20 mwf pp ch 02(d-1) cleared

DESCRIPTION

Powerpoint.TRANSCRIPT

2

Managers’ Responsibilities

Copyright © 2015 Pearson Education, Inc.

LearnImprove

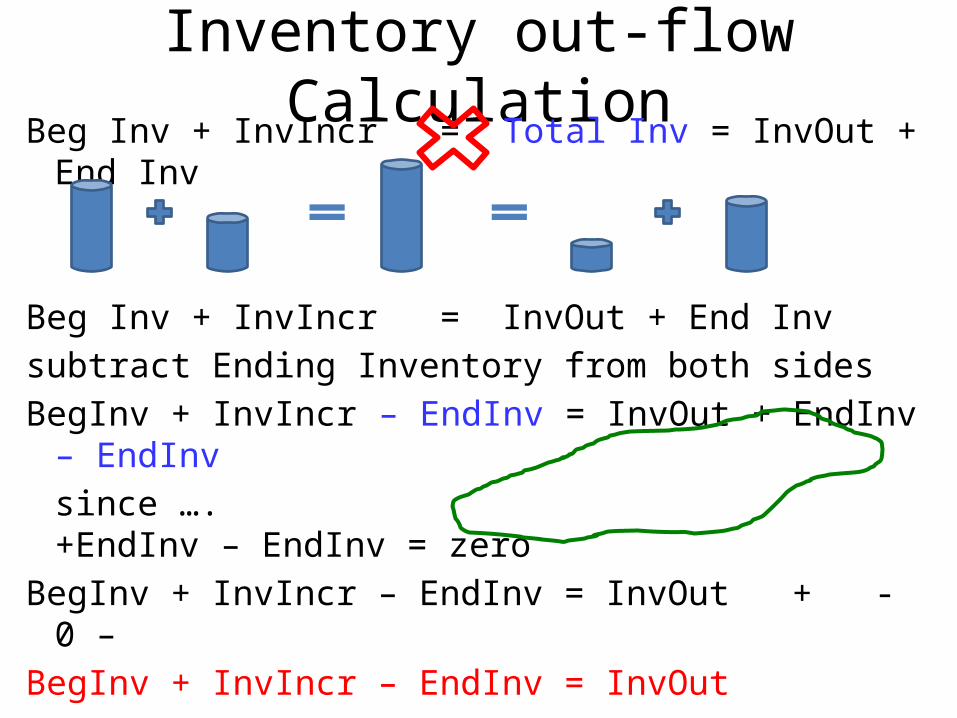

Inventory out-flow CalculationBeg Inv + InvIncr = Total Inv = InvOut + End Inv

Beg Inv + InvIncr = InvOut + End Inv subtract Ending Inventory from both sides BegInv + InvIncr – EndInv = InvOut + EndInv – EndInv

since …. +EndInv – EndInv = zeroBegInv + InvIncr – EndInv = InvOut + - 0 –BegInv + InvIncr – EndInv = InvOut

4

Cost of Goods Sold Schedule & Formula

+ Beginning finished goods inventory + BegFG+ Cost of goods manufactured +

CofGM= Cost of goods available for sale– Ending finished goods inventory - EndFG= Cost of goods sold = CofGS

BegFG + CofGM – EndFG = CofGS

Copyright © 2015 Pearson Education, Inc.

Pg 67

5

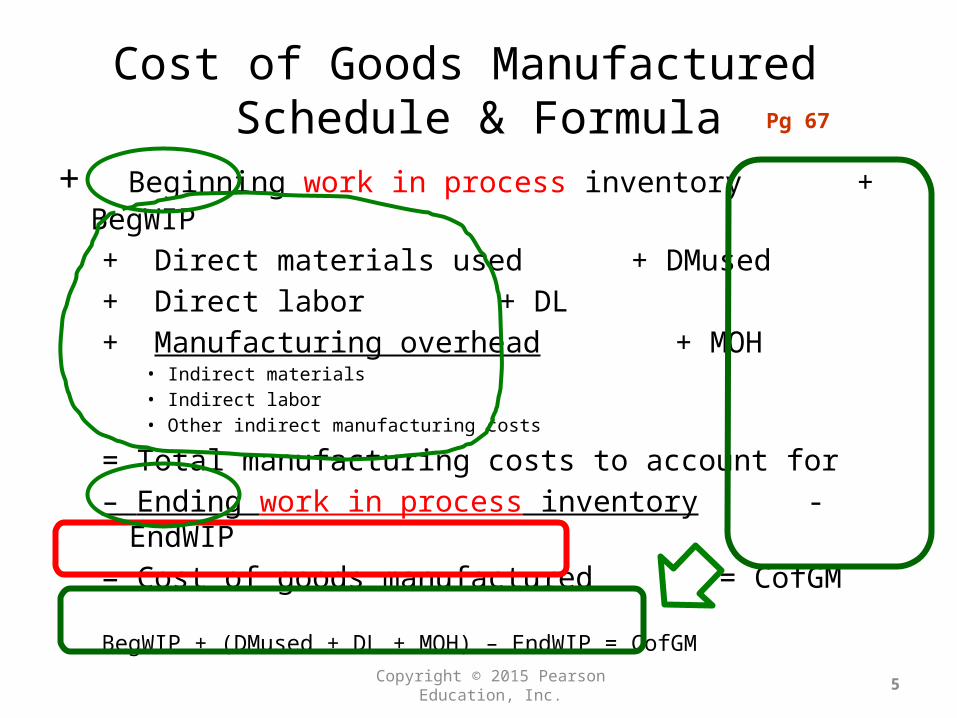

Cost of Goods Manufactured Schedule & Formula

+ Beginning work in process inventory + BegWIP+ Direct materials used + DMused+ Direct labor + DL+ Manufacturing overhead + MOH

• Indirect materials• Indirect labor• Other indirect manufacturing costs

= Total manufacturing costs to account for– Ending work in process inventory - EndWIP= Cost of goods manufactured = CofGM

BegWIP + (DMused + DL + MOH) – EndWIP = CofGM

Copyright © 2015 Pearson Education, Inc.

Pg 67

6

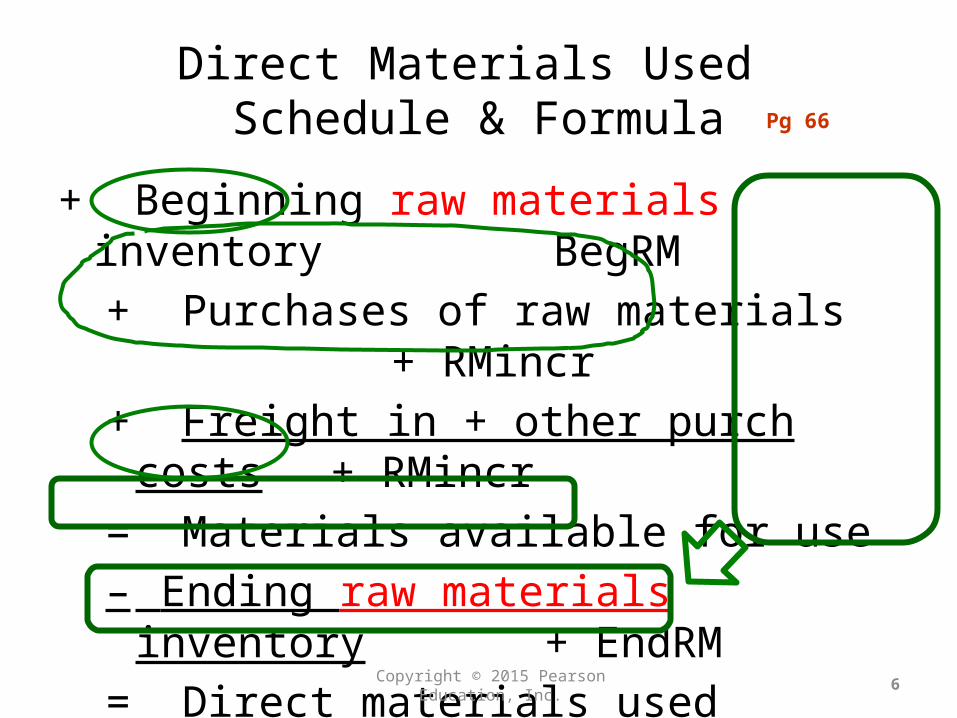

Direct Materials Used Schedule & Formula

+ Beginning raw materials inventory BegRM+ Purchases of raw materials + RMincr+ Freight in + other purch costs + RMincr= Materials available for use– Ending raw materials inventory + EndRM= Direct materials used = DMused

BegRM + (RMPurch + Frt) – EndRM = DMU

Copyright © 2015 Pearson Education, Inc.

Pg 66

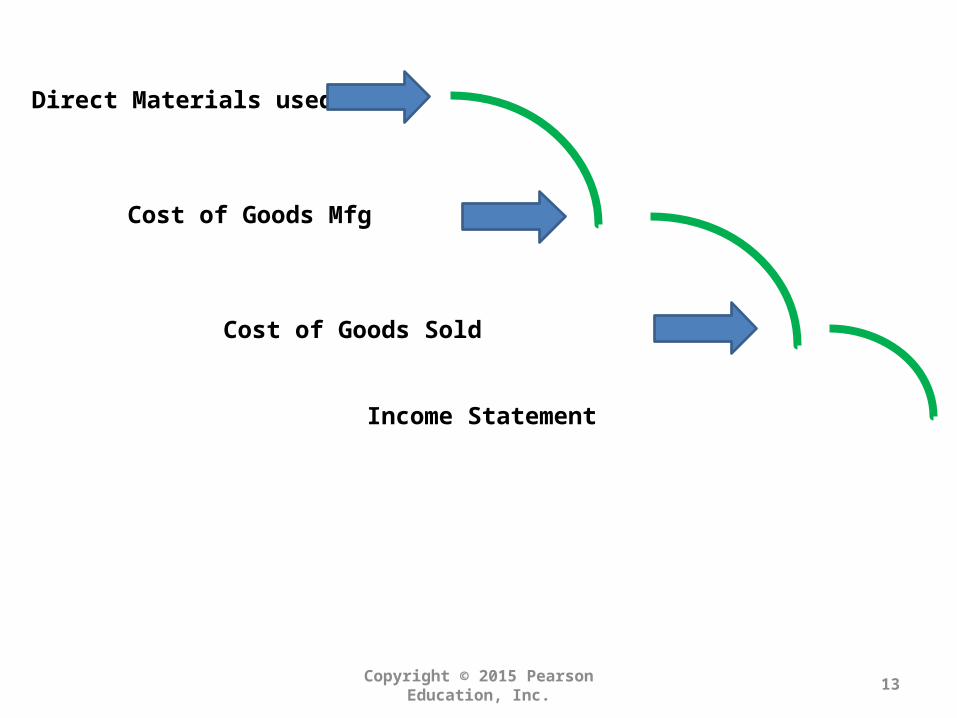

7Copyright © 2015 Pearson Education, Inc.

Direct Materials used

Cost of Goods Mfg

Cost of Goods Sold

Income Statement

DM UsedBegInv + InvIncr – EndInv = CofGMfg

CofGS

Cost Flows Visualized (Exhibit 2-7)

2015 Fall(c-1)

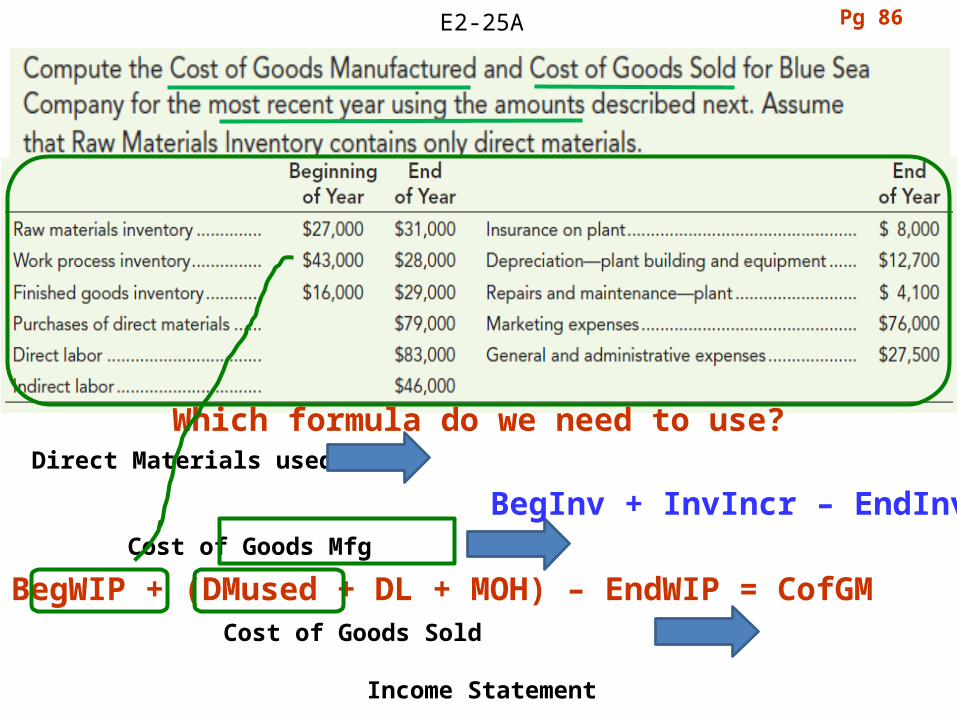

E2-25A Pg 86

Which formula do we need to use?Direct Materials used

Cost of Goods Mfg

Cost of Goods Sold

Income Statement

BegWIP + (DMused + DL + MOH) – EndWIP = CofGM

BegInv + InvIncr – EndInv

Computation of Direct Materials Used

Direct materials used:Beginning raw materials inventory

Purchases of direct materialsImport duties

Freight-inDirect materials available for useEnding raw materials inventoryDirect materials used

E2-25(a)

Beg + Incr – Ending .. of ??http://www.wavsource.com/snds_2015-08-23_2824562050165472/movies/wizard/melting2.wav

Pg 86Direct Materials Used

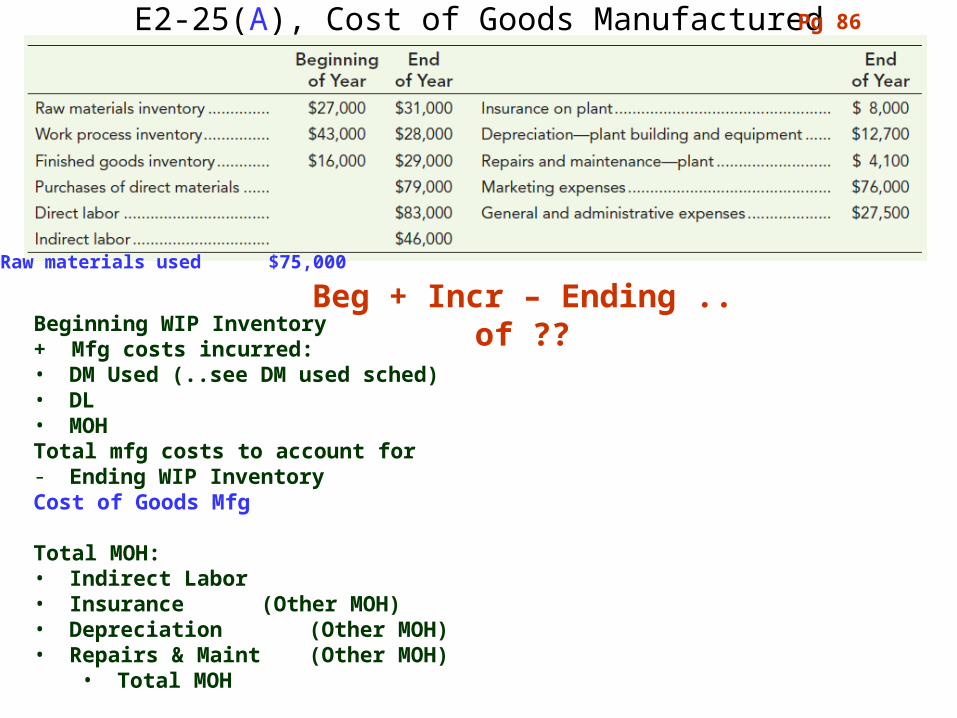

E2-25(A), Cost of Goods Manufactured

Beginning WIP Inventory+ Mfg costs incurred:• DM Used (..see DM used sched)• DL• MOHTotal mfg costs to account for- Ending WIP InventoryCost of Goods Mfg

Total MOH:• Indirect Labor• Insurance (Other MOH)• Depreciation (Other MOH)• Repairs & Maint (Other MOH)

• Total MOH

Beg + Incr – Ending .. of ??Raw materials used $75,000

Pg 86

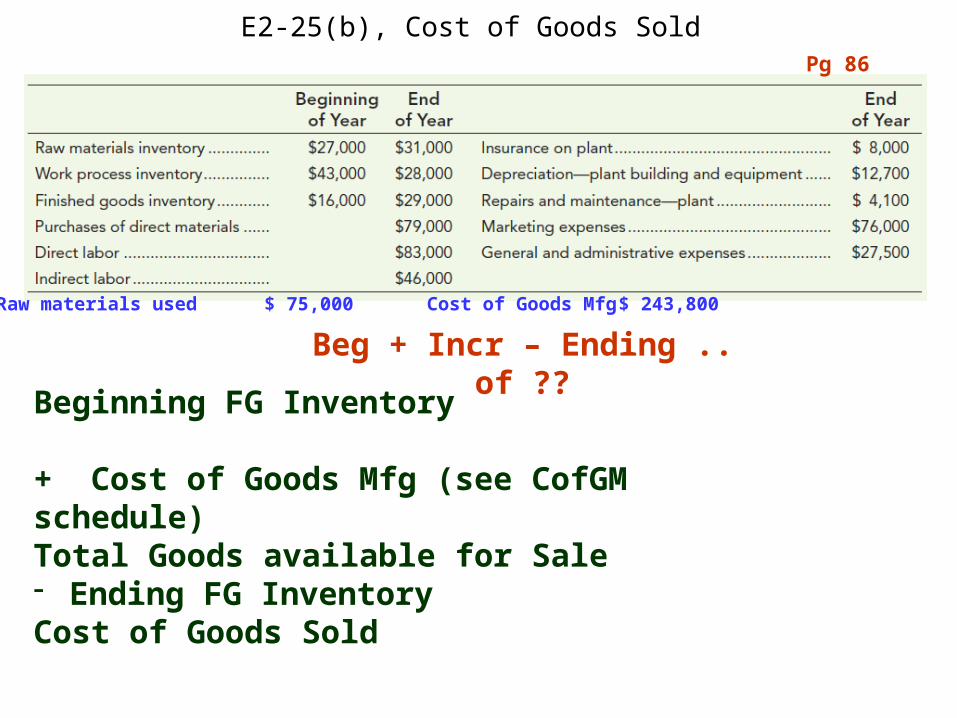

E2-25(b), Cost of Goods Sold

Beginning FG Inventory

+ Cost of Goods Mfg (see CofGM schedule)Total Goods available for Sale- Ending FG InventoryCost of Goods Sold

Beg + Incr – Ending .. of ??Raw materials used $ 75,000 Cost of Goods Mfg $ 243,800

Pg 86

13Copyright © 2015 Pearson Education, Inc.

Direct Materials used

Cost of Goods Mfg

Cost of Goods Sold

Income Statement

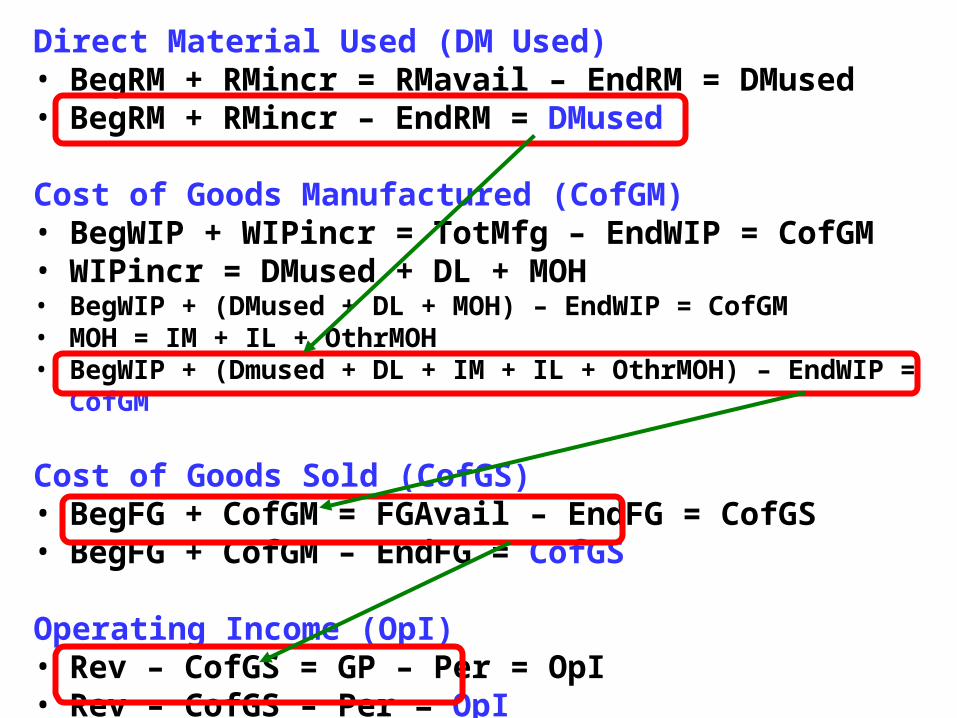

Direct Material Used (DM Used)• BegRM + RMincr = RMavail – EndRM = DMused• BegRM + RMincr – EndRM = DMused

Cost of Goods Manufactured (CofGM)• BegWIP + WIPincr = TotMfg – EndWIP = CofGM• WIPincr = DMused + DL + MOH• BegWIP + (DMused + DL + MOH) – EndWIP = CofGM• MOH = IM + IL + OthrMOH• BegWIP + (Dmused + DL + IM + IL + OthrMOH) – EndWIP = CofGM

Cost of Goods Sold (CofGS)• BegFG + CofGM = FGAvail – EndFG = CofGS• BegFG + CofGM – EndFG = CofGS

Operating Income (OpI)• Rev – CofGS = GP – Per = OpI• Rev – CofGS – Per = OpI

Using the formulas to solve a problem• BegRM + RMincr – EndRM = DMused• BegWIP + (DMused + DL + IM + IL + OthrMOH) – EndWIP = CofGMfg• BegFG + CofGMfg – EndFG = CofGS• Sales – CofGS – Per = OpI

Use DMused formula to solve for Ending Raw Material inventory(EndRM)• BegRM + RMincr – EndRM = DMused

• since EndRM = EndRM … add EndRM to both sides

• BegRM + RMincr – EndRM + EndRM = Dmused + EndRM

since -EndRM + EndRM = 0 so substitute zero in the formula• BegRM + RMincr + 0 = DMused + EndRM

• BegRM + RMincr = DMused + EndRM• since DMused = DMused .. subtract DMused from both sides

• BegRM + RMincr – DMused = DMused – DMused + EndRM• +DMused – DMused = 0 so substitute -0- in the formula

• BegRM + RMincr – DMused = 0 + EndRM

• BegRM + RMincr – DMused = EndRM

Pg 87

Direct Materials used = BegRM + (RMPurch+FrtIn+Duties)-EndRMCost of Goods Mfg = BegWIP+DMused+DL+(IM+IL+OMOH)-EndWIP

Cost of Goods Sold = BegFG + CofGMfg - EndFGIncome Statement Rev – CofGS = GP – Per = OpI

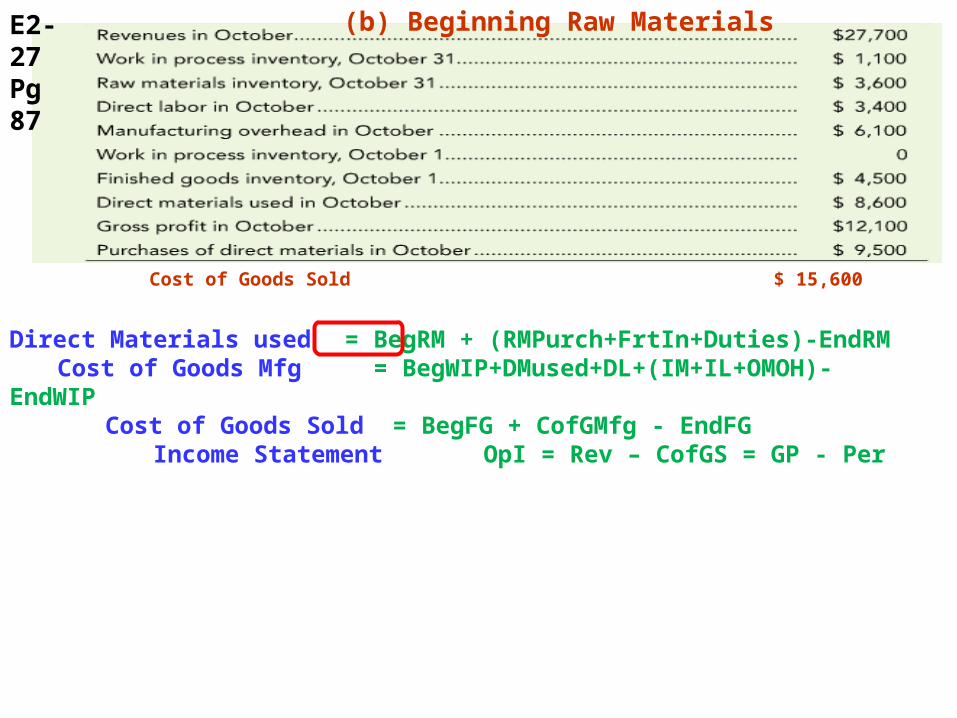

(a) Cost of Goods SoldE2-27Pg 87

Direct Materials used = BegRM + (RMPurch+FrtIn+Duties)-EndRMCost of Goods Mfg = BegWIP+DMused+DL+(IM+IL+OMOH)-EndWIP

Cost of Goods Sold = BegFG + CofGMfg - EndFGIncome Statement OpI = Rev – CofGS = GP - Per

(b) Beginning Raw MaterialsE2-27Pg 87

Cost of Goods Sold $ 15,600

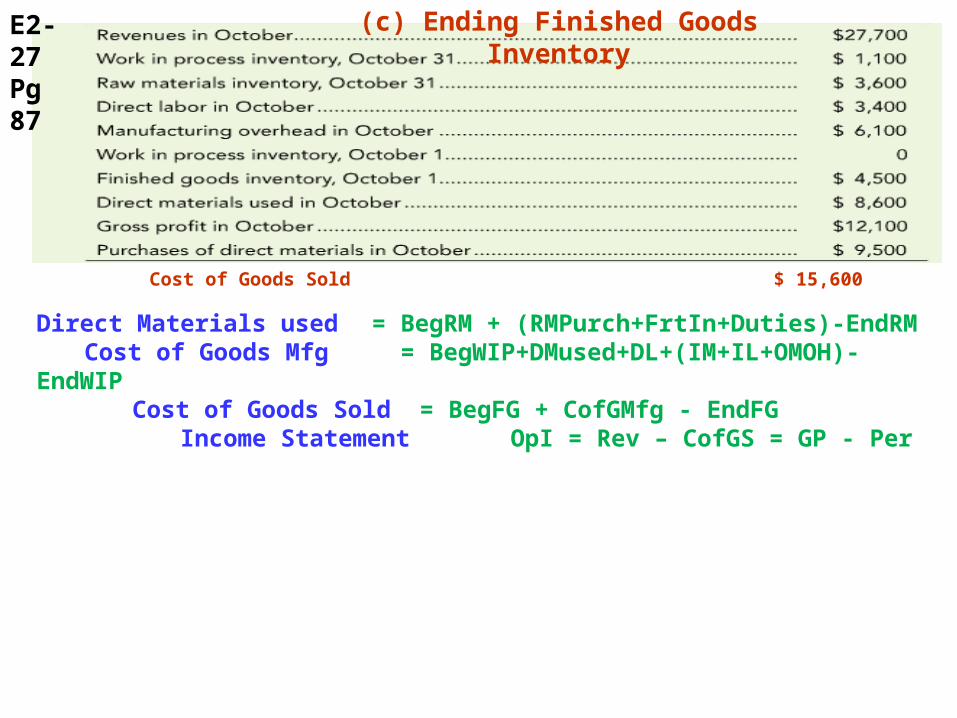

(c) Ending Finished Goods InventoryE2-27Pg 87

Direct Materials used = BegRM + (RMPurch+FrtIn+Duties)-EndRMCost of Goods Mfg = BegWIP+DMused+DL+(IM+IL+OMOH)-EndWIP

Cost of Goods Sold = BegFG + CofGMfg - EndFGIncome Statement OpI = Rev – CofGS = GP - Per

Cost of Goods Sold $ 15,600

20

Cost Behavior

Variable costs Change in total cost in direct proportion to changes in volume

Fixed costs Stay constant in total cost over a wide range of activity levels

Copyright © 2015 Pearson Education, Inc.

Cost behavior—how costs change as volume changes.

What are some examples of Variable costs?What are some examples of Fixed costs?

21

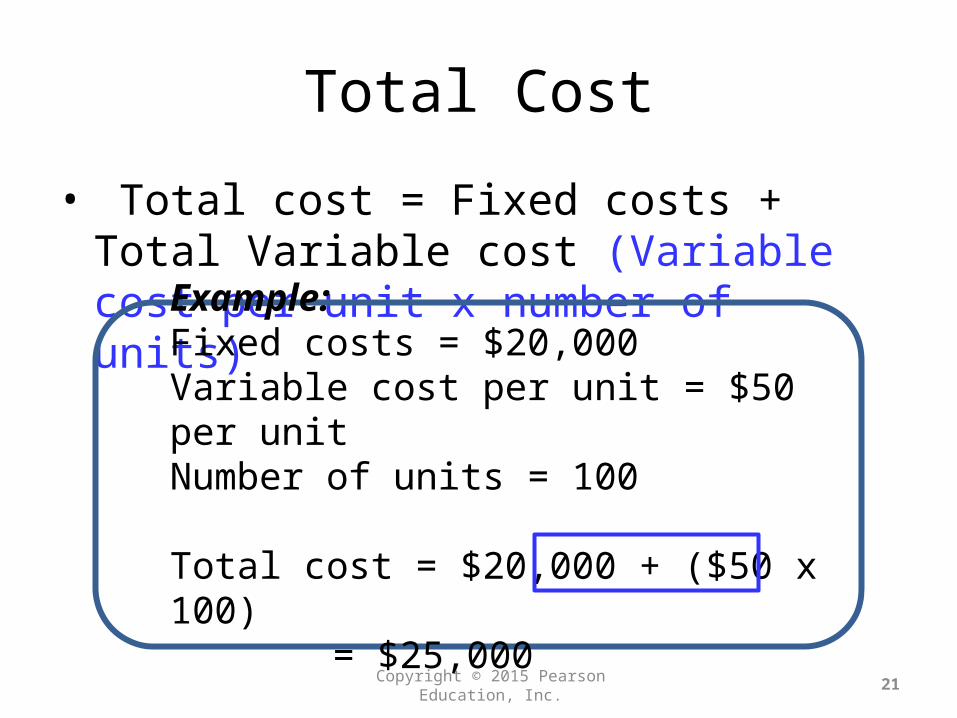

Total Cost

• Total cost = Fixed costs + Total Variable cost (Variable cost per unit x number of units)

Example:Fixed costs = $20,000Variable cost per unit = $50 per unitNumber of units = 100

Total cost = $20,000 + ($50 x 100) = $25,000

Copyright © 2015 Pearson Education, Inc.

Cost Behavior SummarizedTotal Dollars Cost per Unit

Variable Costs

Change in proportion with

outputMore output = More cost

Fixed Costs Unchanged in relation to output

Change inversely with

outputMore output = lower

cost per

unit

Total Dollars Cost Per Unit

Variable Costs

Change in proportion with

outputMore output = More

cost

Unchanged in relation to

output

Fixed Costs

Unchanged in relation to

output

Change inversely with

outputMore output = lower

cost per unit

222-

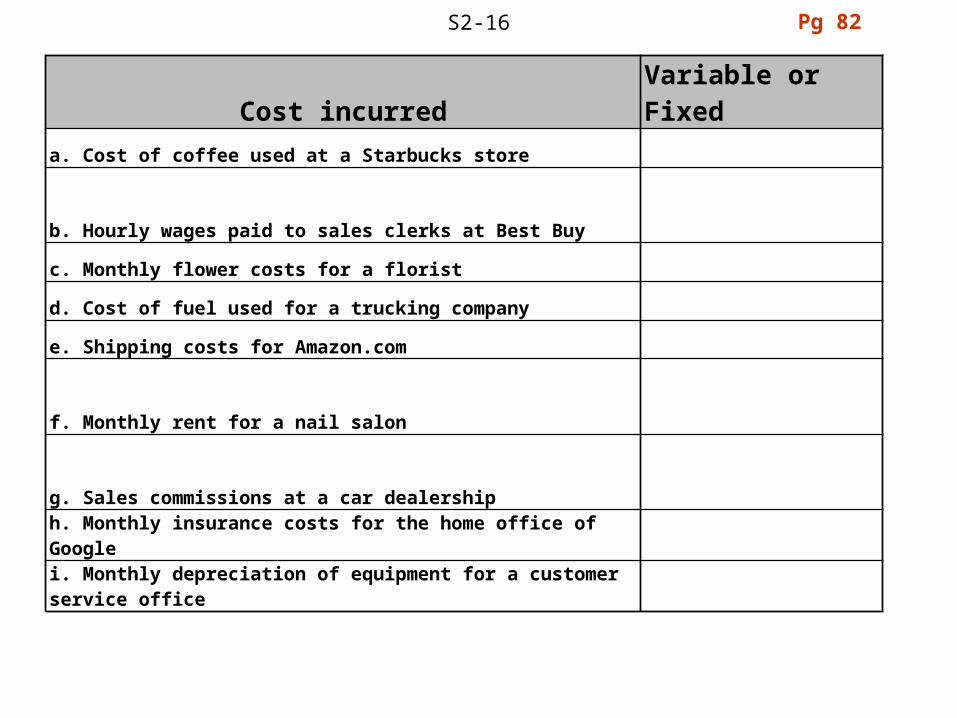

S2-16

Cost incurred Variable or Fixeda. Cost of coffee used at a Starbucks store

b. Hourly wages paid to sales clerks at Best Buy

c. Monthly flower costs for a florist

d. Cost of fuel used for a trucking company

e. Shipping costs for Amazon.com

f. Monthly rent for a nail salon

g. Sales commissions at a car dealership

h. Monthly insurance costs for the home office of Google

i. Monthly depreciation of equipment for a customer service office

Pg 82

S2-16 (continued)

Cost incurred Variable or Fixedj. Cost of fabric used at a clothing manufacturer

k. Cost of fruit sold at a grocery store

l. Monthly office lease costs for a CPA firm

m. Monthly cost of French fries at a McDonald’s restaurant

n. Property taxes for a restaurant

o. Depreciation of exercise equipment at the YMCA

Pg 82

Multiple Classifications of Costs

• Costs may be classified as:– Direct/Indirect, and – Variable/Fixed

• These multiple classifications give rise to important cost combinations:– Direct and variable– Direct and fixed– Indirect and variable– Indirect and fixed

252-

26

Controllable vs Uncontrollable Relevant vs Irrelevant Costs

Controllable Management can influence or change cost

Uncontrollable Management cannot change or influence cost in the short run

Copyright © 2015 Pearson Education, Inc.

Relevant Differential costs, which are costs that differ between alternatives

IrrelevantCosts that do not differ between alternativesorSunk costs – costs incurred in the past that cannot be changed

E2-28 pg 87

Cost incurred relevant/irrelevanta. The interest rate paid on invested funds, when deciding how much inventory to keep on-hand

b. Cost of computers purchased 6 months ago, when deciding whether to upgrade to computers with faster processing speedc. The property tax rates in different locales, when deciding where to locate the company’s headquartersd. The type of fuel (gas or diesel) used by delivery vans, when deciding which make and model of van to purchase for the company’s delivery van fleet.e. Cost of operating automated production machinery versus the cost of direct labor, when deciding whether to automate production.

f. The fair market value of old manufacturing equipment when deciding whether or not to replace it with newer equipment.g. Cost of purchasing packaging materials from an outside vendor, when deciding whether to continue manufacturing the packaging materials in-house.h. Depreciation expense on old manufacturing equipment when deciding whether or not to replace it with newer equipment.i. The cost of land purchased 3 years ago, when deciding whether to build on the land now or wait two more years before building.