the capital market in malaysia - regional...

TRANSCRIPT

The Capital Market in Malaysia

Yutaka Shimomoto

Yutaka Shimomoto is Economist, Asian Development Bank and Chief Economist, Nikko Securities Co., Ltd. (1997–1999)

80 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

IntroductionThe capital market in Malaysia has undergone a ro-bust development since the late 1980s. The delistingof Malaysian and Singaporean companies from theirrespective stock exchanges at the end of 1989 wasa milestone in the development of Malaysia’s equitymarket. With the proliferation of privatization projectsand the equity boom in 1993, market capitalizationexceeded that of Singapore by the mid-1990s, mak-ing the Malaysian market one of the fastest growingin the region.

The equity market has contributed to the develop-ment of the private sector, with initial public offer-ings (IPOs) and issuances of new shares enablingmany companies to obtain cheap financing. Equityinvestments by individual, institutional, and foreigninvestors increased substantially, and market infra-structure was developed accordingly. Computerizedtrading, electronic clearing and settlement, and cen-tral depository systems were in place by the end of1997. The regulators, the Kuala Lumpur Stock Ex-change (KLSE) and Securities Commission (SC),have been improving standards on transparency, dis-closure, accounting, and corporate governance. Butthese standards still fall short of international stan-dards, as was revealed, for instance, by the Renong-United Engineers (Malaysia) (UEM) case in Novem-ber 1997, resulting in a loss of market confidence.

Meanwhile, various steps were taken in the late1980s to develop the bond market. Initially, effortswere focused on Government and Cagamas bonds.The central bank, Bank Negara Malaysia (BNM),played an important role in introducing the principaldealer and auction systems to develop the second-ary market for these bonds. However, BNM’s at-tempts were only partially successful. The statutoryrequirements for holding Government and Cagamasbonds have impeded market development. Moreover,the lack of benchmark yield curve and the issue ofriba (interest) had serious implications for bond mar-ket development. The latter was addressed in the

mid-1990s when new debt instruments based on Is-lamic principles were issued.

Since 1995, the Government has encouraged pri-vate and public entities to issue bonds to raise funds,while BNM has tried to develop market infrastruc-ture to support bond issues. During the financial cri-sis, some bonds issued by the private sector defaulted,hurting confidence in the market. As the financialcrisis deepened, many listed companies and stock-brokers became distressed and some private debtsecurities defaulted. Thus the capital market in Ma-laysia is facing serious challenges. The Governmentintroduced measures to curb speculation on foreigncurrency and to restrict the trading of Malaysianequities within KLSE on 1 September 1998, causingtemporary adverse effects on the capital market. Inorder to restore foreign investors’ market confidence,these measures need to be lifted.

OverviewCapital Market DevelopmentAs Singapore was once part of Malaysia, compa-nies in these two countries listed on both KLSE andthe Stock Exchange of Singapore (SES) until the endof 1989. Since then, KLSE has taken various mea-sures, including the introduction of computerized trad-ing, a central depository, and efficient clearing andsettlement systems, to develop market infrastructure.In addition, the regulatory framework has been re-viewed to promote IPOs and equity investments bydomestic and foreign investors. As a result, somebig privatized companies (e.g., Telekom MalaysiaBerhad and Tenaga Nasioni Berhad [TNB]) werelisted on KLSE, making it one of the fastest-growingmarkets in the region in the mid-1990s.

By the end of the 1980s, the primary market forGovernment bonds was relatively developed. TheGovernment introduced the principal dealer systemto develop the secondary market as well, and at thesame time, an auction system for Government secu-rities to promote fair pricing. Although the private

81THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

debt securities (PDS) market had deepened whenthe first Cagamas bonds were issued in October 1987,it did not develop until the mid-1990s. The Govern-ment has introduced various measures to enhancemarket infrastructure and put in place an appropri-ate regulatory framework. These included the es-tablishment of a credit rating agency (1990), guide-lines on PDS issues (1992), tax exemption on inter-est income from PDS (1993), scripless trading forunlisted PDS (1996), an auction system for the PDSprimary market (1996), and a bond information anddissemination system (1997). Despite Governmentefforts, a lack of benchmark yield curve hinders thedevelopment of the bond market.

Financial Crisis and the CapitalMarketThe financial crisis in Malaysia has predominantlyaffected the banking sector. At the end of 1997, bank-ing sector assets accounted for RM480 billion or 1.8times the gross national product (GNP). These fig-ures indicate that a substantial amount of funds hadbeen mobilized and provided to the private sector asloans. However, given the implicit control of BNM,external debts in the private sector are relatively small.The banking crisis was more a result of overlending,coupled with the lack of prudential regulation andsupervision.

The capital market, in particular the equity mar-ket, played an indirect role in increasing the numberof bank loans. Banks actively raised funds in theequity market, which expanded their capital base.With the development of the capital market and capi-tal account liberalization, disintermediation emergedto some extent. However, the role of bond and off-shore markets was not so significant except for bondswith warrants issued during the equity boom in themid-1990s.

Corporate entities, at the same time, activelytapped funds in the equity market, resorting to IPOsand new issues of shares for easy financing duringthe equity boom that began in 1992. Some corporate

players, in particular, obtained funds from the capitalmarket and banks to optimize their financial assets.They were successful in building up corporate em-pires while the boom lasted. However, when it wasover, they had to settle large debts from the bankingsector and bond market. With the bankruptcy of thesecorporate players, nonperforming loans (NPLs) ofcertain banks mounted.

Loans for share purchase contributed to an in-crease in banks’ NPLs. In addition, stockbrokers hadbeen providing their customers with credit facilitiesfor share trading. However, when share prices col-lapsed in the wake of the financial crisis starting inJuly 1997, banking institutions and stockbrokers in-curred losses resulting from loan defaults of custom-ers, in particular. The capital base of stockbrokerswas not sufficient to cope with the big losses. As aresult, some stockbrokers became distressed andwere suspended by KLSE.

Capital Market ProspectsThe market infrastructure for the equity market mightbe developed, but transparency, disclosure, and cor-porate governance need to be improved. In particu-lar, speedy and frequent disclosure of appropriateinformation is essential. In addition, the details of assetvalue and off-balance-sheet items should also be dis-closed. BNM has introduced a quarterly disclosurestandard for banks, for example, on profit and lossaccounts, and NPLs. Disclosure of the balance sheetis also necessary.

Since disclosure practices and corporate gover-nance do not conform to international standards, le-gal enforcement needs improvement. Most inves-tors are focused on short-term placements, makingit difficult to enhance corporate governance. Thepublic has to be encouraged to make long-term in-vestments. An increase in dividend payments couldbe considered. Dividends are subject to withholdingtax while interest income from long-term deposits,bonds, and capital gains from sale of shares aretax-exempt. Due to the withholding tax, companies,

82 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

particularly major shareholders, are reluctant to payhigh dividends. They prefer to use the profit forfurther expansion, which leads to an increase in assetvalues (capital gains). In addition, they tend to maxi-mize their returns by injecting their family assets intothe listed company. If they were exempted from thetax on dividends, companies would increase their pay-out ratios and investors would be encouraged to holdshares for longer periods. In this case, shareholdersmust pay more attention to the management of com-panies in order to receive better dividends. This could,in turn, improve corporate governance.

Before the crisis, funds required by the privatesector were readily available from commercial banks,the equity market, and offshore markets as a resultof the deregulation and liberalization of financial mar-kets during the decade. However, the financial envi-ronment changed after the crisis began. The privatesector experienced difficulties securing funds because(i) commercial banks faced liquidity problems,(ii) bearish equity market made it difficult for com-panies to float new shares, and (iii) offshore loansbecame costly due to currency depreciations. As theGovernment has also suffered tight budgetary con-straints, partly because of a decline in revenues fromtraditional sources, it is seriously considering the bondmarket as an alternative source of funds for the pri-vate and public sectors.

Equity MarketRevival of Foreign ExchangeControlA shock wave hit the equity market when BNM andKLSE announced curbs on foreign exchange andtrading of shares respectively on 1 September 1998(the US dollar was fixed at RM3.80 the next day)with immediate effect. The measures included:

• restricting the trading of Malaysian shares withinKLSE, and

• allowing foreigners to sell shares any time butproceeds could not be converted into foreign cur-

rency unless the shares had been held for at leastone year.

BNM’s exchange control measures were intro-duced primarily to regain monetary independence andinsulate the Malaysian economy from possible furtherdeterioration in the world economic and financial en-vironment. Meanwhile, KLSE’s measures were aimedat restoring confidence by ensuring an orderly andfair market, and improving overall transparency in thestock market. These promote greater accountabilityand disclosure without compromising investor confi-dentiality. The critical issue is how to exit from thesecontrol measures with minimum disruption.

With KLSE recognizing the trading of Malaysianshares in KLSE only, the Central Limit Order Book(CLOB), the over-the-counter market in Singaporewhere many Malaysian shares have been traded,was badly hit. CLOB ceased the trading of Malay-sian shares on 4 September 1998.

As Malaysia needs foreign capital, foreign inves-tors have an important role to play. Without a robustequity market, corporate entities have to rely on thebanking sector for financing, putting an additionalburden on a liquidity-tight sector. For this reason, theauthorities should review the measures and put inplace an environment that will attract local and for-eign investors to the equity market.

STOCKBROKERSDuring the market downturn in 1997-1998, it wasgenerally found that stockbroking firms with insuffi-cient capitalization, poor risk-management capabili-ties, and substantial counterparty exposures experi-enced more severe difficulties in managing the fall-out from the crisis.

Stockbrokers’ faulty internal management and riskcontrol was a leading factor in these incidents. Thelack of supervision by KLSE may have also contrib-uted to the problems. KLSE subsequently introduceda new single client and single security limit for mar-gin financing on 19 January 1998. The single clientlimit was set at 30 percent of the adjusted capital

83THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

while the single security limit was pegged at 20 per-cent of the adjusted capital or 10 percent of the paid-up capital of the listed company, whichever is lower.In addition, KLSE introduced a gearing ratio of twotimes against adjusted capital (1.5 times for utilizedborrowings). Stockbrokers were required to fullycomply with the ratios by the end of 1999. With thenew requirements, stockbrokers will be eventuallyforced to increase their capital bases, which are nowunder review by KLSE and SC.

KLSE sets the capital requirements and restric-tions for stockbrokers. They must have:

• paid-up capital of more than RM20 million;• minimum liquid assets of RM500,000 or 5 per-

cent of aggregate debt, whichever is larger; and• restrictions on single customer or single securi-

ties.Despite these requirements and restrictions, stock-

brokers still became distressed. Stockbrokers’ capi-tal should be increased to accommodate any futurelosses.

In addition, share-purchase financing became an-other source of problems. Stockbrokers had arrangedfor their customers to obtain credit facilities fromcommercial banks and finance companies. Share-purchase financing had been profitable for these fi-nancial institutions as well as stockbrokers. Hence,these financial institutions provided investors withcredit through stockbrokers, resulting in an increasein share-purchase financing. Although BNMannounced a ceiling on share-purchase financing on28 March 1997, it was too late to minimize the lossesof banks and finance companies.

BNM monitors share-purchase financing butKLSE should also review the margin trading ratiodepending on market conditions in order to betterregulate the market.

DISCLOSUREFrequency and timing of disclosure are urgent issuesto be addressed. The regulators, KLSE, SC, and theRegistrar of Companies (ROC), supervise and en-

force disclosure standards based on the SecuritiesIndustry Act, Companies Act, and rules and regula-tions set by KLSE and SC. There are three types ofdisclosure: initial, periodic, and continuous. KLSE isresponsible for day-to-day supervision and enforce-ment. An initial disclosure is required in the case ofIPOs, and the information that has to be disclosed ina prospectus is stipulated in the Companies Act. Whileinitial disclosure is deemed to conform to interna-tional standards, there are problems with periodic andcontinuous disclosures.

For periodic disclosure, listed companies are re-quired to disclose their profit and loss accounts twicea year and their balance sheets at the end of the fi-nancial year. Moreover, financial statements must bedisclosed within 90 days of the account book closing.

However, investors may not be able to get timelydetails of the financial condition of these companies.The urgency of providing timely information to in-vestors is illustrated by the case of Time EngineeringBhd (TEB), which was among the listed companiesannouncing financial results within the required pe-riod, only to be suspended by KLSE for insolvency.

The present disclosure standards were decided inthe days before the widespread use of computers.Current technology allows companies to discern theirfinancial positions more promptly. Regulators shouldrequire listed companies to report their unaudited fi-nancial records (profit and loss account and balancesheet) quarterly and within a month of the accountbeing closed, rather than within 90 days.

The TEB case also indicates that there are someproblems on continuous disclosure. When the unau-dited financial statement of TEB was disclosed inmid-March 1998, the company did not reveal anyspecific problems. However, by July, TEB was in-solvent, indicating a drastic deterioration of financialposition in the interim. In Chapter 6 of the SC Guide-lines, the requirement for timely disclosure of infor-mation is clearly stipulated. Under this rule, TEBshould have disclosed negative information within therequired period.

84 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

KLSE, ROC, and SC have been improving ac-counting, auditing, financial reporting, and disclosurestandards. For instance, KLSE has introduced awatch list of companies.

1 These measures will help

investors obtain better information for their invest-ment decisions compared with a few years ago.

Meanwhile, BNM requires banks to disclose theirprofit and loss accounts and NPL ratio on a quar-terly basis. This will also help improve disclosurestandards. However, banks are not required to pub-lish their balance sheets quarterly. Off-balance-sheetitems are increasing, as the banking business becomesmore sophisticated. Similarly, asset value of securi-ties, asset-liability mismatches, credit risk, and liquidityrisk are not adequately disclosed. Investors need suchcritical information. Otherwise, they get a clear pic-ture of a bank’s financial condition only at the end ofthe financial year.

Corporate GovernanceWith disclosure practices not conforming to interna-tional standards, legal enforcement not adequately inplace, and most investors focused on short-termplacements, it is difficult to improve standards ofcorporate governance. A regulatory framework hasto be promptly put in place, while the public shouldbe encouraged to make long-term investments toenhance corporate governance.

INSTITUTIONAL INVESTORSInstitutional investors (e.g., Permodaran NasionalBhd. [PNB] and Employees’ Provident Fund [EPF])can play vital roles in enhancing corporate gover-nance, which has become an increasingly impor-tant issue in Malaysia. PNB was established to in-crease Bumiputras’ (indigenous people) share-holdings (up to 30 percent by 1990). It owns sizablestakes in listed companies in various sectors: bank-ing, manufacturing, services, transport, construction,trading, mining, plantation, and conglomerates. EPFand other Government-related investment institu-

tions have also mobilized their funds to attain na-tional goals, i.e., they are expected to increaseBumiputras’ shareholding up to 30 percent. For thisreason, these institutional investors are basicallylong-term investors.

Dividends are small and capital gains through thedisposal of shares are not expected, given the pas-sive investment policy. Nonetheless, PNB and otherpublic investment entities such as EPF have beenaggressively investing in equities. Despite a relativelylow return on investment (ROI) (EPF’s dividendsfell to 6.7 percent in 1997 from 7.7 percent in 1996),these institutional investors have not come under firefrom the public. Part of the reason is the book value/cost accounting system. However, the goal to in-crease Bumiputras’ shareholding up to 30 percentdiscourages them from selling shares in the market.As such, these institutional investors can exercisetheir rights to increase either or both dividends andthe asset values of the invested companies by im-proving corporate governance. Nevertheless, if theaccounting method were switched to the marked-to-market system, the investment behavior of PNB orEPF would have to change.

INDIVIDUAL INVESTORSMany listed companies are owned by one shareholderor a family group (referred to here as “ownergroup”). In contrast to the spirit of corporate gover-nance, these owner groups insist on exercising theirrights of share ownership, believing that they are le-gally entitled to control the company. This is a con-cept generally accepted by even small shareholders.Corporate governance poses a challenge to this con-cept. For instance, sales of overvalued properties andcompanies to the listed companies controlled by theowner groups take place occasionally. This is partlydue to the passiveness of individual investors whohold shares for a short period (they seldom attendgeneral meetings), and expectations that the dealswill contribute to increases in share prices.

85THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

Many individual investors in Malaysia regard theequity market as a kind of casino, in which the publicacts as speculative and short-term investors. Sincethe onset of the equity boom in late 1992, many in-vestors have expressed their investment performancein terms of “win” or “lose.” This suggests that thepublic is concerned only with capital gains. It alsoindicates that many investors do not consider whethera company is financially sound or not. As long asshare prices are increasing, they do not care abouttransparency or corporate governance, even wel-coming “rumor-driven” speculative price movements.

The public generally stays clear of foreign-ownedcompanies, which tend to have conservative man-agement styles, and pay relatively high dividends.Individual investors are attracted by shares that carrythe expectation of sharp price hikes.

Given the public’s reluctance to demand or exer-cise their rights over their shares, an effective wayof improving corporate governance should be identi-fied. The distressed market sent a serious messageto the securities industries, bankers, regulators, andGovernment officials, who are considering how toregain market confidence. They are particularly con-cerned with foreign investors as their investmentsattract local investors to the market. For this reason,regulators are ready to take serious measures to en-hance corporate governance.

MAJORITY SHAREHOLDERSA listed company is a precious asset for an ownergroup, which will try to maximize profits from the firmthrough every possible means, causing conflict of in-terest between majority and minority shareholders.

Compensation for directors and executives inMalaysia is relatively low. Since dividends are sub-ject to tax, the owner group will want to maximizebenefits in other ways. Therefore, the provision oftax deductible nonpecuniary benefits (e.g., car, house,or travel) is not unusual in Malaysia and they areconsidered as equitable returns from investment in alisted company.

Owner groups also turn to other means to maxi-mize their profits, tending to sell products or servicesof the listed company to a connected company atbelow market price, or the listed company buys prod-ucts, services, or assets of a connected company atabove market price. During the equity boom of themid-1990s, there were many cases in which an ownergroup bought a listed company and sold connectedcompanies to the listed company in the form of shareswap. This practice provides the owner group withvarious profits, as follows:

• in addition to the sale of their assets at abovemarket price, the owner group is able to convertilliquid assets to liquid assets;

• it can use the shares of the listed company ascollateral and invest the borrowed money in otherbusinesses; and

• it can obtain more business opportunities fromthe listed company.

Such related party transactions are restricted bylaw; however, it is difficult to curb these practiceswithin the present legal framework. If new incen-tives for the owner group were devised, such as taxexemption on dividends and a reduction in incometax on directors’ fees, these issues would be ad-dressed to some extent.

Legal FrameworkRENONG-UEM DEAL AND THE WEAKNESSESOF THE LEGAL FRAMEWORKCorporate governance, transparency, and disclosurestandards will improve if an adequate regulatoryframework (legislation, supervision, market surveil-lance, law enforcement, and penalties) is put in place.Regulators must have a legal base on which to put inplace a robust market framework. The need for abetter regulatory environment is illustrated by theRenong-UEM deal.

UEM bought a 32.6 percent stake in cash-strappedRenong Bhd. for RM3.24 billion in November 1997.Some of the issues that emerged from the deal in-cluded the following:

86 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

• UEM was given a waiver from making a gen-eral offer and purchased Renong’s stakes fromrelated parties; and

• UEM’s financial soundness will deteriorate asthe acquisition of Renong stakes was made atabove market price using borrowed money.

Fund managers and analysts were unhappy withthe deal, while investors expressed their disillusionand lack of confidence in the market.

Several issues concerning legal framework andcorporate governance arose from the Renong-UEMcase. According to the Companies Act, shareholderapproval is not required for cash transactions. Offi-cial approval for mergers and acquisitions and take-overs basically comes from SC. But in the case ofan acquisition paid for in cash, SC approval is notrequired, unless enforced by other regulatory authori-ties such as the Foreign Investment Committee (FIC)(SC guideline 17.05; Acquisitions by Cash). FIC hasthe power to waive a general offer in the nationalinterest. It used this power to approve the Renong-UEM deal, although it is questionable whether it wasall in the national interest.

Despite serious losses to the investors, theRenong-UEM deal was deemed legal by regulators.No directors or executives were charged by the au-thorities. UEM was fined only RM100,000 by KLSEfor a breach of disclosure requirements. If directorsand executives responsible for negligence or crimi-nal acts faced stiffer penalties, they might try harderto comply with the rules and regulations.

INSTITUTIONAL INVESTORS ANDUNLISTED BANKSAs EPF, PNB, and other Government-controlled in-stitutional investors are allowed to adopt the bookvalue/cost accounting system, their asset portfoliosdo not reflect market value. Thus, it is important touse instead the marked-to-market accounting sys-tem, and present a real picture of their performanceto the public. Institutional investors should reviewtheir investment policies to improve return on in-

vestment (ROI) by taking a more active governancerole.

The Ministry of Finance, Inc. (MOFI) andKhazanah Holdings Bhd. (Khazanah) were estab-lished by the Government as private entities to investin strategic projects such as infrastructure, publicutilities, and industrial projects (Telekom, Tenaga,Proton, etc.). Their investment policy of passive port-folio management is similar to those of EPF and PNB.Detailed information on MOFI and Khazanah arenot disclosed to the public. Since these entities’ ma-jor shareholder is the public, and their sources of fundsbelong to the taxpayers, full disclosure of their finan-cial statements would improve transparency and dis-closure standards.

As the financial crisis deepened, large NPLs ofunlisted commercial banks (e.g., Bank Bumiputra andSime Bank) have emerged. Although BNM sets vari-ous requirements to ensure the soundness of banks,unlisted commercial banks are not subject to require-ments set by SC and KLSE, resulting in their low de-gree of transparency, disclosure, and corporate gov-ernance standards. Such standards need to be im-proved because these banks retain sizable financialassets and provide listed companies with a substantialamount of loans and guarantees. Any difficulties willhave adverse impact on listed companies.

Recommended MeasuresFOREIGN EXCHANGE CONTROL ANDRESTRICTIONS ON FOREIGN INVESTORSAlthough capital control measures implemented byBNM were aimed to restore order in the economyand stockmarket, investors’ disappointment, in par-ticular that of foreign investors, resulted in panic sell-ing. The measures taken by KLSE to disallow trad-ing of Malaysian shares on CLOB in Singaporeproved a big blow to foreign investors. Although theMalaysian authorities had never officially sanctionedthe trading of Malaysian shares on CLOB, it hadhelped attract foreign investors to Malaysian shares.If the Malaysian authorities were unhappy with

87THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

CLOB, they could have taken the same restrictivemeasures long ago.

The Government and KLSE must urgently takenecessary measures to attract foreign investors to themarket. First, restrictions on foreign exchange for port-folio investments should be lifted as soon as possible.Foreign investors had believed that the Malaysianmarket was undervalued. In fact, they had been care-fully planning to invest in the market once macroeco-nomic and political situations improved. Second, theCLOB issue should be solved urgently and amicably.Third, the Malaysian authorities should encourageMalaysian companies to be listed in overseas marketsas many Asian corporate companies had been pro-moting the idea of listing their shares on foreign mar-kets before the onset of the financial crisis.

STOCKBROKERSShare-purchase financing and margin trading financ-ing contributed to the banking crisis to some extent.The former is subject to the supervision of BNMand the latter is under SC regulation. Although bothregulators have tried to restore order, they have notbeen successful. KLSE has introduced measures toenhance prudential standards of stockbrokers. In turn,stockbrokers should improve their internal controlmeasures to avoid huge losses, particularly on mar-gin trading.

SC and KLSE should review the margin tradingratio depending on market conditions. As the StockExchange of Thailand had changed the margin ratiofrequently depending on market sentiment, KLSEshould follow suit.

LEGAL FRAMEWORKPriority has been given to sustaining share prices tostabilize the equity market. However, the authoritiesshould take long-term measures to promote a morerobust development of the market. As the Renong-UEM deal indicated, the lack of legal framework toenforce transparency, disclosure, and corporate gov-ernance has been challenged. It is important for regu-

lators to have a legal base from which to promote arobust market framework.

Investors want restoration of discipline in the mar-ket and the regulators should respond to this demandswiftly. In connection with this, FIC’s power shouldbe reviewed. FIC was established originally to as-sess the foreign investment from the viewpoint ofnational interest. But its power should be confined tomatters relating to foreign investments.

Moreover, an additional regulatory framework willbe required to enhance the transparency of Govern-ment-related institutional investors.

CORPORATE GOVERNANCEGiven that the disclosure practices and accountingsystems do not satisfy investors’ expectations, thelegal enforcement is not adequately in place, and mostinvestors are focused on short-term investments, itis difficult to improve the standard of corporate gov-ernance. A regulatory framework must be promptlyput in place. In addition, the general public should beencouraged to make long- term investments to en-hance corporate governance. Increasing the dividendpayments might be one answer.

As investors in many listed companies in such sec-tors as banking, manufacturing, services, transport,construction, trading, mining, plantation, and conglom-erates, public investment entities such as PNB, EPFand other government-related investment institutionsare basically long-term investors. With dividends pay-ments small and capital gains not expected, their roleis to increase Bumiputra’s shareholdings. This wasmade possible partly due to the book value/cost ac-counting system. If the accounting method werechanged to the market value (marked-to-market) sys-tem, the investment behavior of PNB or EPF wouldchange. These institutional investors could then ex-ercise their rights to increase either or both dividendsand the asset values of the companies. This wouldenable them to optimize the benefits to the public,while enhancing standards of transparency, disclo-sure, and corporate governance.

88 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

Bond MarketGovernment Bond Market

ISSUES RELATED TO MONETARY POLICY

Monetary PolicyOf the 10 monetary policy instruments,

2 the most

common in Malaysia are reserve requirement, liquidityrequirement, credit control and guidelines on lending,and direct lendings/borrowings. Although the liquid-ity requirement was set by BNM to maintain pru-dential standards in banking institutions, it functionsas a monetary instrument.

Reserve and liquidity requirements for commer-cial banks were set at 4 and 15 percent of eligibleliabilities, respectively.

3 However, the liquidity require-

ment was replaced with a new framework in Janu-ary 1999. The new liquidity framework requires com-mercial banks to maintain certain liquid assets basedon the maturity profile of their assets, liabilities, andoff-balance sheet commitments, and to make a pro-jection of their liquidity surplus and shortfall. Theassessment will be based upon the ability of a com-mercial bank to match its short-term liquidity require-ment, which will be determined by reckoning thematuring obligations and assets. It is envisaged thatthe new framework will lead to commercial banksoptimizing their asset management in the secondarymarket.

When a certain sector of the economy overheats,credit to that sector is controlled. BNM has usedshort-term direct borrowings, generally with maturi-ties of between one and three months, to sterilizelarge capital inflows since late 1991. In some cases,however, the maturity has been lengthened to sixmonths. Since February 1993, BNM has also issuedBank Negara bills (BNBs) to mop up excess liquid-ity.

BNM’s use of direct instruments as primary in-struments for monetary regulation and indirect in-struments as supplementary instruments suggests thatthere are some impediments to the use of open mar-

ket operations in Malaysia as a tool of monetarypolicy. In fact, direct lending/borrowing has been amore effective monetary tool than open market op-erations. High reserve and liquidity requirement ra-tios and inefficient open market operations have hin-dered the development of the bond market.

In March 1998, BNM announced a new monetarypolicy with changes from direct instruments to indi-rect instruments (employing open market operationsand repurchase operations). With the policy changes,coupled with the deepening financial crisis, BNMreduced the reserve requirement from 13.5 to 4 per-cent (four times since February 1998) to supply li-quidity to the banking system. The liquidity require-ment ratio for commercial banks was also decreasedfrom 17 to 15 percent on 16 September. The reduc-tion in statutory requirements will help increase li-quidity in the banking system. Meanwhile, the bench-mark interest rate (three-month interbank rate) wascut to 8 percent to reduce the cost of funds. Thiswas made possible by fixing the foreign exchangerate at RM3.80 against $1 on 2 September.

Open Market OperationsOpen market operations are not often used as a

monetary tool in Malaysia due to underdevelopedsecondary market in Government bonds. The instru-ments used for open market operations are Treasurybills (T-bills), Malaysian Government securities(MGS), Government investment issues (GIIs), Ma-laysia Savings Bonds, BNBs, Cagamas papers,banker’s acceptance (BAs), negotiable certificatesof deposit, and Floating Rate Negotiable Certificatesof Deposit (FRNCDs). However, trading of Gov-ernment bonds has been limited, attributable to theissuance of bonds with low market yields.

4

To address this issue, a new issuing practice andother measures were introduced between 1986 and1989. With the introduction of the principal dealer on1 January 1989 involving selected commercial banks,merchant banks, and discount houses, open marketoperations began to take place between BNM and

89THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

securities to meet the liquidity requirement. The Gov-ernment, BNM, and Cagamas Bhd. issue other se-curities such as T-bills, BNBs, Malaysia SavingsBonds, Cagamas bonds, and other papers to meetthis demand.

While the liquidity requirement helps maintain pru-dence among banking institutions, it also increasesthe costs of funds to them. They receive depositsfrom customers and are required to invest a certainportion of money in the eligible securities to complywith the liquidity requirement. Due to the illiquid sec-ondary market, banking institutions usually hold thesecurities until maturity. Thus they are exposed tomaturity mismatch and interest risks, resulting in high-cost investments.

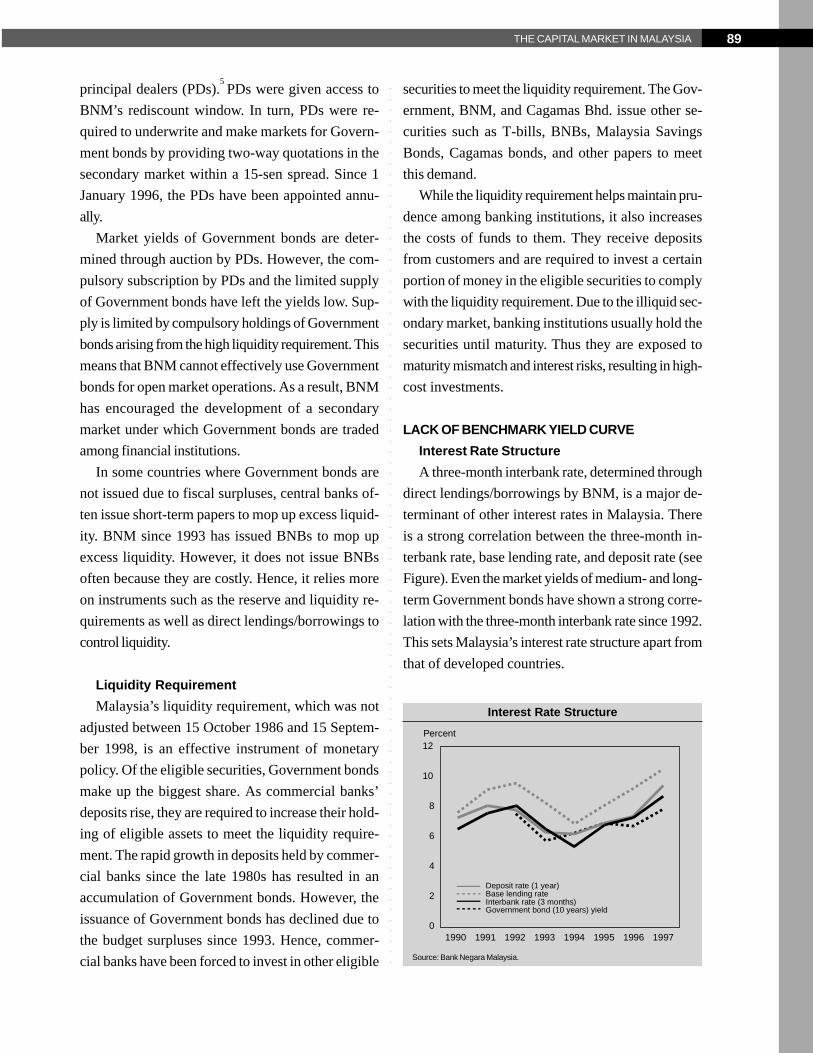

LACK OF BENCHMARK YIELD CURVEInterest Rate StructureA three-month interbank rate, determined through

direct lendings/borrowings by BNM, is a major de-terminant of other interest rates in Malaysia. Thereis a strong correlation between the three-month in-terbank rate, base lending rate, and deposit rate (seeFigure). Even the market yields of medium- and long-term Government bonds have shown a strong corre-lation with the three-month interbank rate since 1992.This sets Malaysia’s interest rate structure apart fromthat of developed countries.

principal dealers (PDs).5 PDs were given access to

BNM’s rediscount window. In turn, PDs were re-quired to underwrite and make markets for Govern-ment bonds by providing two-way quotations in thesecondary market within a 15-sen spread. Since 1January 1996, the PDs have been appointed annu-ally.

Market yields of Government bonds are deter-mined through auction by PDs. However, the com-pulsory subscription by PDs and the limited supplyof Government bonds have left the yields low. Sup-ply is limited by compulsory holdings of Governmentbonds arising from the high liquidity requirement. Thismeans that BNM cannot effectively use Governmentbonds for open market operations. As a result, BNMhas encouraged the development of a secondarymarket under which Government bonds are tradedamong financial institutions.

In some countries where Government bonds arenot issued due to fiscal surpluses, central banks of-ten issue short-term papers to mop up excess liquid-ity. BNM since 1993 has issued BNBs to mop upexcess liquidity. However, it does not issue BNBsoften because they are costly. Hence, it relies moreon instruments such as the reserve and liquidity re-quirements as well as direct lendings/borrowings tocontrol liquidity.

Liquidity RequirementMalaysia’s liquidity requirement, which was not

adjusted between 15 October 1986 and 15 Septem-ber 1998, is an effective instrument of monetarypolicy. Of the eligible securities, Government bondsmake up the biggest share. As commercial banks’deposits rise, they are required to increase their hold-ing of eligible assets to meet the liquidity require-ment. The rapid growth in deposits held by commer-cial banks since the late 1980s has resulted in anaccumulation of Government bonds. However, theissuance of Government bonds has declined due tothe budget surpluses since 1993. Hence, commer-cial banks have been forced to invest in other eligible

Interest Rate Structure

1990 1991 1992 1993 1994 1995 1996 19970

2

4

6

8

10

12

Deposit rate (1 year)Base lending rateInterbank rate (3 months)Government bond (10 years) yield

Percent

Source: Bank Negara Malaysia.

90 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

But the interest rate structure poses a problem tothe Government bond market. Despite the Govern-ment’s insistence that its bonds be issued at marketrates, the market yields clearly indicate the presenceof distortions in the interest rate structure. As com-mercial banks are required by BNM to hold a cer-tain amount of Government bonds that carry lowyields, they are paying the cost of the distortion. Thisis eventually passed on to their depositors and bor-rowers. If the Government takes appropriate mea-sures to correct the distortions, institutional inves-tors, who hold a large amount of the low-yield bonds,may also be forced to accept substantial losses. Arise in interest rates in 1989 left banking institutionswith large capital losses because of the low yieldbond requirement. To cope with the difficulties, BNMintroduced in April 1989 a new accounting systemfor the valuation of bonds. Commercial banks areallowed to book the value of Government bonds atcost, adjusted for amortization of premiums or ac-cretion of discount. They are permitted to amortizethe gains or losses over the maturity period. Althoughthe fundamental issue of the low yield Governmentbonds remained unresolved, this new accounting sys-tem gave an incentive for commercial banks to in-vest in the bonds.

Auction System for Government BondsAlong with the PD system, the Government intro-

duced an auction system in January 1989 to put apricing structure in place. Government bonds, withmaturity period of up to 10 years, are issued by auc-tion through PDs. In turn, financial institutions haveto purchase the securities through PDs. Governmentbonds with a maturity period exceeding 10 years aresubject to advance subscription by EPF and the Na-tional Savings Bank (NSB). The auction system andthe principal dealer system have, to a certain extent,contributed to the development of the Governmentbond market.

These systems worked well during the period ofstable interest rates, and trading of Government bonds

has gradually increased. But when interest rates rosebetween 1990 and 1992, the PD system did not serveits purpose. The auction system operated as if therewas fair pricing of Government bonds. In an auctionof Government bonds, PDs have the obligation tounderwrite the entire amount of primary issue. Asthere are 14 PDs, appointed in 1998, each PD isrequired to subscribe to a minimum of 10 percent ofthe entire issue (this means that the total biddingamount will be at least 140 percent of the amountissued). Therefore, undersubscription has not becomean issue. PDs submit the notation at the market interms of yields. The market yield is determined bythe weighted average yield of successful bids. Mean-while, the issuer reserves the right to accept or re-ject any or all the bids submitted by PDs. Thus, it isdifficult to obtain a fair market yield.

In addition, an underlying factor has distortedmarket yield. Liquidity requirements for banking in-stitutions and statutory requirements for EPF andNSB have created high demand for Governmentbonds. However, there have been fewer issuancesof bonds by the Government due to the fiscal sur-pluses since 1993. The high demand and short sup-ply have made the issuance of Government bondswith low market yields possible and prevented thecreation of a benchmark yield curve, which is impor-tant for the development of the overall bond market.This has been identified as an important issue and assuch, the liquidity requirement is being reviewed.

INACTIVE BOND TRADINGNarrow Investor BaseCommercial banks, finance companies, and mer-

chant banks have to comply with statutory require-ments and invest in eligible securities (mostly Gov-ernment and Cagamas bonds). The Government alsorequires EPF and NSB to hold a certain percentageof their funds in Government bonds. EPF has beenthe biggest subscriber to Government bonds, althoughits holdings have declined due to limited supply. Gov-ernment bonds’ share of the total funds managed

91THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

had fallen to 29.4 percent (RM38.1 billion) at theend of 1997.

In fact, when a new EPF Act was introduced inJune 1991, holdings of “eligible securities” were re-duced from 70 to 50 percent, “provided that the totalamount of funds invested in such securities at anyone time shall not be less than 70 percent of the Fund’stotal investments” (Section 26, EPF Act, 1991). Thisclause gave EPF a broader flexibility in portfoliomanagement. Eligible securities include loans that arefully guaranteed by the federal Government, BNMpapers with a maturity of at least three years fromthe date of issue, and any instrument issued by astate government or local authorities with a maturityof at least three years from the date of issue. Sincethen, EPF has diversified its portfolio and invested inother instruments, a policy change made due to itsincreasing funds. As the issuance of Governmentbonds declined due to fiscal surpluses, these institu-tions are confronted with a shortage of eligible secu-rities and as a result, have maintained a captive in-vestment policy on Government bonds and seldomtraded in the markets.

Ineffective Principal Dealer SystemA new principal dealer system, with an annual

review of the dealership, was introduced in January1996 to promote trading in the secondary market.However, the trading volume declined to RM12.4billion in 1997 from RM25.4 billion in 1996 while theamount outstanding fell to RM69.9 billion in 1997 fromRM72.2 billion in 1996. This was attributed to fewerGovernment bonds outstanding, and commercialbanks’ tendency to hold Government bonds untilmaturity. Inactive bond trading has made it difficultfor the PD system to develop a robust secondarymarket.

Through repurchase agreements with BNM, PDsare allowed to secure funds from BNM for a periodof less than one month. This is an attractive incen-tive. However, PDs cannot hedge the interest risksthrough a bond futures market, because it does not

exist in Malaysia. Similarly, PDs’ main sources offunds are short-term deposits, and the lack of a fu-tures market has contributed to increased interestrisks. As a result, PDs have been incorporating thecost of risks in their price quotations.

PDs are composed of commercial banks, mer-chant banks, and discount houses. Commercial andmerchant banks are subject to reserve and liquidityrequirements. These requirements push up the costsof funds, which result in higher price quotations. AsPDs are required to play the role of market makers,they are expected to accommodate any amount ofsale or purchase orders placed by customers. How-ever, since the prices offered by PDs are not attrac-tive to investors, bonds are seldom traded. High costsand risks associated with bond holdings are the majorreasons for the ineffectiveness of the PD system.

Lack of Borrowing, Short Selling, andFutures MarketThe lack of borrowing and short selling as well as

the absence of a futures market have hindered thedevelopment of the secondary market in Malaysia.If the framework of borrowing bonds is improved,investors can borrow bonds against the collateral ofcash for short selling.

Malaysia Monetary Exchange (MME) is planningto introduce bond futures to make the borrowing ofbonds an attractive investment option in Malaysia. Ifbond borrowing is institutionalized and short selling isencouraged, demand for bonds will increase. A well-developed futures market plays an important role forthe development of a secondary market.

Private Debt Securities MarketUNDERDEVELOPED PRIVATE DEBT SECURITIESMARKETThe types of private debt securities (PDS) issued inMalaysia are straight bonds, bonds with warrants(BWs), convertible bonds, Islamic bonds, andCagamas bonds. Cagamas bonds, BWs, and straightbonds were the most common PDS issued until 1993,

92 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

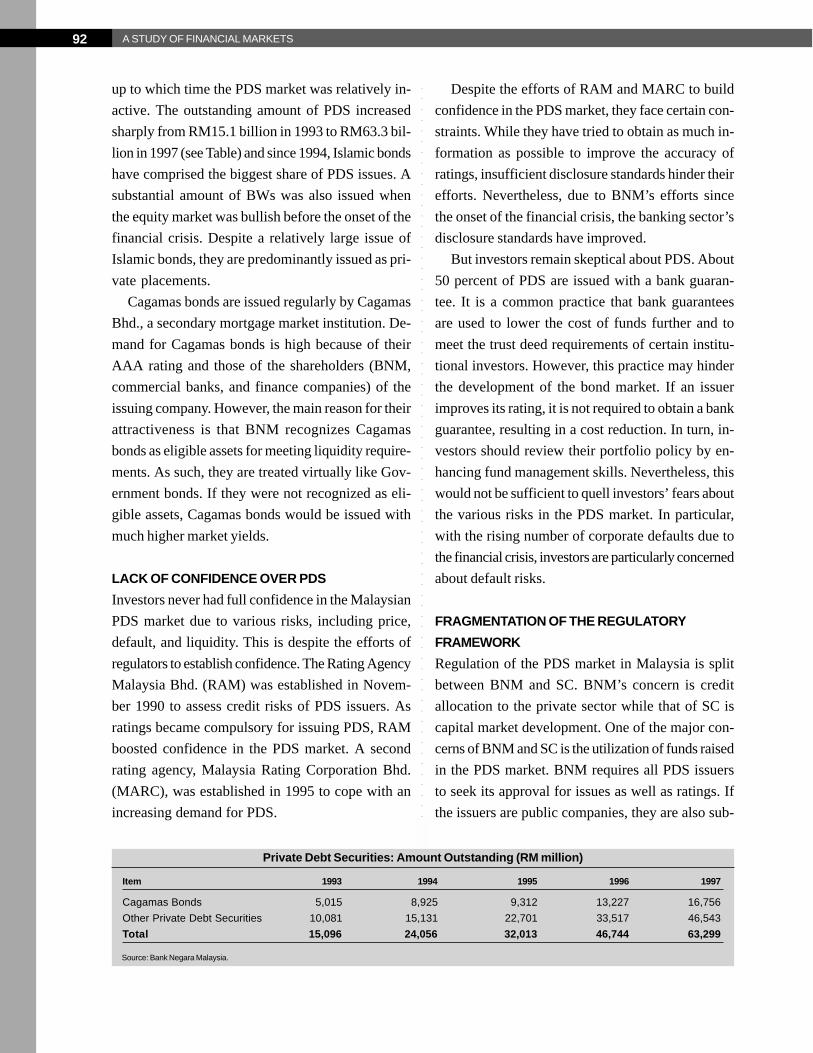

up to which time the PDS market was relatively in-active. The outstanding amount of PDS increasedsharply from RM15.1 billion in 1993 to RM63.3 bil-lion in 1997 (see Table) and since 1994, Islamic bondshave comprised the biggest share of PDS issues. Asubstantial amount of BWs was also issued whenthe equity market was bullish before the onset of thefinancial crisis. Despite a relatively large issue ofIslamic bonds, they are predominantly issued as pri-vate placements.

Cagamas bonds are issued regularly by CagamasBhd., a secondary mortgage market institution. De-mand for Cagamas bonds is high because of theirAAA rating and those of the shareholders (BNM,commercial banks, and finance companies) of theissuing company. However, the main reason for theirattractiveness is that BNM recognizes Cagamasbonds as eligible assets for meeting liquidity require-ments. As such, they are treated virtually like Gov-ernment bonds. If they were not recognized as eli-gible assets, Cagamas bonds would be issued withmuch higher market yields.

LACK OF CONFIDENCE OVER PDSInvestors never had full confidence in the MalaysianPDS market due to various risks, including price,default, and liquidity. This is despite the efforts ofregulators to establish confidence. The Rating AgencyMalaysia Bhd. (RAM) was established in Novem-ber 1990 to assess credit risks of PDS issuers. Asratings became compulsory for issuing PDS, RAMboosted confidence in the PDS market. A secondrating agency, Malaysia Rating Corporation Bhd.(MARC), was established in 1995 to cope with anincreasing demand for PDS.

Despite the efforts of RAM and MARC to buildconfidence in the PDS market, they face certain con-straints. While they have tried to obtain as much in-formation as possible to improve the accuracy ofratings, insufficient disclosure standards hinder theirefforts. Nevertheless, due to BNM’s efforts sincethe onset of the financial crisis, the banking sector’sdisclosure standards have improved.

But investors remain skeptical about PDS. About50 percent of PDS are issued with a bank guaran-tee. It is a common practice that bank guaranteesare used to lower the cost of funds further and tomeet the trust deed requirements of certain institu-tional investors. However, this practice may hinderthe development of the bond market. If an issuerimproves its rating, it is not required to obtain a bankguarantee, resulting in a cost reduction. In turn, in-vestors should review their portfolio policy by en-hancing fund management skills. Nevertheless, thiswould not be sufficient to quell investors’ fears aboutthe various risks in the PDS market. In particular,with the rising number of corporate defaults due tothe financial crisis, investors are particularly concernedabout default risks.

FRAGMENTATION OF THE REGULATORYFRAMEWORKRegulation of the PDS market in Malaysia is splitbetween BNM and SC. BNM’s concern is creditallocation to the private sector while that of SC iscapital market development. One of the major con-cerns of BNM and SC is the utilization of funds raisedin the PDS market. BNM requires all PDS issuersto seek its approval for issues as well as ratings. Ifthe issuers are public companies, they are also sub-

Private Debt Securities: Amount Outstanding (RM million)

Item 1993 1994 1995 1996 1997

Cagamas Bonds 5,015 8,925 9,312 13,227 16,756Other Private Debt Securities 10,081 15,131 22,701 33,517 46,543Total 15,096 24,056 32,013 46,744 63,299

Source: Bank Negara Malaysia.

93THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

ject to the approval of SC. As most of issuers arelisted (public) companies, they have to obtain approv-als from the two regulators.

A third force in the regulation of PDS issues isROC. Although BNM and SC have set guidelinesfor the PDS market, the details of PDS issues arestipulated in the Companies Act of 1965. In particu-lar, ROC requires issuers to register prospectusesunless PDS are either guaranteed by the federal Gov-ernment or issued in private placement. It also re-quires an issuer to provide certain information in theprospectus that complies with the requirements setby BNM and SC.

BNM set guidelines on the issuance of PDS inDecember 1988. The main requirements are:

• minimum shareholders’ funds for issuers set atRM25 million;

• disclosure of proceeds’ utilization and sourcesof repayment;

• minimum size of an issue set at RM25 million;• debt-equity ratio of issuers kept within pruden-

tial limits;• underwriting requirements; and• minimum rating of BBB for long-term papers

and P3 for short-term papers.In addition, approval should be obtained from the

Controller of Foreign Exchange if PDS are issuedon a bearer basis and by a nonresident (foreign) con-trolled company. Although the Banking Departmentof BNM acts as one-stop coordinating departmentand a separate application for approval from theController of Foreign Exchange is not required, thisrequirement has become a stumbling block in gettingswift approval.

Even if issuers comply with the requirements setby BNM and SC, they (except Cagamas Bhd.) arerequired to obtain approvals from the two bodies.The approval process usually takes a few months(sometimes up to six). This delay is an importantimpediment to issuers who may miss an opportunityto issue PDS at low cost and may have to seek fresh

ratings if there is a change in the financial environ-ment in the meantime.

BNM, SC, and the departments concerned haverecognized some of these problems and organizedinterdepartmental meetings twice a year on the de-velopment of the bond market.

NARROW INVESTOR BASESome investors were restricted from investing in PDSuntil June 1997, when the Minister of Domestic Tradeand Consumer Affairs made an order to lift the re-strictions stipulated in section 47B of the CompaniesAct of 1965. These restricted investors included fundmanagers, individuals, and corporate entities withincertain criteria, offshore banks, and offshore insur-ance companies. Nevertheless, some institutional in-vestors are still reluctant to invest in PDS. For in-stance, Pilgrims Fund was established to invest inequities because its unit holders are unwilling to re-ceive interest income. PNB invests in Islamic bondsbut will not diversify its portfolio.

The Government has reviewed its policy of re-quiring EPF to hold Government bonds. EPF isnow allowed to invest more funds in other securi-ties such as equities and PDS. In fact, EPF hasbeen providing private entities engaged in infra-structure projects with a large amount of funds inthe form of loans and PDS. However, EPF’s port-folio management has come under fire over its lowdividend rate of 6.7 percent in 1997 (one-year fixeddeposit rate was 9.3 percent at the end of 1997).Consequently, EPF has reviewed its fund manage-ment policy.

Both EPF and PNB have adopted an accountingsystem based on cost/book value. They have dividedtheir portfolio investments into two categories: short-term and long-term. Securities in the long-term cat-egory are recorded in book or cost value. However,the differences between the book/cost value andmarket value are adjusted (but not fully) in the in-vestment revaluation reserve item. This accounting

94 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

method does not reflect the clear financial positionsof these institutions. Subsequently, the institutionsmanage their funds without paying much attention toperformance. As these are public funds, they mayhave to reconsider their investment policies whenthe accounting system is reviewed. Despite beingexempted from paying stamp duty and income taxon interest earnings, individuals are not investing muchin the PDS market. Investment in PDS by unit trustshas not been actively promoted and this is also con-tributing to the low level of individual investments inthe PDS market.

MARKET INFRASTRUCTUREBNM has been trying to develop a market infrastruc-ture for PDS, improving the trading, clearing, settle-ment, and depository systems. To this end, BNM in-troduced SPEEDS (Sistem Pemindahan Elektronikuntuk Dana dan Sekuriti: the electronic funds andsecurities transfer settlement system) in the PDSmarket (unlisted bonds only) in January 1996.SPEEDS comprises two components: InterbankFund Transfer System (IFTS) and Scripless Securi-ties Trading System (SSTS). All new issues of un-listed long-term bonds are required to be made inscripless form and traded under SPEEDS to facili-tate the transfer of securities, payment of interest,and redemptions. In the near future, it is planned thatall unlisted PDS will be issued in scripless form.

With the introduction of the Fully Automated Sys-tem for Tendering (FAST) of PDS in 1997, all com-mercial papers (CPs), medium-term notes (MTNs)and Islamic CPs (including private placements),except long-term bonds, are issued through FAST.The system was introduced to provide a uniform setof procedures to govern the issuance and tenderingof PDS.

The Bond Information and Dissemination System(BIDS) was launched in October 1997. BIDS hasbeen providing information on primary and second-ary markets including information on all outstandingPDS, Government bonds, T-bills, and Cagamas pa-

pers. It helps to improve the liquidity and efficiencyof the markets.

While most of PDS trading takes place in over-the-counter markets, Cagamas bonds, like all Gov-ernment bonds, are traded in SPEEDS. As the Ma-laysian Institute of Bond Dealers was incorporatedin 1996, a trading facility similar to the Thai BondDealing Center could be introduced when BIDS isfully installed. BNM should speed up the remainingwork of market infrastructure development to facili-tate PDS trading.

UNDERWRITERSMerchant banks generally carry out underwriting ofPDS, although some discount houses are also allowedto underwrite. They were required to earn at least30 percent of their income from fee-based businessactivities until the end of 1996. In the mid-1990s, theypreferred to underwrite equities rather than PDS dueto the equity boom and the limited demand for PDSby institutional investors.

With the increasing variety of PDS, merchantbanks now have more business opportunities to un-derwrite them, especially as Islamic bonds are ac-ceptable to a wide variety of institutional investors.However, merchant banks have relatively small capi-tal bases, such that an unsuccessful underwriting couldendanger their position. This is a disincentive for themand other underwriters to actively participate in un-derwriting and market making.

Reserve and liquidity requirements are also animpediment to underwriting in the PDS market. Anunderwriter subscribes to PDS, then allots them tovarious investors. If the underwriter failed to allotthe PDS immediately, it would have to secure thenecessary funds to pay the issuer. It usually obtainsthe funds in interbank markets. Although the moneyis borrowed for underwriting, it is considered as aneligible liability and is subject to reserve and liquidityrequirements. This increases the cost to issuers; thusunderwriters request BNM to waive the statutoryrequirements.

95THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

SINGLE CUSTOMER LIMITBanking institutions such as commercial banks, mer-chant banks, and finance companies are subject tothe single customer limit under which they cannotprovide a single customer with loans exceeding 25percent of shareholders’ funds. Since PDS are con-sidered as loans to BNM, banking institutions aresubject to this limit but discount houses are not.Hence, discount houses usually take positions on PDS,thereby limiting the market players.

If a banking institution would like to take a posi-tion on a specific PDS that exceeds the single cus-tomer limit, it has to request BNM to waive the limit.This issue has not arisen much since most bankinginstitutions do not invest in PDS. However, as BNMis planning to abolish discount houses, it will have toreview the regulation.

Overall Bond MarketINTERESTAs the majority of Malaysians (mostly Malays) areMoslems, whose teachings prohibit payment of in-terest, many are reluctant to invest in interest-bear-ing instruments. Motivated primarily by the riba is-sue, the Government established PNB, the biggestunit trust company, to encourage the bumiputras(mostly Moslems) to mobilize their savings throughunit trusts that invest mostly in equities.

The Government started issuing Government In-vestment Notes in 1983 and BNM has also imple-mented a similar scheme. These instruments aresimilar to Government bonds and BNBs. However,they do not carry coupons but instead, pay dividends,which are roughly equivalent. In March 1993,commercial banks introduced noninterest bearingaccounts. A similar innovation has emerged inthe PDS market and the first Islamic bond was is-sued in 1990. Since then, the volume of Islamicbond issues has increased steadily, and in 1997,RM5.2 billion was raised by Islamic bond issues,representing the biggest share (26.9 percent) in thePDS market.

ISLAMIC BONDSThe increasing volume of Islamic bonds has contrib-uted to the development of the PDS market over thelast few years. However, PDS trading remains rela-tively inactive. Islamic bonds are issued through pri-vate placement, allotting the bonds to Governmentinstitutions. For instance, Kuala Lumpur InternationalAirport Bhd. (KLIA) issued a RM2.2 billion Islamicbond in 1996. KLIA, a company developing the newKuala Lumpur International Airport, can obtain fi-nancial support from the Government since it is anational project. As a result, a large portion of theKLIA Islamic bond was allotted to EPF. Similarly,many Islamic bonds (especially if the amount involvedis large) have been issued with Government support.This implies that the market yield of most Islamicbonds is below that of the market, which createsadverse effects on the secondary market.

KHAZANAH BONDSGiven the lack of a benchmark yield curve andshortage of Government bonds, the Government de-cided to issue khazanah bonds to help foster a ro-bust bond market. The first khazanah bonds wereissued in September 1997, based on the Islamicmudharabah concept (no coupon or interest pay-ment), with a face value of RM1 billion and matu-rity of three years. Khazanah bonds were expectedto be issued every quarter and the maturity to ex-tend from three to 10 years within five years. Dueto the financial crisis, however, the issuance ofkhazanah bonds was temporarily stopped in De-cember 1997, but resumed in March 1998 (RM1billion, with a three-year zero coupon).

DISTORTION OF YIELDDespite BNM’s persistence in deregulating interestrates, long-term rates (yields) are not yet fully liber-alized in Malaysia. Yields are determined throughthe auction of Government bonds but the auction isconducted through compulsory subscription by PDs.In addition, the auction reflects a high demand for

96 A STUDY OF FINANCIAL MARKETS

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

Government bonds by banking institutions and theshort supply of Government bonds, resulting in lowyields.

The distortion can also be observed in the PDSmarket. For instance, Cagamas papers are also is-sued by auctions, producing yields similar to those ofGovernment bonds. Most Islamic bonds are issued byprivate placement, and issuers and investors—basi-cally Govemment-related companies or institutions—are influenced by the Government. As a result, inves-tors are expected to accept the offered price of bonds.Hence, bond yields in Malaysia, regardless of whetherthey are Government bonds or PDS, have been sys-tematically distorted by the Government.

The secondary market is adversely affected by thedistorted yields. Despite the Government’s introduc-tion of a new accounting system for valuation of Gov-ernment bonds held by banking institutions, many bankshave not actively traded in the secondary market partlyto avoid losses. As PDS are issued in a manner simi-lar to Government bonds, trading remains inactive.

Recommended MeasuresMONETARY POLICYBNM has been employing direct lendings/borrow-ings as a major instrument for monetary regulation.In March 1998, it announced, in a policy change, thatopen market operations would be used as a majorinstrument for monetary management. However, toachieve this, there has to be a sufficient supply offinancial instruments in the market. The large out-standing Government bonds (RM69.9 billion at theend of 1997), Cagamas papers, and khazanah bondscannot be used for open market operations now sincethey have been issued at lower yields than prevailingmarket rates. Thus, BNM has to depend on short-term papers, such as T-bills, BNBs, BAs, and NCDS.BNM should issue more BNBs for open market op-erations.

In line with the policy change, reserve and liquid-ity requirements were reviewed in July 1998. To ad-just the liquidity requirement, a marking system should

be introduced to spare existing Government bond-holders from incurring big losses. For instance, a cer-tain percentage of Government bonds held by com-mercial banks, finance companies, merchant banks,EPF, and NSB should be defined as permanent hold-ings and these institutions should be required to holdthe bonds until maturity. This measure should remainin force until the yields of financial institutions’ hold-ings of Government bonds become market-based orinterest rates decline to levels below the marketyields.

PRIMARY MARKET AND BENCHMARKINTEREST RATESA short-term benchmark interest rate can be obtainedthrough open market operations. However, the cre-ation of a long-term benchmark yield curve shouldbe the target. BNM has studied the possibility of cre-ating a benchmark yield curve through Cagamaspapers. But it realized that the demand for Cagamaspapers would decline substantially if they were to beexcluded from the list of eligible securities. More-over, Cagamas papers should be issued with highmarket yields. Since September 1997, the Govern-ment has started issuing khazanah bonds, which arenot recognized as eligible securities, hoping that theywill help to create a benchmark yield curve.

The existing auction system by PDs has hinderedthe creation of a benchmark yield curve. PDs’ com-pulsory subscription should be eliminated, and thestatutory requirements for banking institutions, insur-ance companies, EPF, and NSB should be reduced.With a new auction framework to improve price quo-tations, Government bonds, Cagamas papers, andkhazanah bonds would be issued at market rates.

With the July 1998 changes in policy, the capabil-ity of khazanah bonds to create a benchmark yieldcurve was enhanced. In addition, if a new auctionsystem without compulsory subscription to Govern-ment bonds, Cagamas papers, and other papers wereintroduced, it would help successfully launch the is-suance of debt securities at market rate.

97THE CAPITAL MARKET IN MALAYSIA

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

○

With the introduction of Islamic bonds, the pri-mary market for PDS has developed rapidly. How-ever, the demand for Islamic bonds has been artifi-cially created through either or both statutory require-ments and Government guidelines in the case of bigissues. This has resulted in large issues of these bondsat distorted rates. The Government should thoroughlyreview the issuance of Islamic bonds. A fair yieldcurve would be reinstated if Government bonds,Cagamas papers, and Khazanah bonds would beissued at fair market rates.

Cagamas bonds are issued to finance the purchaseof mortgage loans from commercial banks and fi-nance companies. Their role is important in address-ing certain issues in the banking sector, such as ma-turity mismatch and liquidity enhancement. Never-theless, the sale of housing loans is undertaken withrecourse. This means that the sold loans still remainin the seller’s balance sheet. Since Cagamas Bhd.has addressed the recourse issue, BNM should takenecessary measures to facilitate the sale of mort-gage loans without recourse.