f6 passcard.pdf

TRANSCRIPT

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 1/179

http://freeaccastudymaterial.com

fb.com/freeaccastudymaterial

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 2/179

ACCA Passcards

Paper F6Taxation (UK)

FA 2014

For exams from 1 April 2015

to 31 March 2016

ACCA APPROVED CONTENT PROVIDER

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 3/179

Fundamentals Paper F6

Taxation FA 2014

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 4/179

First edition 2007, Ninth edition October 2014

ISBN 9781 4727 2243 0

e ISBN 9781 4727 2566 0

British Library Cataloguing-in-Publication DataA catalogue record for this book is available from the

British Library

Your learning materials, published by BPP LearningMedia Ltd, are printed on paper obtained from traceablesustainable sources.

Published byBPP Learning Media Ltd,BPP House, Aldine Place,142–144 Uxbridge Road,London W12 8AA

www.bpp.com/learningmedia

Printed in the United Kingdomby Ricoh UK Ltd

Unit 2Wells PlaceMerstham, RH1 3LG

All rights reserved. No part of this publication may bereproduced, stored in a retrieval system or transmitted, iany form or by any means, electronic, mechanical,photocopying, recording or otherwise, without the priorwritten permission of BPP Learning Media.

©

BPP Learning Media Ltd2014

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 5/179

Page iii

Welcome to BPP Learning Media's ACCA Passcards for Fundamentals Paper F6 Taxation (UK).

They save you time. Important topics are summarised for you.

They incorporate diagrams to kick start your memory.

They follow the overall structure of the BPP Learning Media Study Texts, but BPP Learning Media'sACCA Passcards are not just a condensed book. Each card has been separately designed for clearpresentation. Topics are self contained and can be grasped visually.

ACCA Passcards are still just the right size for pockets, briefcases and bags.

ACCA Passcards focus on the exam you will be facing.

Run through the complete set of Passcards as often as you can during your final revision period. The day

before the exam, try to go through the Passcards again! You will then be well on your way to passing yourexams.

Good luck!

ContentsPreface

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 6/179

ContentsPreface

Page

1 Introduction to the UK tax system 1

2 Computing taxable income 93 Computing the income tax liability 17

4 Employment income 23

5 Taxable and exempt benefits.The PAYE system 27

6 Pensions 35

7 Property income 41

8 Computing trading income 45

9 Capital allowances 51

10 Assessable trading income 57

11 Trading losses 61

Pa

12 Partnerships and limited liabilitypartnerships 6

13 National insurance contributions 6

14 Computing chargeable gains 7

15 Chattels and the principal private residenceexemption 8

16 Business reliefs 8

17 Shares and securities 9

18 Self-assessment and payment of tax by

individuals 919 Inheritance tax 1

20 Computing taxable total profits 1

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 7/179

ContePage v

Page

21 Computing the corporation tax liability 123

22 Chargeable gains for companies 12723 Losses 135

24 Groups 139

Pa

25 Self-assessment and payment of tax bycompanies 1

26 An introduction to VAT 1

27 Further aspects of VAT 1

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 8/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 9/179

1: Introduction to the UK tax system

Topic List

The overall function and purpose oftaxation in a modern economy

Different types of taxes

Principal sources of revenue law andpractice

Tax avoidance and tax evasion

This chapter contains background knowledge which underpins the whole of your later studies of taxation.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 10/179

Tax avoidanceand tax evasion

Principal sources ofrevenue law and practice

Different typesof taxes

The overall function and purposeof taxation in a modern economy

Economic factorsTaxation represents a withdrawal from the UK economy. Tax policies can be used to encourage anddiscourage certain types of activity.

Saving Charitable donations Entrepreneurs Investment in plant and machinery

Encourages

Smoking Alcohol Motoring

Discourages

Social factorsTax policies can be used to redistribute wealth

Direct taxes – tax only those who have these resources Indirect taxes – discourage spending Progressive taxes – target those who can afford to pay

Environmental factorsTaxes may be levied for environmentalreasons

Climate change levy Landfill tax

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 11/179

Tax avoidanceand tax evasion

Principal sources ofrevenue law and practice

Different typesof taxes

The overall function and purposeof taxation in a modern economy

1: Introduction to the UK tax sysPage 3

Directtaxes

Indirecttaxes

Income tax Individuals Partnerships

Corporation tax Companies

Capital gains tax Individuals Partnerships Companies (in the form of corporation tax)

Inheritance tax Individuals

National insurance Employers Employees Self-employed

Value added tax Businesses (both incorporated and unincorporate

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 12/179

HM Revenue and Customs

Structure of the UK Tax system

Tax avoidanceand tax evasion

Principal sources ofrevenue law and practice

Different typesof taxes

The overall function and purposeof taxation in a modern economy

Treasury

Officers of Revenue and Customs Crown Prosecution Service

Appeals heard by

First Tier Tribunal (most cases) Upper Tribunal (complex cases)

Sources of revenue law and practice

StatuteStatutory instrument

Law

Statements of practice

Extra-statutory concessionsExplanatory leafletsRevenue and Customs BriefInternal Guidance (HMRC manuals)Working Together

Practice

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 13/179

1: Introduction to the UK tax sysPage 5

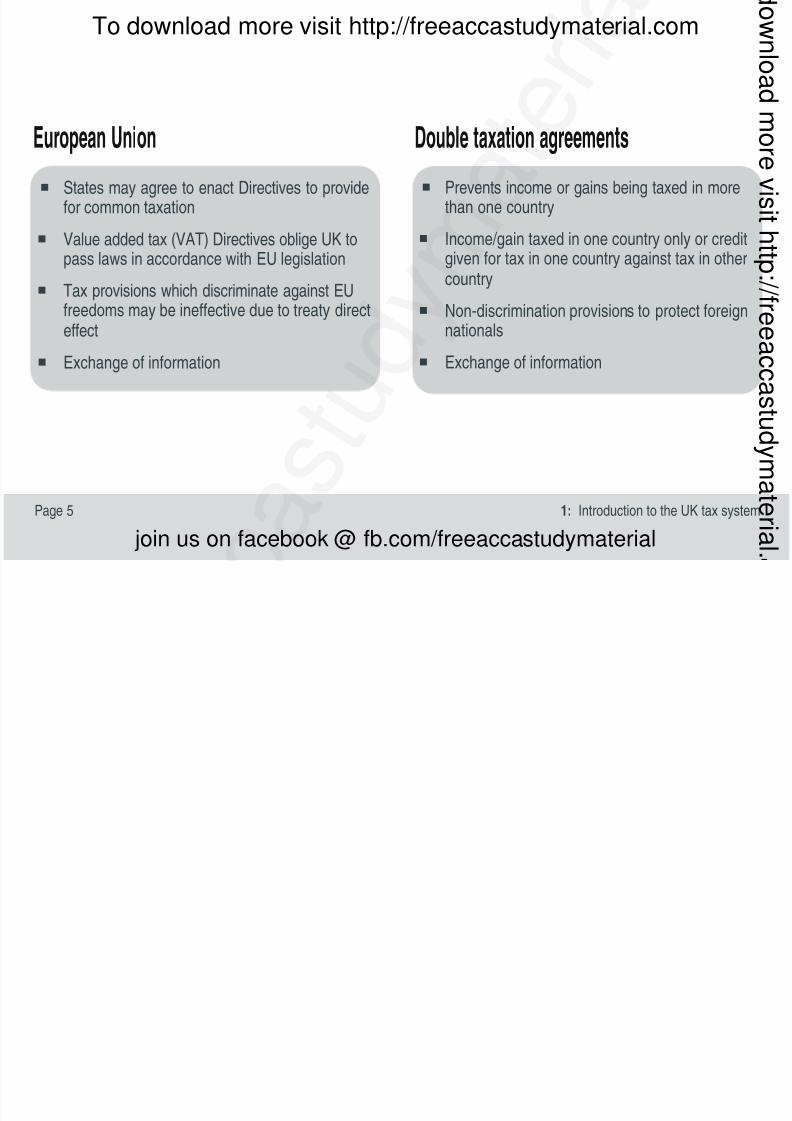

European Union Double taxation agreements

States may agree to enact Directives to providefor common taxation

Value added tax (VAT) Directives oblige UK topass laws in accordance with EU legislation

Tax provisions which discriminate against EUfreedoms may be ineffective due to treaty directeffect

Exchange of information

Prevents income or gains being taxed in morethan one country

Income/gain taxed in one country only or credgiven for tax in one country against tax in othecountry

Non-discrimination provisions to protect foreignationals

Exchange of information

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 14/179

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 15/179

1: Introduction to the UK tax sysPage 7

General Anti-Abuse Rule (GAAR)

HMRC can counteract tax advantages from abusive tax arrangements

Tax arrangements involve obtaining a tax advantage as (one of) their mainpurpose(s)

Arrangements are abusive if they cannot be regarded as a reasonable course ofaction and result in eg significantly less income, profits or gains being taxable

Tax advantage includes relief or repayment of tax

HMRC may counteract tax advantages arising by eg increasing the taxpayer'stax liability

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 16/179

Tax avoidanceand tax evasion

Principal sources ofrevenue law and practice

Different typesof taxes

The overall function and purposeof taxation in a modern economy

Concerns whether client is honest with HMRC

Professional judgement of accountant

Must act honestly and objectively

Recommend disclosure to HMRC

If no disclosure, cease to act

Make money laundering report

Inform HMRC but not details of why

Avoid 'tipping-off' the client

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 17/179

2: Computing taxable income

Topic List

Scope of income tax

Computing taxable income

Chargeable/Exempt incomeDeductible interest

The computation of income tax is a key exam topic. Onof the 15 mark questions in Section B will focus on income tax. Income tax will also be tested in Section Aand may also appear in the 10 mark questions in Section B. This chapter deals with computing taxable income which draws together all of the taxpayer's income. In the next chapter you will see how the incomtax liability is computed on taxable income.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 18/179

Computingtaxable income

Deductibleinterest

Scope ofincome tax

Chargeable/Exempt income

Test 1st: Automatically not UK resident

In UK < 16 days in tax year

In UK < 46 days in tax year, not resident inany of three previous tax years

Works full time overseas in tax year, not inUK > 90 days in tax year

Test 2nd: Automatically UK reside

In UK > 183 days in tax year

Only home in UK

Works full time in UK in tax year

An individual who is UK resident is taxable on world-wide income.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 19/179

2: Computing taxable incoPage 11

Test 3rd: UK ties

Close family (spouse or civil partner/minor child)resident in UK

Home available in UK, used in tax year

Substantive work in UK

In UK > 90 days in either of two previous tax yea

Spends more time in UK than anywhere else in tayear (if previously resident only)

Number of ties requiredto be UK resident

depends on number of days

spent in UK in tax year

(see Tax Tables)

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 20/179

Computingtaxable income

Deductibleinterest

Scope ofincome tax

Chargeable/Exempt income

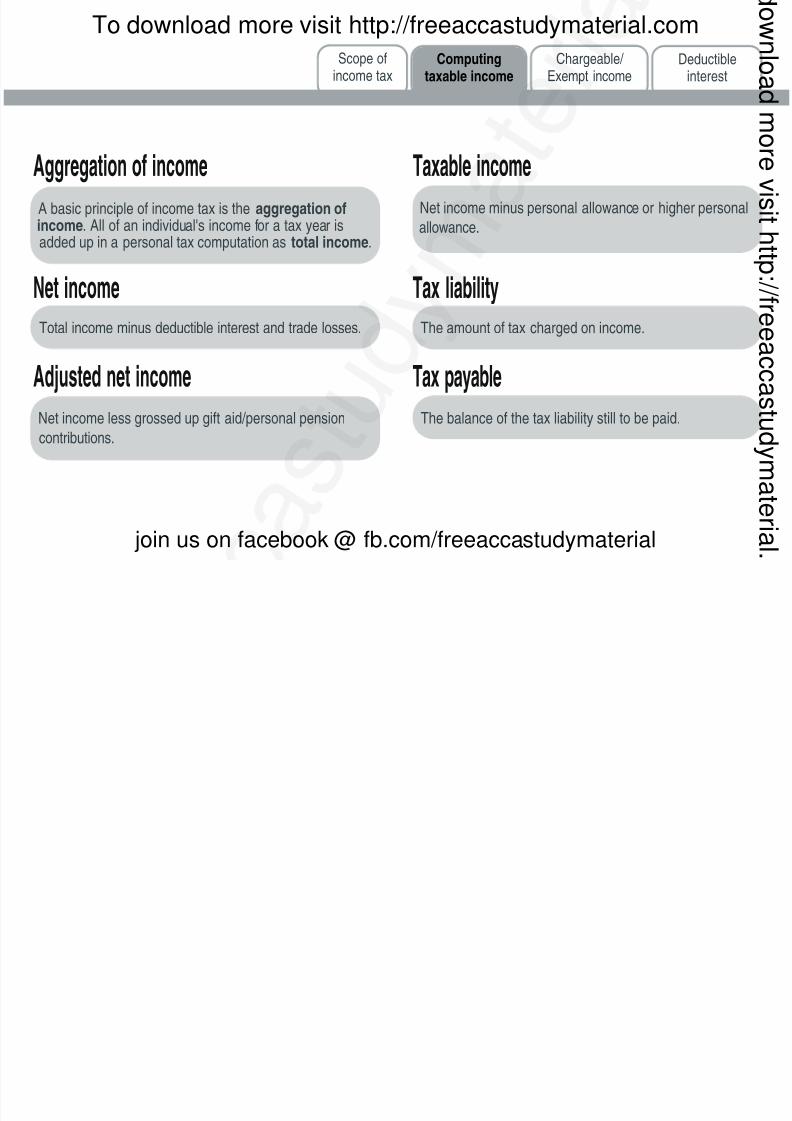

Aggregation of income

A basic principle of income tax is the aggregation ofincome. All of an individual's income for a tax year isadded up in a personal tax computation as total income.

Taxable income

Net income minus personal allowance or higher person

allowance.

Adjusted net incomeNet income less grossed up gift aid/personal pension

contributions.

Net incomeTotal income minus deductible interest and trade losses.

Tax liabilityThe amount of tax charged on income.

Tax payableThe balance of the tax liability still to be paid.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 21/179

2: Computing taxable incoPage 13

Personal allowance andhigher personal allowance

Individual born on or after 6 April 1948

£10,000 for 2014/15

Restrict if adjustednet income > £100,000

by £1 for each £2 excess(nil if > £120,000).

Individual born 5 April 1948 or before

£10,500 born 6.4.38 to 5.4.48 for 2014/15£10,660 born before 6.4.38 for 2014/15

Restrict if adjustednet income > £27,000

by £1 for each £2 excess

to minimum £10,000(unless income > £100,000, thenrestrict as for standard allowance)

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 22/179

Computingtaxable income

Deductibleinterest

Scope ofincome tax

Chargeable/Exempt income

Exempt income

Types of income Income taxed at source

The main types of income for individuals are:

Profits of trades, professions and vocations

Income from employment and pensions

Property income

Savings and investment income, including interestand dividends

Many sorts of investment income are taxed at sourcefor every £100 of income, the individual only receives£80 of interest or £90 of dividends from UK companieThe taxable income in both cases is £100, but credit igiven for the tax suffered.

Premium bond prizes Income from New Individual Savings Accounts (NISAs) Returns on National Savings Certificates

Leave exempt income out of

personal tax computations.

This applies to bank andbuilding society interest.

Tax credits on dividecan be offset to redua tax bill but are neverepaid to a taxpayer.

credits on other taxeincome can be repai

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 23/179

Computingtaxable income

Deductibleinterest

Scope ofincome tax

Chargeable/Exempt income

2: Computing taxable incoPage 15

Deductible interest

Interest paid on a particular type of loan is

deducted from total income to compute netincome.

For purchase of an interest in a partnership, or

For purchase of plant and machinery forpartnership (purchase must be by partner), or

For purchase of plant and machinery for use inemployment (purchase must be by employee)

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 24/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 25/179

3: Computing the income tax liability

Topic List

Computing income tax

Gift aid

Child benefit chargeJointly held property

In this chapter we deal with computing income tax, usintaxable income that was covered in the previous chapteWe also look at how gift aid donations are given tax relief, the computation of the child benefit charge and how jointly held property is taxed.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 26/179

Jointly heldproperty

Child benefitcharge

Gift aidComputingincome tax

If non-savings income does not exceed the starting rate limit, then the savings income is taxed at the startingrate (10%) up to the starting rate limit: £2,880 for 2014/15

Total non-savings, savings and dividend income separately

Deduct deductible interest, losses and the personal allowancefrom non-savings income first, then savings income thendividend income

Tax non-savings income, then savings income, then dividendincome

There is only one set of rate bands to cover all

types of income.

Broadly interest

At 20%, 40% and 45%

At 10%, 20%, 40% and 45%

At 10%, 32.5% and 37.5%

Computing income tax

1

2

3

The basic rate limit and higher rate limit

must be increased by the gross amount oany gift aid donation/personal pensioncontribution (amount paid × 100/80).

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 27/179

Jointly heldproperty

Child benefitcharge

Gift aidComputingincome tax

3: Computing the income tax liabPage 19

Gift aid

Gift aid donations are charitable gifts of money which qualify for tax relief.

Donor must make a gift aid declaration to the charity.

Basic rateBasic rate tax relief given by treating

donation as net of basic rate tax

Higher and additionalrate

Higher and additional rate tax reliefgiven by increasing limits by grossed

up donation

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 28/179

Jointly heldproperty

Child benefitcharge

Gift aidComputingincome tax

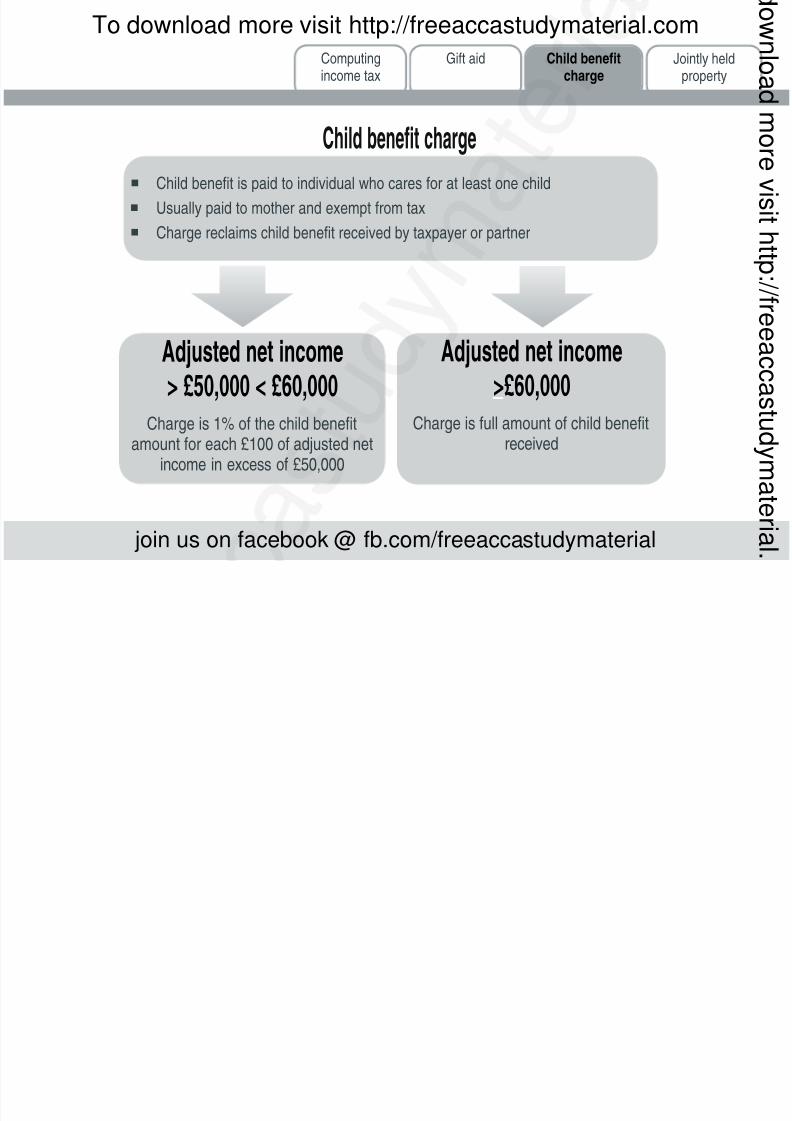

Child benefit charge

Child benefit is paid to individual who cares for at least one child

Usually paid to mother and exempt from tax

Charge reclaims child benefit received by taxpayer or partner

Adjusted net income

> £50,000 < £60,000Charge is 1% of the child benefit

amount for each £100 of adjusted netincome in excess of £50,000

Adjusted net income

>£60,000Charge is full amount of child benefit

received

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 29/179

Jointly heldproperty

Child benefitcharge

Gift aidComputingincome tax

3: Computing the income tax liabPage 21

Jointly held property

Spouses and civil partners often hold property jointly, sometimes in unequal proportions.

For tax purposes treat the income received fromsuch property as shared equally.

If the actual interests in the property are unequal,spouses/civil partners can declare this to HMRCand income is then shared in actual proportions.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 30/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 31/179

4: Employment income

Topic List

Employment and self-employment

Basis of assessment

Allowable deductions

Although this exam is mainly computational you may beasked to describe the difference between employment and self-employment in a Section B question.

You also need to be aware of the final two topics in thischapter: when employment income is assessed and thedeductions that you may be able to make in computing

the amount of assessable employment income.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 32/179

Allowabledeductions

Employment andself-employment

Basisof assessment

Whether a contract is a contract of service or acontract for services will depend on a number offactors.

Employed or self-employed

An employee works under a contract of service anda self-employed person under a contract for services.

The degree of control exercised over theperson doing the work

Whether he must accept further work

Whether the other party must provide further wo

Whether he provides his own equipment

Whether entitled to benefits eg pension

Whether he hires his own helpers

What degree of financial risk he takes

What degree of responsibility for investmentand management he has

Whether he can profit from sound manageme Whether he can work when he chooses

The wording used in any agreement betweenparties

Factors

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 33/179

Allowabledeductions

Employment andself-employment

Basisof assessment

4: Employment incoPage 25

Earnings are taxed in the year in which they arereceived.

Employees/directors are taxed on income fromthe employment:

Cash earnings Benefits

Employment income

The general definition of the date of receipt isthe earlier of:

The time payment is made The time entitlement to payment arises

Directors are deemed to receive earnings on the earlieof the following:

The time given by the general rule

The time the amount is credited in the company's

accounting records The end of the company's period of account (if the

amount has been determined by then)

When the amount is determined (if after the end othe company's period of account)

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 34/179

Allowabledeductions

Employment andself-employment

Basisof assessment

Expenses specifically deductible against earnings:

Insurance premiums to cover directors' and employees'liabilities (and payments to meet those liabilities)

Subscriptions to relevant professional bodies

Qualifying travel expenses – costs the employee incurstravelling in the performance of his duties or/and travellingto or from a place attended in the performance of duties

Contributions (within limits) to a registered occupational

pension schemePayments to charity under a payroll deductionscheme

1

2

3

4

5

The strictness of this test has beenemphasised in many cases.

The general rule is that expenses can only be deducted fromearnings if they are incurred wholly, exclusively and necessarily

in performing the duties of the employment.

Normal commuting does not qualify Relief is available for expenses incurred by

employee working at a temporary location oa secondment of 24 months or less

If a mileage allowance is paid relief isavailable for any shortfall of allowance actuapaid below statutory mileage allowance

Exam focusIf you have to decide whether an expensis deductible, put yourself in HMRC'sposition and try to find an argumentagainst deducting it. If you can find aspecific argument, the expense is probabnot deductible.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 35/179

5: Taxable and exempt benefits.The PAYE system

Topic List

Taxable benefits

Exempt benefits

The PAYE system

Benefits may be tested as part of a Section B question or in Section A so it is vital that you are able to calculatthe taxable value of benefits provided to employees.Youalso need to be aware of the benefits that are exempt from tax.

The deduction of tax from employment income through the PAYE system is also important.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 36/179

VouchersGeneral business expenses

The PAYEsystem

Exemptbenefits

Taxablebenefits

Taxed on most employees

Except excluded employees (eg earn less

than £8,500 p.a. and not director) onlytaxable on certain benefits

'P11D employees' are employees who arenot excluded employees.

Cash vouchers

Credit token

Non-cash vouchers

Taxable on all employees (cost of providing benefit)

Reimbursed expenses taxable onemployees (not excluded employees).

May make deduction claim.

Non-cash benefits

Including excluded employees

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 37/179

Accommodation Living expenses

5: Taxable and exempt benefits. The PAYE sysPage 29

Annual value of accommodation is a

taxable benefit on all employees, unless job related.

Additional charge if costs more than£75,000.

Living expenses connected with

accommodation (eg gas bills) are taxable P11D employees only. However, if theaccommodation is job-related, the maximuamount taxable is 10% of net earnings.

Excess multiplied by official rate ofinterest at the start of the tax year

Includingexcludedemployees

Original cost plus the cost ofimprovements incurred priorto start of tax year

Vans

£3,090 charge if available for privateuse (not home/work commuting)

£581 charge for private fuel

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 38/179

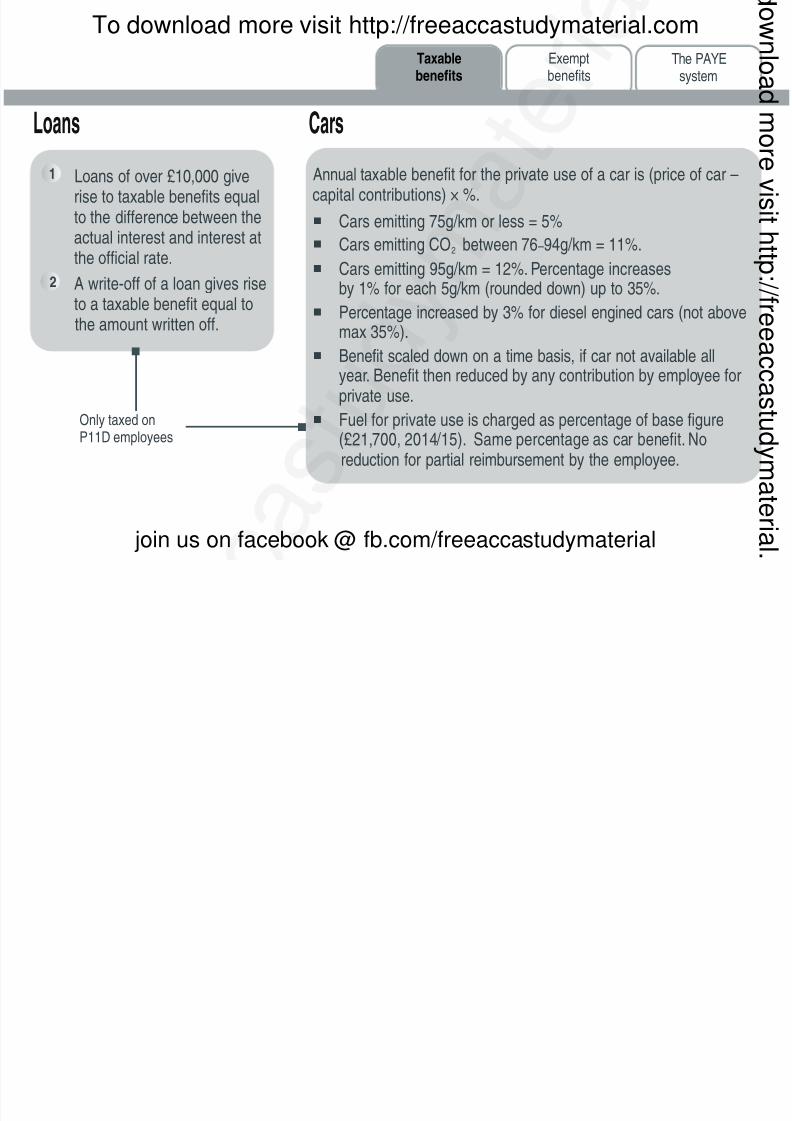

Loans Cars

The PAYEsystem

Exemptbenefits

Taxablebenefits

Annual taxable benefit for the private use of a car is (price of car –

capital contributions) × %. Cars emitting 75g/km or less = 5%

Cars emitting CO2 between 76–94g/km = 11%.

Cars emitting 95g/km = 12%. Percentage increasesby 1% for each 5g/km (rounded down) up to 35%.

Percentage increased by 3% for diesel engined cars (not abovmax 35%).

Benefit scaled down on a time basis, if car not available allyear. Benefit then reduced by any contribution by employee fo

private use. Fuel for private use is charged as percentage of base figure

(£21,700, 2014/15). Same percentage as car benefit. Noreduction for partial reimbursement by the employee.

Loans of over £10,000 give

rise to taxable benefits equalto the difference between theactual interest and interest atthe official rate.

A write-off of a loan gives riseto a taxable benefit equal tothe amount written off.

1

2

Only taxed onP11D employees

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 39/179

Other benefits

5: Taxable and exempt benefits. The PAYE sysPage 31

In general, if an asset is made available for private use, theannual taxable benefit is 20% of the market value when theasset was first provided, less any employee contribution.

If the asset is subsequently givento the employee the taxable

benefit is the higher of:(i) Original MV less amounts

already taxed

(ii) Market value at date of gift

less any employee contribution.

Taxable value of other benefits charged on

employees other than excluded employees

Excluded employees taxed only on secondhandvalue as cash earnings

Cost of provision of benefit less anyamount made good by employee

Not used if asset is bicycle

Private use of asset

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 40/179

The PAYEsystem

Exemptbenefits

Taxablebenefits

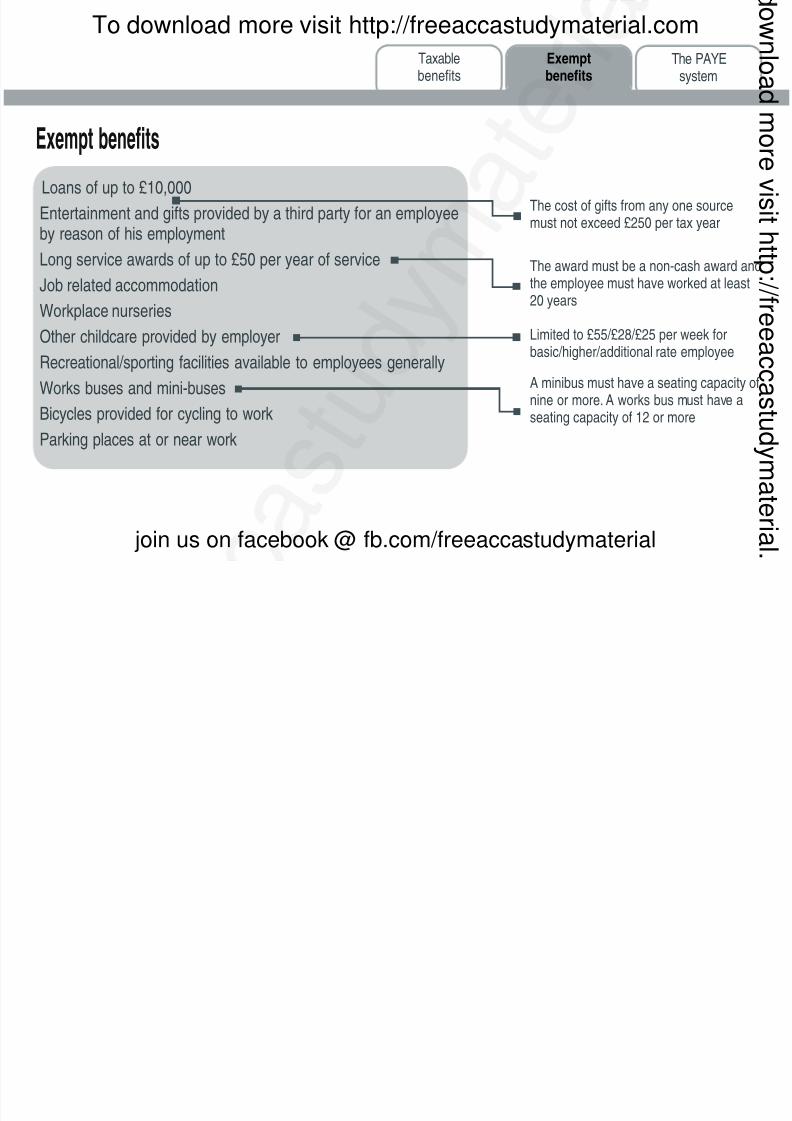

Exempt benefits

Loans of up to £10,000Entertainment and gifts provided by a third party for an employeeby reason of his employment

Long service awards of up to £50 per year of service

Job related accommodation

Workplace nurseries

Other childcare provided by employer

Recreational/sporting facilities available to employees generally

Works buses and mini-busesBicycles provided for cycling to work

Parking places at or near work

The cost of gifts from any one sourcemust not exceed £250 per tax year

The award must be a non-cash award the employee must have worked at lea20 years

Limited to £55/£28/£25 per week forbasic/higher/additional rate employee

A minibus must have a seating capacitnine or more. A works bus must have aseating capacity of 12 or more

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 41/179

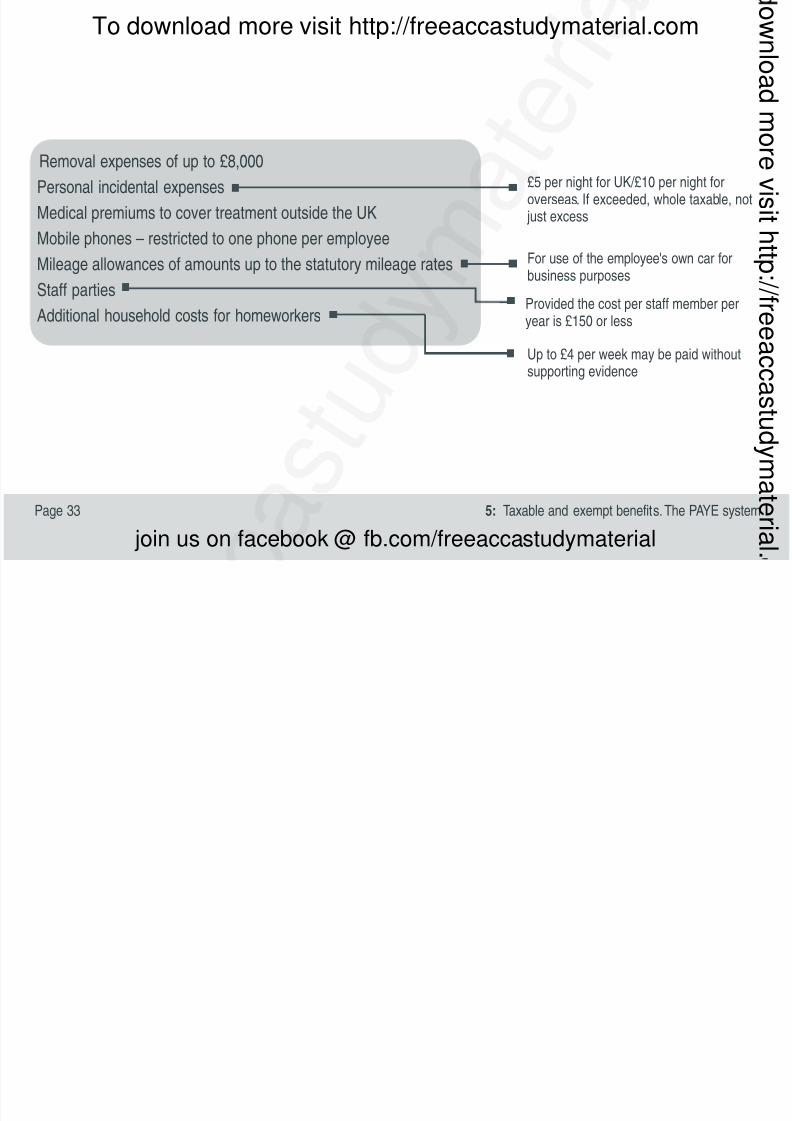

5: Taxable and exempt benefits. The PAYE sysPage 33

Removal expenses of up to £8,000

Personal incidental expensesMedical premiums to cover treatment outside the UK

Mobile phones – restricted to one phone per employee

Mileage allowances of amounts up to the statutory mileage rates

Staff parties

Additional household costs for homeworkers

For use of the employee's own car forbusiness purposes

Provided the cost per staff member peryear is £150 or less

Up to £4 per week may be paid withoutsupporting evidence

£5 per night for UK/£10 per night for

overseas. If exceeded, whole taxable, n just excess

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 42/179

PAYE settlement agreements

The PAYEsystem

Exemptbenefits

Taxablebenefits

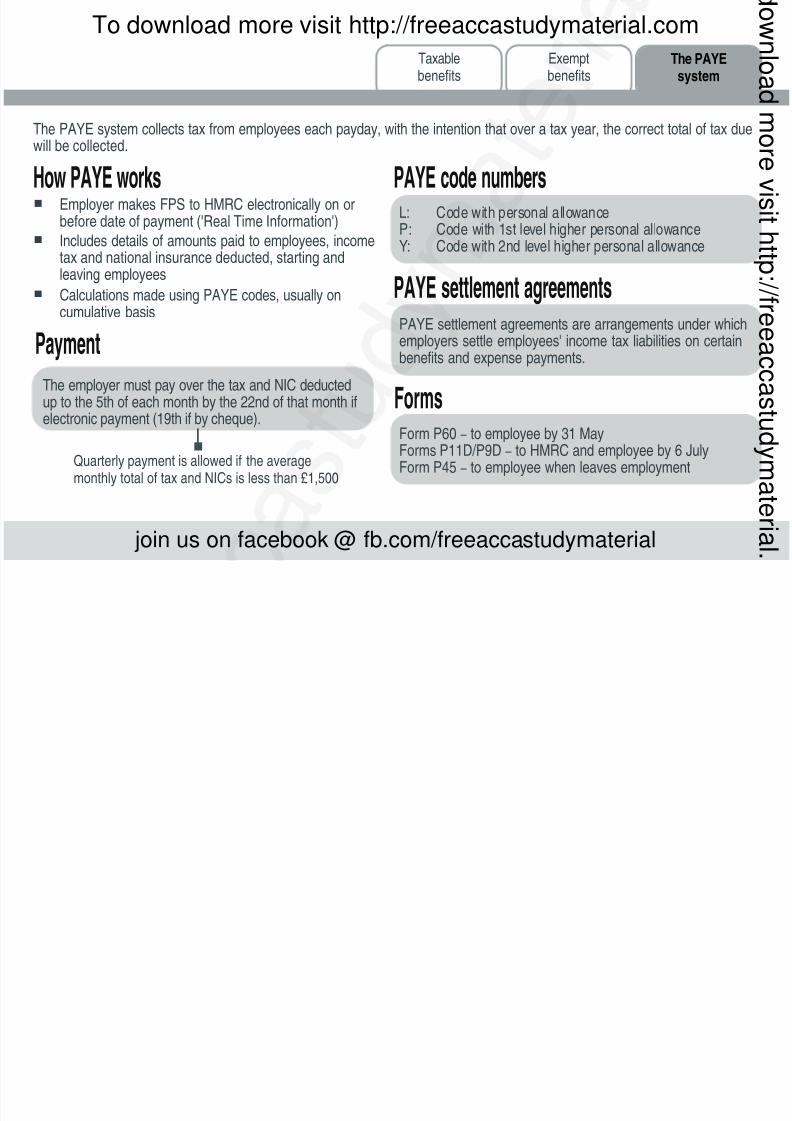

The PAYE system collects tax from employees each payday, with the intention that over a tax year, the correct total of tax dwill be collected.

How PAYE works Employer makes FPS to HMRC electronically on or

before date of payment ('Real Time Information')

Includes details of amounts paid to employees, incometax and national insurance deducted, starting andleaving employees

Calculations made using PAYE codes, usually oncumulative basis

The employer must pay over the tax and NIC deductedup to the 5th of each month by the 22nd of that month ifelectronic payment (19th if by cheque).

PAYE code numbers

Forms

Quarterly payment is allowed if the averagemonthly total of tax and NICs is less than £1,500

PAYE settlement agreements are arrangements under whicemployers settle employees' income tax liabilities on certainbenefits and expense payments.

L: Code with personal allowanceP: Code with 1st level higher personal allowanceY: Code with 2nd level higher personal allowance

Form P60 – to employee by 31 MayForms P11D/P9D – to HMRC and employee by 6 JulyForm P45 – to employee when leaves employment

Payment

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 43/179

6: Pensions

Topic List

Types of pension scheme

Contributions to pension schemes

Receiving benefits from pensionarrangements

A single regime applies to all pensions, whether occupational or personal.

Pension contributions are a tax efficient way of saving fretirement.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 44/179

Contributions topension schemes

Receiving benefits frompension arrangements

Types ofpension scheme

Pension Schemes

Occupational Pension Scheme Personal Pension Scheme

Employees only All individuals

Defined Benefits Money Purchase

Pension based onearnings andlength of service

No guarantee of amountof pension. Investmentsare used to 'build up' fund

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 45/179

Annual limit

Contributions topension schemes

Receiving benefits frompension arrangements

Types ofpension scheme

6: PensPage 37

Maximum contribution attracting taxrelief is higher of:

Relevant earnings

£3,600 pa

£1,250,000 is maximum value for pension fund.

Employment income, trading income andfurnished holiday lettings income

£40,000 for 2014/15 C/f unused allowance max three years Tax charge on excess – treat as

additional non-savings income

Count towards allowances (annual and lifetime) Trade deduction for employer Tax free benefit for employee No NIC for employer or employee

Lifetime allowance

Annual allowance Employer contributions

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 46/179

Contributions topension schemes

Receiving benefits frompension arrangements

Types ofpension scheme

Occupationalpension

Personalpension

Deduct gross employee contributionsdirectly from earnings to find

net earnings

Paid net so automatic 20% tax relief

Higher rate (and additional rate)taxpayers increase basic rate (andhigher rate) limits by gross

contributions

This is the same method of givingtax relief as for gift aid donations

Also deduct grosscontributions from neincome to find adjus

net income for PArestriction

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 47/179

Contributions topension schemes

Receiving benefits frompension arrangements

Types ofpension scheme

6: PensPage 39

Pension fundat retirement

Taxable annualpension (usually)

Tax-free lump sum

If fund exceeds lifetime allowance£1.25m then tax charge on excess

25% if excesstaken as pension

55% if excesstaken as lump su

Maximum 1/4 of fund

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 48/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 49/179

7: Property income

Topic List

Computation

Furnished holiday lettings andrent-a-room relief

Property income is calculated as if the letting were a business run by the taxpayer.

There are special rules for furnished holiday lettings, anfor rooms let in the taxpayer's own home.

Property income could be tested in Section A and/or inSection B question, either as a 10 mark question or as part of a 15 mark question.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 50/179

Computation Furnished holiday lettingsand rent-a-room relief

Computation

Calculate property income profits on anaccruals basis in the same way as youcalculate trading profits.

Accounts are drawn up as for a sole trader butwith a year end of 5 April.

Rents and expenses of all properties are

pooled to give a single property income figure.If a lease for n years (50 or less) is granted fora premium, the proportion of the premiumtreated as rent is (premium – (premium ×0.02(n–1))).

Exception For furnished residential lettings, a 10% wearand tear allowance can be claimed.Capital allowances are not available.

Exception Keep a separate pool of profits/losses fromletting furnished holiday lettings.

Property income

Property income covers rent from UK property.

2

1

3

4

LossesLosses are carried forward against futureincome from the UK property business.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 51/179

7: Property incoPage 43

Computation Furnished holiday lettingand rent-a-room relief

Furnished Holiday Lettings must be

On a commercial basis

Available for letting for 210 days in the tax year

Actually let for 105 days in the tax year

Not in longer term occupation for more than 155 days during the tax year

The rent-a-room scheme exempts rent of up to £4,250a year on rooms in the landlord's main residence.

Rollover relief, entrepreneurs' relief and giftrelief are available

Loss relief – but only c/f against FHL profit

Capital allowances are available on furniture

Income is earnings for pension purposes

Continuous periods of mo

than 31 days during whichthe accommodation is in tsame occupation

Furnished holiday lettings

Furnished holiday lettings are treated as a trade formany income tax and CGT purposes

Rent-a-room scheme

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 52/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 53/179

8: Computing trading income

Topic List

Badges of trade

The adjustment of profits

Cash basis of accounting

The 'badges of trade' can be used to determine whetheor not an individual is carrying on a trade. If a trade is being carried on, the profits of the trade are taxable as trading income. Otherwise the profit may be taxable as capital gain.

In this chapter we will look at the badges of trade and athe adjustments needed in the computation of trading

income.

This is a key exam topic. It may form part of a 15 mark Section B question where you may be required to compute tax adjusted trading profits.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 54/179

Cash basis ofaccounting

The adjustmentof profits

Badgesof trade

The subject matter The frequency of transactions Similar trading transactions/interests The length of ownership Organisation as a trade Supplementary work and marketing A profit motive The way in which the asset sold was acquired Method of finance The taxpayer's intentions

Badges of trade

If on applying the badges of trade HMRconclude that a trade is being carried othe profits are taxable as trading incom

To arrive at taxable trading profits, the naccounts profit must be adjusted. We loat this in the rest of this chapter.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 55/179

Cash basis ofaccounting

The adjustmentof profits

Badgesof trade

8: Computing trading incoPage 47

Certain items of expenditure are not deductible for trading income purposes and so must be added back to thnet accounts profit when computing trading profits. Conversely other items are deductible.

Expenditure incurred wholly and exclusively fortrade purposes

Gifts to customers not costing more than £50 perdonee per year

Interest on borrowings for trade purposes

Pre-trading expenditure

Deductible expenditure

The gift must carry a conspicuous advertisement fthe business and not be food, drink, tobacco orvouchers exchangeable for goods.

If incurred in the seven years prior to the start of tr

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 56/179

Cash basis ofaccounting

The adjustmentof profits

Badgesof trade

Fines and penalties

Depreciation

Appropriations (eg salary and interest paid toproprietor)

Capital expenditure

Entertaining

Legal fees relating to capital items

General provisions

Any expense not incurred wholly and exclusively fortrade purposes

Gift aid donations

Political donations

Part of leasing cost of cars with CO2 emissions over

130 g/km

Non-deductible expenditure Employee parking fines incurred whilst onemployer's business are, however, allowed

The cost of initial repairs to make an asset fit touse is disallowable capital expenditure (Law Shipping ) but the cost of initial repairs to remednormal wear and tear is allowable (Odeon Associated Theatres Ltd v Jones )

Staff entertaining is deductible

Fees relating to the renewal of a short lease aredeductible

Disallow any general provision for impairmentlosses. A specific provision is however allowed.

These are dealt with in the personal taxcomputation

Disallow 15% of leasing cost

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 57/179

Cash basis ofaccounting

The adjustmentof profits

Badgesof trade

8: Computing trading incoPage 49

Normal basis of accounting is accruals basis

Cash basis of accounting can be used insteadby small unincorporated businesses

To start cash basis of accounting, receiptsmust not exceed VAT registration threshold

Election required

Cash basis of accounting

Cash received

less

Expenses paid

Profit

Taxable

Loss

c/f against cashsurplus

Includescapital

expendituon P&M

(except ca

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 58/179

Cash basis ofaccounting

The adjustmentof profits

Badgesof trade

Motor cars (business mileage)

Business premises used as trader's home(eg guesthouse)

Fixed rate expenses Only examinable in context ofcash basis

Rates given in question where

relevant

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 59/179

9: Capital allowances

Topic List

What is plant?

Allowances on plant and machinery

Special assets

Capital allowances are given instead of depreciation, onplant and machinery. They are trading expenses deducted in arriving at taxable trading profits.

Capital allowances are a frequently examined topic.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 60/179

Allowances onplant and machinery

Whatis plant?

Specialassets

Statute

Machinery

There are two sources of the rules on what qualifies as plant and is therefore eligible for capital allowances.

Statutory exclusions

The following items are excluded as plant by statute.

Buildings and parts of buildings

– However, utility systems provided to meet theparticular requirements of the trade, lifts, alarmsystems and several other items can be plant

Structures, with some exceptions: dry docks andpipelines

LandStatutory inclusions

Computer software qualifies as plant by statute.

Machinery also qualifies for allowances whermachinery is given its ordinary every daymeaning.

Case law

The courts tend to allow items as plant if theyperform a function (eg moveable officepartitions) in the particular trade, rather thanform part of the setting within which the tradeis carried on.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 61/179

Allowances onplant and machinery

Whatis plant?

Specialassets

9: Capital allowanPage 53

Writing down allowances (WDAs)

18% per annum on a reducing balance basis in main pool

WDA given on pool balance after adding current periodadditions and deducting current period disposals

18% × months/12 in a period that is not 12 months long

Reduced WDAs can be claimed

Expenditure on long life assets, integral features, thermalinsulation, solar panels and cars with CO2 emissions over

130g/km goes in a special rate pool. WDA is 8% per annum

on a reducing balance basis Small balance (up to £1,000) on main pool and/or special

rate pool can be given WDA equal to balance

Deduct lower of

(i) Disposal proceeds(ii) Original cost

Main pool includes cars withCO2 emissions 130g/km or les

without private use

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 62/179

Allowances onplant and machinery

Whatis plant?

Specialassets

First year allowances (FYAs)

FYA of 100% available for expenditure

on new cars with CO2 emissions95g/km or less

Not pro-rated in short/long period ofaccount

Annual Investment Allowance (AIA)

All businesses are entitled to AIA of £500,000 per

12 month period

£500,000 maximum allowance is proportionatelyincreased/reduced if period of account is not12 months

Allocate AIA to assets eligible for lowest rate of WDA(special rate pool items before main pool items)

Transfer balance after AIA to pool for same periodWDAs

Expenditure on plant and machinery(although not cars) is entitled to the AIA.

Interaction with VAT

Expenditure exclusive of input VAT ifrecoverable

Expenditure inclusive of input VAT if notrecoverable eg car not wholly used forbusiness

Disposal proceeds exclusive of outputVAT

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 63/179

9: Capital allowanPage 55

Balancing adjustments arise

On cessation to deal withbalances remaining afterdeduction of disposal proceeds.

When a non-pooled asset issold.

When a column balancebecomes negative.

This will be a balancingcharge

Short life assets/privateuse assets

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 64/179

Allowances onplant and machinery

Whatis plant?

Specialassets

Short life assets (SLA)

An election can be made to depool assets. Depooled assets must be disposed of within

eight years of end of the period of acquisition.

From a planning point of view depooling is usefulif balancing allowances are expected.

Conversely, in general, assets should not bedepooled if they are likely to be sold within eightyears for more than their tax written down values.

Not cars

– Within two years of the endof the accounting period ofacquisition (companies)

– 31 Jan, 22 months from endof tax year (unincorporatedbusinesses)

Otherwise the balance ofexpenditure must be

transferred back to pool

Private use assets

Do not pool private use assets Show full value of asset/allowances in colum

Can only claim the business proportion ofallowances

Assets used privately by aproprietor (not an employee)so not relevant to companies

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 65/179

10: Assessable trading income

Topic List

Current year basis

Commencement

Cessation

We have seen how to calculate the taxable trading proffor a business. We now see how these profits are allocated to tax years.

This topic may be tested in Section A or in a Section B question which could be a 10 mark question or as part a 15 mark question.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 66/179

CessationCurrent yearbasis

Commencement

Current year basis

Overlap profits

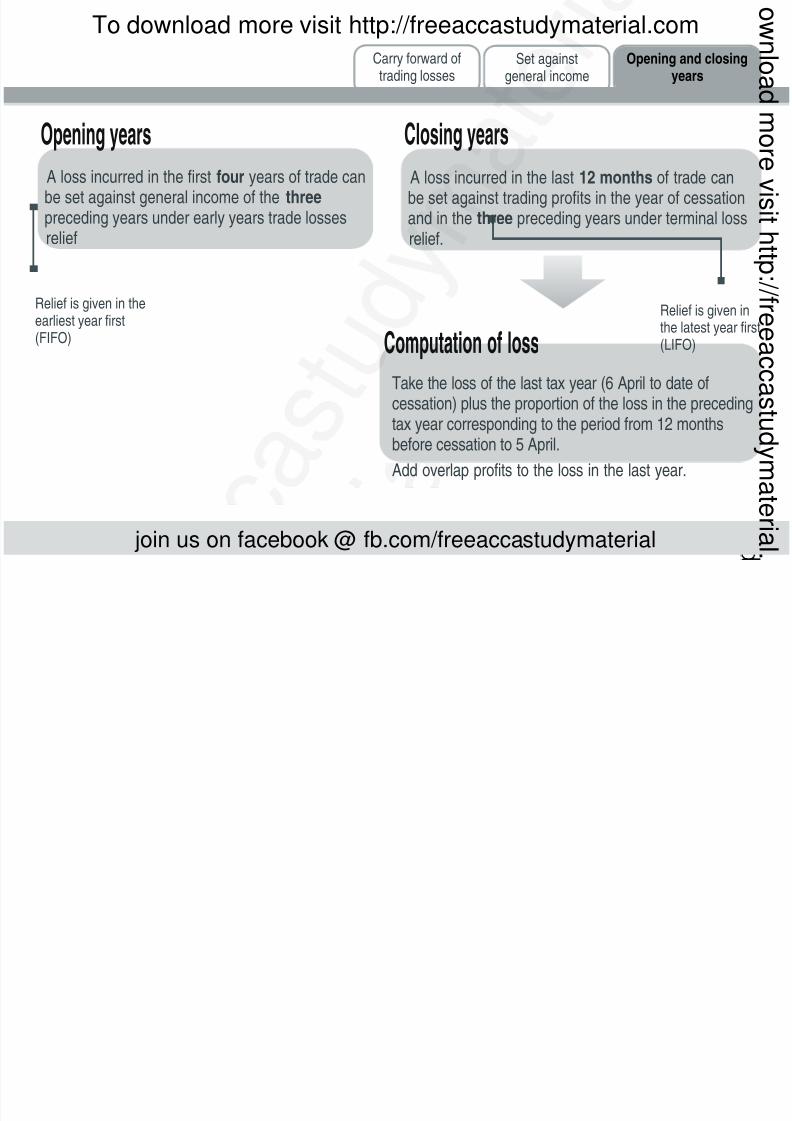

There are special rules which apply in the openand closing years of a business.

Opening years

Any profits taxed twice areoverlap profits. They may bededucted on cessation.

The basis period for a tax year is normally the

period of account ending in the year.

Tax year Basis period

1 Date of commencement to following 5 April.

2 (a) If no accounting date ends in year: 6 April – 5 April

(b) If period of account ending in year is less than

12 months: first 12 months(c) Otherwise: 12 months to accounting date ending

in Year 2

3 12 months to accounting date ending in year

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 67/179

CessationCurrent yearbasis

Commencement

10: Assessable trading incoPage 59

Final yearThe basis period for the final year starts at the end of the basis period for the previous year and ends at cessation.

Any overlap profits are deducted from the final year's profits.

ExampleBrenda has been carrying on a sole trade for many years preparing accounts to 30 April each year. She closes dowher business on 30 September 2014.The results of her final two periods of trading are:

£y/e 30 April 2014 24,000p/e 30 September 2014 5,000

Brenda had overlap profits on commencement of £10,000.

The final year is 2014/15 and the basis period for this year runs from 1 May 2013 to 30 September 2014. She candeduct the overlap profits. Her taxable trading income for 2014/15 is therefore £(24,000 + 5,000 – 10,000) = £19,00

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 68/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 69/179

11: Trading losses

Topic List

Carry forward of trading losses

Set against general income

Opening and closing years

This is another key exam topic. It is likely to be tested inSection B.

There is no general rule that sole traders can get relief for their losses.The conditions of a specific relief must complied with. We look at these reliefs in this chapter.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 70/179

Opening and closingyears

Set againstgeneral income

Carry forward oftrading losses

Carry forward trade loss relief

A loss not otherwise relieved may be set against the firstavailable profits of the same trade.

Losses must be set against the first availableprofits: they cannot be saved up until it suits

the trader to use them.

Losses may be carried forward for anynumber of years.

A loss is calculated in exactly the same way as a profit.If there is a loss in a basis period the taxable tradeprofits for the tax year are nil – instead the loss isavailable in that tax year to be used as the traderchooses.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 71/179

Opening and closingyears

Set againstgeneral income

Carry forward oftrading losses

11: Trading losPage 63

Relief against general incomeRelief is against the income of the tax year of the lossand/or the preceding tax year.

ExampleSue starts trading on 1.10.14. Her losses arey/e 30.9.15 £(50,000)

y/e 30.9.16 £(20,000)Losses for the tax years are:2014/15 £(25,000)2015/16 £(50,000 – 25,000) = £(25,002016/17 £(20,000)

Partial claims are not allowed: the whole loss must be soff, if there is income (or, if chosen, gains) to absorb it inthe chosen tax year.

Exam focusBefore recommending relief against general income, considwhether it would lead to the waste of the personal allowancThis is often a significant tax planning point.

Losses in two overlapping basis periods aregiven to the earlier tax year only.

Can extend the claim to net gains of the same year,less brought forward capital losses.

Relief against non-trading income restricted to greater o25% of adjusted total income and £50,000

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 72/179

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 73/179

12: Partnerships and limited liabilitypartnerships

Topic List

Sharing profits between partners

Losses

Partnerships are another key exam topic.You should beprepared to answer a Section B question on this topic,although it may also be tested in Section A. The technique is to allocate the profits between the partnersand then look at each partner independently.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 74/179

LossesSharing profitsbetween partners

When a partner joins, the first period of accounfor his own business runs from the date of jointo the firm's next accounting date.The normal

basis period rules for opening years apply to h

When a partner leaves, the last period of accofor his own business runs from the firm's mostrecent accounting date to the day he leaves. Thnormal cessation rules apply to him.

Remember to pro-rate the annualsalary/interest if the period is not 12 monthslong.

then

Compute trading results for a partnership as a whole in thesame way as you would compute the profits for a sole trader

Divide results for each period of account between partners

First allocate salaries and interest on capital to the partners,then share the balance of profits among the partnersaccording to the profit-sharing ratio for the period of account

Each partner is taxed as if he were running his ownbusiness, and making profits and losses equal to his shareof the firm's results for each period of account

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 75/179

LossesSharing profitsbetween partners

12: Partnerships and limited liability partnershPage 67

Consider all available loss reliefs for eachindividual partner

Next calculate the loss for each tax year

Divide the loss for each period of accountbetween the partners

Partners are entitled to the same loss reliefs assole traders:

Losses

1

2

3

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 76/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 77/179

13: National insurance contributions

Topic List

NICs for employees

NICs for the self-employed

Although often overlooked, national insurance contributions represent a significant cost to taxpayers.

National insurance contributions could be tested in Section A and also as part of a Section B question.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 78/179

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 79/179

NICs for theself-employed

NICs foremployees

13: National insurance contributiPage 71

Class 2

Class 2 are paid at a flat weekly rate. Paid by directdebit or on demand.

Class 4

Class 4 NICs are 9% of any profits falling betweena lower and an upper limit and 2% above upperlimit. Class 4 NICs are collected at the same timeas the associated income tax liability.

Exam focusIn questions which ask whether someonshould trade as a sole trader or through company (as a director) the cost of NICsoften tips the balance in favour of being sole trader.

These limits will be given to you on the exam pa

Profits are the taxable profits, as reduced by tradlosses. Personal pension contributions do notreduce profits.

The self-employed pay Class 2 and Class 4 NICs.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 80/179

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 81/179

14: Computing chargeable gains

Topic List

Chargeable persons, disposalsand assets

Basic computation

Losses

The charge to CGT for individuals

Spouses and civil partners

Part disposals

Damage, loss or destruction

It is important that you can calculate chargeable gains realised by individuals and calculate their capital gains tax liability having dealt with losses and the offset of theannual exempt amount.

You may find that the basic topics in this chapter are tested in Section A and you should also be prepared to

answer a Section B question containing a number of disposals of chargeable assets.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 82/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge toCGT for individuals

Basiccomputation

LossesChargeable persons,disposals and assets

Chargeable persons, disposals and assets

Three elements are needed for a chargeable gain to arise.

A chargeable disposal: this includes sales, gifts andthe destruction of assets. Transfer of assets on death isnot chargeable.

A chargeable person: individuals are chargeablepersons.

A chargeable asset: most assets are chargeable, butsome assets are exempt.

1

2

3

CGT applies primarily to personsresident in the UK

CarsSome chattels (eg racehorses)

GiltsQCBs

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 83/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge toCGT for individuals

Basiccomputation

LossesChargeable persons,disposals and assets

14: Computing chargeable gaPage 75

Computation

Compute a gain as follows: £Proceeds XLess: Cost (X)__Gain X__

Actual proceeds or market valuethe case of gifts and disposals whare not bargains at arms length.

Include:

(1) Original cost of the asset or marketvalue if that was used as proceeds for person who sold the asset to thisindividual.

(2) Enhancement expenditure which wasreflected in the state and nature of theasset at the time of disposal or was onpreserving the owner's legal right to thasset.

(3) Incidental costs of acquisition anddisposal.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 84/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge toCGT for individuals

Basiccomputation

LossesChargeable persons,disposals and assets

Deduct allowable capital losses from gains in the tax year in which they arise (before deducting the annualexempt amount).

Allowable losses brought forward are only set off toreduce current year gains less current year allowablelosses to the annual exempt amount.

ExampleZoë made gains of £14,000 in 2014/15. She had brough

forward capital losses of £8,000.Brought forward capital losses of £3,000 will be set off in2014/15 to preserve annual exempt amount of £11,000.The remaining losses will be carried forward to 2015/16

Any loss which cannot be set offis carried forward to set againstfuture gains.

Set off losses against gains notqualifying for entrepreneurs' relieffirst.

Order of set off

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 85/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge to CGTfor individuals

Basiccomputation

LossesChargeable persons,disposals and assets

14: Computing chargeable gaPage 77

Rates

18% – within basic rate band

Deduct the annual CGT exempt amount of £11,000 (2014/15) to compute an individual's taxable gains.

10% – entrepreneurs' relief gains 28% – above basic rate limit

taxable income andgains qualifying forentrepreneurs' relief

deducted first

remember to increaselimit by gross gift aiddonations/personal

pension contributions

from gains not qualifying forentrepreneurs' relief first

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 86/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge toCGT for individuals

Basiccomputation

LossesChargeable persons,disposals and assets

No gain/no loss disposals

When the second spouse/civil partner sells the asset, assume that he/she bought the asset for its original cos

Disposals between spouses and civil partners do not give rise to gains or losses.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 87/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge toCGT for individuals

Basiccomputation

LossesChargeable persons,disposals and assets

14: Computing chargeable gaPage 79

Part disposals

On a part disposal, you are only allowed to take

part of the cost of the asset into account. Costs attributable solely to the part disposed of

are taken into account in full

For other costs, take into account A/(A+B) ofthe cost– A is the proceeds of the part sold– B is the market value of the part retained

ExampleX owns land which originally cost £30,000. It soldquarter interest in the land for £18,000. Theincidental costs of disposal were £1,000.Themarket value of the three-quarter share remainingis estimated to be £36,000.What is the chargeabgain?

£Proceeds 18,00Less: Incidental costs of disposal (1,00____

17,00

Less: × 30,000 (10,00_____

7,00________36,00018,000

18,000

+

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 88/179

Spouses andcivil partners

Partdisposals

Damage, losor destructio

The charge toCGT for individuals

Basiccomputation

LossesChargeable persons,disposals and assets

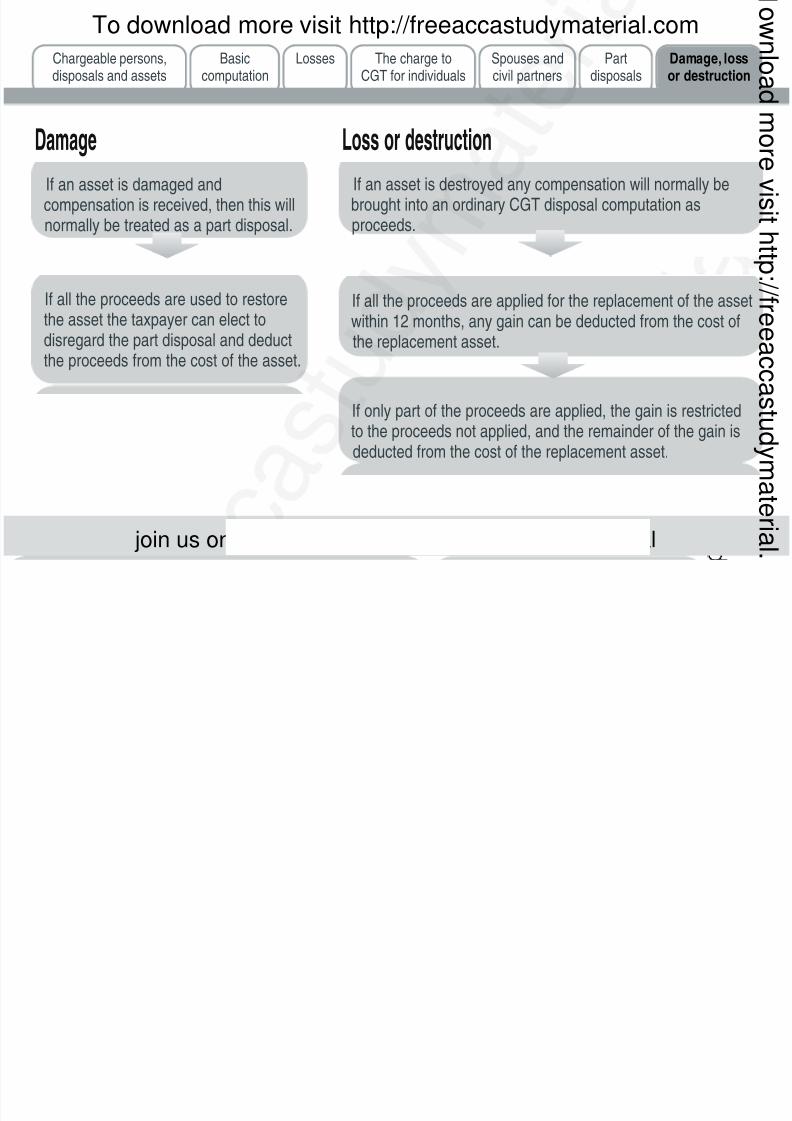

Loss or destructionDamage

If an asset is damaged andcompensation is received, then this willnormally be treated as a part disposal.

If an asset is destroyed any compensation will normally bebrought into an ordinary CGT disposal computation asproceeds.

If all the proceeds are applied for the replacement of the asswithin 12 months, any gain can be deducted from the cost ofthe replacement asset.

If all the proceeds are used to restorethe asset the taxpayer can elect todisregard the part disposal and deductthe proceeds from the cost of the asset.

If only part of the proceeds are applied, the gain is restrictedto the proceeds not applied, and the remainder of the gain isdeducted from the cost of the replacement asset.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 89/179

15: Chattels and the principal private residencexemption

Topic List

Chattels

Wasting assets

Private residences

In this chapter we look at the rules which apply for calculating the gains on certain special types of asset.

The chattel rules may well be tested in Section A.The rules on private residences could form part of a SectionB question.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 90/179

Chattels

Privateresidences

Wastingassets

Chattels

A chattel is an item of tangible moveable property

(eg a painting).

Wasting chattels

Gains on chattels sold for gross proceeds of £6,000 orless are exempt.

The maximum gain on chattels sold for more than£6,000 is 5/3 (gross proceeds – £6,000).

Losses on chattels sold for under £6,000 are restrictedby assuming the gross proceeds to be £6,000.

Chattels with a remaining estimated useful of 50 years or less.

Wasting chattels are exempt from CGTunless capital allowances could have beeclaimed on them.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 91/179

15: Chattels and the principal private residence exempPage 83

Privateresidences

Wastingassets

Chattels

Exception

A wasting asset is one with an estimated remaining useful life of

50 years or less and whose original value will fall over time.

Wasting assets have their cost written downover time on a straight line basis.

ExampleJo bought a copyright with a remaining life of 40 yearsfor £10,000. He sold the copyright 15 years later for£30,000. Calculate the gain arising.

£Proceeds 30,000Less: Cost (£10,000 × 25/40) (6,250)______Gain 23,750____________

Number of years remaining

Number of years on acquisition

Wasting asset

Assets eligible for capital allowancesand used in a trade do not have theircost written down.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 92/179

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 93/179

15: Chattels and the principal private residence exempPage 85

A gain arising whilst a PPR is let is exempt up tothe lower of:

£40,000

The amount of the PPR exemption

The gain in the let period

The private residence exemption covers house plus up to half a hectare of groundA larger area may be allowed for

substantial houses.12

3

Letting exemption Permitted area

When part of residence is used exclusively for business purposes, that part of gain istaxable. Last 18 months exemption does not apply.

Business use

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 94/179

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 95/179

16: Business reliefs

Topic List

Entrepreneurs' relief

Rollover relief

Gift relief

In a Section B exam question you should look out for thavailability of various reliefs. However, do take care to ensure that you do not claim relief when you are not allowed to.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 96/179

Entrepreneurs'relief

Giftrelief

Rolloverrelief

Sole trader business/partnership

Shares in 'personal' trading company owned byemployee/officer

Business assets

Available for material disposal of

business assets

Business owned for one year prior todisposal or business has ceased withinpast three years and business owned atleast one year prior to cessation

Entrepreneurs' relief

Tax net gains at 10%

Lifetime limit of £10m gains

Claim by 12 months from 31 January following tax year of disposal

'Personal' trading companyrequiresshareholding/voting rights

of at least 5%

Must be the disposal othe whole or part of the

business, not justindividual assets ifbusiness continues

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 97/179

Entrepreneurs'relief

Giftrelief

Rolloverrelief

16: Business rePage 89

Taxpayers can claim to defer gains arisingon the disposal of business assets that arebeing replaced if both the old and the new

assets are on the list of eligible assets.

The new asset must be bought in theperiod starting 12 months before andending 36 months after the disposal.

Exam focusIf a question mentions the sale of somebusiness assets and the purchase of

others, look out for rollover relief but do notjust assume that it is available: the assetsmight be of the wrong type, eg moveableplant and machinery.

Is the new asset a depreciating asset?

Is the new asset a non-depreciating asset?

A depreciating asset is one withexpected life of 60 years or less(eg fixed plant and machinery).

Land and buildings (including parts of buildings) occuas well as used only for the purposes of the trade.

Fixed (that is, immovable) plant and machinery.

Goodwill

Eligible assets

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 98/179

Entrepreneurs'relief

Giftrelief

Rolloverrelief

For a non-depreciating asset the gain is deductedfrom the base cost of the new asset.

For a depreciating asset the gain is deferred until itcrystallises at a later date.

Relief is proportionately restricted when an ashas not been used for trade purposes throughits life.

If a part of the proceeds of the old asset are notreinvested, the gain is chargeable up to the amou

not reinvested.

If a non-depreciating qualifying asset is boughtbefore the gain crystallises, the deferred gain mbe rolled into the base cost of that asset.

The gain crystallises on the earliest of:

the disposal of the replacement asset

ten years after the acquisition of the

replacement asset

the date the replacement asset ceases to beused in the trade

1

2

3

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 99/179

Entrepreneurs'relief

Giftrelief

Rolloverrelief

16: Business rePage 91

The gain is deducted from the recipient's basecost.

Gift relief may be claimed to defer gains arising onbusiness assets. Assets used in a trade

Shares and securities in tradingcompany which is either unlistedor the donor's personal company

Qualifying assetsGift relief

Any actual proceeds in excess of cost reduce the

gain for which relief can be claimed.

If balance sheet of companycontains non business assets gain

eligible restricted to CBA/CA × gain

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 100/179

Notes

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 101/179

17: Shares and securities

Topic List

Matching

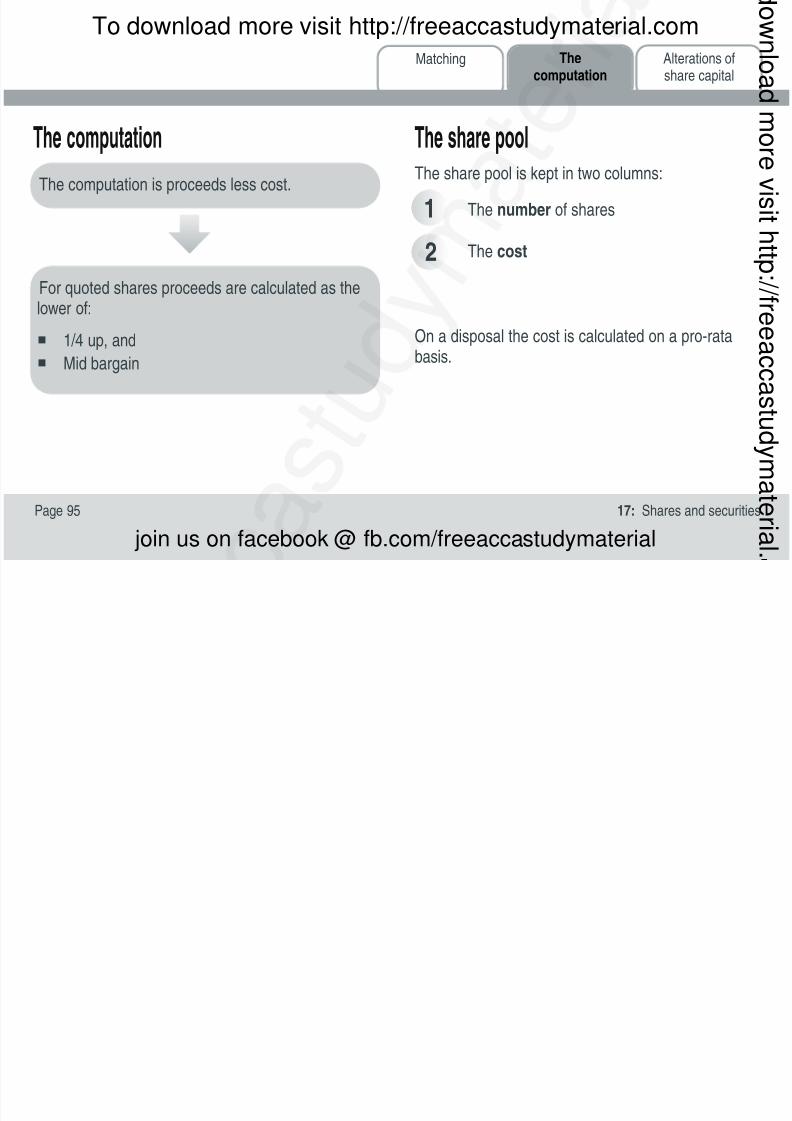

The computation

Alterations of share capital

The matching rules for shares and securities are vitally important, in particular in a Section B question. If you dnot know the matching rules you will not be able to compute a gain on the disposal of shares.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf

http://slidepdf.com/reader/full/f6-passcardpdf 102/179

Matching rules for individuals

Alterations ofshare capital

Thecomputation

Matching

The matching rules for shares held by an individual are different to the matching rules for shares held by acompany. Take care not to confuse the two.

Disposals by individual shareholders are matched withacquisitions in the following order:

Same day acquisitions

Acquisitions within the following 30 days

Any shares in the share pool

Exam focusLearn the 'matching rules' because a crucifirst step to getting a shares question right to correctly match the shares sold to theoriginal shares purchased.

To download more visit http://freeaccastudymaterial.com

join us on facebook @ fb.com/freeaccastudymaterial

8/17/2019 f6 passcard.pdf