bot 介紹. 課程重點 何謂 project finance 何謂 bot...

TRANSCRIPT

BOT 介紹

課程重點• 何謂 Project Finance

• 何謂 BOT

• 台灣促進民間參與重大公共建設• 台灣 BOT 案例

Project Finance

• The objective of using project financing to raise capital is to create a structure that is bankable (of interest to investors) and to limit the stakeholders’ risk by diverting some risks to parties that can better manage them.

• In project financing, an independent legal vehicle is created to raise the funds required for the project.

• Payment of principal, interest, dividends and operating expenses is derived from the project’s revenues and assets.

• The investors, in both debt and equity, require certain basic legal, regulatory and economic conditions throughout the life of the project.

Public finance• A government borrows funds to finance an infrastr

ucture project and gives a sovereign guarantee to lenders to repay all funds.

• Government may contribute its own equity in addition to the borrowed funds.

• Lenders analyse Government’s total ability to raise funds through taxation and general public enterprise revenues, including new tariff revenue from the project.

• The sovereign guarantee shows up as a liability on Government’s list of financial obligations.

Corporate finance• A private company borrows funds to

construct a new project and guarantees to repay lenders from its available operating income and its base of assets.

• The company may choose to contribute its own equity as well.

• In performing credit analysis, lenders look at the company’s total income from operations, its stock of assets, and its existing liabilities.

• The loan shows up as a liability on the company’s balance sheet.

Project finance• A team or consortium of private firms establish

a new project company to build, own and operate a specific infrastructure project.

• The new project company is capitalised with equity contributions from each of the sponsors.

• The project company borrows funds from lenders. The lenders look to the projected future revenue stream generated by the project and the project company’s assets to repay all loans.

• The host country government does not provide a financial guarantee to lenders; sponsoring firms provide limited guarantees.

• Project financing uses the project’s assets and/or future revenues as the basis for raising funds.

• Generally, the sponsors create a special purpose, legally independent company in which they are the principal shareholders.

• The newly created company usually has the minimum equity required to issue debt at a reasonable cost, with equity generally averaging between 10 and 30 per cent of the total capital required for the project.

• Individual sponsors often hold a sufficiently small share of the new company’s equity, to ensure that it cannot be construed as a subsidiary for legal and accounting purposes.

The legal vehicle (company) frequently has more than one sponsor, generally because:

• the project exceeds the financial or technical capabilities of one sponsor

• the risks associated with the project have to be shared

• a larger project achieves economies of scale that several smaller projects will not achieve

• the sponsors complement each other in terms of capability

• the process requires or encourages a joint venture with certain interests (e.g. local participation or empowerment)

• the legal and accounting rules stipulate a maximum equity position by a sponsor, above which the project company will be considered a subsidiary.

Project funding alternative

• Common equity represents ownership of the project. The sponsors usually hold a significant portion of the equity in the project.

• Preferred equity.• Convertible debt• Unsecured debt 信用貸款• Secured debt may also be short- or long-te

rm and is secured by specific assets or sources of revenues.

• Lease financing. Tax issues and the strength of the collateral are usually the driving forces behind a lease strategy.

BOT

A shortage of funds is one of the principal reasons governments have

turned to this method.

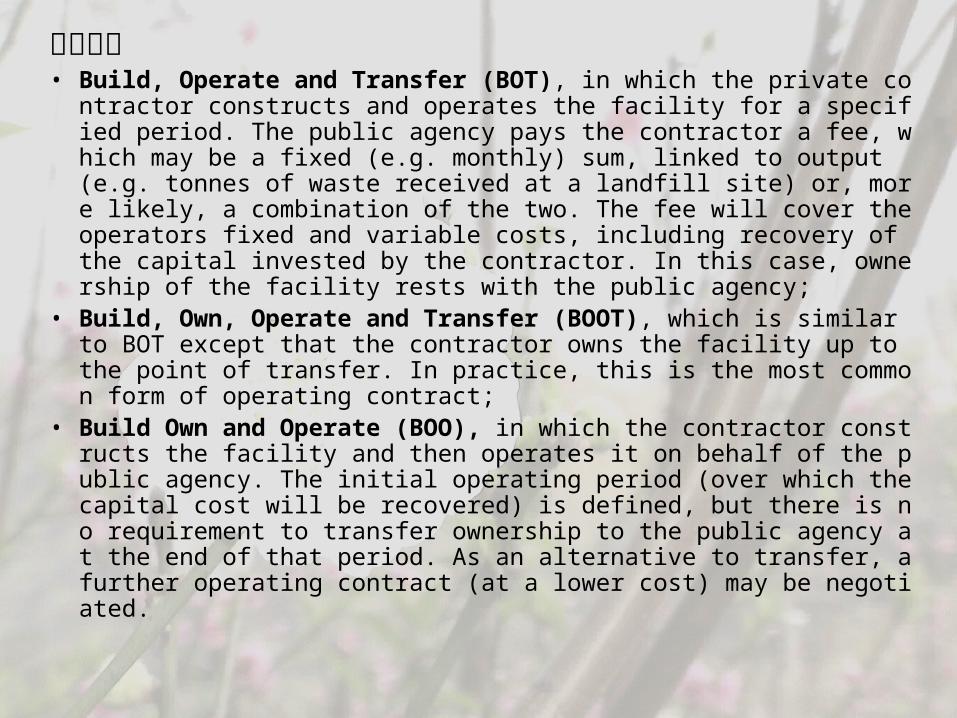

契約種類• Build, Operate and Transfer (BOT), in which the private contractor

constructs and operates the facility for a specified period. The public agency pays the contractor a fee, which may be a fixed (e.g. monthly) sum, linked to output (e.g. tonnes of waste received at a landfill site) or, more likely, a combination of the two. The fee will cover the operators fixed and variable costs, including recovery of the capital invested by the contractor. In this case, ownership of the facility rests with the public agency;

• Build, Own, Operate and Transfer (BOOT), which is similar to BOT except that the contractor owns the facility up to the point of transfer. In practice, this is the most common form of operating contract;

• Build Own and Operate (BOO), in which the contractor constructs the facility and then operates it on behalf of the public agency. The initial operating period (over which the capital cost will be recovered) is defined, but there is no requirement to transfer ownership to the public agency at the end of that period. As an alternative to transfer, a further operating contract (at a lower cost) may be negotiated.

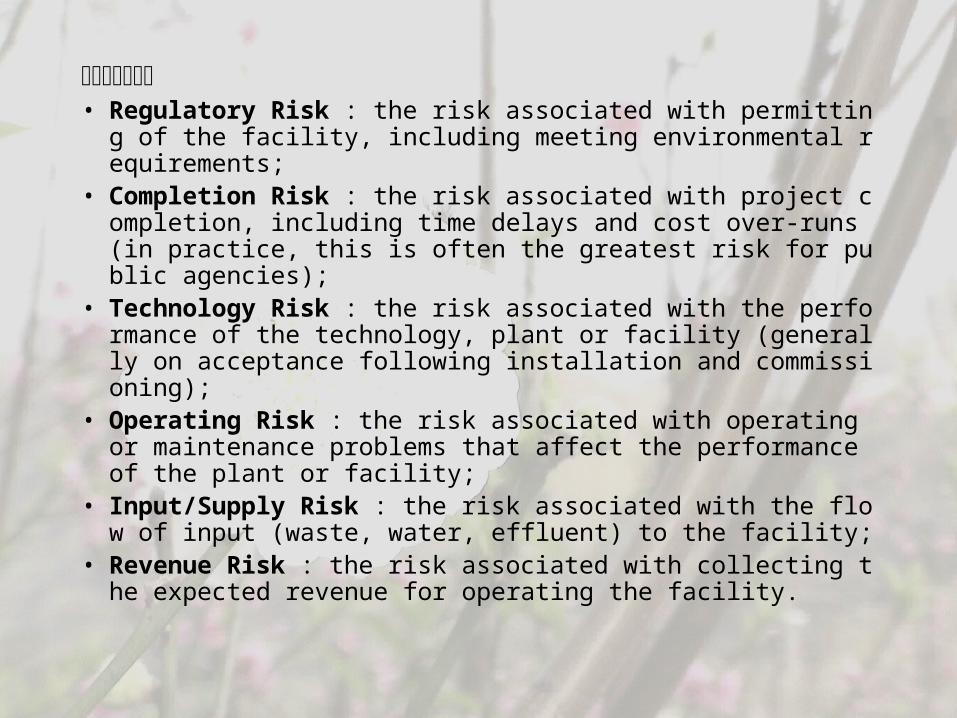

民民民民民民民• Regulatory Risk : the risk associated with permitting of the

facility, including meeting environmental requirements;• Completion Risk : the risk associated with project completi

on, including time delays and cost over-runs (in practice, this is often the greatest risk for public agencies);

• Technology Risk : the risk associated with the performance of the technology, plant or facility (generally on acceptance following installation and commissioning);

• Operating Risk : the risk associated with operating or maintenance problems that affect the performance of the plant or facility;

• Input/Supply Risk : the risk associated with the flow of input (waste, water, effluent) to the facility;

• Revenue Risk : the risk associated with collecting the expected revenue for operating the facility.

台灣促進民間參與重大公共建設

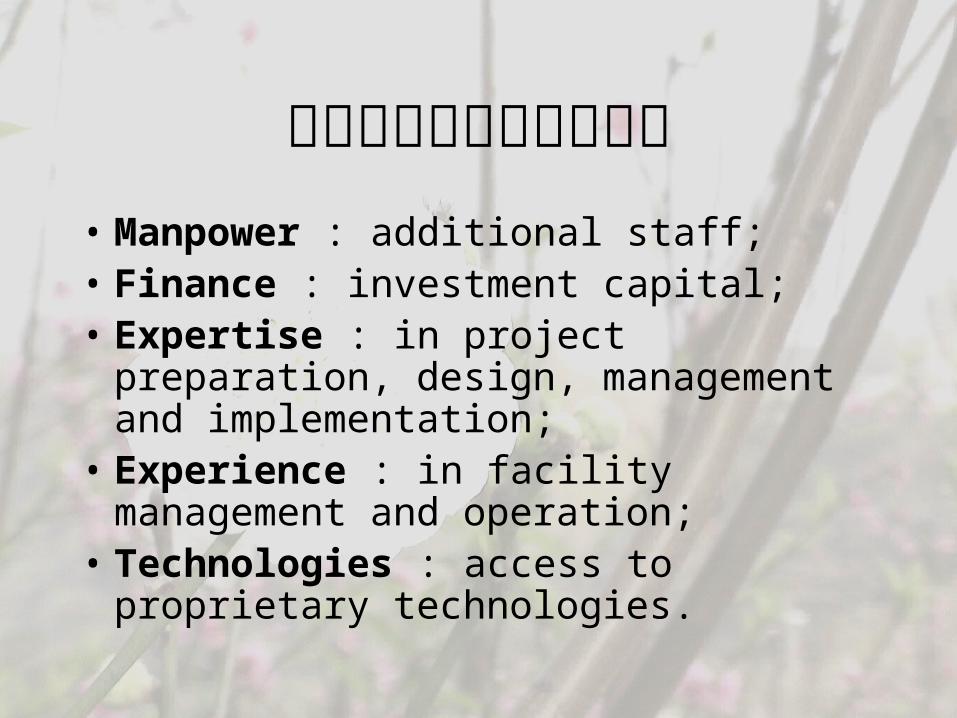

民間參與公共建設的考量• Manpower : additional staff;• Finance : investment capital;• Expertise : in project preparation, design,

management and implementation;• Experience : in facility management and

operation;• Technologies : access to proprietary

technologies.

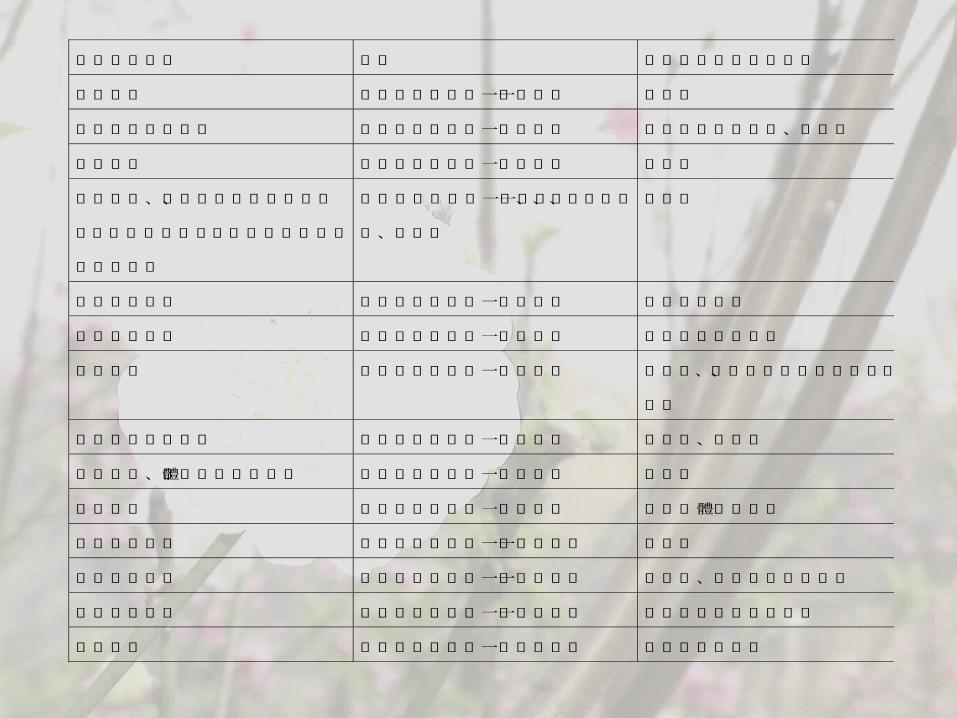

公共建設類別 依據 中央目的事業主管機關

交通建設 促參法第三條第一項第一款 交通部

環境污染防治設施 促參法第三條第一項第二款 行政院環境保護署、內政部

水利設施 促參法第三條第一項第三款 經濟部

共同管道、污水下水道、自來水設

施、社會福利設施、公園綠地設施、

新市鎮開發

促參法第三條第一項第一、三、五、

十、十二款

內政部

衛生醫療設施 促參法第三條第一項第四款 行政院衛生署

勞工福利設施 促參法第三條第一項第五款 行政院勞工委員會

文教設施 促參法第三條第一項第六款 教育部、行政院文化建設委員會、內

政部

觀光遊憩重大設施 促參法第三條第一項第七款 交通部、內政部

電業設施、公用氣體燃料設施 促參法第三條第一項第八款 經濟部

運動設施 促參法第三條第一項第九款 行政院體育委員會

重大工業設施 促參法第三條第一項第十一款 經濟部

重大商業設施 促參法第三條第一項第十一款 經濟部、行政院農業委員會

重大科技設施 促參法第三條第一項第十一款 行政院國家科學委員會

農業設施 促參法第三條第一項第十三款 行政院農業委員

民間參與的步驟

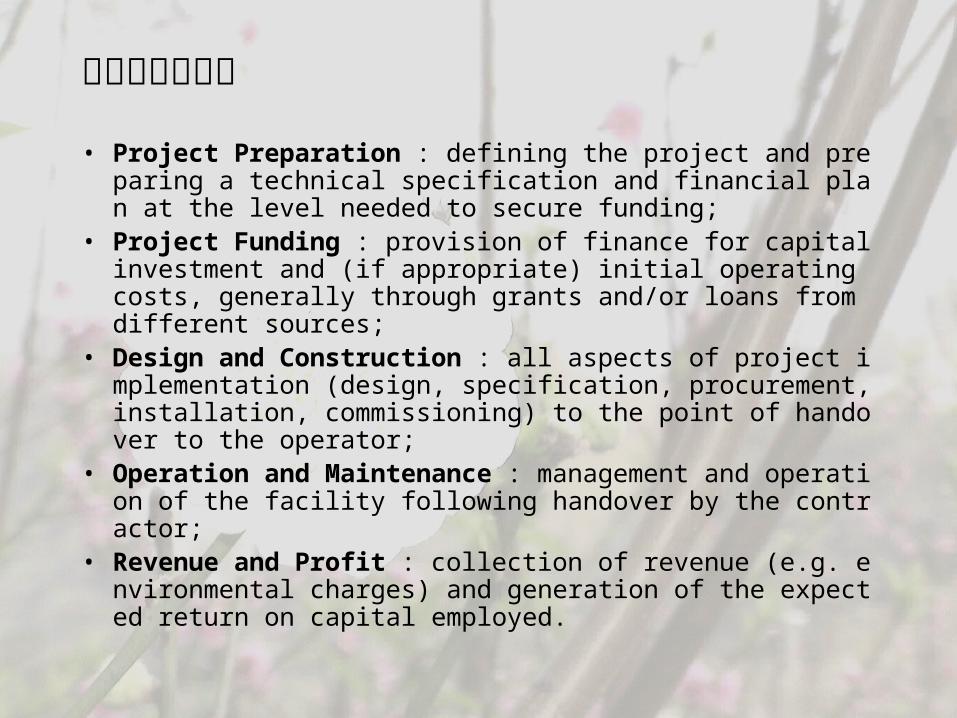

• Project Preparation : defining the project and preparing a technical specification and financial plan at the level needed to secure funding;

• Project Funding : provision of finance for capital investment and (if appropriate) initial operating costs, generally through grants and/or loans from different sources;

• Design and Construction : all aspects of project implementation (design, specification, procurement, installation, commissioning) to the point of handover to the operator;

• Operation and Maintenance : management and operation of the facility following handover by the contractor;

• Revenue and Profit : collection of revenue (e.g. environmental charges) and generation of the expected return on capital employed.

民間可參與的內容• Technical Assistance, mainly focused on P

roject Preparation;• Private Finance, mainly focused on Project

Funding;• Turnkey Contract, mainly focused on Desi

gn and Construction;• Operating Contracts, mainly focused on O

peration and Maintenance;• Full Privatisation, mainly focused on Reve

nue and Profit.

BOT 案例

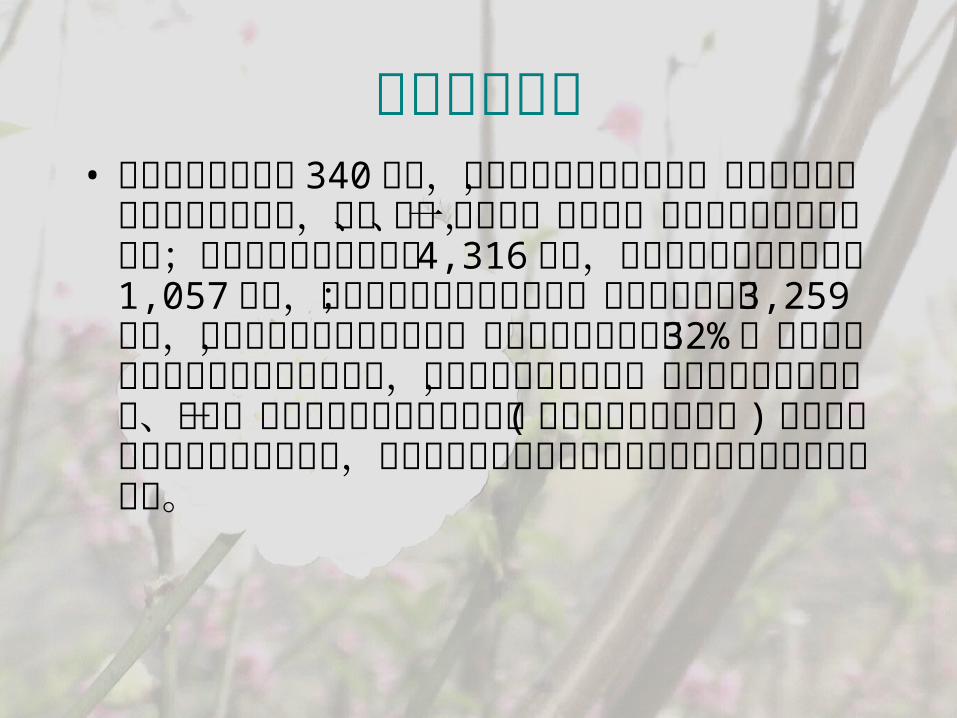

南北高速鐵路• 台灣高速鐵路全長 340 公里,沿線共經過十四個

縣市,端點為台北市及高雄市兩大城市,北、中、南各設一調車場,主要的維修基地設於南部;高鐵總工程經費新台幣 4,316 億元,其中政府必須辦理事項為 1,057 億元,主要用於購地及拆遷補償;民間投資額度為 3,259 億元,其中土木工程為最大部份,佔高鐵總工程經費之 32% 。為了減少介面整合的困難與不確定性,及有效掌控興建時程,除了高鐵建設用地取得、南港-板橋段路線地下化土建工程 ( 不含軌道及機電設施 ) 及管理與監督由政府負責辦理外,民間投資範圍涵蓋其他所有高鐵計畫工程之設計及施工。

高鐵民間投資案甄審作業分為兩階段辦理:• 第一階段為申請人資格審查,以確定有興趣參與

本案的民間投資者,並瞭解其組成、工作經驗實績,以及企劃構想,本階段僅衡量其興建營運能力,不作優劣評比。有台灣高鐵企業聯盟與中華高鐵企業聯盟兩家合格。

• 第二階段則由合格申請人與高鐵局充分討論協商,讓合格申請人瞭解政府的實際需求,提出成熟的投資計畫,再行甄審評決。就合格申請人之興建能力、營運能力、公司組織健全性、財務計畫可行性、附屬事業收入、權利金支付額度、要求政府投資額度及其他等項目進行評審。按「最有利於政府之條件」及「需要政府投資額度最少」等標準綜合審議,評定台灣高速鐵路企業聯盟所提申請案為最優申請案件。

中正機場至台北捷運系統• 為提高民間參與之誘因,本案採端點固定、中

間路線容許民間機構規劃調整之方式辦理。• 初審有聯捷交通事業、上慶捷運、長生國際開發、台聯捷運及中華工程等五家通過成為合格申請人

• 第二階段之甄審,由長生國際開發股份有限公司籌備處獲選為最優申請案件申請人,中華工程股份有限公司及上慶捷運股份有限公司則分別為第一及第二順位次優申請人。

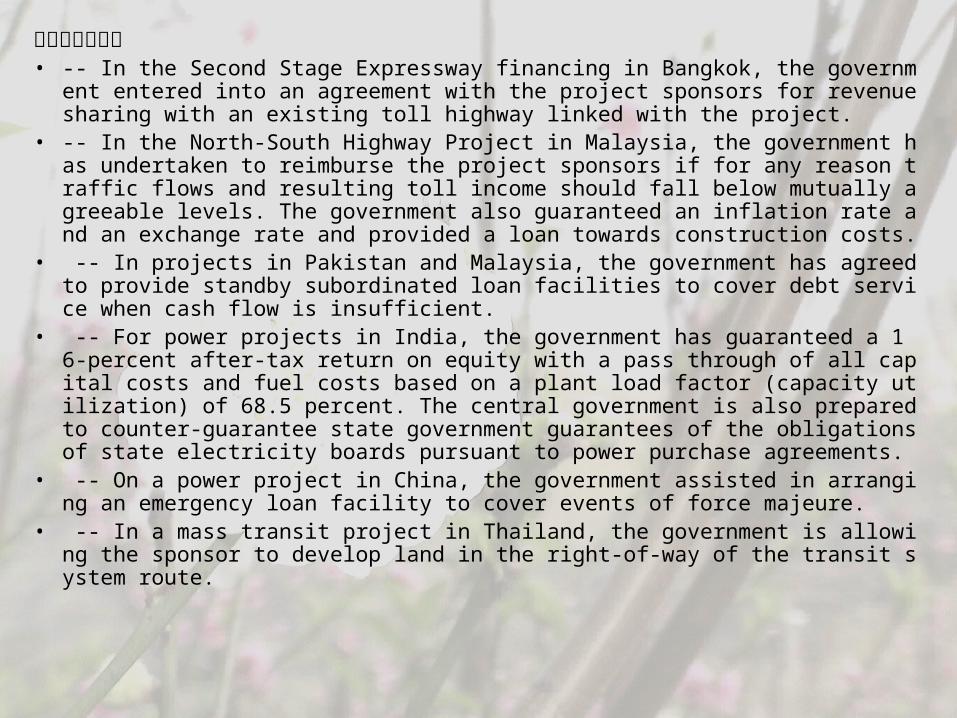

政府的協助案例• -- In the Second Stage Expressway financing in Bangkok, the government entered

into an agreement with the project sponsors for revenue sharing with an existing toll highway linked with the project.

• -- In the North-South Highway Project in Malaysia, the government has undertaken to reimburse the project sponsors if for any reason traffic flows and resulting toll income should fall below mutually agreeable levels. The government also guaranteed an inflation rate and an exchange rate and provided a loan towards construction costs.

• -- In projects in Pakistan and Malaysia, the government has agreed to provide standby subordinated loan facilities to cover debt service when cash flow is insufficient.

• -- For power projects in India, the government has guaranteed a 16-percent after-tax return on equity with a pass through of all capital costs and fuel costs based on a plant load factor (capacity utilization) of 68.5 percent. The central government is also prepared to counter-guarantee state government guarantees of the obligations of state electricity boards pursuant to power purchase agreements.

• -- On a power project in China, the government assisted in arranging an emergency loan facility to cover events of force majeure.

• -- In a mass transit project in Thailand, the government is allowing the sponsor to develop land in the right-of-way of the transit system route.