investment idea - hdfc ltd - hold

TRANSCRIPT

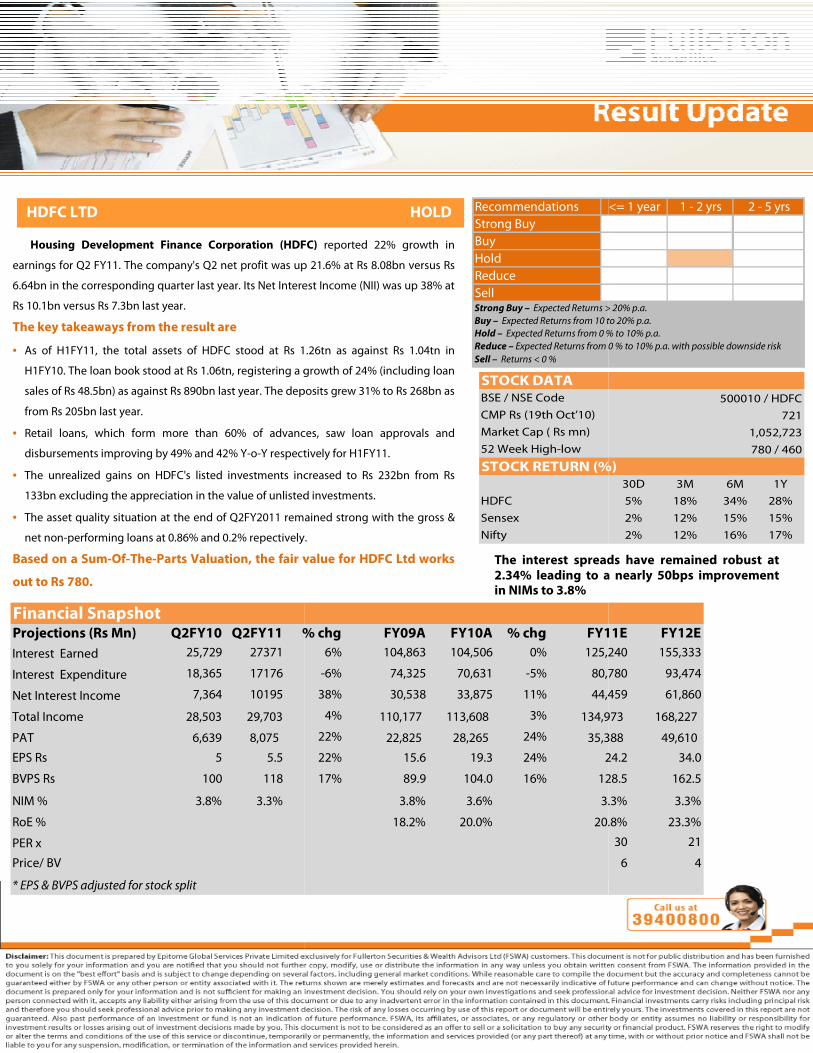

HDFC LTD

Housing Development Finance Corporation (HDFC)

earnings for Q2 FY11. The company's Q2 net profit was up 21.

6.64bn in the corresponding quarter last year. Its Net Interest Income

Rs 10.1bn versus Rs 7.3bn last year.

The key takeaways from the result are

• As of H1FY11, the total assets of HDFC stood at Rs 1

H1FY10. The loan book stood at Rs 1.06tn, registering a growth of 24%

sales of Rs 48.5bn) as against Rs 890bn last year. The deposits

from Rs 205bn last year.

• Retail loans, which form more than 60% of advances

disbursements improving by 49% and 42% Y-o-Y respectively

• The unrealized gains on HDFC's listed investments increased

133bn excluding the appreciation in the value of unlisted investments

• The asset quality situation at the end of Q2FY2011 remained

net non-performing loans at 0.86% and 0.2% repectively.

Based on a Sum-Of-The-Parts Valuation, the fair value for

out to Rs 780.

Projections (Rs Mn) Q2FY10 Q2FY11 % chg

Interest Earned 25,729 27371

Interest Expenditure 18,365 17176

Net Interest Income 7,364 10195

Total Income 28,503 29,703

PAT 6,639 8,075

EPS Rs 5 5.5

BVPS Rs 100 118

NIM % 3.8% 3.3%

RoE %

PER x

Price/ BV

* EPS & BVPS adjusted for stock split

Financial Snapshot

HOLD

Housing Development Finance Corporation (HDFC) reported 22% growth in

The company's Q2 net profit was up 21.6% at Rs 8.08bn versus Rs

et Interest Income (NII) was up 38% at

1.26tn as against Rs 1.04tn in

, registering a growth of 24% (including loan

deposits grew 31% to Rs 268bn as

more than 60% of advances, saw loan approvals and

respectively for H1FY11.

increased to Rs 232bn from Rs

the appreciation in the value of unlisted investments.

The asset quality situation at the end of Q2FY2011 remained strong with the gross &

repectively.

, the fair value for HDFC Ltd works The interest spreads have remain2.34% leading to a nearly in NIMs to 3.8%

Recommendations

Strong Buy

Buy

Hold

Reduce

SellStrong Buy – Expected Returns > 20% p.a.

Buy – Expected Returns from 10 to 20% p.a.

Hold – Expected Returns from 0 % to 10% p.a.

Reduce – Expected Returns from 0 % to 10% p.a. with possible downside risk

Sell – Returns < 0 %

BSE / NSE Code

CMP Rs (19th Oct’10)

Market Cap ( Rs mn)

52 Week High-low

HDFC

Sensex

Nifty

STOCK RETURN (%)

STOCK DATA

% chg FY09A FY10A % chg FY11E

6% 104,863 104,506 0% 125,240

-6% 74,325 70,631 -5% 80,780

38% 30,538 33,875 11% 44,459

4% 110,177 113,608 3% 134,973

22% 22,825 28,265 24% 35,388

22% 15.6 19.3 24% 24.2

17% 89.9 104.0 16% 128.5

3.8% 3.6% 3.3%

18.2% 20.0% 20.8%

30

6

spreads have remained robust at leading to a nearly 50bps improvement

<= 1 year 1 - 2 yrs 2 - 5 yrs

Expected Returns > 20% p.a.

Expected Returns from 10 to 20% p.a.

Expected Returns from 0 % to 10% p.a.

Expected Returns from 0 % to 10% p.a. with possible downside risk

30D 3M 6M 1Y

5% 18% 34% 28%

2% 12% 15% 15%

2% 12% 16% 17%

780 / 460

STOCK RETURN (%)

500010 / HDFC

721

1,052,723

FY11E FY12E

125,240 155,333

80,780 93,474

44,459 61,860

134,973 168,227

35,388 49,610

24.2 34.0

128.5 162.5

3.3% 3.3%

20.8% 23.3%

30 21

6 4

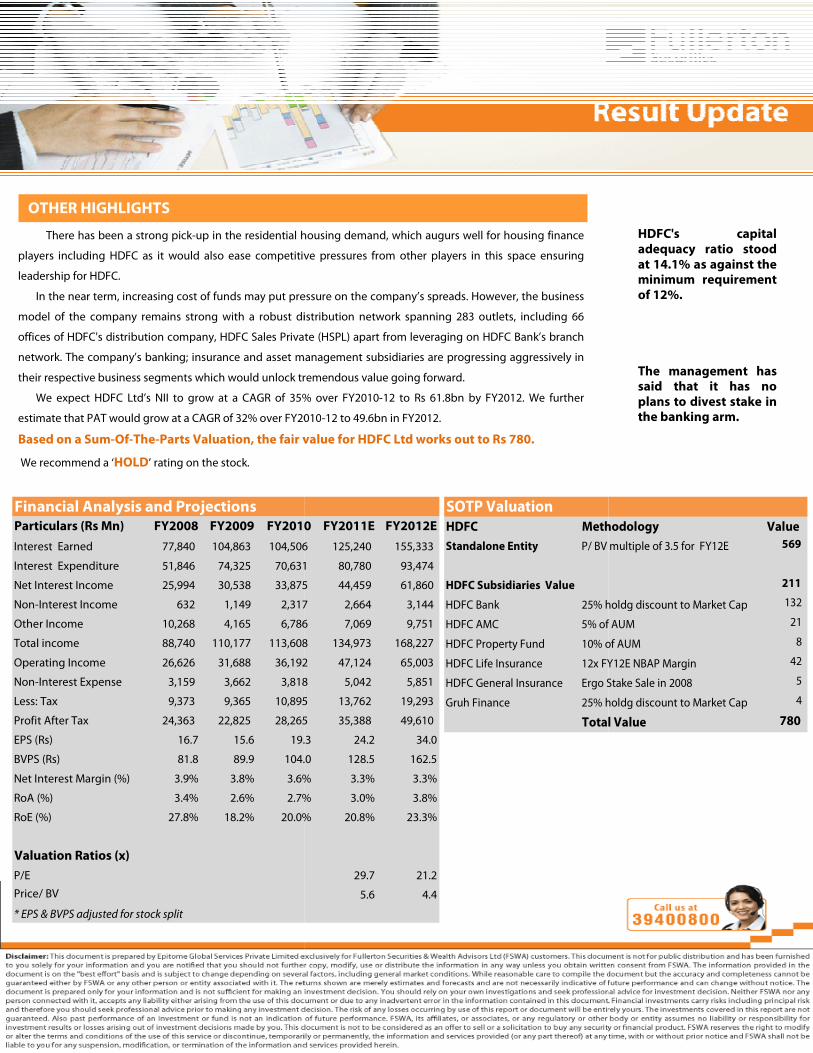

OTHER HIGHLIGHTS

There has been a strong pick-up in the residential housing demand, which augurs well

players including HDFC as it would also ease competitive press

leadership for HDFC.

In the near term, increasing cost of funds may put pressure on the company

model of the company remains strong with a robust distribution network span

offices of HDFC's distribution company, HDFC Sales Private (HSPL)

network. The company’s banking; insurance and asset management

their respective business segments which would unlock tremendous

We expect HDFC Ltd’s NII to grow at a CAGR of 35% over FY2010

estimate that PAT would grow at a CAGR of 32% over FY2010

Based on a Sum-Of-The-Parts Valuation, the fair value for

We recommend a ‘HOLD’ rating on the stock.

Particulars (Rs Mn) FY2008 FY2009 FY2010

Interest Earned 77,840 104,863 104,506

Interest Expenditure 51,846 74,325 70,631

Net Interest Income 25,994 30,538 33,875

Non-Interest Income 632 1,149 2,317

Other Income 10,268 4,165 6,786

Total income 88,740 110,177 113,608

Operating Income 26,626 31,688 36,192

Non-Interest Expense 3,159 3,662 3,818

Less: Tax 9,373 9,365 10,895

Profit After Tax 24,363 22,825 28,265

EPS (Rs) 16.7 15.6 19.3

BVPS (Rs) 81.8 89.9 104.0

Net Interest Margin (%) 3.9% 3.8% 3.6%

RoA (%) 3.4% 2.6% 2.7%

RoE (%) 27.8% 18.2% 20.0%

Valuation Ratios (x)

P/E

Price/ BV

* EPS & BVPS adjusted for stock split

Financial Analysis and Projections

up in the residential housing demand, which augurs well for housing finance

ve pressures from other players in this space ensuring

cost of funds may put pressure on the company’s spreads. However, the business

distribution network spanning 283 outlets, including 66

offices of HDFC's distribution company, HDFC Sales Private (HSPL) apart from leveraging on HDFC Bank’s branch

asset management subsidiaries are progressing aggressively in

tremendous value going forward.

% over FY2010-12 to Rs 61.8bn by FY2012. We further

% over FY2010-12 to 49.6bn in FY2012.

aluation, the fair value for HDFC Ltd works out to Rs 780.

SOTP Valuation

HDFC Methodology

Standalone Entity P/ BV multiple of 3.5 for FY12E

HDFC Subsidiaries Value

HDFC Bank 25% holdg discount to Market Cap

HDFC AMC 5% of AUM

HDFC Property Fund 10% of AUM

HDFC Life Insurance 12x FY12E NBAP Margin

HDFC General Insurance Ergo Stake Sale in 2008

Gruh Finance 25% holdg discount to Market Cap

Total Value

FY2010 FY2011E FY2012E

104,506 125,240 155,333

70,631 80,780 93,474

33,875 44,459 61,860

2,317 2,664 3,144

6,786 7,069 9,751

113,608 134,973 168,227

36,192 47,124 65,003

3,818 5,042 5,851

10,895 13,762 19,293

28,265 35,388 49,610

19.3 24.2 34.0

104.0 128.5 162.5

3.6% 3.3% 3.3%

2.7% 3.0% 3.8%

20.0% 20.8% 23.3%

29.7 21.2

5.6 4.4

HDFC's capital adequacy ratio stood at 14.1% as against the minimum requirement of 12%. The management has said that it has no plans to divest stake in the banking arm.

Methodology Value

P/ BV multiple of 3.5 for FY12E 569

211

25% holdg discount to Market Cap 132

5% of AUM 21

10% of AUM 8

12x FY12E NBAP Margin 42

Ergo Stake Sale in 2008 5

25% holdg discount to Market Cap 4

Total Value 780