in the united states district court for the northern district of texas

TRANSCRIPT

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 1

IN THE UNITED STATES DISTRICT COURTFOR THE NORTHERN DISTRICT OF TEXAS

DALLAS DIVISION

RALPH S. JANVEY, IN HIS CAPACITY AS COURT-APPOINTED RECEIVER FOR THE STANFORD INTERNATIONAL BANK, LTD., ET AL.

Plaintiff,

v.

JAMES R. ALGUIRE, ET AL.

Relief Defendants.

§§§§§§§§§§§§

Case No. 03:09-CV-0724-N

________________________________________________________________________

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS

________________________________________________________________________

The Receiver, Ralph S. Janvey, (the “Receiver”) hereby files his First Amended

Complaint Against Certain Stanford Investors (the “First Amended Complaint”), stating as

follows:

SUMMARY

1. The ultimate purpose of this Receivership is to make the “maximum disbursement

to claimants.” This requires the Receiver to maximize the pool of assets that will be available for

distribution. To accomplish this, the Receiver must take control of all assets of the Estate and

traceable to the Estate, “wherever located,” including money stolen from investors through fraud.

2. The Receiver’s investigation to date reveals that CD sales generated substantially

all of the income for the Stanford Defendants and the many related Stanford entities. Revenue,

let alone any profit, from all other activities and investments was miniscule in comparison.

Money that new investors were deceived into paying to purchase CDs funded the Stanford

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 1 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 2

network; lavish offices and appointments; extravagant lifestyles for the individual defendants

and their families; employees’ salaries; Loans, SIBL CD commissions, SIBL Quarterly Bonuses,

Performance Appreciation Rights Plan (“PARS”) Payments, Branch Managing Director

Quarterly Compensation, and Severance Payments to financial advisors, managing directors, and

other Stanford employees; and CD proceeds in the form of purported CD interest payments and

redemptions (“CD Proceeds”) to the investors named in the concurrently filed Appendix (the

“Stanford Investors”).

3. The Stanford Investors not only received from SIBL sums equal to their

investments in SIBL CDs, but they also received payments in excess of their respective

investments.1 The CD Proceeds the Stanford Investors received from SIBL were not, in fact,

their actual principal or interest earned on the funds they invested. Instead, the money used to

make those payments came directly from the sale of SIBL CDs to other investors.

4. When Stanford made purported CD principal and interest payments to the

Stanford Investors, he did no more than take money out of other investors’ pockets and put it into

the hands of the Stanford Investors. For the more than 20,000 investors who have thus far

received little or nothing from their investment in Stanford CDs, money recovered from

wherever it resides today is likely the largest portion of the money they will ever receive in

restitution. CD Proceeds — comprising purported CD principal and interest payments to the

Stanford Investors — are little more than stolen money and do not belong to the Stanford

Investors who received such funds but belong, instead, to the Receivership Estate.

1 Prior to filing this First Amended Complaint, the Receiver contacted all of the Stanford Investors named herein for whom he had contact information and offered to settle the claims against them in exchange for payment of the amounts they received in excess of their investments in SIBL CDs. The Receiver made similar offers to other investors, who accepted the Receiver’s proposal prior to the filing of this First Amended Complaint. The Receiver believes that continued discussions with many of the Stanford Investors named herein will result in additional such settlements and dismissal of claims against those investors.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 2 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 3

5. At this stage of the Receivership, the Receiver has identified substantial sums of

CD Proceeds paid to the Stanford Investors and, through this First Amended Complaint, seeks

the return of those funds to the Receivership Estate in order to make an equitable distribution to

claimants. At a minimum, the Stanford Investors named in the Appendix received over

$545 million in CD Proceeds.

6. The Receiver seeks an order that: (a) CD Proceeds received directly or indirectly

by the Stanford Investors from fraudulent CDs were fraudulent conveyances or, in the

alternative, unjustly enriched the Stanford Investors; (b) CD Proceeds received directly or

indirectly by the Stanford Investors from fraudulent CDs are property of the Receivership Estate

held pursuant to a constructive trust for the benefit of the Receivership Estate; (c) each of the

Stanford Investors is liable to the Receivership Estate for an amount equaling the CD Proceeds

he, she, or it received; and (d) awards attorney’s fees and costs to the Receiver.

PARTIES

7. The parties to this complaint are the Receiver and the Stanford Investors named in

the Appendix filed concurrently herewith.

8. The named Stanford Investors either have already been served or will be served

pursuant to the Federal Rules of Civil Procedure, through their attorneys of record, or by other

means approved by order of this Court.

PROCEDURAL HISTORY

9. On July 28, 2009, the Receiver filed an Amended Complaint Naming Relief

Defendants (Doc. 14) and an Appendix in support thereof (Doc. 15). The July 28th Amended

Complaint named both investors and certain former Stanford financial advisors as relief

defendants. The Receiver now respectfully files this First Amended Complaint Against Certain

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 3 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 4

Stanford Investors, amending herein his claims against certain Stanford investors and naming

additional investors as defendants. The Receiver files this First Amended Complaint as a result

of the Fifth Circuit’s recent ruling regarding the Receiver’s relief-defendant claims,2 and he

amends his claims against the certain Stanford investors named herein to assert fraudulent-

transfer claims and, in the alternative, unjust-enrichment claims. This complaint is not intended

to impact the claims asserted by the Receiver in this lawsuit against any category of defendants

other than Stanford investors. This First Amended Complaint Against Certain Stanford Investors

does not alter or amend the claims the Receiver asserted against former Stanford employees in

his First Amended Complaint Against Former Stanford Employees (Doc. 118) and the Appendix

thereto (Doc. 119).

JURISDICTION & VENUE

10. This Court has jurisdiction over this action, and venue is proper, under Section

22(a) of the Securities Act (15 U.S.C. § 77v(a)), Section 27 of the Exchange Act (15 U.S.C.

§ 78aa), and under Chapter 49 of Title 28, Judiciary and Judicial Procedure (28 U.S.C. § 754).

11. Further, as the Court that appointed the Receiver, this Court has jurisdiction over

any claim brought by the Receiver to execute his Receivership duties.

12. Further, within 10 days of his appointment, the Receiver filed the original

Complaint and Order Appointing the Receiver in 29 United States district courts pursuant to 28

U.S.C. § 754, giving this Court in rem and in personam jurisdiction in each district where the

Complaint and Order have been filed.

13. Further, each of the Stanford Investors who submitted an Application for Review

and Potential Release of Stanford Group Company (“SGC”) Brokerage Accounts made the

2 Per Rule 41, the Receiver intends to file a notice of dismissal of his relief-defendant claims against the Stanford investors who were named in the Amended Complaint Naming Relief Defendants (Doc. 14) and the supporting Appendix (Doc. 15).

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 4 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 5

following declaration: “By filing this application, I submit to the exclusive jurisdiction of the

United States District Court for the Northern District of Texas, Dallas Division and irrevocably

waive any right I or any entity I control may otherwise have to object to any action being brought

in the Court or to claim that the Court does not have jurisdiction over the matters relating to my

account.”

14. Further, a number of the Stanford Investors have filed motions to intervene in

SEC v. Stanford International Bank, Ltd., et al., Case No. 3:09-cv-298-N. By filing motions to

intervene, they have consented as a matter of law to the Court’s personal jurisdiction. See In re

Bayshore Ford Trucks Sales, Inc., 471 F.3d 1233, 1246 (11th Cir. 2006); County Sec. Agency v.

Ohio Dep’t of Commerce, 296 F.3d 477, 483 (6th Cir. 2002); Pharm. Research & Mfrs. v.

Thompson, 259 F. Supp. 2d 39, 59 (D.D.C. 2003); City of Santa Clara v. Kleppe, 428 F. Supp.

315, 317 (N.D. Ca. 1976).

STATEMENT OF FACTS

15. On February 16, 2009, the Securities and Exchange Commission commenced a

lawsuit in this Court against R. Allen Stanford, two associates, James M. Davis and Laura

Pendergest-Holt, and three of Mr. Stanford’s companies, Stanford International Bank, Ltd.

(“SIB,” “SIBL,” or “the Bank”), SGC, and Stanford Capital Management, LLC (collectively, the

“Stanford Defendants”). On the same date, the Court entered an Order appointing a Receiver,

Ralph S. Janvey, over all property, assets, and records of the Stanford Defendants, and all entities

they own or control.

16. As alleged by the SEC, the Stanford Defendants marketed fraudulent SIBL CDs

to investors exclusively through SGC financial advisors pursuant to a Regulation D private

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 5 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 6

placement. SEC’s First Amended Complaint (Doc. 48), ¶ 23.3 The CDs were sold by Stanford

International Bank, Ltd. Id.

17. The Stanford Defendants orchestrated and operated a wide-ranging Ponzi scheme.

Defendant James M. Davis has admitted that the Stanford fraud was a Ponzi scheme from the

beginning. Doc. 771 (Davis Plea Agreement) at ¶ 17(n) (Stanford, Davis, and other conspirators

created a “massive Ponzi scheme”); Doc. 807 (Davis Tr. of Rearraignment) at 16:16-17, 21:6-8,

21:15-17 (admitting the Stanford Ponzi fraud was a “massive Ponzi scheme ab initio”).

18. In marketing, selling, and issuing CDs to investors, the Stanford Defendants

repeatedly touted the CDs’ safety and security and SIBL’s consistent, double-digit returns on its

investment portfolio. Id. ¶ 31.

19. In its brochure, SIBL told investors, under the heading “Depositor Security,” that

its investment philosophy is “anchored in time-proven conservative criteria, promoting stability

in [the Bank’s] certificate of deposit.” SIBL also emphasized that its “prudent approach and

methodology translate into deposit security for our customers.” Id. ¶ 32. Further, SIBL stressed

the importance of investing in “marketable” securities, saying that “maintaining the highest

degree of liquidity” was a “protective factor for our depositors.” Id. ¶ 45.

20. In its 2006 and 2007 Annual Reports, SIBL told investors that the Bank’s assets

were invested in a “well-balanced global portfolio of marketable financial instruments, namely

U.S. and international securities and fiduciary placements.” Id. ¶ 44. More specifically, SIBL

represented that its 2007 portfolio allocation was 58.6% equity, 18.6% fixed income, 7.2%

precious metals, and 15.6% alternative investments. Id.

3 Unless otherwise stated, citations to Court records herein are from the case styled SEC v. Stanford Int’l Bank, Ltd., et al., Civil Action No. 3-09-CV-0298-N.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 6 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 7

21. Consistent with its Annual Reports and brochures, SIBL trained SGC financial

advisors, in February 2008, that “liquidity/marketability of SIB’s invested assets” was the “most

important factor to provide security to SIB clients.” Id. ¶ 46. In training materials, the Stanford

Defendants also claimed that SIBL had earned consistently high returns on its investment of

deposits (ranging from 11.5% in 2005 to 16.5% in 1993). Id. ¶ 24.

22. Contrary to the Stanford Defendants’ representations regarding the liquidity of its

portfolio, SIBL did not invest in a “well-diversified portfolio of highly marketable securities.”

Instead, significant portions of the Bank’s portfolio were misappropriated by Defendant Allen

Stanford and were either placed in speculative investments (many of them illiquid, such as

private equity deals), diverted to other Stanford Entities “on behalf of shareholder” - i.e., for the

benefit of Allen Stanford, or used to finance Allen Stanford’s lavish lifestyle (e.g., jet planes, a

yacht, other pleasure craft, luxury cars, homes, travel, company credit card, etc.). In fact, at

year-end 2008, the largest segments of the Bank’s portfolio were: (i) at least $1.6 billion in

undocumented “loans” to Defendant Allen Stanford; (ii) private equity; and (iii) over-valued real

estate. Id. ¶¶ 24, 48.

23. In an effort to conceal their fraud and ensure that investors continued to purchase

the CD, the Stanford Defendants fabricated the performance of SIBL’s investment portfolio. Id.

¶ 5.

24. SIBL’s financial statements, including its investment income, were fictional. Id.

¶ 37. In calculating SIBL’s investment income, Defendants Stanford and James Davis provided

to SIBL’s internal accountants a pre-determined return on investment for the Bank’s portfolio.

Id. Using this pre-determined number, SIBL’s accountants reverse-engineered the Bank’s

financial statements to reflect investment income that SIBL did not actually earn. Id.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 7 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 8

25. CD Proceeds from the Ponzi scheme were transferred by the Stanford Defendants

to the Stanford Investors solely for the purpose of concealing and perpetuating the fraudulent

scheme. Such CD Proceeds were paid to the Stanford Investors from funds supplied by other

investors who bought the fraudulent CDs.

26. For a time, the Stanford Defendants were able to keep the fraud going by using

funds from current sales of SIBL CDs to make purported interest and redemption payments on

pre-existing CDs. See id. ¶ 1. However, in late 2008 and early 2009, CD redemptions increased

to the point that new CD sales were inadequate to cover redemptions and normal operating

expenses. As the depletion of liquid assets accelerated, this fraudulent Ponzi scheme collapsed.

REQUESTED RELIEF

27. This Court appointed Ralph S. Janvey as Receiver for the “assets, monies,

securities, properties, real and personal, tangible and intangible, of whatever kind and

description, wherever located, and the legally recognized privileges (with regard to the entities),

of the Defendants and all entities they own or control,” including those of the Stanford Group

Company brokerage firm. Order Appointing Receiver (Doc. 10) at ¶¶ 1-2; Amended Order

Appointing Receiver (Doc. 157) at ¶¶ 1-2. The Receiver seeks the relief described below in this

capacity.

28. Paragraph 4 of the Order Appointing Receiver, entered by the Court on February

16, 2009, authorizes the Receiver “to immediately take and have complete and exclusive control,

possession, and custody of the Receivership Estate and to any assets traceable to assets owned by

the Receivership Estate.” Order Appointing Receiver (Doc. 10) at ¶ 4; Amended Order

Appointing Receiver (Doc. 157) at ¶ 4. Paragraph 5(c) of the Order specifically authorizes the

Receiver to “[i]nstitute such actions or proceedings [in this Court] to impose a constructive trust,

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 8 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 9

obtain possession, and/or recover judgment with respect to persons or entities who received

assets or records traceable to the Receivership Estate.” Order Appointing Receiver (Doc. 10) at

¶ 5(c); Amended Order Appointing Receiver (Doc. 157) at ¶ 5(c).

29. One of the Receiver’s key duties is to maximize distributions to defrauded

investors and other claimants. See Amended Order Appointing Receiver (Doc. 157) at ¶ 5(g), (j)

(ordering the Receiver to “[p]reserve the Receivership Estate and minimize expenses in

furtherance of maximum and timely disbursement thereof to claimants”); Scholes v. Lehmann, 56

F.3d 750, 755 (7th Cir. 1995) (receiver’s “only object is to maximize the value of the [estate

assets] for the benefit of their investors and any creditors”); SEC v. TLC Invs. & Trade Co., 147

F. Supp. 2d 1031, 1042 (C.D. Cal. 2001); SEC v. Kings Real Estate Inv. Trust, 222 F.R.D. 660,

669 (D. Kan. 2004). But before the Receiver can attempt to make victims whole, he must locate

and take exclusive control and possession of assets of the Estate or assets traceable to the Estate.

Doc. 157 ¶ 5(b).

30. The Stanford Investors named in the Appendix received money that they may

have believed was a return on an investment placed with what they thought was a legitimate

bank. In reality, the money the Stanford Investors received was not their money, was not a

return on their investments, and was not generated by any of SIBL’s other business ventures.

The CD Proceeds were simply money that came from the more than 20,000 CD holders who

were deceived into purchasing CDs and who by chance, or as the result of sales tactics by

Stanford financial advisors and other employees, had not withdrawn funds from SIBL as of the

date the Receivership was put in place. The Stanford Investors’ CD Proceeds must be returned

to the Receivership Estate to compensate victims of the Stanford fraud according to principles of

law and equity.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 9 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 10

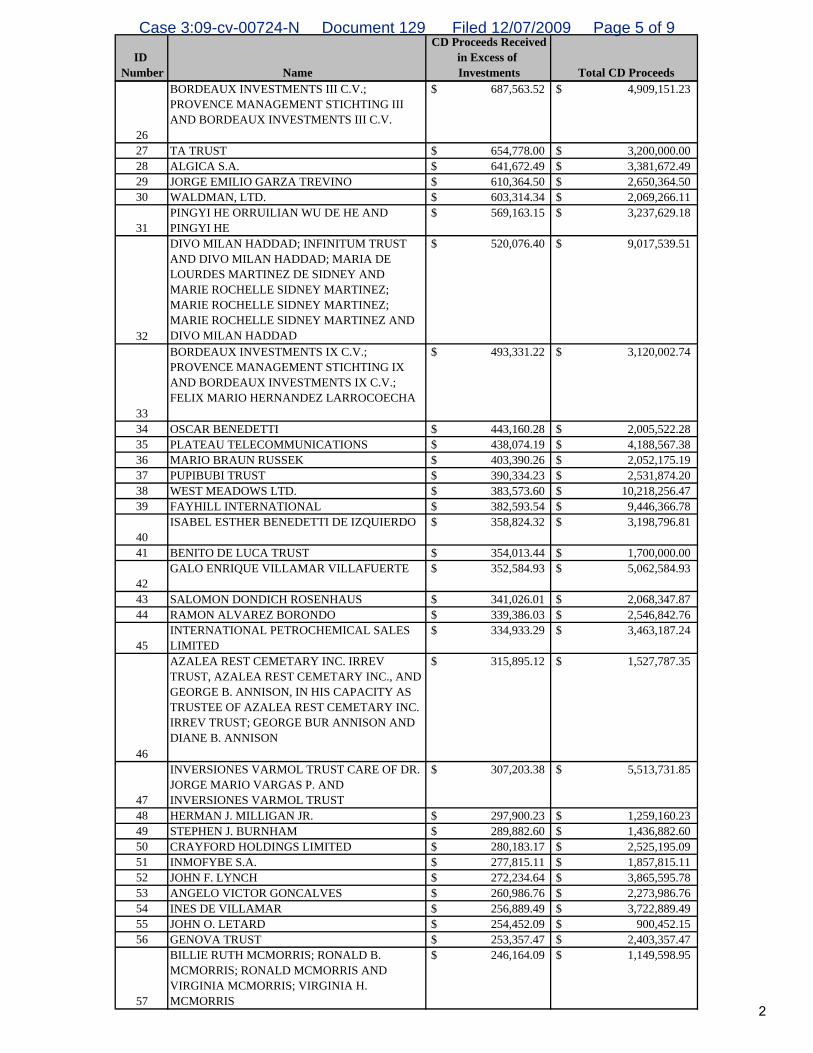

31. The Stanford Investors received CD Proceeds ranging in amounts from

approximately $119,000 to over $90 million. See App. at “Total CD Proceeds” column. These

Stanford Investors received, at a minimum, the “Total CD Proceeds” amounts associated with

their names in the Appendix. See id. Collectively, the Stanford Investors received more than

$545 million in CD Proceeds, at least. See id. at 6. In addition, each of these Stanford Investors

received more in CD Proceeds than they invested in SIBL CDs. See id. at “CD Proceeds

Received in Excess of Investments” column. All combined, these Stanford Investors received

approximately $93.8 million more in CD Proceeds than they invested. See id at 6.

I. The Receiver is Entitled to Disgorgement of CD Proceeds Fraudulently Transferred to the Stanford Investors

32. The Receiver is entitled to disgorgement of all CD Proceeds paid to the Stanford

Investors because such payments constitute fraudulent transfers under applicable law. The

Stanford Defendants transferred the CD Proceeds to the Stanford Investors with actual intent to

hinder, delay, or defraud their creditors; as a result, the Receiver is entitled to the disgorgement

of those CD Proceeds from the Stanford Investors.

33. The Receiver may avoid transfers made with the actual intent to hinder, delay, or

defraud creditors. “[T]ransfers made from a Ponzi scheme are presumptively made with intent to

defraud, because a Ponzi scheme is, as a matter of law, insolvent from inception.” Quilling v.

Schonsky, No. 07-10093, 2007 WL 2710703, at *2 (5th Cir. Sept. 18, 2007); see also Warfield v.

Byron, 436 F.3d 551, 558 (5th Cir. 2006). The uncontroverted facts establish that the Stanford

Defendants were running a Ponzi scheme and, to keep the scheme going, paid the Stanford

Investors with CD Proceeds taken from other SIBL CD investors. The Receiver is, therefore,

entitled to disgorgement of the fraudulently transferred CD Proceeds that the Stanford Investors

received.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 10 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 11

34. Consequently, the burden is on the Stanford Investors to establish an affirmative

defense, if any, of both objective good faith and provision of reasonably equivalent value. See,

e.g., Scholes, 56 F.3d at 756-57 (“If the plaintiff proves fraudulent intent, the burden is on the

defendant to show that the fraud was harmless because the debtor’s assets were not depleted

even slightly.”). The Receiver is, therefore, entitled to recover the full amount of CD Proceeds

that the Stanford Investors received, unless the Stanford Investors prove both objective good

faith and reasonably equivalent value.

35. The good-faith element of this affirmative defense requires that the Stanford

Investors prove objective — not subjective — good faith. Warfield v. Byron, 436 F.3d 551,

559-560 (5th Cir. 2006) (good faith is determined under an “objectively knew or should have

known” standard); In re IFS Fin. Corp., Bankr. No. 02-39553, 2009 WL 2986928, at *15

(Bankr. S.D. Tex. Sept. 9, 2009) (objective standard is applied to determine good faith); Quilling

v. Stark, No. 3-05-CV-1976-BD, 2007 WL 415351, at *3 (N.D. Tex. Feb. 7, 2007) (good faith

“must be analyzed under an objective, rather than a subjective, standard. The relevant inquiry is

what the transferee objectively knew or should have known instead of examining the transferee’s

actual knowledge from a subjective standpoint.”) (internal citations and quotation marks

omitted). In addition, the case law is uniformly clear that reasonably equivalent value can never

be proven as to amounts received in excess of investments. See Donell v. Kowell, 533 F.3d 762,

776 (9th Cir. 2008) (“We are aware that it may create a significant hardship when an innocent

investor such as Kowell is informed that he must disgorge profits he earned innocently, often

years after the money has been received and spent. Nevertheless, courts have long held that is

more equitable to attempt to distribute all recoverable assets among the defrauded investors who

did not recover their initial investments rather than to allow the losses to rest where they fell.”);

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 11 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 12

see also Scholes v. Lehmann, 56 F.3d 750, 757-58 (7th Cir. 1995) (“He should not be permitted

to benefit from a fraud at their expense merely because he was not himself to blame for the

fraud. All he is being asked to do is to return the net profits of his investment-the difference

between what he put in at the beginning and what he had at the end.”).

36. Moreover, under applicable fraudulent transfer law, the Receiver is entitled to

attorney’s fees and costs for his claims against the Stanford Investors. See, e.g., TEX. BUS. &

COM. CODE ANN. § 24.013 (Vernon 2009) (“[T]he court may award costs and reasonable

attorney’s fees as are equitable and just.”). As a result, the Receiver requests reasonable

attorney’s fees and costs for prosecuting his fraudulent-transfer claims against the Stanford

Investors.

37. In order to carry out the duties delegated to him by this Court, the Receiver seeks

complete and exclusive control, possession, and custody of all CD Proceeds received by the

Stanford Investors.

38. The Stanford Defendants, who orchestrated the Ponzi scheme, transferred the CD

Proceeds to the Stanford Investors with actual intent to hinder, delay, or defraud their creditors.

The Receiver is, therefore, entitled to disgorgement of all CD Proceeds fraudulently transferred

to the Stanford Investors. Pursuant to the equity powers of this Court, the Receiver therefore

seeks an order (a) establishing that the CD Proceeds received directly or indirectly by the

Stanford Investors from fraudulent CDs were fraudulent conveyances; (b) ordering that CD

Proceeds received directly or indirectly by the Stanford Investors from fraudulent CDs are

property of the Receivership Estate held pursuant to a constructive trust for the benefit of the

Receivership Estate; (c) ordering that each of the Stanford Investors is liable to the Receivership

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 12 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 13

Estate for an amount equaling the amount of CD Proceeds he, she, or it received; and (d)

awarding attorney’s fees and costs to the Receiver.

II. In the Alternative, the Receiver is Entitled to Disgorgement of CD Proceeds from the Stanford Investors under the Doctrine of Unjust Enrichment

39. In the alternative, the Receiver is entitled to disgorgement of the CD Proceeds

paid to the Stanford Investors pursuant to the doctrine of unjust enrichment under applicable law.

The Stanford Investors hold CD Proceeds they obtained as a result of taking undue advantage,

and such CD Proceeds in equity and good conscience belong to the Receivership for ultimate

distribution to the defrauded investors.

40. The Stanford Investors listed in the Appendix not only received a full return on

their CD investments, but they also received CD Proceeds in excess of those investments. The

Stanford Investors received a 100% return on their investments in an economy where — if they

had invested in the market rather than a Ponzi scheme — they would have recovered barely 60%

of their market investments.4 The market losses these Stanford Investors avoided by investing in

the Stanford Ponzi scheme have come at the expense of the thousands of other investors whose

own CD investments subsidized both the Stanford Investors’ return of invested funds and money

received in excess of those investments.

41. In order to carry out the duties delegated to him by this Court, the Receiver seeks

complete and exclusive control, possession, and custody of all CD Proceeds received by the

Stanford Investors.

42. The Stanford Investors have been unjustly enriched by their receipt of CD

Proceeds. Pursuant to the equity powers of this Court, the Receiver therefore seeks an order (a)

establishing that each of the Stanford Investors were unjustly enriched by CD Proceeds received 4 Between January 2008 and January 2009, the S&P 500 and the Dow Jones Industrial Average fell 39.3% and 33.6%, respectively.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 13 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 14

directly or indirectly from fraudulent CDs; (b) ordering that CD Proceeds received directly or

indirectly by the Stanford Investors from fraudulent CDs are property of the Receivership Estate

held pursuant to a constructive trust for the benefit of the Receivership Estate; and (c) ordering

that each of the Stanford Investors is liable to the Receivership Estate for an amount equaling the

amount of CD Proceeds he, she, or it received; and (d) awarding attorney’s fees and costs to the

Receiver.

PRAYER

43. The Receiver respectfully requests the following:

(a) An Order providing that CD Proceeds received directly or indirectly by the

Stanford Investors from fraudulent CDs were fraudulent conveyances under

applicable law or, in the alternative, that the Stanford Investors were unjustly

enriched by CD Proceeds received directly or indirectly from fraudulent

CDs;

(b) An Order providing that CD Proceeds received directly or indirectly by the

Stanford Investors from fraudulent CDs are property of the Receivership

Estate;

(c) An Order providing that CD Proceeds received directly or indirectly by the

Stanford Investors from fraudulent CDs are subject to a constructive trust for

the benefit of the Receivership Estate;

(d) An Order establishing the amount of CD Proceeds each of the Stanford

Investors received;

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 14 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 15

(e) An Order providing that each of the Stanford Investors is liable to the

Receivership Estate for an amount equaling the amount of CD Proceeds he,

she, or it received from fraudulent CDs;

(f) An award of costs, attorney’s fees, and prejudgment interest; and

(g) Such other and further relief as the Court deems proper under the

circumstances.

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 15 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 16

Dated: December 7, 2009 Respectfully submitted,

BAKER BOTTS L.L.P.By: /s/ Kevin M. Sadler

Kevin M. SadlerTexas Bar No. [email protected] I. HowellTexas Bar No. [email protected] T. ArlingtonTexas Bar No. [email protected] San Jacinto Center98 San Jacinto Blvd.Austin, Texas 78701-4039(512) 322-2500(512) 322-2501 (Facsimile)

Timothy S. DurstTexas Bar No. [email protected] Ross AvenueDallas, Texas 75201(214) 953-6500(214) 953-6503 (Facsimile)

ATTORNEYS FOR RECEIVER RALPH S. JANVEY

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 16 of 17

RECEIVER’S FIRST AMENDED COMPLAINTAGAINST CERTAIN STANFORD INVESTORS 17

CERTIFICATE OF SERVICE

On December 7, 2009, I electronically submitted the foregoing document with the clerk of the court of the U.S. District Court, Northern District of Texas, using the electronic case filing system of the Court. I hereby certify that I will serve the Stanford Investors individually or through their counsel of record, electronically, or by other means authorized by the Court or the Federal Rules of Civil Procedure.

/s/ Kevin M. SadlerKevin M. Sadler

Case 3:09-cv-00724-N Document 128 Filed 12/07/2009 Page 17 of 17

APPENDIX IN SUPPORT OF RECEIVER’S FIRST AMENDED COMPLAINT AGAINST CERTAIN STANFORD INVESTORS

IN THE UNITED STATES DISTRICT COURT FOR THE NORTHERN DISTRICT OF TEXAS

DALLAS DIVISION

RALPH S. JANVEY, IN HIS CAPACITY AS COURT-APPOINTED RECEIVER FOR THE STANFORD INTERNATIONAL BANK, LTD., ET AL. Plaintiff, v. JAMES R. ALGUIRE, ET AL. Relief Defendants.

§ § § § § § § § § § § §

Case No. 03:09-CV-0724-N

__________________________________________________________________________

APPENDIX IN SUPPORT OF RECEIVER’S FIRST AMENDED COMPLAINT AGAINST CERTAIN STANFORD INVESTORS

__________________________________________________________________________

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 1 of 9

APPENDIX IN SUPPORT OF RECEIVER’S FIRST AMENDED COMPLAINT AGAINST CERTAIN STANFORD INVESTORS

Dated: December 7, 2009 Respectfully submitted,

BAKER BOTTS L.L.P. By: /s/ Kevin M. Sadler

Kevin M. Sadler Texas Bar No. 17512450 [email protected] Robert I. Howell Texas Bar No. 10107300 [email protected] David T. Arlington Texas Bar No. 00790238 [email protected] 1500 San Jacinto Center 98 San Jacinto Blvd. Austin, Texas 78701-4039 (512) 322-2500 (512) 322-2501 (Facsimile) Timothy S. Durst Texas Bar No. 00786924 [email protected] 2001 Ross Avenue Dallas, Texas 75201 (214) 953-6500 (214) 953-6503 (Facsimile)

ATTORNEYS FOR RECEIVER RALPH S. JANVEY

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 2 of 9

APPENDIX IN SUPPORT OF RECEIVER’S FIRST AMENDED COMPLAINT AGAINST CERTAIN STANFORD INVESTORS

CERTIFICATE OF SERVICE

On December 7, 2009, I electronically submitted the foregoing document with the clerk of the court of the U.S. District Court, Northern District of Texas, using the electronic case filing system of the Court. I hereby certify that I will serve the Stanford Investors individually or through their counsel of record, electronically, or by other means authorized by the Court or the Federal Rules of Civil Procedure.

/s/ Kevin M. Sadler Kevin M. Sadler

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 3 of 9

ID Number Name

CD Proceeds Received in Excess of Investments Total CD Proceeds

1

GARY D. MAGNESS IRREVOCABLE TRUST, GARY MAGNESS, GMAG LLC AND MAGNESS SECURITIES LLC

$ 10,650,666.14 $ 90,411,977.14

2JUERGEN KURT WAGENTROTZ AND JURGEN KURT WAGENTROTZ ERNST

$ 8,589,727.46 $ 44,168,667.09

3 ROBERTO GALLARDO KURI $ 6,417,324.64 $ 6,417,324.64

4

ANTONY MANSOUR AND REHAN MANSOUR, ANTONY MANSOUR, JOSEPHINE MERY, FANCOISE SOLANGE MERY AND JOSEPHINE MERY

$ 5,332,910.14 $ 10,827,566.82

5 COMPANIA MINERA CAOPAS SA DE CV $ 5,119,458.09 $ 13,508,505.76 6 ANGLO-ATLANTIC STEAMSHIP CO. LTD. $ 4,276,637.90 $ 16,276,637.90 7 AYSE OYA ERHAN $ 3,282,388.14 $ 3,282,388.14

8

BORDEAUX INVESTMENTS I C.V.; PROVENCE MANAGEMENT STICHTING I AND BORDEAUX INVESTMENTS I C.V.

$ 3,063,621.89 $ 7,424,640.52

9 LEOPOLDO AROSEMENA CEVASCO $ 2,589,786.69 $ 2,929,286.22 10 KIRKWELL C.V. $ 2,388,114.97 $ 13,791,011.03 11 ALNOOR NATHOO $ 1,745,935.00 $ 1,745,935.00 12 BRETT LANDES $ 1,508,512.83 $ 12,512,705.59

13

EDWARD HYLTON JONES AND EDWARD HYLTON JONES AND SHIRLEY GLORIA JONES

$ 1,476,400.18 $ 8,367,336.14

14CLAUDIO ENRIQUE HERNANDEZ VILLALOBOS

$ 1,106,429.75 $ 4,999,383.94

15BRUCE THOMPSON AND MICHELLE THOMPSON AND BRUCE THOMPSON

$ 1,081,369.51 $ 12,597,948.06

16 THOMAS J. MORAN $ 987,675.25 $ 5,670,425.25

17

GEORGE JOSEPH ROLLAR AND GEORGE JOSEPH ROLLAR AND DOLORES MAY PAYER ROLLAR

$ 936,250.10 $ 12,936,230.10

18 AUBREY O'NEAL CLEMENT $ 924,408.16 $ 8,524,408.16

19

THE ANTHONY JOSEPH ANTINORI TRUST AND ANTHONY JOSEPH ANTINORI; AND STEVEN JAMES ANTINORI IN HIS CAPACITY AS TRUSTEE OF THE ANTHONY JOSEPH ANTINORI TRUST; THE STEVEN JAMES ANTINORI TRUST AND STEVEN JAMES ANTINORI

$ 880,657.48 $ 5,080,657.48

20

ARTURO ORTEGA GONZALEZ AND MARIA CAROLINA ORTEGA GONZALEZ AND GERMAN LUIS ORTEGA GONZALEZ AND ARTURO ORTEGA GONZALEZ

$ 853,341.46 $ 3,228,141.03

21 TEBEL CORPORATION $ 815,855.77 $ 3,601,507.98

22

NAIRC B.V., NAIRC-NETHERLANDS ANTILLEAN INSURANCE AND NAIRC-NETHERLANDS ANTILLEAN INSURANCE AND REINSURANCE COMPANY

$ 803,511.11 $ 5,280,924.84

23 INTERMEDIA LTD. $ 755,310.82 $ 3,863,952.14

24CORPORATION NACIONAL DE INVERSIONES SA DE CV

$ 752,611.74 $ 5,752,611.74

25

ALBERTO JAVIER BOTELLO REED; SILVIA GUADALUPE TAMEZ DE BOTELLO

$ 733,001.32 $ 5,490,419.98

1

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 4 of 9

ID Number Name

CD Proceeds Received in Excess of Investments Total CD Proceeds

26

BORDEAUX INVESTMENTS III C.V.; PROVENCE MANAGEMENT STICHTING III AND BORDEAUX INVESTMENTS III C.V.

$ 687,563.52 $ 4,909,151.23

27 TA TRUST $ 654,778.00 $ 3,200,000.00 28 ALGICA S.A. $ 641,672.49 $ 3,381,672.49 29 JORGE EMILIO GARZA TREVINO $ 610,364.50 $ 2,650,364.50 30 WALDMAN, LTD. $ 603,314.34 $ 2,069,266.11

31PINGYI HE ORRUILIAN WU DE HE AND PINGYI HE

$ 569,163.15 $ 3,237,629.18

32

DIVO MILAN HADDAD; INFINITUM TRUST AND DIVO MILAN HADDAD; MARIA DE LOURDES MARTINEZ DE SIDNEY AND MARIE ROCHELLE SIDNEY MARTINEZ; MARIE ROCHELLE SIDNEY MARTINEZ; MARIE ROCHELLE SIDNEY MARTINEZ AND DIVO MILAN HADDAD

$ 520,076.40 $ 9,017,539.51

33

BORDEAUX INVESTMENTS IX C.V.; PROVENCE MANAGEMENT STICHTING IX AND BORDEAUX INVESTMENTS IX C.V.; FELIX MARIO HERNANDEZ LARROCOECHA

$ 493,331.22 $ 3,120,002.74

34 OSCAR BENEDETTI $ 443,160.28 $ 2,005,522.28 35 PLATEAU TELECOMMUNICATIONS $ 438,074.19 $ 4,188,567.38 36 MARIO BRAUN RUSSEK $ 403,390.26 $ 2,052,175.19 37 PUPIBUBI TRUST $ 390,334.23 $ 2,531,874.20 38 WEST MEADOWS LTD. $ 383,573.60 $ 10,218,256.47 39 FAYHILL INTERNATIONAL $ 382,593.54 $ 9,446,366.78

40ISABEL ESTHER BENEDETTI DE IZQUIERDO $ 358,824.32 $ 3,198,796.81

41 BENITO DE LUCA TRUST $ 354,013.44 $ 1,700,000.00

42GALO ENRIQUE VILLAMAR VILLAFUERTE $ 352,584.93 $ 5,062,584.93

43 SALOMON DONDICH ROSENHAUS $ 341,026.01 $ 2,068,347.87 44 RAMON ALVAREZ BORONDO $ 339,386.03 $ 2,546,842.76

45INTERNATIONAL PETROCHEMICAL SALES LIMITED

$ 334,933.29 $ 3,463,187.24

46

AZALEA REST CEMETARY INC. IRREV TRUST, AZALEA REST CEMETARY INC., AND GEORGE B. ANNISON, IN HIS CAPACITY AS TRUSTEE OF AZALEA REST CEMETARY INC. IRREV TRUST; GEORGE BUR ANNISON AND DIANE B. ANNISON

$ 315,895.12 $ 1,527,787.35

47

INVERSIONES VARMOL TRUST CARE OF DR. JORGE MARIO VARGAS P. AND INVERSIONES VARMOL TRUST

$ 307,203.38 $ 5,513,731.85

48 HERMAN J. MILLIGAN JR. $ 297,900.23 $ 1,259,160.23 49 STEPHEN J. BURNHAM $ 289,882.60 $ 1,436,882.60 50 CRAYFORD HOLDINGS LIMITED $ 280,183.17 $ 2,525,195.09 51 INMOFYBE S.A. $ 277,815.11 $ 1,857,815.11 52 JOHN F. LYNCH $ 272,234.64 $ 3,865,595.78 53 ANGELO VICTOR GONCALVES $ 260,986.76 $ 2,273,986.76 54 INES DE VILLAMAR $ 256,889.49 $ 3,722,889.49 55 JOHN O. LETARD $ 254,452.09 $ 900,452.15 56 GENOVA TRUST $ 253,357.47 $ 2,403,357.47

57

BILLIE RUTH MCMORRIS; RONALD B. MCMORRIS; RONALD MCMORRIS AND VIRGINIA MCMORRIS; VIRGINIA H. MCMORRIS

$ 246,164.09 $ 1,149,598.95

2

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 5 of 9

ID Number Name

CD Proceeds Received in Excess of Investments Total CD Proceeds

58 SLEEPING DOG HOLDINGS, LTD. $ 242,247.86 $ 1,578,105.82 59 SHENOOR JADAVJI $ 235,311.12 $ 1,811,706.62 60 PHILLIP E. LANKFORD JR. $ 227,091.90 $ 625,091.90 61 WAYLAND B. ALEXANDER $ 212,211.54 $ 734,912.32 62 THOMAS W. SLAUGHTER $ 211,481.93 $ 634,481.93 63 LUPE MARTINEZ TRUST $ 210,386.63 $ 2,364,903.13

64JAMIE COHEN BENREY AND SUSANA PEREZ DE COHEN

$ 208,771.30 $ 2,398,317.27

65 WILLIAM C. PROVINE $ 204,125.61 $ 1,949,125.61 66 TROY L. LILLIE JR. $ 203,451.44 $ 954,310.10 67 RONALD W. PARKER $ 202,353.43 $ 693,781.54

68MICHAEL WHEATLEY AND BETTY WHEATLEY

$ 199,508.38 $ 1,699,535.78

69 HERRERA HOLDINGS LTD $ 192,198.53 $ 3,692,198.53 70 MICHAEL A. SPEEG $ 187,181.18 $ 837,379.64 71 ANTHONY G. PARKER $ 183,692.20 $ 1,003,163.24 72 COFFEY OVERSEAS LIMITED $ 183,494.81 $ 1,493,478.92 73 JAMES D. SIMMONS $ 181,839.52 $ 836,364.81 74 THOMAS H. TURNER $ 181,615.32 $ 2,957,505.32 75 LAURA JEANETTE N. LEE $ 176,724.64 $ 525,006.15 76 DENNIS L. KIRBY $ 175,006.66 $ 580,958.77 77 CLYDE ANDERSON $ 174,856.85 $ 704,866.71 78 GOLD WING PARTNERS $ 174,445.65 $ 1,425,426.79 79 SOCIEDAD GENERAL DE INVERSIONES $ 173,659.10 $ 1,996,089.10 80 DOROTHY T. DUNCAN $ 170,458.52 $ 564,694.24 81 JAMES W. BORING JR. $ 167,087.27 $ 612,235.25 82 MICHAEL J. DRAGO $ 165,483.89 $ 592,193.23 83 FRANZ KONRAD ROSEN $ 164,809.43 $ 1,883,920.47 84 SAXONIA FOUNDATION $ 160,931.01 $ 2,255,430.40 85 SANDRA F. HARRELL $ 154,587.85 $ 404,587.85 86 BETTE JO HEASLIP $ 153,433.03 $ 703,433.03

87RONALD E. WELLS; RONALD E. WELLS SR. AND LUTHER D WELLS

$ 152,816.01 $ 833,634.76

88 MALTON OVERSEAS LTD. $ 151,285.82 $ 1,802,058.77 89 ARISTIDE TRELOAR $ 150,706.07 $ 649,730.37 90 TIMOTHY A. JOHNSON $ 149,572.57 $ 852,446.20 91 DENNIS CHILDRESS $ 147,426.06 $ 646,426.06 92 NORFE S.A $ 146,164.17 $ 2,551,164.17 93 MUDDY WATER HOLDINGS LIMITED $ 144,719.09 $ 1,585,349.04 94 GARY WOOD $ 141,619.74 $ 641,619.74 95 PEGGY PAYNE MORAGNE $ 141,229.66 $ 401,818.31 96 CHARLIE L. MASSEY $ 140,747.84 $ 390,809.49

97

RICHARD A. DEVALL; RICHARD DEVALL AND SUE M. DEVALL; SUE M. DEVALL

$ 140,492.62 $ 552,871.02

98

HARDEE M. BRIAN AND BETTY JO BRIAN; YOUNG FAMILY CEMETARY TRUST

$ 139,989.40 $ 615,503.58

99

JOSE LUCIANO MENDEZ ALONSO AND MARIA DEL ROCIO CORONA ODRIOZOLA

$ 134,411.06 $ 753,391.06

100RICHARD S. FEUCHT; RICHARD S. FEUCHT AND JOAN A. FEUCHT

$ 133,701.68 $ 549,863.28

101

KRIMICH LTD.; MARIA TERESA SAN SEBASTIAN DE VALLE AND JOSE MARIA VALLE ESCAMEZ

$ 129,663.90 $ 2,834,000.00

102 TARRAL E. DAIGLE $ 126,361.20 $ 407,361.20 103 DARRELL D. COURVILLE $ 125,960.34 $ 685,960.34 104 GENE CAUSEY $ 123,288.92 $ 613,288.92 105 KENNETH W. DOUGHERTY $ 122,527.19 $ 641,527.19

3

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 6 of 9

ID Number Name

CD Proceeds Received in Excess of Investments Total CD Proceeds

106 YAIR SHAMIR AND ELLA SHAMIR $ 119,765.82 $ 1,119,720.82 107 JOHN D. COOPER $ 119,750.43 $ 619,750.43 108 JOHN R. HOLGUIN $ 118,725.76 $ 660,144.24 109 EMMA LEE LEFEBVRE $ 117,977.06 $ 205,981.88 110 LOUISE D PATTERSON $ 115,637.49 $ 2,115,637.49 111 ARTHUR R. WAXLEY JR. $ 115,268.15 $ 616,268.15 112 RAUL RODRIGUEZ MENDEZ $ 114,580.58 $ 454,581.81 113 JOHN E. TAYLOR $ 113,431.70 $ 639,109.67

114THOMAS E. BROWN AND BARBARA BROWN $ 109,254.20 $ 2,109,254.20

115 CHARLES L. WHITE $ 108,813.61 $ 558,813.61 116 CLAUDE M. NEEDHAM $ 107,224.36 $ 393,458.36 117 DONNA M. VINES $ 107,059.59 $ 346,142.84 118 HENRY A. MENTZ III $ 106,709.47 $ 706,719.47 119 ROBERT S. GREER AND ALICE D. GREER $ 102,523.66 $ 1,152,523.66 120 GAINES D. ADAMS $ 101,859.44 $ 453,139.44 121 ROBERT L. BUSH $ 100,849.09 $ 826,383.56 122 THE DAVIS REVOCABLE TRUST $ 100,260.79 $ 857,660.79 123 DAVID TOPP AND DORA TOPP $ 98,648.14 $ 1,098,648.14 124 MARY E. GERRY $ 98,380.29 $ 432,442.99 125 JAMES E. RICHARDSON FAMILY TRUST $ 97,757.04 $ 5,097,757.04 126 JEFF P. PURPERA JR. $ 97,693.42 $ 597,693.42 127 EMOLYN L. WATTS $ 95,010.68 $ 364,391.35 128 ROBERT SOULE $ 91,266.03 $ 457,234.31 129 CHARLES E. SMITH $ 90,859.07 $ 486,996.16 130 JAMES E. BROWN SR. $ 90,386.71 $ 590,386.71 131 EDGAR THERON OVERLAND $ 90,361.49 $ 416,269.22 132 TERRY N. TULLIS $ 89,938.39 $ 449,245.41 133 LUSKY INVESTMENT PARTNERSHIP, LP $ 87,889.50 $ 287,889.50 134 DENNIS LANTRIP $ 87,795.71 $ 477,927.39

135

AUDREY LETARD; JUDY A. VARNADO AND PATRICIA A. ALLISON AND AUDREY A. LETARD; PATRICIA A. ALLISON

$ 85,769.23 $ 344,189.98

136JOHN G. DENISON AND KATHY R. DENISON $ 85,734.45 $ 585,734.45

137 ROBERT J. BRUNO $ 82,262.63 $ 582,263.63

138

CHARLES R. SANCHEZ AND MAMIE C. SANCHEZ; CHARLES R. SANCHEZ SR.; MAMIE C. SANCHEZ

$ 82,204.45 $ 517,110.12

139

BORDEAUX INVESTMENTS X C.V.; PROVENCE MANAGEMENT STICHTING X AND BORDEAUX INVESTMENTS X C.V.

$ 81,941.84 $ 664,151.84

140 TERESA MEMUN DE ALFIE $ 81,578.67 $ 276,090.99 141 EDITH IRMA WATTS $ 79,224.44 $ 539,225.13 142 EARL L. CROSBY $ 75,276.22 $ 175,276.22 143 LARRY N. SMITH $ 73,370.47 $ 485,678.50

144ROBERT B. CRAWFORD JR. AND JODIE F. CRAWFORD

$ 72,197.81 $ 322,197.81

145LYDA D. TYMIAK; LYDA D. TYMIAK FAMILY TRUST AND LYDA D. TYMIAK

$ 70,535.29 $ 570,546.25

146 DIANE DUNN $ 70,527.65 $ 245,527.65 147 RADIUM COMPANY LTD. $ 69,415.76 $ 2,069,415.76 148 JOSE ALBERTO ROMERO VILORIA $ 68,972.06 $ 8,235,849.49 149 YENZO INVESTMENT, INC. $ 68,495.27 $ 843,541.50

150

BBRATSS PRODUCTIONS, INC.; TIMOTHY RUSSELL RICKETTS AND ROSE S. RICKETTS

$ 66,459.73 $ 2,416,459.73

151 MELVIN S. TAUB AND CAROL TAUB $ 65,959.17 $ 1,065,959.17 4

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 7 of 9

ID Number Name

CD Proceeds Received in Excess of Investments Total CD Proceeds

152 ROSS D. BRUCE AND MARSHA C. BRUCE $ 64,991.83 $ 564,991.83 153 NONNA E TRUST $ 63,529.53 $ 3,079,824.08 154 EUGENE L. CROXTON JR. $ 61,805.39 $ 161,805.39 155 PINOT HOLDINGS LIMITED $ 60,808.26 $ 1,083,208.85

156KEVIN A. MCKENZIE AND DENISE T. MCKENZIE

$ 56,727.82 $ 806,974.43

157 GWENDOLYN E. FABRE $ 55,453.05 $ 355,934.17

158

BLUFF CREEK REDI-MIX, INC.; FLEN ROCK COMPANY, LLC.; FLENIKEN SAND & GRAVEL, INC.; LYMAN L. FLENIKEN JR.

$ 55,052.80 $ 643,354.14

159DOT G. MELDER; JACK W. MELDER; JACK W. MELDER AND DOT G. MELDER

$ 51,689.19 $ 506,154.82

160 FRANCIS NEZIANYA $ 51,635.86 $ 301,635.86 161 AMARA TRUST $ 49,948.93 $ 399,948.93 162 ROBERT C. WILLIAMS $ 48,727.92 $ 263,727.92

163WILLIAM BRUCE JOHNSON AND JENNIFER SAVOIC JOHNSON

$ 45,414.72 $ 245,464.04

164 MICHAEL S. ASMER $ 42,664.50 $ 1,029,844.69 165 OLIVIA S. WARNOCK $ 42,455.46 $ 392,684.49 166 ROBERT YOUNG JR. $ 42,117.20 $ 360,476.58 167 MICHAEL J. TIMMONS $ 40,081.62 $ 540,081.62 168 WILLIAM E. ENSMINGER $ 39,845.96 $ 154,845.96

169DANIEL JOSEPH DAIGLE AND JILDA ANN DAIGLE; JILDA A. DAIGLE

$ 39,820.10 $ 282,664.32

170 JOHNNIE A. GRIFFITH $ 38,521.26 $ 504,427.86 171 ARCHIE SMITH $ 37,753.36 $ 510,998.65 172 TAHSIN YILMAZ KALKAVAN $ 37,705.31 $ 287,705.31

173JANE M. PRIDGEN AND ROBERT GRAY MATLOCK

$ 35,771.54 $ 185,771.54

174 ROLAND SAM TORN $ 35,354.86 $ 1,035,354.86 175 ARTHUR TORNO $ 33,945.60 $ 283,945.60 176 JOSEPH A. CHUSTZ $ 33,340.28 $ 598,797.31

177

CHERAY ZAUDERER HODGES; LUTHER HARTWELL HODGES; LUTHER HARTWELL HODGES AND CHERAY ZAUDERER HODGES

$ 30,575.00 $ 2,480,701.04

178 MONTY M. PERKINS $ 29,491.95 $ 129,491.95 179 MURPHY BUELL $ 29,483.22 $ 417,216.30 180 BARBARA ANTHONY $ 29,097.56 $ 345,381.68 181 MICHAEL R. HOLCOMB $ 28,364.18 $ 278,364.18 182 LARRY W. PERKINS $ 27,640.62 $ 427,640.62 183 JIMMY QUEBEDEAUX $ 26,693.16 $ 330,756.21 184 CARL M. WEBB III $ 25,391.64 $ 125,391.64 185 RISIA TOPP WINE $ 23,911.16 $ 223,911.16 186 CAROLYN CRANSTON $ 22,783.85 $ 149,054.72 187 BRIAN U. LONCAR AND SUE A. LONCAR $ 22,517.55 $ 222,517.55

188

INVERSIONES PATRICK ROGER P AND PATRICK PETIOT; PATRICK LORIS ROGER PETIOT

$ 21,740.61 $ 726,140.84

189 GERALD S. PASTERNAK $ 20,839.38 $ 370,839.38 190 JUDITH P. SIMMONS $ 20,463.87 $ 422,748.77 191 JOHN E. WILSON $ 19,527.19 $ 405,074.46

192SAMUEL R. MOORE AND MARTHA W. MOORE

$ 18,045.11 $ 218,045.11

193CARLOS LANDEROS GALLEGOS AND MARIA DE JESUS LANDEROS GALLEGOS

$ 18,000.00 $ 268,000.00

194 DIFFICULTY HOLDINGS LIMITED $ 16,855.75 $ 616,734.19 195 DOROTHEA M. YOUNG $ 15,562.29 $ 124,680.29 196 JUANITA QUINEALTY $ 15,446.22 $ 119,446.22

5

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 8 of 9

ID Number Name

CD Proceeds Received in Excess of Investments Total CD Proceeds

197 ANTONIO SANCHEZ RAMOS $ 15,083.89 $ 528,918.97

198ELENA TRON DE ZEPEDA CARRANZA; MAURICIO ZEPEDA CARRANZA

$ 13,529.30 $ 2,590,188.72

199 ANTHONY J. VENTRELLA $ 13,427.03 $ 483,222.26

200JONATHAN LARKIN STOCK TRUST AND JONATHAN LARKIN

$ 12,925.82 $ 262,925.82

201VINETA P. STANSEL AND HOWARD STANSEL $ 11,847.39 $ 256,161.20

202 CHARLES A. JAMES $ 10,149.06 $ 360,149.06

TOTAL $ 93,788,316.33 $ 545,712,937.03

6

Case 3:09-cv-00724-N Document 129 Filed 12/07/2009 Page 9 of 9