survey on employment in european shipbuilding countries...

TRANSCRIPT

AgS-Monitoring Shipbuilding

Survey on Employment in European Shipbuilding Countries

- Selected Results -

Sector Committee Shipbuilding

Thorsten Ludwig

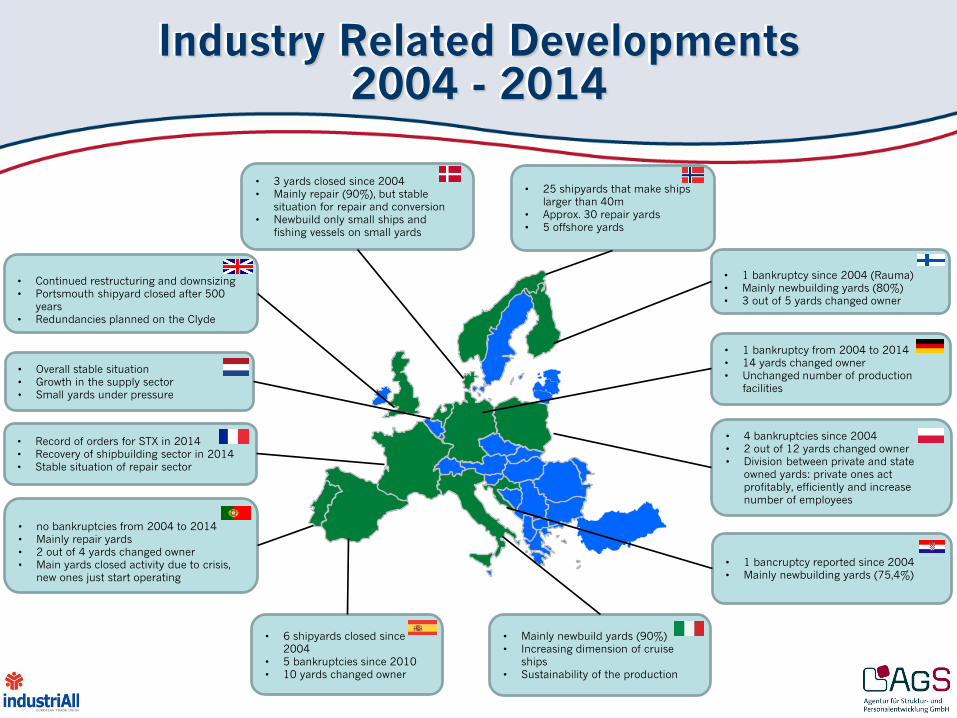

Industry Related Developments 2004 - 2014

• Overall stable situation • Growth in the supply sector • Small yards under pressure

• Record of orders for STX in 2014 • Recovery of shipbuilding sector in 2014 • Stable situation of repair sector

• no bankruptcies from 2004 to 2014 • Mainly repair yards • 2 out of 4 yards changed owner • Main yards closed activity due to crisis,

new ones just start operating

• 6 shipyards closed since 2004

• 5 bankruptcies since 2010 • 10 yards changed owner

• Mainly newbuild yards (90%) • Increasing dimension of cruise

ships • Sustainability of the production

• 1 bancruptcy reported since 2004 • Mainly newbuilding yards (75,4%)

• 4 bankruptcies since 2004 • 2 out of 12 yards changed owner • Division between private and state

owned yards: private ones act profitably, efficiently and increase number of employees

• 1 bankruptcy from 2004 to 2014 • 14 yards changed owner • Unchanged number of production

facilities

• 1 bankruptcy since 2004 (Rauma) • Mainly newbuilding yards (80%) • 3 out of 5 yards changed owner

• 25 shipyards that make ships

larger than 40m • Approx. 30 repair yards • 5 offshore yards

• 3 yards closed since 2004 • Mainly repair (90%), but stable

situation for repair and conversion • Newbuild only small ships and

fishing vessels on small yards

• Continued restructuring and downsizing • Portsmouth shipyard closed after 500

years • Redundancies planned on the Clyde

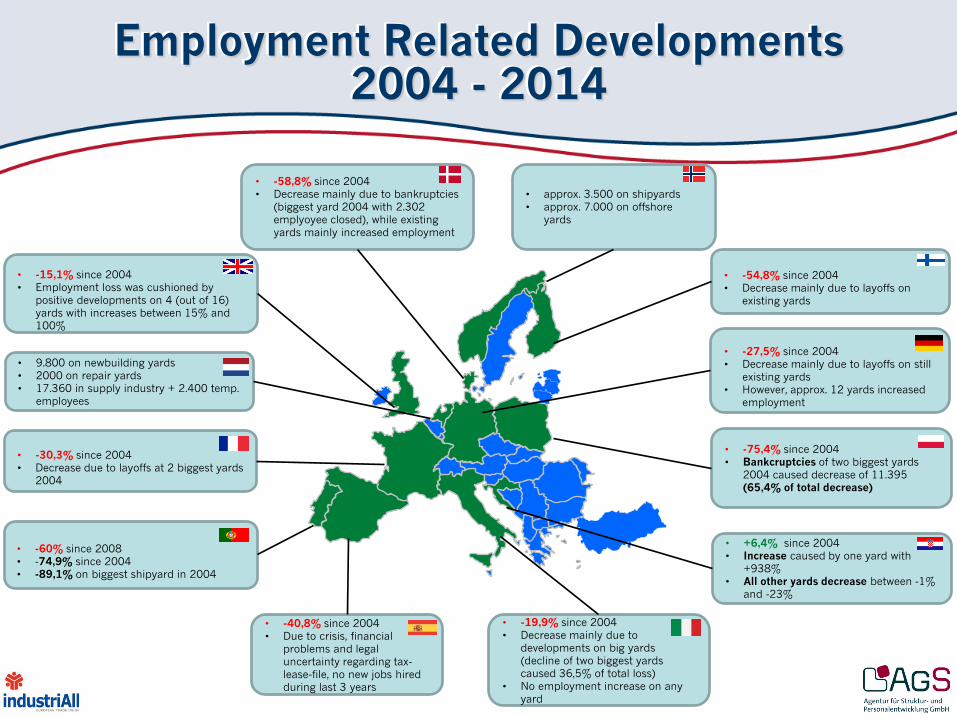

Employment Related Developments 2004 - 2014

• 9.800 on newbuilding yards • 2000 on repair yards • 17.360 in supply industry + 2.400 temp.

employees

• -30,3% since 2004 • Decrease due to layoffs at 2 biggest yards

2004

• -60% since 2008 • -74,9% since 2004 • -89,1% on biggest shipyard in 2004

• -40,8% since 2004 • Due to crisis, financial

problems and legal uncertainty regarding tax-lease-file, no new jobs hired during last 3 years

• -19,9% since 2004 • Decrease mainly due to

developments on big yards (decline of two biggest yards caused 36,5% of total loss)

• No employment increase on any yard

• +6,4% since 2004 • Increase caused by one yard with

+938% • All other yards decrease between -1%

and -23%

• -75,4% since 2004 • Bankcruptcies of two biggest yards

2004 caused decrease of 11.395 (65,4% of total decrease)

• -27,5% since 2004 • Decrease mainly due to layoffs on still

existing yards • However, approx. 12 yards increased

employment

• -54,8% since 2004 • Decrease mainly due to layoffs on

existing yards

• approx. 3.500 on shipyards • approx. 7.000 on offshore

yards

• -58,8% since 2004 • Decrease mainly due to bankruptcies

(biggest yard 2004 with 2.302 emplyoyee closed), while existing yards mainly increased employment

• -15,1% since 2004 • Employment loss was cushioned by

positive developments on 4 (out of 16) yards with increases between 15% and 100%

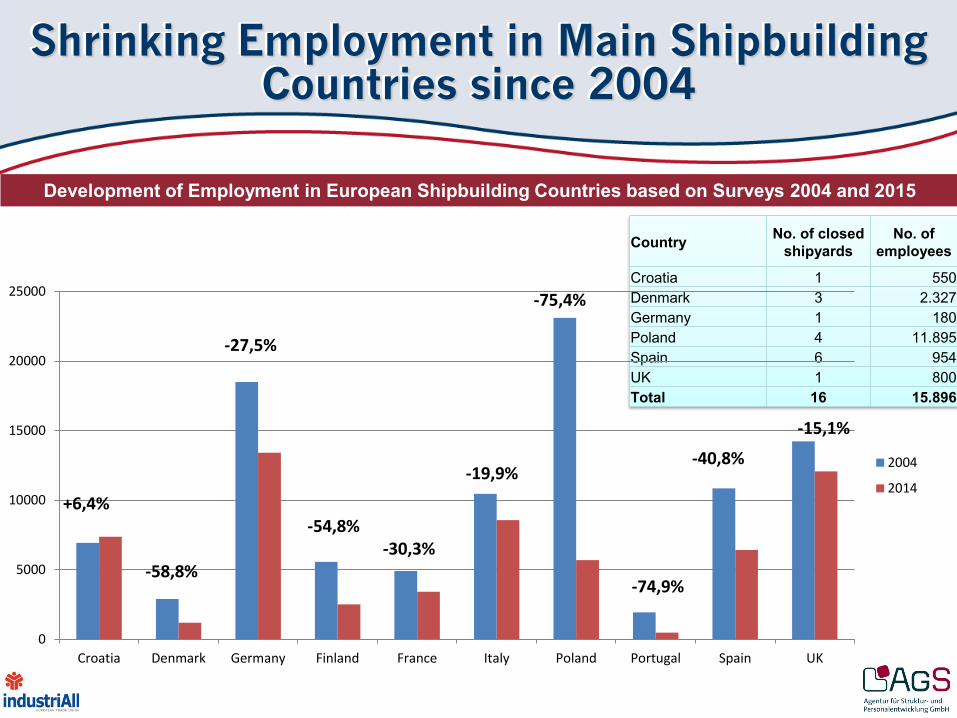

Shrinking Employment in Main Shipbuilding Countries since 2004

Development of Employment in European Shipbuilding Countries based on Surveys 2004 and 2015

Country No. of closed shipyards

No. of employees

Croatia 1 550 Denmark 3 2.327 Germany 1 180 Poland 4 11.895 Spain 6 954 UK 1 800 Total 16 15.896

0

5000

10000

15000

20000

25000

Croatia Denmark Germany Finland France Italy Poland Portugal Spain UK

2004

2014+6,4%

-58,8%

-27,5%

-54,8% -30,3%

-19,9%

-75,4%

-74,9%

-40,8%

-15,1%

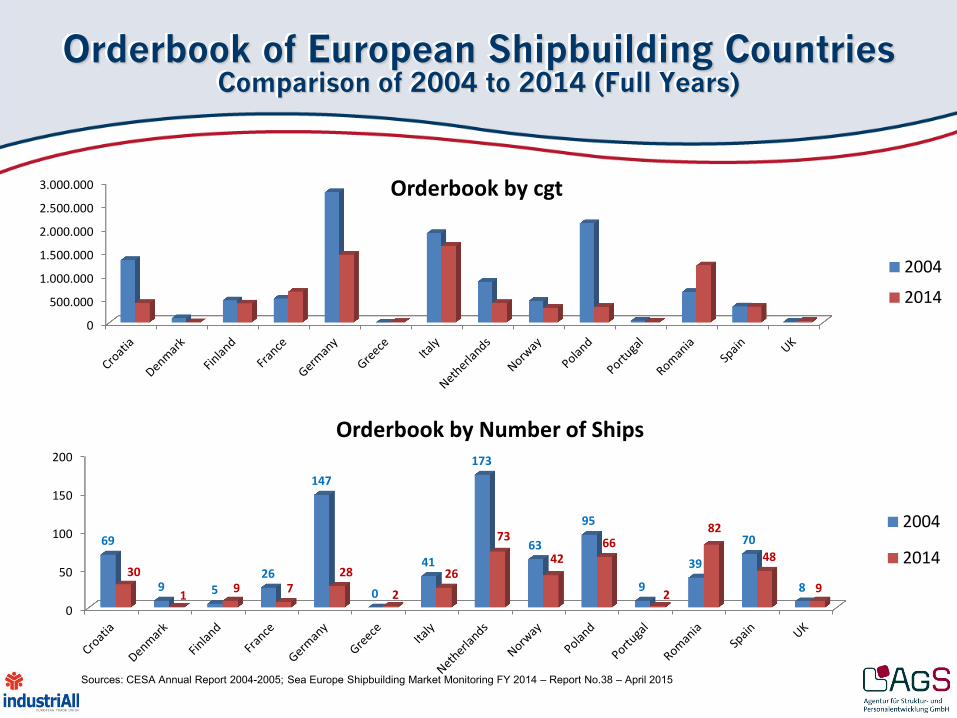

Orderbook of European Shipbuilding Countries Comparison of 2004 to 2014 (Full Years)

0

500.000

1.000.000

1.500.000

2.000.000

2.500.000

3.000.000 Orderbook by cgt

2004

2014

0

50

100

150

200

69

9 5 26

147

0

41

173

63

95

9

39

70

8 30

1 9 7 28

2

26

73

42 66

2

82

48

9

Orderbook by Number of Ships

2004

2014

Sources: CESA Annual Report 2004-2005; Sea Europe Shipbuilding Market Monitoring FY 2014 – Report No.38 – April 2015

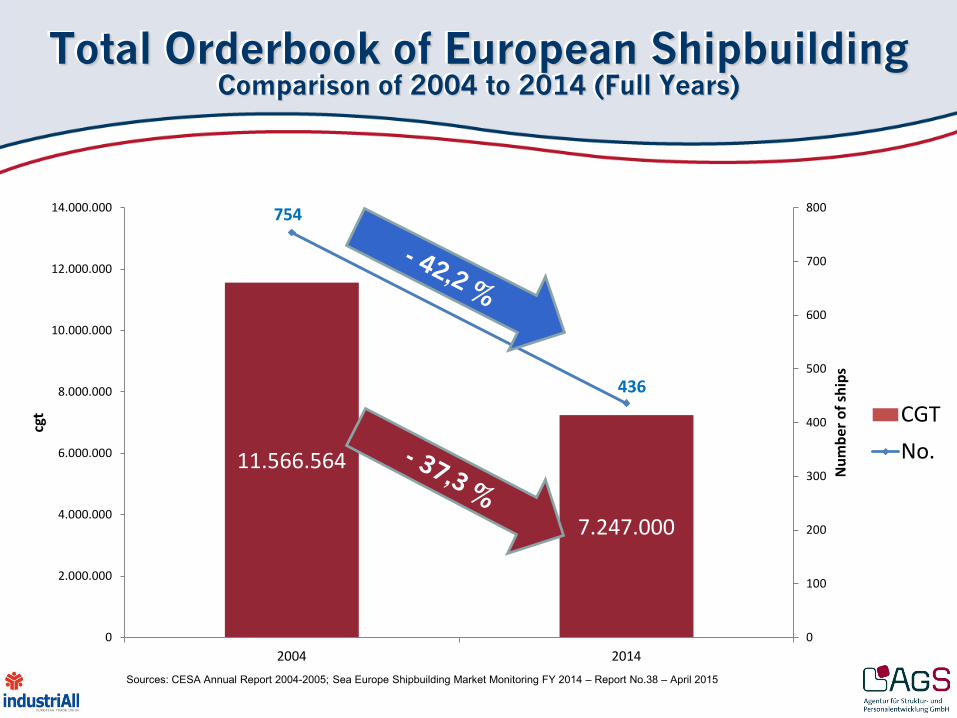

Total Orderbook of European Shipbuilding Comparison of 2004 to 2014 (Full Years)

11.566.564

7.247.000

754

436

0

100

200

300

400

500

600

700

800

0

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

2004 2014

Num

ber o

f shi

ps

cgt CGT

No.

Sources: CESA Annual Report 2004-2005; Sea Europe Shipbuilding Market Monitoring FY 2014 – Report No.38 – April 2015

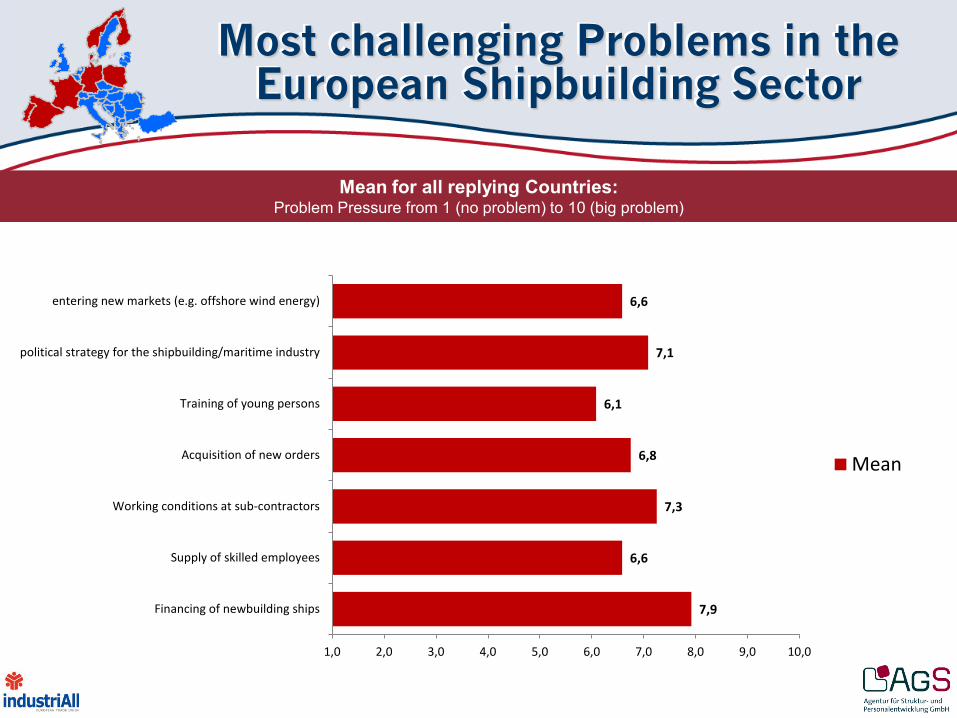

Most challenging Problems in the European Shipbuilding Sector

Mean for all replying Countries: Problem Pressure from 1 (no problem) to 10 (big problem)

7,9

6,6

7,3

6,8

6,1

7,1

6,6

1,0 2,0 3,0 4,0 5,0 6,0 7,0 8,0 9,0 10,0

Financing of newbuilding ships

Supply of skilled employees

Working conditions at sub-contractors

Acquisition of new orders

Training of young persons

political strategy for the shipbuilding/maritime industry

entering new markets (e.g. offshore wind energy)

Mean

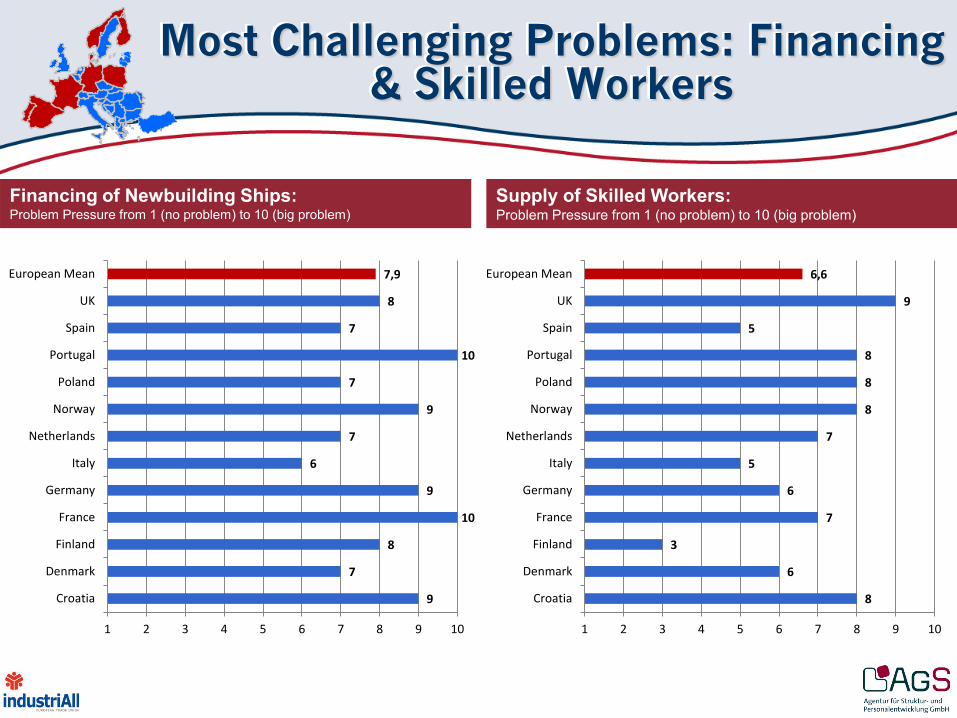

Most Challenging Problems: Financing & Skilled Workers

Financing of Newbuilding Ships: Problem Pressure from 1 (no problem) to 10 (big problem)

Supply of Skilled Workers: Problem Pressure from 1 (no problem) to 10 (big problem)

9

7

8

10

9

6

7

9

7

10

7

8

7,9

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

8

6

3

7

6

5

7

8

8

8

5

9

6,6

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

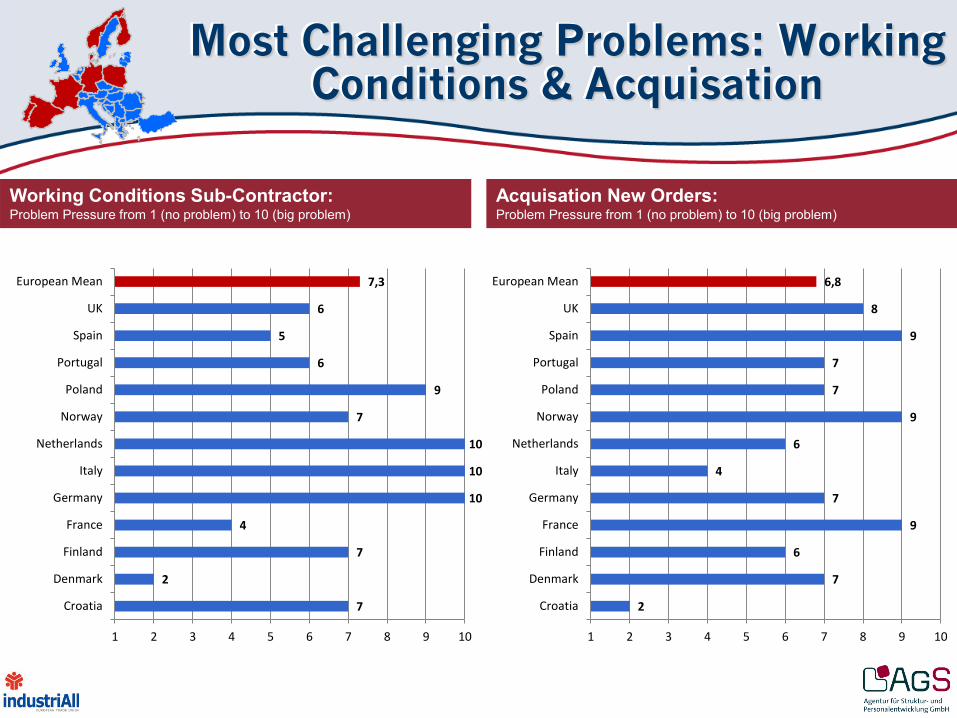

Most Challenging Problems: Working Conditions & Acquisation

Working Conditions Sub-Contractor: Problem Pressure from 1 (no problem) to 10 (big problem)

Acquisation New Orders: Problem Pressure from 1 (no problem) to 10 (big problem)

7

2

7

4

10

10

10

7

9

6

5

6

7,3

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

2

7

6

9

7

4

6

9

7

7

9

8

6,8

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

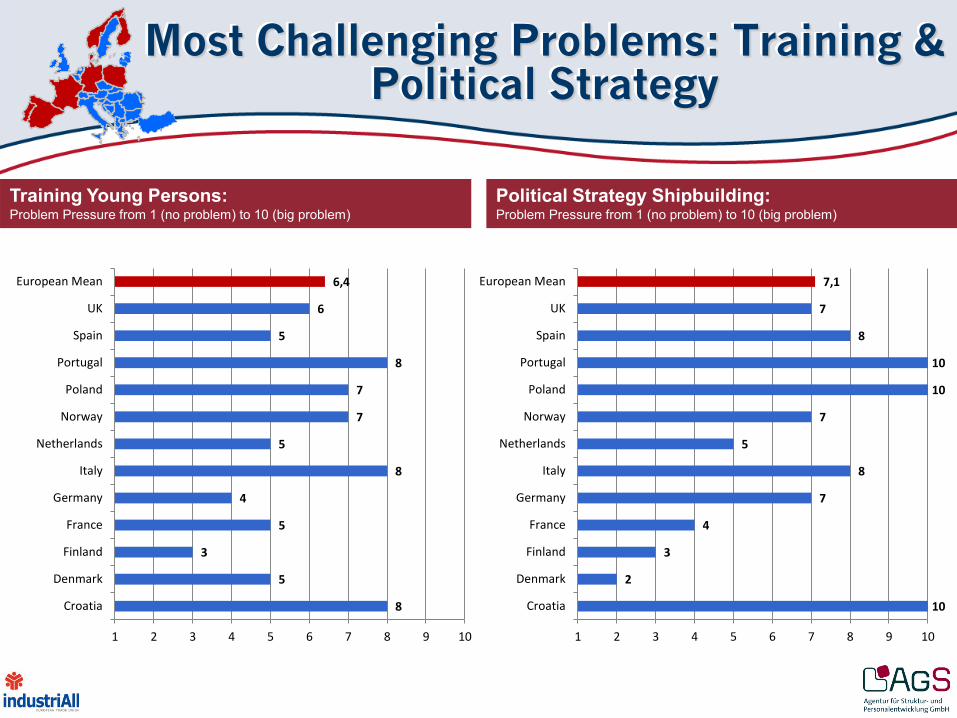

Most Challenging Problems: Training & Political Strategy

Training Young Persons: Problem Pressure from 1 (no problem) to 10 (big problem)

Political Strategy Shipbuilding: Problem Pressure from 1 (no problem) to 10 (big problem)

8

5

3

5

4

8

5

7

7

8

5

6

6,4

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

10

2

3

4

7

8

5

7

10

10

8

7

7,1

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

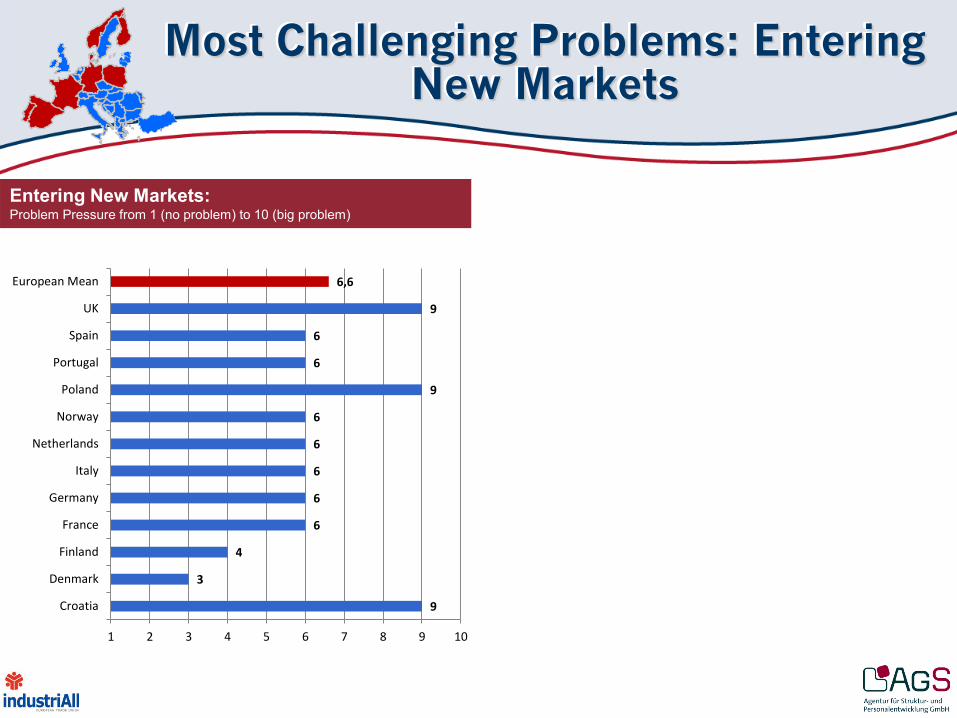

Most Challenging Problems: Entering New Markets

Entering New Markets: Problem Pressure from 1 (no problem) to 10 (big problem)

9

3

4

6

6

6

6

6

9

6

6

9

6,6

1 2 3 4 5 6 7 8 9 10

Croatia

Denmark

Finland

France

Germany

Italy

Netherlands

Norway

Poland

Portugal

Spain

UK

European Mean

European Shipbuilding Survey 2015: Main Results I

• Decrease in employment in almost all main European shipbuilding countries (except Croatia).

• Employment loss most severe in Poland and Portugal.

• Decline in employment is not concentrated on particular regions.

• In six countries closure of shipyards could be observed resulting in a loss of 15.896 jobs in total.

• Europe‘s role on the world shipbuilding market diminished since 2004 with China gaining momentum.

• Diversifying trends can be observed in most countries.

European Shipbuilding Survey 2015: Main Results II

• The problem pressure (from trade unionists‘ point of view) differs considerably between the countries which participated in the survey.

• In the two countries with most extreme decline in employment, the lack of a political strategy for the shipbuilding sector is regarded most challenging.

• In more traditional countries like Italy, the Netherlands and Germany, working conditions at subcontractors appears to be a major challenge for the shipbuilding sector.

• All participants indicated a relatively high problem pressure for financing new ships.