acg european capital tour: investing pitfalls / lessons learned and big success stories

TRANSCRIPT

ACG EUROPEAN CAPITAL TOUR KEY NOTE PRESENTATION

TOPICS

1

I. Alvarez & Marsal Perspectives on the Current State of European Market [Sovereign / PE / Distress]

II. Middle Market Opportunities III. Pitfalls [Do’s and Don’ts]

ALVAREZ & MARSAL ROUTES TO MARKET & VERTICALS

2

Ø Restructuring

Ø Private Equity

Ø Corporate

Ø Financial Institutions

Ø Real Estate

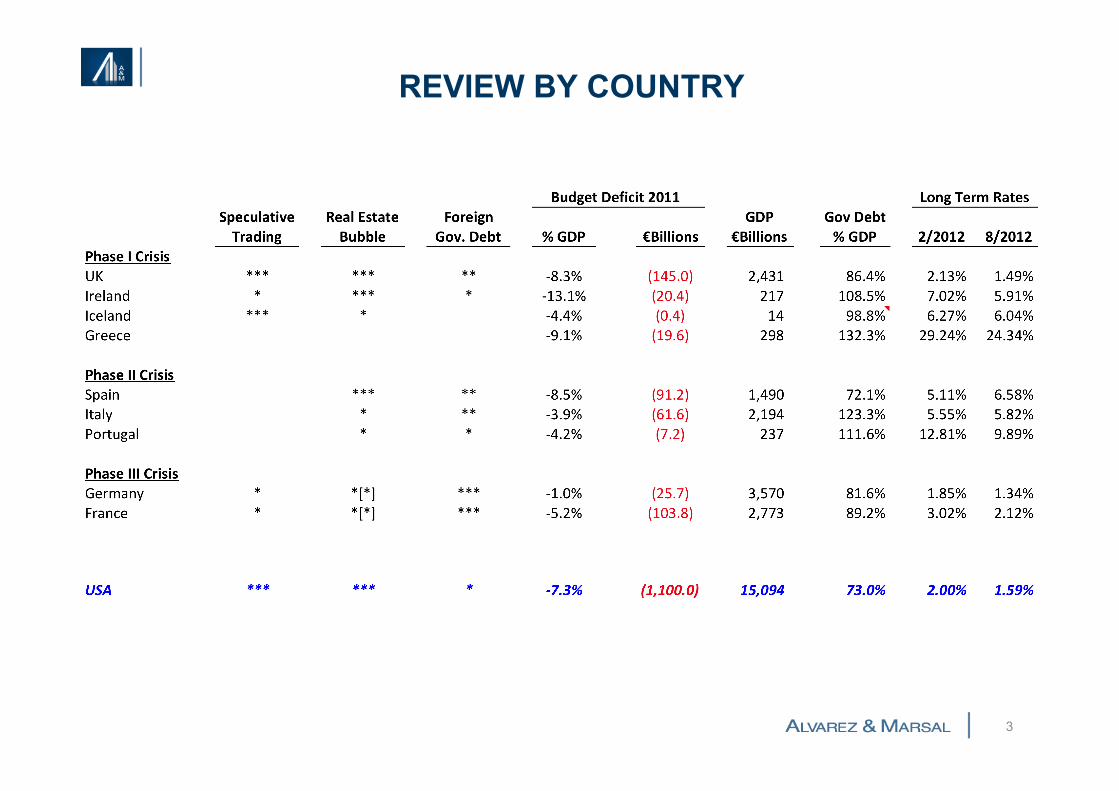

REVIEW BY COUNTRY

3

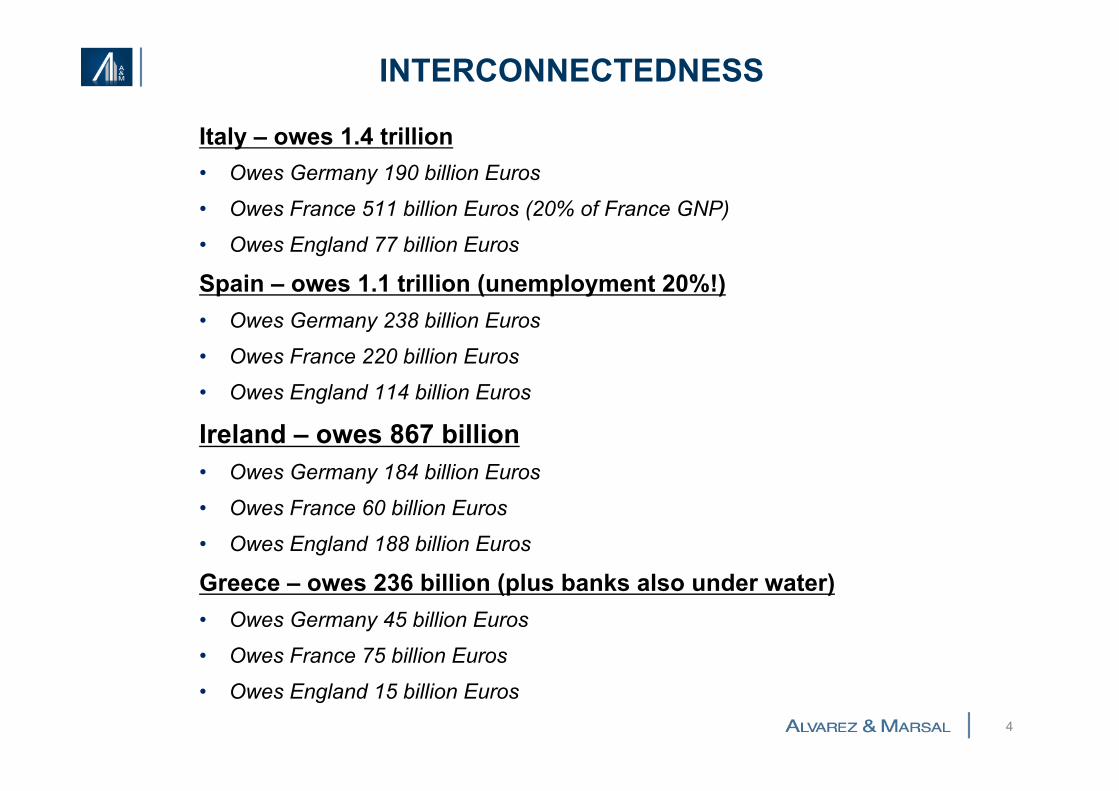

INTERCONNECTEDNESS

4

Italy – owes 1.4 trillion • Owes Germany 190 billion Euros

• Owes France 511 billion Euros (20% of France GNP)

• Owes England 77 billion Euros

Spain – owes 1.1 trillion (unemployment 20%!) • Owes Germany 238 billion Euros

• Owes France 220 billion Euros

• Owes England 114 billion Euros

Ireland – owes 867 billion • Owes Germany 184 billion Euros

• Owes France 60 billion Euros

• Owes England 188 billion Euros

Greece – owes 236 billion (plus banks also under water) • Owes Germany 45 billion Euros

• Owes France 75 billion Euros

• Owes England 15 billion Euros

TOPICS

5

I. Alvarez & Marsal Perspectives on the Current State of European Market [Sovereign / PE / Distress]

II. Middle Market Opportunities III. Pitfalls [Do’s and Don’ts]

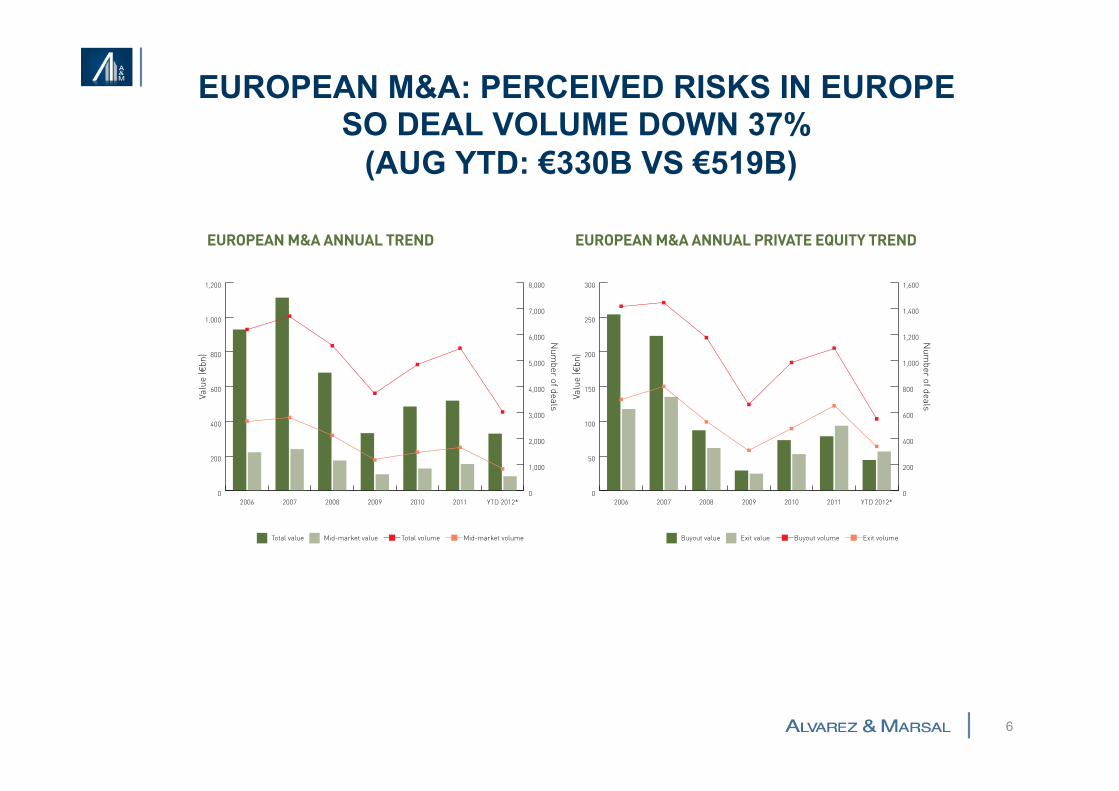

EUROPEAN M&A: PERCEIVED RISKS IN EUROPE SO DEAL VOLUME DOWN 37%

(AUG YTD: €330B VS €519B)

6

EUROPE

Monthly M&A Insider 22

TREND GRAPHS

EUROPEAN M&A QUARTERLY TREND

0

100

200

300

400

500

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Valu

e (!

bn)

Total value Mid-market value

Num

ber of deals

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Total volume Mid-market volume

0

10

20

30

40

50

60

70

80

90

100

110

120

130

140

Q312*

Q212

Q112

Q411

Q311

Q211

Q111

Q410

Q310

Q210

Q110

Q409

Q309

Q209

Q109

Q408

Q308

Q208

Q108

Q407

Q307

Q207

Q107

Q406

Q306

Q206

Q106

Buyout value Exit value Buyout volume Exit volume

Valu

e (!

bn)

Num

ber of deals

0

50

100

150

200

250

300

350

400

450

EUROPEAN M&A ANNUAL TREND EUROPEAN M&A ANNUAL PRIVATE EQUITY TREND

0

200

400

600

800

1,000

1,200

YTD 2012*201120102009200820072006

Total value Mid-market value

Num

ber of deals

Valu

e (!

bn)

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

Total volume Mid-market volume

0

50

100

150

200

250

300

YTD 2012*201120102009200820072006

Valu

e (!

bn)

Buyout value Exit value

Num

ber of deals

Buyout volume Exit volume

0

200

400

600

800

1,000

1,200

1,400

1,600

EUROPEAN M&A QUARTERLY PRIVATE EQUITY TREND

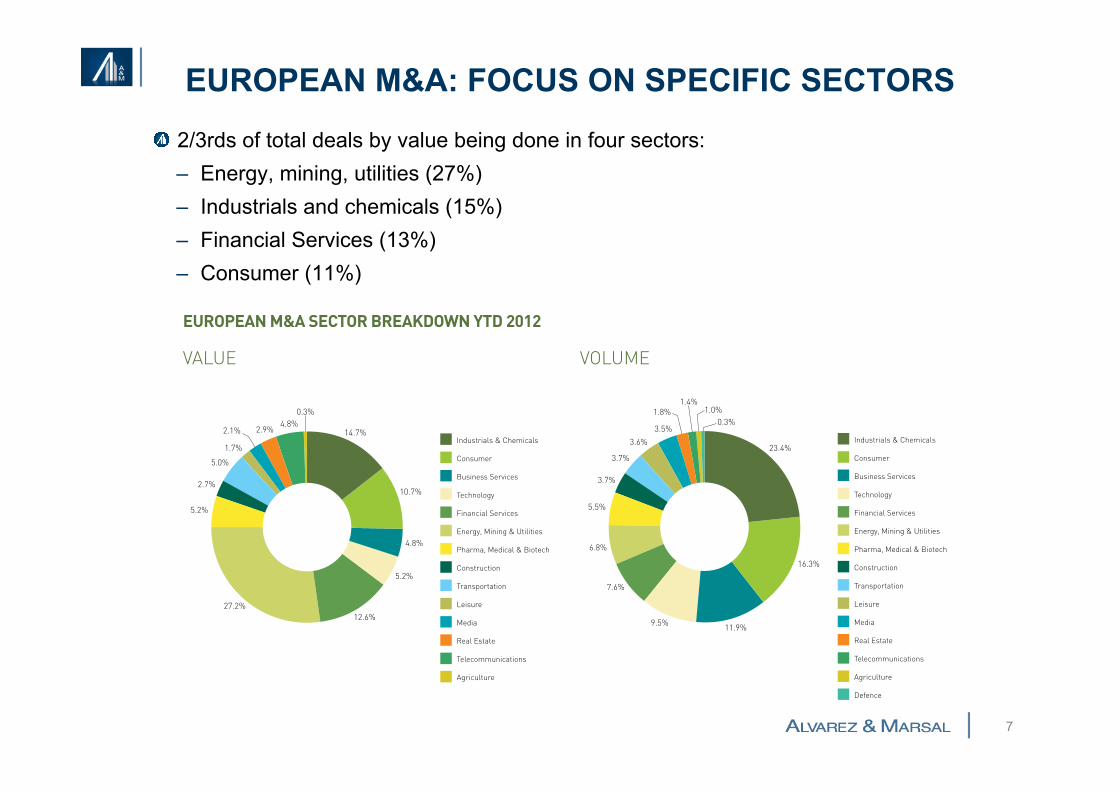

EUROPEAN M&A: FOCUS ON SPECIFIC SECTORS

" 2/3rds of total deals by value being done in four sectors: – Energy, mining, utilities (27%) – Industrials and chemicals (15%) – Financial Services (13%) – Consumer (11%)

7

EUROPE

Monthly M&A Insider 23

TREND GRAPHS

EUROPEAN M&A GEOGRAPHIC BREAKDOWN YTD 2012

VALUE VOLUME

UK

CEE

Iberia

France

Nordic

Germany

Benelux

Italy

Switzerland

Others

7.9%

12.7%

14.2%

6.2%

20.8%

8.5%

4.8%

8.3%

8.2%

8.4%

12.9%

8.6%

3.1%6.2%

5.7%22.3%

10.4%

11.5%

5.3%

14.0%

UK

CEE

Iberia

France

Nordic

Germany

Benelux

Italy

Switzerland

Others

EUROPEAN M&A SECTOR BREAKDOWN YTD 2012

VALUE VOLUME

4.8%

10.7%

14.7%

5.2%

2.7%

1.7%

5.0%

2.9%4.8%

0.3%

2.1%

12.6%

5.2%

27.2%

Industrials & Chemicals

Consumer

Business Services

Technology

Financial Services

Energy, Mining & Utilities

Pharma, Medical & Biotech

Construction

Transportation

Leisure

Media

Real Estate

Telecommunications

Agriculture

3.7%

23.4%

3.5%

6.8%

3.6%

5.5%

3.7%

1.8%1.4%

1.0%0.3%

16.3%

11.9%9.5%

7.6%

Industrials & Chemicals

Consumer

Business Services

Technology

Financial Services

Energy, Mining & Utilities

Pharma, Medical & Biotech

Construction

Transportation

Leisure

Media

Real Estate

Telecommunications

Agriculture

Defence

EUROPEAN M&A: POCKETS OF VALUE " Opportunities are based around a several specific themes: § #1: Financial institutions – selling portfolios of (non)performing

assets § #2: Distressed debt investing – loan-to-own § #3: Corporate carve-outs / divestitures of non core assets § #4: Bolt-ons for existing PE portfolio companies

8

TOPICS

9

I. Alvarez & Marsal Perspectives on the Current State of European Market [Sovereign / PE / Distress]

II. Middle Market Opportunities III. Pitfalls [Do’s and Don’ts]

PORTFOLIOS & DUE DILIGENCE CONSIDERATIONS

10

III. Implications for TPG

Conclusions

Ø Cash

Ø Management quality

Ø Understand the business & the true value drivers and sensitivities

Ø Planning and execution is key

Ø Contingencies – build a Plan B

Ø Gain Stakeholder support before you need it