webinar viability consolidated v1.0

TRANSCRIPT

1

WEBINAR ON

The Viability of Microinsurance

Presenter:Craig ChurchillTeam Leader

Microinsurance Innovation FacilityPresenter:

Alok AgarwalExecuitve Director

ICICI LombardIndia

Presenter:Pedro Bulcão

Chief Executive Officer Sinaf Seguros

Brazil

Moderator:Jasmin Suministrado

Knowledge OfficerMicroinsurance Innovation Facility

2

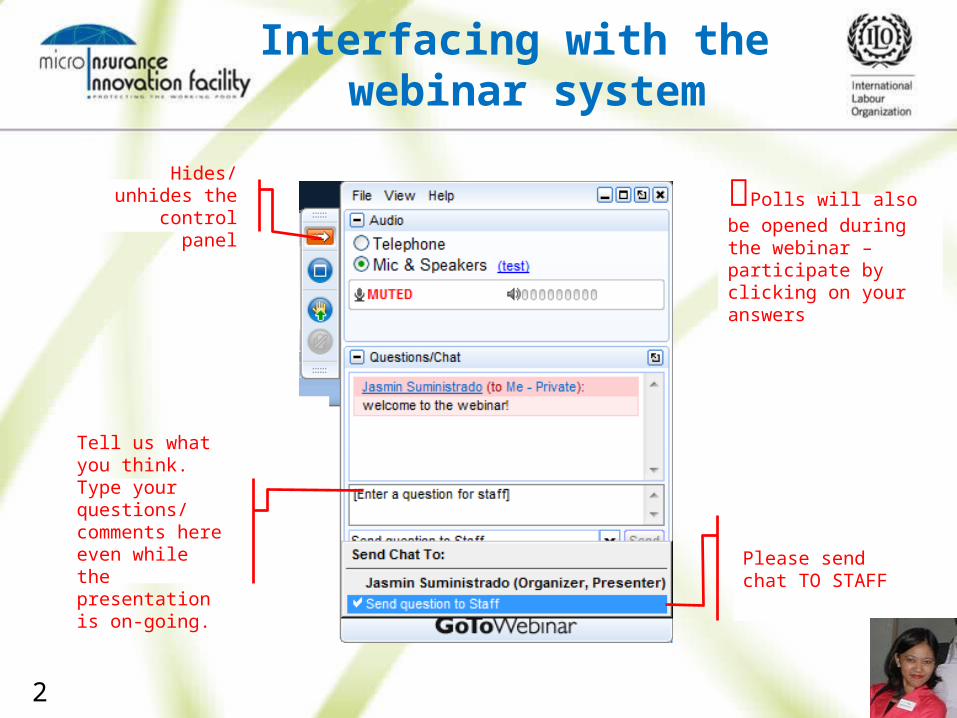

Interfacing with the webinar system

Hides/unhides the control

panel Polls will also be opened during the webinar – participate by clicking on your answers

Tell us what you think. Type your questions/ comments here even while the presentation is on-going.

Please send chat TO STAFF

3

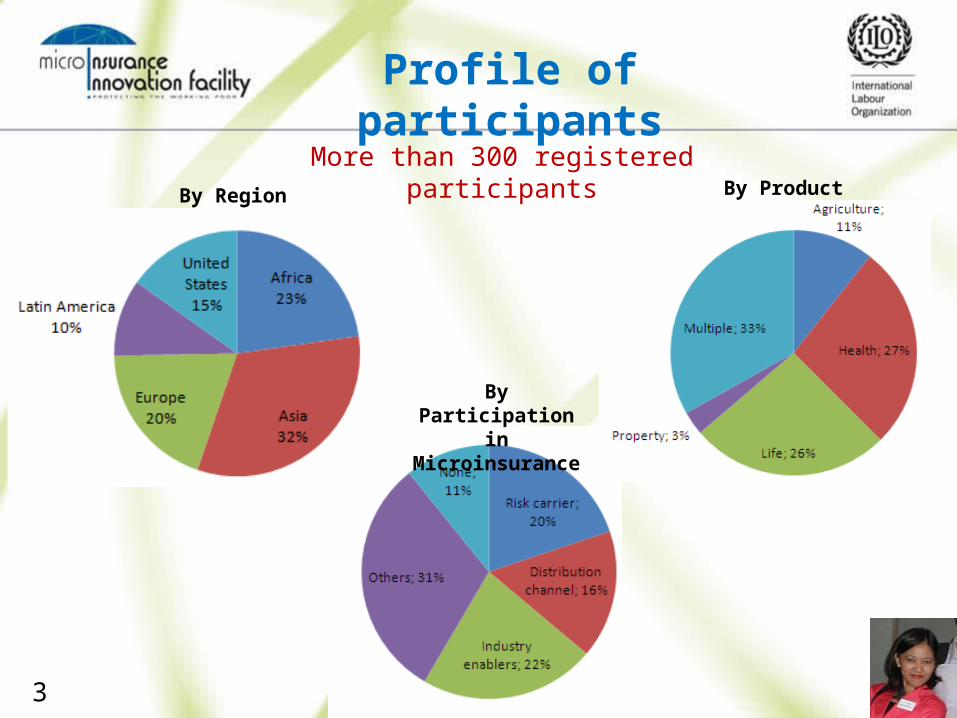

Profile of participants

More than 300 registered participants

By Participation in Microinsurance

By Region By Product

4

WEBINAR ON

The Viability of Microinsurance

Presenter:Craig ChurchillTeam Leader

Microinsurance Innovation FacilityPresenter:

Alok AgarwalExecuitve Director

ICICI LombardIndia

Presenter:Pedro Bulcão

Chief Executive Officer Sinaf Seguros

Brazil

Moderator:Jasmin Suministrado

Knowledge OfficerMicroinsurance Innovation Facility

5

Introduction

• Why did we conduct this study?• Sampling• Challenges in assessing profitability

Structure of presentation

1. Introduction of the schemes

2. Growth

3. Efficiency and productivity

4. Viability

6

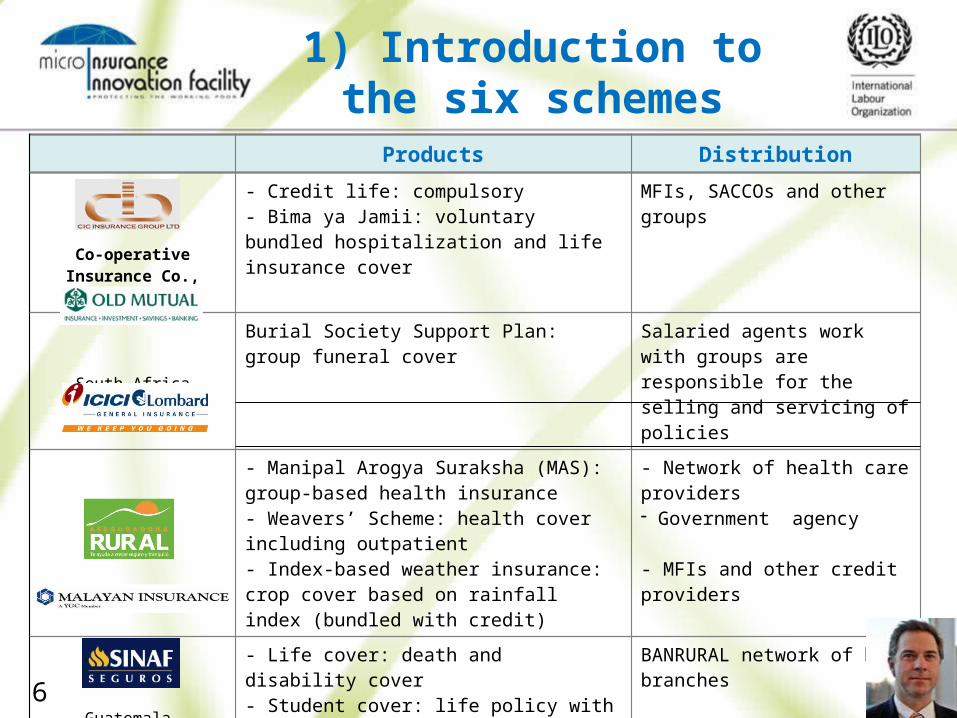

1) Introduction to the six schemes

Products Distribution

Co-operative Insurance Co., Kenya

- Credit life: compulsory - Bima ya Jamii: voluntary bundled hospitalization and life insurance cover

MFIs, SACCOs and other groups

South Africa

Burial Society Support Plan: group funeral cover

Salaried agents work with groups are responsible for the selling and servicing of policies

India

- Manipal Arogya Suraksha (MAS): group-based health insurance- Weavers’ Scheme: health cover including outpatient- Index-based weather insurance: crop cover based on rainfall index (bundled with credit)

- Network of health care providers- Government agency

- MFIs and other credit providers

Guatemala

- Life cover: death and disability cover- Student cover: life policy with additional health cover

BANRURAL network of bank branches

PhilippinesLife cover with additional benefits (e.g. fire assistance)

Pawn shops, rural banks and other credit providers

Brazil

- Funeral- Term life and personal accident

Tied agents (in-house sales force)

7

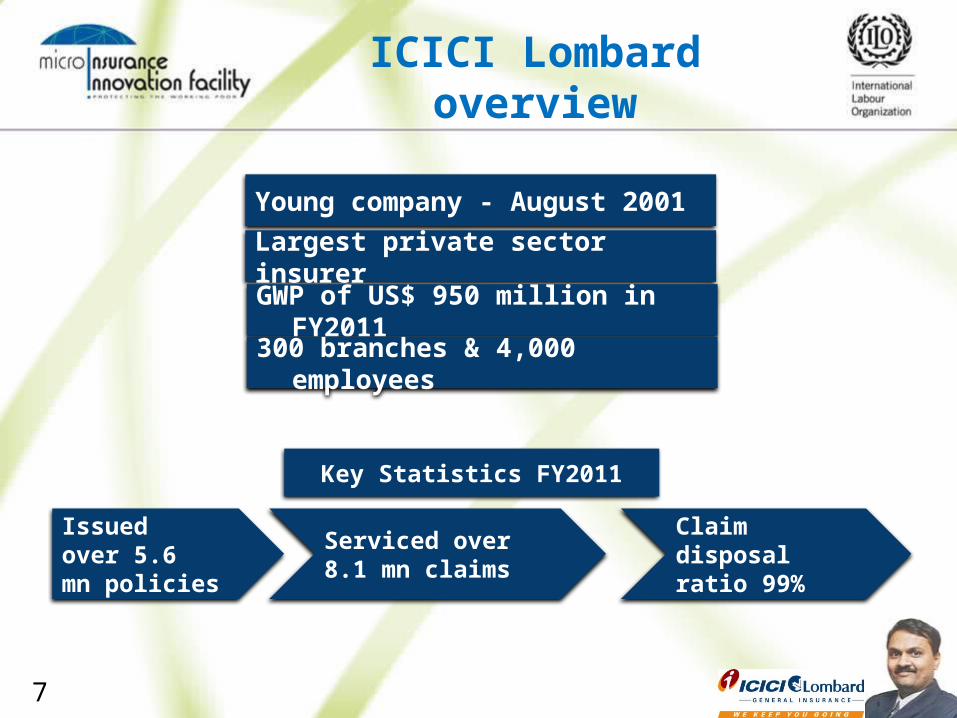

ICICI Lombard overview

Young company - August 2001

Largest private sector insurer

GWP of US$ 950 million in FY2011

300 branches & 4,000 employees

Issued over 5.6 mn policies

Serviced over 8.1 mn claims

Claim disposal ratio 99%

Key Statistics FY2011

8

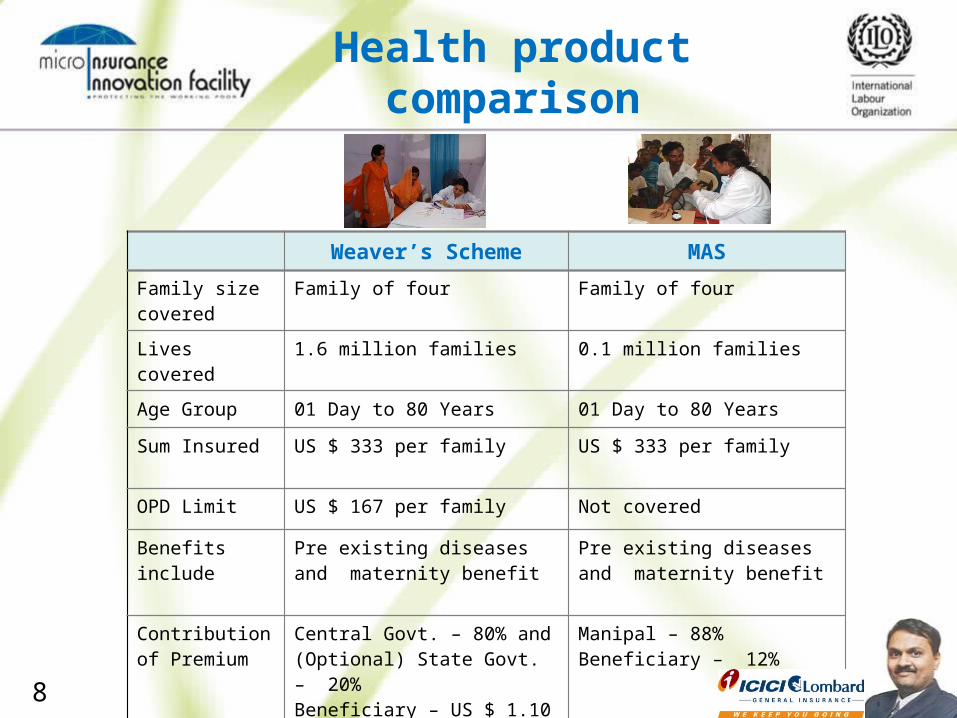

Health product comparison

Weaver’s Scheme MASFamily size covered

Family of four Family of four

Lives covered 1.6 million families 0.1 million families

Age Group 01 Day to 80 Years 01 Day to 80 Years

Sum Insured US $ 333 per family US $ 333 per family

OPD Limit US $ 167 per family Not covered

Benefits include Pre existing diseases and maternity benefit

Pre existing diseases and maternity benefit

Contribution of Premium

Central Govt. – 80% and (Optional) State Govt. – 20%Beneficiary – US $ 1.10

Manipal – 88%Beneficiary – 12%

9

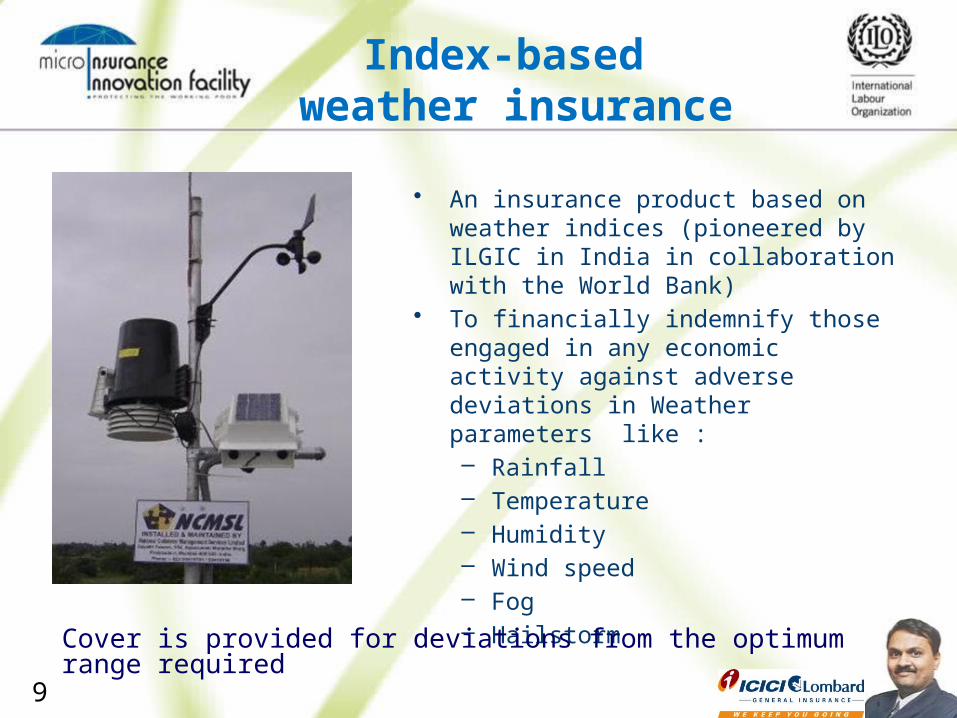

Index-based weather insurance

• An insurance product based on weather indices (pioneered by ILGIC in India in collaboration with the World Bank)

• To financially indemnify those engaged in any economic activity against adverse deviations in Weather parameters like :– Rainfall – Temperature– Humidity– Wind speed– Fog– Hailstorm

Cover is provided for deviations from the optimum range required

10

Sinaf overview

Sinaf’s Products

Funeral

Personal Accident

Family income benefit: 06 to 24 months

Senior couple or individual life insuranceFuneral (relatives)

• Life insurance company, 30 years experience with funeral insurance;

• Operating at the metropolitan area of Rio de Janeiro, Brazil;• Totally focused on low income market;• Distribution by an in-house sales-force.

11

Target market

12

Structure of presentation

1. Introduction of the schemes

2. Growth

3. Efficiency and productivity

4. Viability

13

2) Growth

Growth is a key objective for both social and commercial reasons– Social: want to make cover available to as many low-income

households as possible– Commercial: Need to achieve economies of scale, reduce

adverse selection

14

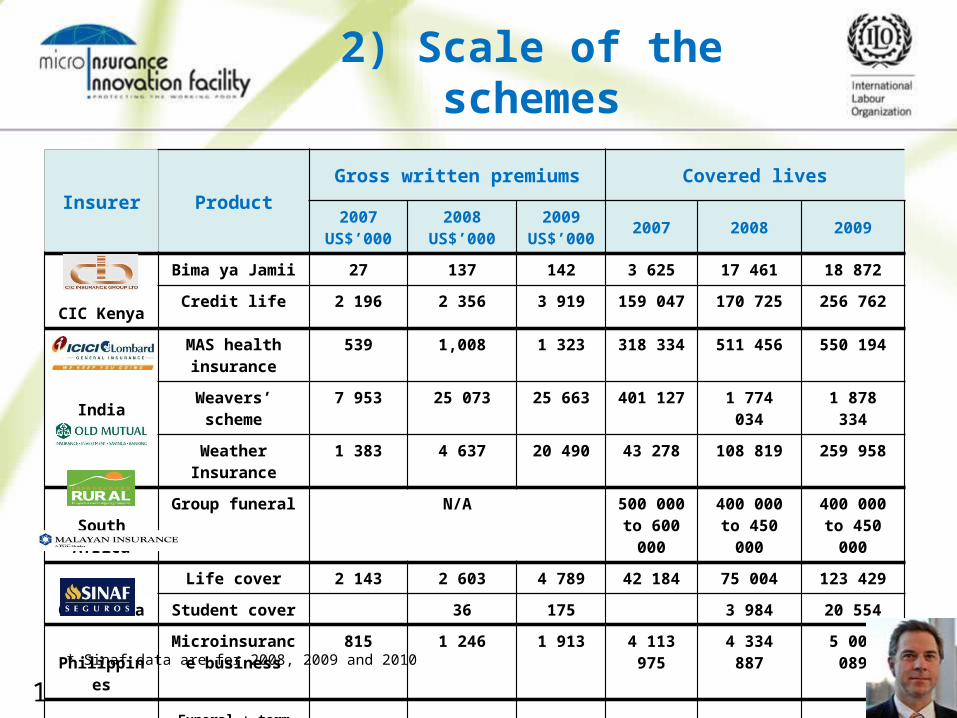

2) Scale of the schemes

Insurer ProductGross written premiums Covered lives

2007US$’000

2008US$’000

2009US$’000 2007 2008 2009

CIC Kenya

Bima ya Jamii 27 137 142 3 625 17 461 18 872

Credit life 2 196 2 356 3 919 159 047 170 725 256 762

India

MAS health insurance

539 1,008 1 323 318 334 511 456 550 194

Weavers’ scheme 7 953 25 073 25 663 401 127 1 774 034 1 878 334

Weather Insurance 1 383 4 637 20 490 43 278 108 819 259 958

South AfricaGroup funeral N/A 500 000 to

600 000400 000 to

450 000400 000 to

450 000

Life cover 2 143 2 603 4 789 42 184 75 004 123 429

Guatemala Student cover 36 175 3 984 20 554

PhilippinesMicroinsurance

business815 1 246 1 913 4 113 975 4 334 887 5 009 089

Brazil*Funeral + term

life/Personal accident* 17 584 21 746 25 775 356 935 360 742 405 057

* Sinaf data are for 2008, 2009 and 2010

15

Realigning objective, make government a catalyst to micro

insurance business

• Higher growth in weather business seen due to increased sum insured and multiple covers offered during renewals

• Realigning organization business objective with governments social security schemes helps to build scale

• Building the capacity to deliver services – Claim settlement capacity should be robust

• Transparency in dealing with government helps to manage reputation risk – e.g. Low claim bonus in renewals

16

2) Scale of the schemes

Insurer ProductGross written premiums Covered lives

2007US$’000

2008US$’000

2009US$’000 2007 2008 2009

CIC Kenya

Bima ya Jamii 27 137 142 3 625 17 461 18 872

Credit life 2 196 2 356 3 919 159 047 170 725 256 762

India

MAS health insurance

539 1,008 1 323 318 334 511 456 550 194

Weavers’ scheme 7 953 25 073 25 663 401 127 1 774 034 1 878 334

Weather Insurance 1 383 4 637 20 490 43 278 108 819 259 958

South AfricaGroup funeral N/A 500 000 to

600 000400 000 to

450 000400 000 to

450 000

Life cover 2 143 2 603 4 789 42 184 75 004 123 429

Guatemala Student cover 36 175 3 984 20 554

PhilippinesMicroinsurance

business815 1 246 1 913 4 113 975 4 334 887 5 009 089

Brazil*Funeral + term

life/Personal accident* 17 584 21 746 25 775 356 935 360 742 405 057

* Sinaf data are for 2008, 2009 and 2010

17

Growth

18

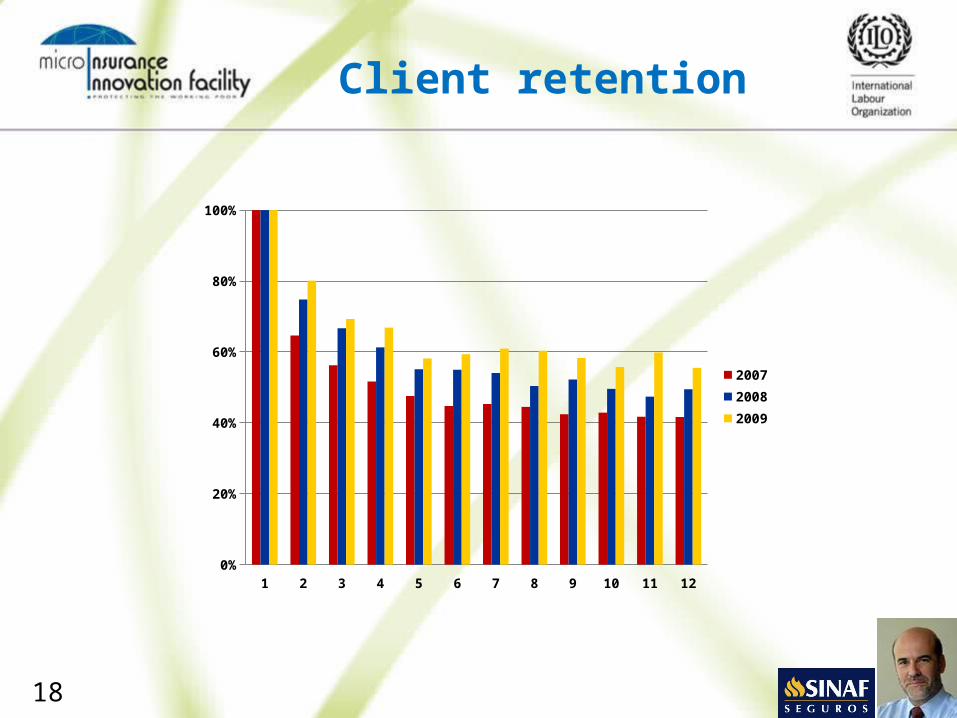

Client retention

1 2 3 4 5 6 7 8 9 10 11 120%

20%

40%

60%

80%

100%

2007 2008 2009

19

Structure of presentation

1. Introduction of the schemes

2. Growth

3. Efficiency and productivity

4. Viability

20

3) Efficiency and productivity

• Difficult to assess actual microinsurance expenses in commercial insurance companies

• Need to minimize operational expenses to provide value to the target group

• Depends significantly on the means of distribution

21

3) Expenses

Insurer Product Expense Ratio (%)

2007 2008 2009

CIC, Kenya

Bima ya Jamii 35 41 58

Credit life 27 26 29

India

MAS health insurance 20 20 16

Weavers’ scheme 15 12 10

Weather insurance 20 20 20

South Africa Group funeral 30 to 40 >40 >40

Guatemala

Life cover 7 14 10

Student cover13 9

PhilippinesMicroinsurance business 40 38 35

Brazil*

Funeral and term life/personal accident * 61 61 55

* Sinaf data are for 2008, 2009 and 2010; and cover both management and commercial expenses

22

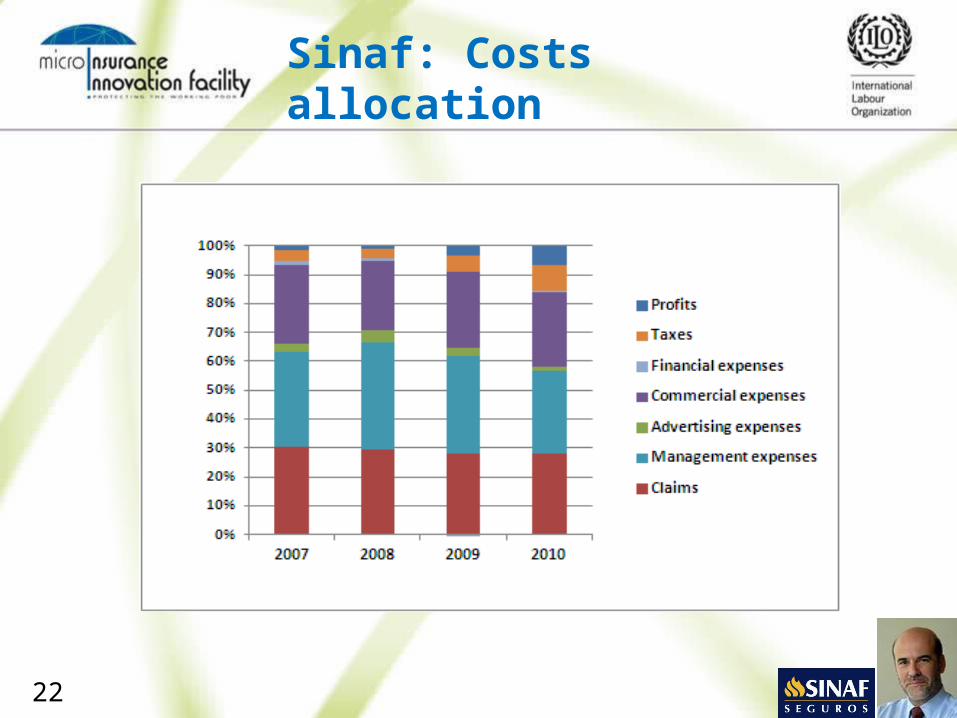

Sinaf: Costs allocation

23

Technology and process efficiency in health

This has led to claims reduction by 10%

Enrollment Efficiency Claims Efficiency

Hygiene in enrollment Higher renewal %

Reduction of claim TAT De empanelment of

fraudulent hospital

In-housing of claimsRural POSFraud trigger mechanism Internal surveillance

team

Action taken

Results

Target renewal customer first Use smart card for long term Monitor vendor performance Use client network to enroll

Process Efficiency

24

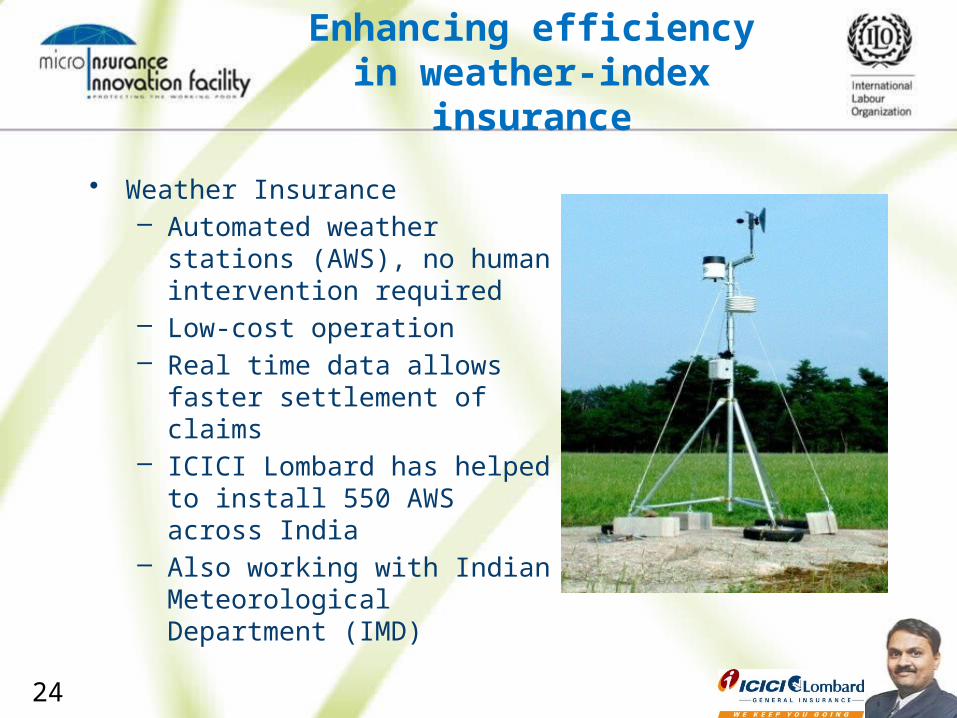

Enhancing efficiency in weather-index insurance

• Weather Insurance– Automated weather stations

(AWS), no human intervention required

– Low-cost operation– Real time data allows faster

settlement of claims – ICICI Lombard has helped to

install 550 AWS across India– Also working with Indian

Meteorological Department (IMD)

25

Sales Office Manager

Structured for productivity

26

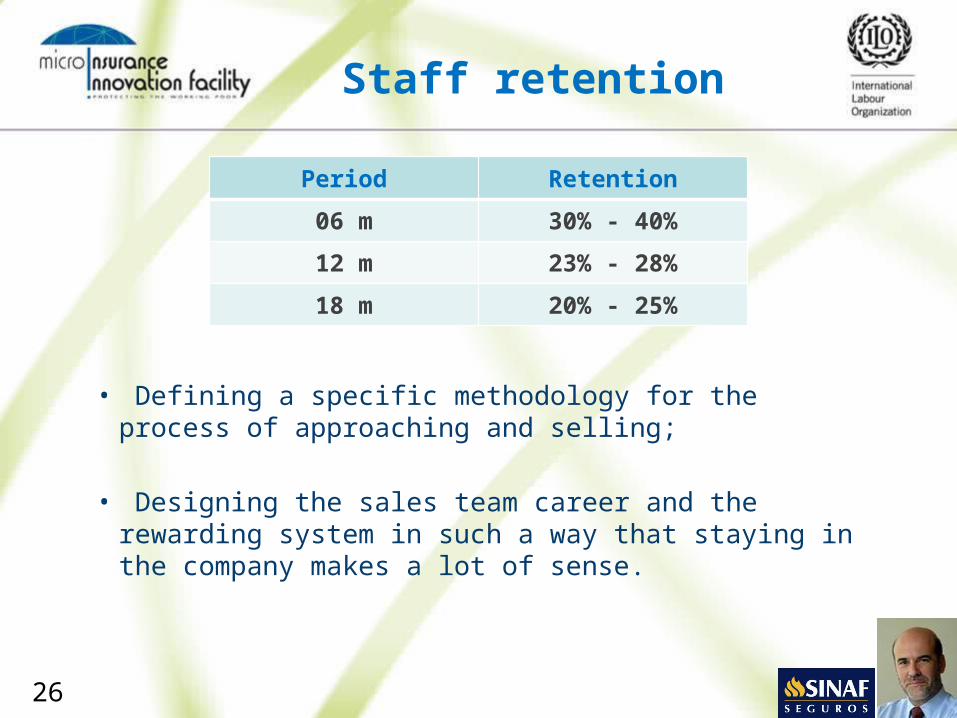

Staff retention

Period Retention06 m 30% - 40%12 m 23% - 28%18 m 20% - 25%

• Defining a specific methodology for the process of approaching and selling;

• Designing the sales team career and the rewarding system in such a way that staying in the company makes a lot of sense.

27

Structure of presentation

1. Introduction of the schemes

2. Growth

3. Efficiency and productivity

4. Viability

28

4) Viability

Insurer Product Combined ratio (%)

2007 2008 2009

CIC, Kenya

Bima ya Jamii 39 48 73

Credit life 32 34 34

India

MAS health insurance130 129 126

Weavers’ scheme 122 113 116

Weather insurance 135 95 97

South Africa Group funeral >120 >120 >105

Guatemala

Life cover 9 52 42

Student cover 24 40

PhilippinesMicroinsurance business 53 65 53

Brazil*

Funeral*95 94 91Term life / personal

accident*

* Sinaf data are for 2008, 2009 and 2010

29

Viability

30

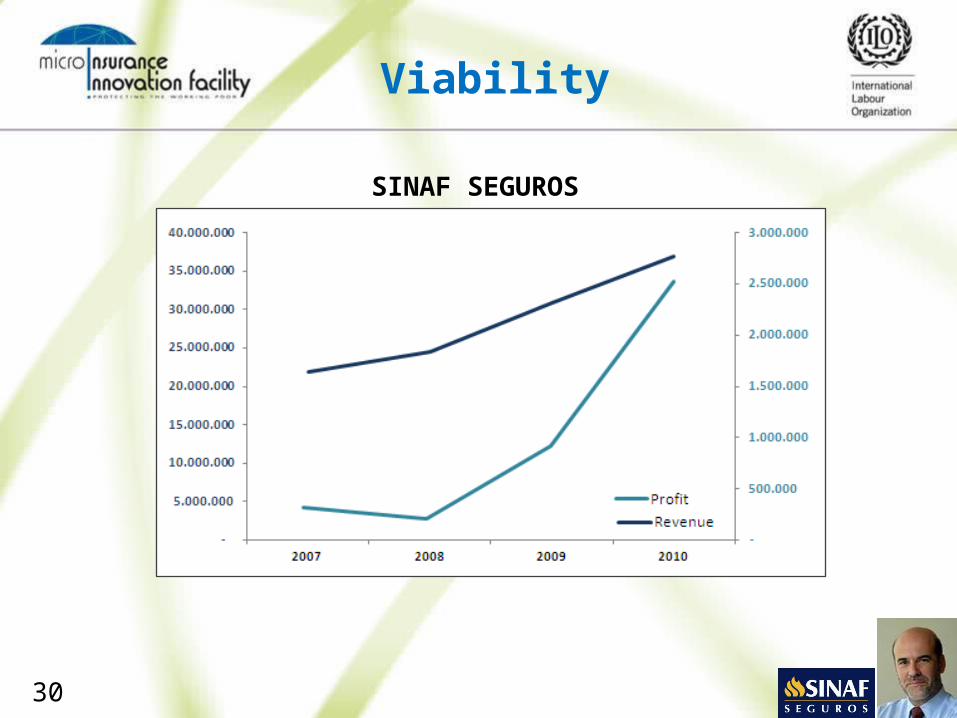

Viability

SINAF SEGUROS

31

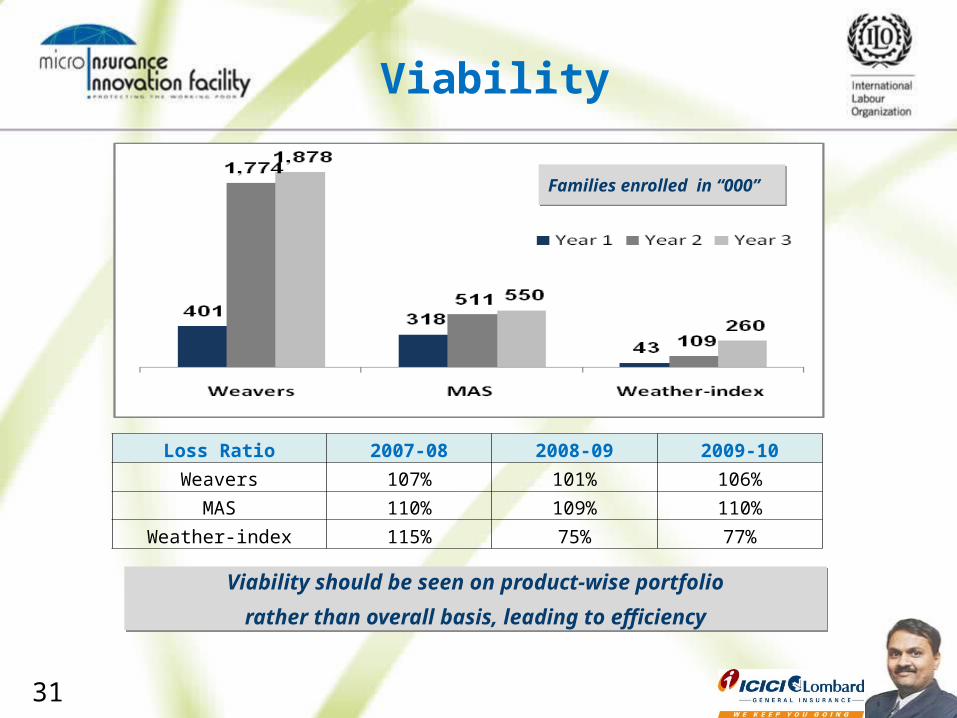

Viability should be seen on product-wise portfoliorather than overall basis, leading to efficiency

Viability

Families enrolled in “000”

Loss Ratio 2007-08 2008-09 2009-10Weavers 107% 101% 106%

MAS 110% 109% 110%Weather-index 115% 75% 77%

32

WEBINAR ON

The Viability of Microinsurance

Presenter:Craig ChurchillTeam Leader

Microinsurance Innovation FacilityPresenter:

Alok AgarwalExecuitve Director

ICICI LombardIndia

Presenter:Pedro Bulcão

Chief Executive Officer Sinaf Seguros

Brazil

Moderator:Jasmin Suministrado

Knowledge OfficerMicroinsurance Innovation Facility

ON Q&A