insurtech what’s in it for the customer

TRANSCRIPT

IoT: What’s in it for the customer?

Matteo Carbone

@mcIns_

London, June 13

#InsurIoT

The background of the thoughts I will share with you today

Principal@ Bain & Company

• Financial Service and Digital Practices

• 12 years strategic consulting experience

• Focused on insurance and innovation

InsurtechInfluencer

• Speaker and writer on insurance innovation

• Insurance Thought Leader

• Top 50 InsurTechInfluencer

Founder of Connected Insurance Observatory

• Responsible of the Observatory on Telematics, Connected Insurance and Innovation

• Advisor of more than 50 international players on Insurance IoT

50

#InsurIoTMatteo Carbone

I founded a think thank focused on Insurance IoT

More than 45 players joined this first edition of the Observatory

Insurers

30 Insurers part of Insurance Groups

representing 66% of the P&C Italian insurance

market

Reisurers

3 primary International Reinsures30 3

Aiba Appian Aubay DigitalTech

Guidewire IRSA SYSDATA Vodafone Automotive

Belron

Portolano Cavallo

Studio legale

#InsurIoTMatteo Carbone

Insurance IoT is not about things, is about connecting insurance with people and their risks

Connected insurance:

Applications

Health Industrial risksAutomotive Building Life

insurance solution that provides the use

of sensors for collecting data on the state of an insured risk and

telematics for the remote transmission of the collected data and

their use on the Insurance value chain

Surce: ConncetedInsurance Observatory

#InsurIoTMatteo Carbone

Black-box

More than 4 Millions of insurance black boxes fitted in

the cars +4

Penetration

Telematics represent 16% of the auto insurance contracts sold and renewed at Q4 '15 16%

Best practice

One of the main Italian insurance Groups reached a penetration greater

than 40% on his auto insurance portfolio

>40%Insurers

26 Insurers are offering a motor third part liability cover telematics based on the Italian market

26

Insurance telematics is mainstream in Italy

65% NOW!

65% of the Insurers at the Connected Insurance Observatory have already seen a material impact of telematics on the Italian auto insurance marketSource: Connected Insurance Observatory

#InsurIoTMatteo Carbone

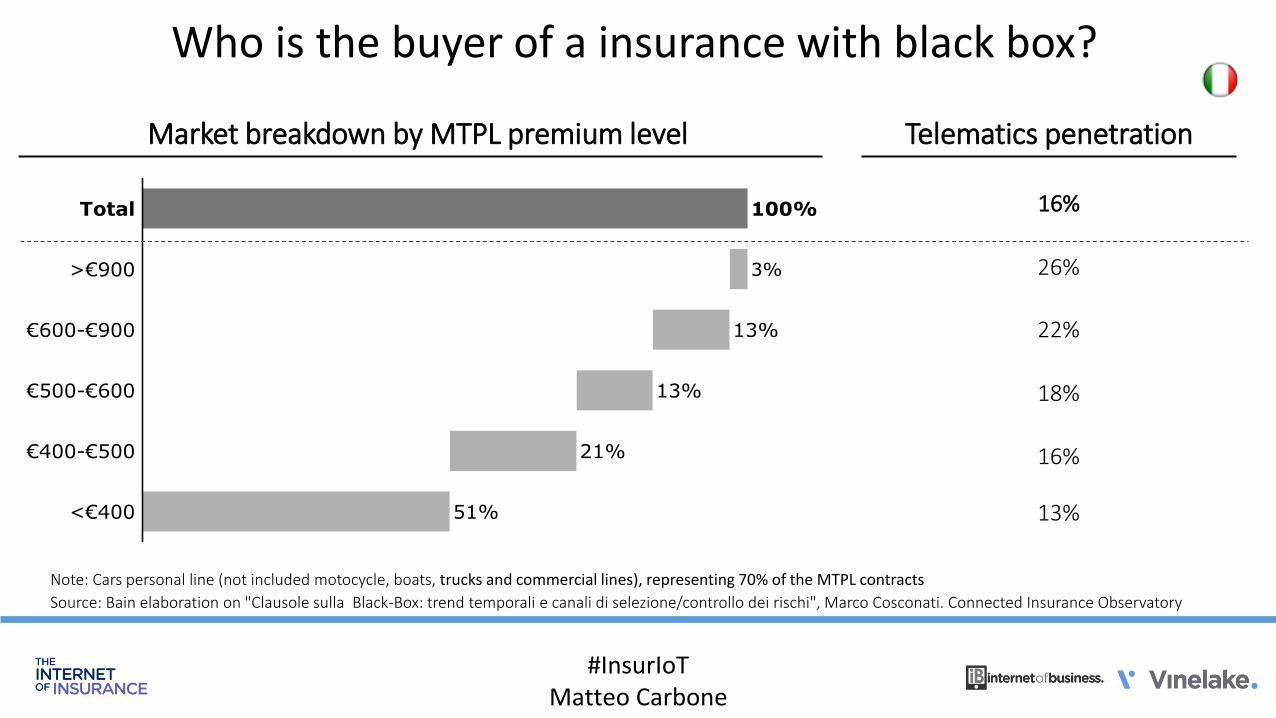

Who is the buyer of a insurance with black box?

#InsurIoTMatteo Carbone

Source: Bain elaboration on "RCA e black box: analisi degli acquirenti", Sergio Desantis. Connected Insurance Observatory

Telematics penetration on MTPL policies by age

Age

Who is the buyer of a insurance with black box?

Source: Bain elaboration on "Clausole sulla Black-Box: trend temporali e canali di selezione/controllo dei rischi", Marco Cosconati. Connected Insurance Observatory

Note: Cars personal line (not included motocycle, boats, trucks and commercial lines), representing 70% of the MTPL contracts

Market breakdown by MTPL premium level Telematics penetration

16%

26%

22%

18%

16%

13%

#InsurIoTMatteo Carbone

The client perspective

MTPL +theft (discounted) + black box MTPL (discounted) + black box

When the value increase is positive and material, there is an effective use case for the client and a selling speech for the distributor

#InsurIoTMatteo Carbone

Source: Connected Insurance Observatory

Why motor insurance telematics?

“I am the Career Genie.

I grant 3 wishes that help people

along with their jobs.” “For my first wish, I would like safe drivers

to buy my Motor insurance product”

Source: From an Andrew Dart's article originally appeared in the Asia Insurance Review, September 2014 editionImage: Courtesy from cliparts.co

"Genie, I'm an Insurance CEO"

“It’s done, now you have the black box”

#InsurIoTMatteo Carbone

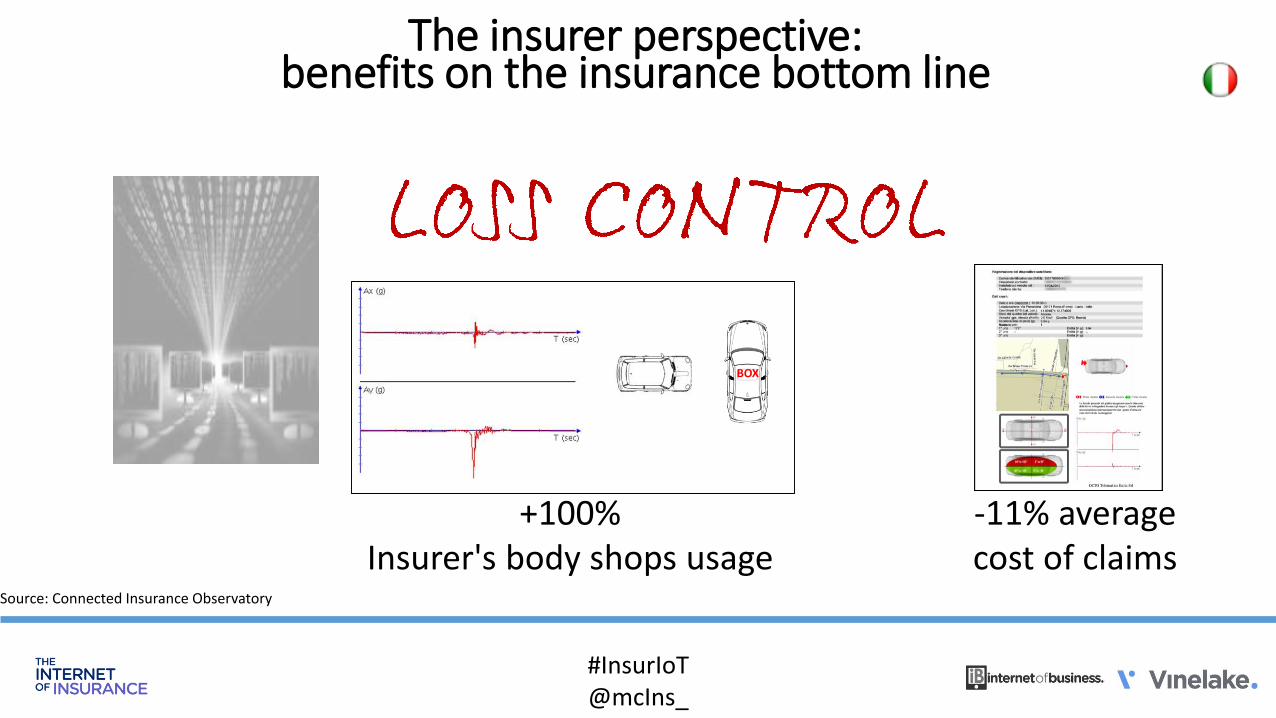

The insurer perspective: benefits on the insurance bottom line

Matteo Carbone, 28 April 2016

#InsurIoTMatteo Carbone

MTPL claims frequency

-20%

Surce: Connceted Insurance Observatory

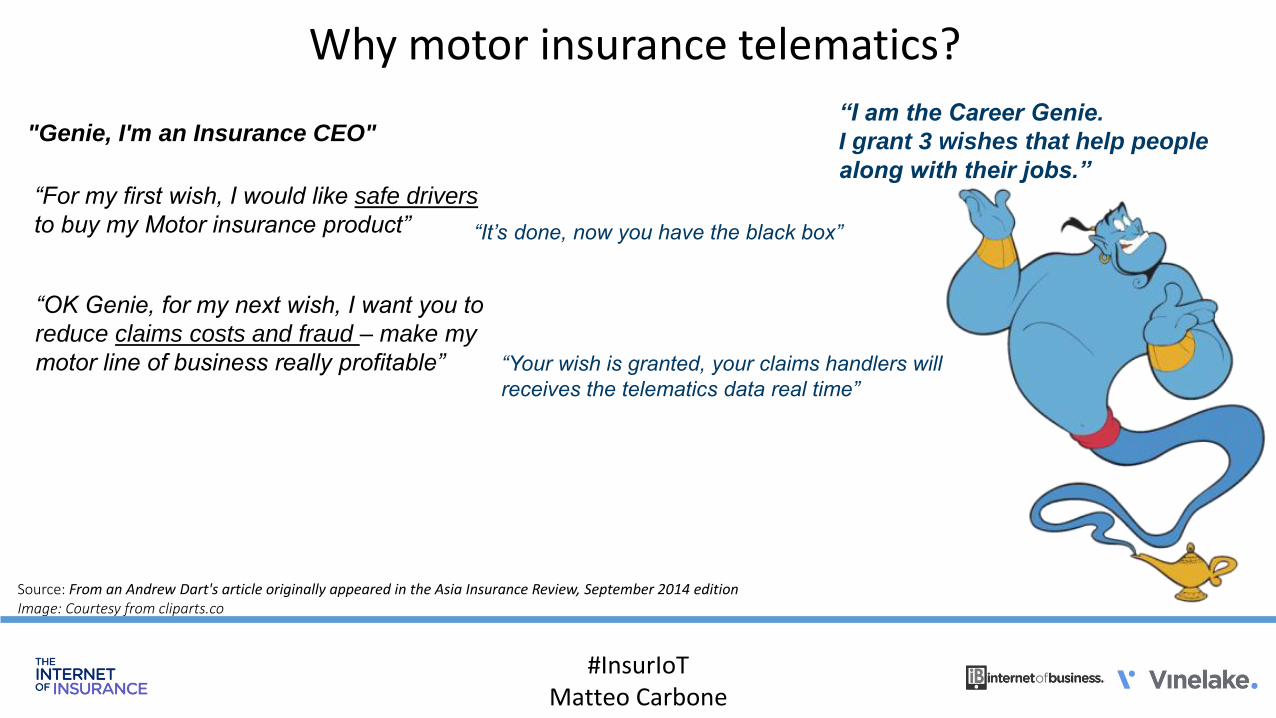

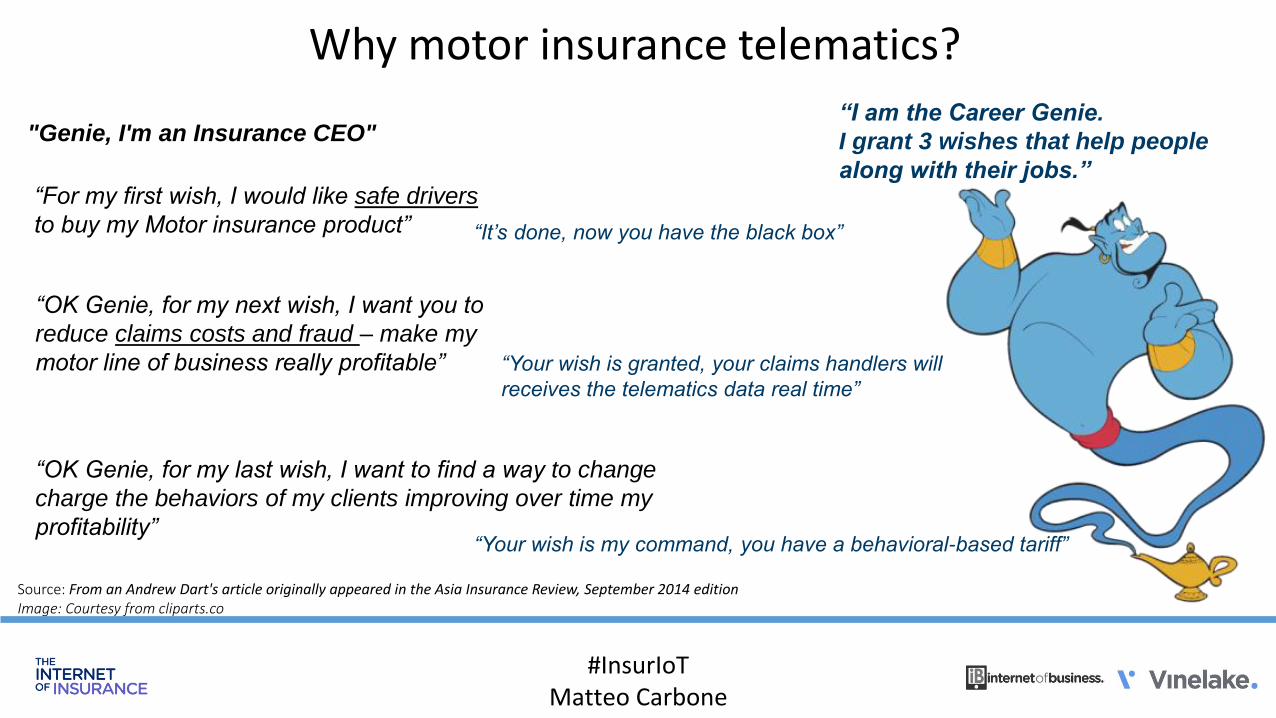

Why motor insurance telematics?

“I am the Career Genie.

I grant 3 wishes that help people

along with their jobs.” “For my first wish, I would like safe drivers

to buy my Motor insurance product”

“OK Genie, for my next wish, I want you to

reduce claims costs and fraud – make my

motor line of business really profitable”

Source: From an Andrew Dart's article originally appeared in the Asia Insurance Review, September 2014 editionImage: Courtesy from cliparts.co

"Genie, I'm an Insurance CEO"

“It’s done, now you have the black box”

“Your wish is granted, your claims handlers will

receives the telematics data real time”

#InsurIoTMatteo Carbone

The insurer perspective: benefits on the insurance bottom line

Matteo Carbone, 28 April 2016

#InsurIoT@mcIns_

+100%Insurer's body shops usage

BOX

-11% average cost of claims

Source: Connected Insurance Observatory

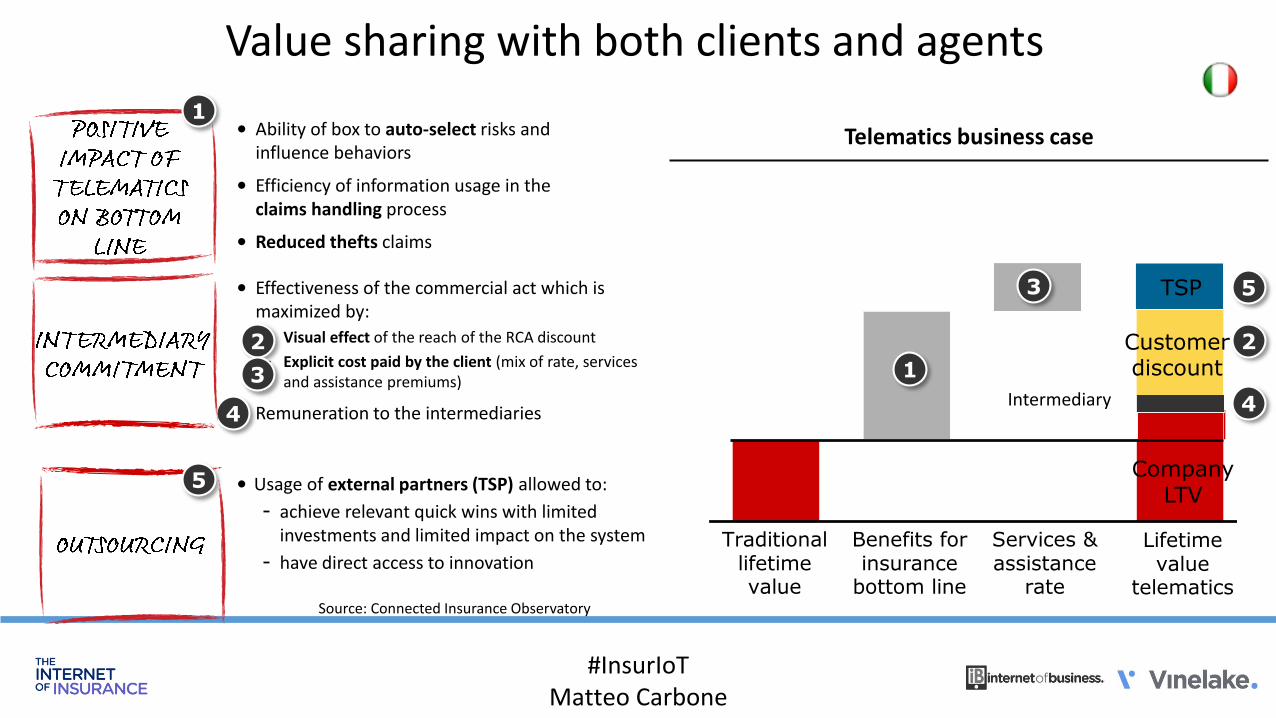

• Ability of box to auto-select risks and influence behaviors

• Efficiency of information usage in the claims handling process

• Reduced thefts claims

• Usage of external partners (TSP) allowed to:

- achieve relevant quick wins with limited investments and limited impact on the system

- have direct access to innovation

• Effectiveness of the commercial act which is maximized by:

- Visual effect of the reach of the RCA discount

- Explicit cost paid by the client (mix of rate, services and assistance premiums)

• Remuneration to the intermediaries

Value sharing with both clients and agents

Traditionallifetimevalue

Benefits forinsurance

bottom line

Services & assistance

rate

Customerdiscount

TSP

Lifetimevalue

telematics

CompanyLTV

• Distributor

Telematics business case1

1

2

3

2

3 5

44Intermediary

#InsurIoTMatteo Carbone

5

Source: Connected Insurance Observatory

Why motor insurance telematics?

“I am the Career Genie.

I grant 3 wishes that help people

along with their jobs.” “For my first wish, I would like safe drivers

to buy my Motor insurance product”

“OK Genie, for my next wish, I want you to

reduce claims costs and fraud – make my

motor line of business really profitable”

“OK Genie, for my last wish, I want to find a way to change

charge the behaviors of my clients improving over time my

profitability”

Source: From an Andrew Dart's article originally appeared in the Asia Insurance Review, September 2014 editionImage: Courtesy from cliparts.co

"Genie, I'm an Insurance CEO"

“It’s done, now you have the black box”

“Your wish is granted, your claims handlers will

receives the telematics data real time”

“Your wish is my command, you have a behavioral-based tariff”

#InsurIoTMatteo Carbone

Basic black-box PAYD PHYD0

20

40

60

80

100%10

Premium adjustment

17 9

At renewalAt renewal

Premium adjustment

Tariff benchmarking – March '16 Number of products

The market was not focused on pricing telematics-based, but the approached are becoming more sophisticated

Market offer evolutionNumber of products

Flat discount

#InsurIoTMatteo Carbone

Source: Connected Insurance Observatory

Why risk-based pricing?

Premium adjustment based on the behaviors, with a mechanism understandable and communicable

Risk-based pricing to offer a competitive renewal rate to the low risk client, in order to retain them and improve the technical profitability of the auto insurance telematics portfolio

Make clients less riskyRetention

of low risk clients

• How to engage the client?

• Is a discount on the insurance rate at renewal enough?

• Other reward could be used?

• Which variables are really effective to identify the low risk clients?

• With the discount diffusion on the low risk clients, how to manage the technical equilibrium of the part of the portfolio without telematics?

#InsurIoTMatteo Carbone

Other ways to change behaviors

Economics auto telematics

Traditionallifetimevalue

Partnerscontribu-

tions

Discounts/cash back to the client

Fee for ecosystemof partners

Fee for the intermediary

Lifetimevalue

telematics

LTV for the Insurer

Benefits on the

insurancebottom line

Additionalfees

Weather alert based on geo-localization

5

Antitheft service if the box registers a different-than-usual driving

style

3

"Live" concierge supporting navigation

1

Alert if the vehicle exits a "safe area" (or enters an

"unsafe area") of the city, defined by the client

(e.g. parental control options)

4

Alert in case speed limits are

exceeded

2

Highway/ parking area tolling

6

Road or medical

assistance via dedicated button

7

Simplified claim notification,

including automatic form fill-in based

on telematics data

8

Damages Photo

Claims feature

Claim certification

at client's disposal

Automatic assistance to the client on

the premises in case of severe

accident9

10

11

Client assistance and personalized

case management in case of crash

Parking localization

Street sweeping

alerts

Alert if the car is hit when

parked

Antitheft service if the box is removed/ uninstalled

Alert in case the vehicle is moved when the

engine is off (e.g.

tow-away)

14

1516

1312

Stolen vehicle

recovery

17

The insurer can keep more value with use cases

based on a broad suite of services

and rewards

#InsurIoTMatteo Carbone

Source: Connected Insurance Observatory

Connected insurance market adoption requires defined sequential steps

Which is the best

way to do it for

my company?

Does the

approach make

sense?

There is a

ROI of the

use case?

•First pilots •Roll out on few pioneers

•Pilot phases diffusion over the greatest part of players, by using a "me-too" approach

•Only few top players understand telematics full potential (UW, claims, VAS), define their own approach (eg: big data) and push the selling phase

•Commercial offer differentiation

•Telematics potential fully understood and increased commercial push by all players

•Differentiating solutions / providers over top players

•Telematics approach is the standard for the insurance business

•Relationship consolidation between top players and providers, best practices cross-country diffusion

#InsurIoTMatteo Carbone

Incubation phase

Growth phase

Maturity phase

Exploration phase

Learning phase

Source: Connected Insurance Observatory

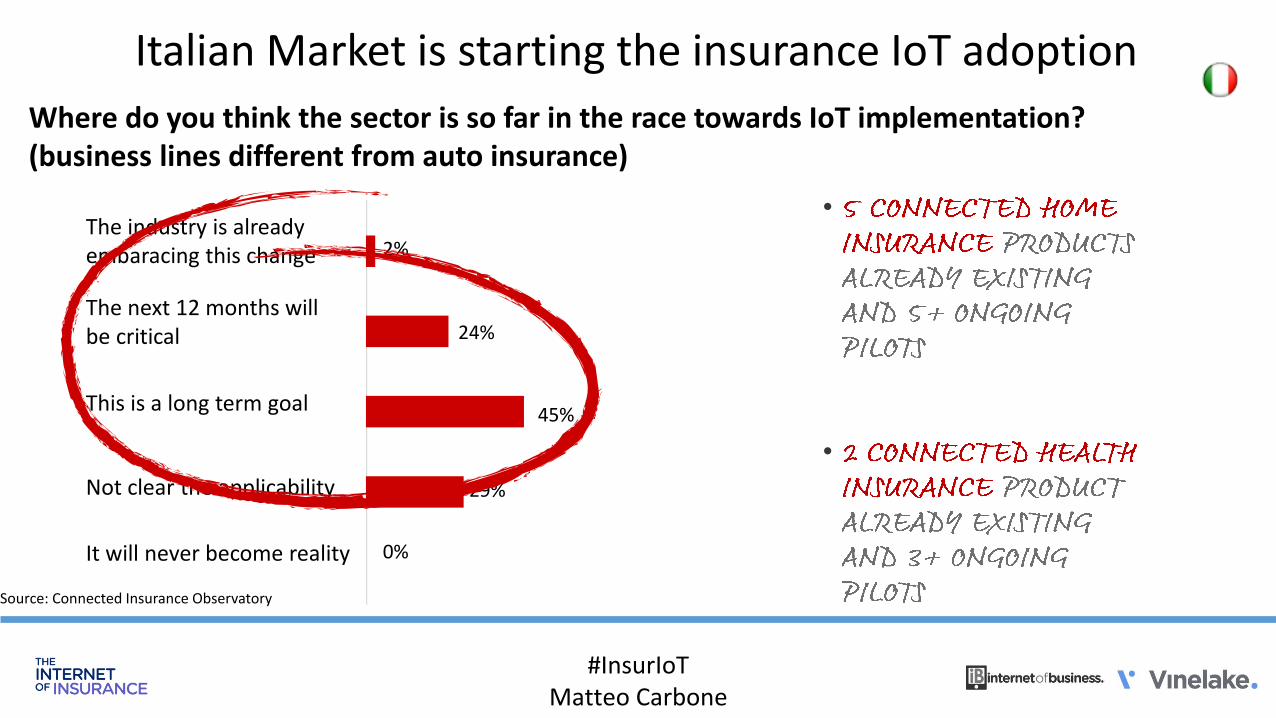

Italian Market is starting the insurance IoT adoption

Where do you think the sector is so far in the race towards IoT implementation? (business lines different from auto insurance)

The industry is already embaracing this change

The next 12 months will be critical

This is a long term goal

Not clear the applicability

It will never become reality

29%

45%

24%

2%

•

•

0%

#InsurIoTMatteo Carbone

Source: Connected Insurance Observatory

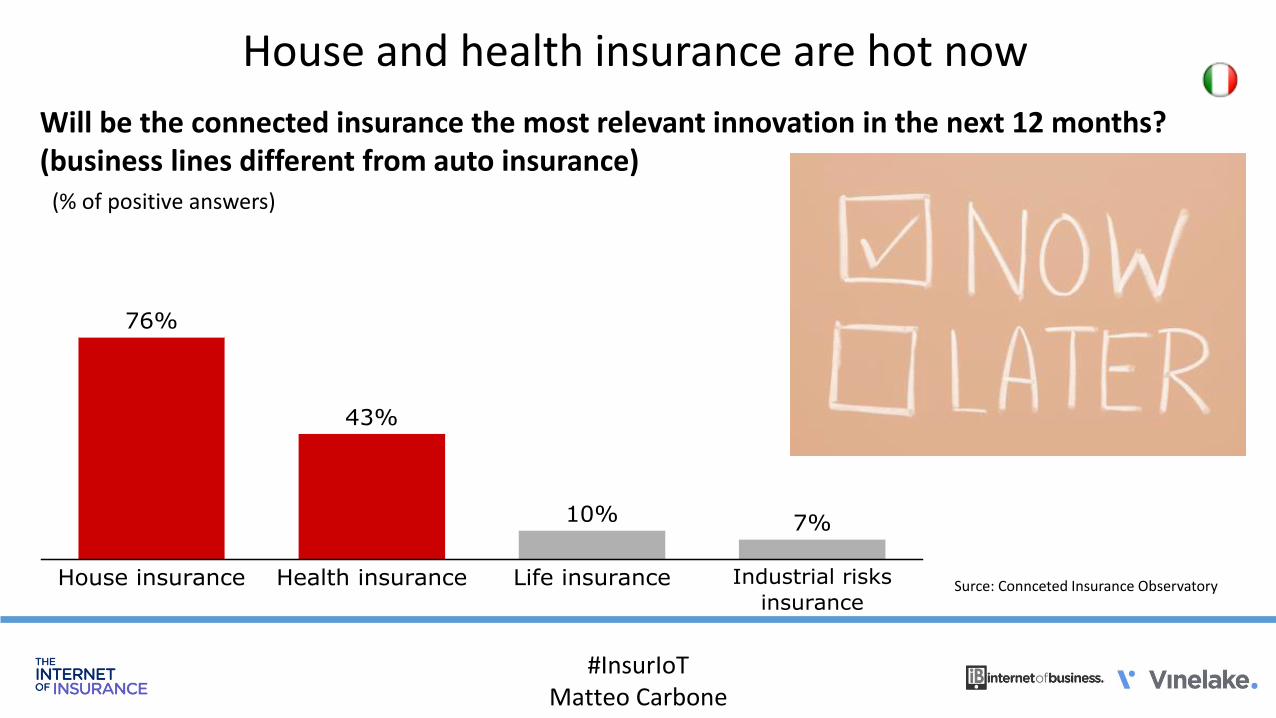

House and health insurance are hot now

Will be the connected insurance the most relevant innovation in the next 12 months? (business lines different from auto insurance)

(% of positive answers)

Surce: Connceted Insurance Observatory

#InsurIoTMatteo Carbone

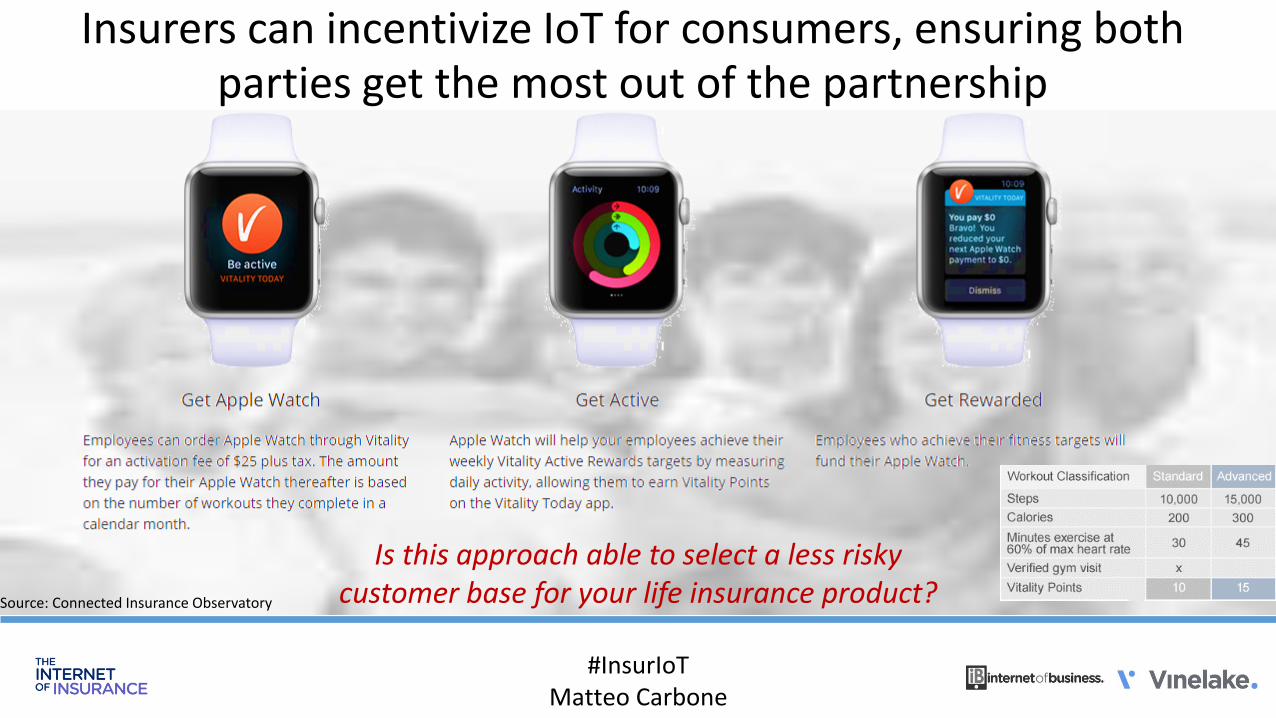

Insurers can incentivize IoT for consumers, ensuring bothparties get the most out of the partnership

Is this approach able to select a less risky customer base for your life insurance product?

#InsurIoTMatteo Carbone

Source: Connected Insurance Observatory

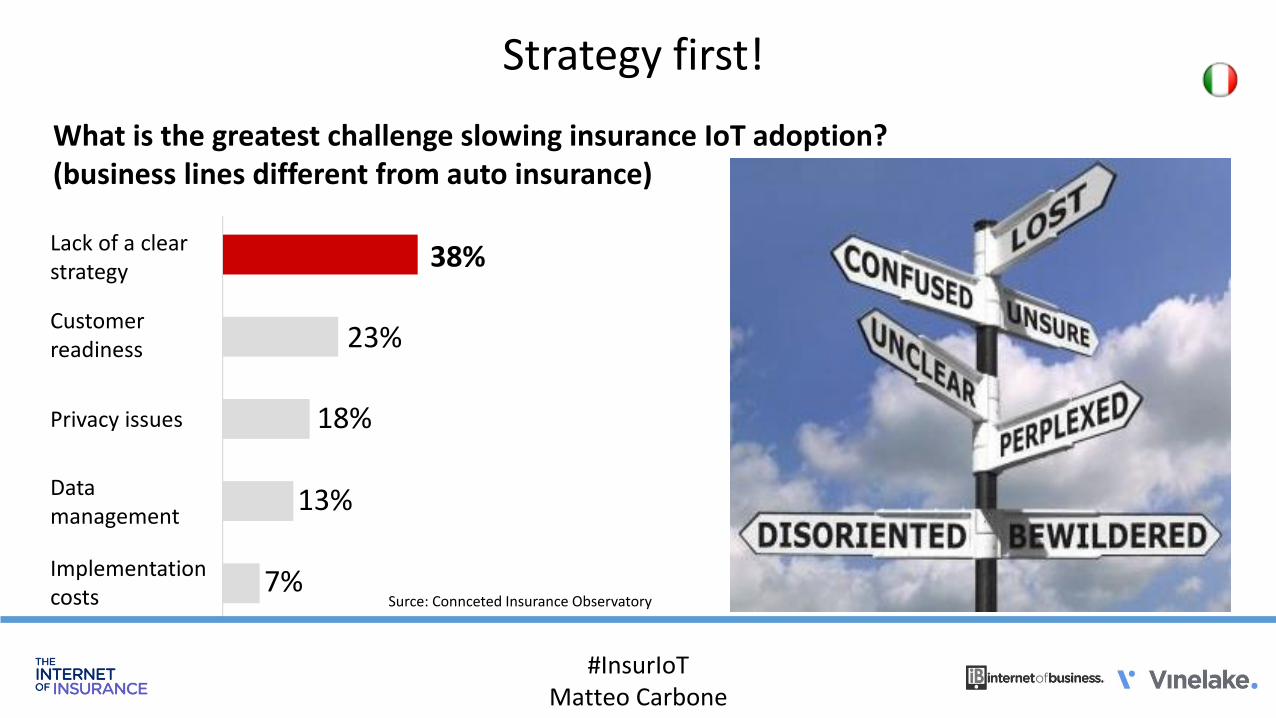

Strategy first!

What is the greatest challenge slowing insurance IoT adoption?(business lines different from auto insurance)

Lack of a clear strategy

38%

Customer readiness

Privacy issues

Data management

Implementation costs

23%

18%

13%

7%Surce: Connceted Insurance Observatory

#InsurIoTMatteo Carbone

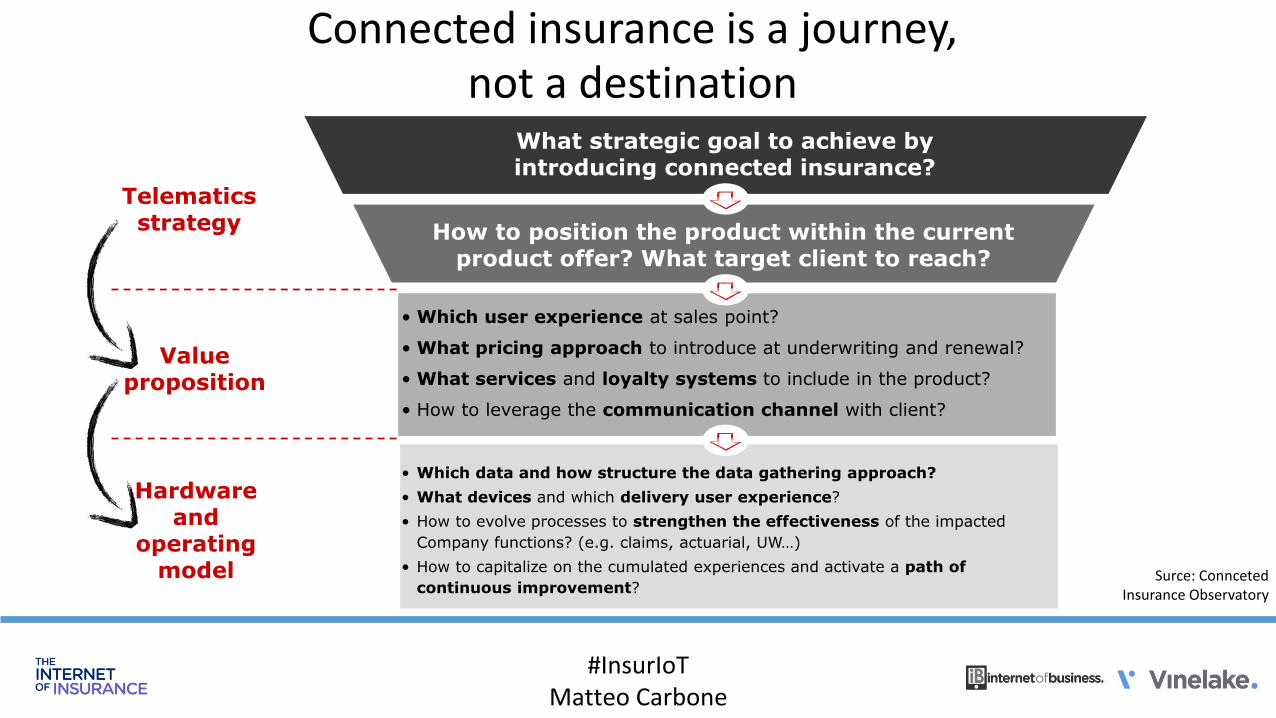

Connected insurance is a journey,not a destination

Surce: ConncetedInsurance Observatory

Telematics strategy

Value proposition

What strategic goal to achieve by introducing connected insurance?

How to position the product within the current product offer? What target client to reach?

Hardware and

operating model

• Which user experience at sales point?

• What pricing approach to introduce at underwriting and renewal?

• What services and loyalty systems to include in the product?

• How to leverage the communication channel with client?

• Which data and how structure the data gathering approach?

• What devices and which delivery user experience?

• How to evolve processes to strengthen the effectiveness of the impacted

Company functions? (e.g. claims, actuarial, UW…)

• How to capitalize on the cumulated experiences and activate a path of

continuous improvement?

#InsurIoTMatteo Carbone

Insurance IoT connects Insurerwith people and their risks.

Data is the new oil!Matteo Carbone

@mcIns_

London, June 13

#InsurIoT