basel iibanking

TRANSCRIPT

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 1/22

BASEL II ACCORD:BASEL II ACCORD:

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 2/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 3/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 4/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 5/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 6/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 7/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 8/22

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 9/22

Reasons

Demand for credit from corporate hasbeen a lackluster

Enactment of the SARFESI Act

Banks have been more cautious in lending Demand for corporate credit has beenjaded hence banks have parked theirsurplus in government securities

Treasury income of banks have increasedfor 95 bn in FY02 to 195 bn in FY04

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 10/22

Backdrop

The BASEL Committee was establishedin 1974 as a group of 10 members

The main objective was to formulatebroad Supervisory Standards &Guidelines

The BC does not have any legal binding & it recommends Best practices

In 1988 the committee introducedcapital measurement system commonly referred to as the BASEL CapitalAccord

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 11/22

Why BASEL II ???

There was need felt that contemporary

norms were not in coherence with the

changing needs of risk managementThe banks were in expansion face due

to liberalization and globalization

The globalization had paved way forintroduction of new norms

Align country led policies with

international best practices

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 12/22

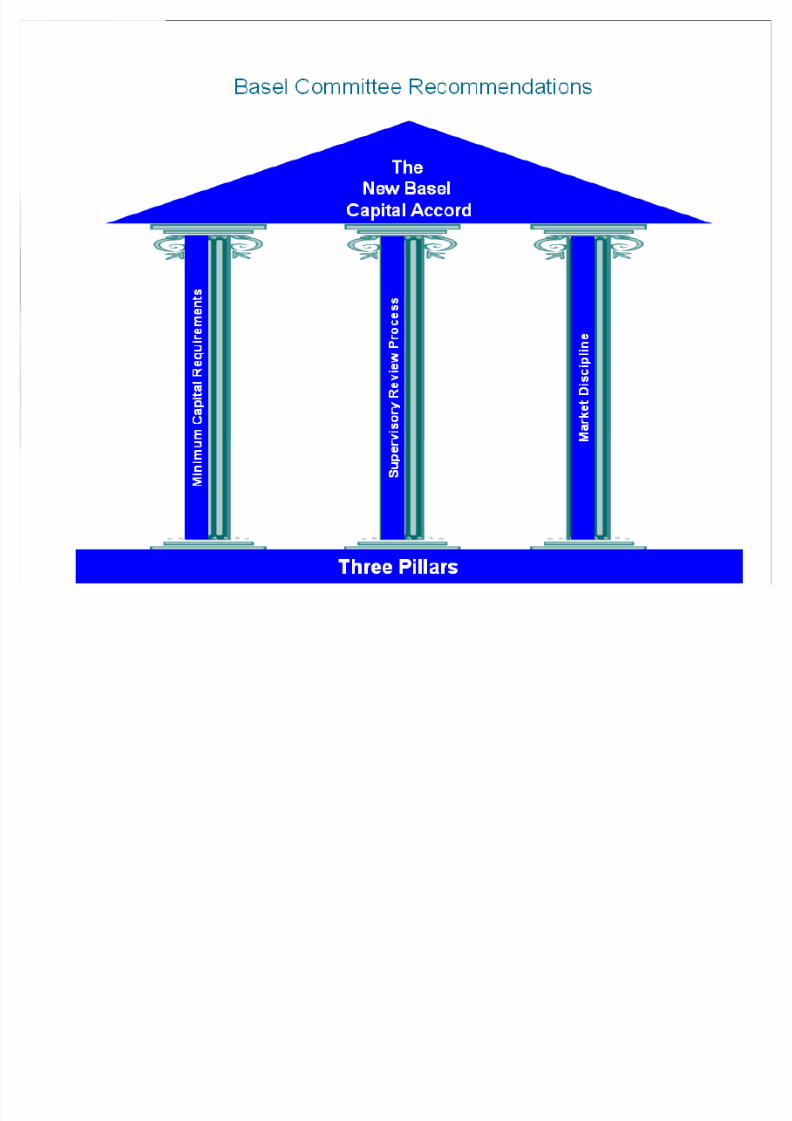

BASEL II Accord

It was introduced in June 1999

It consists of three pillars

Pillar 1: Capital requirementPillar 2: Operational Risk

Pillar 3: Market Risk

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 13/22

Issues involving CorporateGovernance in RIL

Authority withdrawn from theboard members without informing

the statutory authorities.Allotment of shares of relianceinfocomm to Mukesh Ambani @Rs.1 per share

Are there any regulatory provisionswith regard to annulment shares

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 14/22

ETHICAL ISSUES

Routing the ISD calls as domesticones and unethically parting away

with the legitimate share of revenues of BSNL

Buyback Vs Bonus

Family stake Vs Public Interest

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 15/22

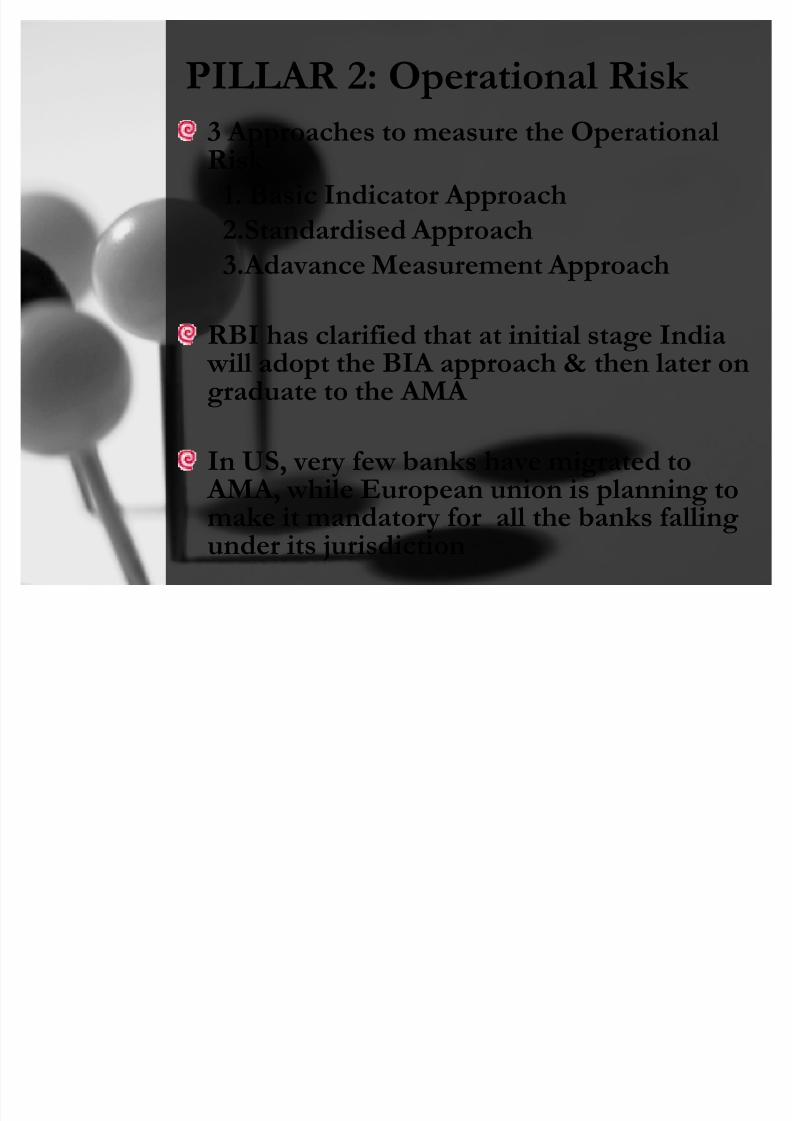

PILLAR 2: Operational Risk

3 Approaches to measure the OperationalRisk

1. Basic Indicator Approach

2.Standardised Approach

3.Adavance Measurement Approach

RBI has clarified that at initial stage Indiawill adopt the BIA approach & then later ongraduate to the AMA

In US, very few banks have migrated toAMA, w hile European union is planning tomake it mandatory for all the banks falling

under its jurisdiction

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 16/22

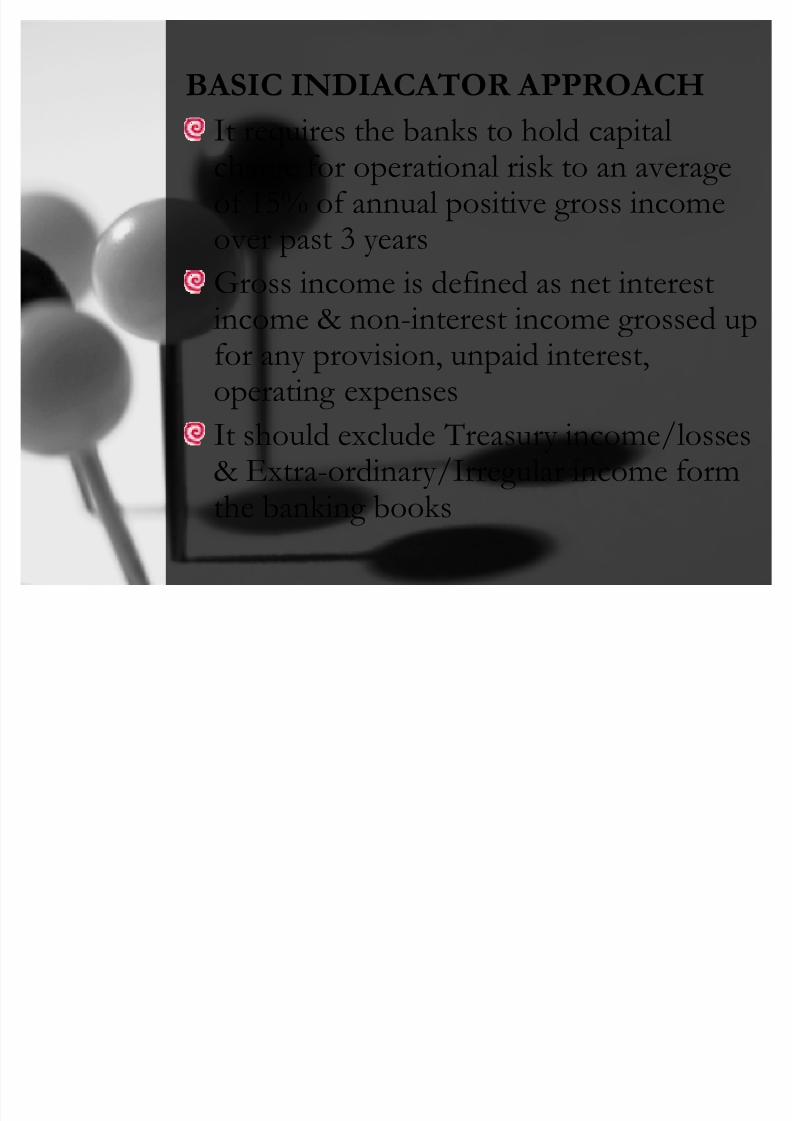

BASIC INDIACATOR A PPROACH

It requires the banks to hold capitalcharge for operational risk to an averageof 15% of annual positive gross incomeover past 3 years

Gross income is defined as net interestincome & non-interest income grossed upfor any provision, unpaid interest,operating expenses

It should exclude Treasury income/losses& Extra-ordinary/Irregular income formthe banking books

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 17/22

BASIC INDIACATOR A PPROACH

As per ICRA·s estimate Indian bankswill need additional capital to an extentof Rs.120 billion to meet the capitalcharge requirement for operational risk under BASEL II normsMost of this capital is required by PublicSector Banks

details with respect to all categories of banks {PSU, Pvt} have been annexedas a part of report on page no. 45

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 18/22

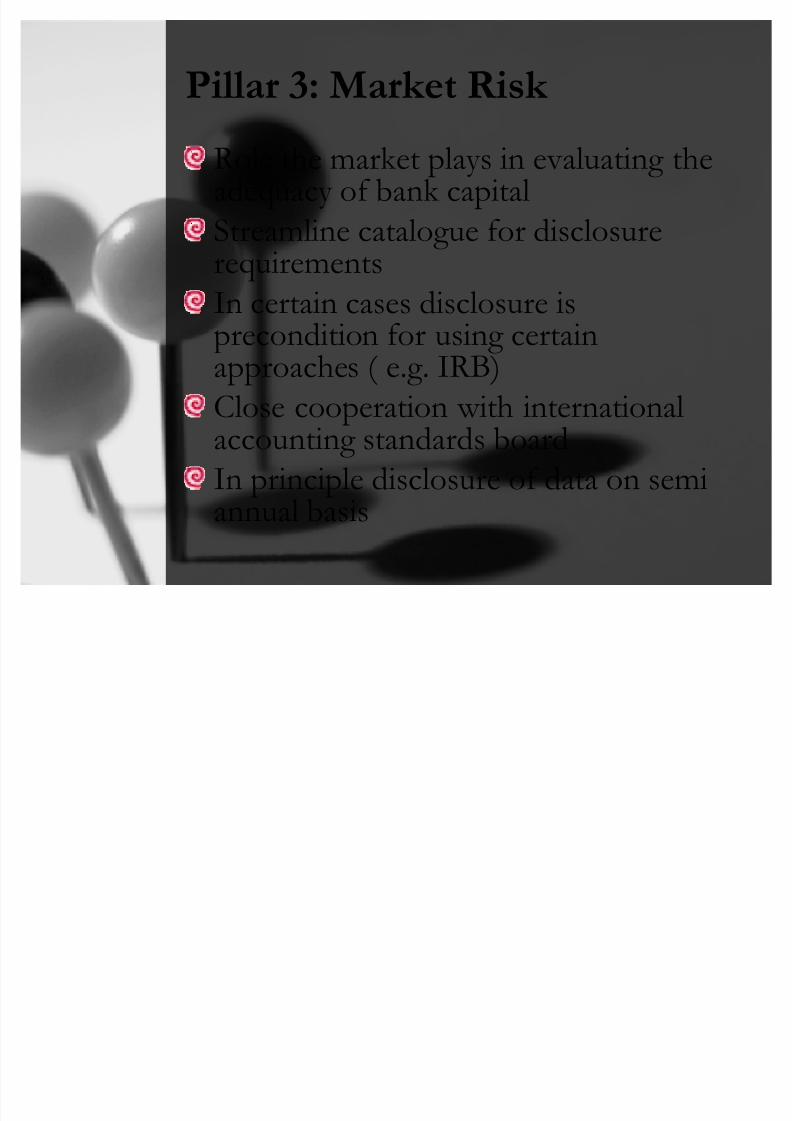

Pillar 3: Market Risk

Role the market plays in evaluating theadequacy of bank capital

Streamline catalogue for disclosure

requirementsIn certain cases disclosure isprecondition for using certainapproaches ( e.g. IRB)

Close cooperation with internationalaccounting standards board

In principle disclosure of data on semiannual basis

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 19/22

BASEL I Vs BASEL II

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 20/22

Roadblocks

Standardized approach and externalcredit rating agenciesDifficulties in implementing IRB

based credit risk managementCost of IT nearly 70% of cost of implementation

Multiple supervisory bodies visIRDA, SEBI, RBI etc

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 21/22

Basel II

A Way forward {IMPACT}

Improved Risk Management &Capital Adequacy

Curtailment of credit toinfrastructure projects

Preference for mortgage credit toconsumer credit

8/7/2019 basel iibanking

http://slidepdf.com/reader/full/basel-iibanking 22/22

Recommendations

Government·s initiatives for smootherimplementation of BASEL II norms

Relax the limits for exposure of banks

to the capital marketsClear road map for implementation

Capitalization & Depreciation of capital

expenditure on ITTraining of professional from ICAI,ICSI for risk management audits