kabalikat para sa maunlad na buhay, inc. (kmbi ) – … rating 3 head office: manila valenzuela...

TRANSCRIPT

July 2008

CONTACTS

MicroFinanza Rating srl Corso Sempione, 65 20149 Milan – Italy Tel: +39-02-3656.5019 [email protected] www.microfinanzarating.com

Kabalikat para sa Maunlad na Buhay, Inc. (KMBI) #12 San Francisco St., Karuhatan, Valenzuela City, Philippines 1441

Tel.: (+632) 291.14.84 to 86 Fax: (+632) 292.24.41

Email: [email protected]

Kabalikat para sa Maunlad na Buhay, Inc. (KMBI) – Philippines

Private Rating

Final Report

Kabalikat para sa Maunlad na Buhay, Inc. (KMBI) is a non-stock, non-government development organization formally established on the 27th of November 1986 with the aim of providing micro-entrepreneurs sustainable microfinance, training, and demand-driven non-financial services. Since 2005 KMBI is offering life micro-insurance services in partnership with Cocolife, a local insurance company. KMBI started its operations in the island of Luzon, in the peri-urban and rural areas surrounding the city of Manila, and since 1999 expanded its outreach in the islands of Mindanao and Cebu, steadily growing in terms of borrowers and portfolio, which amount as of May 2008 respectively to 116,052 and US$ 8 Mln. KMBI is an Opportunity International partner since 1994 and part of the Alliance of Philippine Partners in Enterprise Development (Append). Although most of its outstanding portfolio is at the moment fed with compulsory savings, KMBI is also partnering with several domestic financial institutions and one international investor (Oikocredit) for funding provision.

Legal Form NGO Network of reference Opportunity International Inception year November 1986 Area of intervention Urban, semi urban Credit methodology Village Banking

-

2,000,000

4,000,000

6,000,000

8,000,000

10,000,000

12,000,000

14,000,000

16,000,000

Dec06 Dec07 May08

Liabilities and equity - US$

Equity Obligatory savings Short term liabilities

Long term liabilities Other liabilities

Portfolio quality evolution

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

Dec06 Dec07 May08

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Gross outstanding portfolio PAR 30

Write-off ratio Restructured portfolio

MicroFinanza Rating 2

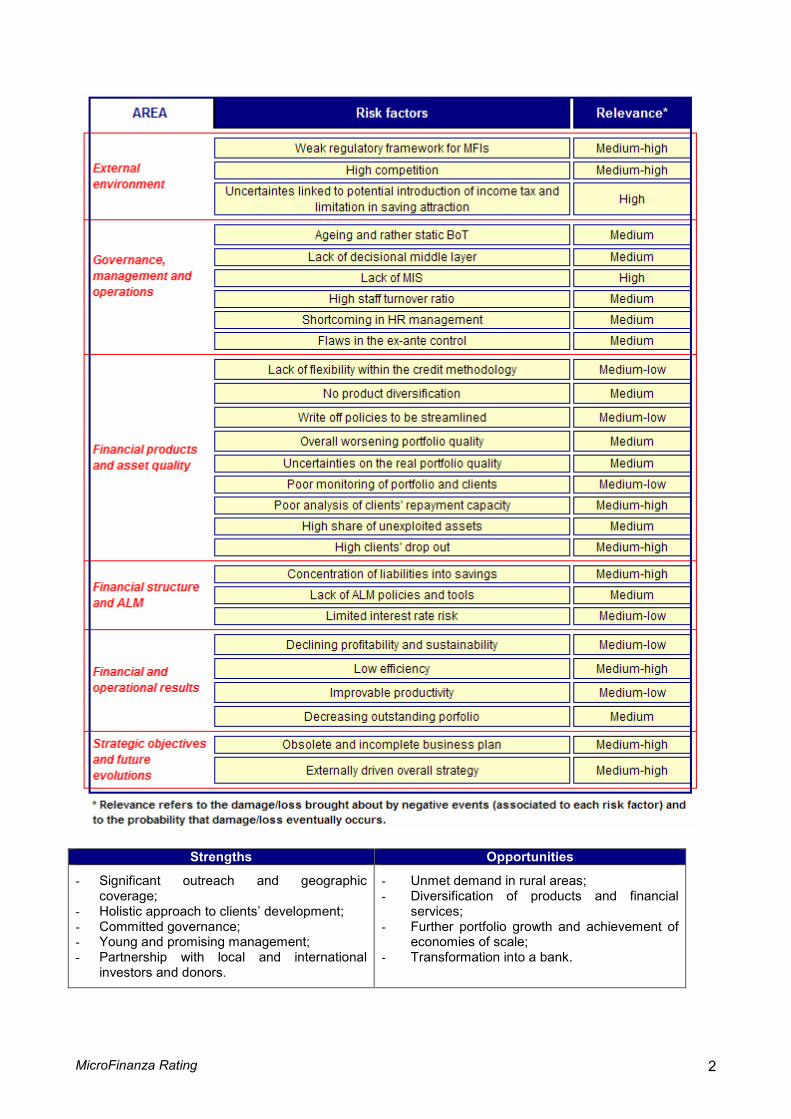

Strengths Opportunities

- Significant outreach and geographic coverage;

- Holistic approach to clients’ development; - Committed governance; - Young and promising management; - Partnership with local and international

investors and donors.

- Unmet demand in rural areas; - Diversification of products and financial

services; - Further portfolio growth and achievement of

economies of scale; - Transformation into a bank.

MicroFinanza Rating 3

Head Office: Manila Valenzuela

Branches: Metro Davao 1 Metro Davao 2 Digos Tagum Gensan Koronadal Tacurong Kidapawan Butuan Comval San Francisco Surigao Metro Manila South 1 Metro Manila South 2 Upper Cavite Lower Cavite Central Cavite Calamba San Pablo Sta Cruz Binan Lipa Batangas Lucena Gumaca Naga Legazpi Iriga Daet Camarin Pasig Marikina West Avenue Tandang Sora Valenzuela Meycauayan San Jose

Final opinion KMBI is characterized by a good geographic coverage compared to the other Microfinance NGOs in the Philippines. Performance results are positive even though in a downward trend over the last three years due to the low level of efficiency and the scarce exploitation of economies of scale deriving from a quite obsolete lending methodology. This is emphasized by the lack of MIS which contributes to further lower the overall internal control and ex-ante procedures of an organizational structure characterized by a weak middle management layer. Although quite active and committed, the main governance body is rather static in terms of operational innovations, resulting in a strategy mainly focused on increasing the number of clients without properly taking into account the current development status of the institution and its potential for growth (market demand). Finally, the institution is highly exposed to regulatory risk as the attraction of deposits is not regulated by the Central Bank, while it seems likely that the Tax Bureau will force NGOs to reimburse taxes in arrears since 2005.

Growth

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

Dec06 Dec07 May08

Active gross portfolio

Total assets

Active clients (number)

Funding liabilities

Equity

MicroFinanza Rating 4

Benchmarking

All figures of peer groups are referred to the MicroBanking Bulletin (MBB) database updated as of December 2007. KMBI ratios indicated here do not fully correspond to the ratios presented in the report as they are calculated according to the MBB methodology

1.

The benchmark shows that KMBI has a larger portfolio size compared to the other MFIs using the village banking methodology and the medium size FSS MFIs in Asia, while its portfolio stands at lower levels than average large MFI in Asia and the chosen sample of Philippine MFIs, though Card NGO and TSKI with their large portfolio significantly skew the average. In terms of outreach KMBI performs much better than the other peer groups, and it is in line with other MFIs within the country, demonstrating the generally strong social orientation of not-for-profit microfinance institutions in the Philippines. KMBI is characterized by worse values in terms of portfolio at risk than the other peer groups, as a result of a credit process showing some shortcomings especially in terms of clients’ repayment capacity analysis and increasing over-indebtedness of borrowers. As for profitability, the institution shows adequate levels of adjusted return on equity, more thanks to the very high portfolio yield than to good performances in terms of efficiency. Productivity stands at lower values than the other Asian MFIs FSS (large and medium) and notably than microfinance institutions using the village banking methodology, showing that there exists some room for improvement. On the other end, KMBI enjoys a good staff allocation ratio which in turn triggers an adequate number of borrowers per staff member.

1 The MBB adjusts the financial data to produce a common treatment for the effect of: a) inflation, b)subsidies, and c)loan loss provisioning and write-off (see MBB , Appendix I: Notes to Adjustments and Statistical Issues).

MicroFinanza Rating 5

Table of contents 1. External Environment and KMBI positioning ...................................................................... 6 Institutional background ............................................................................................................... 6 Macroeconomic context ............................................................................................................... 6 Microfinance sector ..................................................................................................................... 7 Regulation and supervision ......................................................................................................... 7 Market positioning ....................................................................................................................... 8

2. Governance and operational structure ............................................................................... 10 Ownership and Governance ...................................................................................................... 10 Organisation and structure ........................................................................................................ 11 Human Resources ..................................................................................................................... 12 Internal control and operational risk management ..................................................................... 13 Accounting and external audit ................................................................................................... 13 Management Information System (MIS) .................................................................................... 13

3. Lending and savings operations .......................................................................................... 15 4. Assets structure and quality .................................................................................................. 17 Assets structure ......................................................................................................................... 17 Portfolio structure ...................................................................................................................... 17 Loan portfolio quality ................................................................................................................. 18

5. Financial structure and ALM .................................................................................................. 20 Liabilities and equity structure ................................................................................................... 20 Assets and Liabilities Management ........................................................................................... 21

6. Financial and operational results ......................................................................................... 22 7. Strategic objectives and financial needs ........................................................................... 24 General guidelines for future evolution ...................................................................................... 24 Financial needs ......................................................................................................................... 25

8. Details of the risk factors ........................................................................................................ 26 Annex 1 - Financial statements ................................................................................................. 29 Annex 2 - Financial statements’ adjustments ....................................................................... 31 Annex 3 - Financial ratios............................................................................................................ 32 Annex 4 - Definitions .................................................................................................................... 34 Annex 5 - Guidelines of reporting and accounting .............................................................. 35 Annex 6 - Rating Scale ................................................................................................................. 36

KMBI – Philippines – July 2008 Chapter 1

MicroFinanza Rating 6

1. External Environment and KMBI positioning

Institutional background Kabalikat para sa Maunlad na Buhay, Inc. (KMBI) is a non-stock, non-government development organization formally established on the 27th of November 1986 thanks to an initial capitalization of PhP 132,000 (about US$ 3,500), with the aim of providing micro-entrepreneurs with sustainable microfinance, training, and demand-driven non-financial services. KMBI started its operations in the island of Luzon, in the peri-urban and rural areas surrounding the city of Manila, and since 1999 expanded its outreach in the islands of Mindanao and Cebu, steadily growing in terms of borrowers and portfolio, which amount as of May 2008 respectively to 116,052 and US$ 8 Mln. KMBI is an Opportunity International partner since 1994 and part of the Alliance of Philippine Partners in Enterprise Development (Append), which facilitates the growth and viability of the eleven OI implementing partners in the Philippines and supports the development of new financial services, such as micro-insurance and housing loans, and the delivery of community and business development services. KMBI is also part of the Microfinance Council of the Philippines, the main microfinance association in the country. Although most of its outstanding portfolio is at the moment fed with compulsory savings, KMBI is also partnering with several domestic financial institutions and one international investor (Oikocredit) for funding provision. Since 2005 KMBI is offering life micro-insurance services in partnership with Cocolife, a local insurance company. Macroeconomic context Gloria Macapagal Arroyo became president of the Philippines in January 2001 after the previous president, Joseph Estrada, was brought down by a peaceful popular uprising. Mrs Arroyo claimed further victory in the presidential election of May 2004, but since then she had to face several challenges to her leadership. In 2005 she was accused of interfering with the popular vote and in February 2006 she declared a state of emergency after claiming to have uncovered a coup plot. The authority of the president, Gloria Macapagal Arroyo is likely to remain vulnerable over the next 2 years, also due to the continual shift in allegiances of the political parties. However, the president’s strengthened position in the lower house will make it difficult for the opposition to impeach her, and as a result she is likely to remain in power until the end of her term in 2010. Arroyo, a practicing economist, has made the economy the focus of her presidency. Economic growth in terms of gross domestic product has averaged 5.0% during the Arroyo presidency from 2001 up to the first quarter of 2008. In 2007 GDP growth scored the highest rate in 3 decades reaching 6.8% after an already robust 5.5% experienced over 2006. The significant growth over 2007 was mainly triggered by private consumption, based on the significant inflow of remittances, and the services sector.

However, private consumption has lost momentum this year due to rapidly raising inflation, which climbed to 9.6% year on year in May 2008 and

12.5% as of August 2008, the highest value in 17 years. Due to high inflation GDP growth eased to 5.2% in the first quarter of 2008 and reversed to 3.4% in the second, lowering the expectation for growth from 6% to 4.5% in 2008 and 6.2% to 4.7% over 2009. At the same time forecasts for

KMBI – Philippines – July 2008 Chapter 1

MicroFinanza Rating 7

inflation has been revised from 4% to 10.5% in 2008 and 3.6% to 8% in 2009. The lower than expected economic growth may trigger a more expansionary fiscal policy, which would raise concerns about fiscal consolidation and impede the efforts to lower the budget deficit, both measures necessary to maintaining global investor confidence. Microfinance sector The Philippines microfinance sector is potentially one of the largest in Asia, with a funding gap for the almost 6 Mln households2 under the poverty line amounting, according to ADB, to US$ 2Bln. In fact, over 17 million people in the Philippines still do not have access to microfinance services, and in some regions (particularly ARMM) microfinance institutions (MFIs) have reached less than 15% of all households.3 Although a continued unmet demand for microfinance services remains, various actors are working towards filling the gap in financial service access, including commercial banks, regulated financial institutions, rural and thrift banks, microfinance NGOs and cooperatives. By 2006, there were estimated to be over 500 MFIs operating with an outreach of over 1.5 million clients and serving the sector with a variety of financial and non-financial services including credit, savings and insurance. The Philippine microfinance sector has come a long way since its origins in donor-funded and government initiated programs in the 1980s. In addition to creating an enabling policy environment4, the government provides wholesale funding and technical assistance to accredited MFIs through the People’s Credit and Finance Corporation (PCFC) which lends to over 200 MFIs working in all 80 provinces nationwide. Other industry-wide capacity building initiatives include programs from the Asian Development Bank (ADB) and the USAID funded Microenterprise Access to Banking Services (MABS) project which is working to expand mobile banking services nationwide. In addition, Philippine MFIs are networked together through various groups including the Microfinance Council of the Philippines (MCPI), APPEND, NATCCO, PHILNET and RBAP as well as regional networks such as the Mindanao Microfinance Council. The major providers of microfinance in the Philippines are Rural Banks, Thrift Banks, NGOs and cooperatives. As of July 2008 there exist 729 Rural Banks, representing 2.9% of the overall financial system, 109 Thrift Banks (8%), about 300 NGOs, with a negligible share of the credit market covered, and commercial banks, representing almost its 90%. Cooperatives show a limited and localized outreach, with only few cooperatives which have reached noticeable portfolio sizes (e.g. CCT Credit Cooperative). Although the number of Rural Banks and NGOs engaged in microfinance is significant, their size in terms of outstanding portfolio is still relatively small, with only 3 Rural Banks with a portfolio above US$ 15 Mln. At the same time NGOs, showing important performances in terms of number of clients, remains at very low levels when considering loan portfolio, with some noticeable exceptions, such as Card NGO, with a portfolio as of June 2008 amounting to US$ 33 Mln. Because of the regulatory environment in the Philippines in terms of taxation and saving attraction many MFIs, such as CARD, TSKI and NWTF, have a dual existence as NGO and rural or thrift bank, in order to be able to offer a full range of banking services and target low end clients at affordable cost. Regulation and supervision Regulation and supervision within the sector depends largely on the legal form of the institution, as microfinance NGOs are not regulated by the Central Bank. In fact, NGOs are only registered with the Securities and Exchange Commission (SEC), to which they have to file annual audited financial statements and general information sheets disclosing microfinance operations. At the

2 Only 1.4 Mln households was served in 2004. 3 Asian Development Bank “Report and Recommendation of the President to the Board of Directors on a Proposed

Loan and Technical Assistance Grant to the Republic of the Philippines for the Microfinance Development Program,” RRP: PHI 38579, October 2005. 4 In the 1990s the Central Bank (Bangko Sentral ng Pilipinas) relaxed the bank entry and branching requirements which led to the creation of numerous rural banks with operations focused at the provincial levels. In 1997 the government set forth an official Microfinance Policy while in 2002 a General Banking Law was established and various circulars since then have begun to set up the national framework for microfinance regulation and supervision. Other reforms in recent years include the adoption of international accounting and financial reporting standards and Basel II standards.

KMBI – Philippines – July 2008 Chapter 1

MicroFinanza Rating 8

moment, microfinance NGOs are not legally permitted to collect savings5; however in practice many NGO institutions collect both mandatory and voluntary savings from their members6. In view of the regulatory gap, MCPI has taken steps towards submitting its NGO member institutions to voluntary self-regulation through a common draft “Memorandum of Agreement” which member MFIs agreed to in 2006. Notably, the Memorandum includes a “Compensating Balance Rule” that prohibits MFIs from collecting savings in excess of the total outstanding portfolio, and more generally from collecting savings from the public (non-clients). Nevertheless, the Memorandum has not been adopted by the Central Bank and therefore the collection of savings from microfinance NGOs in the Philippines is now carried out in the absence of a regulatory framework, with the Memorandum acting as a self-regulatory tool for the MCPI members. At the same time NGOs do not pay profit taxes, and it seems likely that the Tax Bureau will force these type of MFIs to reimburse taxes in arrears since 2005. NGO MFIs and the microfinance associations are currently lobbying with the BSP and the tax bureau for dissuading them from applying the standard taxation system and alternative solutions have been proposed.

Market positioning KMBI offers loans and insurance services to micro-entrepreneurs in urban and peri-urban areas through the group lending methodology. The MFI shows as of May 2008 a good geographical outreach, with 36 branches spread across Luzon, Mindanao and Cebu, though the diversification of its product offer is significantly poor, as only one product is currently offered. Competition within the sector is high, particularly among the largest MFIs (CARD, TSKI, NWTF, etc.) that have a combined outreach of over 600,000 clients and the top 10 MFIs that account for over 75% of total outstanding loan portfolio in the sector. Besides the top tier of MFIs, numerous 2nd tier institutions are working to expand their service offer and consolidate their performance in order to remain or gain relevance in the increasingly competitive market. All major MFIs, rural banks, and cooperatives, such as TSPI, CARD, CCT, ASA, can be considered KMBI competitors, showing overall similar or lower effective interest rates. Nevertheless, rural banks, although burdened by more bureaucratic credit processes, can generally offer higher amounts and longer maturities, while most of other microfinance providers enjoy a better diversified product offer, often including individual loans. Client over-indebtedness is growing in prevalence, particularly in areas with strong MFI competition and saturation. Although the Bankers Association of the Philippines has operated a private, nationwide credit bureau since 1990, there is no Credit Bureau connected specifically to microfinance clients. MCPI has worked to promote sector collaboration among its members through gathering a black list of the clients of regulated MFI; however to date the utilization of this facility has been low. Although competition is rapidly growing triggering client over-indebtedness and increasing credit risk, the market shows a certain level of unmet demand especially in rural area, which can initially be served only at the cost of increasing operating expenses and overall operational risk. Within this highly competitive context KMBI presents some competitive advantages:

� Good geographic outreach; � Less bureaucratic procedures for disbursement than rural banks; � Customer based approach and holistic view of clients’ development; � Partnership with important international and domestic investors and stakeholders; � Good availability of funding.

KMBI main competitive disadvantages can be identified in the followings:

� Still very limited product offer, with only group lending offered; � Loan maturity offered shorter than some competitors; � Rigidities in the conditions offered to repeated clients (maturity and interest rates); � Slightly higher interest rates than rural banks and some MFIs;

5 The regulation permits only banks, formal financial institutions and cooperatives to collect savings. 6 On average, microfinance NGOs present a ratio of savings over portfolio of about 60% (ASHI presents a ratio of 24% as of December 2007).

KMBI – Philippines – July 2008 Chapter 1

MicroFinanza Rating 9

� NGOs collecting compulsory savings subject to potential liquidity crises.

KMBI – Philippines – July 2008 Chapter 2

MicroFinanza Rating 10

2. Governance and operational structure

Ownership and Governance KMBI has been registered in 1986 as non governmental organization and it operates according to the mandate received from the Security and Exchange Commission (SEC). The current legal status does not foresee any owners and the initial founder after 22 years of KMBI operations still seats in the Board of Trustees (BoT) as Chairman.

The BoT is composed of 7 members out of whom 2 are not currently active due to personal reasons and in the process of leaving the governance body. KMBI is currently seeking 4 new professionals, with the objective to have a BoT including 9 members as foreseen in the Bylaw. Over the last twenty years the composition of the BoT has never changed denoting a main governance body rather static. Hence, the institution has not implemented relevant strategic innovations initiated by the BoT especially in terms of the business model with operations and procedures which have been remaining unchanged since KMBI inception. On the other end, the BoT provides a sound support to the executive management in terms of fostering the institutional growth of the institution (mainly in terms of number of clients) and public relations, while the lack of technical expertise in microfinance prevents the body from providing guidance on some of its primary needs (i.e. MIS, products development, etc). Since 1994, the institution is affiliated to the Opportunity International Network and in 2001 it started the process of assets transfer to Opportunity Microfinance Bank, but the agreement with the other three partners failed and KMBI continued to operate as NGO. Nevertheless, the transformation into a bank remains one of the main goal of the institution (see chapter 7). In the case of transformation into a bank, the current BoT will likely remain in charge of the NGO, which will continue to operate, while a new body will be established for the bank

KMBI – Philippines – July 2008 Chapter 2

MicroFinanza Rating 11

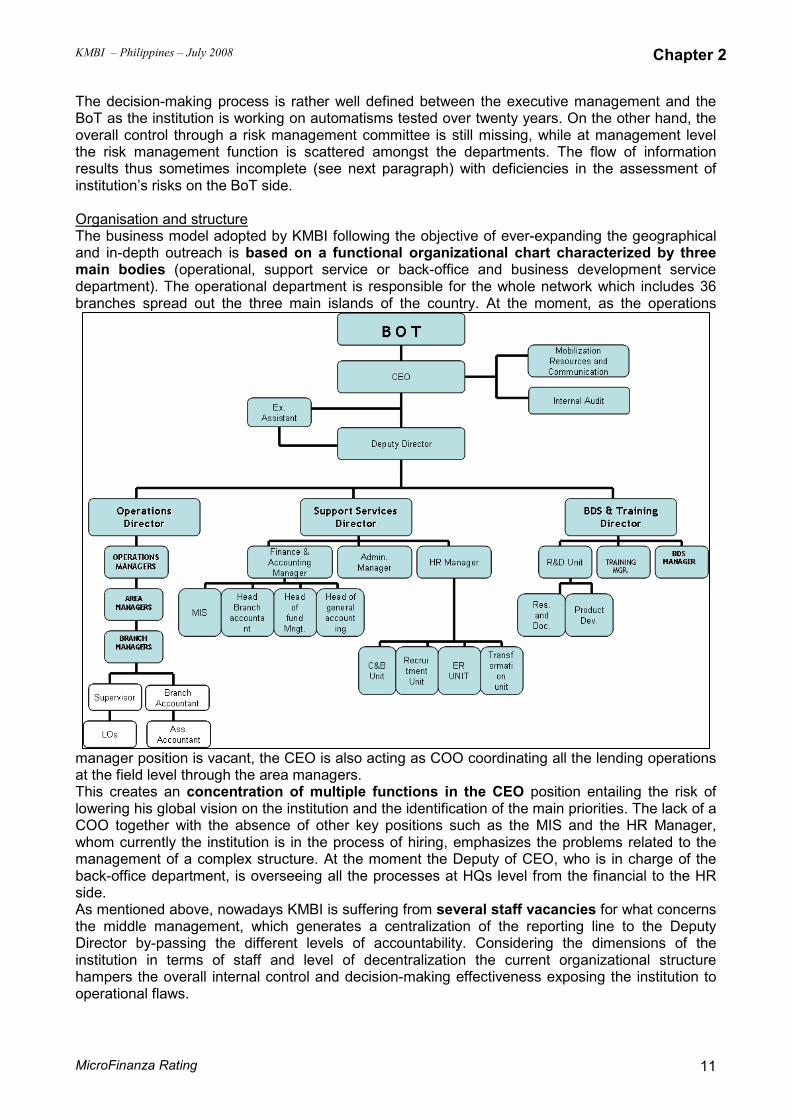

The decision-making process is rather well defined between the executive management and the BoT as the institution is working on automatisms tested over twenty years. On the other hand, the overall control through a risk management committee is still missing, while at management level the risk management function is scattered amongst the departments. The flow of information results thus sometimes incomplete (see next paragraph) with deficiencies in the assessment of institution’s risks on the BoT side. Organisation and structure The business model adopted by KMBI following the objective of ever-expanding the geographical and in-depth outreach is based on a functional organizational chart characterized by three main bodies (operational, support service or back-office and business development service department). The operational department is responsible for the whole network which includes 36 branches spread out the three main islands of the country. At the moment, as the operations

manager position is vacant, the CEO is also acting as COO coordinating all the lending operations at the field level through the area managers. This creates an concentration of multiple functions in the CEO position entailing the risk of lowering his global vision on the institution and the identification of the main priorities. The lack of a COO together with the absence of other key positions such as the MIS and the HR Manager, whom currently the institution is in the process of hiring, emphasizes the problems related to the management of a complex structure. At the moment the Deputy of CEO, who is in charge of the back-office department, is overseeing all the processes at HQs level from the financial to the HR side. As mentioned above, nowadays KMBI is suffering from several staff vacancies for what concerns the middle management, which generates a centralization of the reporting line to the Deputy Director by-passing the different levels of accountability. Considering the dimensions of the institution in terms of staff and level of decentralization the current organizational structure hampers the overall internal control and decision-making effectiveness exposing the institution to operational flaws.

KMBI – Philippines – July 2008 Chapter 2

MicroFinanza Rating 12

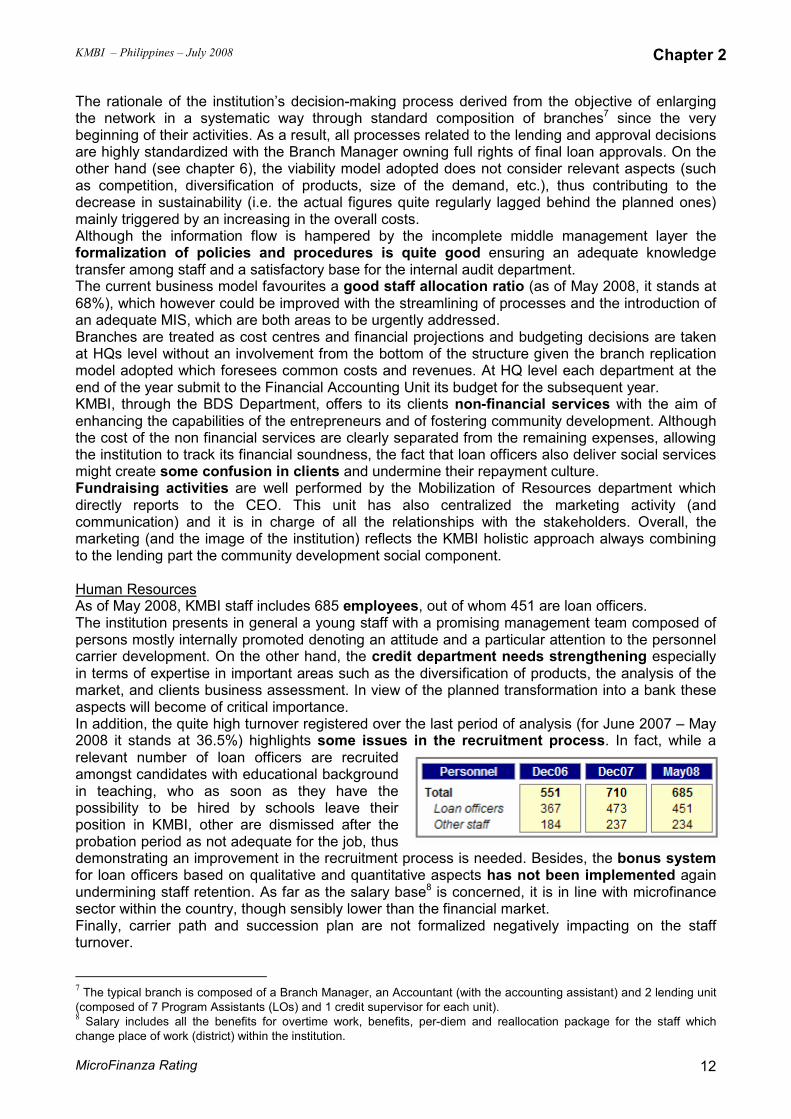

The rationale of the institution’s decision-making process derived from the objective of enlarging the network in a systematic way through standard composition of branches7 since the very beginning of their activities. As a result, all processes related to the lending and approval decisions are highly standardized with the Branch Manager owning full rights of final loan approvals. On the other hand (see chapter 6), the viability model adopted does not consider relevant aspects (such as competition, diversification of products, size of the demand, etc.), thus contributing to the decrease in sustainability (i.e. the actual figures quite regularly lagged behind the planned ones) mainly triggered by an increasing in the overall costs. Although the information flow is hampered by the incomplete middle management layer the formalization of policies and procedures is quite good ensuring an adequate knowledge transfer among staff and a satisfactory base for the internal audit department. The current business model favourites a good staff allocation ratio (as of May 2008, it stands at 68%), which however could be improved with the streamlining of processes and the introduction of an adequate MIS, which are both areas to be urgently addressed. Branches are treated as cost centres and financial projections and budgeting decisions are taken at HQs level without an involvement from the bottom of the structure given the branch replication model adopted which foresees common costs and revenues. At HQ level each department at the end of the year submit to the Financial Accounting Unit its budget for the subsequent year. KMBI, through the BDS Department, offers to its clients non-financial services with the aim of enhancing the capabilities of the entrepreneurs and of fostering community development. Although the cost of the non financial services are clearly separated from the remaining expenses, allowing the institution to track its financial soundness, the fact that loan officers also deliver social services might create some confusion in clients and undermine their repayment culture. Fundraising activities are well performed by the Mobilization of Resources department which directly reports to the CEO. This unit has also centralized the marketing activity (and communication) and it is in charge of all the relationships with the stakeholders. Overall, the marketing (and the image of the institution) reflects the KMBI holistic approach always combining to the lending part the community development social component. Human Resources As of May 2008, KMBI staff includes 685 employees, out of whom 451 are loan officers. The institution presents in general a young staff with a promising management team composed of persons mostly internally promoted denoting an attitude and a particular attention to the personnel carrier development. On the other hand, the credit department needs strengthening especially in terms of expertise in important areas such as the diversification of products, the analysis of the market, and clients business assessment. In view of the planned transformation into a bank these aspects will become of critical importance. In addition, the quite high turnover registered over the last period of analysis (for June 2007 – May 2008 it stands at 36.5%) highlights some issues in the recruitment process. In fact, while a relevant number of loan officers are recruited amongst candidates with educational background in teaching, who as soon as they have the possibility to be hired by schools leave their position in KMBI, other are dismissed after the probation period as not adequate for the job, thus demonstrating an improvement in the recruitment process is needed. Besides, the bonus system for loan officers based on qualitative and quantitative aspects has not been implemented again undermining staff retention. As far as the salary base8 is concerned, it is in line with microfinance sector within the country, though sensibly lower than the financial market. Finally, carrier path and succession plan are not formalized negatively impacting on the staff turnover.

7 The typical branch is composed of a Branch Manager, an Accountant (with the accounting assistant) and 2 lending unit (composed of 7 Program Assistants (LOs) and 1 credit supervisor for each unit). 8 Salary includes all the benefits for overtime work, benefits, per-diem and reallocation package for the staff which change place of work (district) within the institution.

KMBI – Philippines – July 2008 Chapter 2

MicroFinanza Rating 13

At the moment KMBI does not have a dedicate HR manager9 and the deputy of the CEO is coordinating all the HR processes and procedures. Staff appraisal is adequately carried out on a semi-annual basis and it follows the hierarchical structure for which each supervisor assesses the immediate subordinated staff together with a self-assessment undertaken by the employee. Training sessions are regularly delivered to the new staff by the branch managers in the already existing branches, while for the newly opened branches the training unit (together with the area manager) is responsible for preparing the staff locally. External training are based on the availability of providers within the local market and at the moment these types of training are mostly undergone by the top management. Overall, the training functions are split into two units (one reporting to the BDS department and the other one to the Support Services Department) somehow hampering training delivery efficiency and effectiveness (i.e. risk of training replication). Internal control and operational risk management KMBI does not have a risk management department overseeing all spheres within the internal control management and joining into a unique framework all the ex-ante procedures currently in place to mitigate the financial, credit and operational risks. On the other hand, the institution has established an internal audit (IA) department aiming at conducting ex-post investigation on the degree of compliance of the procedures at field and department level. The IA department is composed of 6 staff out of whom 3 have been hired during the last 9 months. The expansion of the department is the result of the necessity to increase the ex-post control as the previous on-site visits (1-2 a year) were not enough to ensure a thorough supervision. Currently 5 staff are responsible for branches audit according to a rotation rule. The IA department provides the Executive Director with two kind of reports respectively on a monthly and on a quarterly basis. The former is performed in order to check the inventory status at branch level, while the latter is aimed at carrying out a portfolio and accounting audit and takes usually between 1 and 2 weeks, also including on-site checks of a sample of clients covering almost 60% of the group centers in each branch. In addition, the audit department is in charge of checking the different departments and their expenses evolution versus the budget. In general, all the procedure ex-post are satisfactorily carried out and formalized in the audit manual, while ex-ante procedures and their monitoring are not properly coordinated and strongly hampered by the lack of a proper MIS and improvable segregation of functions and cash handling, which trigger a poor control on credit activities, characterized by a high level of decentralization and recurrent frauds. Accounting and external audit Over the period of analysis (2005, 2006 and 2007) KMBI’s financial statements were audited by SyCip Gorres Velayo and Co. (SGV and Co.)10 and, as of December 2007, the auditors expressed that KMBI’s financial statements are fairly compiled according to the Philippines Financial Reporting Standard. The main differences highlighted between the National Financial Reporting Standard and the IFRS are in reference with the interest accrual system which reflects the calculation of accrual interests only at the end of the year and not on a daily/monthly basis. In addition, grants for operating expenses received are not isolated after the net income lowering the full transparency of the financial results. Management Information System (MIS) The MIS represents for KMBI the main weakness exposing the institution to high operational risks. The institution recently (June 2008) hired an MIS officer who will be in charge of streamlining processes and consolidating the current equipment mostly at hardware level.

9 The institution is in the process of hiring an HR manager. 10 The audit company is a member of Ernst and Young Global.

KMBI – Philippines – July 2008 Chapter 2

MicroFinanza Rating 14

As of now, the institution is not endowed with an MIS neither in terms of a loan tracking nor an accounting system able to ensure a proper management of portfolio and accounting information and at the same time to provide the different departments with automated reliable reports. For what concerns the loan tracking system, all data are kept on paper through worksheets designed in 3 ad hoc booklets, with one copy remaining respectively with the leader of the group center (see chapter 3), one kept by the institution and one by the individual group members. The information about repayments and disbursement are then consolidated by the branch accountant and his assistant and transmitted to the HQs on a daily and monthly basis. The consolidation and the generation of information is performed through excel entailing manual errors and wasting of time. The institution does not have a consolidated database at central level including all clients and group’s information as the most relevant data are still kept on paper. Therefore, the institution is highly exposed to systematic mistakes and possibilities of frauds (i.e. ghost clients, no tracking of individual clients credit history). In addition, the lack of MIS is hampering the internal control rendering complex the detection of anomalies within the credit processes. Besides, the profitability of the institution is negatively affected by high operating expenses due to the manual work needed to ensure a minimum information flow between branches and HQs and the flexibility of the business model is also hampered by the absence of an MIS. Similarly, staff retention is undermined as the staff in charge of elaborating the information result to be overloaded and constantly under pressure. Back-up of available electronic documents at HQ level is carried out twice a week through the internal private network and on a monthly basis through CDs. At branch level, back-ups are not systematically nor frequently undertaken.

KMBI – Philippines -July 2008 Chapter 3

MicroFinanza Rating 15

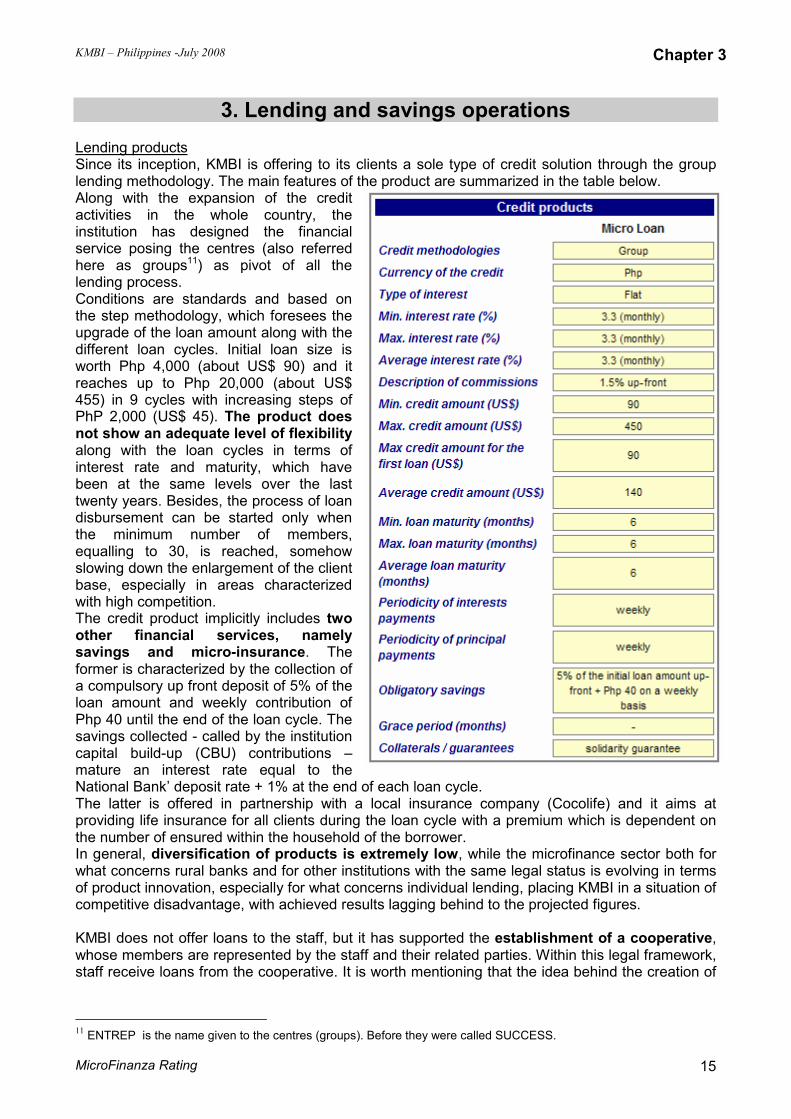

3. Lending and savings operations Lending products Since its inception, KMBI is offering to its clients a sole type of credit solution through the group lending methodology. The main features of the product are summarized in the table below. Along with the expansion of the credit activities in the whole country, the institution has designed the financial service posing the centres (also referred here as groups11) as pivot of all the lending process. Conditions are standards and based on the step methodology, which foresees the upgrade of the loan amount along with the different loan cycles. Initial loan size is worth Php 4,000 (about US$ 90) and it reaches up to Php 20,000 (about US$ 455) in 9 cycles with increasing steps of PhP 2,000 (US$ 45). The product does not show an adequate level of flexibility along with the loan cycles in terms of interest rate and maturity, which have been at the same levels over the last twenty years. Besides, the process of loan disbursement can be started only when the minimum number of members, equalling to 30, is reached, somehow slowing down the enlargement of the client base, especially in areas characterized with high competition. The credit product implicitly includes two other financial services, namely savings and micro-insurance. The former is characterized by the collection of a compulsory up front deposit of 5% of the loan amount and weekly contribution of Php 40 until the end of the loan cycle. The savings collected - called by the institution capital build-up (CBU) contributions – mature an interest rate equal to the National Bank’ deposit rate + 1% at the end of each loan cycle. The latter is offered in partnership with a local insurance company (Cocolife) and it aims at providing life insurance for all clients during the loan cycle with a premium which is dependent on the number of ensured within the household of the borrower. In general, diversification of products is extremely low, while the microfinance sector both for what concerns rural banks and for other institutions with the same legal status is evolving in terms of product innovation, especially for what concerns individual lending, placing KMBI in a situation of competitive disadvantage, with achieved results lagging behind to the projected figures. KMBI does not offer loans to the staff, but it has supported the establishment of a cooperative, whose members are represented by the staff and their related parties. Within this legal framework, staff receive loans from the cooperative. It is worth mentioning that the idea behind the creation of

11 ENTREP is the name given to the centres (groups). Before they were called SUCCESS.

KMBI – Philippines -July 2008 Chapter 3

MicroFinanza Rating 16

the cooperative is to exploit its role as potential shareholder for the expected setting up of the bank (see chapter 7). Lending procedures Lending policies are adequately formalized in the operations manual, which includes specific instructions to the credit officers on how to proceed with the groups since their formation until the repayments of the weekly instalments. Overall, the lending process takes 2 additional days after the 5 days during which loan officers organize the groups (from the orientation to the credit application collection meeting). At the Centre level, the group leader is responsible for the withdrawal of the loan at a KMBI partner bank and for the weekly repayments. All transactions are performed through banks apart from some circumstances12 during which the branch accountant collects loan repayments. The lending process has the same duration for repeated loan cycles, which have necessarily to follow most of the steps denoting a quite high rigidity in the methodology. This rigidity is worsened by the necessity to have always 30 members within a group before disbursing the loans. The analysis of the clients’ repayment capacity is very basic which is reasonable for the group lending methodology and given the loan size. However, the analysis of the ability to repay the loan is carried out once every three years generating the risk of not being able to capture all the changes in the client’s business evolution. Besides, the expenses of the business, the interest from the loan and the impact of the obligatory savings are not taken into account in the already overly simple cash flow, while often the loan amount granted does not reflect the member’s repayment capacity. Considering that all information about the loan lifespan of a single borrower is only collected at Centre level, the institution is not fully aware of the creditworthiness of single borrowers. In particular, in the case of loan default of one borrower the Centre intervenes charging a penalty (which is only internal and not submitted to the institution) and there are not documents indicating the individual status of each clients. Loans are backed with the solidarity guarantee, in some cases supported by physical collateral which can be demanded if the borrower is repeatedly late with the loan repayment. Collateral informal agreements are in force only at Centre level. Loan recovery is effectively carried out by the program assistant together with the group leader in case of a single borrower default. On the other hand, there does exist some difficulties in the loan recovery when a significant number of clients default within a group. This seems to be happening quite often due to the inaccuracy of the ex-ante procedures, especially for what concerns the mentioned evaluation of the repayment capacity for repeated groups. Thanks to weekly repayments loan officers carry out a constant supervision on the clients’ business albeit the information obtained during the visits and data on the credit evolution are not systematically kept in a system (see chapter 2) hampering a comprehensive understanding of the credit risk associated to the outstanding portfolio.

12 The branch Accountant accepts repayments when banks are already closed. During this type of transaction the

institution has experienced some small frauds as a procedure for cash handling is not well defined taking into account a proper segregation of functions.

KMBI – Philippines -July 2008 Chapter 4

MicroFinanza Rating 17

4. Assets structure and quality

Assets structure As of May 2008 net portfolio represents on average year on year 60% of total assets indicating a poor level of concentration of resources into the core business. The ratio remains constant over the three periods of analysis at around 60% (58% over 2006). The significant share of assets represented by liquid assets strongly limits the assets concentration into loan portfolio. In fact, liquid assets remain on average at very high levels, standing on average over the period

April 2007 – May 2008 at 31%, only partially justified by the necessity to keep liquid reserves for covering the liquidity risk triggered by the important amount of obligatory savings collected from current borrowers. The high levels of liquid assets is triggered by the conservative liquidity management, which to cope with the risk of maturity mismatches is based more on maintaining large liquid reserves than on a careful cash flow management, which should also take into consideration the historical trend of deposits retention. On the other end, the large share of cash and banks and short term investments, mainly represented by interbank placements13, significantly mitigate the risk of severe liquidity shortages in the case KMBI will be forced to pay taxes in arrear since 200514 and/or the BSP will conservatively regulate microfinance funds’ deposits collection. The large amount of liquid assets as of May 2008 has also been triggered by the declining demand for credit due to ever increasing competition and the need to accrue enough cash to pay the initial paid-in capital for the planned establishment of KMBI Bank. Portfolio structure As of May 200815, KMBI total outstanding portfolio is worth US$ 8 M, showing a slight 6.3% decline since December 2007, when it was about US$ 9 M, which represents an inversion in the general increasing trend characterizing the previous periods of analysis. The growth over the last three years has been rather modest, mainly due, as mentioned above, to increasing competition. The reverse of the generally increasing trend in portfolio has been also triggered by the adverse weather conditions at the beginning of 2008, affecting clients’ businesses, the closing of a branch in Mindanao16 in January 2008, due to pressure by a local revolutionary group, and the ever augmenting competition. Number of active clients follows a similar trend, declining of 14% from December 2007 to May 2008 after having experience a good 45% growth since December 2006. Outreach in depth remains at very good levels over time, with the average loan disbursed size

13 Yielding from 2.9% to 7% annual.

14 Only for 2005 KMBI would have to pay the Tax Bureau US$ 1.7M.

15 Portfolio data for the last period might not be fully reliable as the information have been manually tracked and have not

been audited by an independent external firm. 16 The branch of Compostela Valley.

Assets composition - May 2008

15%

59%

1% 3%

3%

19%

Cash and Banks Net Portfolio Net Fixed Assets

Financial Investments Accrued interest Other Assets

Liquid assets evolution (.000)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Dec05

Jun05

Dec05

Jun06

Dec06

Jun07

Dec07

May08

0%

5%

10%

15%

20%

25%

30%

35%

40%

Total assets Liquid assets Liquid assets (%)

KMBI – Philippines -July 2008 Chapter 4

MicroFinanza Rating 18

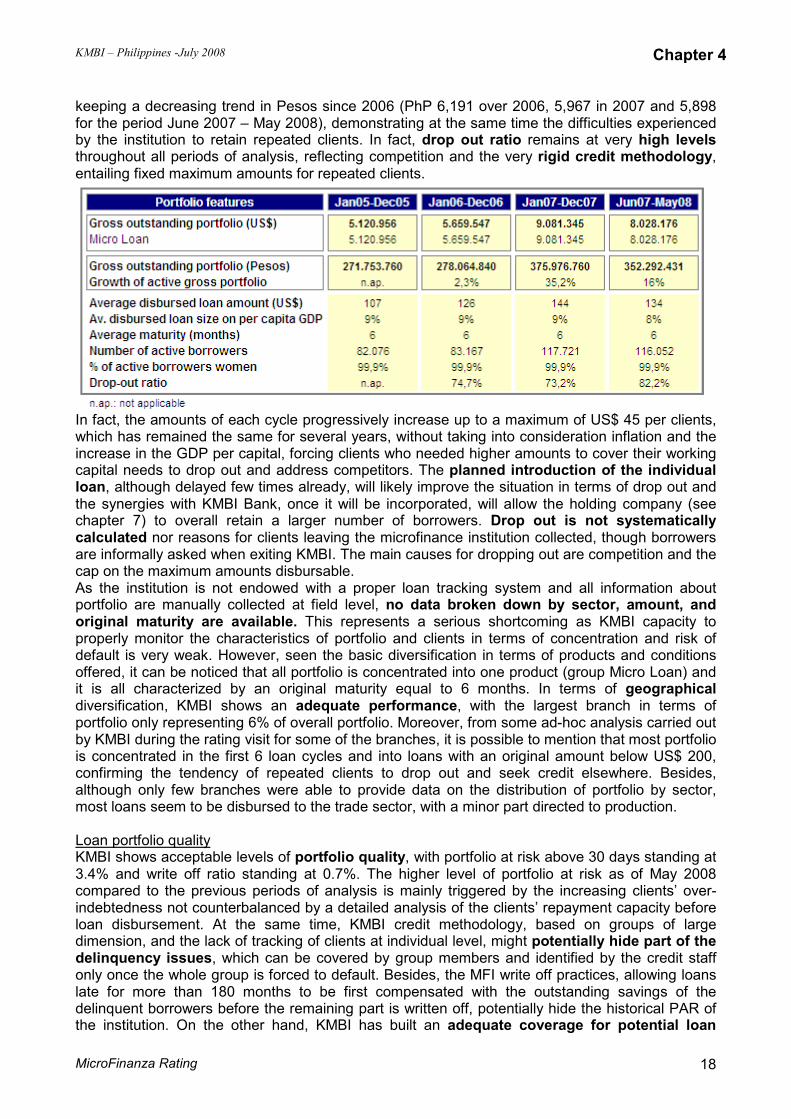

keeping a decreasing trend in Pesos since 2006 (PhP 6,191 over 2006, 5,967 in 2007 and 5,898 for the period June 2007 – May 2008), demonstrating at the same time the difficulties experienced by the institution to retain repeated clients. In fact, drop out ratio remains at very high levels throughout all periods of analysis, reflecting competition and the very rigid credit methodology, entailing fixed maximum amounts for repeated clients.

In fact, the amounts of each cycle progressively increase up to a maximum of US$ 45 per clients, which has remained the same for several years, without taking into consideration inflation and the increase in the GDP per capital, forcing clients who needed higher amounts to cover their working capital needs to drop out and address competitors. The planned introduction of the individual loan, although delayed few times already, will likely improve the situation in terms of drop out and the synergies with KMBI Bank, once it will be incorporated, will allow the holding company (see chapter 7) to overall retain a larger number of borrowers. Drop out is not systematically calculated nor reasons for clients leaving the microfinance institution collected, though borrowers are informally asked when exiting KMBI. The main causes for dropping out are competition and the cap on the maximum amounts disbursable. As the institution is not endowed with a proper loan tracking system and all information about portfolio are manually collected at field level, no data broken down by sector, amount, and original maturity are available. This represents a serious shortcoming as KMBI capacity to properly monitor the characteristics of portfolio and clients in terms of concentration and risk of default is very weak. However, seen the basic diversification in terms of products and conditions offered, it can be noticed that all portfolio is concentrated into one product (group Micro Loan) and it is all characterized by an original maturity equal to 6 months. In terms of geographical diversification, KMBI shows an adequate performance, with the largest branch in terms of portfolio only representing 6% of overall portfolio. Moreover, from some ad-hoc analysis carried out by KMBI during the rating visit for some of the branches, it is possible to mention that most portfolio is concentrated in the first 6 loan cycles and into loans with an original amount below US$ 200, confirming the tendency of repeated clients to drop out and seek credit elsewhere. Besides, although only few branches were able to provide data on the distribution of portfolio by sector, most loans seem to be disbursed to the trade sector, with a minor part directed to production. Loan portfolio quality KMBI shows acceptable levels of portfolio quality, with portfolio at risk above 30 days standing at 3.4% and write off ratio standing at 0.7%. The higher level of portfolio at risk as of May 2008 compared to the previous periods of analysis is mainly triggered by the increasing clients’ over-indebtedness not counterbalanced by a detailed analysis of the clients’ repayment capacity before loan disbursement. At the same time, KMBI credit methodology, based on groups of large dimension, and the lack of tracking of clients at individual level, might potentially hide part of the delinquency issues, which can be covered by group members and identified by the credit staff only once the whole group is forced to default. Besides, the MFI write off practices, allowing loans late for more than 180 months to be first compensated with the outstanding savings of the delinquent borrowers before the remaining part is written off, potentially hide the historical PAR of the institution. On the other hand, KMBI has built an adequate coverage for potential loan

KMBI – Philippines -July 2008 Chapter 4

MicroFinanza Rating 19

losses, with a risk coverage ratio equal to 117.1%, though in a decreasing trend since 2007, also due to quickly increasing portfolio at risk. Loan loss provisioning follows best practices (see annex 5), also includes a provision of 1% of performing portfolio, which is to be considered necessary considering that all outstanding portfolio is uncollateralized.

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000Portfolio quality (Pesos .000)

Outstanding portfolio PAR 30 (amount) PAR 30 (%)

KMBI – Philippines – July 2008 Chapter 5

MicroFinanza Rating 20

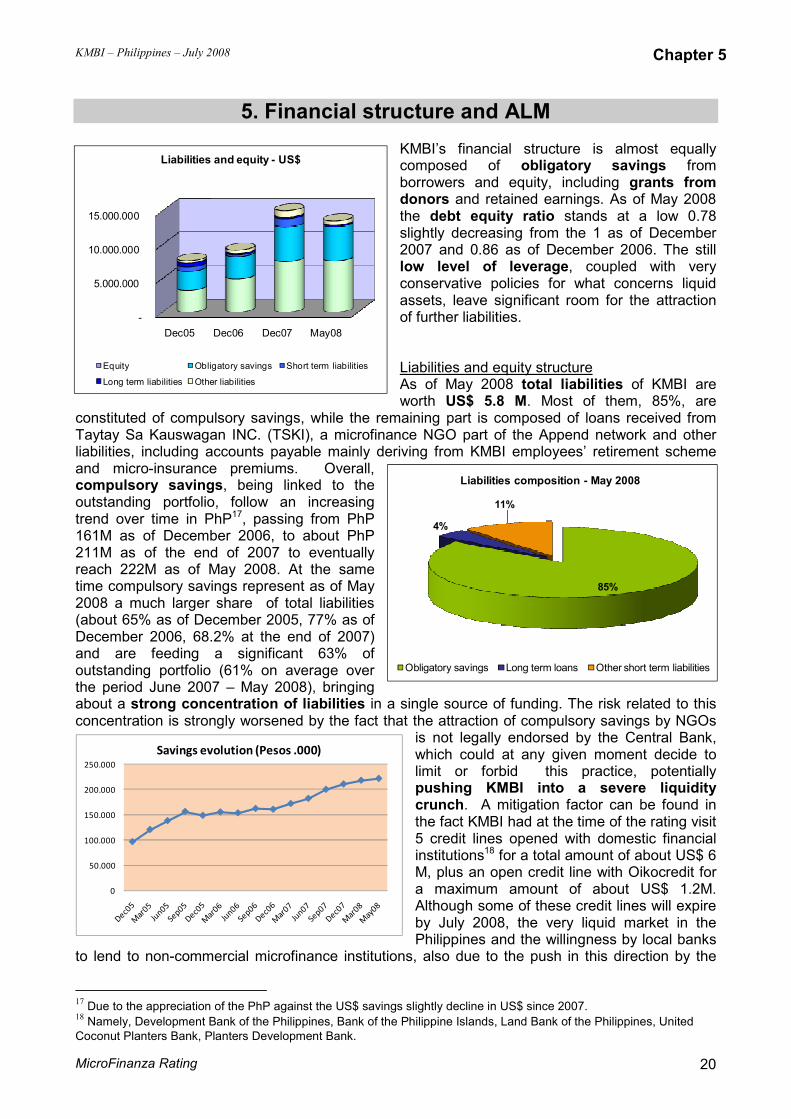

5. Financial structure and ALM

KMBI’s financial structure is almost equally composed of obligatory savings from borrowers and equity, including grants from donors and retained earnings. As of May 2008 the debt equity ratio stands at a low 0.78 slightly decreasing from the 1 as of December 2007 and 0.86 as of December 2006. The still low level of leverage, coupled with very conservative policies for what concerns liquid assets, leave significant room for the attraction of further liabilities. Liabilities and equity structure As of May 2008 total liabilities of KMBI are worth US$ 5.8 M. Most of them, 85%, are

constituted of compulsory savings, while the remaining part is composed of loans received from Taytay Sa Kauswagan INC. (TSKI), a microfinance NGO part of the Append network and other liabilities, including accounts payable mainly deriving from KMBI employees’ retirement scheme and micro-insurance premiums. Overall, compulsory savings, being linked to the outstanding portfolio, follow an increasing trend over time in PhP17, passing from PhP 161M as of December 2006, to about PhP 211M as of the end of 2007 to eventually reach 222M as of May 2008. At the same time compulsory savings represent as of May 2008 a much larger share of total liabilities (about 65% as of December 2005, 77% as of December 2006, 68.2% at the end of 2007) and are feeding a significant 63% of outstanding portfolio (61% on average over the period June 2007 – May 2008), bringing about a strong concentration of liabilities in a single source of funding. The risk related to this concentration is strongly worsened by the fact that the attraction of compulsory savings by NGOs

is not legally endorsed by the Central Bank, which could at any given moment decide to limit or forbid this practice, potentially pushing KMBI into a severe liquidity crunch. A mitigation factor can be found in the fact KMBI had at the time of the rating visit 5 credit lines opened with domestic financial institutions18 for a total amount of about US$ 6 M, plus an open credit line with Oikocredit for a maximum amount of about US$ 1.2M. Although some of these credit lines will expire by July 2008, the very liquid market in the Philippines and the willingness by local banks

to lend to non-commercial microfinance institutions, also due to the push in this direction by the

17 Due to the appreciation of the PhP against the US$ savings slightly decline in US$ since 2007.

18 Namely, Development Bank of the Philippines, Bank of the Philippine Islands, Land Bank of the Philippines, United

Coconut Planters Bank, Planters Development Bank.

-

5.000.000

10.000.000

15.000.000

Dec05 Dec06 Dec07 May08

Liabilities and equity - US$

Equity Obligatory savings Short term liabilities

Long term liabilities Other liabilities

85%

4%

11%

Liabilities composition - May 2008

Obligatory savings Long term loans Other short term liabilities

0

50.000

100.000

150.000

200.000

250.000

Savings evolution (Pesos .000)

KMBI – Philippines – July 2008 Chapter 5

MicroFinanza Rating 21

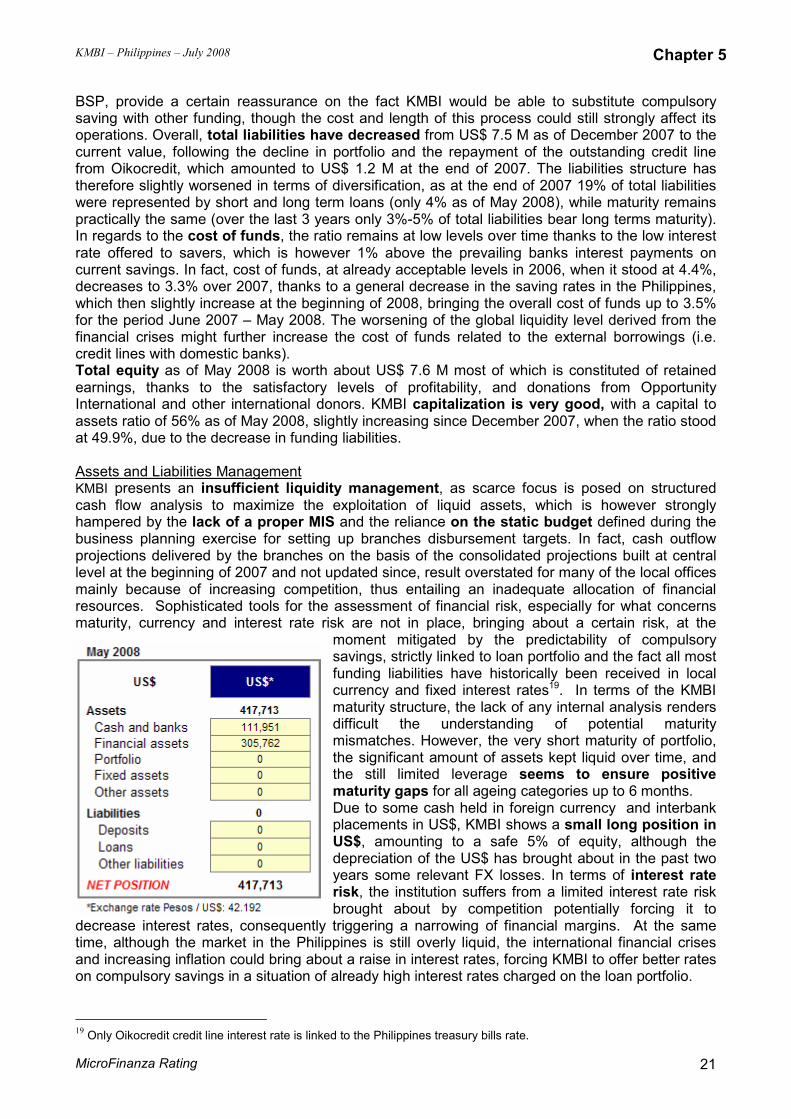

BSP, provide a certain reassurance on the fact KMBI would be able to substitute compulsory saving with other funding, though the cost and length of this process could still strongly affect its operations. Overall, total liabilities have decreased from US$ 7.5 M as of December 2007 to the current value, following the decline in portfolio and the repayment of the outstanding credit line from Oikocredit, which amounted to US$ 1.2 M at the end of 2007. The liabilities structure has therefore slightly worsened in terms of diversification, as at the end of 2007 19% of total liabilities were represented by short and long term loans (only 4% as of May 2008), while maturity remains practically the same (over the last 3 years only 3%-5% of total liabilities bear long terms maturity). In regards to the cost of funds, the ratio remains at low levels over time thanks to the low interest rate offered to savers, which is however 1% above the prevailing banks interest payments on current savings. In fact, cost of funds, at already acceptable levels in 2006, when it stood at 4.4%, decreases to 3.3% over 2007, thanks to a general decrease in the saving rates in the Philippines, which then slightly increase at the beginning of 2008, bringing the overall cost of funds up to 3.5% for the period June 2007 – May 2008. The worsening of the global liquidity level derived from the financial crises might further increase the cost of funds related to the external borrowings (i.e. credit lines with domestic banks). Total equity as of May 2008 is worth about US$ 7.6 M most of which is constituted of retained earnings, thanks to the satisfactory levels of profitability, and donations from Opportunity International and other international donors. KMBI capitalization is very good, with a capital to assets ratio of 56% as of May 2008, slightly increasing since December 2007, when the ratio stood at 49.9%, due to the decrease in funding liabilities. Assets and Liabilities Management KMBI presents an insufficient liquidity management, as scarce focus is posed on structured cash flow analysis to maximize the exploitation of liquid assets, which is however strongly hampered by the lack of a proper MIS and the reliance on the static budget defined during the business planning exercise for setting up branches disbursement targets. In fact, cash outflow projections delivered by the branches on the basis of the consolidated projections built at central level at the beginning of 2007 and not updated since, result overstated for many of the local offices mainly because of increasing competition, thus entailing an inadequate allocation of financial resources. Sophisticated tools for the assessment of financial risk, especially for what concerns maturity, currency and interest rate risk are not in place, bringing about a certain risk, at the

moment mitigated by the predictability of compulsory savings, strictly linked to loan portfolio and the fact all most funding liabilities have historically been received in local currency and fixed interest rates19. In terms of the KMBI maturity structure, the lack of any internal analysis renders difficult the understanding of potential maturity mismatches. However, the very short maturity of portfolio, the significant amount of assets kept liquid over time, and the still limited leverage seems to ensure positive maturity gaps for all ageing categories up to 6 months. Due to some cash held in foreign currency and interbank placements in US$, KMBI shows a small long position in US$, amounting to a safe 5% of equity, although the depreciation of the US$ has brought about in the past two years some relevant FX losses. In terms of interest rate risk, the institution suffers from a limited interest rate risk brought about by competition potentially forcing it to

decrease interest rates, consequently triggering a narrowing of financial margins. At the same time, although the market in the Philippines is still overly liquid, the international financial crises and increasing inflation could bring about a raise in interest rates, forcing KMBI to offer better rates on compulsory savings in a situation of already high interest rates charged on the loan portfolio.

19 Only Oikocredit credit line interest rate is linked to the Philippines treasury bills rate.

KMBI – Philippines – July 2008 Chapter 6

MicroFinanza Rating 22

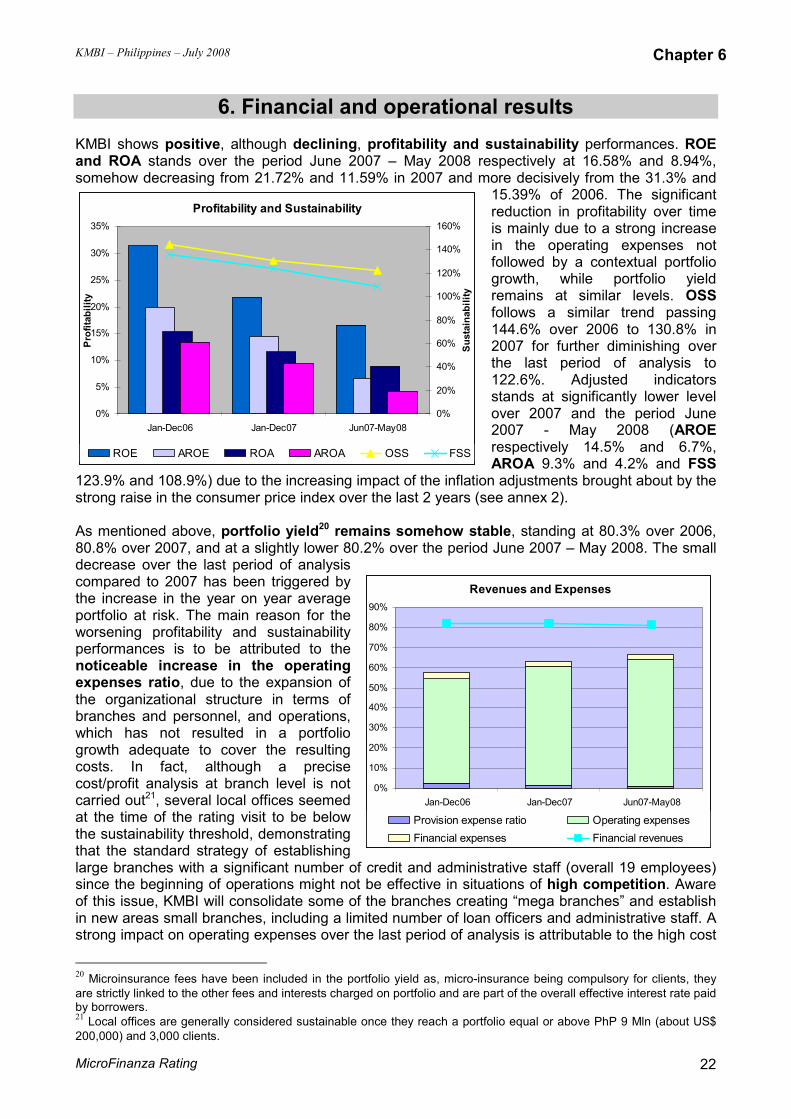

6. Financial and operational results KMBI shows positive, although declining, profitability and sustainability performances. ROE and ROA stands over the period June 2007 – May 2008 respectively at 16.58% and 8.94%, somehow decreasing from 21.72% and 11.59% in 2007 and more decisively from the 31.3% and

15.39% of 2006. The significant reduction in profitability over time is mainly due to a strong increase in the operating expenses not followed by a contextual portfolio growth, while portfolio yield remains at similar levels. OSS follows a similar trend passing 144.6% over 2006 to 130.8% in 2007 for further diminishing over the last period of analysis to 122.6%. Adjusted indicators stands at significantly lower level over 2007 and the period June 2007 - May 2008 (AROE respectively 14.5% and 6.7%, AROA 9.3% and 4.2% and FSS

123.9% and 108.9%) due to the increasing impact of the inflation adjustments brought about by the strong raise in the consumer price index over the last 2 years (see annex 2). As mentioned above, portfolio yield20 remains somehow stable, standing at 80.3% over 2006, 80.8% over 2007, and at a slightly lower 80.2% over the period June 2007 – May 2008. The small decrease over the last period of analysis compared to 2007 has been triggered by the increase in the year on year average portfolio at risk. The main reason for the worsening profitability and sustainability performances is to be attributed to the noticeable increase in the operating expenses ratio, due to the expansion of the organizational structure in terms of branches and personnel, and operations, which has not resulted in a portfolio growth adequate to cover the resulting costs. In fact, although a precise cost/profit analysis at branch level is not carried out21, several local offices seemed at the time of the rating visit to be below the sustainability threshold, demonstrating that the standard strategy of establishing large branches with a significant number of credit and administrative staff (overall 19 employees) since the beginning of operations might not be effective in situations of high competition. Aware of this issue, KMBI will consolidate some of the branches creating “mega branches” and establish in new areas small branches, including a limited number of loan officers and administrative staff. A strong impact on operating expenses over the last period of analysis is attributable to the high cost

20 Microinsurance fees have been included in the portfolio yield as, micro-insurance being compulsory for clients, they

are strictly linked to the other fees and interests charged on portfolio and are part of the overall effective interest rate paid by borrowers. 21 Local offices are generally considered sustainable once they reach a portfolio equal or above PhP 9 Mln (about US$

200,000) and 3,000 clients.

Profitability and Sustainability

0%

5%

10%

15%

20%

25%

30%

35%

Jan-Dec06 Jan-Dec07 Jun07-May08

Pro

fita

bil

ity

0%

20%

40%

60%

80%

100%

120%

140%

160%

Su

sta

inab

ilit

yROE AROE ROA AROA OSS FSS

Revenues and Expenses

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Jan-Dec06 Jan-Dec07 Jun07-May08

Provision expense ratio Operating expenses

Financial expenses Financial revenues

KMBI – Philippines – July 2008 Chapter 6

MicroFinanza Rating 23

of the organization of the annual Append camp and other meetings (10% of Jan – May 2008 total operating expenses). It is worth mentioning that KMBI shows historically low levels of efficiency, with an operating expenses ratio well above 50% for all period of analysis, denoting the high cost of carrying out operations also triggered by the lack of an MIS system, the low average disbursed loan size and the strong geographical decentralization. Although the operational margin22 remains at adequate levels thanks to the high effective interest rates charged to borrowers, it has been rapidly declining from the 24.1% in 2006 and 17.4% over 2007 to 13.1% over the last period of analysis, due to the already mentioned noticeable increase in the operating expenses ratio, which abundantly counterbalance the small decrease in the funding expenses ratio since 2006 and the smaller expenses dedicated to the provisioning for potential loan losses. The potential increase in expenses in the case KMBI will be forced to pay the profit tax since 2005, and will need in the future to diversify its financial structure with loans from domestic and international investors, could strongly impact on the institution’s margins and urgently call for better performances in terms of efficiency and productivity. Staff allocation ratio shows adequate levels, with the majority of staff engaged into credit operation, although also giving hints that the credit department might be overstaffed.

This

is confirmed by the loan officer productivity by borrowers, which stands at rather low levels if considering KMBI offers credit to large groups, composed of 30 or more members, a methodology that usually facilitates higher productivity. Funding expenses ratio remains rather stable over the last 2 periods on analysis, while diminishing since the period January – December 2006, due to the increase in the cost of obligatory savings (see chapter 5). Provision expenses ratio shows lower values in 2007 and over period June 2007 – May 2008, due to the noticeable betterment of portfolio quality at the end of 2007. However, due to the worsening of PAR 30 over the first 5 months of 2008, the provision expense ratio has significantly increased, standing for the period January – May 2008 at 3.8%.

Overall, KMBI has been characterized by good financial performances, which are however sustained mainly through high portfolio yield than with satisfactory levels of efficiency and productivity. Operating expenses show high and increasing values, strongly influencing operational margins, which are rapidly decreasing and could suffer further narrowing in the case KMBI will be forced to pay profit taxes since 2005 or to increasingly use financial resources from domestic and international investors, while deposit rates could be contextually becoming more expensive. Moreover, the ever increasing competition could force the institution to decrease its interest rates, thus exercising additional pressure on margins. The streamlining of the organizational structure, also through the purchase of a proper MIS and the rationalization of the expansion model, becomes of critical importance for allowing KMBI to maintain good profitability and sustainability performances while further expanding on the territory.

22 Financial revenues minus operational and financial expenses.

KMBI – Philippines – July 2008 Chapter 7

MicroFinanza Rating 24

7. Strategic objectives and financial needs General guidelines for future evolution KMBI strategic objectives are pointed out in the Business Plan compiled for the period 2007-2011, while the budget for the same timeframe groups all the planned financial achievements. The BP includes 7 main objectives and presents an operational plan rather detailed for the 5 years with the activities to be implemented in each department. Nevertheless, the contents as well as the figures have not been updated since the first edition of the business plan (end of 2006). As a result, the current status of the MFI significantly lags behind the timeframe defined at the beginning. The business plan reflects the holistic approach of the institution (i.e. providing financial services and fostering community development) and the main goal is to reach 250,000 clients by the end of 2011. In order to achieve this level of outreach the institution intends to open 30 additional branches by 2011. In terms of portfolio, according to the figures highlighted in the balance sheet for 2008, the institution should reach US$ 30 Mln, while as of May 2008 KMBI has an outstanding portfolio equal to about US$ 8 Mln. The projections reflect the aggressive strategy focused on expanding the network without taking into account important aspects such as competition and the capacity of the structure to absorb such an important growth. This is quite notable also analysing the monthly planned cash flow and the actual result which systematically show relevant discrepancies. For what concerns the organizational structure, as mentioned in the second chapter, the institution suffers from multiple staff deficiencies especially in the middle management while the business plan does not include the proper steps to cover this important issue. Furthermore, although the institution has planned to develop and implement an MIS replacing the current Excel in 2007, the process has been delayed and still not significant actions have been undertaken in this regard. The need of a system able to capture all portfolio data ensuring a more effective control was already highlighted 2 years ago by the periodical assessment performed by the Opportunity International network. For what concerns the legal framework, KMBI is planning to transform into a bank, a process which has been partially undergone in 200123 but not concluded. According to the BP, the transformation into a bank was to be implemented by 2007, but the definition of the ownership structure has become increasingly complicated. In particular, the fact that the new regulation allows NGOs to be shareholder in other financial institutions for a maximum of 40%24 has introduced the challenge of defining the remain portion of ownership. KMBI intends to include the staff cooperative25 as second shareholder (for 40%) and the remaining 20% inviting some private investors. However, the participation of the cooperative will require time as it will need to build the necessary capital. Beside the establishment of the bank, KMBI intends to maintain the NGO in existence as demonstrated by the planned growth. The role of the NGO will be as an incubator expanding the outreach and then transferring the best repeated clients to the bank. In addition, an independent training entity will be set up and together with the NGO and the bank will depend on the KMBI Holding. The institution presents multiple deficiencies not only in terms of staff but also for what concerns product development. The process of transformation will require a strengthening of the MIS and the credit department as main priorities. For this reason, the timeframe regarding the transformation will likely undergo further delays. In addition, a revision of the cost structure will be

23 In 2001, KMBI was involved in the creation of Opportunity Microfinance Bank (OMB) transferring part of the assets, but

the process was not concluded as the other parties involved had some problems. However, the OMB was created and KMBI continues to operate as NGO. 24 Previously NGOs were allowed to be shareholder for a maximum of 70%.

25See chapter 3. The cooperative (called 4HG) has been established with the aim of providing loans to the staff and

related parties. The cooperative is managed by the staff and KMBI does not have any shares within this organization.

KMBI – Philippines – July 2008 Chapter 7

MicroFinanza Rating 25

of critical importance taking into account the growing competition and further need for funds the institution will face within the banking sector. Financial needs KMBI funding strategy is mainly based on savings, while the remaining portion is represented by liabilities from local banks26 bearing an interest rate of 6% and a credit line from Oikocredit (which bears 9.5% interest rate). Partnerships with local banks will be the main reference for KMBI as the Philippines financial market is quite liquid and bears lower financial costs compared to the international one.

26 Local banks such as Landbank, BPI and DVP.

KMBI – Philippines – July 2008 Chapter 8

MicroFinanza Rating 26

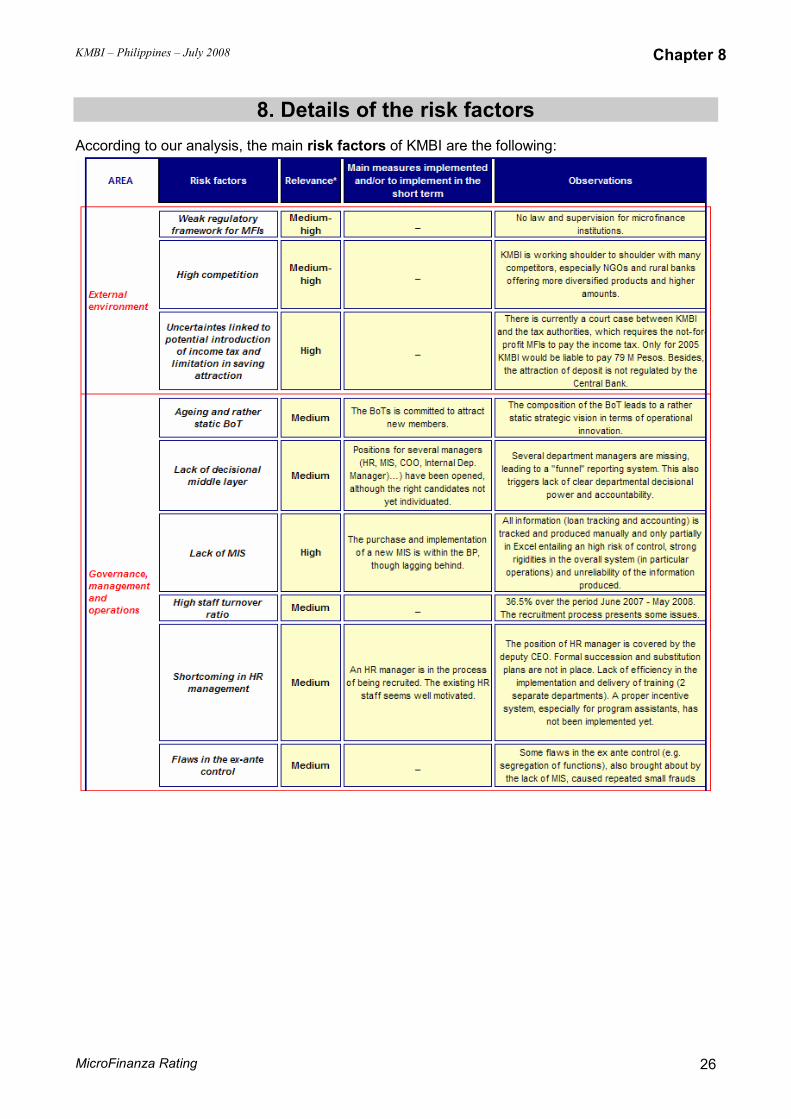

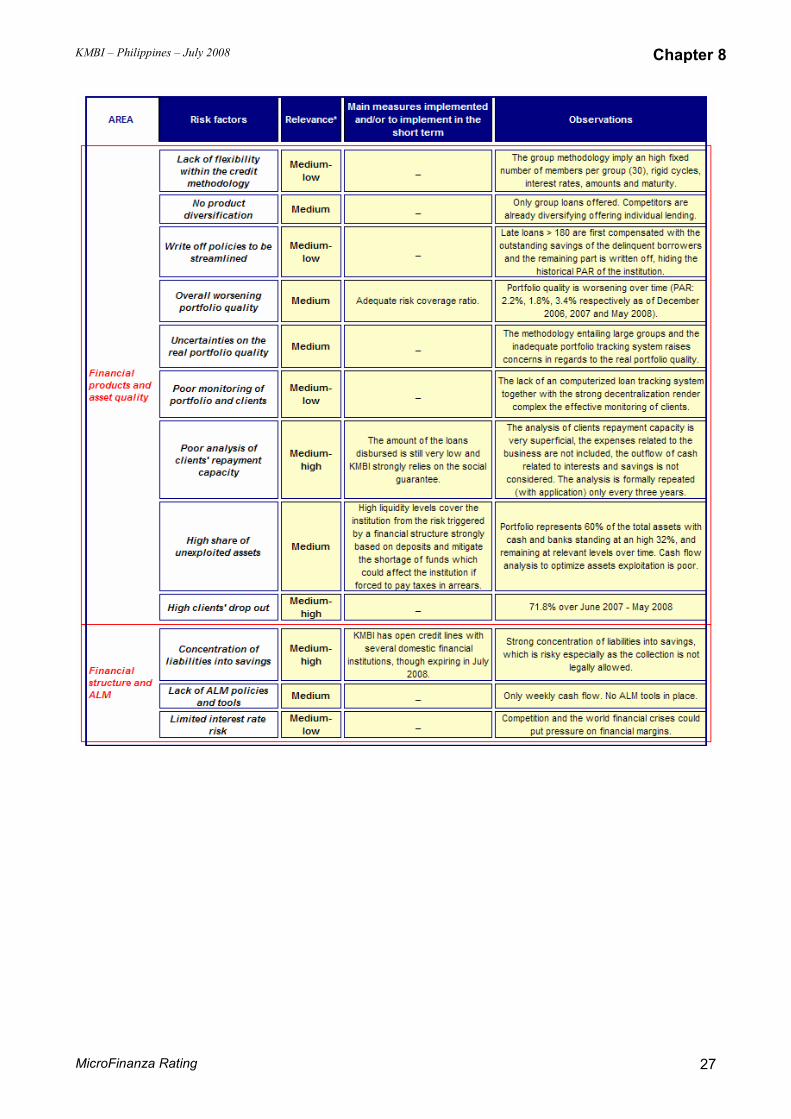

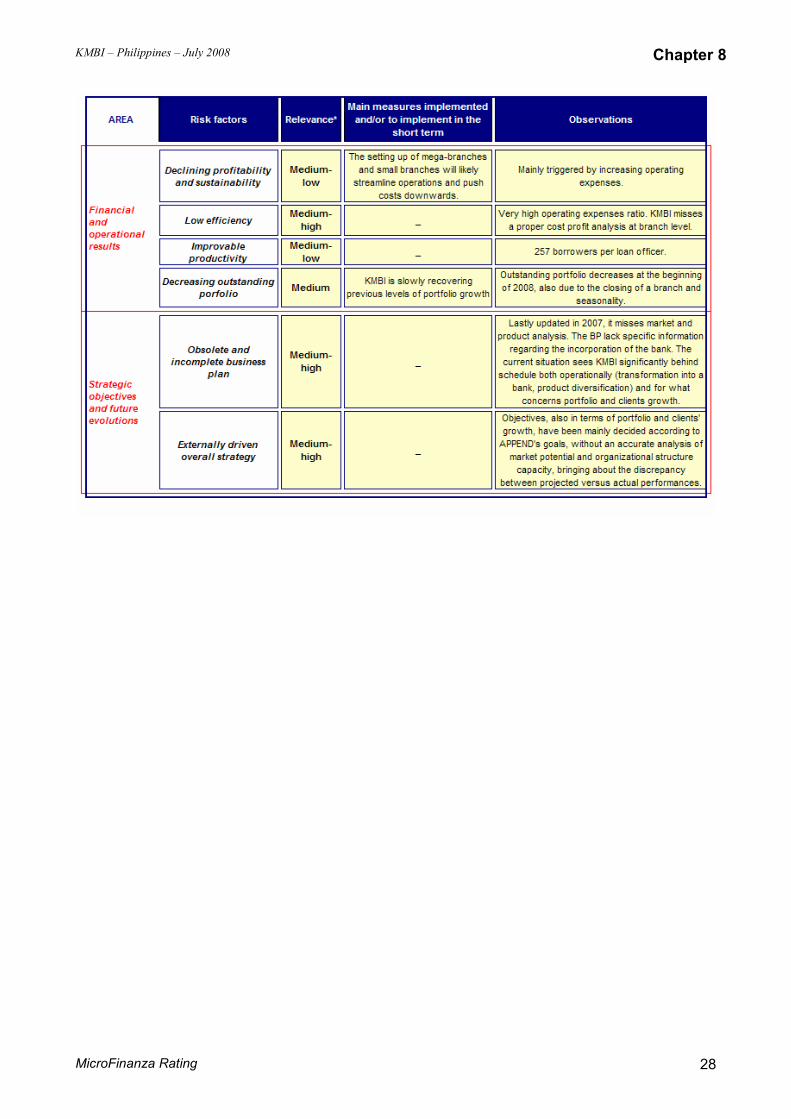

8. Details of the risk factors

According to our analysis, the main risk factors of KMBI are the following:

KMBI – Philippines – July 2008 Chapter 8

MicroFinanza Rating 27

KMBI – Philippines – July 2008 Chapter 8

MicroFinanza Rating 28

KMBI – Philippines – July 2008 Annex 1

MicroFinanza Rating 29

Annex 1 - Financial statements

KMBI – Philippines – July 2008 Annex 1

MicroFinanza Rating 30

KMBI – Philippines – July 2008 Annex 2

MicroFinanza Rating 31

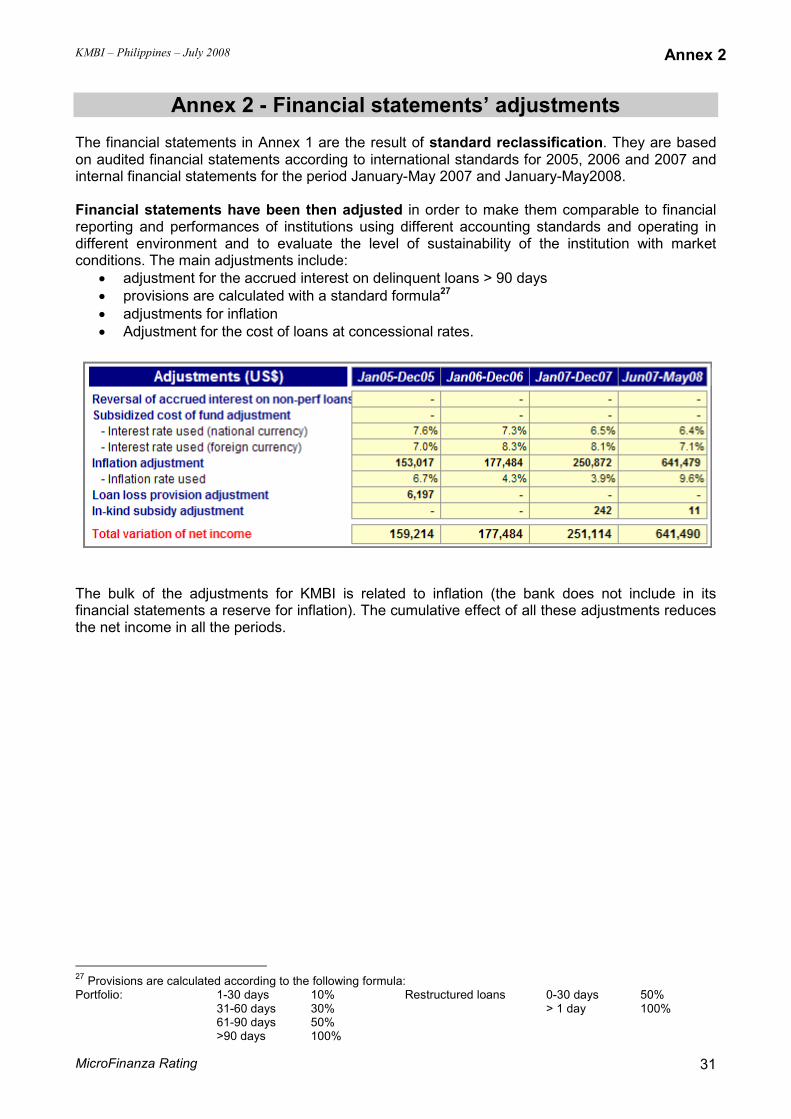

Annex 2 - Financial statements’ adjustments The financial statements in Annex 1 are the result of standard reclassification. They are based on audited financial statements according to international standards for 2005, 2006 and 2007 and internal financial statements for the period January-May 2007 and January-May2008.

Financial statements have been then adjusted in order to make them comparable to financial reporting and performances of institutions using different accounting standards and operating in different environment and to evaluate the level of sustainability of the institution with market conditions. The main adjustments include:

• adjustment for the accrued interest on delinquent loans > 90 days • provisions are calculated with a standard formula27 • adjustments for inflation • Adjustment for the cost of loans at concessional rates.

The bulk of the adjustments for KMBI is related to inflation (the bank does not include in its financial statements a reserve for inflation). The cumulative effect of all these adjustments reduces the net income in all the periods.

27 Provisions are calculated according to the following formula:

Portfolio: 1-30 days 10% Restructured loans 0-30 days 50% 31-60 days 30% > 1 day 100% 61-90 days 50% >90 days 100%

KMBI – Philippines – July 2008 Annex 3

MicroFinanza Rating 32

Annex 3 - Financial ratios

KMBI – Philippines – July 2008 Annex 3

MicroFinanza Rating 33

KMBI – Philippines – July 2008 Annex 4

MicroFinanza Rating 34

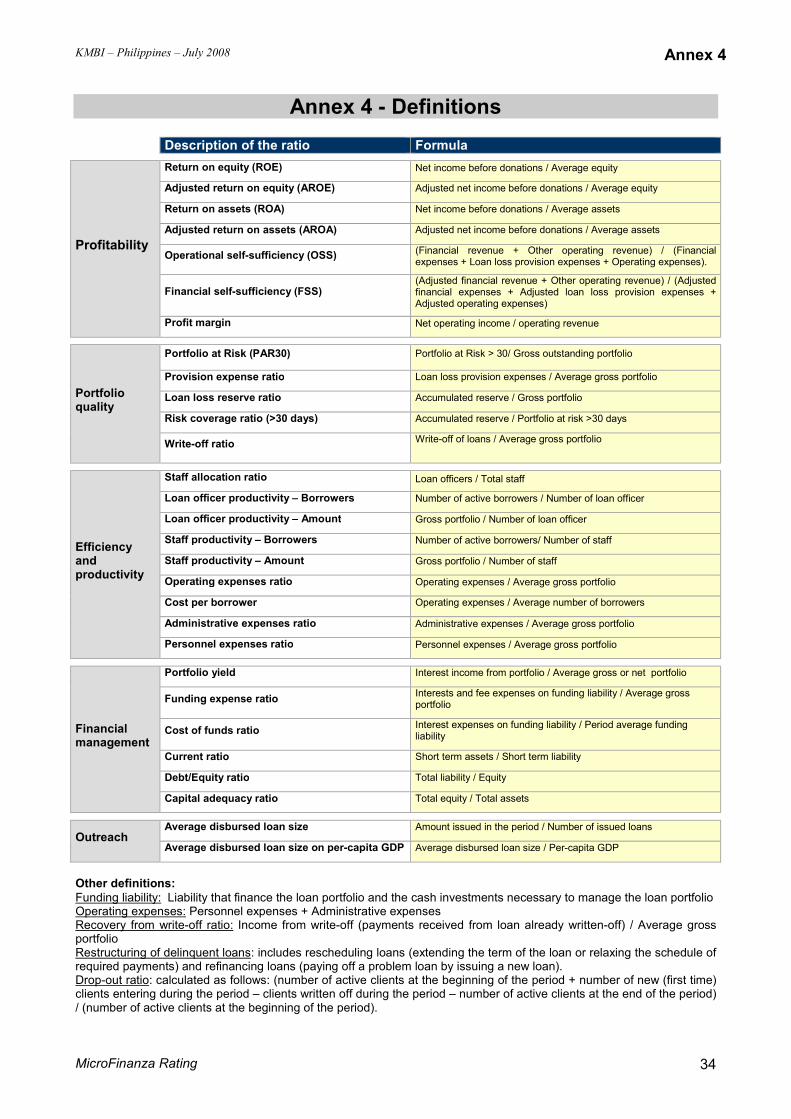

Annex 4 - Definitions

Description of the ratio Formula

Profitability

Return on equity (ROE) Net income before donations / Average equity

Adjusted return on equity (AROE) Adjusted net income before donations / Average equity

Return on assets (ROA) Net income before donations / Average assets

Adjusted return on assets (AROA) Adjusted net income before donations / Average assets

Operational self-sufficiency (OSS) (Financial revenue + Other operating revenue) / (Financial expenses + Loan loss provision expenses + Operating expenses).

Financial self-sufficiency (FSS) (Adjusted financial revenue + Other operating revenue) / (Adjusted financial expenses + Adjusted loan loss provision expenses + Adjusted operating expenses)

Profit margin Net operating income / operating revenue

Portfolio quality

Portfolio at Risk (PAR30) Portfolio at Risk > 30/ Gross outstanding portfolio

Provision expense ratio Loan loss provision expenses / Average gross portfolio

Loan loss reserve ratio Accumulated reserve / Gross portfolio

Risk coverage ratio (>30 days) Accumulated reserve / Portfolio at risk >30 days

Write-off ratio Write-off of loans / Average gross portfolio

Efficiency and productivity

Staff allocation ratio Loan officers / Total staff

Loan officer productivity – Borrowers Number of active borrowers / Number of loan officer

Loan officer productivity – Amount Gross portfolio / Number of loan officer

Staff productivity – Borrowers Number of active borrowers/ Number of staff

Staff productivity – Amount Gross portfolio / Number of staff

Operating expenses ratio Operating expenses / Average gross portfolio

Cost per borrower Operating expenses / Average number of borrowers

Administrative expenses ratio Administrative expenses / Average gross portfolio

Personnel expenses ratio Personnel expenses / Average gross portfolio

Financial management

Portfolio yield Interest income from portfolio / Average gross or net portfolio

Funding expense ratio Interests and fee expenses on funding liability / Average gross portfolio

Cost of funds ratio Interest expenses on funding liability / Period average funding liability

Current ratio Short term assets / Short term liability

Debt/Equity ratio Total liability / Equity

Capital adequacy ratio Total equity / Total assets

Outreach Average disbursed loan size Amount issued in the period / Number of issued loans

Average disbursed loan size on per-capita GDP Average disbursed loan size / Per-capita GDP

Other definitions: Funding liability: Liability that finance the loan portfolio and the cash investments necessary to manage the loan portfolio Operating expenses: Personnel expenses + Administrative expenses Recovery from write-off ratio: Income from write-off (payments received from loan already written-off) / Average gross portfolio Restructuring of delinquent loans: includes rescheduling loans (extending the term of the loan or relaxing the schedule of required payments) and refinancing loans (paying off a problem loan by issuing a new loan). Drop-out ratio: calculated as follows: (number of active clients at the beginning of the period + number of new (first time) clients entering during the period – clients written off during the period – number of active clients at the end of the period) / (number of active clients at the beginning of the period).

KMBI – Philippines – July 2008 Annex 5

MicroFinanza Rating 35

Annex 5 - Guidelines of reporting and accounting Financial statements Over the period of analysis (2005, 2006 and 2007) KMBI Bank’s financial statements were audited respectively by Laya Mananghya (KPMG), Manabat Sanagustin and Co. (KPMG) SyCip Gorres Velayo and Co. (SGV and Co.) according to Philippines Accounting Standards.

Loan loss provision and write-offs