Why profits are important & higher corporate tax rates are a bad idea

©2015 Canadian Manufacturers & Exporters

Since 1871, we have made a difference for Canada’s manufacturing and exporting communities. Fighting for their future. Saving them money. Helping them grow.

The association directly represents more than 10,000 leading companies nationwide. More than 85 per cent of CME’s members are small and medium-sized enterprises.

As Canada’s leading business network, CME, through various initiatives including the establishment of the Canadian Manufacturing Coalition, touches more than 100,000 companies from coast to coast, engaged in manufacturing, global business and service-related industries.

CME’s membership network accounts for anestimated 82 per cent of total manufacturing production and 90 per cent of Canada’s exports

1

Why Profits are Important & Higher Corporate Tax Rates are a Bad Idea

Summary Businesses grow by making money – by generating profits. They use their profits to re-‐invest in their business, raise financing, or pay dividends to their shareholders. In either case, profits are essential for business growth – and ultimately for the employment, incomes, and the prosperity of all Canadians. Profits are important. Here are three important reasons why: • The dividends that they generate make a major contribution to personal incomes,

pensions, and savings; • Higher after-‐tax rates of return on capital increase rates of business investment and

economic growth; and, • Higher profit margins reduce Canada’s unemployment rate and accelerate job growth. Corporate income tax rates have come down in Canada over the past 15 years, helping to boost business profits, investment, economic growth, and employment. However, some provincial governments have recently reversed the trend. Corporate tax rates are also an issue in the 2015 federal election campaign. From a responsible fiscal policy perspective, raising tax rates on business profits is simply a bad idea. Higher corporate tax rates would depress rates of return on invested capital and make Canada a less attractive location for businesses to invest. They would decelerate the growth of business investment, leading to a net economic loss for the Canadian economy. And, they would increase Canada’s unemployment rate, thereby eroding job growth. Based on the current state of the Canadian economy and Canadian business finances, every one percentage point increase in the corporate income tax rate would, on an annual basis: • Transfer $2.86 billion in business profits to the federal government, $560 million from

manufacturers; • Cut dividend payments to Canadians by $1.8 billion, and reduce their savings by even more; • Lower the rate of return on the capital stock of Canada’s business sector by 0.77

percentage points;

2

• Reduce business investment activity by 0.4% or approximately $7.0 billion; • Depress manufacturing investment by $2.8 billion; • Lead to a net loss in GDP of $4.1 billion; • Reduce the after-‐tax profit margin of Canadian business by 0.19 percentage points or $4.3

billion; and, • Eliminate 73,000 to 75,000 jobs. Corporate Profits are Important Businesses grow by making money – by generating profits. They use their profits to re-‐invest in their business, raise financing, or pay dividends to their shareholders. In either case, profits are essential for business growth – and ultimately for the employment, incomes, and the prosperity of all Canadians. Yet, the role and the importance of profits are not well or widely understood. Profits represent more than just what is left over after businesses pay their bills. They make up a substantial part of the returns on investment that businesses use to determine whether or not it makes sense for them to make an investment in the first place, and if so whether to do that in Canada. For that reason, profits are not something that can simply be transferred from the business sector to be spent by government without a loss to the economy in the form of less competitive businesses and consequently lower levels of investment and job growth. Recent economic analyses have made the point well. D. Chen and J. Mintz have shown that lower corporate tax rates in Canada have encouraged capital investment without a significant erosion of corporate tax revenues as a share of GDP1. B. Dahlby has estimated the marginal cost of the federal corporate income tax to the Canadian economy. He concludes that every dollar of tax raised erodes the tax base in Canada by $1.452. Dahlby and E. Ferede have estimated that a one percentage-‐point increase in the combined federal-‐provincial tax rate leads to a 2.3% contraction in the corporate tax base3. M. Parsons has found that a 10% reduction in the cost of capital in Canada leads to a 7% increase in the capital stock4. L.P. Field

1 D. Chen and J. Mintz, “The 2014 Global Tax Competitiveness Report: A Proposed Business Tax Agenda,” SPP Research Papers, 8(4), School of Public Policy, University of Calgary, September 2014. 2 B. Dahlby, “Reforming the Tax Mix in Canada”, SPP Research Papers, 5(14), School of Public Policy, University of Calgary, 2012. 3 B. Dahlby and E. Ferede, “What Does it Cost Society to Raise a Dollar of Tax Revenue? The Marginal Cost of Public Funds,” C.D. Howe Institute Commentary No. 324, C.D. Howe Institute, Toronto, 2011. 4 M. Parsons, “The Effect of Corporate Taxes on Canadian Investment: An Empirical Investigation”, Finance Canada Working Paper 2008-‐01, Ottawa, 2008.

3

and J.H. Heckemeyer have estimated that a one point reduction in the corporate income tax rate results in a 2.49% increase in foreign direct investment in Canada5. And, in his most recent report on corporate taxation, Jack Mintz estimates that each percentage point increase in the corporate tax rate leads to a loss of 75,000 jobs6. The importance of corporate profitability and of keeping corporate tax rates low should be reflected in Canadian fiscal policy, especially on the part of governments anxious to encourage economic and employment growth. Yet, whether or not corporate tax rates should be increased has become an issue in the 2015 federal election. Provincial governments in Ontario, Alberta, and New Brunswick have recently raised their corporate tax rates. Higher mandatory overhead costs – payroll taxes, sales taxes, property taxes, and costs of regulatory compliance – are also eroding business profits and the corporate tax base. All of these policy measures are detrimental to business competitiveness, and as a result to investment, economic, and job growth. Canadian Businesses Generate a Lot of Profit Canadian corporations generated a record $308 billion in profits in 2014. They paid $64.3 billion in corporate income taxes – also a record amount. After their income taxes were paid, Canada’s corporate sector was left with $243.2 billion in after-‐tax earnings7. Corporations retained 88% of their after-‐tax earnings in Canada last year; the other 12% were distributed as dividends to foreign shareholders. Just over 62% of their after-‐tax profits were paid as dividends to Canadian shareholders. Another 2.3% were remitted by crown corporations to government. The remaining 23% were kept as retained earnings by business, increasing their asset base and enabling them to raise additional financing for operating and investment purposes. Corporate profits will not be as strong in 2015 as they were last year because of the widespread impact of lower commodity and energy prices. Canadian corporations made $130.7 billion in pre-‐tax profits during the first two quarters of 2015. They paid $29.8 billion in corporate income taxes. Their after-‐tax profits amounted to $100.9 billion. 5 L.P. field and J.H. Heckemeyer, “FDI and Taxation: A Meta-‐Study,” Journal of Economic Surveys, 25(2), 2011, 233-‐72. 6 J. Mintz, An Agenda for Tax Reform in Canada, Canadian Council of Chief Executives, 2015, 13-‐14. 7 Corporate finance and taxation data are from Statistics Canada’s Quarterly Financial Statistics for Enterprises program which comprise financial statements collected from incorporated businesses. CANSIM table 187-‐001, Statistics Canada.

4

Manufacturers have a big stake in tax policy and what happens to corporate profits. The sector is one of the most important profit generators in the country. Manufacturers account for 11% of Canada’s GDP, but since the beginning of 2014 they have generated 16% of all business profits both on a pre-‐tax and after-‐tax basis. And, over the same period, they paid 17% of total corporate income taxes collected by government. These are all big numbers, but Canada’s business sector is big. The total operating revenue of Canada’s corporate sector exceeded $3.7 trillion in 2014 and $1.8 trillion during the first half of 2015. So the profit margin of Canadian companies amounted to 7.9% of their revenues on a before-‐tax basis and 6.2% of revenues after taxes were paid. With revenues of $760 billion in 2014 and $366 billion during the first half of 2015, manufacturers’ profit margins were lower, averaging 6.3% before tax and 4.9% after taxes were paid. Based on the current financial performance of Canada’s business sector, a one percentage point increase in the combined federal-‐provincial corporate tax rate would transfer $2.86 billion in business profits to government, of which $560 million would come from manufacturers. A one percentage point increase in the combined federal-‐provincial corporate tax rate would cut corporate dividend payments by $2.1 billion and the personal income of Canadians by $1.8 billion. It would reduce savings even more as stock prices would decline. Corporate Tax Rates Have Come Down Canada’s federal and provincial corporate income tax rates have fallen significantly over the past 15 years. As a result, the amount of profit that companies have at their disposal, after taxes are paid, has increased. The federal statutory tax rate on general business income was reduced from 28% in 2000 to 21% from 2004 to 2007, and then again by 2012 to its current rate of 15%. With provincial tax rates on corporate income also falling, Canada’s average federal-‐provincial statutory corporate tax rate dropped from just over 43% in 2000 to 25% in 2012 and 2013. However, recent increases in provincial corporate tax rates have again pushed the average combined statutory rate up to approximately 26.3% in 2015.

5

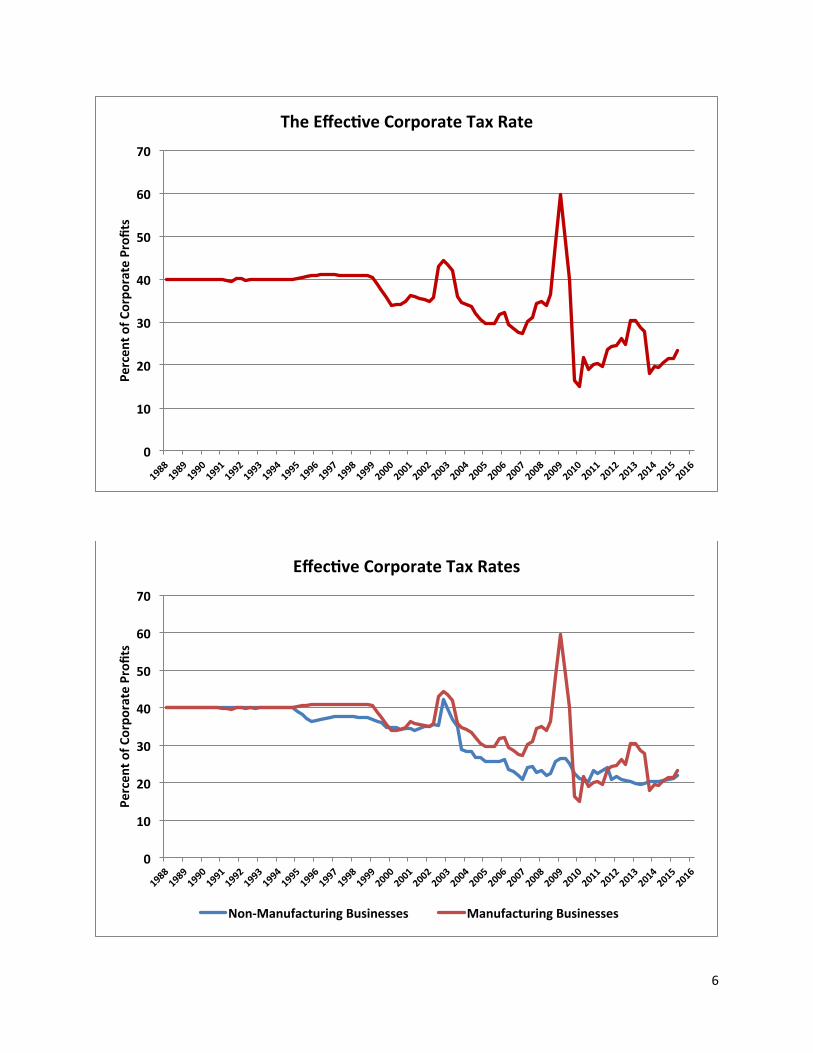

Statutory tax rate reductions translate into lower effective tax rates on corporate income. Effective tax rates measure the amount of income taxes that corporations actually pay as a percentage of their before-‐tax profits. They differ from statutory rates because they take into consideration additional tax credits applied against taxes payable, include corporations that pay the lower small business tax rate, and reflect actual tax payments as opposed to the amount of income tax owing for any specific period of time. (Scheduled tax payments may lead to a spike in effective tax rates if profits suddenly drop, as was the case during the recession of 2008/09). The effective corporate rate has declined from around 40% throughout most of the 1990s to 22% during the first half of 2015. Again, the impact of recent increases in provincial rates can be seen. Canada’s effective corporate tax rate fell to 18% in 2013 but has since risen to 23% in the second quarter of 2015.

28.0 27.0 25.0 23.0 21.0 21.0 21.0 21.0 19.5 19.0 18.0 16.5 15.0 15.0 15.0 15.0

15.1 15.1 15.1

15.1 15.1 15.1 15.1 15.1

14.0 14.0 13.0 11.5

10.0 10.5 10.5 11.3

0

5

10

15

20

25

30

35

40

45

50

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Percen

t of C

orpo

rate Profits

Combined Federal-‐Provincial Statutory Corporate Income Tax Rates

Federal Average Provincial

6

0

10

20

30

40

50

60

70

Percen

t of C

orpo

rate Profits

The EffecZve Corporate Tax Rate

0

10

20

30

40

50

60

70

Percen

t of C

orpo

rate Profits

EffecZve Corporate Tax Rates

Non-‐Manufacturing Businesses Manufacturing Businesses

7

Canada’s manufacturing sector has generally paid a greater share of its profits in corporate taxes than other business sectors. This reflects the resort of previous federal and provincial governments to capital taxes and surtaxes levied on larger corporations, the relatively capital intensive nature of manufacturing, and the volatility of profit performance. However, the tax reforms implemented over the past 15 years have brought effective tax rates for manufacturers more in line with those paid by other business sectors. Pre-‐tax profit margins have declined in Canada over the past 25 years. However, lower corporate tax rates mean that today Canadian companies are earning more profits after tax as a percentage of their revenues than in previous years.

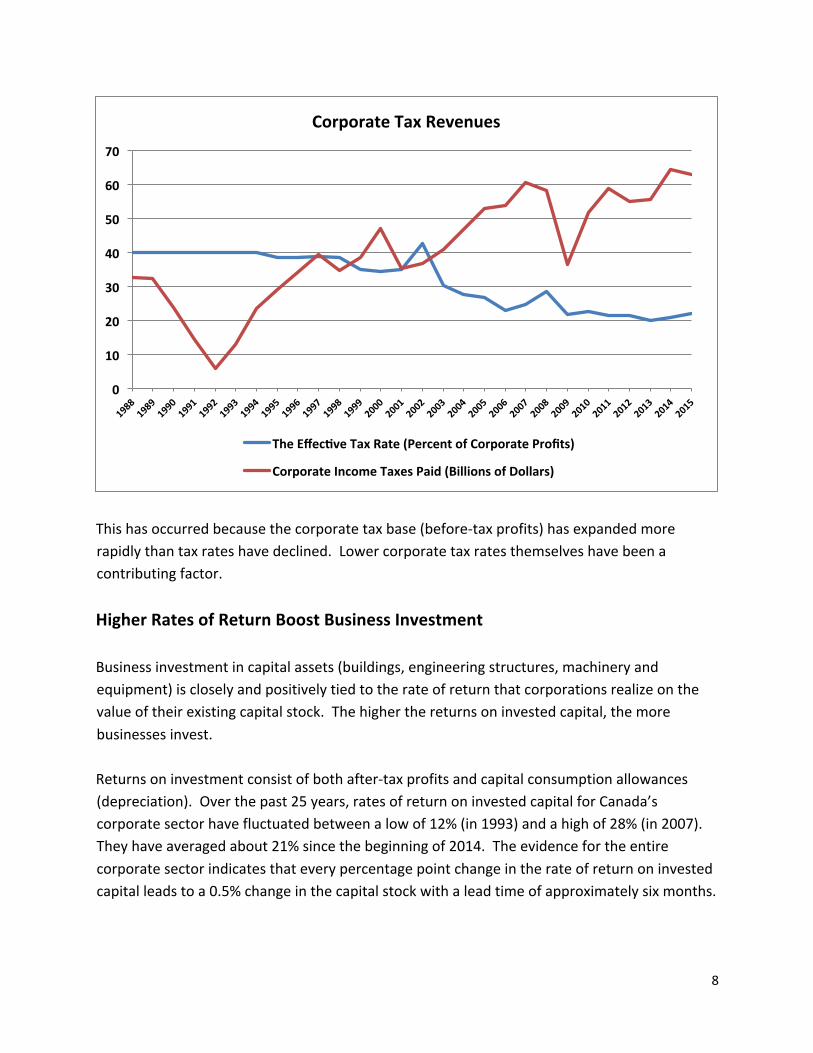

Corporate Tax Revenues Have Gone Up Higher after-‐tax profit margins do not mean that governments are collecting less in the way of corporate income taxes. Even though effective corporate tax rates have fallen, the amount of money that businesses actually pay in corporate taxes increased 34% between 2000 and 2014.

-‐2 -‐1 0 1 2 3 4 5 6 7 8 9

10

Percen

t of R

even

ue

Corporate Profit Margins

Before-‐Tax Profit Margin A^er-‐Tax Profit Margin

8

This has occurred because the corporate tax base (before-‐tax profits) has expanded more rapidly than tax rates have declined. Lower corporate tax rates themselves have been a contributing factor. Higher Rates of Return Boost Business Investment Business investment in capital assets (buildings, engineering structures, machinery and equipment) is closely and positively tied to the rate of return that corporations realize on the value of their existing capital stock. The higher the returns on invested capital, the more businesses invest. Returns on investment consist of both after-‐tax profits and capital consumption allowances (depreciation). Over the past 25 years, rates of return on invested capital for Canada’s corporate sector have fluctuated between a low of 12% (in 1993) and a high of 28% (in 2007). They have averaged about 21% since the beginning of 2014. The evidence for the entire corporate sector indicates that every percentage point change in the rate of return on invested capital leads to a 0.5% change in the capital stock with a lead time of approximately six months.

0

10

20

30

40

50

60

70

Corporate Tax Revenues

The EffecZve Tax Rate (Percent of Corporate Profits)

Corporate Income Taxes Paid (Billions of Dollars)

9

Manufacturing investment is also very sensitive to rates of return on invested capital. Over the past 25 years, manufacturers have seen their rates of return fluctuate between a low of 11% (in 1992) and a high of 32% (in 2000). Returns have averaged around 20% of invested capital since the beginning of 2014. For manufacturing, every percentage point change in the rate of return on invested capital leads to a 1.2% change in the capital stock. There is a lead time of 12 to 18 months before capital investments are actually made8. Based on the current financial performance of Canadian corporations, every one point increase in the combined federal-‐provincial corporate tax rate would reduce the rate of return on capital by 0.77 percentage points and lower capital investment intentions by approximately 0.4% or $7.0 billion. Manufacturers would see their rate of return fall by 0.74 percentage points, reducing their investment intentions by 0.9% or by $2.8 billion.

8 This is why an extended period of accelerated capital consumption allowances (rates of depreciation) is so important for Canadian manufacturers. The ten-‐year ACCA announced in the 2015 federal budget should increase the rate of return on capital assets in manufacturing by 1.5 percentage points and increase capital investment by approximately $5.6 billion.

0

5

10

15

20

25

30

Percen

t Returns on Investment & Growth of the Capital Stock

Annual A^er-‐Tax Return on Invested Capital (Percent of Capital Stock)

Year-‐over-‐Year Percent Change in Capital Assets

10

Business Investment and Economic Growth Businesses invest to improve productivity and expand production – to compete and grow. Higher rates of investment enable business growth, increasing personal incomes and employment while at the same time expanding the tax base. Business investment is an important contributor to overall economic activity (Gross Domestic Product). At a macro-‐economic level, lower corporate tax rates have raised returns on invested capital, boosted business investment, and accelerated economic growth. An increase in corporate tax rates would have the opposite impact. If profits are transferred from businesses to government in the form of corporate income taxes and then spent in the economy, they would still contribute to economic growth. However, more money would be lost to the economy as a result of foregone business investment than would be repurposed by government. In fact, based on the relationship between after-‐tax rates of return and investment performance, every dollar of corporate tax revenue raised and subsequently spent by government leads to a net loss in GDP of approximately $1.449.

9 This is in line with B. Dahlby’s findings noted above.

-‐10

-‐5

0

5

10

15

20

25

30

35

Percen

t Returns on Investment & Growth of the Capital Stock in

Manufacturing

Annual A^er-‐Tax Return on Invested Capital (Percent of Capital Stock)

Year-‐over-‐Year Percent Change in Capital Assets

11

As a result, based on the current financial performance of Canadian corporations, every one point increase in the combined federal-‐provincial corporate tax rate would lead to a net economic loss of $4.1 billion. Wages, salaries, and benefits in Canada currently average around $55,000 per employee. Every one percentage point increase in the corporate tax rate would therefore lead to the loss of 74,800 jobs10. More Profitable Businesses Hire More People Another way of estimating the impact that changing corporate tax rates have on jobs is by analyzing the relationship that can be seen between corporate after-‐tax profit margins on the one hand and the unemployment rate on the other.

Higher after-‐tax corporate profit margins are directly correlated with lower overall rates of unemployment in Canada, with changes in profitability usually preceding changes in unemployment by a period of three to six months11. 10 This supports J. Mintz’s conclusions noted above. 11 Employment data are from Statsistics Canada’s Labour Force Survey. CANSIM table 282-‐0001, Statistics Canada.

0

2

4

6

8

10

12

14

Percen

t

Profitable Businesses Create Jobs

Corporate A^er-‐Tax Profit Margin Canada's Unemployment Rate

12

When businesses are more profitable, they invest and grow. Not only do they employ more people directly, but they positively contribute to job growth across the Canadian economy, including public sector jobs. On the other hand, when profits come under pressure, labour and capital expenditures are cut back and the rate of unemployment goes up. Every point increase in the after-‐tax profit margin of Canada’s corporate sector (after-‐tax profits as a percent of total business revenue) lowers Canada’s unemployment rate by approximately 2 percentage points and vice versa. The impact of an increase in corporate tax rates would be to reduce after-‐tax profits by the equivalent amount of taxes raised plus a reduction in sales revenue equivalent to the net economic loss of the tax rate increase (which would also fall to the bottom line). Based on the current state of the Canadian economy and Canadian business finances, every one point increase in the combined federal-‐provincial corporate tax rate would reduce after-‐tax profits by $4.3 billion and the after-‐tax profit margin for business by 0.19 percentage points. This would in turn increase Canada’s unemployment rate by 0.38 percentage points, leading to the loss of approximately 73,000 jobs. Increasing Corporate Tax Rates is a Bad Idea Higher corporate income tax rates will depress rates of return on invested capital and make Canada a less attractive location for businesses to invest. They will decelerate the growth of business investment, leading to a net economic loss for the Canadian economy. They will increase Canada’s unemployment rate and erode employment growth. Based on the current state of the Canadian economy and Canadian business finances, every one percentage point increase in the corporate income tax rate would, on an annual basis: • Transfer $2.86 billion in business profits to the federal government, $560 million from

manufacturers; • Cut dividend payments to Canadians by $1.8 billion, and reduce their savings by even more; • Lower the rate of return on the capital stock of Canada’s business sector by 0.77

percentage points; • Reduce business investment activity by 0.4% or approximately $7.0 billion; • Depress manufacturing investment by $2.8 billion; • Lead to a net loss in GDP of $4.1 billion; • Reduce the after-‐tax profit margin of Canadian business by 0.19 percentage points or $4.3

billion; and, • Eliminate 73,000 to 75,000 jobs.