstanding

$824.2 Million Market Capitalization (as of March 31, 2011)

$1,781.3 Million in Annual Revenue (2010)ES $ ,78 3 (2010)

$131.3 Million in Annual EBITDA(2010)

$TSX:

FE

$33.0 Million in Annual Net Earnings (2010)

$2.88 EBITDA per Share (2010)

T

7

$ .88 (2010)

$163.6 Million cash holdings as of Dec. 31, 2010

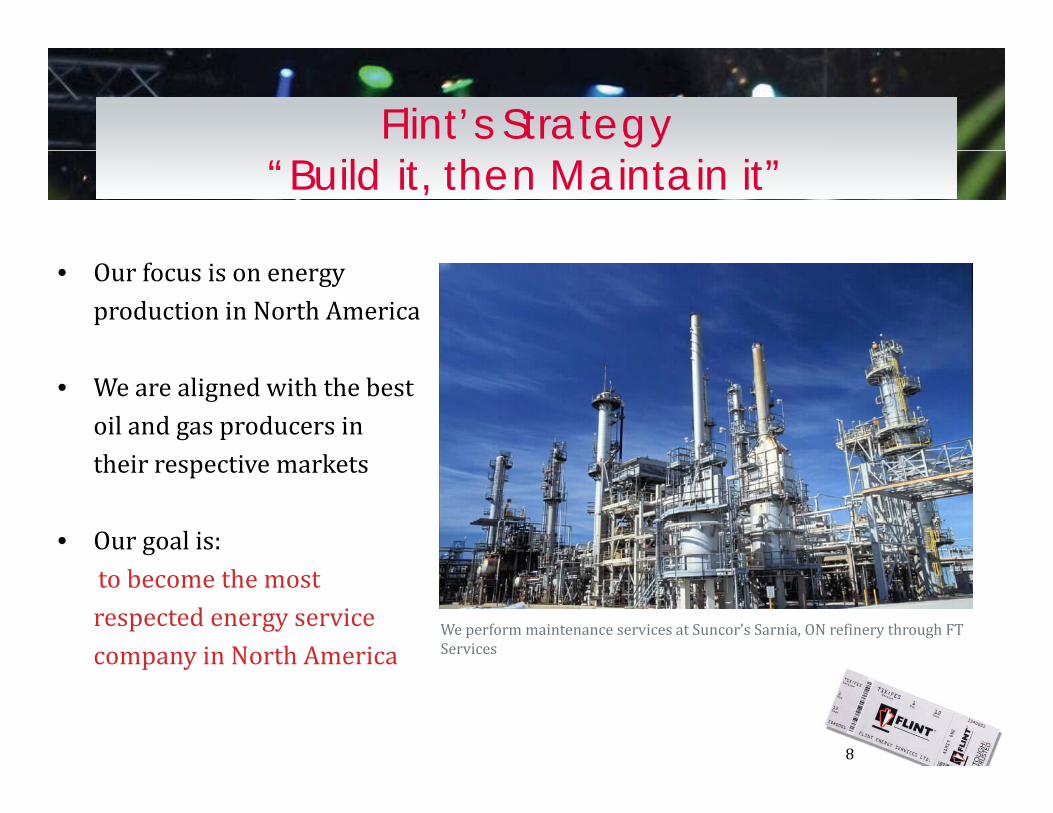

Flint’s Strategy - “Build it then Maintain it”

Flint’s Strategyit”“Build it, then Maintain it”

• Our focus is on energy production in North America

• We are aligned with the best oil and gas producers in th i ti k ttheir respective markets

• Our goal is:to become the most respected energy service company in North America

We perform maintenance services at Suncor’s Sarnia, ON refinery through FT Services

8

company in North America

Full Cycle ServicesFull-Cycle Services

OILFIELD PRODUCTION FACILITY MAINTENANCESERVICES SERVICES INFRASTRUCTURE SERVICES

Early cycle Late cycleEarly cycle Late cycle

Upstream Drilling Downstream RefiningMidstream Production

9

Transportation, Construction, Manufacturing & Maintenance

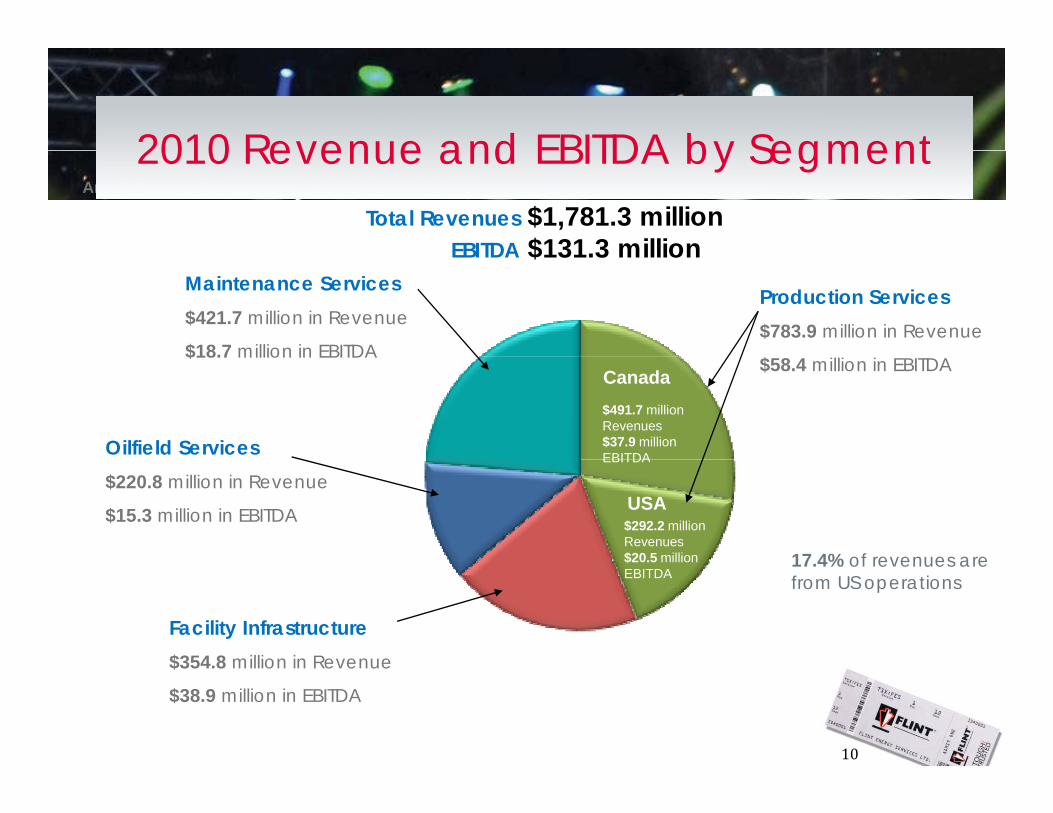

2010 Revenue by Segment2010 Revenue and EBITDA by Segment2010 Revenue by Segment

Total Revenues $1,781.3 millionEBITDA $131 3 million

Amounts in C$ millions

2010 Revenue and EBITDA by Segment

EBITDA $131.3 millionProduction Services$783.9 million in Revenue

Maintenance Services$421.7 million in Revenue

$18.7 million in EBITDA$58.4 million in EBITDA

Oilfield Services

$18.7 million in EBITDACanada$491.7 million Revenues$37.9 million EBITDA

$220.8 million in Revenue

$15.3 million in EBITDA USA

EBITDA

$292.2 million Revenues$20.5 million 17 4% of revenues are

Facility Infrastructure$354 8 million in Revenue

$20.5 million EBITDA

17.4% of revenues arefrom US operations

10

$354.8 million in Revenue

$38.9 million in EBITDA

Fabrication & Construction ActivitiesFabrication & Construction Activities

Top L: Shell’s Albian Sands Project, NE ABTop R: BP Node 3 in NE BCTop R: BP Node 3, in NE BCBottom L: Module Fabrication, Sherwood Park, AB

11

Manufacturing ActivitiesManufacturing Activities

Add global poly

Top L: Flint Global Poly, Edmonton, ABTop R: JW Williams, Casper, WYBottom L: Flint Process Systems, Halkirk, AB

Add paint earth

12

Transportation ActivitiesTransportation Activities

Top L: Rig Move MarcellusTop L: Rig Move, Marcellus Basin, PATop R: P&V, Cold Lake, ABBottom L: New Rig Moving Office Texas

13

Office, Texas

Maintenance ActivitiesMaintenance Activities

Top L: Nexen’s Long Lake Facilities p gTop R: Suncor Energy’s Firebag 1 & 2Bottom L: Tubular Management, Nisku, ABAdd tubular management

14

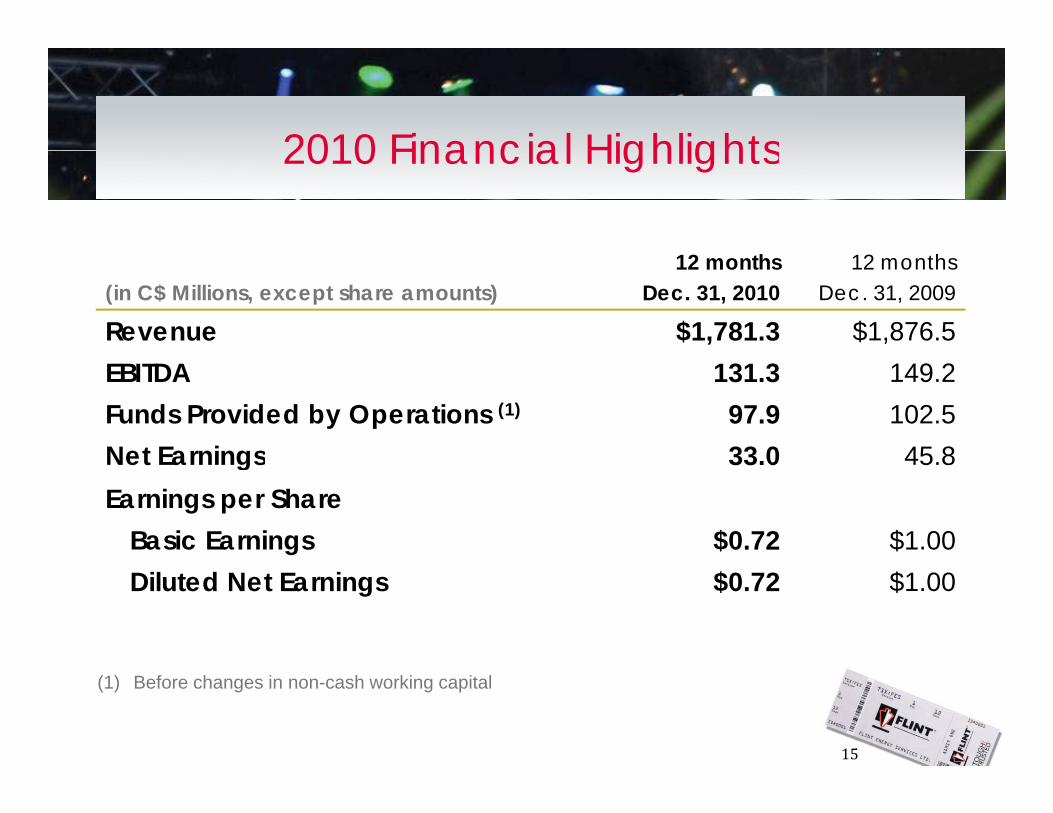

2010 Financial Highlights2010 Financial Highlights

(in C$ Millions, except share amounts)12 months

Dec. 31, 201012 months

Dec. 31, 2009

Revenue $1,781.3 $1,876.5EBITDA 131.3 149.2Funds Provided by Operations (1) 97.9 102.5Net Earnings 33 0 45 8Net Earnings 33.0 45.8Earnings per Share

Basic Earnings $0.72 $1.00Diluted Net Earnings $0.72 $1.00

15

(1) Before changes in non-cash working capital

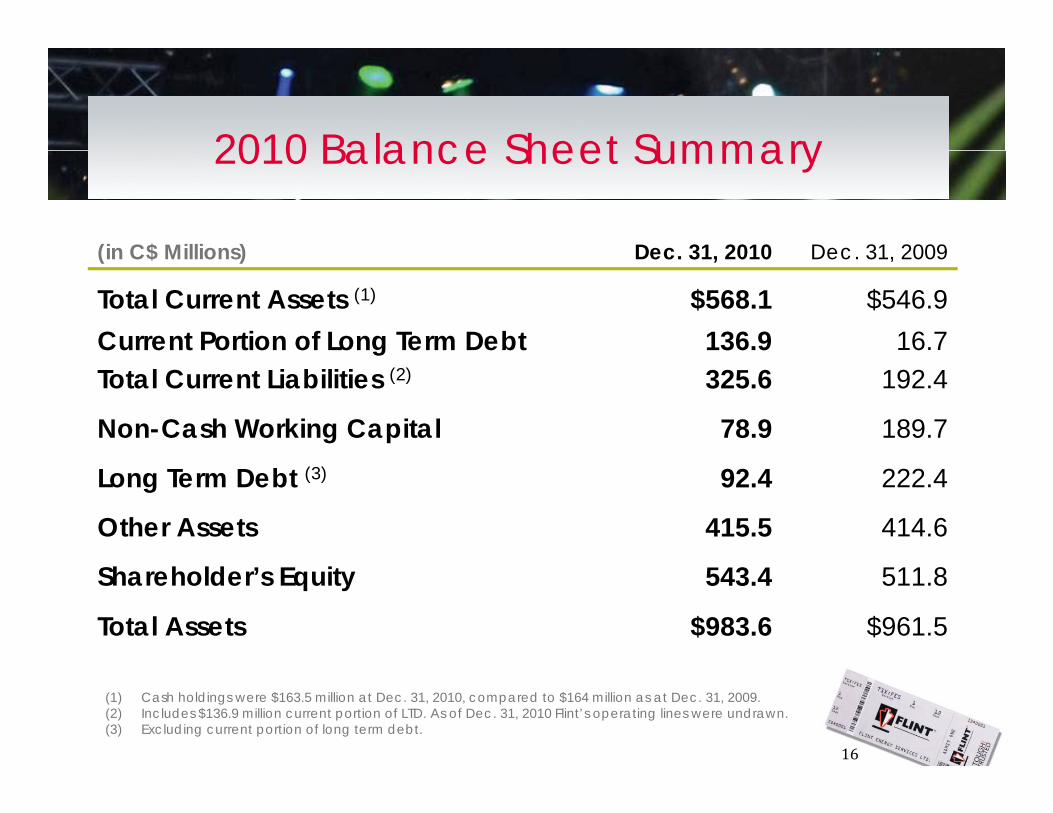

2010 Balance Sheet Summary

(in C$ Millions) Dec 31 2010 Dec 31 2009

2010 Balance Sheet Summary

(in C$ Millions) Dec. 31, 2010 Dec. 31, 2009

Total Current Assets (1) $568.1 $546.9Current Portion of Long Term Debt 136.9 16.7gTotal Current Liabilities (2) 325.6 192.4

Non-Cash Working Capital 78.9 189.7

Long Term Debt (3) 92.4 222.4

Other Assets 415.5 414.6

Shareholder’s Equity 543.4 511.8

Total Assets $983.6 $961.5

16

(1) Cash holdings were $163.5 million at Dec. 31, 2010, compared to $164 million as at Dec. 31, 2009. (2) Includes $136.9 million current portion of LTD. As of Dec. 31, 2010 Flint’s operating lines were undrawn. (3) Excluding current portion of long term debt.

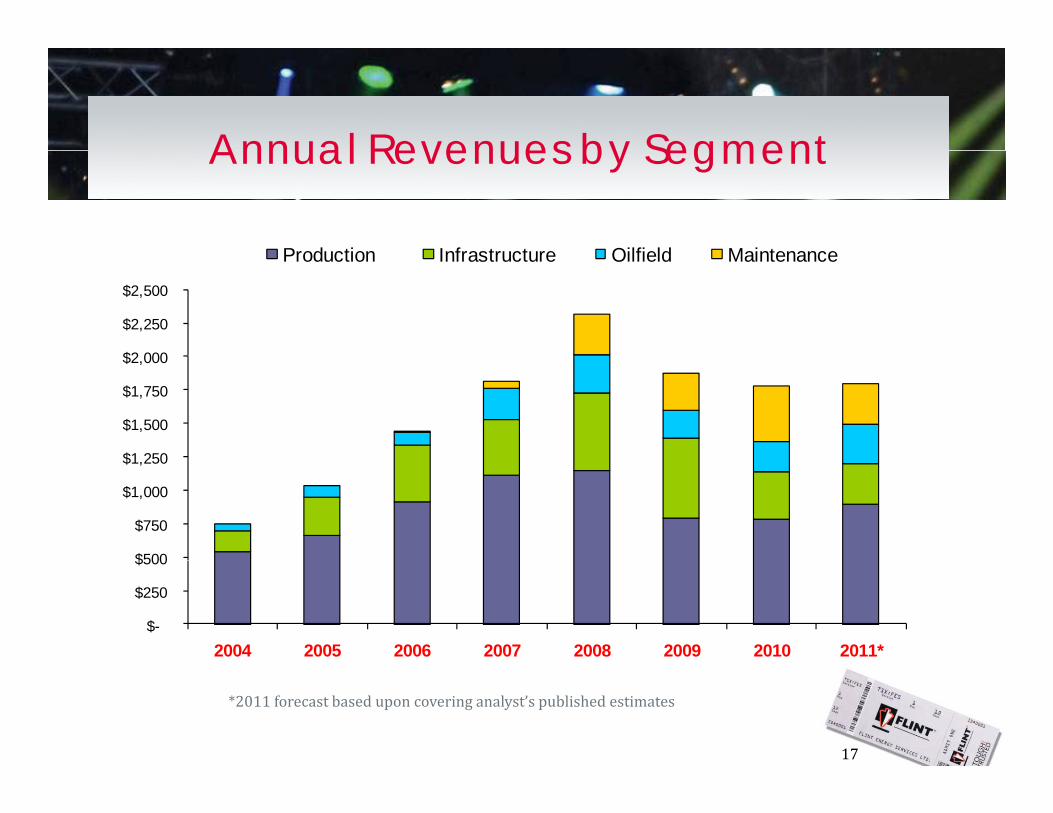

Annual Revenues by Segment

Production Infrastructure Oilfield Maintenance

Annual Revenues by Segment

$2 000

$2,250

$2,500

Production Infrastructure Oilfield Maintenance

$1 250

$1,500

$1,750

$2,000

$500

$750

$1,000

$1,250

$-

$250

$500

2004 2005 2006 2007 2008 2009 2010 2011*

17

*2011 forecast based upon covering analyst’s published estimates

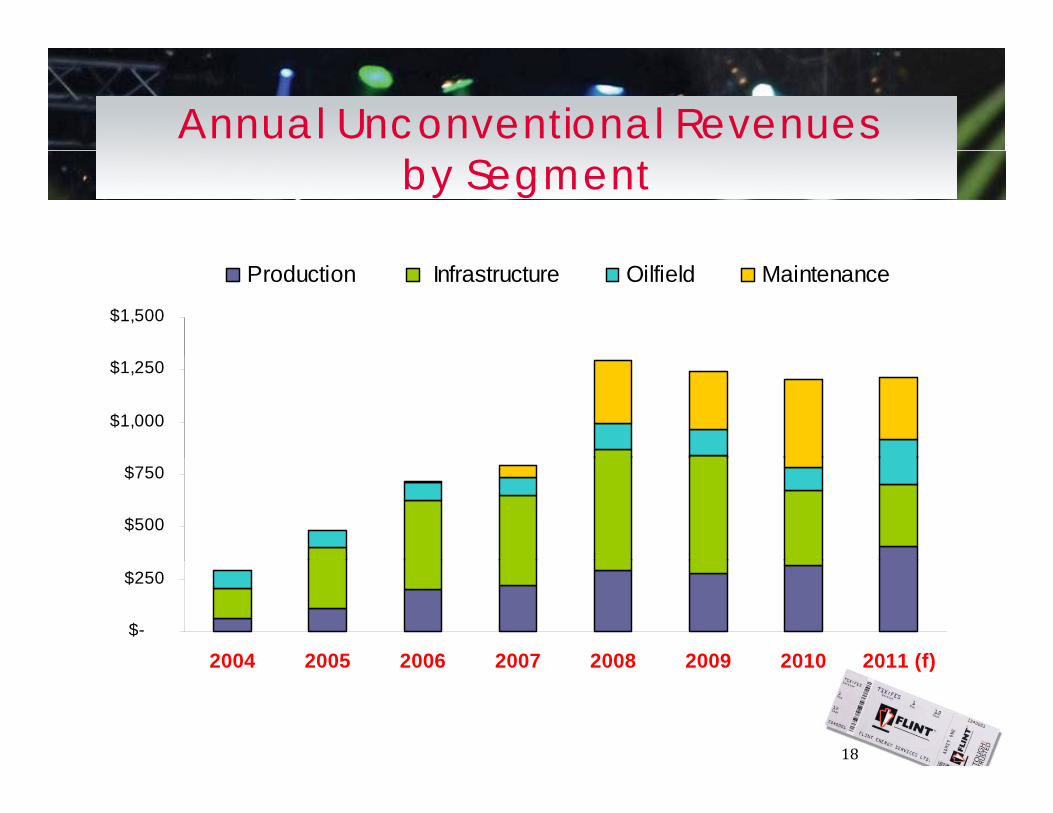

Annual Unconventional Revenues by Segment

$1,500

Production Infrastructure Oilfield Maintenance

$1,000

$1,250

$500

$750

$-

$250

2004 2005 2006 2007 2008 2009 2010 2011 (f)

18

2004 2005 2006 2007 2008 2009 2010 2011 (f)

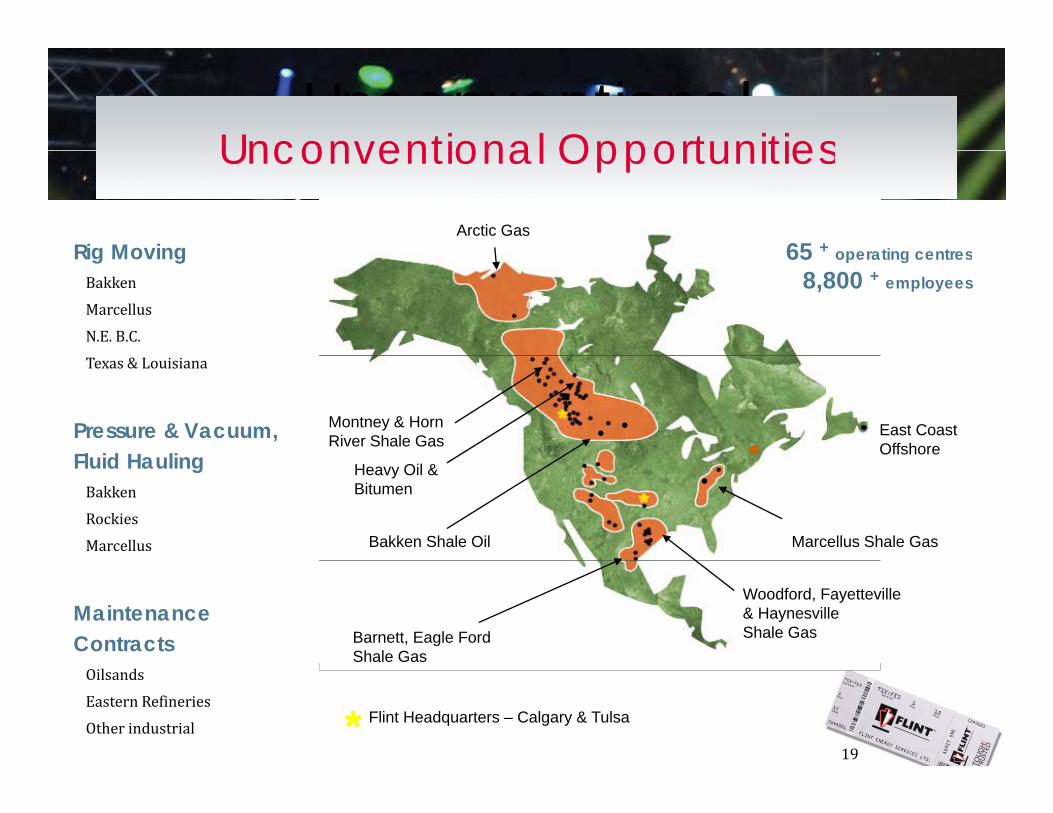

Unconventional i iUnconventional OpportunitiesOpportunities

Rig MovingArctic Gas

65 + operating centres

Unconventional Opportunities

Rig MovingBakken

Marcellus

N.E. B.C.

65 operating centres

8,800 + employees

Texas & Louisiana

Pressure & Vacuum, Fluid Hauling

Montney & Horn River Shale Gas

East CoastOffshoreFluid Hauling

Bakken

Rockies

Marcellus Bakken Shale Oil Marcellus Shale Gas

Heavy Oil & Bitumen

Maintenance Contracts

Woodford, Fayetteville & HaynesvilleShale GasBarnett, Eagle Ford

Shale Gas

19

Oilsands

Eastern Refineries

Other industrial ** Flint Headquarters – Calgary & Tulsa

2011 Forecast Drivers

• US & Canadian drilling increased 33% and 43% ti l i 2010 t il i d

2011 Forecast Drivers

respectively in 2010 on stronger oil prices and increased shale gas activity. We expect activity to remain strong in 2011.

• Mid stream capital spending has picked up in both• Mid‐stream capital spending has picked up in both Canada and the US.

• Oil sands capital spending reached an estimated $14 to $15 billion in 2010 and is projected to increase to24” pipeline installation near Fort McMurray AB to $15 billion in 2010, and is projected to increase to $22 billion by 2014 with a number of new project approvals and stable oil pricing.

• WTI crude oil is forecast in the $100 ‐ $110/bbl

24 pipeline installation near Fort McMurray, AB

WTI crude oil is forecast in the $100 $110/bbl range in 2011, and increase to $115/bbl by 2015.

• Natural gas is expected to trade below $5/mcf from 2011 through 2015.

20

0 t oug 0 5

70 acre module fabrication yard, Sherwood Park, AB

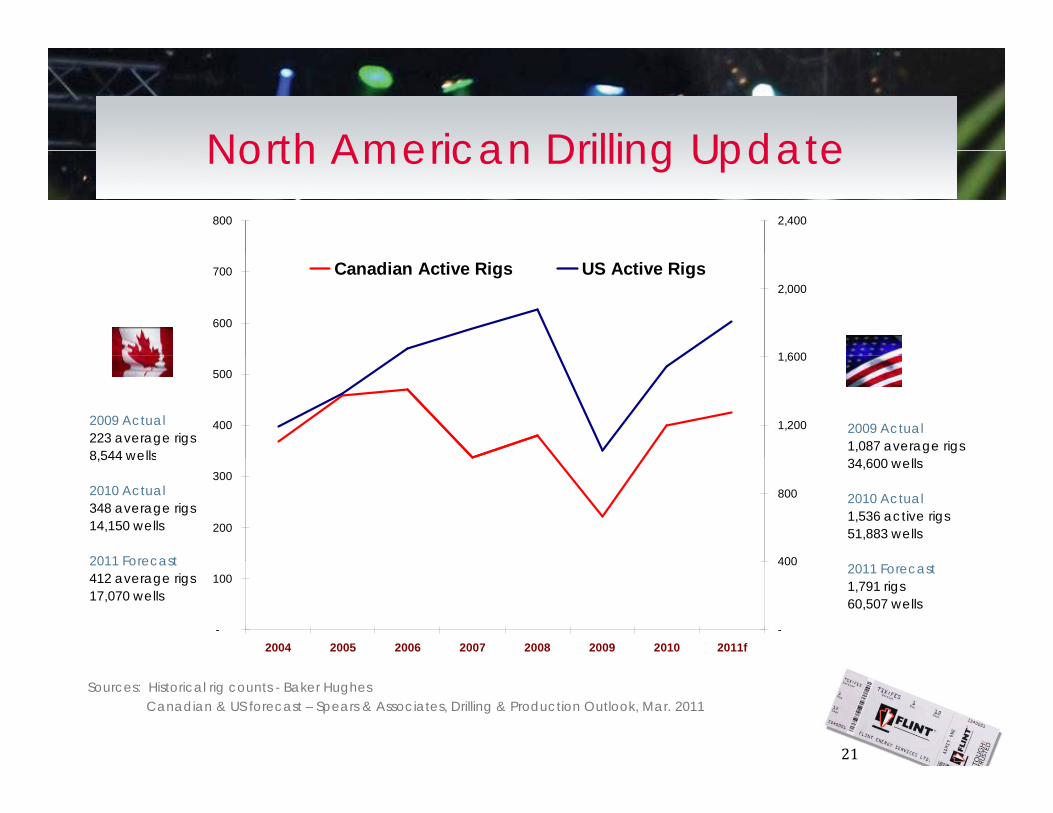

North American Drilling Update800 2,400

North American Drilling Update

600

700

1 600

2,000Canadian Active Rigs US Active Rigs

2009 Actual223 average rigs 8 544 wells

400

500

1,200

1,600

2009 Actual1,087 average rigs

8,544 wells

2010 Actual 348 average rigs 14,150 wells

2011 Forecast

200

300

400

800

34,600 wells

2010 Actual 1,536 active rigs 51,883 wells

2011 Forecast 412 average rigs17,070 wells

-

100

2004 2005 2006 2007 2008 2009 2010 2011f-

400 2011 Forecast 1,791 rigs60,507 wells

21

Sources: Historical rig counts - Baker HughesCanadian & US forecast – Spears & Associates, Drilling & Production Outlook, Mar. 2011

Flint’s Oil Sands Construction ActivitiesFlint s Oil Sands Construction Activities

Current Contracts: Contract History:Suncor’s Firebag 3 ‐ site‐wide field construction

Suncor’s Firebag 4 ‐ module fabrication$108 million in contract backlog

Suncor’s Firebag 1 & 2 & Co‐GenSuncor’s Millennium Coker & Vacuum UnitsNexen’s Long Lake GasifierHusky’s Tucker Lake$108 million in contract backlog Husky s Tucker LakeConocoPhillips’ Surmont 1EnCana’s Foster CreekPetro‐Canada’s Mackay RiverShell’s Albian Sands Froth Treatment Statoil’s Leismer SAGD Project

Statoil Leismer SAGD Project

22Shell’s Albian Sands Mine – froth treatment facility

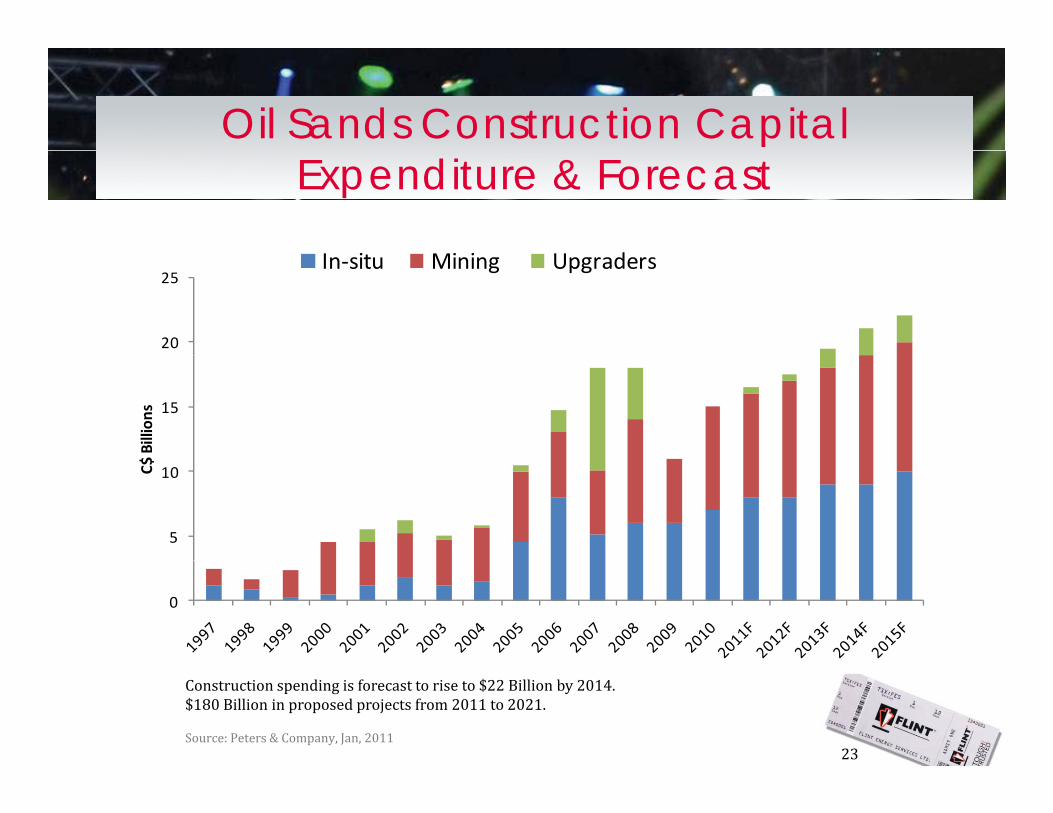

Oil Sands Construction Capital Expenditure & Forecast

i i i d

20

25In‐situ Mining Upgraders

15

$ Billion

s

5

10C$

0

23

Construction spending is forecast to rise to $22 Billion by 2014.$180 Billion in proposed projects from 2011 to 2021.

Source: Peters & Company, Jan, 2011

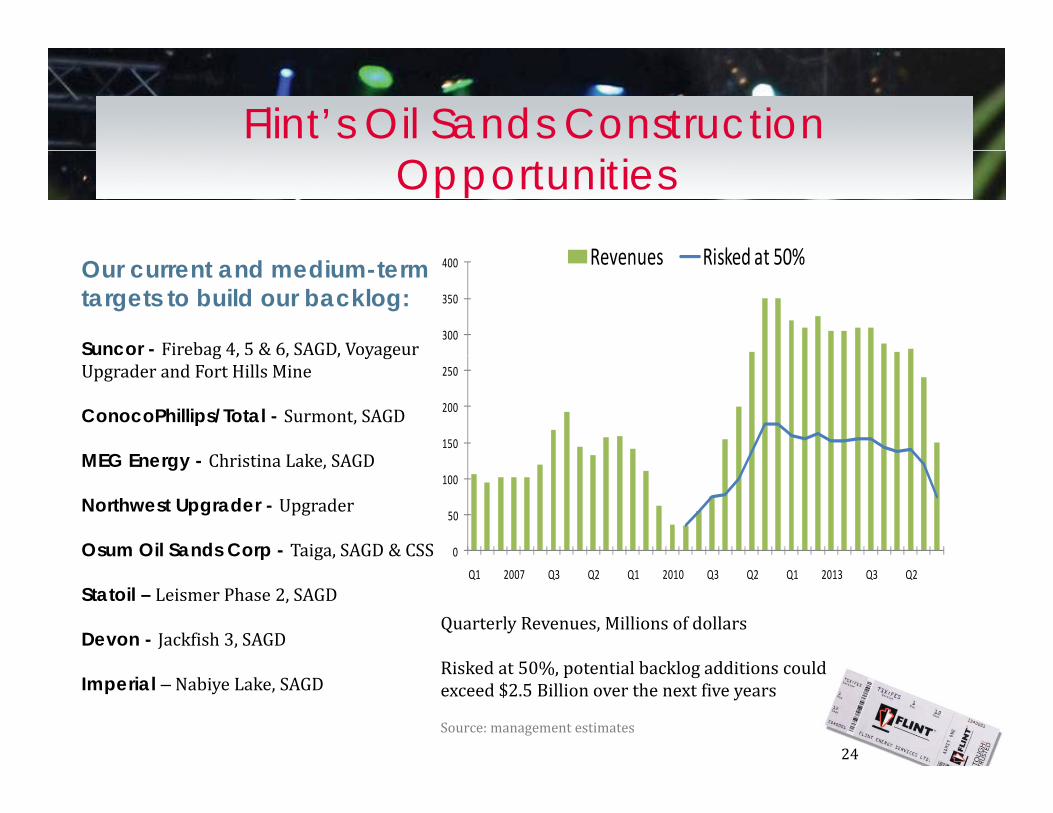

Flint’s Oil Sands Construction Opportunities

Revenues Risked at 50%

300

350

400 Revenues Risked at 50%Our current and medium-term targets to build our backlog:

Suncor - Firebag 4, 5 & 6, SAGD, Voyageur

150

200

250

g , , , y gUpgrader and Fort Hills Mine

ConocoPhillips/Total - Surmont, SAGD

MEG Energy Christina Lake SAGD

0

50

100MEG Energy - Christina Lake, SAGD

Northwest Upgrader - Upgrader

Osum Oil Sands Corp - Taiga, SAGD & CSSQ1 2007 Q3 Q2 Q1 2010 Q3 Q2 Q1 2013 Q3 Q2

Quarterly Revenues, Millions of dollars

Ri k d 50% i l b kl ddi i ld

Statoil – Leismer Phase 2, SAGD

Devon - Jackfish 3, SAGD

24

Risked at 50%, potential backlog additions could exceed $2.5 Billion over the next five years

Source: management estimates

Imperial – Nabiye Lake, SAGD

Flint’s Maintenance StrategyFlint’s Oilsands Maintenance gy‘Build it, then Maintain it’

Flint s Oilsands Maintenance

•Bitumen production is expected to increase to over 2.2 million bbl/day by 2015

Oilsands Production & Maintenance Forecast

2.5 Daily Production Annual Maintenance

•Maintenance spending projected to increase 10% annually to $1.6 billion in 2015•Flint’s 50% owned FT Services has

1.0

1.5

2.0

t s 50% o ed Se v ces asthree multi‐year contracts with major oil sands producers•Over $2.1 billion in contracted maintenance backlog 50% to Flint

0.0

0.5

2007 2008 2009e 2010e 2011e 2012e 2013e 2014e 2015e

maintenance backlog 50% to Flint•Maintenance typically covers : day‐to‐day maintenance, sustaining capital, turnarounds, and managing

Millions of barrels per day, Billions of dollars annuallySource: CAPP Oilsands production forecast, Oilsands Review 10/10Maintenance costs adapted from Peters & Company ‐ Oilsands Maintenance

h 2008

25

third party services Forecast March 2008

Wear TechnologiesInnerArmorWh ?

Wear Technologies

Why?– High wear and corrosion issues for

bitumen producers– Complements existing fabrication p g

and maintenance services

What?– Diamond hard carbon coating– Diamond hard carbon coating– Highly resistant to wear and

corrosion

St tStatus– 17 test parts in service with three

different clients– Manufacturing operations in

26

g pCalgary

Wear TechnologiesThermoplastic LinersWhat?

Wear Technologies

What?– Thermoplastic elastomer lined pipe– Development partnership with

DuPont Canada

Why?– Hydro‐slurry pipelines supplying

bitumen to the plants and tailings lines have short life cycles and high y gmaintenance costs

– High level of focus for producers– Viable solutions available are limited

Status– 30” elastomer‐lined test spool for an

oil sands producer in place since October 2010

27

Summary2011 Initiatives Fli t ill

Summary

Flint will:• Capture new opportunities/build backlog in our Facility Infrastructure

segment• Redeploy capital equipment from less active areas to more active North

American basins ongoing• Reduce costs of delivery to improve operating margins ongoing• Commercialize new technologies• Pursue additional strategic growth initiatives

28

St t i ll P iti dStrategically Positioned

Fi i ll StFinancially Strong

Diversified Integrated ServicesDiversified, Integrated Services

InnovativeInnovative

An Encore Performer

29