accion presentation

TRANSCRIPT

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 1/23

ACCIONACCIONInternationalInternationalPoverty Assessment Tool:

Depth of Outreach

SEEP Poverty Assessment Working Group

May 6, 2004

Karen Horn Welch & Patty Lee Devaney

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 2/23

Introduction & ObjectivesIntroduction & Objectives

Brief review of ACCIONs poverty

assessment tool and methodology

Project update

Introduction

Time & cost

Data collection & analysis

Misreporting or data manipulation

Adaptation

Key findings from our poverty assessments

of Mibanco, Peru and SOGESOL, Haiti

Discussion

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 3/23

ACCION poverty ACCION poverty

Assessment ToolAssessment Tool

Based on household-level incomeand expenditure data

Evaluate the absolute poverty level

of MFI clients in comparison withthe national/regional populations.

Examine relationship betweenpoverty and demographic, socio-economic, and loan data

Conduct validation surveys

Monitor poverty on an on-goingbasis

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 4/23

ACCION poverty ACCION poverty

Assessment ToolAssessment Tool

Phase 1: Analysis of MIS data from loan application

Phase 2: Conduct validation surveys

Phase 3: Write poverty assessment report (examining therelationship between poverty and demographic, socio-economic, and loan data)

Phase 4: Implement on-going Poverty Outreach Report

Phase 5: Track poverty outreach over time; understand

client characteristics based on their poverty levels

Phase 6: Develop products to increase outreach to the poor

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 5/23

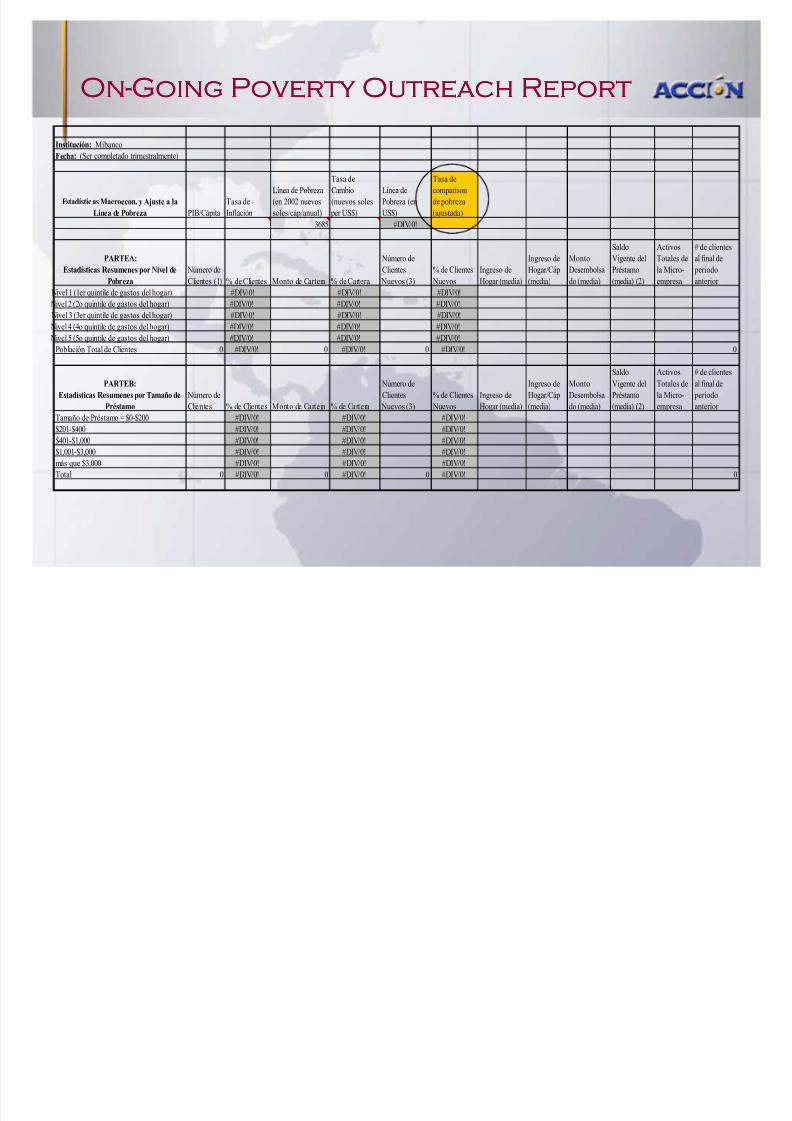

OnOn--Going Poverty Outreach ReportGoing Poverty Outreach Report

Institución: Mibanco

Fecha: (Ser completado trimestralmente)

Estadísticas Macroecon. y Ajuste a la

Línea de Pobreza PIB/Cápita

Tasa de

Inflación

Línea de Pobreza

(en 2002 nuevos

soles/cáp/anual)

Tasa de

Cambio

(nuevos soles

per US$)

Línea de

Pobreza (en

US$)

Tasa de

comparison

de pobreza

(ajustada)

3685 #DIV/0!

PARTEA:

Estadísticas R esumenes por Nivel de

Pobreza Número deClientes (1) % de Clientes Monto de Cartera % de Cartera

Número de

Clientes Nuevos (3)

% de Clientes Nuevos

Ingreso deHogar (media)

Ingreso de

Hogar/Cáp(media)

Monto

Desembolsado (media)

Saldo

Vigente del

Préstamo(media) (2)

Activos

Totales de

la Micro-empresa

# de clientes

al final de

periodoanterior

Nivel 1 (1er quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 2 (2o quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 3 (3er quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 4 (4o quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 5 (5o quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Población Total de Clientes 0 #DIV/0! 0 #DIV/0! 0 #DIV/0! 0

PARTEB:

Estadísticas R esumenes por Tamaño de

Préstamo

Número de

Clientes % de Clientes Monto de Cartera % de Cartera

Número de

Clientes

Nuevos (3)

% de Clientes

Nuevos

Ingreso de

Hogar (media)

Ingreso de

Hogar/Cáp

(media)

Monto

Desembolsa

do (media)

Saldo

Vigente del

Préstamo

(media) (2)

Activos

Totales de

la Micro-

empresa

# de clientes

al final de

periodo

anterior

Tamaño de Préstamo = $0-$200 #DIV/0! #DIV/0! #DIV/0!

$201-$400 #DIV/0! #DIV/0! #DIV/0!

$401-$1,000 #DIV/0! #DIV/0! #DIV/0!

$1,001-$3,000 #DIV/0! #DIV/0! #DIV/0!

más que $3,000 #DIV/0! #DIV/0! #DIV/0!

Total 0 #DIV/0! 0 #DIV/0! 0 #DIV/0! 0

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 6/23

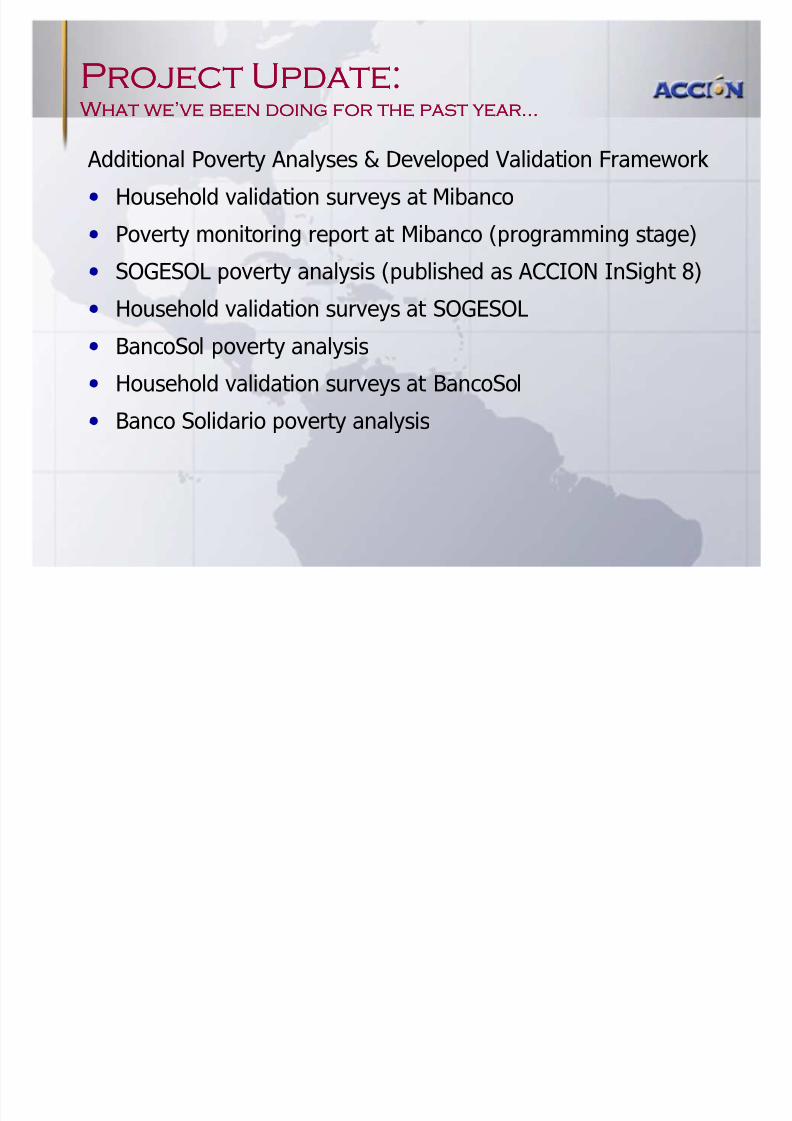

Project Update:Project Update: What we¶ve been doing for the past year« What we¶ve been doing for the past year«

Additional Poverty Analyses & Developed Validation Framework

Household validation surveys at Mibanco

Poverty monitoring report at Mibanco (programming stage)

SOGESOL poverty analysis (published as ACCION InSight 8)

Household validation surveys at SOGESOL

BancoSol poverty analysis

Household validation surveys at BancoSol

Banco Solidario poverty analysis

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 7/23

IntroductionIntroduction

Why did ACCION pursue apoverty measurement tool?

MFI driven: Missions andcompetition

Legislation

Poverty distinctions:

Poor/ non-poor, based onpertinent poverty line

Poverty distribution (1-5)

5 NSE levels (A-E)

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 8/23

Time & CostTime & Cost

Phase 1: Analysis of MIS datafrom loan application

- ACCION Staff: 12 days

- MFI Staff: 5 days

- MFI Management: N/A

- Clients: N/A

Phase 2: Validation surveys

ACCION Staff: 15 days

MFI Staff: 4 days MFI Management: 1 day

Survey Firm: 30 days

Clients: 400 hours

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 9/23

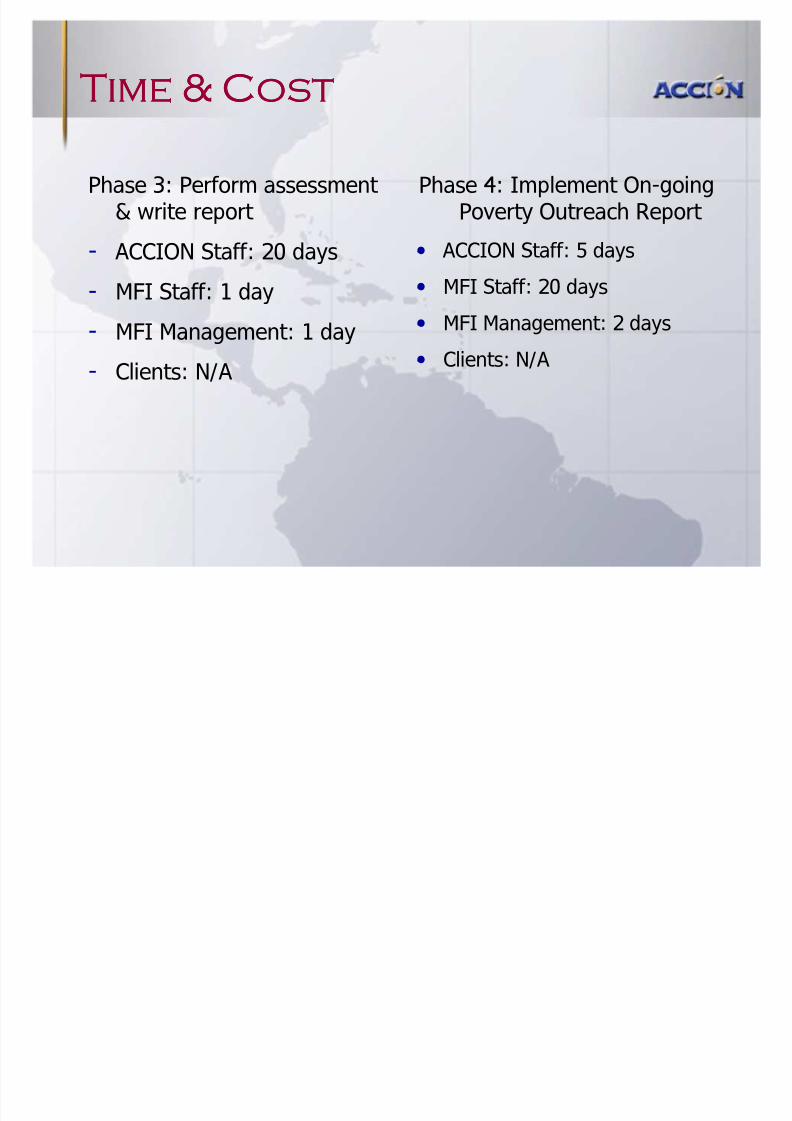

Time & CostTime & Cost

Phase 3: Perform assessment & write report

- ACCION Staff: 20 days

- MFI Staff: 1 day

- MFI Management: 1 day

- Clients: N/A

Phase 4: Implement On-goingPoverty Outreach Report

ACCION Staff: 5 days

MFI Staff: 20 days

MFI Management: 2 days

Clients: N/A

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 10/23

Time & CostTime & Cost

Phase 5: Track MFI povertyoutreach over time

- ACCION Staff: 1 day perquarter

- MFI Staff: .5 days perquarter

- MFI Management: .5 daysper quarter

- Clients: N/A

Phase 6: Product development

ACCION Staff: variable

MFI Staff: variable MFI Management: variable

Clients: variable (may involvefocus groups)

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 11/23

Total BudgetTotal Budget

Costs:ACC ION Poverty Assessment Tool:

Estimated Costs of Adaption, Validation, Implementation, and O n-Going Use

Adaption V alidation Testing Implementation

On-Going Use

(Annual)

Cost Category

I. Personnel $6,400 $2,250 $19,350 $6,800

Including ACCION an d MFI staff

II. Travel, Transportation & Per Diem $2,400 $2,000 $2,400 -

III. Other

Validation survey firm - $10,000 - -

TOTAL ESTIMATED COST $8,800 $14,250 $21,750 6,800$

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 12/23

Frequency: Every time loan data iscollected (baseline data); once everythree years (validation surveys)

Who analyzes the data? MFI management & staff; ACCION poverty team

Feedback: Collaborative process continuous feedback

Decision-making

Early buy-in & frequent interaction with

senior management (commercialmanager) ensures their engagement

Poverty Outreach Report quarterlyreview of results (similar to financialreporting)

Balanced scorecard

Product development

Data Collection &Data Collection &

AnalysisAnalysis

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 13/23

The tool is based on standard loanapplication process

Asking for info pertaining directly to

microenterprise (hh size; income andexpenditure)

Bias clients wanting a bigger loan(overstate income & understateexpenditure)

Validation surveys were meant toovercome the risk of misreporting

Misreporting /Misreporting /

DataManipulationDataManipulation

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 14/23

Validation surveys revealed different results than the originalMIS data.

In asking questions for different purposes, were getting different

answers Loan application gathers information focusing on microenterprise

Validation survey gathers information focusing on entire household

How can we use the results?

We can use the original loan application data for tracking trends anddistribution of poverty (based on expenditure) within the client population

Harder to pinpoint where clients fall relative to the poverty linewithout making an adjustment to the original data

Misreporting /Misreporting /

DataManipulationDataManipulation

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 15/23

Validation FrameworkValidation Framework

Objectives

Assess validity of originalresults

Quantify the differencebetween loan applicationdata & LSMS-type data

Determine an adjustment

factor Sample selection

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 16/23

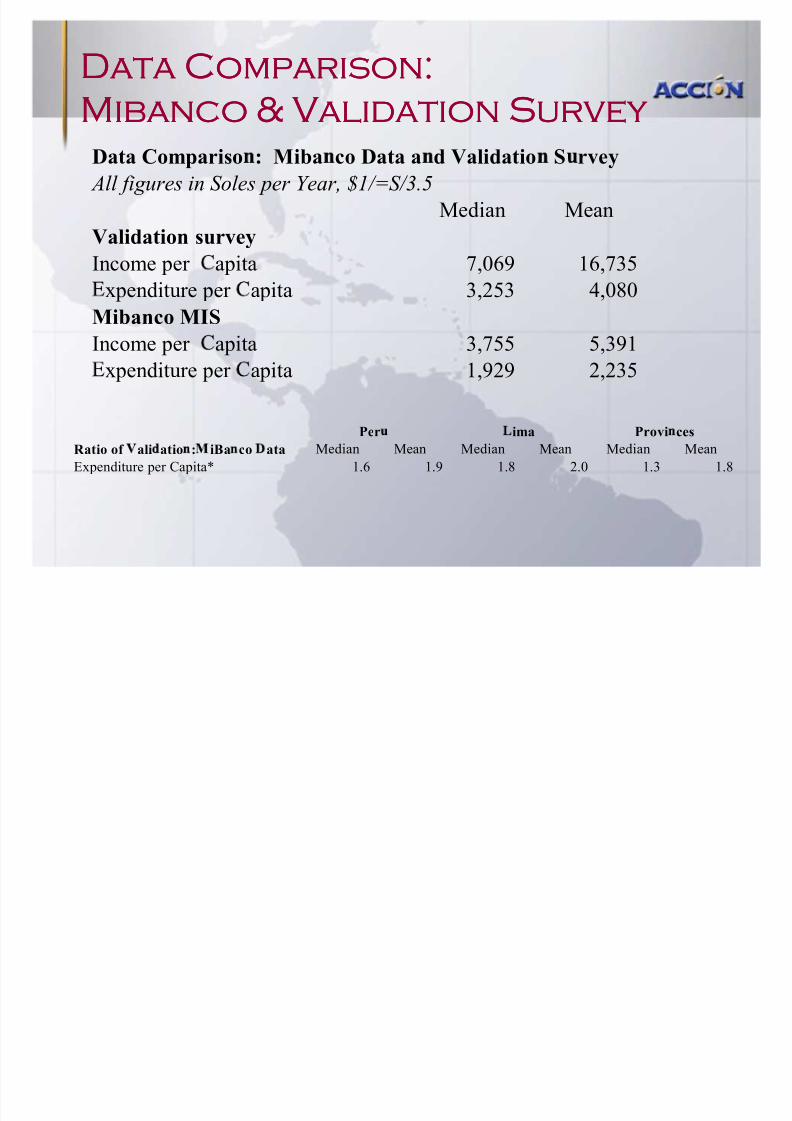

Data Comparison:Data Comparison:

Mibanco & Validation Survey Mibanco & Validation Survey

R atio of ali atio : iBa co ata Median Mean Median Mean Median Mean

Expenditure per Capita* 1.6 1.9 1.8 2.0 1.3 1.8

Per ima Provi ces

Data Compariso : Miba co Data a d Validatio S rvey

All figures in Soles per Year, $1/=S/3.5

Median Mean

Validation survey

Income per apita 7,069 16,735 xpenditure per apita 3,253 4,080

Mibanco MIS

Income per apita 3,755 5,391

xpenditure per apita 1,929 2,235

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 17/23

Data Comparison:Data Comparison:

SOGESOL & Validation Survey SOGESOL & Validation Survey Data Comparison: SOGESOL Data and Validation Survey

All figures are in Gourdes per Year, $1=43g

Median Mean

Validation Survey

Income per apita 103,880 146,358 xpenditure per apita 32,848 50,591

SOGESOL MIS

Income per apita 88,500 196,270

xpenditure per apita 12,000 15,393

Haiti-Port au Prince

Ratio of Validation:SOGESOL Data

Median Mean

Income per apita 1.1 1.9

xpenditure per apita 3.0 4.0

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 18/23

ConsiderationsConsiderations

Adjustment Methodology

Assumptions

Relatively small adjustment factor

Constant variance of adjustment factor across households

Findings

Larger than expected adjustment factor

Wider variance

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 19/23

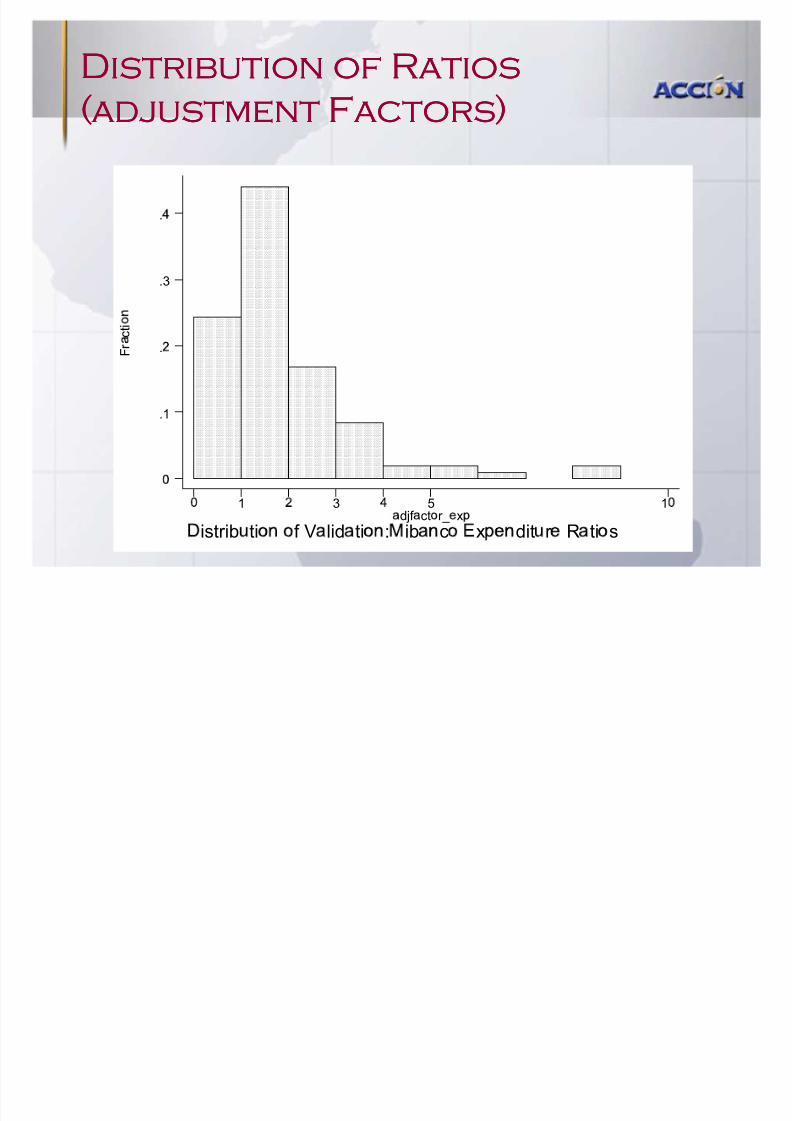

Distribution of RatiosDistribution of Ratios

(adjustment Factors)(adjustment Factors)

F r

c t i

istrib ti f V lid ti : ib c x dit r R ti s

djf ct r_ x1 3 5 1

.1

.

.3

.

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 20/23

ResultsResults --MibancoMibanco

Poverty Measure Adjustment Factor Poverty Rate

1. Individual, household-leveladjustment

HH-specific adjustmentfactor

33%

2. Household-level median adj.

Factor

Lima=1.8

Provinces=1.3

30%

Constant adjustment factor

limited impact on overall poverty rate

cannot accurately classify individual households by povertylevel

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 21/23

Getting back to theGetting back to the

original question«original question«

Given data considerations, how can we accurately track and definethe poverty level of microfinance clients?

Use a constant adjustment factor to the household expenditures

for one portion of the Poverty Outreach Report We can estimate the percentage of the client population above and

below the poverty line with a good degree of certainty

Report unadjusted data for the remainder of the report

Maintains the true distribution of client expenditure and associatedcharacteristics for analysis within the MFI (practical for MFIs purposes)

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 22/23

OnOn--Going Poverty Outreach ReportGoing Poverty Outreach Report

Institución: Mibanco

Fecha: (Ser completado trimestralmente)

Estadísticas Macroecon. y Ajuste a la

Línea de Pobreza PIB/Cápita

Tasa de

Inflación

Línea de Pobreza

(en 2002 nuevos

soles/cáp/anual)

Tasa de

Cambio

(nuevos soles

per US$)

Línea de

Pobreza (en

US$)

Tasa de

comparison

de pobreza

(ajustada)

3685 #DIV/0!

PARTEA:

Estadísticas R esumenes por Nivel de Pobreza

Número deClientes (1) % de Clientes Monto de Cartera % de Cartera

Número de

Clientes Nuevos (3)

% de Clientes Nuevos

Ingreso deHogar (media)

Ingreso de

Hogar/Cáp(media)

Monto

Desembolsado (media)

Saldo

Vigente del

Préstamo(media) (2)

Activos

Totales de

la Micro-empresa

# de clientes

al final de

periodoanterior

Nivel 1 (1er quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 2 (2o quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 3 (3er quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 4 (4o quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Nivel 5 (5o quintile de gastos del hogar) #DIV/0! #DIV/0! #DIV/0!

Población Total de Clientes 0 #DIV/0! 0 #DIV/0! 0 #DIV/0! 0

PARTEB:

Estadísticas R esumenes por Tamaño de

Préstamo

Número de

Clientes % de Clientes Monto de Cartera % de Cartera

Número de

Clientes

Nuevos (3)

% de Clientes

Nuevos

Ingreso de

Hogar (media)

Ingreso de

Hogar/Cáp

(media)

Monto

Desembolsa

do (media)

Saldo

Vigente del

Préstamo

(media) (2)

Activos

Totales de

la Micro-

empresa

# de clientes

al final de

periodo

anterior Tamaño de Préstamo = $0-$200 #DIV/0! #DIV/0! #DIV/0!

$201-$400 #DIV/0! #DIV/0! #DIV/0!

$401-$1,000 #DIV/0! #DIV/0! #DIV/0!

$1,001-$3,000 #DIV/0! #DIV/0! #DIV/0!

más que $3,000 #DIV/0! #DIV/0! #DIV/0!

Total 0 #DIV/0! 0 #DIV/0! 0 #DIV/0! 0

8/7/2019 ACCION Presentation

http://slidepdf.com/reader/full/accion-presentation 23/23

DiscussionDiscussion