the institute of energy economics, japan tokyo, 20 june 2014eneken.ieej.or.jp/data/5537.pdf · the...

TRANSCRIPT

© OECD/IEA 2014© OECD/IEA 2014

The Institute of Energy Economics, Japan

Tokyo, 20 June 2014

Antoine Halff

2014年6月掲載 禁無断転載

© OECD/IEA 2014

The oil market at a junction

• Balances loosen up on paper but must be seen in perspective• The unconventional supply revolution enters a new stage -

matures into an increasingly global phenomenon, not just a US success story

• Political and social change in the MENA raises OPEC supply risk, partly offsetting the impact of higher non-OPEC supply

• The economic recovery buoys demand, but the dynamics of demand growth undergo a structural shift - efficiency gains and fuel switching increasingly balance income and population impacts

• Asia is by far the largest magnet for global crude exports as North America grows into a net oil exporter

• The refining industry faces a new round of restructuring and a potential glut of light products

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Oil demand nears 100 mb/d by 2019, but growth seen slowing down post-2015

+1.3% per annum, 2013-19, as macroeconomic momentum builds

0

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/d

Non-OECD Europe

Africa

FSU

Latin America

Middle East

Non-OECD Asia

OECD Asia Oceania

OECD Europe

OECD Americas

Global oil demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Asia and the Middle East are forecast to dominate growth

Strong gains are also foreseen in Africa, the FSU and the Americas

2001-07 2007-13 2013-19

2001-07 1 102 1.3%2007-13 727 0.8%2013-19 1 272 1.3% Source: IEA, Medium-Term Oil Market Report 2014

This map is w ithout prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

Average global demand growth(kb/d)

28

-327

-30 39 82 100

71

-91

70

127262 307

58 101170

Americas

Africa

Middle East

Europe FSU

779

700655

Asia/Pacific

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Transport demand keeps growing despite increasing inter-fuel competition

Road transport accounting for 4 in every 10 barrels in 2014

54.6%

54.8%

55.0%

55.2%

55.4%

55.6%

0

10

20

30

40

50

60

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/d

Shipping

Jet

Rail

Road diesel

Gasoline

Transport (rhs)

Relative share of transport use is global oil demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Petrochemicals also underpin global LPG demand growth

Underpinned by relatively low-cost LPG (+ ethane) from the US

2001-07 2007-13 2013-19

2001-07 195 2.4%2007-13 225 2.4%2013-19 291 2.7% Source: IEA, Medium-Term Oil Market Report 2014

This map is w ithout prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

Average global LPG and Ethanedemand growth

(kb/d)

19

4

23 117

11

24

74115

20

65 55

8 715

Americas

Africa

Middle East

Europe FSU

113

67 73

Asia/Pacific

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Oil use extends decline in the power generation and residential sectors

Power sector oil-use falls everywhere bar Middle East

0%

20%

40%

60%

80%

100%

Africa Non-OECD Asia China FSU/non-OECD Europe

Latin America Middle East Americas Europe Asia Oceania

Renewable energy

Nuclear

Gas

Oil

Coal

Power generation mix by region, 2019

2014年6月掲載 禁無断転載

© OECD/IEA 2014

US gasoline demand is forecast to lead the OECD downtrend

Ongoing vehicle efficiency gains outweigh US population growth

-4%

-3%

-2%

-1%

0%

1%

2%

0

1

2

3

4

5

6

7

8

9

10

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Litres

of g

asolin

e per

100k

m Average vehicle efficiency (lhs)

Gasoline demand, growth (rhs)

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Demand’s dominant market share to be taken by non-OECD

Traditional OECD/non-OECD split will lose relevance

35%

40%

45%

50%

55%

60%

65%

0

20

40

60

80

100

120

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/d

Middle East

Former Soviet Union

Non-OECD Europe

China

Asia

Non-OECD Americas

Africa

OECD Asia Oceania

OECD Europe

OECD Americas

OECD share

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Supply

2014年6月掲載 禁無断転載

© OECD/IEA 2014

World oil supply capacity continues to expand, led by non-OPEC

Total oil supply capacity grows by 9 mb/d to 105 mb/d Exceptionally strong non-OPEC growth, but slowing later in the

forecast period

-0.5

0.0

0.5

1.0

1.5

2.0

2013 2014 2015 2016 2017 2018 2019

mb/d

OPEC Crude capacity OPEC NGLsGlobal Biofuels Non-OPEC (excl. Biofuels)World

Global oil supply capacity growth

2014年6月掲載 禁無断転載

© OECD/IEA 2014

World trends in capex

Global capital expenditure (including exploration capex) is increasingly targeted at non-conventional/difficult resources

Source: IEA analysis of Rystad Energy data.

*NB: That which excludes the other four non-conventional categories.

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

300

350

2013 2014 2015 2016 2017 2018 2019

billion

USD

Oil shale (kerogen) Oil sandsExtra heavy oil Tight oilDeepwater and ultra-DW* Conventional share

2014年6月掲載 禁無断転載

© OECD/IEA 2014

OPEC production capacity grows 2.1 mb/d

Reaches 37.1 mb/d by 2019 with Iraq to supply 60% of growth Worsening political stability and security issues add downside

risk in Iraq as well as Libya

Incremental OPEC crudeproduction capacity 2013-19 (mb/d)

OPEC crude production capacity

32

33

34

35

36

37

38

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013 -0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

1

IraqUAEAngolaVenezuelaEcuadorSaudi ArabiaIranQatarLibyaNigeriaAlgeriaKuwait

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Iraq faces formidable challenges in meeting ambitious production targets

Iraq production capacity to rise by 1.28 mb/d to 4.54 mb/d by 2019 Weak institutions have lead to delays in contract awards for

infrastructure plans that anchor projects

Iraq crude production capacity growth

0

1 000

2 000

3 000

4 000

5 000

2010 2012 2014 2016 2018

mb/d

Southern area Central and northern KRG

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013

Iraq crude oil production by region

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Saudi Arabia maintains capacity around 12.5 mb/d

Gross capacity increase of 1.45 mb/d offset natural decline rates and allows mature field capacity reductions

Could notionally increase capacity beyond target if needed, with plans on the back burner to add a further 1.9 mb/d

Saudi Arabia crude oil production capacity

8.0

9.0

10.0

11.0

12.0

13.0

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013

2014年6月掲載 禁無断転載

© OECD/IEA 2014

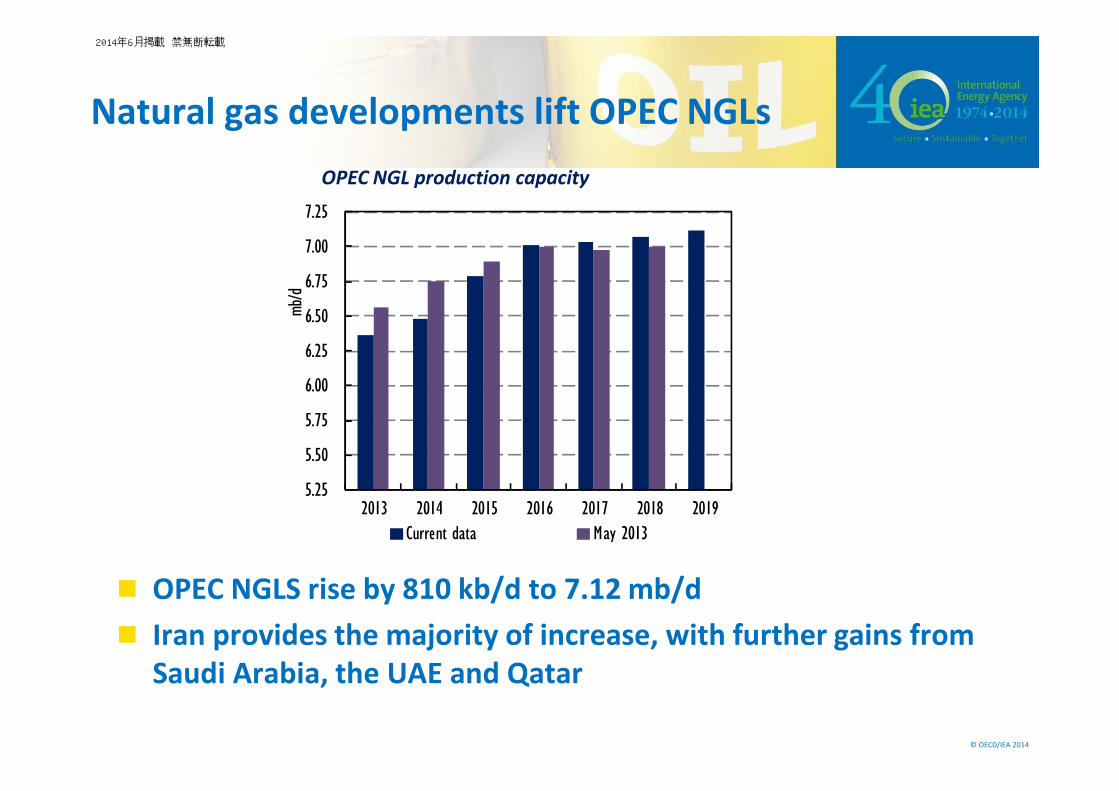

Natural gas developments lift OPEC NGLs

OPEC NGLS rise by 810 kb/d to 7.12 mb/d Iran provides the majority of increase, with further gains from

Saudi Arabia, the UAE and Qatar

OPEC NGL production capacity

5.25

5.50

5.75

6.00

6.25

6.50

6.75

7.00

7.25

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013

2014年6月掲載 禁無断転載

© OECD/IEA 2014

North America continues to lead non-OPEC supply growth

Growth diversifies later in the period Non-OPEC supply grows by 6.2 mb/d to 60.9 mb/d

Annual non-OPEC supply growth

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2003 2005 2007 2009 2011 2013 2015 2017

mb/d

PG and biofuelsOther Asia

China

Middle EastAfrica

Latin AmericaFSU

OECD Pacif icOECD EuropeOECD AmericasTotal

2014年6月掲載 禁無断転載

© OECD/IEA 2014

US oil production driven by LTO and NGLs

By the end of the decade, the majority of US liquids output consists of LTO and NGLs, and total production exceeds 13 mb/d.

0

2

4

6

8

10

12

14

2007 2009 2011 2013 2015 2017 2019

mb/d

LTO Gulf of Mexico NGLs Other liquids Other crude & cond

US total oil production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Canadian oil production driven by oil sands

Bitumen and synthetics lead growth, while core Alberta light and medium production continues to decline.

-

50

100

150

200

250

300

0

1

2

3

4

5

6

2013 2014 2015 2016 2017 2018 2019

kb/dmb

/d

NGLs Alberta L&M BitumenSynthetics Other Growth (RHS)

Canada total oil production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Mexican reform to lift production

In a change from the last Report’s forecast, production forecast to increase in 2018

Some of this is long-planned Pemex projects, but the reform process is seen to affect production in 2019 and beyond

2.65

2.70

2.75

2.80

2.85

2.90

2.95

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013

Mexico total oil production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

North Sea oil production flattens out

Growth set to resume in 2015 for the first time since 2000, as numerous new fields are brought online, though declines marginally again in 2018-2019

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/d

UK Norway Other Ann. Growth (rhs)

North Sea total oil production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Brazil turnaround in sight

Despite challenges, including an indebted and overstretched Petrobras and high decline rates on mature offshore

Increases to average about 160 kb/d per year given major project start ups in the Santos basin

1.6

1.8

2.0

2.2

2.4

2.6

2.8

3.0

3.2

2013 2014 2015 2016 2017 2018 2019

mb/d

-150-100-500

50100150200250300350

2008 2010 2012 2014 2016 2018

kb/d

Campos Santos Other Brazil crude

Total oil production Production by basin

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Russia crude oil steady but on a higher baseline

Russia is expected to maintain the highest crude oil production capacity in the world after Saudi Arabia.

9.2

9.4

9.6

9.8

10.0

10.2

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013

Russia crude oil production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

NGLs gain share of global supply

NGL capacity grows by 1.6 mb/d to 10.7 mb/d in 2019; NGLs, field condensate grow to 17% of global supply, from 16%

0

2

4

6

8

10

12

2013 2014 2015 2016 2017 2018 2019

mb/d

Pentanes

LPG

Ethane

World NGLs production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

The world gas supply getting wetter

Driven by liquids-rich plays in North America, tempered by dry gas increases in Asia later in the period

1.40

1.45

1.50

1.55

1.60

1.65

1.70

2011 2013 2015 2017 2019

barre

ls pe

r 1 0

00 cub

ic me

tres

Barrels of NGLs and condensates per tcm of gas production

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Biofuels growth shift away from OECD and Brazil

Policy support is waning in OECD countries, while their demand growth is already weak. Gasoline subsidies and a weak sugar market are impacting Brazil

Can be advantageous in countries with large product import bills and extant subsidies

World biofuel production

0.0

0.5

1.0

1.5

2.0

2.5

2013 2014 2015 2016 2017 2018 2019

mb/d

US Brazil OECD EUROther 2013 MTOMR

1.2%

1.3%

1.4%

1.5%

1.6%

1.7%

1.8%

1.0

1.2

1.4

1.6

1.8

2013 2014 2015 2016 2017 2018 2019

mboe

/d

Biof. supply (adj. for energy cont.) As % of global oil demand

World biofuel production adj. for energy content as a % of global oil demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Crude trade

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Crude trade shifts further east

Asia imports increase by 2.6 mb/d to 22.1 mb, or 65% of the international crude market

Crude Exports in 2019 and Growth in 2013-19 for Key Trade Routes1

(million barrels per day)

0.2 0.3(0) 2.0 (0.2)

(-0.6) 4.1(-0.6)

0.1(-0.7)

3.11.2 (0.3)

1.0 (+0.1)-0.6

2.21.8 (+0.8)(-0.6)

1.1(+0.3)

Red number in brackets denotes growth in period 2013-19 1.21Excludes Intra-Regional Trade (+0.6)2 Includes Chile3 Includes Israel

5.2(+0.3)

Other Asia

China

OECD Europe

1.6(-0.2)

1.3 (+0.6)OECD Asia

Oceania3

0.5 (-0.0)

0.7(+0.4)

3.6 (-0.5)

OECDAmericas2

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Global crude trade to contract by 1.1 mb/d by 2019

Increased North American and Middle Eastern crude seen being refined close to the wellhead and subsequently exported as products

-2 000

-1 500

-1 000

- 500

0

500

1 000

2013 2014 2015 2016 2017 2018 2019

kb/d

Africa FSU Latin America Middle East OECD Europe OECD Americas OECD Asia Oceania Other Asia Other Europe China

-2 500

-2 000

-1 500

-1 000

- 500

0

500

1 000

2013 2014 2015 2016 2017 2018 2019

kb/d

Regional crude exports, yearly change Regional crude imports, yearly change

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Middle East to remain key crude exporting region throughout the forecast

BUT its exports are forecast to decline to 16.1 mb/d (-900 kb/d) as regional producers refine more oil close to the wellhead Regional refinery capacity growth set to outstrip production growth Decrease in crude shipments will be offset by an anticipated increase in

product exports

Exports projected to be redirected eastwards to non-OECD Asia

-0.60 -0.40 -0.20 0.00 0.20 0.40

China

Oth Asia

Oth Eur

L. America

FSU

Africa

OECD Eur

OECD AO

OECD AM

mb/d

Middle East export growth 2013-19

2014年6月掲載 禁無断転載

© OECD/IEA 2014

FSU to continue to diversify exports eastwards

Shipments to Asia will hit 2.6 mb/d by 2019 Exports to Europe to fall by over 500 kb/d to 3.9 mb/d by 2019

Europe will remain the region’s largest customer, but its share of FSU exports will fall to 54% in 2019 from 65% in 2013

-0.60 -0.30 0.00 0.30 0.60 0.90

China

Oth Asia

Oth Eur

LATAM

Middle East

OECD AO

Africa

OECD AM

OECD Eur

mb/d

FSU export growth 2013-19

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Americas to become a net crude exporter by 2019

In response to soaring supplies from US, Canada and Brazil Which will outstrip regional refinery capacity growth

OECD Americas still to import 3.1 mb/d of mainly heavy sour crudes in 2019, 2.2 mb/d lower than in 2013

Middle East will account for 57% of regional imports But absolute volumes will drop by 600 kb/d

Middle East45%

Latin America30%

Africa15%

FSU5%

Others5%

Middle East57%Latin America

32%

Africa3%

FSU5%

Others3%

OECD American crude imports, 2013 OECD American crude imports, 2019

2014年6月掲載 禁無断転載

© OECD/IEA 2014

China to consolidate its position as the world’s largest importing country

China to import 7.1 mb/d in 2019 China to continue diversifying its crude imports

Imports from the FSU to reach 1.3 mb/d

Most of the growth will be long-haul trade

Africa21%

FSU13%

Latin America10%

Middle East52%

Others4% Africa

17%

FSU19%

Latin America16%

Middle East44%

Others4%

Chinese crude imports, 2013 Chinese crude imports, 2019

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Refining

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Refinery capacity expansions continue…

95% of new capacity comes from the non-OECD, of which Asia accounts for half

-0.5

0.0

0.5

1.0

1.5

2.0

2013 2014 2015 2016 2017 2018 2019

mb/d

OECD North America OECD Europe OECD Pacific FSU China Other Asia Latin America Middle East Africa

CDU Expansions 2013-2019 by Region

Crude Distillation Expansions

2014年6月掲載 禁無断転載

© OECD/IEA 2014

…but plans are getting scaled back in the face of rising over-capacity

Projects slip in Latin America; China stalls new projects on looming surplus capacity, corruption scandals, pollution concerns

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2012 2013 2014 2015 2016 2017 2018

mb/d

OECD Americas Other OECD China Other Asia

Middle East Latin America Other non-OECD

0

200

400

600

800

1 000

1 200

1 400

1 600

2012 2013 2014 2015 2016 2017 2018 2019

kb/d

Current data May-13

Chinese CDU expansions vs . previous

Revisions to capacity expansion plans since 2013 MTOMR

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Chinese product output to balance demand as projects scaled back

Apparent slowdown in gasoil demand growth sees product surpluses emerging. Indeed, China turned net gasoil exporter in 2013

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

Chinese total refinery output vs demand Chinese gasoil refinery output vs demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Diverging trends in OECD refining: Europe & Asia versus North America

OECD Refinery Shutdowns

4.5 mb/d of OECD crude distillation capacity shut since 2008 Surging US LTO, condensate supplies lead to 750 kb/d

expansion in US in 2015-2017

0.0

0.5

1.0

1.5

2008 2009 2010 2011 2012 2013 2014 2015

mb/d

OECD Americas OECD Europe OECD Asia Oceania

- 100

0

100

200

300

400

500

2013 2014 2015 2016 2017 2018 2019

kb/d

Crude distillation Upgrading Desulphurisation

North America Capacity Additions

2014年6月掲載 禁無断転載

© OECD/IEA 2014

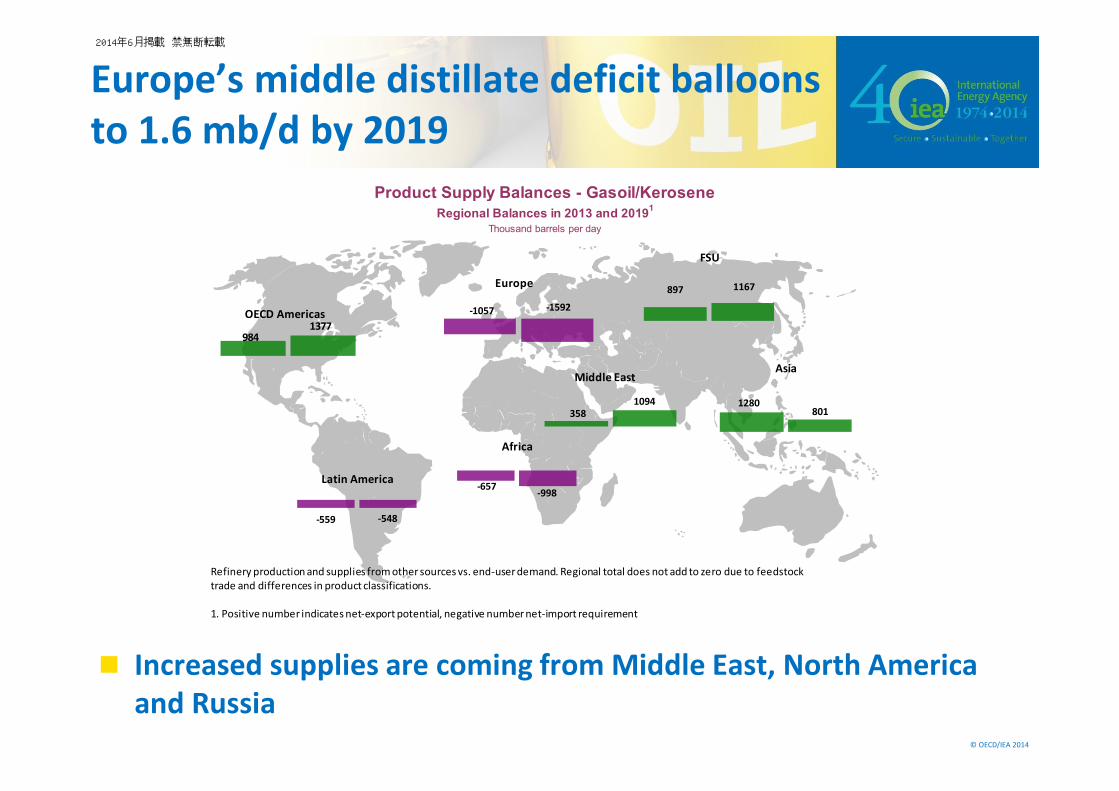

Europe’s middle distillate deficit balloonsto 1.6 mb/d by 2019

Increased supplies are coming from Middle East, North America and Russia

Product Supply Balances - Gasoil/KeroseneRegional Balances in 2013 and 20191

Thousand barrels per day

897 1167

FSU

-1057 -1592

Europe

9841377

OECD Americas

-559 -548

Latin America

3581094

Middle East

1280801

Asia

-657 -998

Africa

Refinery production and supplies from other sources vs. end-user demand. Regional total does not add to zero due to feedstock trade and differences in product classifications.

1. Positive number indicates net-export potential, negative number net-import requirement

2014年6月掲載 禁無断転載

© OECD/IEA 2014

North American gasoline glut emerging

North America faces excess light distillate supply of 1.3 mb/d in 2019, in search of export outlets

Product Supply Balances - Gasoline/NaphthaRegional Balances in 2013 and 20191

Thousand barrels per day

469 528FSU

718652

Europe

-205

1320OECD Americas

154 138

Latin America

7021023

Middle East

-974 -1490

Asia

-143-332

Africa

Refinery Production and supplies from other sources vs. end-user demand. regional total do not add to zero due to feedstock trade and differences in product classifications.

Positive number indicates net-export potential, negative number indicate net-import requirement

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Atlantic Basin product trade to increase

European middle distillate deficit balloons to 1.6 mb/d by 2019,but region struggle to rid itself of surplus gasoline supplies

US refinery industry renaissance, coinciding with sharp drop in demand, takes US to top global naphtha/gasoline supplier

-1 000

- 500

0

500

1 000

1 500

2008 2010 2012 2014 2016 2018

kb/d

Naphtha/gasoline Jet/gasoil

Imports-2 000

-1 500

-1 000

- 500

0

500

1 000

1 500

2008 2010 2012 2014 2016 2018

kb/d

Naphtha/gasoline Jet/gasoil

Imports

Exports

OECD America’s key product balancesEurope’s key product balances

2014年6月掲載 禁無断転載

© OECD/IEA 2014

FSU fuel oil supplies cut back as refiners upgrade and export duties changed

Equalization of Russian fuel oil export duties with crude oil from Jan 2015, has led to refinery upgrading investments

New duties make simple refiners, with high fuel oil yield, uneconomical to run

Fuel oil demand stays unchanged through 2019,as non-OECD offset improvement in OECD

0

200

400

600

800

1 000

1 200

1 400

1 600

2008 2010 2012 2014 2016 2018

kb/d

Jet/gasoil Fuel oil

FSU key product exports Global fuel oil demand

0

2

4

6

8

10

2006 2009 2012 2015 2018

mb/d

North America Europe OECD Asia FSU

Latin America Middle East Africa Non-OECD Asia

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Fuel oil markets could tighten

Russian export duty reform, refinery investments curb output while global demand stays flat – unless marine bunker markets shift away from fuel oil ahead of new IMO sulphur standards

Product Supply Balances - Fuel OilRegional Balances in 2013 and 20191

Thousand barrels per day

1264636

FSU

-58 -166

Europe

175207

OECD Americas

140 113

Latin America

-192 -153

Middle East

-1129 -782

Asia

-67 -110

Africa

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Middle East emerges as large product exporter

New refinery projects coming on stream in the Middle East exceed regional demand growth, resulting in increased product exports – in particular of middle distillates

- 500

0

500

1 000

1 500

2008 2010 2012 2014 2016 2018

kb/d

Naphtha/gasoline Jet/gasoil Fuel oil

Imports

Exports

6.0

7.0

8.0

9.0

10.0

11.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

Middle Eastern product balances Middle East refinery output vs demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Africa and Latin America remain importers

Difficulties in bringing new refinery projects on stream, leaves Africa and Latin America with large product import requirements

Heavy financial burden on governments subsidising fuels

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

Africa refinery output vs total oil demand

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

Latin American refinery output vs total oil demand

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Refinery margins, utilisation rates remain under pressure amid surplus capacity

To bring utilisation rates up to 2006-2008 levels (when margins were healthy), another 4.8 mb/d of capacity would have to be cut, whether through plant closures, projects delays or cancellations

-7.5

-5.0

-2.5

0.0

2.5

5.0

7.5

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14

USD/

bbl

NW Europe Urals NW Europe BrentMED Urals Singapore Dubai

70.0%

75.0%

80.0%

85.0%

90.0%

1Q06 1Q09 1Q12 1Q15 1Q18

World OECD Non-OECD

Benchmark simple refinery margins Refinery utilisation rates

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Summary

2014年6月掲載 禁無断転載

© OECD/IEA 2014

On paper, oil market balance eases, but risks and challenges abound

Nominal spare OPEC capacity to rise from 2013 But high risk remains

- 1

0

1

2

3

4

5

6

7

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/d

Implied spare capacity

Effective OPEC sparecapacity

World demand growth

World supply capacitygrowth

Medium-term oil market balance

2014年6月掲載 禁無断転載

© OECD/IEA 2014

Thank you

Further questions: [email protected]

2014年6月掲載 禁無断転載

お問い合わせ:[email protected]