alternative dispute resolution for financial services options

TRANSCRIPT

Report No. ACS 4668 .

Republic of Bulgaria

Alternative Dispute Resolution

for Financial Services Options

June 2013

.

The World Bank

Private and Financial Sectors Development Department

Central Europe and the Baltic Countries

Europe and Central Asia Region

Washington, D.C.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

1

© 2012 International Bank for Reconstruction and Development / The World Bank 1818 H Street NW,

Washington DC 20433 Telephone: 202-473-1000; Internet: www.worldbank.org

Some rights reserved

This work is a product of the staff of The World Bank with external contributions. Note that The World

Bank does not necessarily own each component of the content included in the work. The World Bank

therefore does not warrant that the use of the content contained in the work will not infringe on the rights

of third parties. The risk of claims resulting from such infringement rests solely with you.

The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views

of The World Bank, its Board of Executive Directors, or the governments they represent. The World

Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors,

denominations, and other information shown on any map in this work do not imply any judgment on the

part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of

such boundaries. Nothing herein shall constitute or be considered to be a limitation upon or waiver of the

privileges and immunities of The World Bank, all of which are specifically reserved.

Rights and Permissions

This work is available under the Creative Commons Attribution 3.0 Unported license (CC BY 3.0)

http://creativecommons.org/licenses/by/3.0. Under the Creative Commons Attribution license, you are

free to copy, distribute, transmit, and adapt this work, including for commercial purposes, under the

following conditions:

Attribution— Please cite the work as follows: World Bank (2013). Bulgaria: Alternative Dispute

Resolution for Financial Services Options. Report No. ACS 4668. Washington, DC: World Bank.

License: Creative Commons Attribution CC BY 3.0.

All queries on rights and licenses should be addressed to the Office of the Publisher, The World Bank,

1818 H Street NW, Washington, DC 20433, USA; fax: 202-522-2625; e-mail: [email protected].

2

CONTENTS

Abbreviations and Acronyms ....................................................................................................................... 3 Acknowledgements ....................................................................................................................................... 4 Preface .......................................................................................................................................................... 5

Executive summary ..................................................................................................................................... 6 ADR in Bulgaria .......................................................................................................................................... 8

What are the benefits of a financial sector ADR? ............................................................................. …..8 What is the legal and regulatory framework for ADR in Bulgaria?..................................................... 10 What are the existing institutional and redress arrangements in Bulgaria?........................................ 11 Summary of current situation ................................................................................................................ 16

Options for reform of the existing financial consumer redress regime ................................................ 17 Status of jurisdiction and decisions ........................................................................................................ 17 Effective handling of complaints by financial services providers ......................................................... 18 Sectoral vs. single cross-sector ADR bodies ........................................................................................... 19

a) Sectoral financial ADRs in the short-term ............................................................................ 20 b) Single cross-sector financial ADR in the long-term ............................................................. 21

Options for sectoral financial ADRs ...................................................................................................... 22 a) ADR for Banking and Non-Bank Credit Institutions ............................................................ 22 Option 1: Minimum change to comply with EU requirements ................................................. 22 Option 2: ADR body for Banking & Credit .............................................................................. 23 b) ADR for Insurance, Securities, and Pensions ....................................................................... 27 Option 3: Complaints department within FSC .......................................................................... 27 Option 4: ADR for NBFIs ......................................................................................................... 28

Conclusion .................................................................................................................................................. 31

References .................................................................................................................................................. 32

Annex: Key features of an effective financial ADR ................................................................................ 33

Figures

Figure 1: Confidence in fast and fair solution of emerging problems in the use of financial services ....... 10

Figure 2: Awareness of CPC activity concerning financial services ........................................................... 10

Figure 3: Institutional set-up for out-of-court redress mechanisms ............................................................ 12

Figure 4: Breakdown of complaints and queries submitted to the FSC for 2012 ....................................... 14

Tables

Table 1: Key recommendations and options for reform ................................................................................ 7

Table 2: EU Consumer Conditions Scoreboard ............................................................................................ 9

Table 3: Main decisions to be considered by the authorities ....................................................................... 17

Boxes Box 1: Benefits of a financial ADR .............................................................................................................. 8

Box 2: Multiple sector-specific ADRs in Poland and Germany ................................................................. 19

Box 3: Selected country examples of single cross-sector ADRs................................................................. 20

3

ABBREVIATIONS AND ACRONYMS

ABB

ABI

ADR

BNB

CCBC

CCFS

CCII

CCPD

CPC

EU

FCPFL

FSC

G20

MEET

MOF

ODR

OECD

WB

Association of Bulgarian Banks

Association of Bulgarian Insurers

Alternative dispute resolution body, for example an ombudsman1

Bulgarian National Bank

Complaints Commission for Banking and Credit (proposed)

Complaints Commission for Financial Services (proposed)

Complaints Commission for Insurance and Investments (proposed)

Conciliation Commission on Payment Disputes

Consumer Protection Commission

European Union

Financial Consumer Protection and Financial Literacy (Steering Committee)

Financial Supervision Commission

Group of Twenty Finance Ministers and Central Bank Governors

Ministry of Economy, Energy and Tourism

Ministry of Finance

Online dispute resolution

Organization for Economic Cooperation and Development

World Bank

1 There are financial ADRs in more than 40 countries worldwide – operating successfully in widely differing local

circumstances. Many use the name ‘ombudsman’. Others use ‘arbiter’, ‘arbitration board’, ‘complaints board’,

‘complaints committee’, ‘complaints service’, ‘disputes board’ or ‘mediator’.

4

ACKNOWLEDGEMENTS

This assessment was prepared by a team comprising Johanna Jaeger (Financial Sector Specialist,

Technical Leader), David Thomas (Dispute Resolution Specialist), and Evgeni Evgeniev (Private

Sector Development Specialist,). Sarah Fathallah (Financial Analyst) provided inputs and support to

the team. Technical guidance was provided by Samuel Munzele Maimbo (Lead Financial Sector

Specialist, Task Team leader), with oversight provided by Douglas Pearce (Acting Service Line

Manager) and Aurora Ferrari (Sector Manager).

The team expresses its appreciation to the Bulgarian authorities for their cooperation and

collaboration during the preparation of this assessment.

5

PREFACE

1. In August 2012, a National Steering Committee for Financial Consumer Protection and

Financial Literacy (FCPFL) – comprising representatives from the Bulgarian National Bank

(BNB), Financial Supervision Commission (FSC), Consumer Protection Commission (CPC) and

Ministry of Finance (MOF) – was established, committed to strengthening consumer protection

and financial literacy. In particular, the Steering Committee is committed to addressing the gaps

in the current regime for consumer protection including ineffective alternative dispute resolution

(ADR) mechanisms.

2. A new EU directive on ADR2 and a new EU regulation on online dispute resolution

(ODR)3 were approved by the European Parliament in March 2013 and by the European Council

(of member-state governments) in April 2013. These include compulsory requirements and

standards for ADRs for member states of the EU (See Box 1). The ADR directive is due to be

implemented by June 2015 and the ODR regulation will apply by the end of 2015. The Ministry

of Economy, Energy and Tourism (MEET) is responsible for implementation of the ADR

directive and ODR regulation in Bulgaria.

2www.europarl.europa.eu/sides/getDoc.do?type=TA&reference=P7-TA-2013-

0066&format=XML&language=EN#BKMD-29. 3 www.europarl.europa.eu/sides/getDoc.do?type=TA&reference=P7-TA-2013-0065&format=XML&language=EN.

Summary of the new ADR directive and ODR regulation

Under the ADR directive, EU member states must:

Ensure that ADRs are available across all consumer sectors for contractual disputes, both domestic

and cross-border, between consumers and traders that provide goods/services. Once made

available, member states are free to make ADRs compulsory.

Ensure that ADRs are monitored by a competent body designated by each member state.

Ensure that those in charge of ADRs must (i) be independent, impartial and not subject to

instructions from either party or their representatives, (ii) be appointed for a term of office of

sufficient duration to ensure the independence of their actions and not be likely to be relieved from

their duties without just cause, and (iii) have the necessary expertise in the field of alternative or

judicial resolution of consumer disputes.

Ensure that ADRs are available to consumers free-of-charge or at a nominal fee.

Ensure that ADRs have a timely (most disputes must be resolved within 90 days of receipt by the

ADR) and effective process (meaning parties do not need lawyers).

Ensure that ADRs have an up-to-date website, with full information, that enables consumers to

submit a complaint online. The ADR must also publish data on the number and types of

complaints, their outcomes, the rate of compliance and any systemic issues identified.

Under the ODR regulation, the European Commission will establish an ODR platform that:

Covers domestic and cross-border disputes about online and other electronic transactions

(excluding phone transactions and cash machines).

Enables complaints to be submitted online, passes them to the relevant national ADR and

facilitates the online communication between the complainant and the ADR.

6

EXECUTIVE SUMMARY

3. The objective of this technical note is to evaluate the existing legal, regulatory and

institutional framework of financial ADR mechanisms in Bulgaria, and to present the authorities

with options for reform and improvement.

4. There is a need to further strengthen and reform the existing financial ADR framework in

Bulgaria. Fortifying the design and structure of financial ADR mechanisms is an important step

to increase currently low levels of consumer trust in financial services. In addition, the

implementation of the recently approved EU Directive on ADR will require a significant amount

of restructuring and reorganization of the existing ADR mechanisms in Bulgaria in order to be

compliant with the new required standards.

5. Taking into account the new EU requirements as well as best practice worldwide, several

options for restructuring of the existing dispute resolution regime are outlined (see Table 1).

6. An ADR will not be a success unless consumers can be confident that financial services

providers will take part and will follow decisions in favor of the consumer. Bearing in mind the

Bulgarian context and the limitations imposed by the Bulgarian constitution, it is recommended

to opt for a compulsory and binding ADR structure, but with a possibility to appeal to court.

Moreover, financial services providers should bear the first-line responsibility for resolving

complaints and be subject to similar complaints handling rules and procedures.

7. Whilst a single cross-sector financial ADR would have some advantages, it may well be

difficult to get all the relevant parties to agree the details in time to achieve this by June 2015.

Given the institutional and political constraints, this technical note considers the option of two

separate financial ADRs in the short term (one for banking & credit and one for insurance &

investments) by building upon the existing structures of the CCPD model. If and when

stakeholders are ready, this structure would allow for a potential consolidation into a single

cross-sector financial ADR in the long term.

8. In order to be successful, the new arrangements for financial ADR need to command

respect from financial services consumers, financial services providers and the authorities.

Where the views of stakeholders currently diverge, some compromise will be necessary in order

to create a coherent and workable system.

7

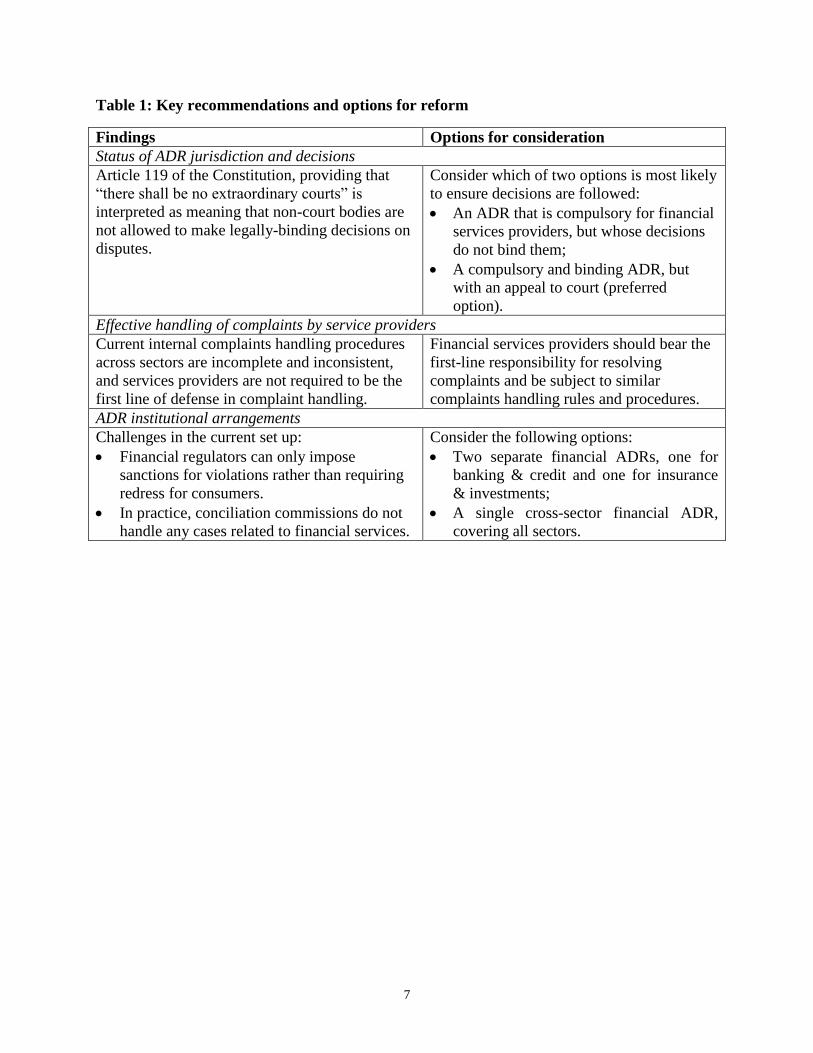

Table 1: Key recommendations and options for reform

Findings Options for consideration

Status of ADR jurisdiction and decisions

Article 119 of the Constitution, providing that

“there shall be no extraordinary courts” is

interpreted as meaning that non-court bodies are

not allowed to make legally-binding decisions on

disputes.

Consider which of two options is most likely

to ensure decisions are followed:

An ADR that is compulsory for financial

services providers, but whose decisions

do not bind them;

A compulsory and binding ADR, but

with an appeal to court (preferred

option).

Effective handling of complaints by service providers

Current internal complaints handling procedures

across sectors are incomplete and inconsistent,

and services providers are not required to be the

first line of defense in complaint handling.

Financial services providers should bear the

first-line responsibility for resolving

complaints and be subject to similar

complaints handling rules and procedures.

ADR institutional arrangements

Challenges in the current set up:

Financial regulators can only impose

sanctions for violations rather than requiring

redress for consumers.

In practice, conciliation commissions do not

handle any cases related to financial services.

Consider the following options:

Two separate financial ADRs, one for

banking & credit and one for insurance

& investments;

A single cross-sector financial ADR,

covering all sectors.

8

ADR IN BULGARIA

What are the benefits of a financial sector ADR?

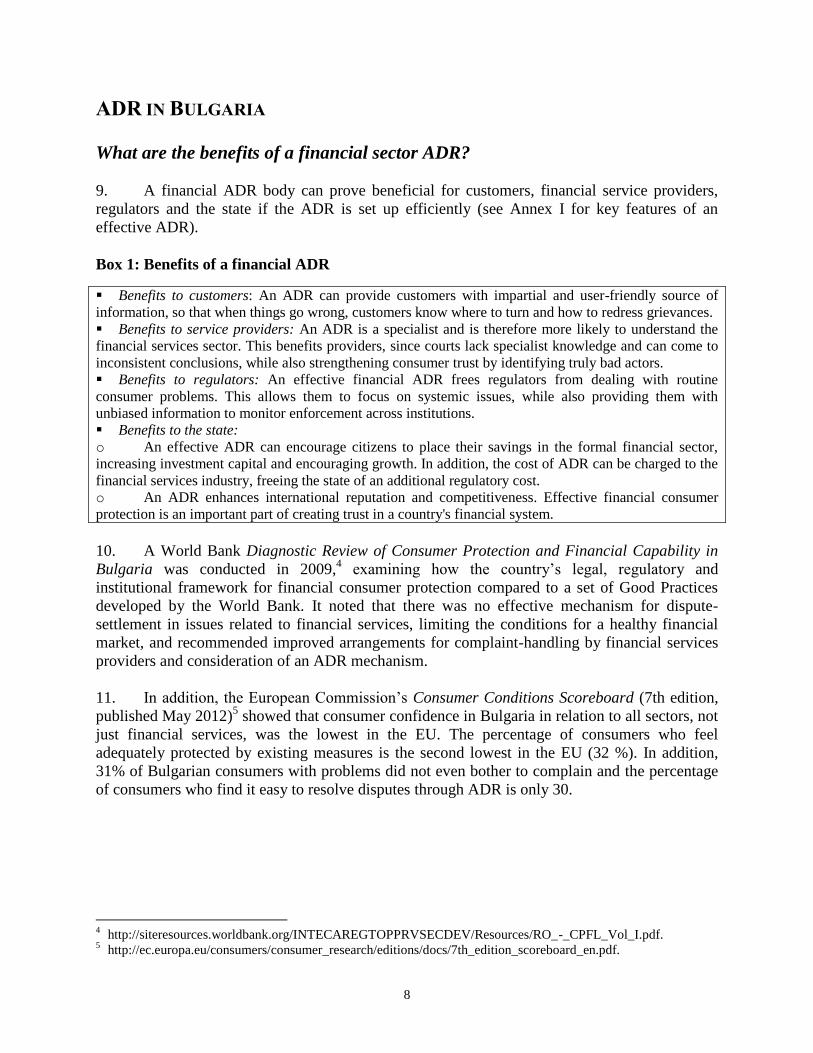

9. A financial ADR body can prove beneficial for customers, financial service providers,

regulators and the state if the ADR is set up efficiently (see Annex I for key features of an

effective ADR).

Box 1: Benefits of a financial ADR

Benefits to customers: An ADR can provide customers with impartial and user-friendly source of

information, so that when things go wrong, customers know where to turn and how to redress grievances.

Benefits to service providers: An ADR is a specialist and is therefore more likely to understand the

financial services sector. This benefits providers, since courts lack specialist knowledge and can come to

inconsistent conclusions, while also strengthening consumer trust by identifying truly bad actors.

Benefits to regulators: An effective financial ADR frees regulators from dealing with routine

consumer problems. This allows them to focus on systemic issues, while also providing them with

unbiased information to monitor enforcement across institutions.

Benefits to the state:

o An effective ADR can encourage citizens to place their savings in the formal financial sector,

increasing investment capital and encouraging growth. In addition, the cost of ADR can be charged to the

financial services industry, freeing the state of an additional regulatory cost.

o An ADR enhances international reputation and competitiveness. Effective financial consumer

protection is an important part of creating trust in a country's financial system.

10. A World Bank Diagnostic Review of Consumer Protection and Financial Capability in

Bulgaria was conducted in 2009,4 examining how the country’s legal, regulatory and

institutional framework for financial consumer protection compared to a set of Good Practices

developed by the World Bank. It noted that there was no effective mechanism for dispute-

settlement in issues related to financial services, limiting the conditions for a healthy financial

market, and recommended improved arrangements for complaint-handling by financial services

providers and consideration of an ADR mechanism.

11. In addition, the European Commission’s Consumer Conditions Scoreboard (7th edition,

published May 2012)5 showed that consumer confidence in Bulgaria in relation to all sectors, not

just financial services, was the lowest in the EU. The percentage of consumers who feel

adequately protected by existing measures is the second lowest in the EU (32 %). In addition,

31% of Bulgarian consumers with problems did not even bother to complain and the percentage

of consumers who find it easy to resolve disputes through ADR is only 30.

4 http://siteresources.worldbank.org/INTECAREGTOPPRVSECDEV/Resources/RO_-_CPFL_Vol_I.pdf.

5 http://ec.europa.eu/consumers/consumer_research/editions/docs/7th_edition_scoreboard_en.pdf.

9

Table 2: EU Consumer Conditions Scoreboard

Overall consumer conditions index

EU best 74%

EU average 62%

Bulgaria / EU lowest 49%

Consumer confidence in consumer-protection measures

EU best 84%

EU average 58%

Bulgaria 32%

EU lowest 28%

Consumers with a problem but who did not complain

EU best 5%

EU average 20%

Bulgaria 31%

EU lowest 59%

Consumers finding it easy to resolve disputes through ADR

EU best 67%

EU average 52%

Bulgaria 30%

EU lowest 27%

Consumers finding it easy to resolve disputes through the courts

EU best 52%

EU average 38%

Bulgaria 30%

EU lowest 10%

12. The 2010 financial literacy survey6 found that Bulgarian citizens tend to distrust the

possibility of a fast and fair response on behalf of the institutions where a problem has emerged.

The majority of the respondents are not familiar with their rights when using financial services.

The poor knowledge goes hand in hand with the distrust in the adequate reaction of the

institutions to an emerging problem. 39% of the people are not convinced their problem could

find a fast solution, and 40% it could find a fair solution. Only 17% expected a fast solution and

only 16% a fair solution. Half of those who had encountered a problem did not undertake any

action and a quarter simply gave up on the product

6 http://siteresources.worldbank.org/FINANCIALSECTOR/Resources/World_Bank_Bulgaria_FinLit_Report.pdf.

10

Figure 1: Confidence in fast and fair solution of emerging problems in the use of financial

services

Source: World Bank Financial Literacy Households Survey in Bulgaria, 2010.

13. The poor awareness of consumer rights with regards to financial services is evident in the

answer to the question about the work of the CPC. Only 17% were aware of CPC’s consumer

protection role in relation to financial services.

Figure 2: Awareness of CPC activity concerning financial services

Source: World Bank Financial Literacy Households Survey in Bulgaria, 2010.

What is the legal and regulatory framework for ADR in Bulgaria?

14. Article 119 of the Bulgarian constitution provides that: (1) Justice shall be administered

by the Supreme Court of Cassation, the Supreme Administrative Court, courts of appeal, regional

courts, courts-martial and district courts; (2) Specialized courts may be set up by virtue of law;

11

(3) There shall be no extraordinary courts. Subsection (3) is interpreted as meaning that non-

court bodies are not allowed to make legally-binding decisions on disputes.

15. In addition, there are three key laws regulating ADR mechanisms related to financial

services in Bulgaria:

The Law on Consumer Protection (Chapter 9) provides that consumers and consumer

associations are entitled to complain to the CPC about violations of the rights given by the Law.7

CPC must take a decision within one month.8 The Law also provides for the MEET to establish

regional conciliation commissions, to resolve disputes between consumers and entrepreneurs.9

These commissions comprise three members: one from CPC, one from an association of

entrepreneurs and one from an association of consumers.10

The commissions seek to achieve an

agreement between the parties11

and operate under regulations set by MEET.12

The Law on Consumer Credit (Chapter 15) provides that consumer-credit providers are

obliged to have a procedure for consumer complaints and to issue a decision within 30 days.13

Consumers can submit complaints in relation to contracts for consumer credit, or brokerage for

provision of consumer credit, to CPC.14

As an alternative, consumers can also refer disputes to

the regional conciliation commissions established under the Law on Consumer Protection.15

The Law on Payment Services and Payment Systems (Chapter 8) requires payment

service providers to have a complaint-handling procedure in place including taking a decision

within seven days.16

The Law provides for the establishment of the Conciliation Commission for

Payment Disputes (CCPD) as an independent conciliation body for settlement of disputes arising

between payment-service providers and payment-service users.17

16. Banks, which dominate the financial sector in Bulgaria, are not required to have

complaints handling procedures in place – except in relation to consumer credit and payment

services. FSC-regulated insurance companies, investment intermediaries and investment-

management companies are required to have efficient and transparent procedures for the

reasonable and timely review of complaints – as a result of national laws implementing European

directives. But these requirements do not extend to pension companies.

What are the existing institutional and redress arrangements in Bulgaria?

17. In the event that a consumer complaint is not resolved with the respective financial

institution, the consumer has, at present, several options: proceed to the court, turn to the

respective financial regulator or use the exiting conciliation mechanisms. Due to the perceived

high cost and lengthy time of proceedings going to court is mostly not considered an option for a

7 Art. 178 of the Law on Consumer Protection.

8 Art. 180 of the Law on Consumer Protection.

9 Art. 182 of the Law on Consumer Protection.

10 Art. 183 of the Law on Consumer Protection.

11 Art. 184 of the Law on Consumer Protection.

12 Art. 185 of the Law on Consumer Protection.

13 Art. 39 of the Law on Consumer Credit.

14 Art. 37 of the Law on Consumer Credit.

15 Art.40 of the Law on Consumer Credit.

16 Art. 127 of the Law on Payment Services and Payment Systems.

17 Art. 128 of the Law on Payment Services and Payment Systems.

12

typical consumer.18

The 2012 EU Consumer Conditions Scoreboard19

results show that 70% of

consumers did not find it easy to resolve disputes through the courts. In addition, the 2012 EU

Justice Scoreboard20

notes that on perceived judicial independence, Bulgaria ranks among the

lowest in the EU (Romania and Slovakia score slightly lower).

18. Institutions involved in out-of-court redress arrangements include (a) the Consumer

Protection Commission and its regional conciliation commissions; (b) the Bulgarian National

Bank; (c) the Financial Supervision Commission; and (d) the Conciliation Commission on

Payment Disputes. Figure 3 lays out the institutional set-up for out-of-court redress mechanisms

highlighting redress responsibilities and powers, procedures and inter-institutional relationships

of all parties involved. BNB, FSC and CPC all receive some complaints – but, though they can

impose sanctions for violations, they cannot require redress for consumers. In practice, CPC’s

regional conciliation commissions are voluntary for the parties involved and their decisions are

not binding. Participation in the specialist Conciliation Commission on Payment Disputes

(CCPD), which is established under the CPC but with a chair and deputy-chair appointed by

BNB, is mandatory for financial services while decisions are non-binding.

Figure 3: Institutional set-up for out-of-court redress mechanisms

18

The World Bank’s 2009 diagnostic review found that the average time for a case to be heard in court was five

years, even with simple cases. 19

http://ec.europa.eu/consumers/consumer_research/editions/docs/7th_edition_scoreboard_en.pdf. 20

http://ec.europa.eu/justice/newsroom/news/130327_en.htm.

13

(a) Consumer Protection Commission (CPC)

19. The Consumer Protection Commission (CPC) is the primary body responsible for

enforcing consumer protection legislation including the Consumer Protection Law and the Law

on Consumer Credit. It operates under the responsibility of the MEET. Its objectives include the

efficient protection of consumers against serious risks and threats, curtailing various forms of

unfair trade practices and other forms of abuse, and improving its own efficiency through

coordination and exchange of information with others.

20. Alongside its wider consumer-protection role, it is the regulator for consumer credit21

,

mortgages and personal leases. Apart from loans and mortgages, CPC does not deal with

individual financial complaints. It transfers those to BNB and FSC. Out of more than 12,000

consumer complaints that CPC handles per year, about 100 relate to administrative violations by

banks and other financial services providers – mainly concerning interest rates on loans and

charges on credit cards.

21. The regional conciliation commissions are voluntary for the parties involved and their

decisions are not binding. In practice, they do not handle financial complaints. In other consumer

sectors, more than 1,000 conciliation proceedings were initiated last year – but only 3% were

resolved, mainly because the trader failed to appear. The large number of scheduled conciliation

proceedings and the slow and inefficient legal procedure takes up a lot of time of CPC’s legal

experts.

(b) Bulgarian National Bank (BNB)

22. The Bulgarian National Bank (BNB) is in charge of regulating and supervising banks

and non-bank credit institutions in Bulgaria, and it has rather an ancillary role in supporting

financial consumer protection and financial education. Although CPC is the principal authority

for consumer protection, BNB receives and deals with banking complaints – sometimes referred

by CPC and sometimes directly from consumers.

23. Before the financial crisis, BNB received few consumer complaints – about 50 per year.

More recently, and excluding payment services, it received 572 in 2010, 671 in 2011 and 647 in

2012. Typical complaints related to changes of interest rates or unilateral changes of contract

terms in relation to deposits and loans.

24. BNB has four people dedicated to dealing with complaints, with backup from supervisors

and lawyers. Under BNB’s “Internal rules for complaints handling”, complaints are registered in

BNB’s information system, forwarded to the Bank Supervision Department, and distributed to

members of staff. Each case is discussed with the Director who gives instructions on how to

proceed based on the legal powers of the Bank Supervision Department. More complicated cases

may be discussed with other relevant Directorates. As a next step, the staff member writes to the

institution allowing for up to 14 days to provide information and documents (if no reply is

received, BNB can impose supervisory measures or administrative sanctions). Once all necessary

information has been received, the staff member prepares a letter for signature by the

21

Loans between 400 BGN and 40,000 BGN.

14

Director/Deputy Governor of BNB, giving an opinion on how to proceed with the specific

problem. In cases where BNB has no powers by law, the customers are advised to go to court.

BNB recommendations are non-binding but appear to be typically followed by banks.

25. BNB produces an internal annual report setting out amongst others, the number and types

of complaints, trends, names of banks and financial institutions subject to complaints, actions

taken, and suggestions for improvements. In addition, BNB has published on its website a list of

contacts of the complaint departments of banks.

(c) Financial Supervision Commission (FSC)

26. The FSC is a quasi-consolidated regulator that supervises the securities markets as well

as insurance and private pensions. It has consumer protection units in each of its sections for

securities, pensions and insurance to monitor and handle consumer complaints.

27. In 2012 FSC received 1,544 complaints and queries about the entities it regulates. 62.3%

of the complaints related to insurance22

. 11.1% of complaints related to the investment market

and 26.6% of complaints dealt with social security cases (including pensions), mostly concerning

transfers from one pension fund to another. FSC publishes quarterly and annual reports,

analyzing the complaints data that it has handled as well as commenting on trends and

suggestions for improvement.

Figure 4: Breakdown of complaints and queries submitted to the FSC for 2012

Source: FSC.

28. FSC has its own complaints-handling mechanism in place. As a first step, FSC advises

consumers to try to solve their complaint with the respective institution directly. Once

approached by a consumer, FSC conducts an inspection of whether the financial institution has

complied with the normative and legal requirements, timelines and procedures. New complaints

are logged in FSC’s Automatic Information System and then referred to the Legal Division,

Methodology and Complaints Department for further action – and to the relevant Supervision 22 Most insurance complaints related to general insurance, with 3.42% relating to health insurance. Claims formed

the largest topic among general insurance complaints.

15

Division and the Regulatory and Supervisory Operations Division. As a next step, the

information and documentation submitted by the consumer is verified and the respective

financial institution is approached for explanations on the case, including a request for data and

information. On the basis of the information received, a detailed report of the concrete case is

prepared23

by the Legal Division, Methodology and Complaints Department.

29. Challenges in the current set up remain as FSC’s powers are limited to the powers given

to the authority by law and its underlying regulations. So, for example, FSC can assess whether

an insurance company has followed its claims process according to the existing regulatory

framework, but not whether the amount offered is fair.

30. In case of legal and regulatory violations, FSC can impose administrative sanctions.

However, FSC has no power to take biding decisions. If FSC decides that rules have been

broken, it can issue sanctions – but, though it can give the consumer advice, it cannot award any

redress. In addition, FSC’s intervention led to satisfaction of the complainant’s claim in only

20.4% of complaints.

(d) Conciliation Commission on Payment Disputes (CCPD)

31. CCPD is an independent conciliation body for settlement of disputes arising between

payment-service providers and payment-service users. CCPD is not a legal entity. It is

established under the CPC, but the chair and deputy-chair are appointed by BNB. Cases are

considered by a panel of three members (the chair or deputy-chair, one from a list approved by

ABB and one from a list approved by CPC) which prepares a written conciliation proposal.

CCPD members are paid by the body that appointed them while there is no charge to the parties.

32. In 2012, CCPD completed 78 cases. In almost 50% agreement was reached – usually

because the bank accepted a recommendation in favor of the consumer. In 10-15% of cases, the

bank refused to accept a recommendation in favor of the consumer. In the rest of the cases, the

recommendation was against the consumer. Typical disputes concerned (mainly) disputed

payments/withdrawals related with debit and credit cards, with significant numbers involving

internet transactions, disputes about interest and fees on credit cards, and problems with money

transfers (including technical errors, currency exchange, and fees and commissions on USD

accounts).

33. Although CCPD cannot take binding decisions, its decisions are acquiring increasing

respect from banks, and the level of compliance had risen. The setup of the CCPD has achieved

some success. Nevertheless, challenges remain due to limited resources and the lack of legal

status. So far CPC provides a part-time secretary and lends a room once a month. Especially

CPC and ABB members are reportedly not well-compensated for their work, (though motivated

by professional pride) and are hard-pressed in their main jobs. In addition, the current process

appears to be slow compared to international standards24

. Banks can take 3-6 months to deal with

23

After all enquiries and checks have been carried out, a written report is prepared, in accordance with a standard

template – including details on the complaining party, the supervised entity, the subject matter of the complaint and

its ground, the report of the supervised entity, actions taken and violations established, administrative sanctions

imposed, and merit of the complaint. 24

The new ADR directive specifies a maximum of 90 days, with limited exceptions for the most complex cases.

16

disputes at the first stage, with a further 3-6 months when cases reach the CCPD – giving an

overall time of 6-12 months.

Summary of current situation

34. Research shows that consumer trust in Bulgaria is low, and consumers have little

confidence in complaining. This is also reflected in the relatively low numbers of complaints

from financial consumers given the size of the country. Bearing in mind that banks dominate the

financial sector, the number of complaints about banks is particularly low (about 800 shared

among BNB, CPC and CCPD) compared to the number of complaints handled in the much-

smaller insurance sector.

35. Financial services are complex. Consumers need accessible sources of information about

their rights and accessible redress. BNB, FSC and CPC arrangements for handling complaint

enquiries are focused on dealing with administrative violations rather than on redress for

consumers. CCPD does not have facilities for handling enquiries, so that matters which might

have been resolved as enquiries may turn into full-blown cases.

36. In addition, the legal and regulatory framework is incomplete and inconsistent. Financial

services providers do not bear the first-line responsibility for resolving complaints. Banks, which

dominate the financial sector in Bulgaria, are not required to have procedures for handling

consumer complaints – except in relation to consumer credit and payment services. Also there

are significant differences in the complaint-handling requirements for consumer credit, payment

services, insurance and investments.

37. The regional conciliation commissions do not, in practice, handle any cases in relation to

financial services. In the cases they do handle, their success ratio is very low. The CCPD has

achieved some success, but has several limitations of its own. The CCPD process is slow. With

even the smallest cases being decided by a panel of three, it is inherently expensive for a dispute-

resolution process – though currently underfunded. CCPD depends on borrowed administrative

resources and seconded members who are already stretched.

38. There appears to be consensus among stakeholders that financial services require

specialized ADR arrangements and that, in the context of Bulgaria, these arrangements will need

to be provided by the authorities rather than by industry initiatives. But stakeholders currently

have differing priorities about other aspects of ADR for financial consumers. Some favor a

cross-sector approach while others want to proceed with a sectoral approach. And there are

differences of view on the respective involvements of CPC and the regulators in the specialist

field of consumer redress in financial services.

17

OPTIONS FOR REFORM OF THE EXISTING FINANCIAL CONSUMER

REDRESS REGIME

39. Taking into account the new EU requirements as well as best practice worldwide, this

report aims at arrangements that will operate effectively and efficiently, in order to resolve

disputes and misunderstandings at the earliest possible stage, as well as the lowest possible cost.

Various decisions need to be considered by the authorities (see Table 3). In order to be

successful they need to command respect from financial services consumers, financial services

providers and the authorities. Where the views of stakeholders currently diverge, some

compromise will be necessary in order to create a coherent and workable system.

Table 3: Main decisions to be considered by the authorities

1. Decide on the status of ADR jurisdiction and decisions

Consider which of two options is most likely to ensure decisions are followed:

o Option 1: Compulsory jurisdiction, but non-binding decisions

OR

o Option 2: Compulsory jurisdiction and binding decisions, but appeal to court (preferred

option)

2. Require providers to handle and resolve complaints

3. Decide on the structure of the ADR body

Consider setting up sectoral financial ADR(s) in the short term o ADR for banking and credit

AND/OR

o ADR for insurance, securities, and pensions

Potentially consolidate into a single cross-sector financial ADR in the long term

Status of jurisdiction and decisions

40. An ADR will not be a success unless consumers can be confident that financial services

providers will take part and will follow decisions in favor of the consumer. Bearing in mind the

Bulgarian context and the limitations imposed by the Bulgarian constitution, there are two

options for the Bulgarian authorities to consider in relation to the status of jurisdiction and

decisions by any ADR:

Option 1 (compulsory jurisdiction; non-binding decision)

41. Under this option:

if the consumer chooses to take a complaint to the ADR, the financial services

provider must take part; but

even if the provider does take part and the consumer accepts the ADR’s decision, the

provider is not bound by the decision.

18

42. Experience with CCPD suggests that option 1 might well result in a significant number of

financial services providers refusing to comply with the ADR’s decision. The authorities need to

consider how far its members and/or market forces could ‘encourage’ providers to follow

decisions in practice. Non-binding decisions work in some countries (e.g. the Nordics) where the

consumer movement is strong and financial businesses would suffer a loss of market share if

they do not follow recommendations. In view of the lack of consumer power in Bulgaria, there is

a high risk that - unless decisions are made binding - financial businesses will ignore them if they

do not agree.

Option 2 (compulsory jurisdiction; binding decision; appeal to court)

43. Under this option:

if the consumer chooses to take a complaint to the ADR, the financial services provider

must take part; and

if the consumer accepts the ADR’s decision, the provider is bound by the decision; but

either party can, if they wish, appeal to court on the merits of the case (the ADR would

not be making a final decision, in accordance with article 119(3) of the constitution).

44. The likely attitude of the judges is important in relation to this option. If the judges would

be supportive of the ADR (perhaps reinforced by appointing a judge to the supervisory board)

providers would soon be discouraged from appealing – making option 2 the preferred option.

Recommendation: In the Bulgarian context it will need to be considered which of the two options

is most effective in practice and most likely to ensure decisions are followed in practice.

Effective handling of complaints by financial services providers

45. Before taking a complaint to the ADR, the consumer should first be required to take their

complaint to the financial services provider, and allow the provider a reasonable time to resolve

it. Requiring financial services providers to bear the first-line responsibility for resolving

complaints will facilitate a speedier resolution of complaints, reduce the workload of any ADR

body, and help preserve client relationships.

Recommendation: Financial services providers should bear the first-line responsibility for

resolving complaints. Consumers should complain to the provider first, having access to the

ADR only if they are dissatisfied with the provider’s response or if there is no timely response.

46. All financial services providers in Bulgaria should be required to have a complaint-

handling procedure that complies with specified rules. The relevant financial regulator should

monitor and enforce this requirement. It will be more efficient for financial services providers,

and clearer for consumers, if the same rules are applied by all financial regulators. The rules

should identify what is to be treated as a complaint (for example, can it be oral or does it have to

be in writing). They should require providers to have a clear and simple process, publish the

process and give a copy to anyone who complains, provide the complainant with a written

response within some specified time, and disclose that he/she can turn to the ADR if still

dissatisfied.

19

Recommendation: All financial services providers should be required to have a complaint-

handling procedure that complies with specified rules about how they deal with consumer

complaints. It will be more efficient for financial services providers, and clearer for consumers,

if the same rules apply to all sectors.

Sectoral vs. single cross-sector ADR bodies

47. There are several options for the structure of financial ADR in Bulgaria. The EU

Directive on ADR will require significant changes to existing financial ADR arrangements in

Bulgaria. New arrangements must be in place by June 2015. One key question is whether there

should be separate ADRs in each financial services sector or a single cross-sector financial ADR.

Both models are seen in other countries, but with an increasing trend towards a cross-sector

approach. A single cross-sector ADR can contain specialist divisions covering particular types of

cases, so that cases are handled and decided by specialists with relevant expertise.

48. Countries that have separate ADRs in each financial services sector include Belgium,

Denmark, France, Germany, New Zealand, Poland, South Africa and Sweden. Most of these

were originally created by the financial services industry, often in partnership with consumer

groups. In Denmark and Sweden, decisions in each case are made by a panel (as with CCPD). In

the rest, decisions in each case are made by an expert decision-maker, usually called an

ombudsman.

Box 2: Multiple sector-specific ADRs in Poland and Germany

For example in Poland, banking service consumers have access to the industry-appointed

Banking Ombudsman, which provides a decision that binds the financial business but not the

consumer. In insurance, consumers have free access to the government-appointed Insurance

Ombudsman, which provides a non-binding recommendation – with the possibility, at some

cost, of going on to arbitration. In both banking and insurance, consumers can also turn to the

Arbitration Court at the Financial Supervisory Authority, which provides mediation and

decisions binding on both parties. In countries such as Germany, an industry-based

ombudsman structure for each part of the financial sector has proven effective. However, in

the case of such an ombudsman structure established by professional associations, attention

should be paid to the presence of conflicts of interest. Also, consumers may perceive the

ombudsman as someone who will always decide in favor of the financial institution and

against the consumer.

49. Countries that started off with separate ADRs in each financial services sector but which

later went on to amalgamate these into a single cross-sector financial ADR include Australia,

Finland, Ireland, Netherlands, Norway and the United Kingdom. In Norway decisions in each

case are made by a panel (as with CCPD). In the rest, decisions in each case are made by an

expert decision-maker, usually called an ombudsman – though Netherlands has an appeal to a

panel.

20

50. Countries that went straight to a single cross-sector ADR include Armenia, Hungary,

Malta and Taiwan. In the Czech Republic and Trinidad & Tobago, an ADR was established for

banking and then extended to the other sectors. Armenia demonstrates that it is possible for such

an ADR to operate effectively despite the particular challenges of a post-Soviet economy.

Box 3: Selected country examples of single cross-sector ADRs

For example, the UK established the Financial Ombudsman Service by law to function as an

independent institution, dealing with most consumer related financial matters. Its service is

free of charge and binding on the financial service provider. It is funded by levies and case

fees from financial services providers. In the Czech Republic consumers have free access to

the legally-established Financial Arbiter – which covers payment services, consumer credit

and some investment products. The Arbiter provides mediation and decisions binding on the

financial business and consumer. In Hungary, the Financial Arbitration Board (FBA) was set

up in July 2011, in the interest of handling financial consumer disputes between Hungarian

consumers and financial services providers. However, the resolution brought by the FBA is

only binding on the financial institution if it submits itself to the resolution. In Ireland, the

Financial Services Ombudsman’s Bureau is a statutory body dealing with consumer

complaints related to all regulated financial services providers. The Bureau is funded by levies

from financial institutions, and awards are binding on both parties, subject only to appeal to

the High Court.

51. The advantages of a single cross-sector ADR body include that it is simpler for

consumers to know where to take their complaints, and there is greater consistency of process

and of outcomes for financial services providers, which operate in more than one sector. The

increased size of a cross-sector ADR provides efficiencies of scale and increased value for

money, better arrangements for staff training and knowledge-management, and greater flexibility

in coping with peaks and troughs of workload in particular sectors.

52. However, most of the countries that have gone straight to a single cross-sector ADR are

ones with a single cross-sector financial regulator. Such a body is more complex to establish in

countries with multiple sectoral financial regulators.

a) Sectoral financial ADRs in the short-term

53. Due to institutional and political challenges that go hand in hand with the implementation

of a cross-sectoral ADR body, as well as a too-demanding timetable for any legal and regulatory

framework to implement the new EU Directive on ADR, consideration should be given to setting

up separate sectoral financial ADRs.

54. It would be advisable to use a similar, standardized ADR-type model. Having different

types of ADR bodies in different sectors would be more complex for both consumers and

financial services providers – as well as making it more difficult to bring ADR bodies together

when time and circumstances allow.

21

55. It would be helpful if the legal framework adopted in Bulgaria is designed so that the

ADRs can be adapted from time to time – to facilitate extensions in scope (as consumer and

industry confidence grows), and also improvements in the light of experience and adaptations to

reflect changing circumstances.

Recommendation: If it is decided to proceed with separate sectoral financial ADRs, it is

recommended that they are structured similarly in the different sectors, so as to reduce

complexity for consumers and financial services providers, and allow the possibility of merging

them into a single cross-sector ADR (with specialized divisions) if and when the relevant

stakeholders are ready to do so.

b) Single cross-sector financial ADR in the long-term

56. Under this option all financial services cases would go to a single specialized ADR body

(provisional working title: Complaints Commission for Financial Services – CCFS). This would

provide the maximum possible efficiency and flexibility, provide clarity for consumers,

efficiency for financial services providers, and increase value for money through economies of

scale. The proposed CCBC and CBII could be combined into a single cross-sector financial ADR

when and if stakeholders are ready.

57. A cross-sector ADR could include specialist divisions, and a larger body could have

better arrangements for staff training and knowledge-management. It would also be more

flexible in coping with peaks and troughs of workload in particular sectors, by retraining and

redeploying staff from one sector to another.

58. The main challenge presented by this option is the time that may be needed to get a

number of institutions to agree and implement a common cross-sector plan. This may raise

institutional and political challenges – as well as creating a too-demanding timetable for any

legal and regulatory framework.

59. It would be more practicable and economical to establish a single cross-sector ADR

according to the ombudsman model – with each case being decided by a single, expert decision-

maker. Individual decision-makers could specialize in particular sectors. The CCPD model, with

even the smallest cases decided by a panel, would involve more people and more discussion time

– and so be inherently more expensive.

60. But, if considered necessary in Bulgaria, there would be the possibility of an appeal to a

three-person panel. The panel would comprise a consumer specialist and an industry specialist

with an independent chair. The availability of such an appeal should calm any anxiety by the

industry about the possibility of decisions being taken without a full appreciation of any

technical issues and any wider implications. The number of appeals should fall over time as

confidence in the expertise of the decision makers grows. (See Annex I for further information

on the setup of an effective ADR).

22

Recommendation: When and if stakeholders are ready, a single cross-sector financial ADR

(provisional working title: Complaints Commission for Financial Services) should be established

to handle all consumer complaints about financial services. Its coverage, structure, process,

powers and funding should be as described above.

Options for sectoral financial ADRs

a) ADR for Banking and Non-Bank Credit Institutions

Option 1: Minimum change to comply with EU requirements

61. This option would involve amending CCPD and the regional conciliation commissions,

only so far as necessary to comply with the requirements of the EU directive on ADR and

regulation on ODR. It would result in all banking and credit cases (apart from those on payment

services) staying with non-specialized regional conciliation commissions.

62. This option is considered to be the least favorable. It would be contrary to the general

view amongst Bulgarian stakeholders as well as international best practice highlighting the need

to establish separate ADR bodies for financial services. This is especially the case in Bulgaria

where regional conciliation commissions have not proved successful in resolving financial

services disputes. Additionally, the regional conciliation commissions would be likely to

experience difficulty in meeting the ADR directive’s requirement for members with the

necessary specialist knowledge and skills.

Coverage

63. CCPD would continue to cover complaints about payment services while the regional

conciliation commissions would continue to deal with consumer credit complaints, and would

take on complaints about banking and non-bank credit – which would fall to them as the residual

ADR under the directive.

Institutional arrangements

64. Institutional arrangements would remain largely the same, though some changes would

be required. CCPD members would need to be appointed for terms of at least three years25

and

its annual report would need to be expanded to cover all the information required by the

directive.26

In the regional conciliation commissions, members would need to have the necessary 25

Currently, under article 129(1) of the Law on Payment Services and Payment Systems, they can be withdrawn at

any time. 26

Member States shall ensure that ADR entities make publicly available on their websites, on a durable medium

upon request, and by any other means they consider appropriate, annual activity reports. Those reports shall

include the following information relating to both domestic and cross-border disputes: (a) the number of disputes

received and the types of complaints to which they related; (b) any systematic or significant problems that occur

frequently and lead to disputes between consumers and (c) the rate of disputes the ADR entity has refused to deal

with and the percentage share of the types of grounds for such refusal; (d) the percentage shares of solutions

proposed or imposed in favour of the consumer and in favour of the trader, and of disputes resolved by an

amicable solution; (e) the percentage share of ADR procedures which were discontinued and, if known, the

23

knowledge and skills, be appointed for terms of at least three years, and they would need to

publish an annual report complying with new EU requirements. Both CCPD and the regional

conciliation commissions, would have to handle cross-border cases as well as domestic ones,

resolve most disputes within 90 days of receipt, have an up-to-date website (with the information

specified in the directive), and enable online submission of complaints.

Status of jurisdiction and decisions

65. No changes required. As of now, if the consumer chooses to take a complaint to the ADR

rather than to the court, the financial services provider is required to participate (in the case of

CCPD) or refuse to participate (in the case of the regional conciliation commissions). Decisions

would be non-binding.

Decision-maker

66. Decisions could continue to be taken by three-person panels. Conciliation commission

members would need to be appointed for terms of at least three years in order to comply with

new EU requirements.

Funding

67. No changes required. The cost of CCPD would continue to be shared among BNB, CPC

and ABB. The cost of the regional conciliation commissions would continue to come from

MEET’s budget.

Legal and Regulatory Framework

68. The changes required (described above under ‘institutional arrangements’) would involve

consequential amendments to the Law on Payment Services and Payment Systems (which sets

out the arrangements for CCPD), the Law on Consumer Credit (which sets out the role of the

regional conciliation commissions in consumer credit), and the Law on Consumer Protection

(under which the regional conciliation commissions are established).

Option 2: ADR body for Banking & Credit

69. This option would build on the strengths of CCPD, addressing its shortcomings and

extending its scope to cover the whole of the banking and credit sectors. The proposed

Complaints Commission for Banking & Credit – CCBC - (provisional working title) involves

more preparation, but yields considerable benefits. All banking and credit cases (including

payment services and mortgages) would go to a single specialized body. This would be much

more effective than the existing arrangements, clearer for consumers, more efficient for financial

services providers in the sector and provide better value for money.

reasons for their discontinuation; (f) the average time taken to resolve disputes; (g) the rate of compliance, if

known, with the outcomes of the ADR procedures; (h) cooperation of ADR entities within networks of ADR

entities which facilitate the resolution of cross-border disputes, if applicable.

24

Coverage

70. The CCBC would cover complaints about payment services, consumer credit, mortgages

and other banking products and services.

Institutional arrangements

71. CCBC should be established as a legal entity with its own resources. This would facilitate

the extension of its role and scope, as well as underpin its independence. CBCC should have its

own supervisory board, with members appointed by BNB and CPC on terms that provide for

security in office, in order to ensure their independence from those appointing them. It is

recommended that BNB and CPC appoint a balanced membership reflecting regulatory, industry

and consumer knowledge.

72. The supervisory board would be in charge of protecting the independence of the decision-

makers, ensuring that CCBC has sufficient resources to fulfill its role and oversee (on behalf of

stakeholders) that CCBC is effective and efficient. The supervisory board would appoint the

decision-makers by special majority that ensures confidence from all the groups that are

represented. The decision-makers would be appointed for at least a three year term. The chief

decision-maker would be chief executive of CCBC, managing the staff and resources.

73. For maximum efficiency, CCBC staff should deal with enquiries about specific problems

(from potential complainants and from financial services providers) – to resolve

misunderstandings and stop some enquiries turning into cases. CCBC should be able to dismiss

‘hopeless’ cases. It should try to resolve other cases within 90 days of receipt by mediation (if

possible), or by investigation and decision.

74. It is advisable that CCBC has power to demand evidence from parties, draw adverse

inferences against any party that fails to produce information that has been requested, and not

proceed with a case where the complainant fails to provide requested information. CCBC’s

decisions would be based on what is fair in the circumstances of the case, taking into account

what a court would do under law and regulations, any relevant regulatory rules, any relevant

code of conduct, and what was good industry practice at the time of the relevant events.

75. CCBC decision-making should be centralized which facilitates consistency of decision-

making. To enhance consumer accessibility CCBC representatives could make pre-advertised

visits to regional CPC offices in order to collect complaints from consumers face-to-face.

Status of jurisdiction and decisions

76. CCBC will only be a success if consumers can be confident that financial services

providers will take part and will follow decisions in favor of the consumer (which they are not

required to with CCPD). Participation in the new ADR scheme should be compulsory for

financial services provider (as they are required to with CCPD).

25

77. There are two alternatives for the status of decisions. The authorities should consider, in

the light of local conditions, which of two alternatives is likely to be most effective in Bulgaria:

The first alternative is for the decision to be non-binding. This is the current position with

CCPD, where (although compliance has increased) the financial services provider does reject the

decision in a significant minority of cases. The scope of CCBC would, of course, be much wider

than the scope of CCPD. The Steering Committee needs to consider how far its members and/or

market forces could ‘encourage’ providers to follow decisions in practice.

The second alternative is for the decision to be binding on the financial services provider,

but (as in the case of the Irish Financial Services Ombudsman Bureau27

) to allow an appeal to

court – so as to comply with article 119(3) of the Bulgarian constitution. The likely attitude of

the judges is important in relation to this alternative. If the judges would be supportive of CCBC

(perhaps reinforced by appointing a judge to the supervisory board), providers would soon be

discouraged from appealing – making this the preferred alternative. If the decision is to be made

binding, it is recommended to introduce a maximum limit to the amount that CCBC could award.

The limit could start around 25,000 BGN and be increased over time, as confidence in CCBC

grows.

Decision-maker

78. In CCPD, each case is decided by a three-person panel. This is inherently expensive, both

because of the number of people involved and the time needed for discussion amongst them.

However, the involvement of a respective expert does give the industry the confidence that any

decisions will be informed by a full appreciation of any technical issues, and will take account of

any wider implications of the issue being decided.

79. In most financial ADRs (including those in Armenia, Australia, Belgium, Czech

Republic, Finland, France, Germany, Ireland, New Zealand, Poland, South Africa, Taiwan,

Trinidad & Tobago and United Kingdom), each case is decided by a single, expert decision-

maker – usually with individual decision-makers specializing in particular sectors.

80. As CCBC would cover a much wider scope than CCPD, having all decisions made by a

three-person panel would over-stretch the available people as well as being unduly expensive.

Instead, each case could be decided by a single expert decision maker, but (following the

example of the Netherlands28

) there would be the possibility of an appeal to a three-person panel.

The panel would comprise a consumer specialist and an industry specialist with an independent

chair.

81. The availability of such an appeal should calm any anxiety by the industry about the

possibility of decisions being taken without a full appreciation of any technical issues and any

wider implications. The number of appeals should fall over time as confidence in the expertise of

the decision makers grows.

27

www.financialombudsman.ie/complaints-procedure/Appeal.asp. 28

Klachteninstituut Financiële Dienstverlening (Kifid). Website: www.kifid.nl.

26

Funding

82. In compliance with new EU requirements CCBC should be free for complainants, so that

cost is not a barrier to justice – especially for disadvantaged consumers. The budget of CCBC

should be set by its supervisory board, in an amount consistent with the effective and efficient

handling of the likely workload, but subject to approval by BNB and CPC.

83. It is important for any financial ADR that it receives sufficient funding, and that the

funding cannot be used as a means to affect its approach to deciding cases. Subject to those two

points, it makes no significant difference to the effectiveness of the ADR how the funding is

raised.

84. In a majority of countries including Armenia, Australia, Finland, France, Germany,

Ireland, Netherlands, New Zealand and the UK, the cost of the financial ADR is raised from the

relevant financial services providers. Initially, the total cost is raised by a yearly levy on the

relevant financial services providers. Typically, the total levy is apportioned out amongst

financial services providers – using a convenient proxy for market share, such as the number of

accounts or the amount of net assets – and collected by the regulator on behalf of the ADR. In

some countries, once there is sufficient experience of where the work comes from, an increasing

proportion of the funding is moved towards case fees collected by the ADR from providers

which have cases – so that the providers which produce most cases pay most of the cost. For

example, after 20 years’ experience, the Financial Ombudsman Service in the United Kingdom

collects about 80% of its income from case fees. In other countries, for example Lithuania29

and

Spain30

, the ADR bodies are fully funded by state budget.

85. It is for BNB and CPC to consider how far some or all of the cost of CCBC should be

raised from financial services providers, or met out of BNB’s and CPC’s own budgets.

Legal and Regulatory Framework

86. The creation of CCBC would require legislation of its own, including power for the

regulators to issue 'jurisdiction rules' (setting the scope of the ADR) and for CCBC to develop

'procedural rules' with the approval of the regulators. It would also require consequential

amendments to the Law on Payment Services and Payment Systems (transferring jurisdiction

from CCPD to CCBC) and the Law on Consumer Credit (transferring jurisdiction from the

regional conciliation commissions to CCBC). In addition, consequential amendments to the

legislative foundations of BNB and CPC, concerning their respective roles in relation to CCBC

might be required.

Research and consumer awareness

87. Active steps should be taken to ensure consumers know about the new body and how to

approach it. Consumers should be able to contact it without incurring significant cost – for

example, through a free-phone or low-cost phone number.

29

ADR of the State Consumer Rights Protection Authority of Lithuania. 30

ADR structure within Bank of Spain.

27

88. CCBC could draw general lessons from the cases that have been handled and share these

with the Bulgarian government, BNB, CPC, ABB and consumer bodies, as well as helping the

regulators to identify systemic problems and emerging risks.

89. In line with new EU requirements CCBC should publish at least a yearly report, covering

the amount of work it has done, summaries of typical cases, systemic issues and emerging risks

identified, efficiency statistics as well as its financial accounts.

Recommendation: Building upon the existing structures of the CCPD model, a single ADR

(provisional working title: Complaints Commission for Banking & Credit) should be established

by BNB and CPC to handle all consumer complaints about banking and credit. Its coverage,

structure, process, powers and funding should be as described above.

b) ADR for Insurance, Securities, and Pensions

Option 3: Complaints department within FSC

90. This option would mean creating a separate ADR department within FSC, complying

with the requirements of the EU directive on ADR and regulation on ODR. A similar set up, with

consumer redress being dealt with by a department within the sectoral regulator, is used in

Spain31

(though not too successfully) and in France (but only for securities)32

. It is currently used

in Trinidad & Tobago, where the ombudsman is currently an agency of the Central Bank, but the

Central Bank has announced publicly its intention to turn the ADR into a separate independent

body.33

91. However this option provides several shortcomings and is therefore less favorable in the

Bulgarian context. Direct conflicts of interest may arise (for example, a series of successful

complaints might affect the prudential health of an individual financial services provider), and

financial services providers may be reluctant to accept fault and settle cases in favor of

consumers, if they fear that as a result of the same process, they may also be subject to regulatory

sanctions. Also, parties might tend to associate the ADR staff with the regulator, as their work in

the ADR would just be part of their career path within FSC. ADR is not part of regulation, and

requires different skills. It is an alternative to the courts for the resolution of disputes, and should

be independent like the courts.

Coverage

92. FSC’s ADR department would cover redress for complaints about activities regulated by

FSC including insurance, securities and pensions complaints.

31

www.bde.es/bde/en/secciones/servicios/Particulares_y_e/Servicio_de_Reclwww.dgsfp.mineco.es/reclamaciones/in

dex.asp, www.cnmv.es/PortalInversor/home.aspx 32

www.amf-france.org 33

www.ofso.org.tt

28

Institutional arrangements

93. The ADR would be a separate department within FSC - resolving disputes within 90 days

of receipt - using FSC staff and resources. FSC would appoint the decision-makers. For

maximum efficiency, FSC ADR staff would deal with enquiries about specific problems (from

potential complainants and from financial services providers) – to resolve misunderstandings and

stop some enquiries turning into cases.

Status of jurisdiction and decisions

94. If the consumer choses to take a complaint to the ADR body within FSC, rather than the

court, the financial services provider should be required to participate. As the ADR body would

not be independent of the regulator, decisions should be non-binding.

Decision-maker

95. Decisions could continue be taken by individual decision-makers or three-person panels.

Funding

96. The ADR would be part of FSC and so financed from its budget (consisting of 40%

government budget and 60% provider fees).

Legal and Regulatory Framework

97. An FSC ADR body would require amendments to the legislative foundations of FSC, to

give it power to provide ADR and redress.

Option 4: ADR for NBFIs

34

98. Option 4 refers to the establishment of a single specialized ADR body dealing with all

insurance, securities and pensions cases (provisional working title: Complaints Commission for

Insurance & Investments – CCII). The proposed commission would maximize efficiency,

provide clarity for consumers, be efficient for financial services providers in the sector and

provide value for money.

99. This option would parallel CCBC, allowing for the possibility of amalgamating CCII and

CCBC into a single cross-sector financial ADR (with specialized divisions) when and if the

relevant stakeholders are ready.

Coverage

100. The Complaints Commission for Insurance & Investments (CCBC) would cover

consumer complaints about all activities regulated by FSC.

34

Non-bank financial institutions refer to insurance, securities and investment companies.

29

Institutional arrangements

101. It is recommended that CCII is established as a legal entity with its own resources to

underpin its independence. It should have its own supervisory board, with members appointed by

FSC on terms that provide for security in office in order to ensure their independence from FSC.

FSC should ensure a balanced membership reflecting regulatory, industry and consumer

knowledge.

102. The supervisory board would protect the independence of the decision-makers, ensure

that CCII has sufficient resources to fulfill its role and oversee (on behalf of stakeholders) that

CCII is effective and efficient. The supervisory board would appoint the decision-makers by

special majority that ensures confidence from all the groups that are represented. The decision-

makers would be appointed on terms35

that secure their independence from the supervisory board

– including security in office. The chief decision-maker would be chief executive of CCII,

managing the staff and resources.

103. For maximum efficiency, CCII staff would deal with enquiries about specific problems

(from potential complainants and from financial services providers) – to resolve

misunderstandings and stop some enquiries turning into cases. CCII would be able to dismiss

‘hopeless’ cases. It would try to resolve other cases within 90 days of receipt by mediation (if

possible) or by investigation and decision.

104. CCII would have power to demand evidence from the parties, draw adverse inferences

against any party that fails to produce information that has been requested, and not proceed with

a case where the complainant fails to provide requested information. CCII’s decisions would be

based on what is fair in the circumstances of the case, taking into account what a court would do

under law and regulations, any relevant regulatory rules, any relevant code of conduct, and what

was good industry practice at the time of the relevant events.

105. CCII would be based centrally, in view of the need to use financial services specialists

and to secure consistency. But this would not prevent CCII representatives making pre-

advertised visits to regional CPC offices in order to collect complaints from consumers face-to-

face, if these were thought necessary.

Status of jurisdiction and decisions