at751 pension

TRANSCRIPT

AT 751 Group Presentation 11/19/2014

Pension Plan--A Comparison of China and Chile

Yifan ZhaoLu ZhangYun WanNatalia Easton

AT 751 Group Presentation 11/19/2014

Types of Pension Plan

Pay-As-You-Go

Defined Contribution (DC) Most common now in US [401(k) & 403(b)], China and

Chile

Defined Benefit (DB) Unit benefit per year of service Less common

“Hybrid” plans

AT 751 Group Presentation 11/19/2014

Key Characteristics

Pay-as-you-go is highly sensible to deficits due to demographic changes, business cycles, fiscal irresponsibility

DC does not guarantee any level of pension. If the worker does not save enough, his pension will be low. DC are sensible to the quality of the labor market (more labor

market restrictions make people less productive and that lower the future pensions)

The employee bears the investment risk.

Examples: Europe, US, China and Chile fall in some place in between these two systems.

AT 751 Group Presentation 11/19/2014

Key Characteristics

DB pension plan promises to pay you a certain amount of retirement income for life. Predetermined by a formula based on the employee's

earnings history, tenure of service and age

Examples: Some governmental and public entities

AT 751 Group Presentation 11/19/2014

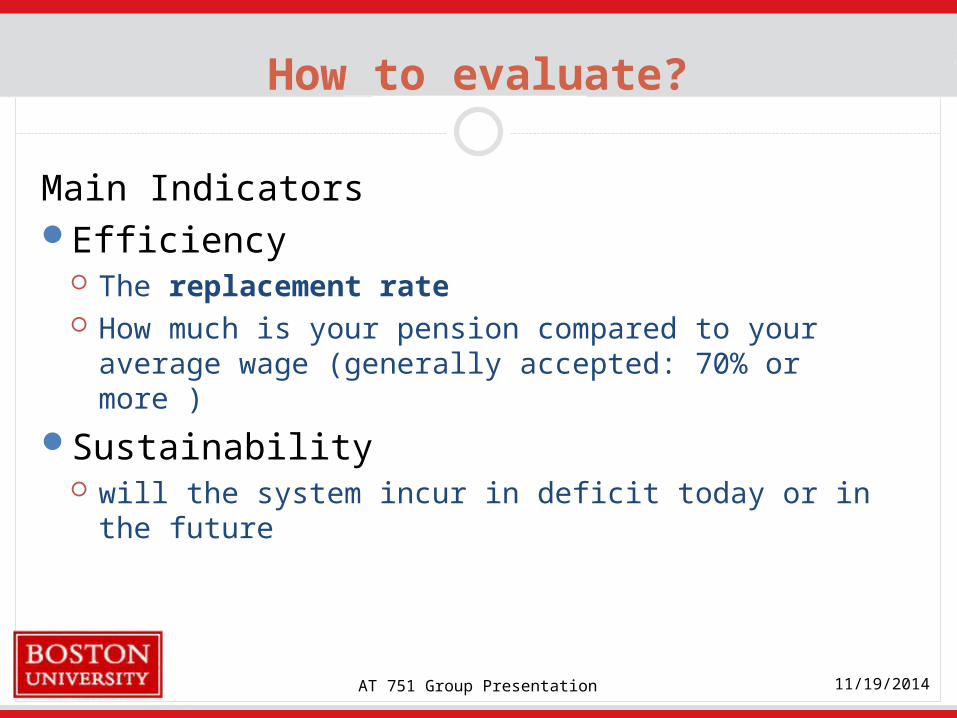

How to evaluate?

Main IndicatorsEfficiency

The replacement rate How much is your pension compared to your average

wage (generally accepted: 70% or more )

Sustainability will the system incur in deficit today or in the future

AT 751 Group Presentation 11/19/2014

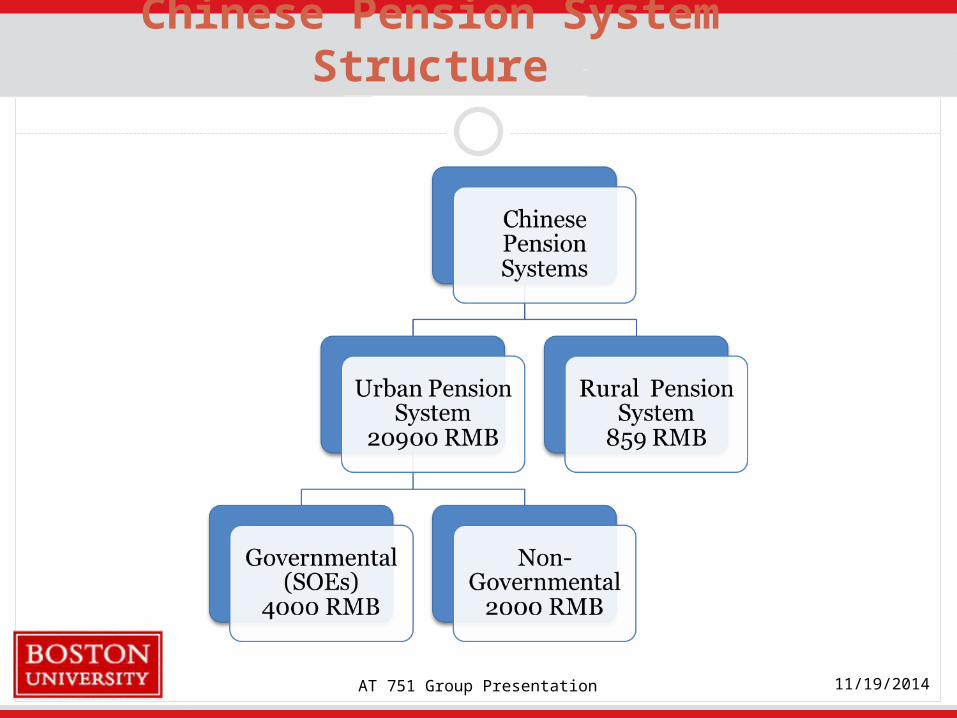

Chinese Pension System Structure

AT 751 Group Presentation 11/19/2014

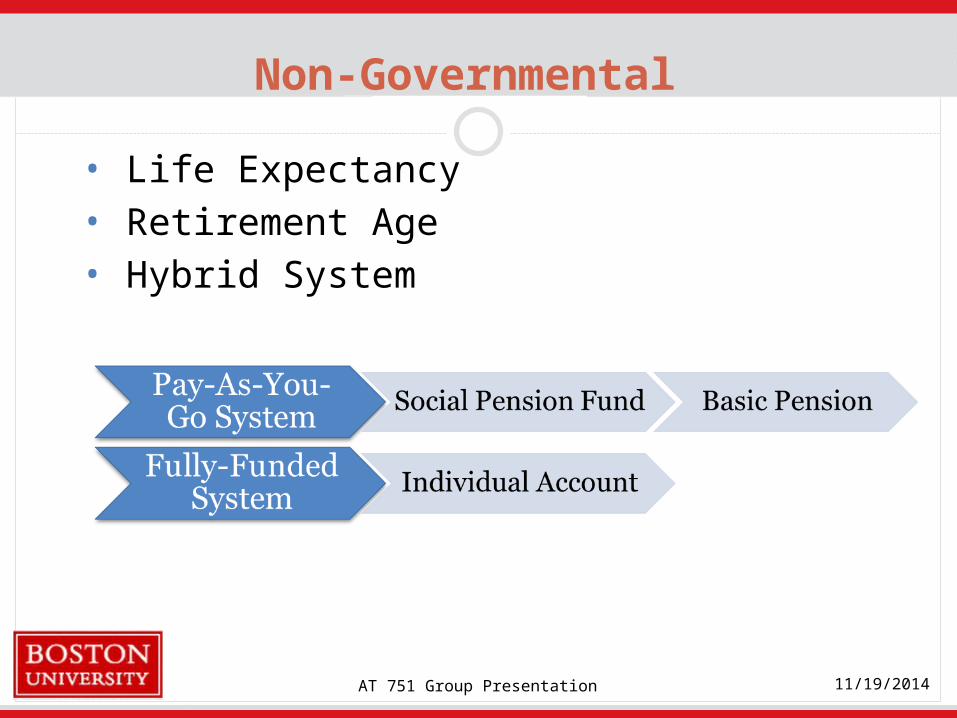

Non-Governmental

• Life Expectancy• Retirement Age• Hybrid System

AT 751 Group Presentation 11/19/2014

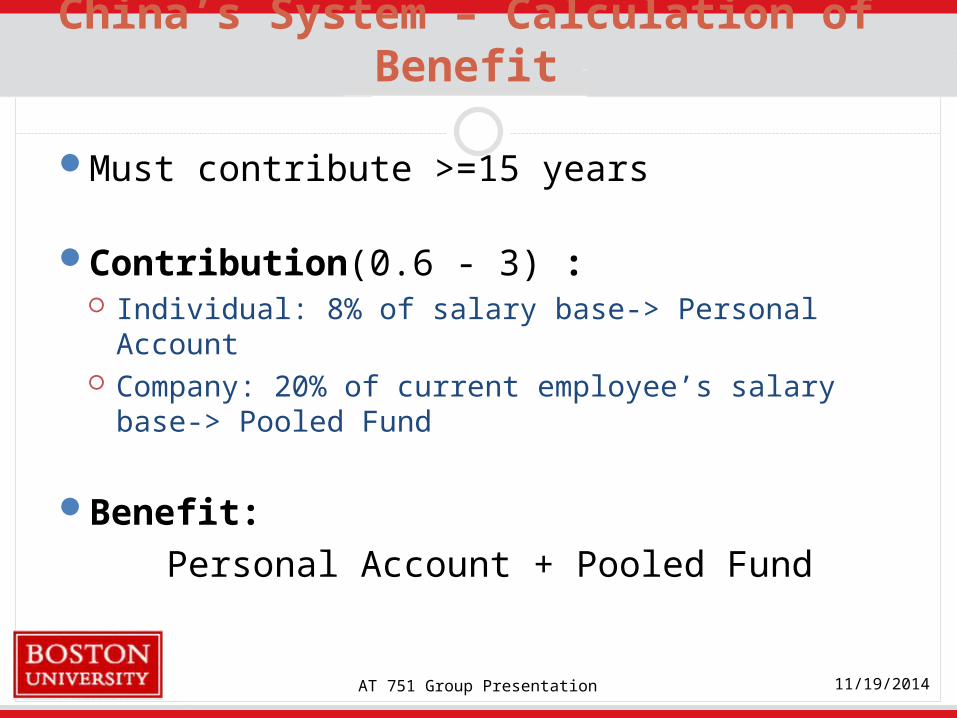

China’s System – Calculation of Benefit

Must contribute >=15 years

Contribution(0.6 - 3) : Individual: 8% of salary base-> Personal Account Company: 20% of current employee’s salary base->

Pooled Fund

Benefit: Personal Account + Pooled Fund

AT 751 Group Presentation 11/19/2014

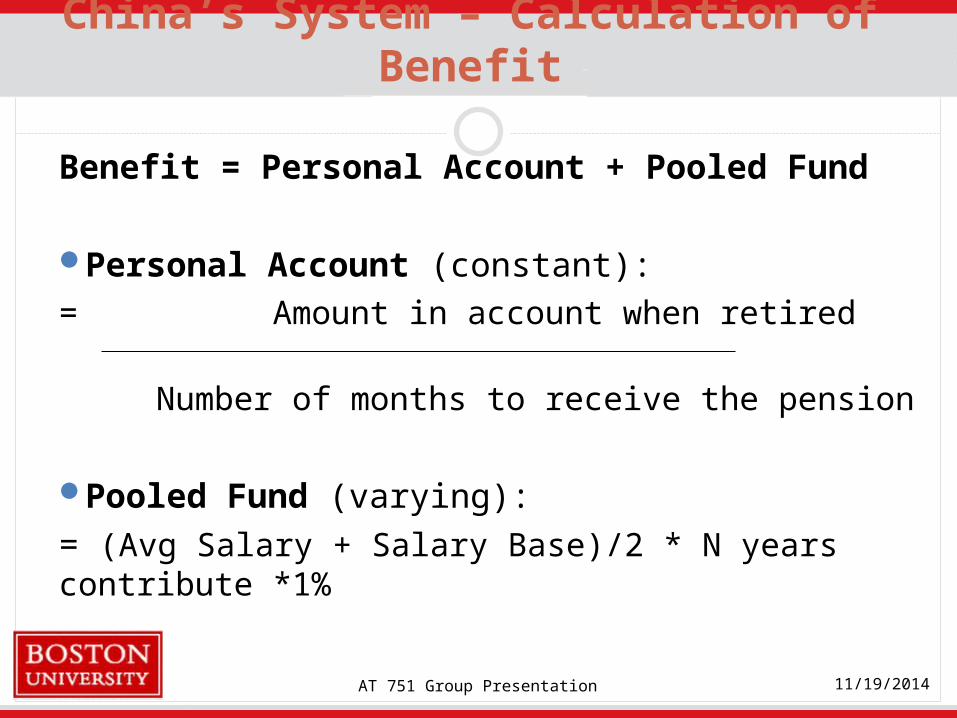

China’s System – Calculation of Benefit

Benefit = Personal Account + Pooled Fund

Personal Account (constant):= Amount in account when retired Number of months to receive the pension

Pooled Fund (varying):= (Avg Salary + Salary Base)/2 * N years contribute *1%

AT 751 Group Presentation 11/19/2014

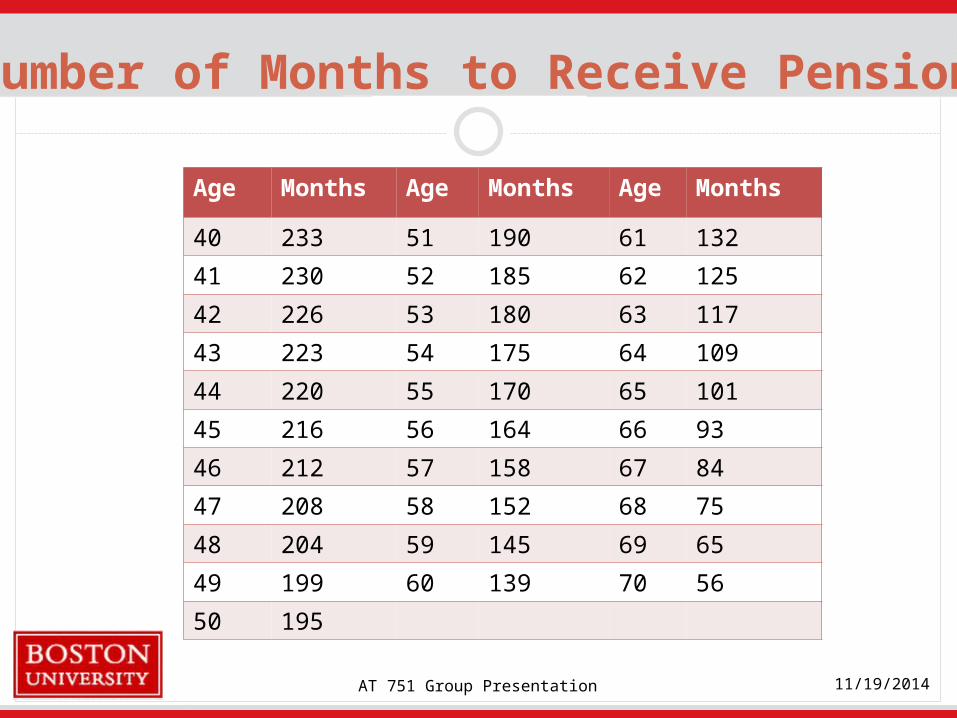

Number of Months to Receive Pension

Age Months Age Months Age Months

40 233 51 190 61 132

41 230 52 185 62 125

42 226 53 180 63 117

43 223 54 175 64 109

44 220 55 170 65 101

45 216 56 164 66 93

46 212 57 158 67 84

47 208 58 152 68 75

48 204 59 145 69 65

49 199 60 139 70 56

50 195

AT 751 Group Presentation 11/19/2014

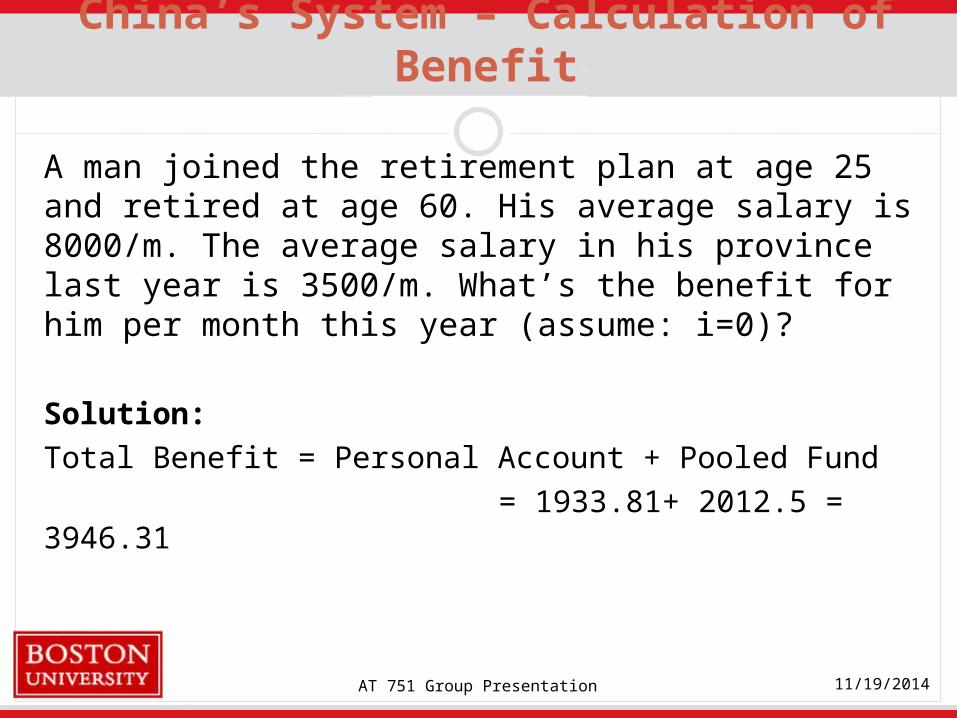

China’s System – Calculation of Benefit

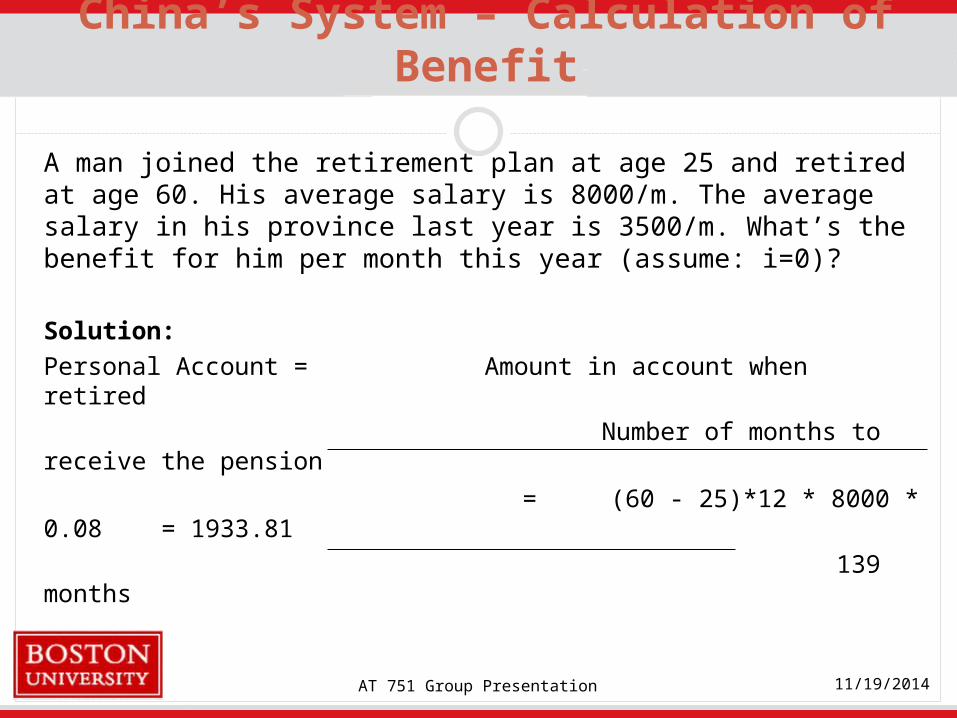

A man joined the retirement plan at age 25 and retired at age 60. His average salary is 8000/m. The average salary in his province last year is 3500/m. What’s the benefit for him per month this year (assume: i=0)?

Solution:Personal Account = Amount in account when retired Number of months to receive the pension

= (60 - 25)*12 * 8000 * 0.08 = 1933.81 139 months

AT 751 Group Presentation 11/19/2014

China’s System – Calculation of Benefit

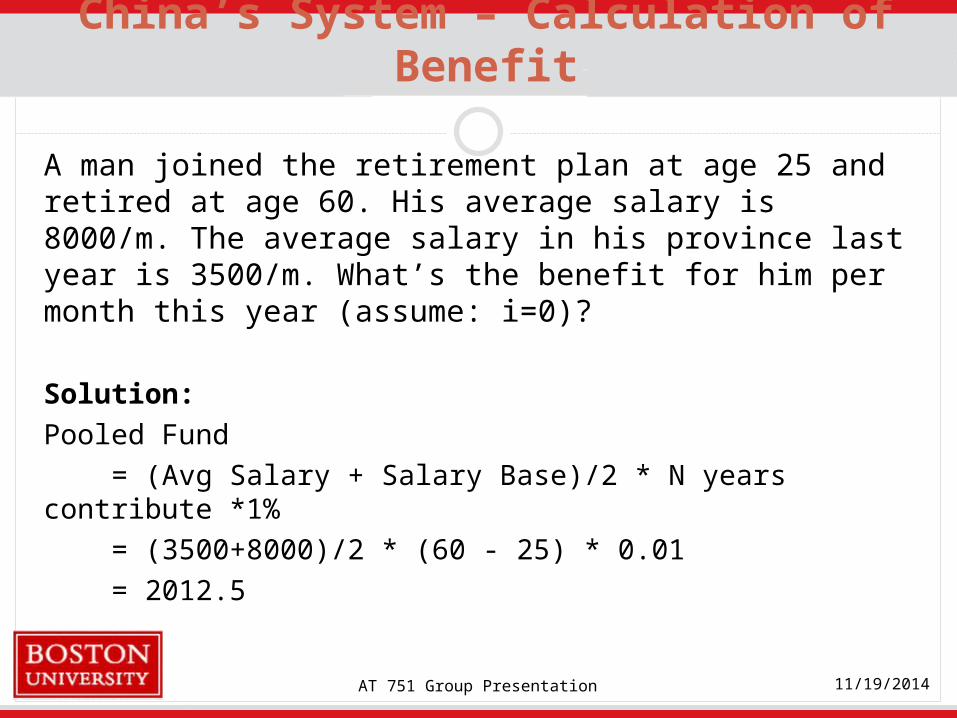

A man joined the retirement plan at age 25 and retired at age 60. His average salary is 8000/m. The average salary in his province last year is 3500/m. What’s the benefit for him per month this year (assume: i=0)?

Solution:Pooled Fund = (Avg Salary + Salary Base)/2 * N years contribute *1% = (3500+8000)/2 * (60 - 25) * 0.01 = 2012.5

AT 751 Group Presentation 11/19/2014

China’s System – Calculation of Benefit

A man joined the retirement plan at age 25 and retired at age 60. His average salary is 8000/m. The average salary in his province last year is 3500/m. What’s the benefit for him per month this year (assume: i=0)?

Solution:Total Benefit = Personal Account + Pooled Fund = 1933.81+ 2012.5 = 3946.31

AT 751 Group Presentation 11/19/2014

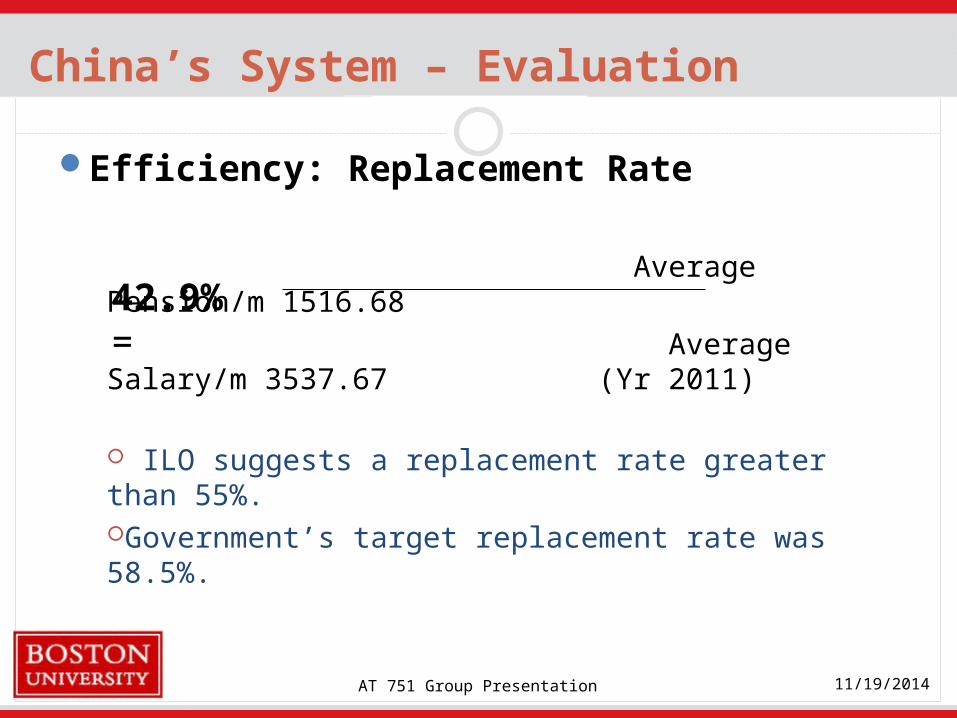

China’s System – Evaluation

Efficiency: Replacement Rate

Average Pension/m 1516.68 Average Salary/m 3537.67 (Yr 2011)

ILO suggests a replacement rate greater than 55%.Government’s target replacement rate was 58.5%.

42.9% =

AT 751 Group Presentation 11/19/2014

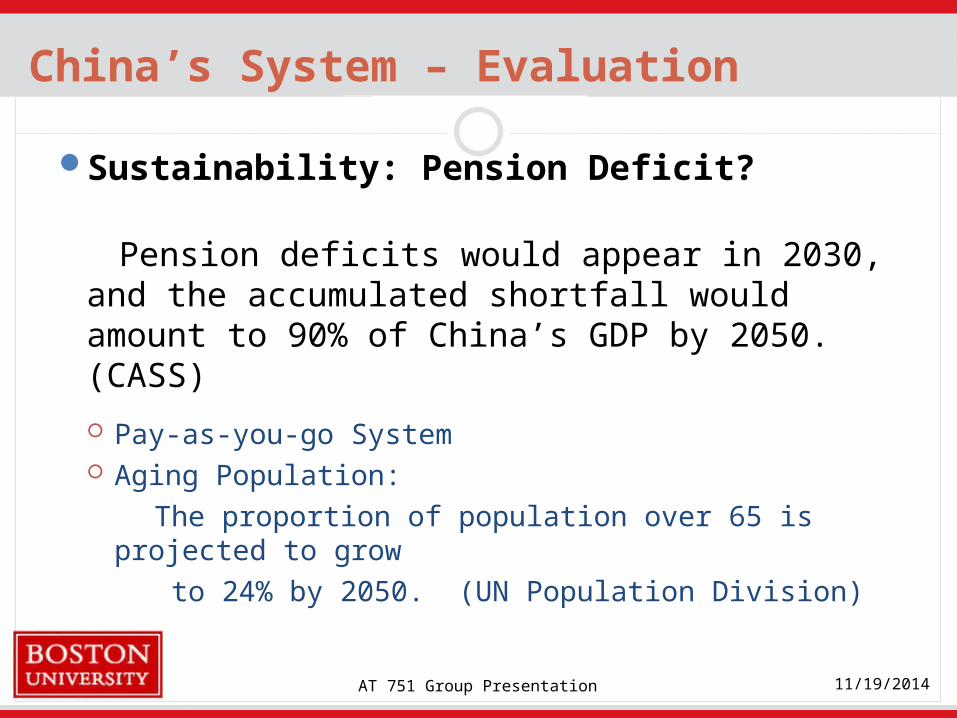

China’s System – Evaluation

Sustainability: Pension Deficit?

Pension deficits would appear in 2030, and the accumulated shortfall would amount to 90% of China’s GDP by 2050. (CASS)

Pay-as-you-go System Aging Population: The proportion of population over 65 is projected to

grow to 24% by 2050. (UN Population Division)

AT 751 Group Presentation 11/19/2014

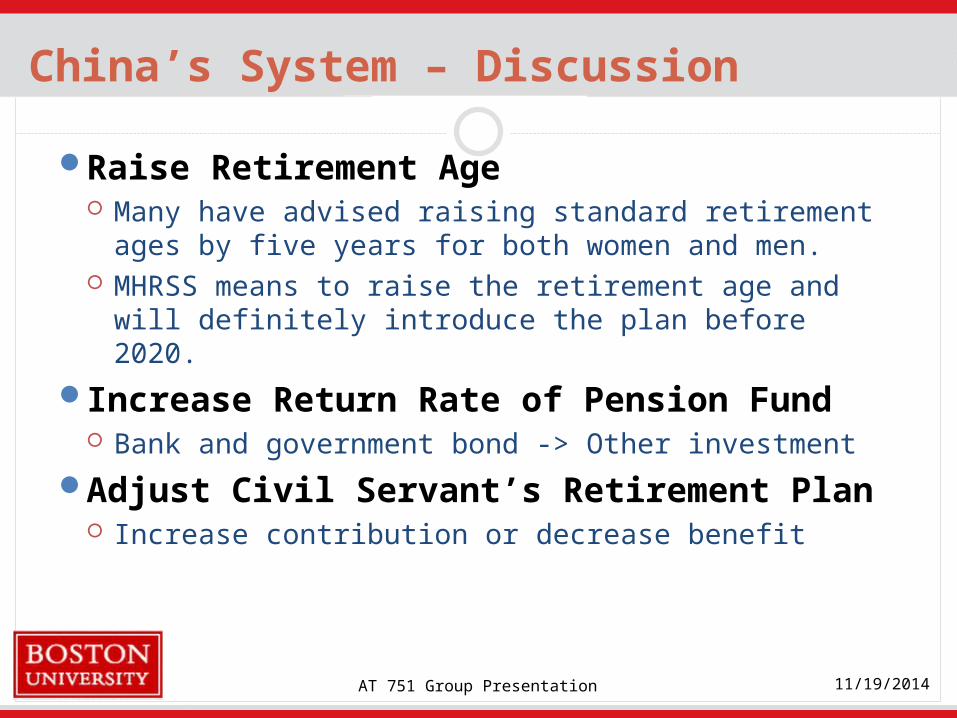

China’s System – Discussion

Raise Retirement Age Many have advised raising standard retirement ages

by five years for both women and men. MHRSS means to raise the retirement age and will

definitely introduce the plan before 2020.

Increase Return Rate of Pension Fund Bank and government bond -> Other investment

Adjust Civil Servant’s Retirement Plan Increase contribution or decrease benefit

AT 751 Group Presentation 11/19/2014

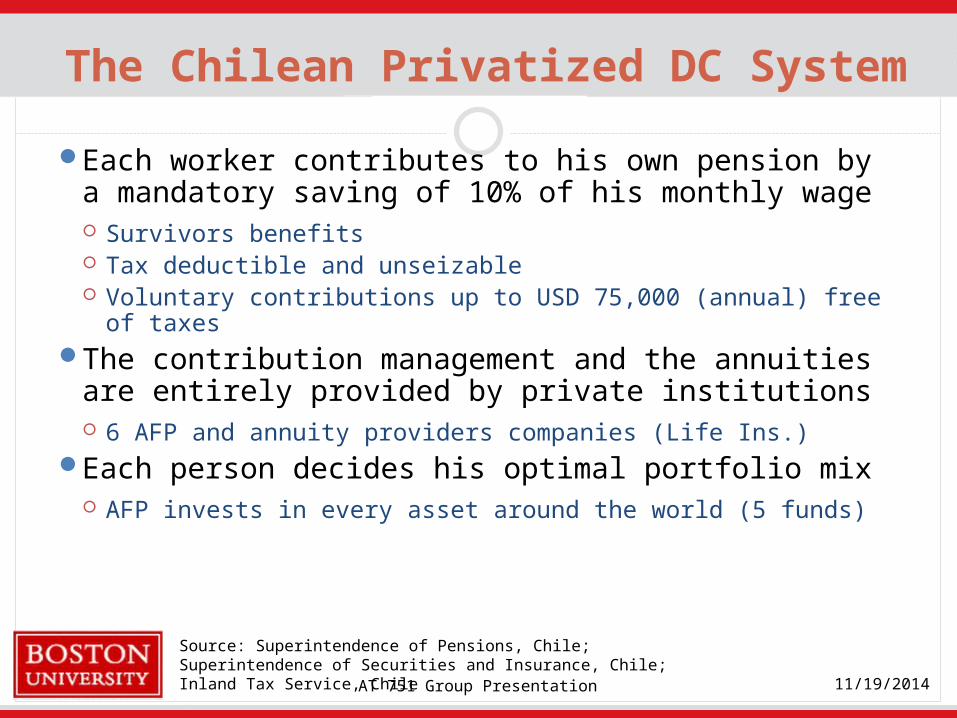

The Chilean Privatized DC System

Each worker contributes to his own pension by a mandatory saving of 10% of his monthly wage Survivors benefits Tax deductible and unseizable Voluntary contributions up to USD 75,000 (annual) free of

taxesThe contribution management and the annuities

are entirely provided by private institutions 6 AFP and annuity providers companies (Life Ins.)

Each person decides his optimal portfolio mix AFP invests in every asset around the world (5 funds)

Source: Superintendence of Pensions, Chile; Superintendence of Securities and Insurance, Chile; Inland Tax Service, Chile

AT 751 Group Presentation 11/19/2014

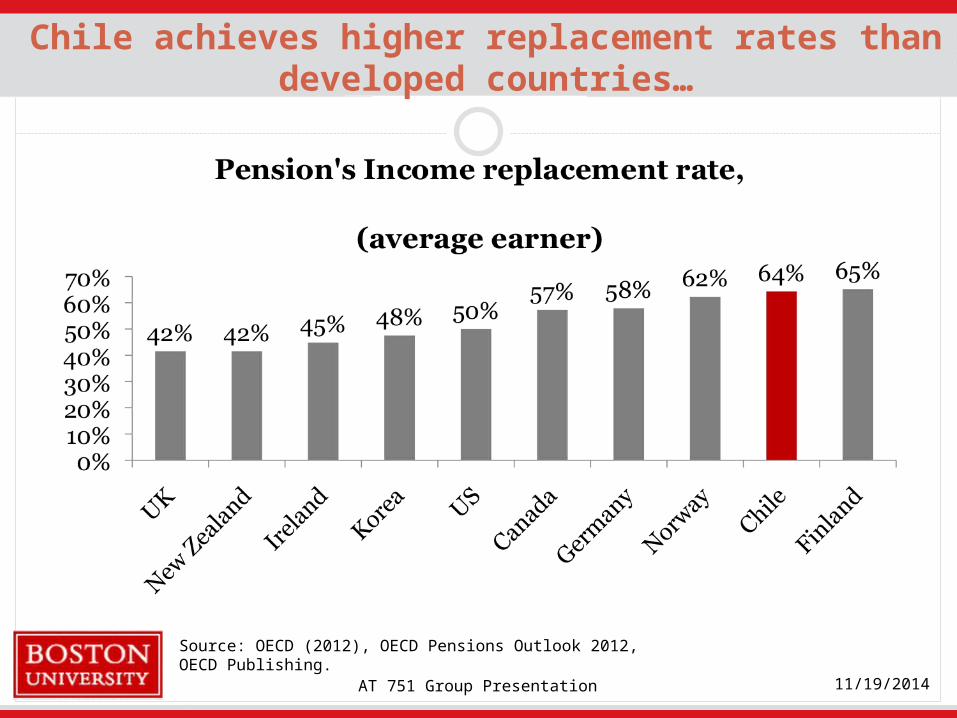

Chile achieves higher replacement rates than developed countries…

Source: OECD (2012), OECD Pensions Outlook 2012, OECD Publishing.

AT 751 Group Presentation 11/19/2014

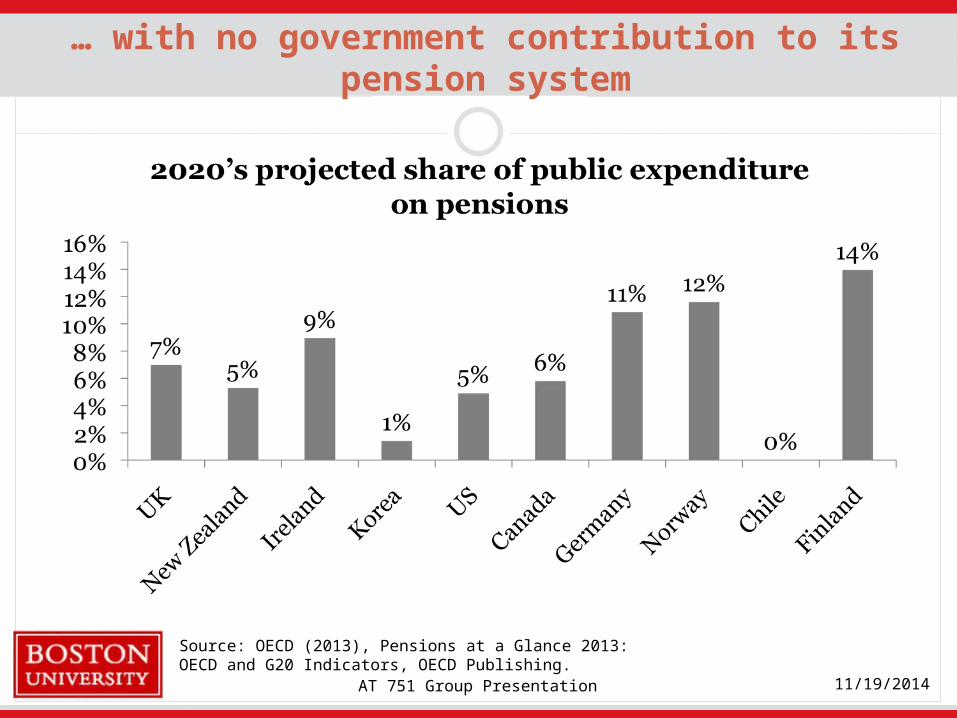

… with no government contribution to its pension system

Source: OECD (2013), Pensions at a Glance 2013: OECD and G20 Indicators, OECD Publishing.

AT 751 Group Presentation 11/19/2014

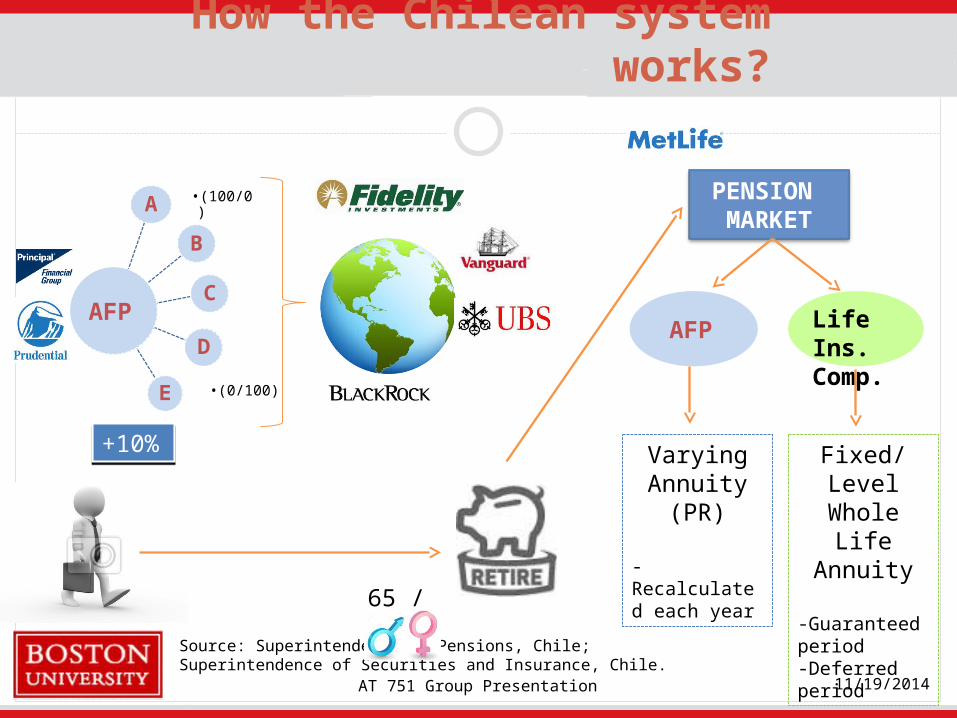

How the Chilean system works?

A •(100/0)

B

E •(0/100)

C

D

AFP

+10%+10%

65 / 60

PENSION MARKET

AFP Life Ins.Comp.

Fixed/Level Whole Life

Annuity

-Guaranteed period -Deferred period

Varying Annuity

(PR)

- Recalculated each year

Source: Superintendence of Pensions, Chile; Superintendence of Securities and Insurance, Chile.

AT 751 Group Presentation 11/19/2014

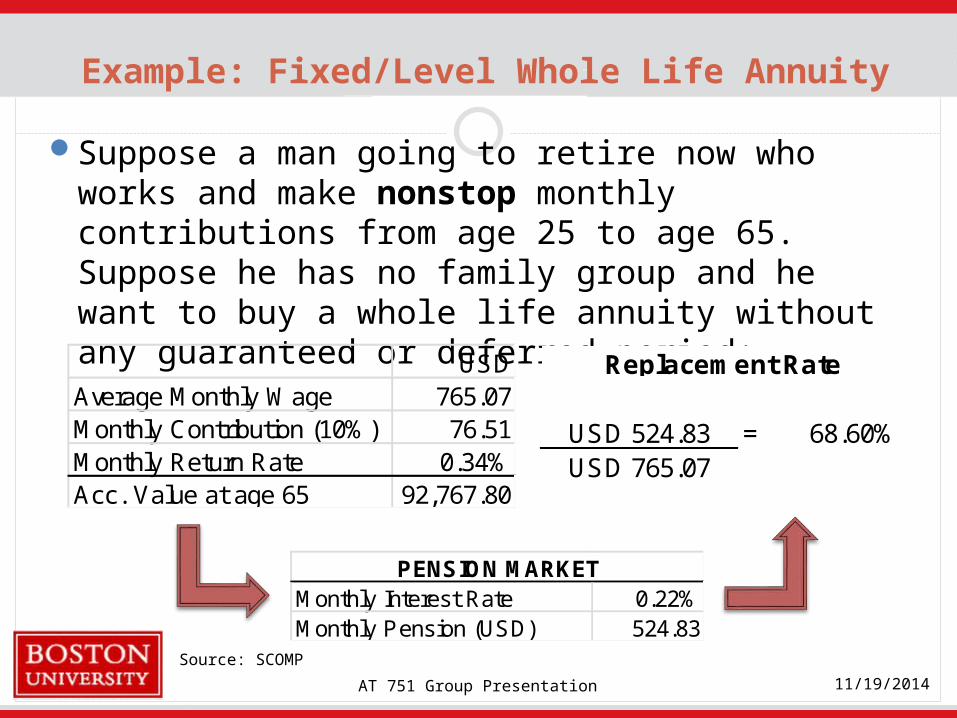

Example: Fixed/Level Whole Life Annuity

Suppose a man going to retire now who works and make nonstop monthly contributions from age 25 to age 65. Suppose he has no family group and he want to buy a whole life annuity without any guaranteed or deferred period:

Monthly Interest Rate 0.22%Monthly Pension (USD) 524.83

PENSION MARKET

USD 524.83 = 68.60%USD 765.07

Replacement RateUSDAverage Monthly Wage 765.07Monthly Contribution (10%) 76.51Monthly Return Rate 0.34%Acc. Value at age 65 92,767.80

Source: SCOMP

The Chilean Pension System is privately run with no government involvement 6 AFP and insurance co.

The system achieves high replacement rates for those who contribute as planned Failing to contribute as

planned results in low pensions

Thanks, Mr. Piñera!

José Piñera (Phd in Economics, Harvard;BU Assistant Professor, 1974)

Summary: Chilean DC System

AT 751 Group Presentation 11/19/2014

Bibliography

Superintendence of Pensions, Chile Superintendence of Securities and Insurance, Chile Inland Tax Service, Chile The System and Pensions Level in Chile: Proposals for their Improvements, K.

Schmidt-Hebbel Social Security, Nolan et al. UN Population Division ILO (International Labor Organization) CASS (Chinese Academy of Social Sciences) MHRSS (Ministry of Human Resources and Social Security) Paying for the Gray – The Economist Why Time is Running Out on China’s Social Security System – Yueran Zhang,

TeaLeafNation http://hi.people.com.cn/n/2014/0311/c231190-20748018.htm OECD (2012), OECD Pensions Outlook 2012, OECD Publishing. OECD (2013), Pensions at a Glance 2013: OECD and G20 Indicators, OECD

Publishing. McGill D M, Brown K N, Haley J J, Fundamentals of private pensions(2009)

AT 751 Group Presentation 11/19/2014

Thank You!