global!real!estate:performance,...

TRANSCRIPT

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 1

GLOBAL REAL ESTATE: Performance, Strategies, Risks, Opportuni=es Simon Fairchild, ExecuFve Director, IPD

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 2

Discussion topics

PERFORMANCE Global trends, and performance cycle? Why focus on ciFes?

IMPLICATIONS What they mean from a strategic perspecFve?

OUTLOOK What are the risks and opportuniFes associated with global invesFng?

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 3

Global Index composiFon by market

3

Source: IPD, KTI

Eurozone / EMEA

38%

Asia Pacific

20%

Americas

42%

United States 38%

Canada 4% Germany

6% France 6%

Netherlands 3%

Japan 15%

Australia 4%

UK 7%

Switzerland 4%

Eurozone

21%

Other EMEA

17% Asia

Pacific

20%

Americas

42%

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 4

Global performance of direct real estate

Annual results based on local currency, unleveraged

Source: IPD

-15

-10

-5

0

5

10

15

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

3 Ye

ars

5 Ye

ars

10 Y

ears

% pa Capital growthIncome returnTotal return5-year annualised total return

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 5

15 14

11 9 9

7 7 7 6 6 6 6 6 5 5 4 4 4 4 4 3 3

2 1 1

-‐2 -‐2

10

5

0

5

10

15

20

South Africa

Canada

United States

Australia

New

Zealand

IPD Glob

al Inde

x

Korea

Switzerland

Sw

eden

Po

land

France

Austria

Finland

Norway

Czech Re

public

Germ

any

Pan-‐Eu

rope

an

Denm

ark

Japan

Belgium

UK

Ireland

Ita

ly

Nethe

rland

s Po

rtugal

Hungary

Spain

% pa Capital growth Income return Total return

Global total returns by country, 2012

Annual results based on local currency composite

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 6

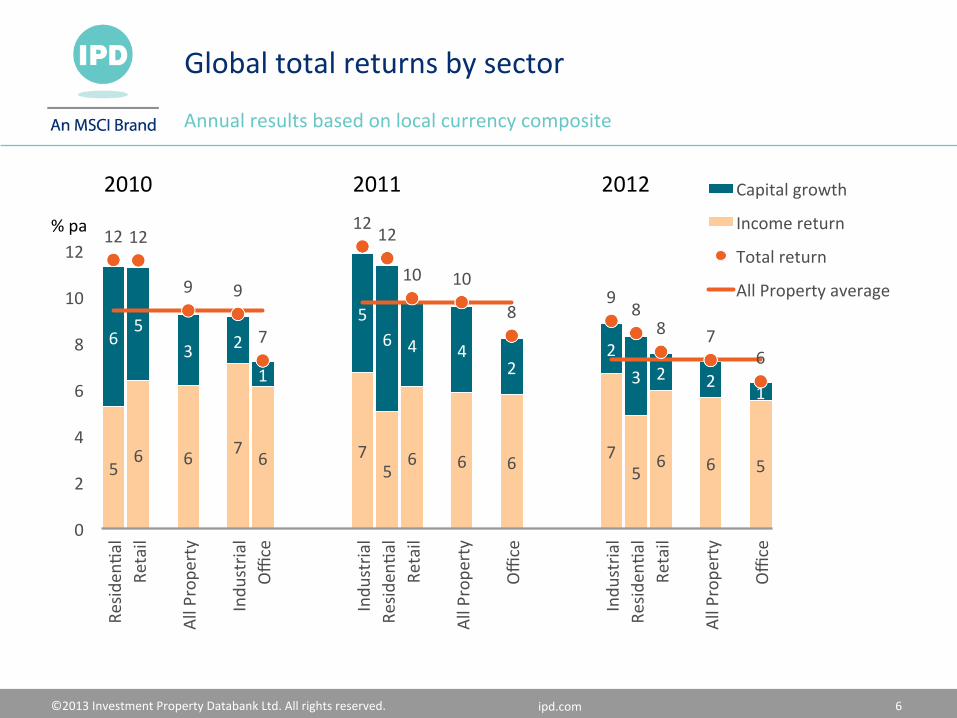

5 6 6 7 6 7

5 6 6 6 7

5 6 6 5

6 5

3 2

1

5 6 4 4

2 2

3 2 2 1

12 12

9 9

7

12 12

10 10

8 9

8 8 7

6

0

2

4

6

8

10

12

Resid

enFa

l Re

tail

All Prope

rty

Indu

stria

l Office

Indu

stria

l Re

siden

Fal

Retail

All Prope

rty

Office

Indu

stria

l Re

siden

Fal

Retail

All Prope

rty

Office

Capital growth

Income return

Total return

All Property average

Global total returns by sector

Annual results based on local currency composite

2010 2011 2012

% pa

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 7

IPD’s Coverage: Real estate performance on 180 major urban markets in 26 countries Today’s presentaFon focuses on performance in 67 of these ciFes

Source: IPD

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 8

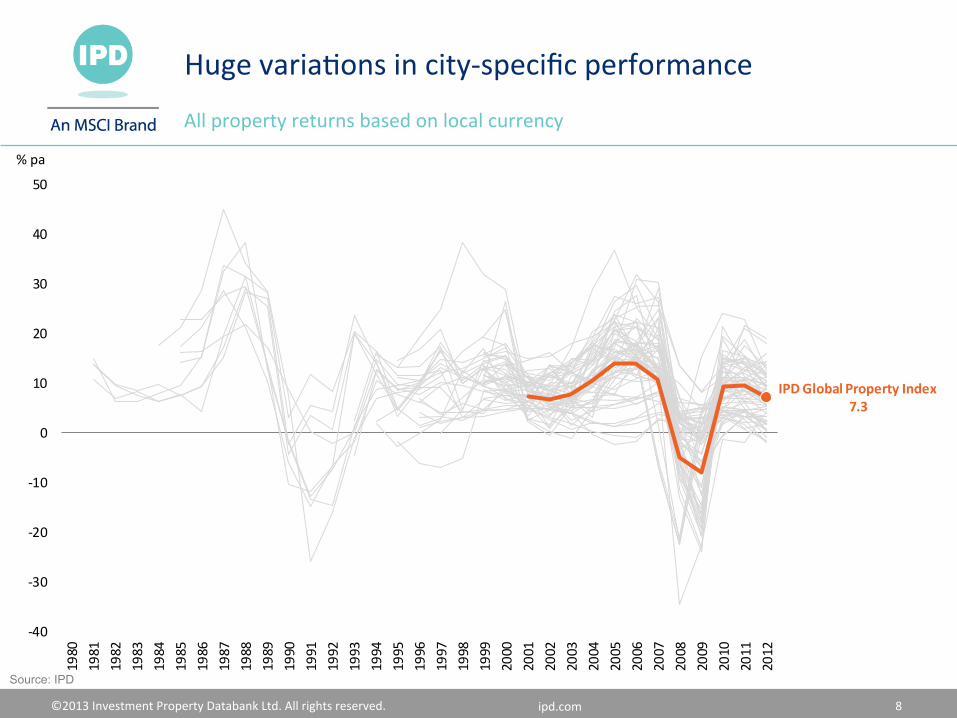

Huge variaFons in city-‐specific performance

All property returns based on local currency

Source: IPD

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

AP

AP

IPD Global Property Index7.3

-‐40

-‐30

-‐20

-‐10

0

10

20

30

40

50

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% pa

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 9

Capturing important differences in cyclical behaviour

All property returns based on local currency

Source: IPD

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

EMEA

AP

AP

London 8.2New York 9.6Hong Kong 12.5

-‐40

-‐30

-‐20

-‐10

0

10

20

30

40

50

1980

1981

1982

1983

1984

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

% pa

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 10

Sub-‐naFonal variaFons maeer

2012 performance for key ciFes across ten countries

Source: IPD

10

5

0

5

10

15

20

Calgary

►CA

NADA

Toronto

Mon

treal

Vancou

ver

San Diego

Houston

Seattle

Denver

San Francis

coBo

ston

Portland

Atlanta

►US

AMiami

Dallas

New York

Los A

ngeles

Chica

goPh

iladelphia

Minneapolis

Washington DC

Perth

Brisb

ane

Melbo

urne

►AU

STRA

LIA

Sydney

Auckland

►NE

W ZEA

LAND

Wellington

Toulou

seLyon

Paris

►FRAN

CEMarseille

Munich

Hambu

rg►

GERM

ANY

Dusseldo

rfFrankfurt

Berlin

Yokohama

►JAPAN

Tokyo

Osaka

Antwerp

►BE

LGIUM

Brussels

Lond

onManchester

►UK

Edinbu

rgh

Birm

ingham

Lisbo

n►

PORT

UGAL

Porto

% pa Capital growthIncome returnTotal returnCountry average

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 11

Discussion topics

PERFORMANCE Global trends, and performance cycle? Why focus on ciFes?

IMPLICATIONS What they mean from a strategic perspecFve?

OUTLOOK What are the risks and opportuniFes associated with global invesFng?

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 12

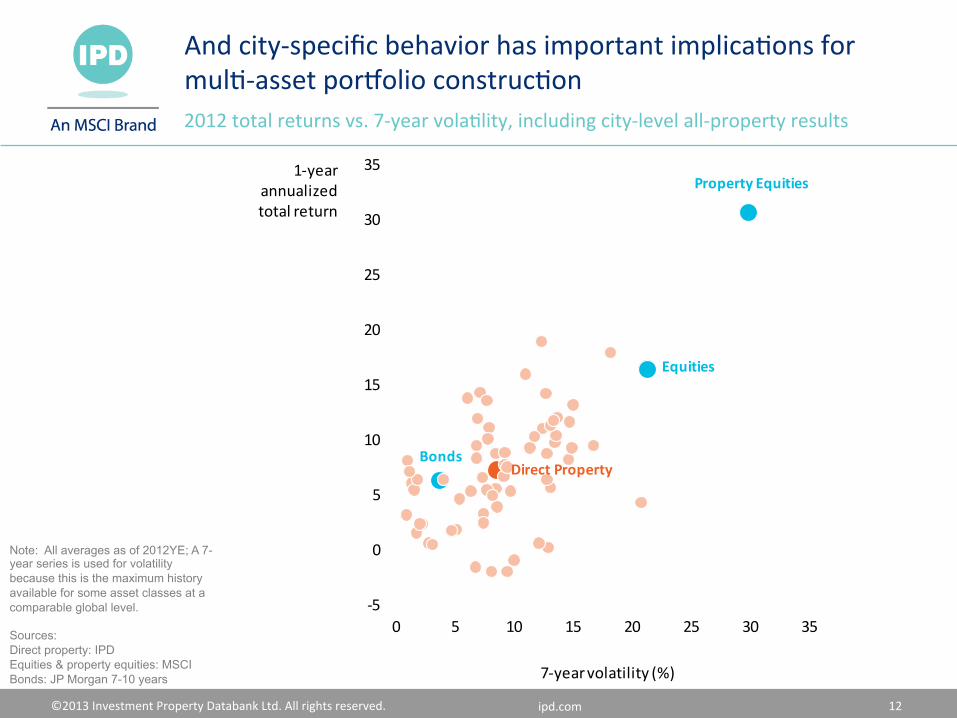

And city-‐specific behavior has important implicaFons for mulF-‐asset porfolio construcFon 2012 total returns vs. 7-‐year volaFlity, including city-‐level all-‐property results

Note: All averages as of 2012YE; A 7-year series is used for volatility because this is the maximum history available for some asset classes at a comparable global level. Sources: Direct property: IPD Equities & property equities: MSCI Bonds: JP Morgan 7-10 years

-‐5

0

5

10

15

20

25

30

35

0 5 10 15 20 25 30 35

1-‐year annualized total return

Property Equities

Equities

BondsDirect Property

7-‐year volatility (%)

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 13

Note: Annual results based on local currency composite; selected cities shown where data are available Source: IPD, KTI (Finland)

Cape Town

DublinFrankfurt

Johannesburg

London

Paris

Perth

Sydney

Calgary

New York

0

2

4

6

8

10

12

14

16

18

20

0 5 10 15 20Volatility (%)

Total return (%)

l EMEAl Asia Pacificl Americas

Tota

l Ret

urn,

%

Toronto

Performance behavior varies across markets 10 year annualised results based on local currency

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 14

Despite these variaFons within ciFes, there are paeerns in the behavior of different types of office market Capital growth 2009-‐12 for four disFnct types of city

Note: Capital values in the office sector indexed to 2009, the turning point of the global financial crisis Source: IPD

Commodity cities Financial & capital citiesManagement of mining, oil, and gas activities Management of strategic global finance or diplomacy

Technical cities National "second" citiesManagement of engineering, technology, and R&D Major cities that are upstaged globally by a larger national peer

80

90

100

110

120

130

140

15020

09

2010

2011

2012

2009 = 100 PerthCalgaryOsloJohannesburgHouston

80

90

100

110

120

130

140

150

2009

2010

2011

2012

2009 = 100 ParisLondonNew YorkHong KongWashington DC

80

90

100

110

120

130

140

150

2009

2010

2011

2012

2009 = 100 MelbourneLyonManchesterChicagoOsaka

80

90

100

110

120

130

140

150

2009

2010

2011

2012

2009 = 100 MunichSeoulStockholmSan DiegoSeattle

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 15

European office markets

2012 total returns for office properFes

Source: IPD Global Cities Report

l Strong (10% or more)

l Moderate (5-‐9%)

l Weak (0-‐5%)

l Declining

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 16

Sub-‐market variaFons are also highly important...

2012 total returns for office properFes

Source: IPD UK Quarterly Digest

l Strong (10% or more)

l Moderate (5-‐9%)

l Weak (0-‐5%)

l Declining▬ 10-‐year annualised

-‐2

0

2

4

6

8

10

12

OuterLondon

UK average City InnerLondon

West End

% pa

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 17

... As are asset-‐specific variaFons

2012 total returns for London properFes*

*Includes office properties as well as other property types Source: IPD

0

50

100

150

200

250

300

350

400

-‐20 -‐15 -‐10 -‐5 0 5 10 15 20 25 30

Number of Assets

2012 Total Return (year over year)

Median TR5.4%

Declining TR18% of assets

>10% TR22% of assets

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 18

Asia: Total returns by market

Annual results based on local currency

0

5

10

15

20

25

China

Hong Kon

g

Indo

nesia

Japan

Korea

Malaysia

Singapore

Taiwan

Thailand

Pan-‐Asia

2010

2011

2012

% pa

8.8

5.5 5.9 6.2

-‐5

0

5

10

15

20

2007 2008 2009 2010 2011 2012 6-‐year annualised

% pa Retail Office Industrial Pan-‐Asia All Property

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 19

Discussion topics

PERFORMANCE Global trends, and performance cycle? Why focus on ciFes?

IMPLICATIONS What they mean from a strategic perspecFve?

OUTLOOK What are the risks and opportuniFes associated with global invesFng?

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 20

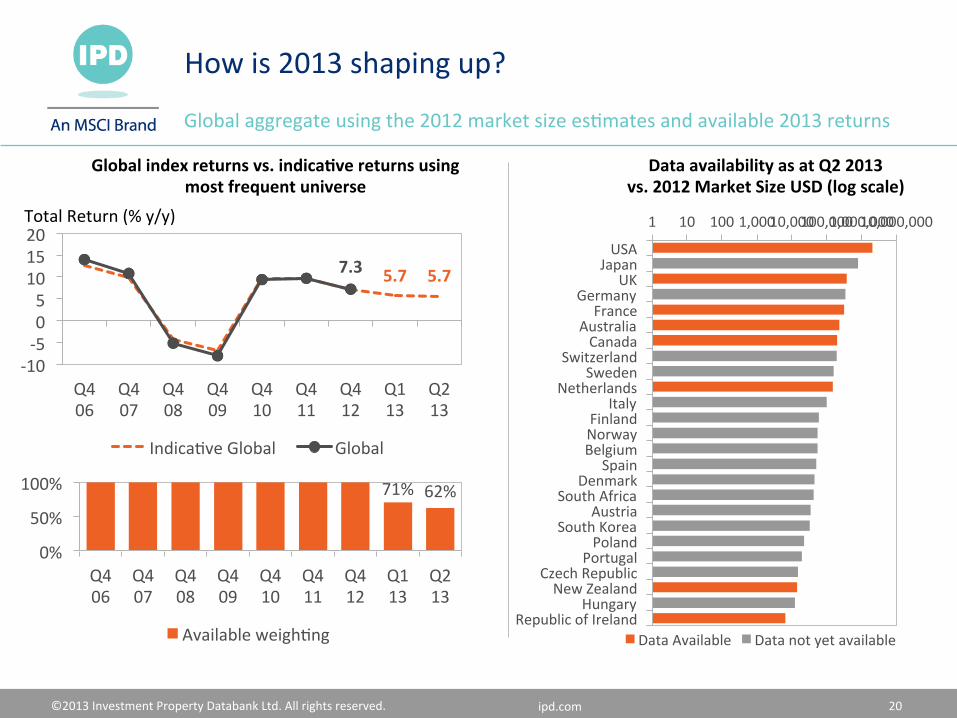

How is 2013 shaping up?

Global aggregate using the 2012 market size esFmates and available 2013 returns

5.7 5.7 7.3

-‐10 -‐5 0 5 10 15 20

Q4 06

Q4 07

Q4 08

Q4 09

Q4 10

Q4 11

Q4 12

Q1 13

Q2 13

IndicaFve Global Global

71% 62%

0%

50%

100%

Q4 06

Q4 07

Q4 08

Q4 09

Q4 10

Q4 11

Q4 12

Q1 13

Q2 13

Available weighFng

Total Return (% y/y) 1 10 100 1,000 10,000 100,000 1,000,000 10,000,000

USA Japan

UK Germany

France Australia Canada

Switzerland Sweden

Netherlands Italy

Finland Norway Belgium

Spain Denmark

South Africa Austria

South Korea Poland

Portugal Czech Republic New Zealand

Hungary Republic of Ireland

Data Available Data not yet available

Data availability as at Q2 2013 vs. 2012 Market Size USD (log scale)

Global index returns vs. indica=ve returns using most frequent universe

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 21

30

40

50

60

70

80

90

100

110

120

2007

2008

2009

2010

2011

2012

Q1 13

Q2 13

Denmark

Germany

Czech Republic

Japan

Belgium

Republic of Ireland

Netherlands

Italy

Portugal

Hungary

Spain

Global 30

40

50

60

70

80

90

100

110

120

2007

2008

2009

2010

2011

2012

Q1 13

Q2 13

Canada

South Africa

USA

Sweden

Switzerland

Global

France

Australia

UK

Austria

South Korea

Norway

Poland

New Zealand

Finland

Capital value performance in this cycle

CV Index 2007 = 100 CV Index 2007 = 100

Recovering Markets Lagging Markets

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 22

25 30 35 40 45 50 55 60 65 70 75 80 85 90 95

100 105 110

2007

2008

2009

2010

2011

2012

Q1 13

Q2 13

San Diego Denver Portland Washington DC Houston San Francisco Boston Seaele Dallas Philadelphia Los Angeles New York Miami Chicago Minneapolis Atlanta Global

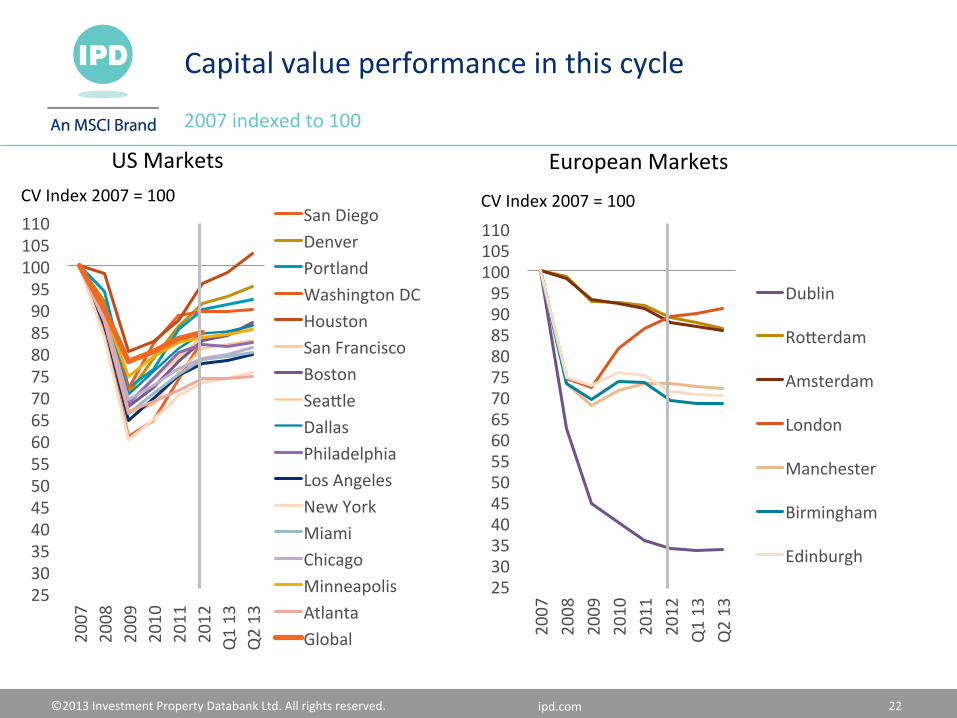

Capital value performance in this cycle

2007 indexed to 100

CV Index 2007 = 100 CV Index 2007 = 100

US Markets European Markets

25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100 105 110

2007

2008

2009

2010

2011

2012

Q1 13

Q2 13

Dublin

Roeerdam

Amsterdam

London

Manchester

Birmingham

Edinburgh

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 23

CiFes are at different stages of their cycle across global markets 2012 performance vs 3-‐year annualized

Source: IPD

Antwerp Paris

Berlin

MunichDublin

Rotterdam

Oslo

Warsaw

Stockholm

Perth

Sydney

Osaka

Tokyo

Calgary

Toronto

Atlanta

Houston

New York

Philadelphia

San Diego

San FranciscoSeattle

Washington DC

Johannesburg

Madrid

Auckland

Geneva

Birmingham

London

-‐10

-‐5

0

5

10

15

20

25

-‐5 0 5 10 15 20

3-‐year annualized (%)

2012annual

(%)

l EMEAl Asia Pacificl Americas

— globalofficeaverage

IMPROVING PEAKING

SLUGGISH SLIPPING

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 24

Performance momentum slowing, but huge variaFons persist All property returns, year-‐over-‐year

Source: IPD

-‐5

0

5

10

15

20

25

Calgary

San Diego

Houston

Cape Tow

nPerth

Toronto

Johann

esbu

rgSeattle

HongKo

ngDe

nver

Mon

treal

San Francisco

Boston

Portland

Vancou

ver

Atlanta

Miami

Dallas

Auckland

Brisb

ane

New

York

Melbo

urne

Los A

ngeles

Chicago

Toulou

seSydn

eyPh

ilade

lphia

Lyon

Lond

onGe

neva

Paris

Singapore

Minneapolis

Zurich

Seou

lStockholm

Mun

ich

Antw

erp

Washington DC

Vienna

Manchester

Oslo

Marseille

Hambu

rgWarsaw

Wellington

Yokohama

Copenh

agen

Dublin

Prague

Tokyo

Dusseldo

rfOsaka

Brussels

Frankfurt

Rotterdam

Lisbon

Amsterdam

Berlin

Milan

Edinbu

rgh

Rome

Birm

ingham

Budape

stPo

rto

Madrid

Barcelon

a

2010

2011

2012

% pa

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 25

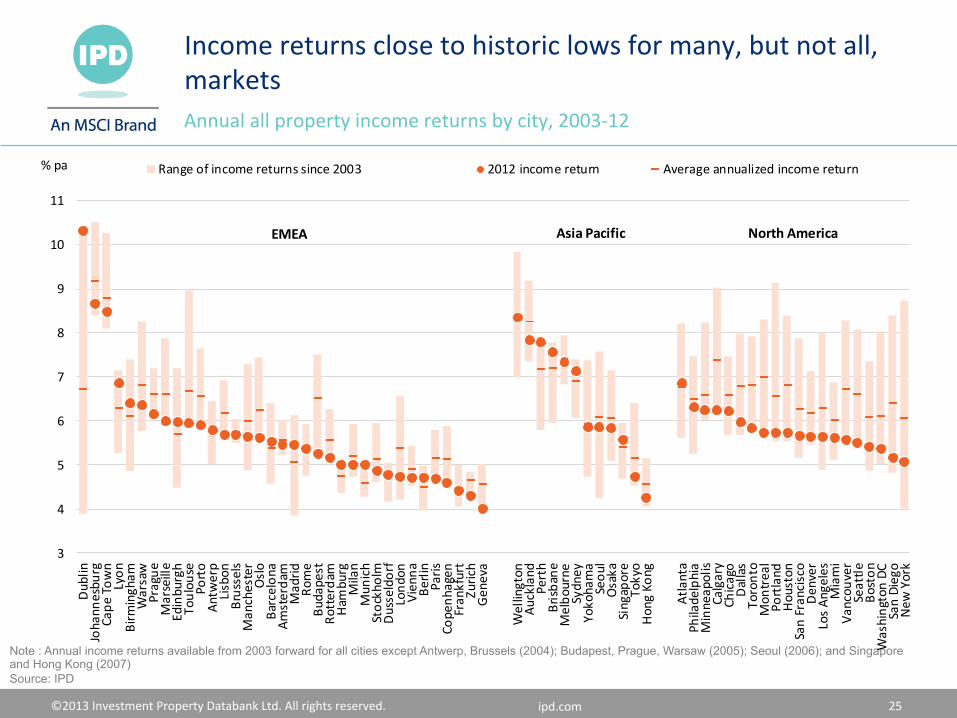

Income returns close to historic lows for many, but not all, markets Annual all property income returns by city, 2003-‐12

Note : Annual income returns available from 2003 forward for all cities except Antwerp, Brussels (2004); Budapest, Prague, Warsaw (2005); Seoul (2006); and Singapore and Hong Kong (2007) Source: IPD

3

4

5

6

7

8

9

10

11

Dublin

Johann

esbu

rgCape Tow

nLyon

Birm

ingham

Warsaw

Prague

Marseille

Edinburgh

Toulou

sePo

rto

Antw

erp

Lisbon

Brussels

Manchester

Oslo

Barcelon

aAm

sterdam

Madrid

Rome

Budapest

Rotterdam

Ham

burg

Milan

Mun

ich

Stockholm

Dusseldorf

Lond

onVienna

Berlin

Paris

Copenh

agen

Frankfurt

Zurich

Geneva

Wellington

Auckland

Perth

Brisbane

Melbo

urne

Sydney

Yokohama

Seou

lOsaka

Singapore

Tokyo

Hong Ko

ng

Atlanta

Philadelphia

Minneapolis

Calgary

Chicago

Dallas

Toronto

Mon

treal

Portland

Houston

San Francisco

Denver

Los An

geles

Miami

Vancou

ver

Seattle

Boston

Washington DC

San Diego

New

York

Range of income returns since 2003 2012 income return Average annualized income return% pa

North AmericaAsia PacificEMEA

©2013 Investment Property Databank Ltd. All rights reserved. ipd.com 26

Where next for the pricing of real estate?

Spread between IPD all property local yield and 10-‐year naFonal bond yield

Source: IPD & OECD

Berlin London Paris Zurich Tokyo Sydney New York Toronto

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%

0

1

2

3

4

5

6

7

8

9

10

11

12

2002

2004

2006

2008

2010

2012

%