get retirement ready. - charles schwab...

TRANSCRIPT

Get retirement ready.

Schwab Moneywise®

Workshop Series Month Day, Year

Schwab Retirement Plan Services 2

Today we’ll talk about

Debunking common assumptions

Putting your plan together

Managing your portfolio while you are waiting

Taking the next step

Schwab Retirement Plan Services

What are your assumptions about retirement? A few common misconceptions:

“I’ve heard I’ll only need 70-80% of my pre-retirement income.”

“When I retire I’ll be in a lower tax bracket.”

“I plan to keep working if I do not have enough.”

“I’ve built up a solid nest egg so interest and dividends will provide all I need in retirement.”

3

Schwab Retirement Plan Services

Put your plan together.

4

Schwab Retirement Plan Services

Put your plan together

Information to consider:

Age now and when you want to retire

Tolerance for risk

Current income

How much you have saved now and plan to save each year

Estimated Social Security benefits – Learn more at SSA.gov

Estimated pension or other income

Expected annual spending

Review, adjust and manage your portfolio allocations

5

Schwab Retirement Plan Services

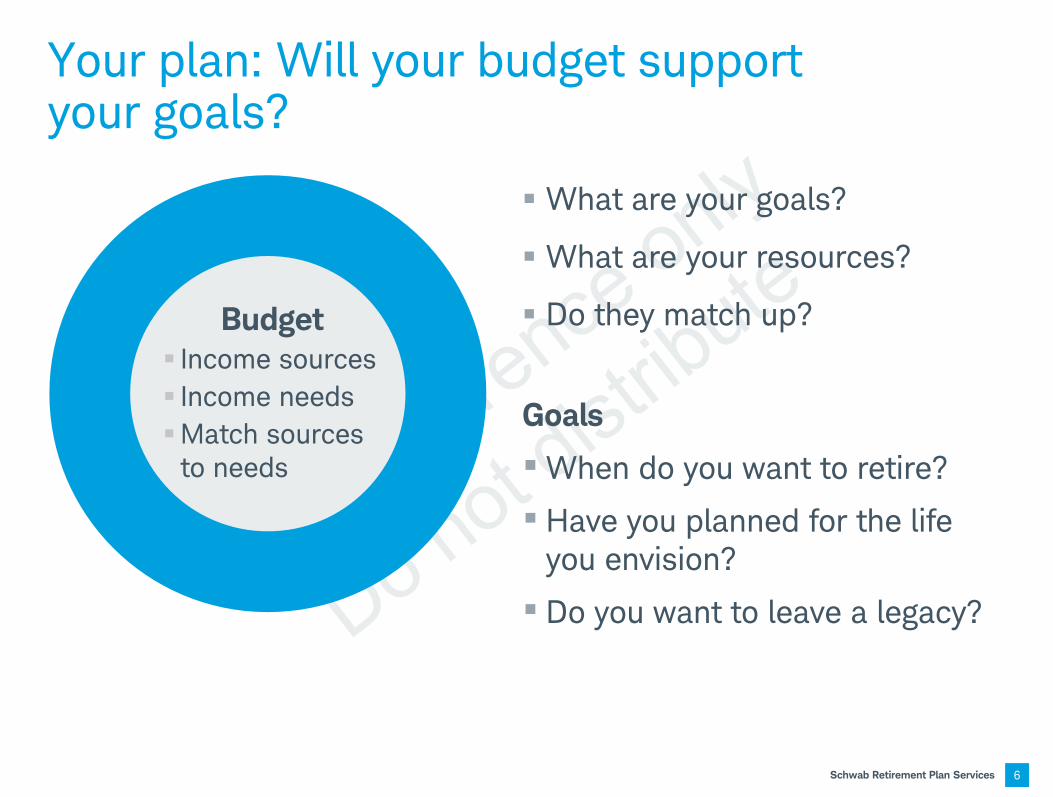

Your plan: Will your budget support your goals?

6

What are your goals?

What are your resources?

Do they match up?

Goals

•When do you want to retire?

• Have you planned for the life you envision?

• Do you want to leave a legacy?

Goals

Budget Income sources Income needs Match sources

to needs

Schwab Retirement Plan Services

When do you want to retire? Age:

Will your resources support your budget? Consider these important factors

Income:

What are your income sources and how much will they generate for you?

Expenses: What expenses will you have in retirement?

Have you saved enough to sustain your expenses throughout retirement?

Savings:

7

Schwab Retirement Plan Services

Calculate your portfolio income requirements

8

Estimated expenses Regular income sources

What your portfolio must provide

= –

Essential Housing Taxes Food and utilities Health Care and insurance Discretionary Travel and entertainment Gifts, hobbies,

memberships

Non-investment income Social Security Employment Rental income Pension Annuities

Investment income Principal Capital gains Interest and dividends Lump sums

Schwab Retirement Plan Services

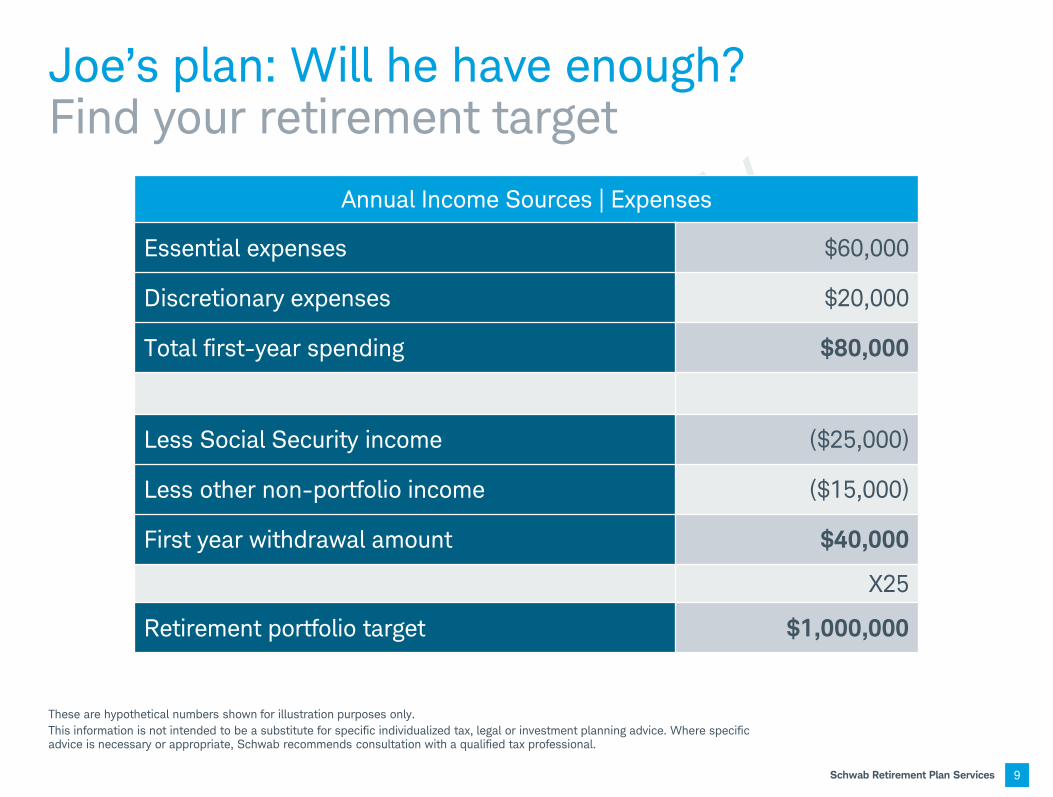

Joe’s plan: Will he have enough? Find your retirement target

Annual Income Sources | Expenses

Essential expenses $60,000

Discretionary expenses $20,000

Total first-year spending $80,000

Less Social Security income ($25,000)

Less other non-portfolio income ($15,000)

First year withdrawal amount $40,000

X25

Retirement portfolio target $1,000,000

9

These are hypothetical numbers shown for illustration purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax professional.

Schwab Retirement Plan Services

Joe’s plan: Will he have enough? Find your retirement target Assumptions:

Portfolio accumulation of $1,000,000

Income $80,000 / year

3% inflation

Social Security and other income unchanged

These are hypothetical numbers shown for illustration purposes only. This information is not intended to be a substitute for specific individualized tax, legal or investment planning advice. Where specific advice is necessary or appropriate, Schwab recommends consultation with a qualified tax professional.

Annual Income Sources

Social Security $25,000

Other non-portfolio $15,000

Portfolio – Initial X 4% $40,000

$80,000

Annual Income Sources

Social Security $25,000

Other non-portfolio $15,000

Portfolio – Year 2 X 3% $41,200

$81,200

Annual Income Sources

Social Security $25,000

Other non-portfolio $15,000

Portfolio – Year 3 X 3% $42,436

$83,436

10

Schwab Retirement Plan Services

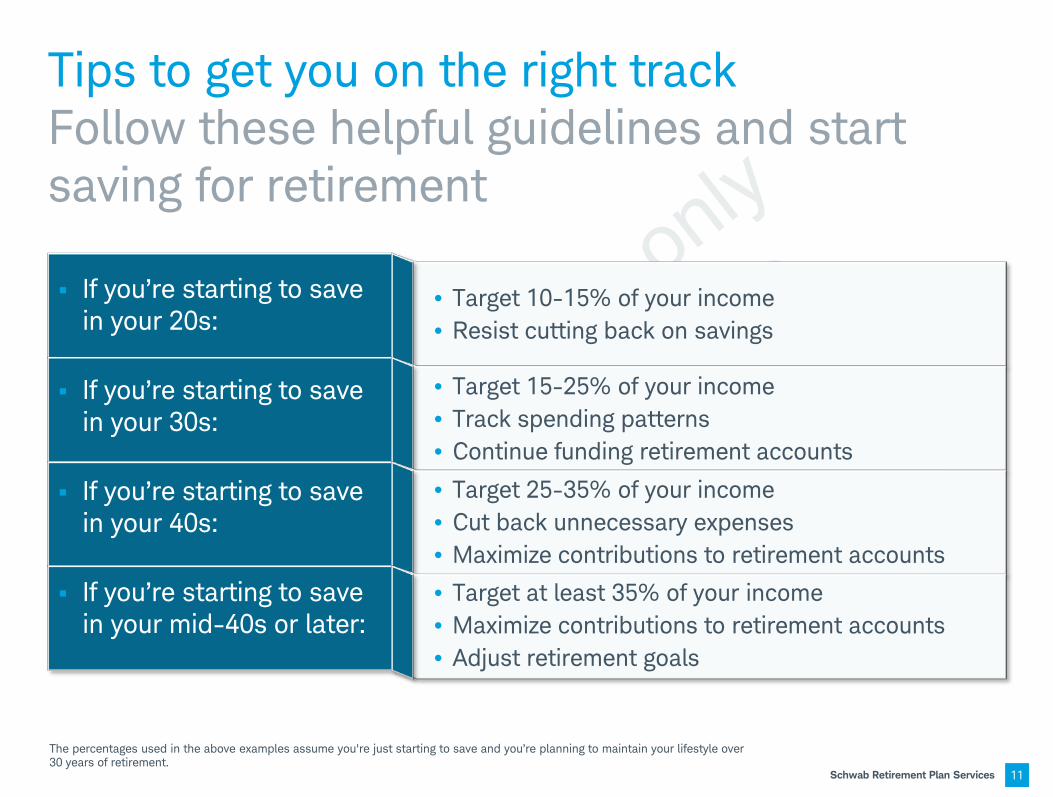

Tips to get you on the right track Follow these helpful guidelines and start saving for retirement

The percentages used in the above examples assume you're just starting to save and you’re planning to maintain your lifestyle over 30 years of retirement.

11

If you’re starting to save in your 20s:

If you’re starting to save in your 30s:

If you’re starting to save in your 40s:

If you’re starting to save in your mid-40s or later:

• Target 10-15% of your income • Resist cutting back on savings

• Target 15-25% of your income • Track spending patterns • Continue funding retirement accounts

• Target 25-35% of your income • Cut back unnecessary expenses • Maximize contributions to retirement accounts

• Target at least 35% of your income • Maximize contributions to retirement accounts • Adjust retirement goals

Schwab Retirement Plan Services

Save more aggressively

Invest efficiently

Spend less in retirement

Delay retirement

Contribute more to retirement plans

Make annual savings adjustments

If you get a bonus, raise or promotion, don’t change your spending habits

Make catch-up contributions

Open additional retirement savings accounts

12

Your plan: Ideas to boost savings

Dennis Getting ready for a long retirement

Get retirement ready

Hear from real people via multi-media experience

Schwab Retirement Plan Services

Manage Your portfolio.

14

Schwab Retirement Plan Services

Your portfolio: Common questions

15

I’m facing hard times, should I tap into my 401k?

My portfolio keeps losing money, can I retire as planned?

Given the market’s moves, should I change my investment mix?

As a retiree, how big of a cash cushion should I have?

Can I count on dividends going forward?

Schwab Retirement Plan Services

Your portfolio: Models for nearing and in retirement

16

Age 60 - 69 Age 70 - 79 Age 80+

Return: (1970 - 2012) Return: (1970 - 2012) Return: (1970 - 2012) Average annual return: 9.6% Average annual return: 9.1% Average annual return: 8.0%

Best year: 30.9% Best year: 27.0% Best year: 22.8%

Worst year: -20.9% Worst year: -12.5% Worst year: -4.6%

Source: Schwab Center for Financial Research with data provided by Morningstar, Inc. The return figures are the average, the maximum and the minimum annual returns of hypothetical asset allocation plans. The asset allocation plans are weighted averages of the performance of the indices used to represent each asset class in the plans and are rebalanced annually. The Conservative allocation is composed of 15% large-cap stocks, 5% international stocks, 50% bonds, and 30% cash. The Moderately Conservative allocation is composed of 25% large-cap stocks, 5% small-cap stocks, 10% international stocks, 50% bonds, and 10% cash. The Moderate allocation is composed of 35% large-cap stocks, 10% small-cap stocks, 15% international stocks, 35% bonds and 5% cash. The indices representing each asset class in the asset allocation plan are S&P 500®Index (large-cap stocks); Russell 2000® Index (small-cap stocks); MSCI EAFE ® net of taxes (international stocks); Barclays U.S. Aggregate Bond Index (bonds); and Citigroup U.S. 3-month Treasury bills (cash.

Long-Term Return Estimate: 5.1% Long-Term Return Estimate: 4.3% Long-Term Return Estimate: 3.5%

CRSP 6-8 was used for small-cap stocks prior to 1979, Ibbotson Intermediate-Term U.S. Government Bond Index was used for bonds prior to 1976, and Ibbotson U.S. 30-day Treasury bills was used prior to 1978. Results assume reinvestment of dividends and interest. Indices are unmanaged, do not incur fees or expenses and cannot be invested in directly. Past performance is no indication of future results. For more information on the methodology for the long-term return estimate calculations, see the Market Insight article “Q&A: Estimating Long-Term Market Returns”.

5%

60% 35%

Moderate Moderately Conservative

Equity Fixed Income Cash Investments

10%

40%

50%

20%

50%

30%

Conservative

Schwab Retirement Plan Services

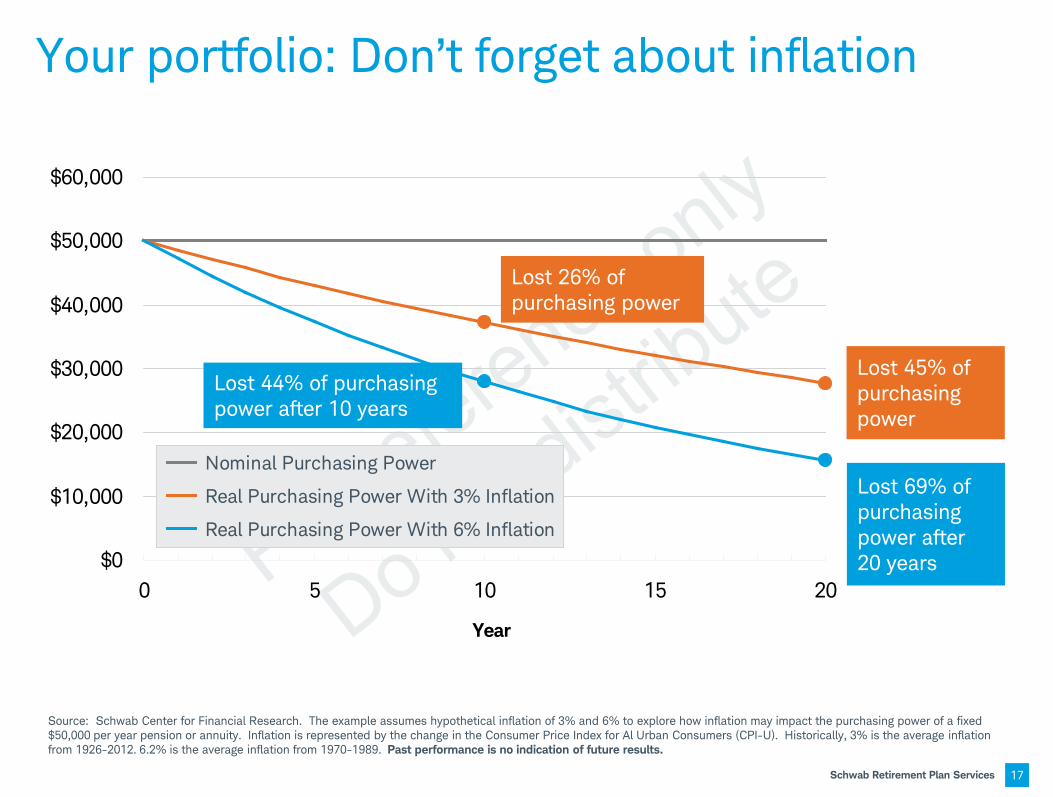

Source: Schwab Center for Financial Research. The example assumes hypothetical inflation of 3% and 6% to explore how inflation may impact the purchasing power of a fixed $50,000 per year pension or annuity. Inflation is represented by the change in the Consumer Price Index for Al Urban Consumers (CPI-U). Historically, 3% is the average inflation from 1926-2012. 6.2% is the average inflation from 1970-1989. Past performance is no indication of future results.

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

0 5 10 15 20

Year

Nominal Purchasing Power

Real Purchasing Power With 3% Inflation

Real Purchasing Power With 6% Inflation

Lost 44% of purchasing power after 10 years

Lost 26% of purchasing power

Lost 45% of purchasing power

Lost 69% of purchasing power after 20 years

Your portfolio: Don’t forget about inflation

17

Schwab Retirement Plan Services

Your portfolio: Importance of rebalancing Impact of market performance on initial 60% stocks, 40% bonds allocation

18

January 2003 to October 2007

Too much risk before bear market

Source: Schwab Center for Financial Research with data from Morningstar, Inc. The portfolio above is composed of 60% stocks and 40% bonds on 12/31/2002, and is not rebalanced through 10/31/2007. It is rebalanced to 60% stocks and 40% bonds on 10/31/07 and not rebalanced through 02/28/2009. Asset class allocations are derived from a weighted average of the total monthly returns of indices representing each asset class. The indices representing the asset classes are the S&P 500 Index (stocks) and the Barclays Capital U.S. Aggregate Bond Index (bonds). Returns assume reinvestment of dividends and interest. Indices are unmanaged, do not incur fees and expenses, and cannot be invested in directly.

Lost recovery potential before bull market

November 2007 to February 2009

40% 60%

30%

70%

60% 40%

Beginning Allocation (Balanced portfolio)

Ending Allocation (No rebalancing)

Schwab Retirement Plan Services

Take the next step.

19

Schwab Retirement Plan Services

Your next steps

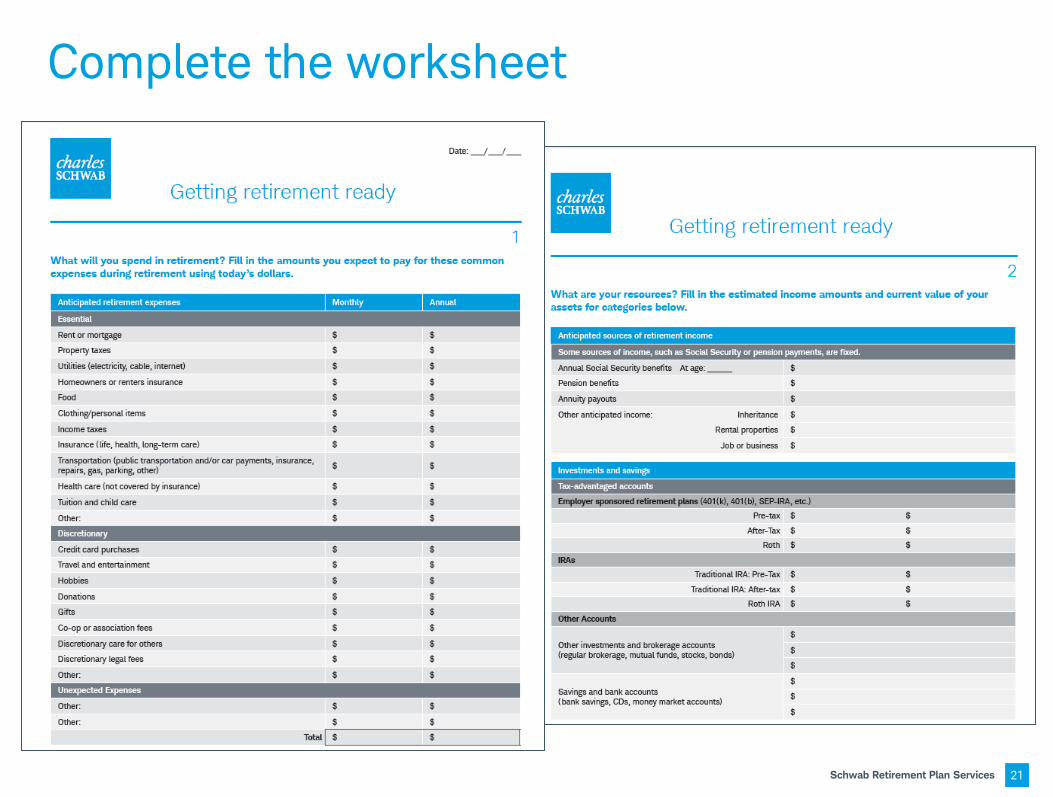

Gather information and complete the “Getting Retirement Ready” worksheet

Utilize the retirement calculator

Check out all the retirement resources available online

Check out your My Retirement Progress™ score

20

Schwab Retirement Plan Services

Complete the worksheet

21

Schwab Retirement Plan Services

Utilize the calculators

Find the retirement calculators on your home page on schwab.com/workplace

Calculators available for those individuals saving for retirement or retiring soon

22

Schwab Retirement Plan Services

Leverage the online resources available to you

23

Access to electronic services may be limited or unavailable during periods of peak demand, market volatility, systems upgrade, maintenance, or for other reasons.

schwab.com/realliferetirement

schwabsavingsfundamentals.com

schwabmoneywise.com

Schwab Retirement Plan Services

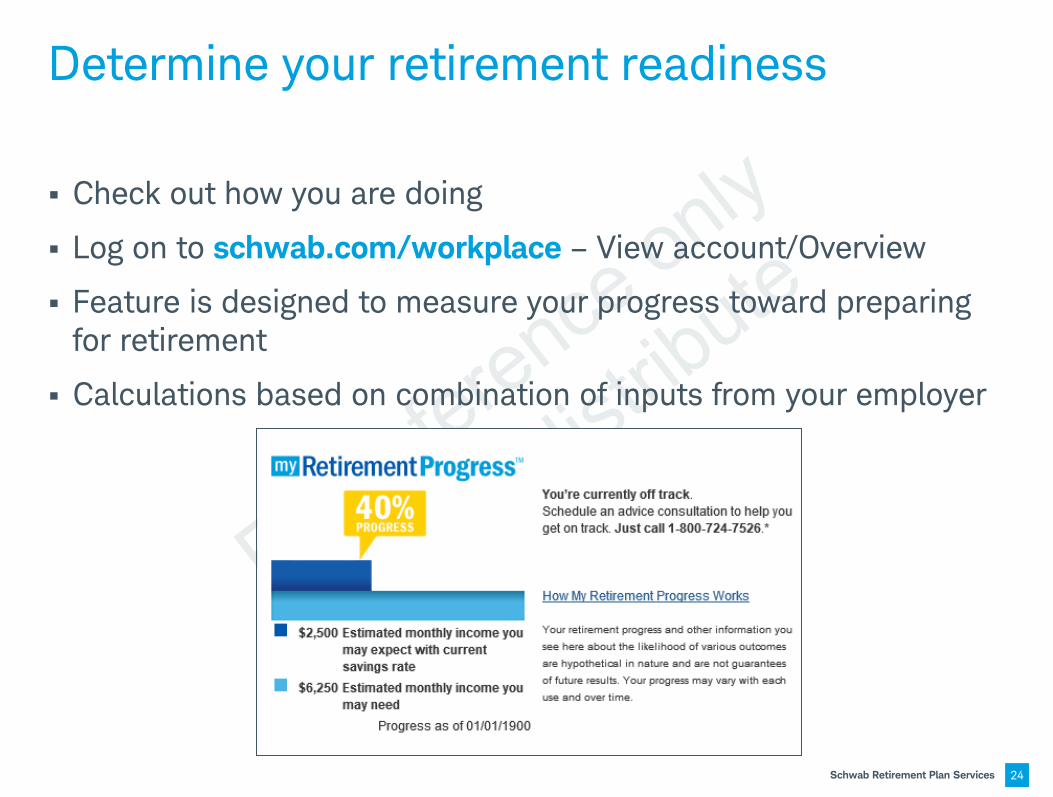

Determine your retirement readiness

Check out how you are doing

Log on to schwab.com/workplace – View account/Overview

Feature is designed to measure your progress toward preparing for retirement

Calculations based on combination of inputs from your employer

24

Schwab Retirement Plan Services

We are here to help

Go online to enroll, change contribution rate, access education, etc. www.schwab.com/workplace

Talk to someone - contact your Schwab Advice Consultant 800-724-7526 Ask question or enroll

in advice

Review your quarterly statement

25

Schwab Retirement Plan Services

Important information Apple, the Apple logo, and iPhone are trademarks of Apple Inc., registered in the U.S. and other countries. System availability and response times are subject to market conditions and mobile connection limitations. Android is a trademark of Google Inc. Use of this trademark is subject to Google Permissions. Amazon, Kindle, Kindle Fire, the Amazon Kindle logo, and the Kindle Fire logo are trademarks of Amazon.com, Inc. or its affiliates.

The Schwab Center for Financial Research is a division of Charles Schwab & Co., Inc.

The information in this presentation is for informational purposes only. It is not intended to be a substitute for specific individualized tax, legal or investment planning advice. Where specific advice is necessary or appropriate, consult with a qualified tax advisor, CPA, financial planner or investment manager.

Schwab Retirement Plan Services, Inc. provides recordkeeping and related services with respect to retirement plans and has provided this communication to you as part of the recordkeeping services it provides to the Plan.

The material contained herein is proprietary to Schwab Retirement Plan Services, Inc. ("SRPS”) and for informational purposes only. None of the information constitutes a recommendation by SRPS. The information is not intended to provide tax, legal, or investment advice. SRPS does not guarantee the suitability or potential value of any particular investment or information source. Certain information presented herein may be subject to change. Neither the presentation nor any information or material contained in it may be copied, assigned, transferred, disclosed, or utilized without the express written approval of SRPS.

Schwab Retirement Planner® provides participants with a retirement savings and investment strategy, a major component of which is a discretionary investment management service furnished by Morningstar Associates, LLC, an independent registered investment advisor and wholly owned subsidiary of Morningstar, Inc. Morningstar Associates is not affiliated with or an agent of Schwab Retirement Plan Services, Inc., Charles Schwab & Co., Inc., a federally registered investment advisor, or their affiliates. There is no guarantee a participant's savings and investment strategy will provide adequate income at or through their retirement. Fees are charged for Schwab Retirement Planner, including its discretionary investment management service, based on the participant's account balance.

Advice Consultants are not employees of Morningstar and act solely as facilitators to participants accessing the Morningstar service.

My Retirement Progress™ percentage is calculated by Schwab Retirement Plan Services, Inc. ("SRPS"), based on and using the data formulated by Morningstar Associates, LLC, an independent registered investment advisor and wholly owned subsidiary of Morningstar, Inc. Morningstar Associates formulates and provides estimated monthly income projections in retirement using savings and investment data and assumptions which include, but are not limited to, current retirement plan balance and savings rate, projected date of and estimated years in retirement, and 100% post-tax replacement income. SRPS cannot alter or influence any of the calculations that Morningstar Associates provides. SRPS then uses the projections formulated by Morningstar Associates to express the potential gap in retirement savings as a percentage that is made available as part of the retirement plan record keeping and related services provided by SRPS. Morningstar Associates is not affiliated with or an agent of SRPS, Charles Schwab & Co., Inc., a federally registered investment advisor, or their affiliates.. To obtain more information about how the percentage is calculated or to provide additional information that can impact My Retirement Progress calculations visit schwab.com/workplace or call 800-724-7526.

26 © ©2014 Schwab Retirement Plan Services, Inc. All rights reserved. (0214-0332)

Thank you.