chinese outbound investment trends' by bank of china international at mines and money hong kong...

TRANSCRIPT

Presented at:

www.minesandmoney.com/hongkong

2013中国矿业海外投资趋势中国矿业海外投资趋势中国矿业海外投资趋势中国矿业海外投资趋势

程雁程雁程雁程雁

董事总经理董事总经理董事总经理董事总经理

投资银行部副主席投资银行部副主席投资银行部副主席投资银行部副主席

全球高级客户全球高级客户全球高级客户全球高级客户/市场总监市场总监市场总监市场总监

2013 China Mining Overseas Investments Trends

Amy Cheng

Managing DirectorVice Chairman, Investment Banking DivisionHead of Senior Clients Relationship Management / Marketing

目录目录目录目录

第一章第一章第一章第一章 中国对外投资现状中国对外投资现状中国对外投资现状中国对外投资现状4

第二章第二章第二章第二章 中国宏观经济发展趋势以及对矿业影响中国宏观经济发展趋势以及对矿业影响中国宏观经济发展趋势以及对矿业影响中国宏观经济发展趋势以及对矿业影响16

第三章第三章第三章第三章 中国矿业海外投资趋势中国矿业海外投资趋势中国矿业海外投资趋势中国矿业海外投资趋势30

第四章第四章第四章第四章 对外投资中存在的问题与解决方法对外投资中存在的问题与解决方法对外投资中存在的问题与解决方法对外投资中存在的问题与解决方法40

第五章第五章第五章第五章 中银国际的业务优势中银国际的业务优势中银国际的业务优势中银国际的业务优势44

3

Table of Contents

Chapter One China Overseas Investments Review 5

Chapter Two China Macroeconomics Trend and Impacts on Mining Sector

17

Chapter Three China Overseas Investments Trend Analysis 31

Chapter Four Problems and Solutions in China Oversea Investment

41

Chapter Five Strategic advantages of BOCI 45

4

第一第一第一第一章章章章::::中国对外投资现状中国对外投资现状中国对外投资现状中国对外投资现状

5

Chapter One: China Overseas Investments Review

6

9.9

20.7

30.1

54.0 51.7

66.0

74.579.7

1 2 3 4 5 6 7 8

中国境外投中国境外投中国境外投中国境外投资资资资趋势趋势趋势趋势增增增增速明显速明显速明显速明显

7

2005 2006 2007 2008 2009 2010 2011 2012

能源和电力48%金属

23%

金融10%

房地产和建筑6%

交通4%

农业3%

科技2%

化工2%

其他2%

� 中国企业“走出去”是近年来中国对外开放快速发展的新领

域,也是中外经贸合作进一步深化的新亮点,发展的势头举

世瞩目

� 自2005年以来,中国企业境外投资总额已达到3,866亿美元,

年复合增长率保持在34.3%;其中仅2012年境外投资总额就

将近800亿美元

� 从投资领域来看,能源和电力、金属以及金融三个行业的投

资额占总投资额的81%

单位:十亿美元

资料来源:券商研究报告

Fast Growth Trend Of China Overseas Investments

8

9.9

20.7

30.1

54.0 51.7

66.0

74.579.7

1 2 3 4 5 6 7 82005 2006 2007 2008 2009 2010 2011 2012

� China’s “Going abroad” grand strategy has been

implemented for over decades. The outbound investments

from China have been growing at an unparallel speed in

recent years

� Since 2005, total overseas investments of Chinese entities

have made US$386 billion, among which US$80 billion was

invested in 2012. The compound annual growth keeps at a

rate of 34.3%

� From an industry perspective, investment appetite falls into

energy and power, metal and finance , which account for

81% of total investment

Source: Brokerage reports

Energy and Power48%

Metal 23%

Finance10%

Real Estate 6%

Transportation4%

Agricultrue3%

Technology2%

Chemical Industrial

2% Others 2%

(In billion USD)

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)中国对外投资中国对外投资中国对外投资中国对外投资2012年年度回顾年年度回顾年年度回顾年年度回顾

9

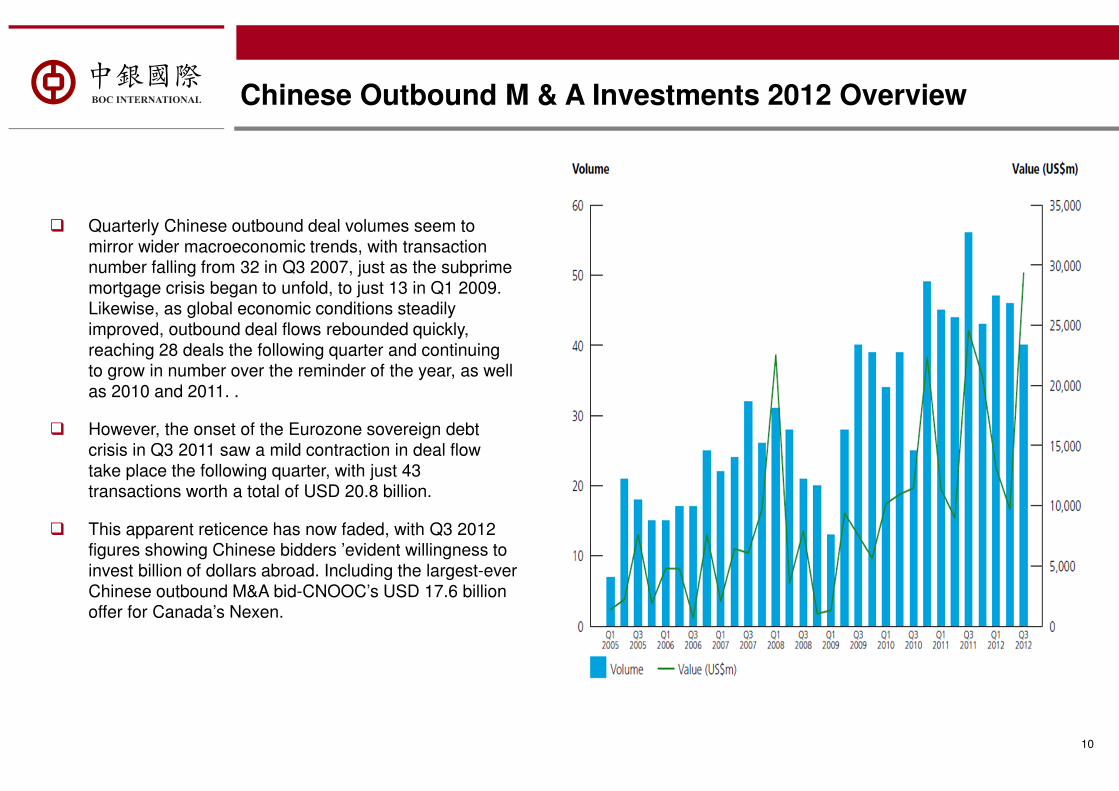

� 中国各季度的对外并购交易量反映出更为广泛的宏观

经济趋势:交易量从2007年第三季度(次贷危机影响

开始显现时)的32宗降至2009年第一季度仅13宗。另

外,随着全球经济形式复苏,对外并购交易迅速回暖

:第一季度达到28宗,余下的季度以及2012年至2011

年的交易量继续增长。

� 然而2011年第三季度欧元区主权债务危机的出现导致

随后季度的交易活动出现小幅度收缩:交易为43宗,

总交易额为208亿美元。

� 2012年第三季度数据表明,中国竞购者对于数十亿美

元的对外投资项目有强烈意愿。其中,中海油斥资176

亿美元收购加拿大Nexen公司,成为有史以来最大一宗

中国对外并购交易。

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)Chinese Outbound M & A Investments 2012 Overview

10

� Quarterly Chinese outbound deal volumes seem to mirror wider macroeconomic trends, with transaction number falling from 32 in Q3 2007, just as the subprime mortgage crisis began to unfold, to just 13 in Q1 2009. Likewise, as global economic conditions steadily improved, outbound deal flows rebounded quickly, reaching 28 deals the following quarter and continuing to grow in number over the reminder of the year, as well as 2010 and 2011. .

� However, the onset of the Eurozone sovereign debt crisis in Q3 2011 saw a mild contraction in deal flow take place the following quarter, with just 43 transactions worth a total of USD 20.8 billion.

� This apparent reticence has now faded, with Q3 2012 figures showing Chinese bidders ’evident willingness to invest billion of dollars abroad. Including the largest-ever Chinese outbound M&A bid-CNOOC’s USD 17.6 billion offer for Canada’s Nexen.

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)中国对外并购投资行业分布中国对外并购投资行业分布中国对外并购投资行业分布中国对外并购投资行业分布

11

2005 – 2012年第三季度中国对外并购投资行业分布年第三季度中国对外并购投资行业分布年第三季度中国对外并购投资行业分布年第三季度中国对外并购投资行业分布((((按交易量计按交易量计按交易量计按交易量计))))

2005 – 2012年第三季度中国对外并购投资行业分布年第三季度中国对外并购投资行业分布年第三季度中国对外并购投资行业分布年第三季度中国对外并购投资行业分布((((按按按按交易额计交易额计交易额计交易额计))))

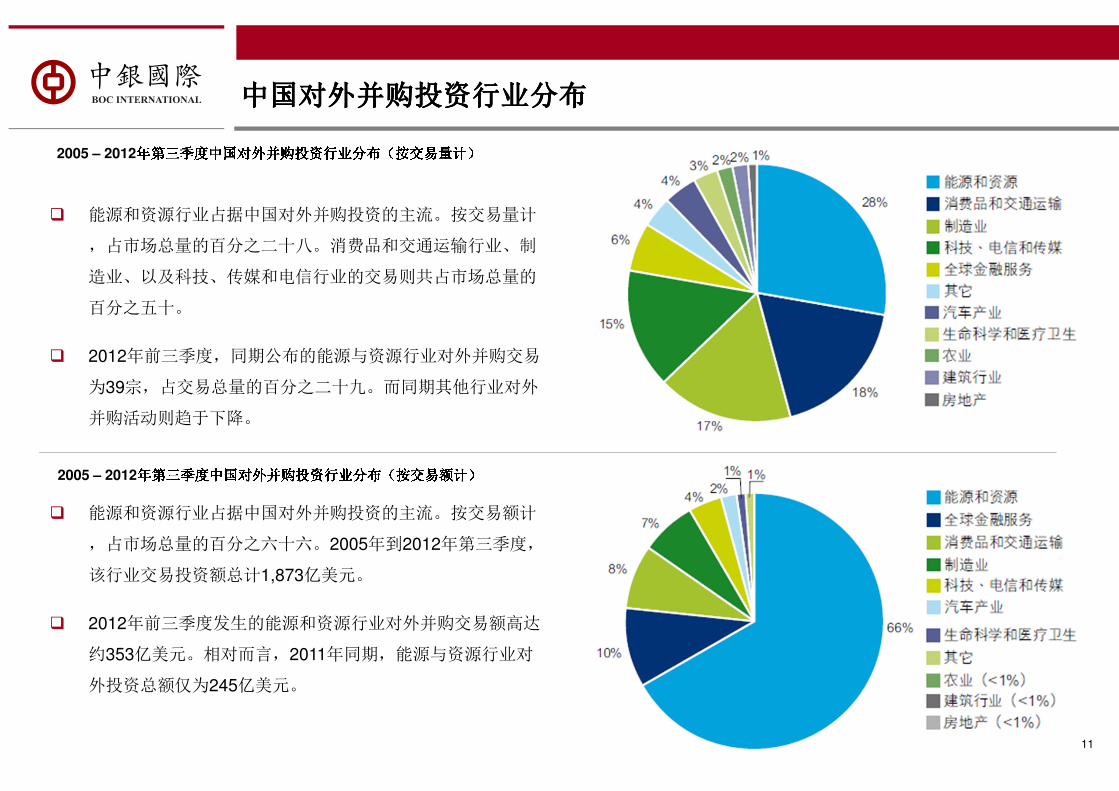

� 能源和资源行业占据中国对外并购投资的主流。按交易量计

,占市场总量的百分之二十八。消费品和交通运输行业、制

造业、以及科技、传媒和电信行业的交易则共占市场总量的

百分之五十。

� 2012年前三季度,同期公布的能源与资源行业对外并购交易

为39宗,占交易总量的百分之二十九。而同期其他行业对外

并购活动则趋于下降。

� 能源和资源行业占据中国对外并购投资的主流。按交易额计

,占市场总量的百分之六十六。2005年到2012年第三季度,

该行业交易投资额总计1,873亿美元。

� 2012年前三季度发生的能源和资源行业对外并购交易额高达

约353亿美元。相对而言,2011年同期,能源与资源行业对

外投资总额仅为245亿美元。

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)Chinese Outbound M & A Investments by Sector

12

2005 – Q3 2012 Chinese outbound M & A investments by sector (volume)

2005 – Q3 2012 Chinese outbound M & A investments by sector (value)

� The energy and resources industry continues to dominate Chinese outbound M & A investments, accounting 28 percent of the overall market by deal volume. Consumer Business & Transportation, Media & Telecommunication sector transactions make up a further 50 percent of the total.

� Acquiring foreign Energy & Resources assets has not waned over the first three quarters of 2012, with some 39 outbound transactions being announced over the period, accounting for 29 percent of all outbound deals by volume. Meanwhile, other industries show the decreasing trends in outbound M & A investments.

� The energy and resources deals made up 66 percent of all China outbound M & A investments in terms of value, with a total of US$ 187.3 billion being spent of on such deals between 2005 and Q3 2012.

� Over the Q1 – Q3 2012 period alone, some US$ 35.3 billion was spent on overseas Energy & Resources acquisitions. In contract, over the same period in 2011, outbound Energy & Resources investments by value totaled just US$ 24.5 billion.

12

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)中国对外并购投资行业分布中国对外并购投资行业分布中国对外并购投资行业分布中国对外并购投资行业分布(续续续续))))

13

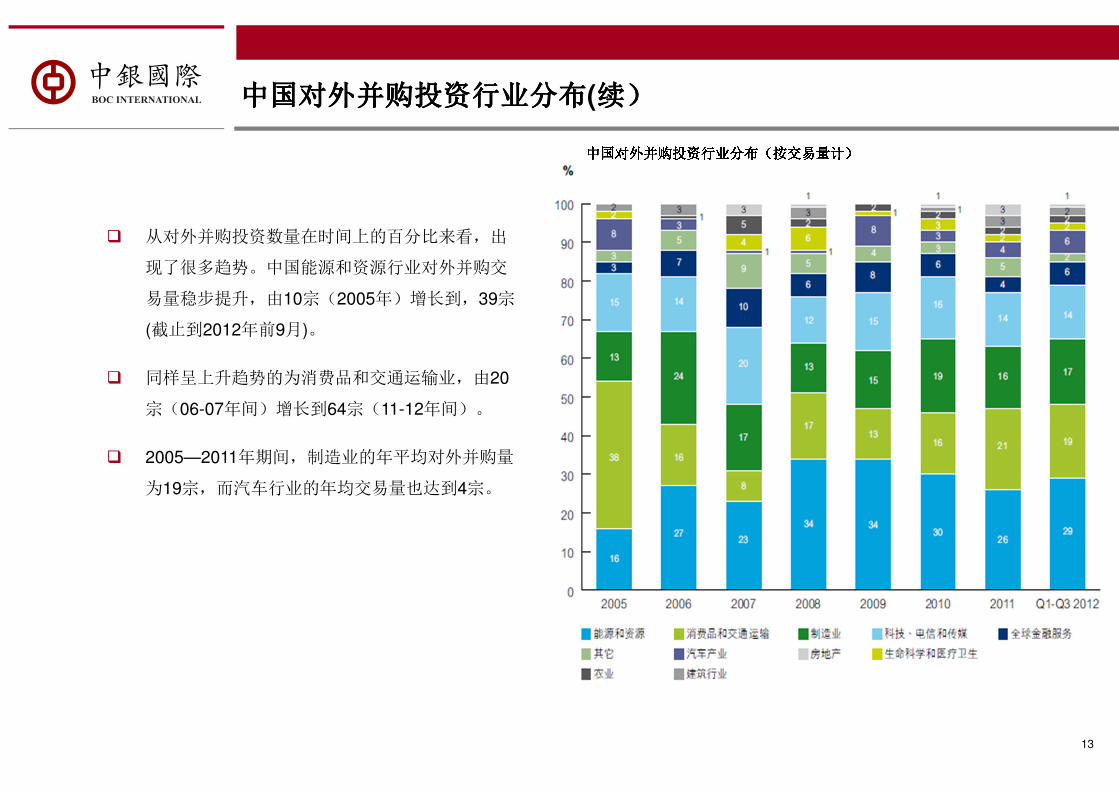

中国对外并购投资中国对外并购投资中国对外并购投资中国对外并购投资行业行业行业行业分布分布分布分布((((按交易量计按交易量计按交易量计按交易量计))))� 从对外并购投资数量在时间上的百分比来看,出

现了很多趋势。中国能源和资源行业对外并购交

易量稳步提升,由10宗(2005年)增长到,39宗

(截止到2012年前9月)。

� 同样呈上升趋势的为消费品和交通运输业,由20

宗(06-07年间)增长到64宗(11-12年间)。

� 2005—2011年期间,制造业的年平均对外并购量

为19宗,而汽车行业的年均交易量也达到4宗。

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)Chinese Outbound M & A Investments by Sector (Cont’d)

Chinese outbound M & A Investments by sector (volume)

� A number of trends emerge when looking at the

percentage distribution of outbound M&A

investments by volume over time. The sector of

China’s foreign Energy & Resource accounts for

a steady-growing proportion of overall outbound

transactions, increasing from 10 deals (2008) to

39 deals (until the first nine months of 2012).

� Consumer Business & Transportation industry

also showed an upward trend in transactions,

rising from 20 deals (06-07) to 64 deals (11-12).

� Over the seven years between 2005---2007,

Manufacturing sector had 19 transactions

annually, while the average number outbound of

Automotive sector was 4.

14

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)中国对外并购投资中国对外并购投资中国对外并购投资中国对外并购投资地区地区地区地区分布分布分布分布

15

2005 – 2012年第三季度中国对外并购投资地区分布年第三季度中国对外并购投资地区分布年第三季度中国对外并购投资地区分布年第三季度中国对外并购投资地区分布((((按交易量计按交易量计按交易量计按交易量计))))

2005 – 2012年第三季度中国对外并购年第三季度中国对外并购年第三季度中国对外并购年第三季度中国对外并购投资投资投资投资地区地区地区地区分布分布分布分布((((按按按按交易额计交易额计交易额计交易额计))))

� 按并购交易量的分布地区来看,2005至2012第三季度,中国

针对西欧资产、美国资产、东南亚资产和澳大拉西亚地区对

外交易并购分别为162宗、 159宗,132宗和130宗。

� 而中国针对中东地区资产对外并购仅为9宗。

� 按并购交易额的分布地区来看,在此期间,中国对西欧地区

对外并购投资额最多,为711亿美元(占25%)。此外,中国

对加大拿地区的投资中,能源和资源行业的投资多达428亿美

元(占95.5%)。

� 在此期间,中国对澳大拉西亚地区和东南亚地区的并购投资

总额分别为312亿和225亿美元。

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)Chinese Outbound M & A Investments by Geography

16

2005 – Q3 2012 Chinese outbound M & A investments by geography (volume)

2005 – Q3 2012 Chinese outbound M & A investments by geography (value)

� In terms of volume by target geographical region, over the 2005—Q3 2012 period, Chinese overseas acquisitions targeting at Western European assets, US assets, South East Asia and Australasia are 162, 159, 132 and 130 respectively.

� However, Chinese outbound acquirers only undertook 9 purchases of targets based in the Middle East.

� In terms of M&A values by target geographical region, deals of Western European targets were the most, which accounted for 71.1 billion of outbound investments (25%). In addition, Chinese investors spent US$ 42.8 billion buying Canadian assets, which was 95.5% of total Canadian assets purchased.

� Meanwhile, Chinese M&A investments into Australasia and South East Asia were US$31.2 billion and US$22.5 billion.

第二第二第二第二章章章章::::中国宏观经济发展趋势以及对矿业影响中国宏观经济发展趋势以及对矿业影响中国宏观经济发展趋势以及对矿业影响中国宏观经济发展趋势以及对矿业影响

17

Chapter Two: China Macroeconomics Trend and Impacts on Mining Sector

18

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)中中中中国宏观经国宏观经国宏观经国宏观经济环境影响金属采矿业济环境影响金属采矿业济环境影响金属采矿业济环境影响金属采矿业

房地产投资受宏观政策影响仍将徘徊在低谷房地产投资受宏观政策影响仍将徘徊在低谷房地产投资受宏观政策影响仍将徘徊在低谷房地产投资受宏观政策影响仍将徘徊在低谷

9.6%9.2%

10.4%

9.3%

7.8%8.3% 8.0%

12.9%

11.0%

15.7%

13.9%

10.5%

12.5% 12.3%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

2008 2009 2010 2011 2012F 2013F 2014F实际国内生产总值增幅 工业生产增幅

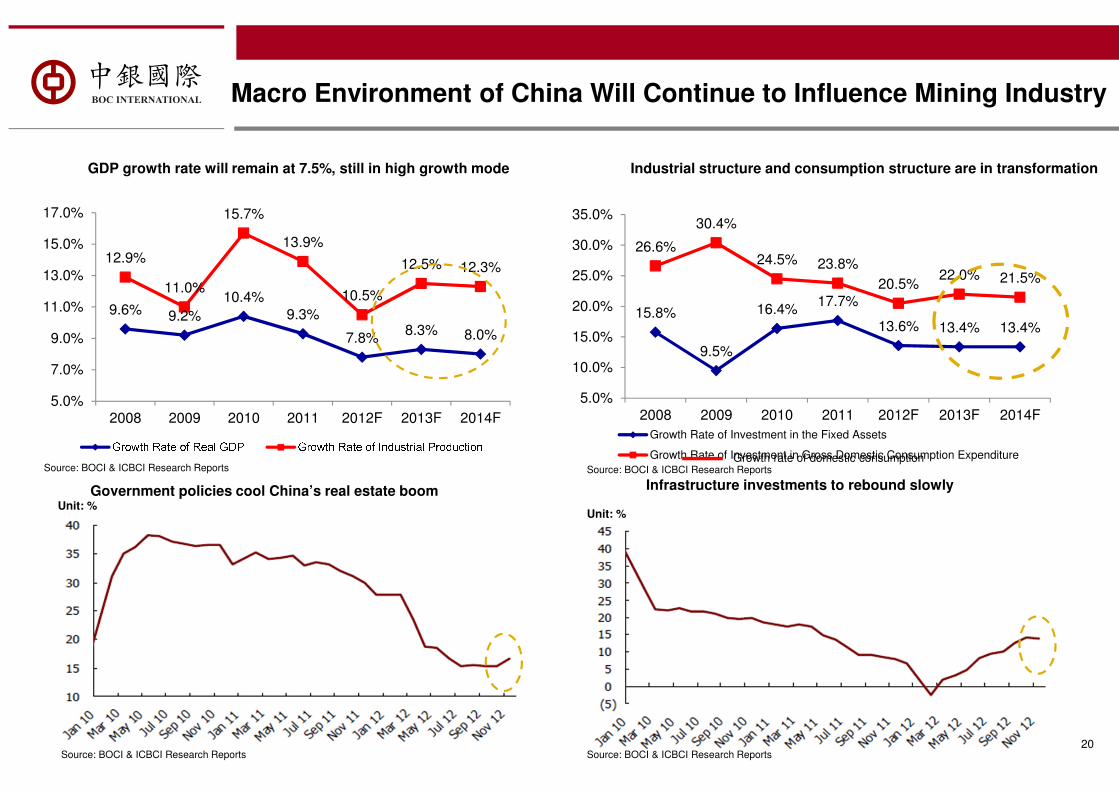

GDP增长保持在增长保持在增长保持在增长保持在7.5%水平水平水平水平,,,,仍然处于高速发展阶段仍然处于高速发展阶段仍然处于高速发展阶段仍然处于高速发展阶段

基建投资已从历史高位回落基建投资已从历史高位回落基建投资已从历史高位回落基建投资已从历史高位回落,,,,并将缓慢回升并将缓慢回升并将缓慢回升并将缓慢回升

15.8%

9.5%

16.4%17.7%

13.6% 13.4% 13.4%

26.6%

30.4%

24.5% 23.8%

20.5%22.0% 21.5%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2008 2009 2010 2011 2012F 2013F 2014F国内最终消费增速 固定资产投资增速

产业结构转型与消费结构调整产业结构转型与消费结构调整产业结构转型与消费结构调整产业结构转型与消费结构调整

19

资料来源:BOCI和ICBCI研究报告

资料来源:BOCI和ICBCI研究报告 资料来源:BOCI和ICBCI研究报告

资料来源:BOCI和ICBCI研究报告单位单位单位单位::::% 单位单位单位单位::::%

单位单位单位单位::::%单位单位单位单位::::%

矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求矿业公司上市的要求(第第第第18章章章章)Macro Environment of China Will Continue to Influence Mining Industry

20

Government policies cool China’s real estate boom Infrastructure investments to rebound slowly

9.6% 9.2%

10.4%9.3%

7.8%8.3% 8.0%

12.9%

11.0%

15.7%

13.9%

10.5%

12.5% 12.3%

5.0%

7.0%

9.0%

11.0%

13.0%

15.0%

17.0%

2008 2009 2010 2011 2012F 2013F 2014FGrowth Rate of Real GDP Growth Rate of Industrial Production

GDP growth rate will remain at 7.5%, still in high growth mode

15.8%

9.5%

16.4%17.7%

13.6% 13.4% 13.4%

26.6%

30.4%

24.5% 23.8%

20.5%22.0% 21.5%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

2008 2009 2010 2011 2012F 2013F 2014F

Growth Rate of Investment in the Fixed Assets

Growth Rate of Investment in Gross Domestic Consumption Expenditure

Industrial structure and consumption structure are in transformation

Source: BOCI & ICBCI Research ReportsGrowth rate of domestic consumption

Unit: %Unit: %

Source: BOCI & ICBCI Research Reports Source: BOCI & ICBCI Research Reports

Source: BOCI & ICBCI Research Reports

产业结构调整下对原材料需求展望产业结构调整下对原材料需求展望产业结构调整下对原材料需求展望产业结构调整下对原材料需求展望

名称名称名称名称 主要应用领域主要应用领域主要应用领域主要应用领域 需求展望需求展望需求展望需求展望

铜铜铜铜

电力、机械制造、家电、房地产

和汽车行业

�电力行业增速预计为7%~8%;家电行业增速在8%~10%之间

�房地产将在未来3 年内维持12~15%左右的投资增速

�未来铜的消费增长将较过去出现较大幅度的回落,但仍可维持5%

以上的水平、稳定持续,

钢材钢材钢材钢材 房地产和基建

�房地产将在未来3 年内维持平均12-15%左右的投资增速

�预计基建投资在转型期将维持稳定增长,但其力度远小于“十一五”

期间

煤炭和焦炭煤炭和焦炭煤炭和焦炭煤炭和焦炭 90%以上的焦炭用于炼钢�受未来中国投资增速回落和能源结构调整的双重打压,未来我国煤

炭消费增长将维持3~4%的增长水平

黄金和贵金黄金和贵金黄金和贵金黄金和贵金

属属属属

国际储备、投资、首饰和工业需

求

�受益于收入水平的提高,投资和首饰需求增速将维持较高水平

非金属矿产非金属矿产非金属矿产非金属矿产

(锂、锰、

锡和稀土等)

机械制造、精密科技等领域 �未来增长可持续趋势并具有巨大潜力

21

Commodities Outlook During Industrial Transformation

NameMajor Areas of

ApplicationDemand Outlook

Copper

Electric powerMachinery manufactureHousehold applianceReal estateAuto industry

� The power industry is expected to increase by 7% - 8% and the growth rate ofhousehold appliance industry will stay constantly between 8% - 10%

� The growth rate of real estate investment will maintain at about 12% -15%

� Copper consumption growth rate will encounter a big drop, but still can remain above 5%

SteelReal estateInfrastructure

� The growth rate of real estate investment will maintain at about 12% -15%

� Infrastructure investment is expected to keep a steady growth during the transformation period, but the rate will be lower than “Eleventh Five-Year Plan”period.

CokingCoal

More than 90% of the coking coal are used for steelmaking

�Hit by the significant drop in investment growth rate and energy structure adjustment, China coal consumption rate will maintain at 3-4% in the future

Gold

International reserves Investment Jewelry Industrial demand

�Benefit from the improvement of income level, there will be an increase demand in investment field and jewelry market.

Lithium, manganese, tin, and rare earth

Manufacturing and hi-tech sectors

�Continuous growth and significant potentials in the future

22

中国矿业中国矿业中国矿业中国矿业-2012年海年海年海年海外投外投外投外投资小结资小结资小结资小结

23

投资金额投资金额投资金额投资金额((((十亿美元十亿美元十亿美元十亿美元)))) 按金额计算投资行业分类按金额计算投资行业分类按金额计算投资行业分类按金额计算投资行业分类

金属采矿业海外交易总金额和交易数目金属采矿业海外交易总金额和交易数目金属采矿业海外交易总金额和交易数目金属采矿业海外交易总金额和交易数目((((十亿美元十亿美元十亿美元十亿美元)))) 金属采矿业交易地区金属采矿业交易地区金属采矿业交易地区金属采矿业交易地区

资料来源:券商研究报告

14.8%

44.7%

17.1%

5.1%

1.8%

12.8%

3.7% 金属采矿能源交通建设农业科技房地产其他2.3

4.7

6.4

16.1

18.5

21.4

56.0

科技

其他

农业

房地产

金属及采矿

交通

能源

6.5

3.8

2.4 2.1 1.3

0.9 0.8 0.5

0.1

7

8

1

3 3 3

1 1 10

2

4

6

8

10

0.0

2.0

4.0

6.0

8.0

煤炭 钢铁 铀 铅锌 铜 金 锂 铝 镍30%

19%13%

7%

4%

9%

5%

4%9%

澳大利亚印尼印度罗马尼亚土耳其俄罗斯赞比亚喀麦隆其他国家

Overseas Mining Investments in 2012

24

Investment amount (in billion US$) Sector overview by amount

Amount and number of cases invested in metals (in billion US$) Countries of investment by amount

Source: Brokerage reports

2.3

4.7

6.4

16.1

18.5

21.4

56.0

科技

其他

农业

房地产

金属及采矿

交通

能源Energy

Transportation

Metal

Real Estate

Agriculture

Others

Technology

14.8%

44.7%

17.1%

5.1%

1.8%

12.8%

3.7% 金属采矿能源交通建设农业科技房地产其他Energy

Transportation

Metal

Real Estate

Agriculture

Technology

Others

6.5

3.8

2.4 2.1 1.3

0.9 0.8 0.5

0.1

7

8

1

3 3 3

1 1 10

2

4

6

8

10

0.0

2.0

4.0

6.0

8.0

煤炭 钢铁 铀 铅锌 铜 金 锂 铝 镍Coal Steel Uranium Lead/Zinc Copper Gold Lithium Aluminum Nickel

30%

19%13%

7%

4%

9%

5%

4%9%

澳大利亚印尼印度罗马尼亚土耳其俄罗斯赞比亚喀麦隆其他国家Australia

Indonesia

India

Romania

Turkey

Russia

Zambia

Cameron

Others

25

中国对外并购交易概览中国对外并购交易概览中国对外并购交易概览中国对外并购交易概览((((2011 – 2012年第三季度年第三季度年第三季度年第三季度))))季度季度季度季度|年份年份年份年份 目标公司目标公司目标公司目标公司 行业划分行业划分行业划分行业划分 目标主要目标主要目标主要目标主要所在国家所在国家所在国家所在国家 竞购公司竞购公司竞购公司竞购公司 竞购公司竞购公司竞购公司竞购公司主要所在主要所在主要所在主要所在地地地地 卖方公司卖方公司卖方公司卖方公司 卖方公司卖方公司卖方公司卖方公司主要所在主要所在主要所在主要所在地地地地 交易价值交易价值交易价值交易价值((((百万美元百万美元百万美元百万美元))))

26

China Outbound M & A Deals Overview (Top 20 over 2011-Q3 2012)

Quarter | Year

Target Company

Sector Target Territory

Bidder Company Bidder Territory

Seller Company

Seller Territory

Deal Value

(US $ m)

27

中国对外并购交易概览中国对外并购交易概览中国对外并购交易概览中国对外并购交易概览((((2011 – 2012年第三季度年第三季度年第三季度年第三季度)()()()(续续续续))))季度季度季度季度|年份年份年份年份 目标公司目标公司目标公司目标公司 行业划分行业划分行业划分行业划分 目标主要目标主要目标主要目标主要所在国家所在国家所在国家所在国家 竞购公司竞购公司竞购公司竞购公司 竞购公司竞购公司竞购公司竞购公司主要所在主要所在主要所在主要所在地地地地 卖方公司卖方公司卖方公司卖方公司 卖方公司卖方公司卖方公司卖方公司主要所在主要所在主要所在主要所在地地地地 交易价值交易价值交易价值交易价值((((百万美元百万美元百万美元百万美元))))

28

China Outbound M & A Deals Overview (Top 20 over 2011-Q3 2012)(Cont’d)

Quarter | Year

Target Company

Sector Target Territory

Bidder Company Bidder Territory

Seller Company

Seller Territory

Deal Value

(US $ m)

对外投资分析对外投资分析对外投资分析对外投资分析

29

� 对外投资是大势所趋对外投资是大势所趋对外投资是大势所趋对外投资是大势所趋。。。。行业将更为广泛行业将更为广泛行业将更为广泛行业将更为广泛,,,,形式多样化形式多样化形式多样化形式多样化,,,,区域国际化区域国际化区域国际化区域国际化。。。。包括一般消费行业包括一般消费行业包括一般消费行业包括一般消费行业((((房地产房地产房地产房地产,,,,日用日用日用日用

品等品等品等品等),),),),机械加工业机械加工业机械加工业机械加工业,,,,矿产能源业矿产能源业矿产能源业矿产能源业,,,,文化娱乐业文化娱乐业文化娱乐业文化娱乐业,,,,教育教育教育教育,,,,卫生卫生卫生卫生,,,,生物制药等生物制药等生物制药等生物制药等

� 并购区域将根据不同行业所确定并购区域将根据不同行业所确定并购区域将根据不同行业所确定并购区域将根据不同行业所确定。。。。价格与价值平衡是基础价格与价值平衡是基础价格与价值平衡是基础价格与价值平衡是基础。。。。矿产能源类矿产能源类矿产能源类矿产能源类,,,,澳大利亚澳大利亚澳大利亚澳大利亚、、、、非洲非洲非洲非洲、、、、东南亚东南亚东南亚东南亚、、、、北北北北

美洲等将为重点投资区域美洲等将为重点投资区域美洲等将为重点投资区域美洲等将为重点投资区域

� 投资形式投资形式投资形式投资形式::::

1. 风险勘探投资风险勘探投资风险勘探投资风险勘探投资。。。。大型项目合作开发大型项目合作开发大型项目合作开发大型项目合作开发,,,,政府与企业合作开发政府与企业合作开发政府与企业合作开发政府与企业合作开发

2. 项目发展项目发展项目发展项目发展。。。。合资合作合资合作合资合作合资合作。。。。市场市场市场市场+资金资金资金资金=项目项目项目项目

3. 股权并购股权并购股权并购股权并购。。。。金融工具的使用金融工具的使用金融工具的使用金融工具的使用;;;;市场转换市场转换市场转换市场转换;;;;价值升值价值升值价值升值价值升值;;;;吸收并购吸收并购吸收并购吸收并购。。。。资金资金资金资金+市场市场市场市场+管理团队管理团队管理团队管理团队

4. 投资主体投资主体投资主体投资主体。。。。各种形式的行业投资各种形式的行业投资各种形式的行业投资各种形式的行业投资;;;;金融投资者金融投资者金融投资者金融投资者;;;;产业与并购投资基金等产业与并购投资基金等产业与并购投资基金等产业与并购投资基金等

General Analysis on Overseas Investments

30

� Overseas investments is the trend. The industries are broad, formats are diversified, targets are global.

Industries include general consumption (real estate, consumer and etc.), machinery, mining & energy,

entertainment, education, healthcare, biotechnology and so on

� Acquisition region is driven by sectors. Price and value is the base. In Mining & Energy sector, Australia, Africa,

Southeast Asia and North America will be primary regions

� Investment types::::

1. Venture exploration investment: Collaboration in mega projects. Government and enterprise joint

development

2. Project development: Form JV in project collaboration. Market + Capital = Project

3. Equity investment: Methods such as use financial instrument; market exchange; valuation improvement;

merger and acquisition. Capital + Market + Management Team = Investment

4. Investment party: Such as industry investors; financial investors; industrial and acquisition funds

第三章第三章第三章第三章::::中中中中国矿业海外投资趋势国矿业海外投资趋势国矿业海外投资趋势国矿业海外投资趋势

31

Chapter Three: China Overseas Investments Trend Analysis in Mining Sector

32

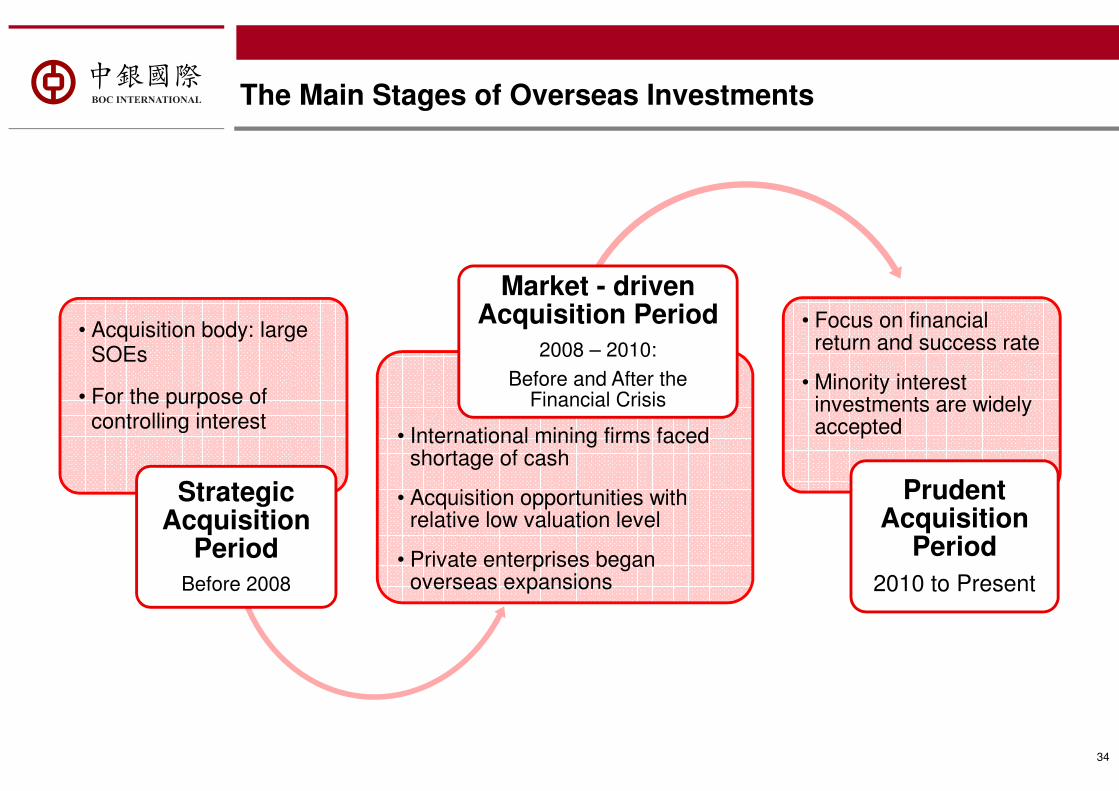

近年来中国矿企海外投资主要阶段近年来中国矿企海外投资主要阶段近年来中国矿企海外投资主要阶段近年来中国矿企海外投资主要阶段

33

• 收购主体以国企为主

• 主要以获取控制权为

目的

战略型收购期

2008年前

• 国际矿企资金紧缺,股价被低估

• 中国企业多进行抄底收购投资

• 民企开始走出国门

市场型收购期

2008年金融危机前后• 更多关注经济回报,注重成功率

• 少数股权投资开始被普遍接受

谨慎型收购期

2010 – 目前

The Main Stages of Overseas Investments

34

• Acquisition body: large SOEs

• For the purpose of controlling interest

Strategic Acquisition

PeriodBefore 2008

• International mining firms faced shortage of cash

• Acquisition opportunities with relative low valuation level

• Private enterprises began overseas expansions

Market - driven Acquisition Period

2008 – 2010:

Before and After the Financial Crisis

• Focus on financial return and success rate

• Minority interest investments are widely accepted

Prudent Acquisition

Period

2010 to Present

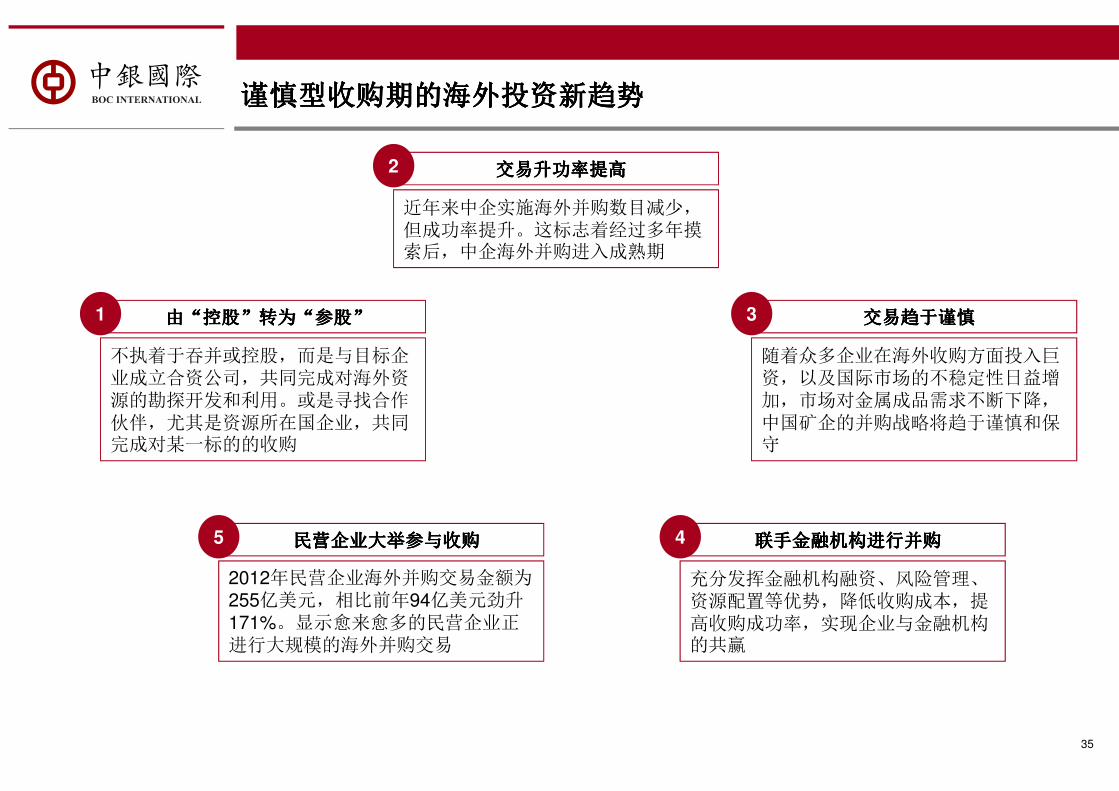

由由由由““““控股控股控股控股””””转为转为转为转为““““参股参股参股参股””””1

不执着于吞并或控股,而是与目标企

业成立合资公司,共同完成对海外资

源的勘探开发和利用。或是寻找合作

伙伴,尤其是资源所在国企业,共同

完成对某一标的的收购

交易升功率提高交易升功率提高交易升功率提高交易升功率提高2

近年来中企实施海外并购数目减少,

但成功率提升。这标志着经过多年摸

索后,中企海外并购进入成熟期

交易趋于谨慎交易趋于谨慎交易趋于谨慎交易趋于谨慎3

随着众多企业在海外收购方面投入巨

资,以及国际市场的不稳定性日益增

加,市场对金属成品需求不断下降,

中国矿企的并购战略将趋于谨慎和保

守

联手金融机构进行并购联手金融机构进行并购联手金融机构进行并购联手金融机构进行并购4

充分发挥金融机构融资、风险管理、

资源配置等优势,降低收购成本,提

高收购成功率,实现企业与金融机构

的共赢

民营企业大举参与收购民营企业大举参与收购民营企业大举参与收购民营企业大举参与收购5

2012年民营企业海外并购交易金额为255亿美元,相比前年94亿美元劲升171%。显示愈来愈多的民营企业正进行大规模的海外并购交易

谨慎型收购期的海外投资新趋势谨慎型收购期的海外投资新趋势谨慎型收购期的海外投资新趋势谨慎型收购期的海外投资新趋势

35

1

Instead of acquiring controlling stake, jointventure with the target company in order tobetter leverage the local intelligences andresources in the operation process are widelyaccepted.

Increasing rate of success2

The number of overseas investments declined,but the rate of success increased. This indicatesthat Chinese investments into overseas afterseveral years of experiments and practiceshave entered into a mature period.

More prudent in M & A transactions3

With many enterprises invest heavily inoverseas acquisitions, as well as the instabilityof the international market, market demand formetal products is declining. Therefore, themining enterprises in China will become morecautious and conservative in potentialtransactions.

Collaborate with financial institutions 4

Give full play to the advantages of financial institutions in the area of financing, risk management, resource allocation and cost reduction to increase the success rate of acquisition, and to achieve a win-win situation of enterprises and financial institutions.

More private enterprises participation 5

In 2012, the amount of private enterprisesoverseas investments are about US$ 25.5billion, rising by 171% compared to previousyear, which shows that an increasing number ofprivate enterprises are carrying out large-scaleoverseas investment activities.

Investment Trend During Prudent Acquisition Period

36

Changing from “controlling investor" to “participation investor””””

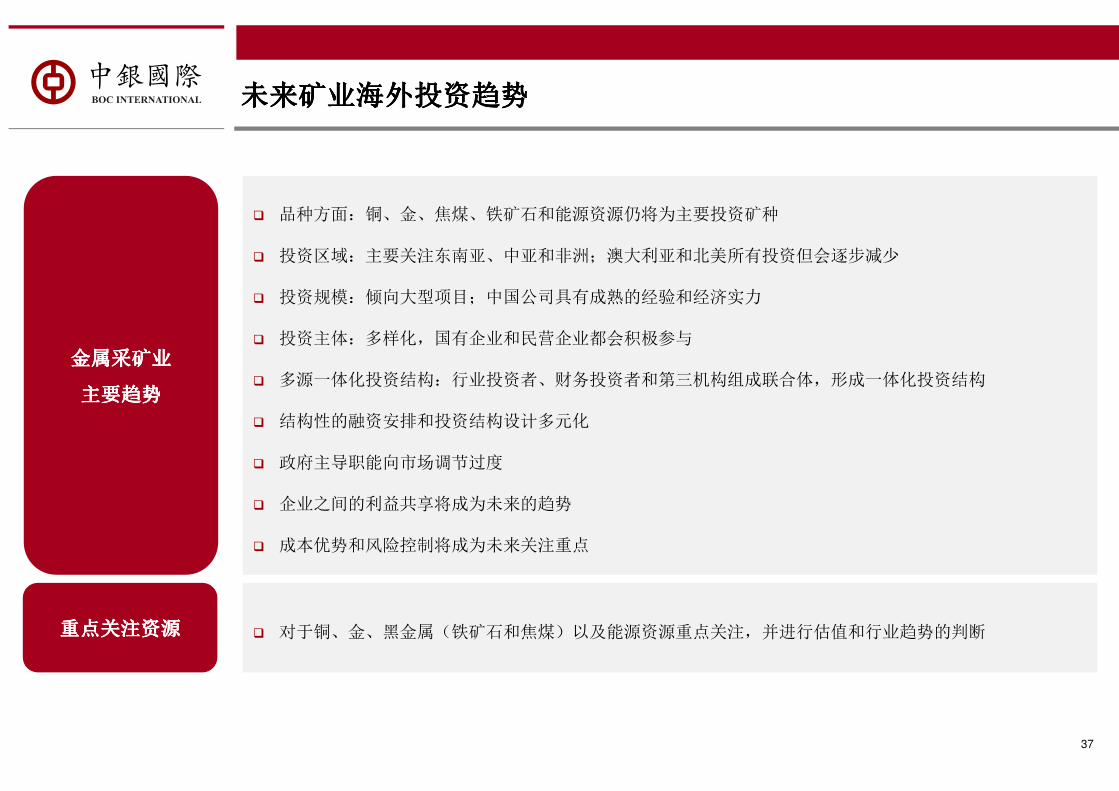

未来矿业海外投资趋势未来矿业海外投资趋势未来矿业海外投资趋势未来矿业海外投资趋势

金属采矿业金属采矿业金属采矿业金属采矿业

主要趋势主要趋势主要趋势主要趋势

� 品种方面:铜、金、焦煤、铁矿石和能源资源仍将为主要投资矿种

� 投资区域:主要关注东南亚、中亚和非洲;澳大利亚和北美所有投资但会逐步减少

� 投资规模:倾向大型项目;中国公司具有成熟的经验和经济实力

� 投资主体:多样化,国有企业和民营企业都会积极参与

� 多源一体化投资结构:行业投资者、财务投资者和第三机构组成联合体,形成一体化投资结构

� 结构性的融资安排和投资结构设计多元化

� 政府主导职能向市场调节过度

� 企业之间的利益共享将成为未来的趋势

� 成本优势和风险控制将成为未来关注重点

37

� 对于铜、金、黑金属(铁矿石和焦煤)以及能源资源重点关注,并进行估值和行业趋势的判断重点关注资源重点关注资源重点关注资源重点关注资源

Overseas Mining Investments Trends

Investment Focus� Copper, gold, coking coal, iron ore and energy related resources will remain as the main investment

targets. valuation and sector forecast will be the key to investment

Trend Analysis on Mining Sector

� Resource Types: Copper, Gold, Coking Coal, Iron Ore and Energy related resources

� Areas: Mainly focus on South-East Asia, Mid-Asia and Africa; Australia and North America in decreasing trend

� Size of Investment: Prefer large size investment, with increased experience and stronger financing capacity of Chinese enterprises

� Investment Vehicle: SOE and private enterprises will both participate

� Investment Structure: Consortium by strategic and financial investors

� Structured financing arrangement and multiple investment structure

� Transaction to Market-driven investment motivations

� Strategic partnership and synergy achieved by corporate

� Focus on cost control and risk management

38

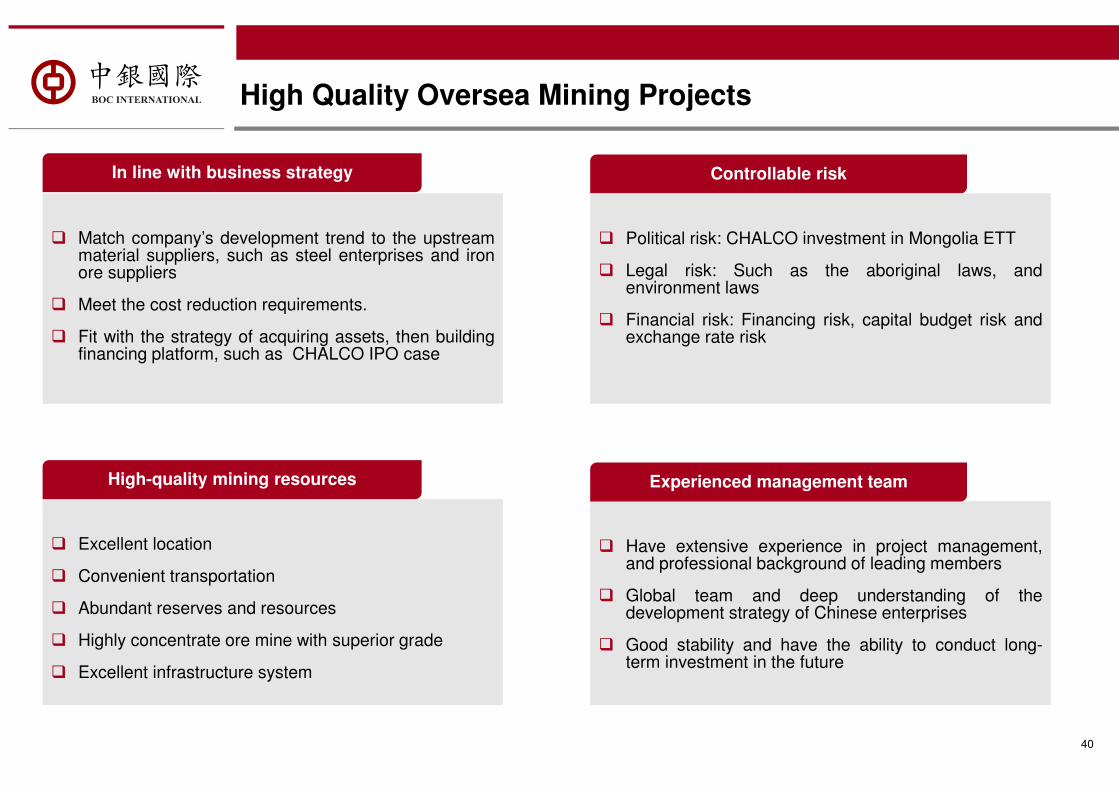

符合公司经营战略符合公司经营战略符合公司经营战略符合公司经营战略

� 具有优势的地理位置

� 便利的交通运输系统

� 巨大的储量、资源量

� 高密度、高品位的矿石

� 成熟的基础配套设施

拥有高质量的矿产资源拥有高质量的矿产资源拥有高质量的矿产资源拥有高质量的矿产资源

高质量的海外矿业投资项目高质量的海外矿业投资项目高质量的海外矿业投资项目高质量的海外矿业投资项目

� 符合公司向上游原材料供应商发展的趋势,如钢企

并购铁矿石供应商

� 符合降低成本考量,如对南美洲、非洲铜矿资源的

收购后就地进行加工冶炼

� 符合先收购资产,再搭建海外融资平台的战略,如

最近在香港联交所上市的中铝矿业

� 政治风险,如中铝投资蒙古ETT风波

� 法律风险,如澳洲、加拿大原住民法律,美国加拿大等国的严

苛环保法律

� 财务风险,如融资风险、资本预算风险及汇率风险

风险可控风险可控风险可控风险可控

经验丰富的管理团队经验丰富的管理团队经验丰富的管理团队经验丰富的管理团队

� 拥有丰富的项目管理经验,其中核心成员具有资深专业背景

� 国际化的团队,深刻了解中国企业的发展蓝图

� 团队具有稳定性,未来能够长期投入到日常业务运营中

39

符合公司经营战略符合公司经营战略符合公司经营战略符合公司经营战略

In line with business strategy

� Excellent location

� Convenient transportation

� Abundant reserves and resources

� Highly concentrate ore mine with superior grade

� Excellent infrastructure system

High-quality mining resources

High Quality Oversea Mining Projects

� Match company’s development trend to the upstreammaterial suppliers, such as steel enterprises and ironore suppliers

� Meet the cost reduction requirements.

� Fit with the strategy of acquiring assets, then buildingfinancing platform, such as CHALCO IPO case

� Have extensive experience in project management,and professional background of leading members

� Global team and deep understanding of thedevelopment strategy of Chinese enterprises

� Good stability and have the ability to conduct long-term investment in the future

40

Controllable risk

Experienced management team

� Political risk: CHALCO investment in Mongolia ETT

� Legal risk: Such as the aboriginal laws, andenvironment laws

� Financial risk: Financing risk, capital budget risk andexchange rate risk

第四第四第四第四章章章章::::对对对对外投资中存在的突出问题与解决方法外投资中存在的突出问题与解决方法外投资中存在的突出问题与解决方法外投资中存在的突出问题与解决方法

41

Chapter Four: Problems and Solutions in China Oversea Investment

42

中中中中国矿业海国矿业海国矿业海国矿业海外投资的主外投资的主外投资的主外投资的主要风险和问要风险和问要风险和问要风险和问题题题题

思维与文化思维与文化思维与文化思维与文化

� 中国企业的思维某种程度上很难直接应用到外国企业中

� 重视企业文化,以及与当地政府、居民、媒体等方的关系

尽职调查尽职调查尽职调查尽职调查

� 并购前应全面考察东道国的投资、税务、劳工等方面的政策

� 任命熟悉当地矿产资源和法律法规的团队进行细致尽调,将潜在风险最小化

政治与安全政治与安全政治与安全政治与安全

� 包括国际关系、国家和地区稳定性对并购交易的影响

� 同时应注意相关国家政治环境变化、民族情绪对并购甚至企业利益的影响

人才与技术人才与技术人才与技术人才与技术

� 专业、高素质的管理及营运人才是制约中国企业海外收购扩张的瓶颈

� 利用人才优势同时发挥专业技术上的特点,才能达到收购后的全面协同效应

43

Major Challenges to Chinese Investors

Consideration & Culture

� The ways of consideration of Chinese enterprises is difficult to apply directly to foreign enterprises

� Pay attention to cooperate culture, and establish close relationship between management and local government, residents, media and other parties

Due Diligence

� Get a complete perspective of the target country’s investment environment, such as tax, labor, and other aspects before taking actions

� Appoint a team familiar with the local mining resource, laws and regulations to carry out the due diligence, so as to minimize the potential risk

Politics & Security

� Pay attention to the influence of international relations, national and regional stability

� Also note the impact of related country‘s political environment changes and the national sentiment, as well as to the business interests

Talents & Technology

� Professional, high-quality management and operating talents are the major reasons restricting Chinese enterprises’ oversea expansion

� Focus on the use of the advantages of human resources and professional talents in order to achieve a overall synergy after the acquisition

44

第五第五第五第五章章章章::::中银国际的业务优势中银国际的业务优势中银国际的业务优势中银国际的业务优势

45

Chapter Five: Strategic advantages of BOCI

46

中银国际中银国际中银国际中银国际----提供全方位服务的投资银行提供全方位服务的投资银行提供全方位服务的投资银行提供全方位服务的投资银行

中银国际在香港拥有深厚的根基中银国际在香港拥有深厚的根基中银国际在香港拥有深厚的根基中银国际在香港拥有深厚的根基,,,,是中国最佳的投资银行是中国最佳的投资银行是中国最佳的投资银行是中国最佳的投资银行

中银国际是中国和香港最受认可的银行品牌中银国际是中国和香港最受认可的银行品牌中银国际是中国和香港最受认可的银行品牌中银国际是中国和香港最受认可的银行品牌—中国银行的全资附属投资银行中国银行的全资附属投资银行中国银行的全资附属投资银行中国银行的全资附属投资银行

1979 1983 1996 1998 1999 2002 2006 2007 2009 2010

1979年,中银国际前身中国建设财务(香港)有限公司在香港成立 1996年,中国银行国际控股有限公司及中国银行国际(英国)有限公司在英国注册成立,为海外业务拓展踏出重要一步 1999年,中银国际与英国保诚集团合资成立中银保诚资产管理公司和信托公司 2006年,中银国际发起设立中国首支契约型产业投资基金——渤海产业投资基金 2009年,中银国际获香港金管局批准开拓私人银行业务,是香港首家中资私人银行1983年,中银集团证券有限公司成立,全面参与香港证券二级市场和期货市场的买卖业务 1998年,中银国际控股有限公司在香港注册成立 2002年,中银国际证券有限责任公司(“中国公司”)在上海成立,成为首家获得人民币普通股(A类)许可证券业务的中外合资的合资证券公司

2007年,中银国际在中资金融机构中率先开展杠杆及结构融资业务 2010年,中银国际获准筹备环球商品业务

� 中国银行是中国四大国有银行之一。其总资产超过1.5万亿美元,净利润达到159亿美元,市值超过 1,456 亿美元。中银国际是中国银行的全资附属公司

� 中银国际是一家领先的投资银行,为客户提供多元化的服务:

� 中银国际于1979 年开始投资银行业务� 中银国际透过分布在香港、北京、上海、纽约、伦敦及新加坡的子公司及分行,为客户提供全面的投行服务� 中银国际在中国、香港、新加坡、美国和英国设有海外办公室,共聘请查过

850名员工� 中国银行、中银国际、中银集团保险和中银集团投资提供多元化的服务,其中包括商业银行服务、投资银行服务、保险服务等,为客户提供一个强大、连贯及全面的银行平台� 中银国际是少数提供H股(香港上市)及A股(国内上市)发行服务的投资银行。因此,我们能为需要同时在国内和香港上市的客户提供一站式的投资银行服务

47

BOCI is the Best Hong Kong Investment Bank with the Deepest Roots in the Region

� Bank of China is one of the four largest commercial banks in China with total assets of over US $1.7 Trn, net profit of US $19.2 Bn and market capitalization over US $120 Bn

� Bank of China International (“BOCI”) is a wholly owned subsidiary of Bank of China

� BOCI is a leading investment bank offering a diverse range of Services

� BOCI started investment banking business in 1979

� BOCI provides a broad range of investment banking services through its subsidiaries and branches in Hong Kong, Beijing, Shanghai, New York, London and Singapore

� BOCI employs over 850 staffs worldwide with offices in China, Hong Kong, Singapore, United States and United Kingdom

� Bank of China, BOCI, BOCG Insurance and BOCG Investment provide a wide range of services, including commercial banking, investment banking, insurance and other services, thus providing a strong integrated banking platform

� BOCI is one of the few investment banks having the capability to provide both H-share (Hong Kong listing) and A-share (China listing) issuance services, thus offering one-stop investment banking services for companies simultaneously listed in China and Hong Kong

BOCI is the Fully Owned Investment Banking Arm of the Most Recognized Banking Brand Name in Hong Kong

1979 1983 1996 1998 1999 2002 2006 2007 2009 2010

In 1979, China Development Finance Company (HK) Limited, the predecessor of BOC International Holdings Limited (“BOCI”), was established in Hong Kong

In 1996, BOC International (UK) Limited was established in the UK, marking an important step towards overseas development

In 1999, BOCI and Prudential Plc together formed BOCI-Prudential Asset Management Limited and BOCI-Prudential Trustee Limited

In 2006, BOCI launched the Bohai Industrial Investment Fund, the first RMB-denominated contractual private equity investment fund in China

In 2009, BOCI received HKMA approval to initiate private banking service and became the first Chinese bank to offer private banking services in Hong Kong

In 1983, Bank of China Group Securities Limited was incorporated in Hong Kong. BOCI became fully engaged in the securities brokerage and futures trading business

In 1998, BOCI was incorporated in Hong Kong

In 2002, BOCI promoted and established BOCI Securities Limited in Shanghai, which was the first Sino-foreign joint-venture securities firm to be granted a general securities license for RMB-denominated ordinary shares (Class A)

In 2007, BOCI launched the Leveraged and Structured Finance business and became the first Chinese financial institutions to offer such service

In 2010, BOCI received approval to begin preparation for setting up its global commodity business

48

BOCI – A Leading Full Service Chinese and Hong Kong Investment Bank

BOCI China

Commercial Banking Business

Investment Banking Business

Insurance Business Other Businesses

Foreign branches covering 28 countries

Over 200 branches in Hong Kong

BOCG Insurance

(Hong Kong)

BOCG Insurance (China)

BOC Aviation

Over 10,000 domestic outlets

BOCG InsuranceBOCG

Investment

100%100% 100%

100%49%

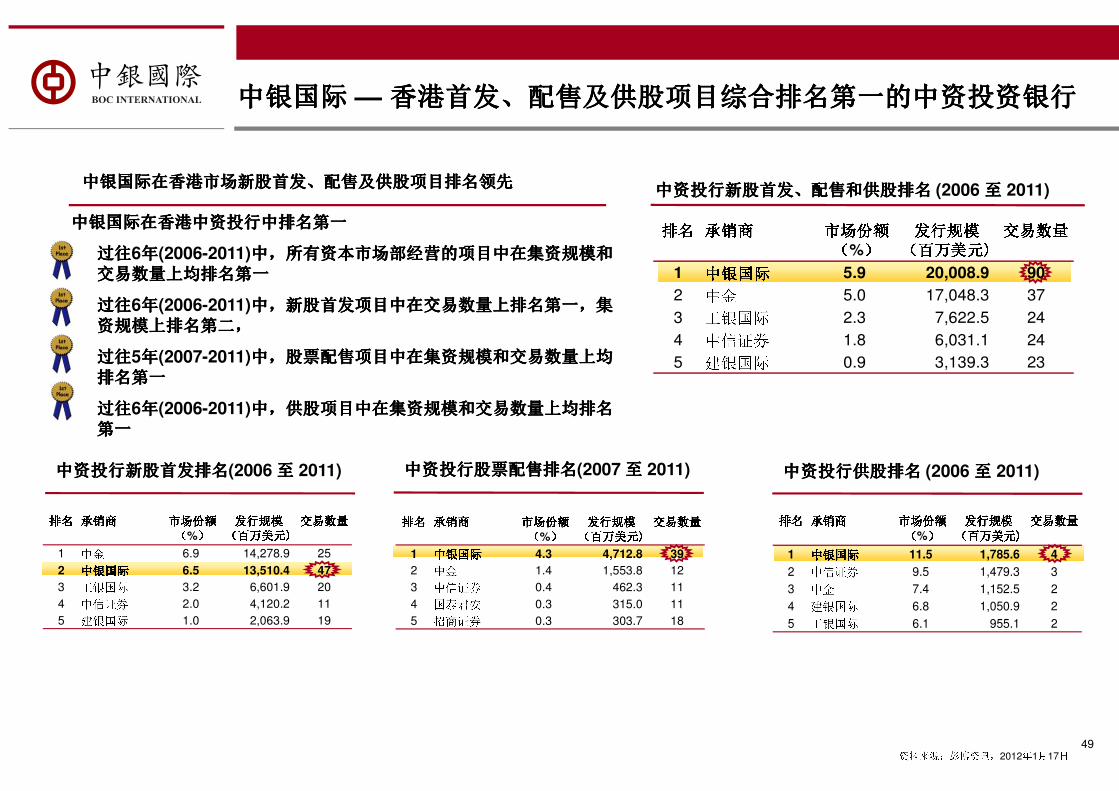

排名排名排名排名 承销商承销商承销商承销商 市场份额市场份额市场份额市场份额((((%)))) 发行规模发行规模发行规模发行规模((((百万美元)百万美元)百万美元)百万美元) 交易数量交易数量交易数量交易数量1 中银国际中银国际中银国际中银国际 5.9 20,008.9 90

2 中金 5.0 17,048.3 37

3 工银国际 2.3 7,622.5 24

4 中信证券 1.8 6,031.1 24

5 建银国际 0.9 3,139.3 23

排名排名排名排名 承销商承销商承销商承销商 市场份额市场份额市场份额市场份额((((%)))) 发行规模发行规模发行规模发行规模((((百万美元)百万美元)百万美元)百万美元) 交易数量交易数量交易数量交易数量1 中金 6.9 14,278.9 25

2 中银国际中银国际中银国际中银国际 6.5 13,510.4 47

3 工银国际 3.2 6,601.9 20

4 中信证券 2.0 4,120.2 11

5 建银国际 1.0 2,063.9 19

排名排名排名排名 承销商承销商承销商承销商 市场份额市场份额市场份额市场份额((((%)))) 发行规模发行规模发行规模发行规模((((百万美元)百万美元)百万美元)百万美元) 交易数量交易数量交易数量交易数量1 中银国际中银国际中银国际中银国际 11.5 1,785.6 4

2 中信证券 9.5 1,479.3 3

3 中金 7.4 1,152.5 2

4 建银国际 6.8 1,050.9 2

5 工银国际 6.1 955.1 2

49

中银国际中银国际中银国际中银国际 — 香港首发香港首发香港首发香港首发、、、、配售及供股项目综合排名第一的中资投资银行配售及供股项目综合排名第一的中资投资银行配售及供股项目综合排名第一的中资投资银行配售及供股项目综合排名第一的中资投资银行

中银国际在香港中资投行中排名第一中银国际在香港中资投行中排名第一中银国际在香港中资投行中排名第一中银国际在香港中资投行中排名第一

过往过往过往过往6年年年年(2006-2011)中中中中,,,,所有资本市场部经营的项目中在集资规模和所有资本市场部经营的项目中在集资规模和所有资本市场部经营的项目中在集资规模和所有资本市场部经营的项目中在集资规模和

交易数量上均排名第一交易数量上均排名第一交易数量上均排名第一交易数量上均排名第一

过往过往过往过往6年年年年(2006-2011)中中中中,,,,新股首发项目中在交易数量上排名第一新股首发项目中在交易数量上排名第一新股首发项目中在交易数量上排名第一新股首发项目中在交易数量上排名第一,,,,集集集集

资规模上排名第二资规模上排名第二资规模上排名第二资规模上排名第二,,,,

过往过往过往过往5年年年年(2007-2011)中中中中,,,,股票配售项目中在集资规模和交易数量上均股票配售项目中在集资规模和交易数量上均股票配售项目中在集资规模和交易数量上均股票配售项目中在集资规模和交易数量上均

排名第一排名第一排名第一排名第一

过往过往过往过往6年年年年(2006-2011)中中中中,,,,供股项目中在集资规模和交易数量上均排名供股项目中在集资规模和交易数量上均排名供股项目中在集资规模和交易数量上均排名供股项目中在集资规模和交易数量上均排名

第一第一第一第一

中银国际在香港市场新股首发中银国际在香港市场新股首发中银国际在香港市场新股首发中银国际在香港市场新股首发、、、、配售及供股项目排名领先配售及供股项目排名领先配售及供股项目排名领先配售及供股项目排名领先

中资投行新股首发中资投行新股首发中资投行新股首发中资投行新股首发、、、、配售和供股排名配售和供股排名配售和供股排名配售和供股排名 (2006 至至至至 2011)

中资投行股票配售排名中资投行股票配售排名中资投行股票配售排名中资投行股票配售排名(2007 至至至至 2011) 中资投行供股排名中资投行供股排名中资投行供股排名中资投行供股排名 (2006 至至至至 2011)中资投行新股首发排名中资投行新股首发排名中资投行新股首发排名中资投行新股首发排名(2006 至至至至 2011)

资料来源:彭博资讯,2012年1月17日

排名排名排名排名 承销商承销商承销商承销商 市场份额市场份额市场份额市场份额((((%)))) 发行规模发行规模发行规模发行规模((((百万美元)百万美元)百万美元)百万美元) 交易数量交易数量交易数量交易数量1 中银国际中银国际中银国际中银国际 4.3 4,712.8 39

2 中金 1.4 1,553.8 12

3 中信证券 0.4 462.3 11

4 国泰君安 0.3 315.0 11

5 招商证券 0.3 303.7 18

50

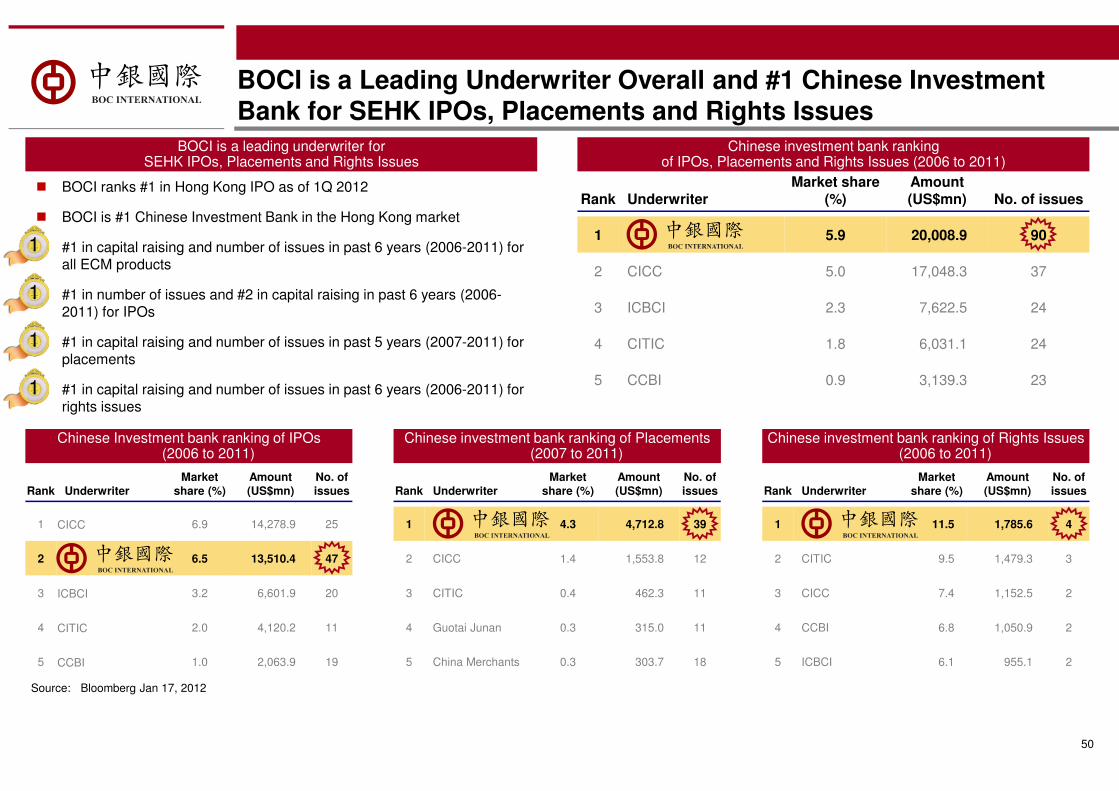

BOCI is a Leading Underwriter Overall and #1 Chinese Investment Bank for SEHK IPOs, Placements and Rights Issues

Rank UnderwriterMarket share

(%)Amount(US$mn) No. of issues

1 5.9 20,008.9 90

2 CICC 5.0 17,048.3 37

3 ICBCI 2.3 7,622.5 24

4 CITIC 1.8 6,031.1 24

5 CCBI 0.9 3,139.3 23

BOCI is a leading underwriter for SEHK IPOs, Placements and Rights Issues

� BOCI ranks #1 in Hong Kong IPO as of 1Q 2012

� BOCI is #1 Chinese Investment Bank in the Hong Kong market

� #1 in capital raising and number of issues in past 6 years (2006-2011) for all ECM products

� #1 in number of issues and #2 in capital raising in past 6 years (2006-2011) for IPOs

� #1 in capital raising and number of issues in past 5 years (2007-2011) for placements

� #1 in capital raising and number of issues in past 6 years (2006-2011) for rights issues

Chinese Investment bank ranking of IPOs(2006 to 2011)

Rank UnderwriterMarket

share (%)Amount(US$mn)

No. of issues

1 CICC 6.9 14,278.9 25

2 6.5 13,510.4 47

3 ICBCI 3.2 6,601.9 20

4 CITIC 2.0 4,120.2 11

5 CCBI 1.0 2,063.9 19

Chinese investment bank ranking of Placements (2007 to 2011)

Rank UnderwriterMarket

share (%)Amount(US$mn)

No. of issues

1 4.3 4,712.8 39

2 CICC 1.4 1,553.8 12

3 CITIC 0.4 462.3 11

4 Guotai Junan 0.3 315.0 11

5 China Merchants 0.3 303.7 18

Chinese investment bank ranking of Rights Issues (2006 to 2011)

Rank UnderwriterMarket

share (%)Amount(US$mn)

No. of issues

1 11.5 1,785.6 4

2 CITIC 9.5 1,479.3 3

3 CICC 7.4 1,152.5 2

4 CCBI 6.8 1,050.9 2

5 ICBCI 6.1 955.1 2

Source: Bloomberg Jan 17, 2012

Chinese investment bank rankingof IPOs, Placements and Rights Issues (2006 to 2011)

111

111

111

111

中银国际中银国际中银国际中银国际----中国与全球资本市场的桥梁中国与全球资本市场的桥梁中国与全球资本市场的桥梁中国与全球资本市场的桥梁

中银国中银国中银国中银国际协同中国银行为客户提供一体化和国际化服务际协同中国银行为客户提供一体化和国际化服务际协同中国银行为客户提供一体化和国际化服务际协同中国银行为客户提供一体化和国际化服务

杠杆及结构融资杠杆及结构融资杠杆及结构融资杠杆及结构融资定息收益定息收益定息收益定息收益

证券零售及证券零售及证券零售及证券零售及

私人银行私人银行私人银行私人银行

证券销售及研究证券销售及研究证券销售及研究证券销售及研究

金融咨询金融咨询金融咨询金融咨询资产管理资产管理资产管理资产管理

并购业务并购业务并购业务并购业务私募基金私募基金私募基金私募基金

股票上市股票上市股票上市股票上市

证券衍生产品证券衍生产品证券衍生产品证券衍生产品 全球大宗商品交易全球大宗商品交易全球大宗商品交易全球大宗商品交易

51

52

BOCI – Bridging China and Global Capital Markets

With in-depth local knowledge of the China market and international perspective on global market, BOCI is an expert in the China capital market business

Leveraged &

Structured FinanceFixed

Income

Retail Brokerage& Private Banking

Equity Sales& Research

FinancialAdvisory

AssetManagement

M&APrivateEquity

EquityOfferings

EquityDerivatives

Global Commodities

免责声明免责声明免责声明免责声明

本讨论材料由中银国际亚洲有限公司(简称“中银国际”)准备。

本讨论材料中所载的信息以最佳努力基础准备,但未经独立验证。中银国际并未就本讨论材料中所载的信息或观点的公正性、准确性、完整

性或正确性做出任何明示或默示的陈述或保证,且任何人士均不得依赖本讨论材料中所载的信息或意见。本讨论材料中所载的信息及意见均

在截至本讨论材料日期的基础上提供并会不经通知而更改,该等信息及意见没有亦不会根据本讨论材料准备之日过后可能发生的任何变更进

行更新。中银国际与其关联方、及其董事、管理人员、雇员、顾问或代表亦不对因使用本讨论材料所载的信息或任何其它与本讨论材料有关

的事宜而导致的损失(无论于侵权法或合同法下或任何其它相关法律上的疏忽或失实陈述)承担任何责任。

本讨论材料包含于各相应日期对未来的观点和预测的陈述。除对过往事实的陈述外,本讨论材料的其他内容皆为包含各类风险和不确定因素

的前瞻性声明。该前瞻性陈述是基于经营情况的假设和超出可控范围的因素做出,并存在着重大的风险和不确定性。本讨论材料不确保有关

陈述可提供准确和与事实相符的预测结果,且未来事件可能与有关预测大相径庭。中银国际概不承担更新任何前瞻性声明的责任。

本讨论材料并非研究报告,亦非由中银国际研究部或其关联方协助准备。接收方应当就公司和建议交易自主地进行独立调查和研究,并寻求

独立法律、法规、会计和税务意见。

本讨论材料不构成或部分构成且不应被理解为于任何司法管辖地区发售或认购股份或证券的要约, 或发售或认购股份或证券的要约邀请, 或参加任何投资活动的引导,亦不构成接收方订立任何合同或作出任何承诺的基础。

本讨论材料的任何部分均不得为了任何目的直接或间接地向任何其它人士(不论该人士是否于接收方的集团或公司或事务所之内或外)以任

何方式复制、再次派发或传阅,亦不得翻印本讨论材料或其任何部分。

53

This material has been prepared by BOC Asia Limited (“BOCI”). It has been prepared for and provided to the recipient (the “Recipient”) for information purposes only. This material should not be distributed, directly or indirectly, in any jurisdiction in which the distribution of these materials would be prohibited. This material is not intended as an offer or the solicitation of an offer to buy or sell any securities.

This material may or may not lead to transactions being entered into between BOCI and the Recipient. Unless and until both BOCI and the Recipient agree to, and sign formal written contracts, it is not intended that either BOCI or the Recipient are, or will be, bound by any of the proposed terms and conditions.

This material is confidential and is intended for use only by the Recipient and its professional advisers and remains the property of BOCI. It should not be reproduced, redistributed, passed on to any other person or published, in whole or in part, for any purpose without the consent of BOCI and must be returned on request to BOCI and any copies thereof destroyed. Nothing in this document should be construed as legal, tax, accounting or investment advice or as an offer by BOCI to purchase securities from or sell securities to the Recipient, or to underwrite securities of the Recipient, or to extend any credit or like facilities to the Recipient, or to conduct any such activity on behalf of the Recipient. BOCI makes no representations or warranties with respect to the material, and disclaims all liability for any use the Recipient or its advisers make of the contents of the material.

Whilst the information in this material is believed to be reliable, it has not been independently verified by BOCI. BOCI makes no representation or warranty (express or implied) of any nature, nor does it accept any responsibility or liability of any kind, with respect to the accuracy or completeness of the information in this material. The Recipient of this document should make its own independent evaluation of any transaction and of the relevance and adequacy of the information in this material and should make such other investigations as it deems necessary to determine whether to participate in any transaction. This shall not, however, restrict, exclude, or limit any duty or liability to a person under any applicable laws or regulations of any jurisdiction which may not lawfully be disclaimed.

Any views or opinions expressed in the material (including statements or forecasts) constitute the judgment of BOCI as of the date indicated and are subject to change without notice. BOCI does not undertake to update this document. The Recipient should not rely on any representations or undertakings inconsistent with the above paragraphs.

BOCI and its affiliates, connected companies, employees or clients may have an interest in the securities or other financial instruments or their related derivatives of the type (“Instruments”) described in the material. This may include dealing, trading, holding, acting as market-makers in such Instruments and may include providing general banking, Chinese banksing, credit and other financial services to any company or issuer of securities or financial instruments referred to herein. BOCI may also have acted as a manager or co-manager of a public offering of such Instruments, and may also have an Chinese banking relationship with any companies mentioned in this material.

Disclaimer

54

Save the Date for Mines and Money Hong Kong 2014

March 24-28, 2014 - Hong Kong Convention & Exhibition Centre

www.minesandmoney.com/hongkongRegister your Interest at: