land uses: biomass for food and fuel in brazil - the next 20 years jose roberto moreira centro...

TRANSCRIPT

LAND USES: BIOMASS FOR FOOD AND FUEL IN BRAZIL - THE NEXT 20 YEARS

JOSE ROBERTO MOREIRA

CENTRO NACIONAL DE REFERENCIA DE BIOMASSA

WORKSHOP

SUSTENTABILIDADE NA GERAÇÃO E USO DE ENERGIA NO BRASIL: OS PRÓXIMOS

VINTE ANOS

CAMPINAS 18-20 DE FEVEREIRO, 2002

TECHNOLOGY ISSUES

Long term technical potential - renewable energy supply

2100 Total EnergyDemand for SRESscenario ranges515-2737 EJ/yr

Long-term Technical Potential(EJ/yr)

Hydro >50Geothermal >20Wind >630Ocean >20Solar >1600Biomass >440Total Renewable >2800

Source: IPCC-TAR, 2001

0

5

10

15

20

25

30

35

40

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

IPCC SRES A2 Scenarios

A2

550550

750750

0

5

10

15

20

25

30

35

40

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

IPCC SRES A1B Scenarios

450450 550550 650650

Glo

bal

An

thro

po

gen

ic C

arb

oo

n D

ioxi

de

Em

issi

on

s (G

tC)

A1B

0

5

10

15

20

25

30

35

40

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

IPCC SRES B1 Scenarios

450450550550

B1

0

5

10

15

20

25

30

35

40

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

IPCC SRES A1T Scenarios

A1T

450450550550

650650

0

5

10

15

20

25

30

35

40

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

IPCC SRES B2 Scenarios

450450 550550 650650

B2

0

5

10

15

20

25

30

35

40

1990 2000 2010 2020 2030 2040 2050 2060 2070 2080 2090 2100

IPCC SRES A1FI Scenarios

450450550550650650

750750

A1FI

How to stabilise concentrations?

Emissions to be avoided: 300-1500 GtC

FIGURA 1: COMPARAÇÃO DAS EMISSÕES CUMULATIVAS DE CARBONO NO PERÍODO 1990 - 2100

COM AS RESERVAS DE COMBUSTÍVEL FÓSSIL E OS RECURSOS BÁSICOS EXISTENSTES

0

1000

2000

3000

4000

5000

6000

B1A1T B2

A1B A2A1F

I

WRE35

0

WRE45

0

WRE55

0

WRE65

0

WRE75

0

WRE10

00IS

92

cum

ula

tive

ca

rbo

n f

rom

199

0-21

00 i

n G

tC

scenarios

fossil fuel resource base

oil, coal and gas reserves

oil and gas reserves (total)

oil and gas reserves (conventional)

1860-1997

SRES illustrative scenarios stabilisation scenarios

1. Os recursos básicos de combustíveis fósseis são várias vezes maiores que a emissão cumulativa de carbono em todos os cenários do IPCC 2000

2. Emissões cumulativs de carbono nos cenários que permitem estabilização do nível de carbono em 450 ppm ou maior são significantemente maiores que as reservas de petróleo e gás, mas menors que as reservas de carvão.

Mitigation options

• Energy efficiency

• Decarbonisation– energy sources

– CO2 removal and storage

• Biological carbon sequestration

• Reducing other greenhouse gases from industry, agriculture, waste management

Mitigation options

• Energy efficiency

• Decarbonisation

–energy sources– CO2 removal and storage

• Biological carbon sequestration

• Reducing other greenhouse gases from industry, agriculture, waste management

Projection of technical energy potential from biomass by 2050.

Region

Population in 2050

Billion

Total landwith cropproductio

npotential

Gha

Cultivated

Land in1990

Gha

Additionalcultivated

landrequired in

2050Gha

Available areafor biomass

production in2050Gha

Max. Additionalamount of energy

from biomassa)

EJ/yr

Developedb) - 0.820 0.670 0.050 0.100 30Latin AmericaCentral &Caribbean

0.286 0.087 0.037 0.015 0.035 11

South America 0.524 0.865 0.153 0.082 0.630 189AfricaEastern 0.698 0.251 0.063 0.068 0.120 36Middle 0.284 0.383 0.043 0.052 0.288 86Northern 0.317 0.104 0.04 0.014 0.050 15Southern 0.106 0.044 0.016 0.012 0.016 5Western 0.639 0.196 0.090 0.096 0.010 3Chinac) - - - - - 2Rest of AsiaWestern 0.387 0.042 0.037 0.010 -0.005 0South –Central 2.521 0.200 0.205 0.021 -0.026 0Eastern 1.722 0.175 0.131 0.008 0.036 11South –East 0.812 0.148 0.082 0.038 0.028 8Total for regionsabove 8.296 2.495 0.897 0.416 1.28 396TOTAL BIOMASS ENERGY POTENTIAL, EJ/yr 441d)

a) Assumed 15 odt/ha/yr and 20Gj/odtb) Here, OECD and Economies in Transitionc) For China, the numbers are projected values from D’Apote (1998) and not maximum estimates.d) Includes 45 EJ/yr of current traditional biomass.

Source: Derived from Fischer and Heilig, 1998; D’Apote, 1998; IIASA/WEC, 1998)

AMOUNT OF LAND REQUIRED FOR ALTERNATIVE ENERGY PRODUCTION

MILLION HA

WIND 300 (1)

SOLAR ENERGY 393 (2)

BIOMASS 1280 (3)

1) 10% of all earth land area with wind speed above 5.1 m/s at 10m height

2) 10% of the land area classified as “other lands” category by the FAO(1999)

3) All potential crop land area not been required for food crops in year 2050 are used

– Potential contribution of Biomass to the world’s energy needs

SourceTimeframe(year)

Totalprojected

global energydemand

(exajoules ayear)

Contribution ofbiomass to energy

demand(exajoules a year)

Comments

Riges 2025 395 145 Based on calculation with theRIGES model

(Johansson andothers, 1993)

2050 561 206

SHELL 2060 1,500 220 Sustained growth scenario(Kassler, 1994) 900 200 Dematerialization scenarioWEC (1994a) 2050 671 – 1,057 94 – 157

2100 895 – 1,880 132 –215Range given here reflects theoutcomes of three scenarios

Greenpeace andSEI

2050 610 114

(Lazarus andothers, 1993)

2100 986 181

A scenario in which fossil fuelsare phased out during the 21st

century

IPCC 2050 560 280 Biomass intensive energysystem development

(Ishitani andJohansson, 1996)

2100 710 325Source: Turkenburg, 2000

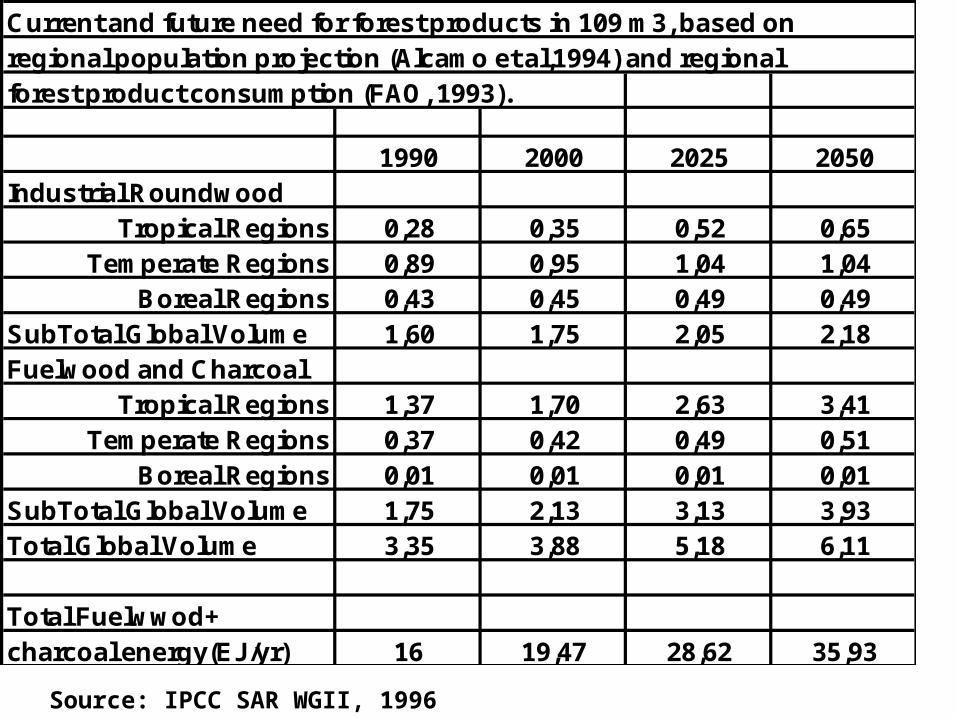

Current and future need for forest products in 109 m3, based on regional population projection (Alcamo et al,1994) and regionalforest product consumption (FAO, 1993).

1990 2000 2025 2050Industrial Roundwood

Tropical Regions 0,28 0,35 0,52 0,65Temperate Regions 0,89 0,95 1,04 1,04

Boreal Regions 0,43 0,45 0,49 0,49SubTotal Global Volume 1,60 1,75 2,05 2,18Fuelwood and Charcoal

Tropical Regions 1,37 1,70 2,63 3,41Temperate Regions 0,37 0,42 0,49 0,51

Boreal Regions 0,01 0,01 0,01 0,01SubTotal Global Volume 1,75 2,13 3,13 3,93Total Global Volume 3,35 3,88 5,18 6,11

Total Fuelwwod+charcoal energy(EJ/yr) 16 19,47 28,62 35,93

Source: IPCC SAR WGII, 1996

Annual Growing Stocks

Tropical RegionTemperate RegionBoreal Region

Fuelwood

5

157,53

2010

105

1,5

Managed Forests Yieds (m3/yr) as 1990Well Managed

ForestsTreesFast Growing

1990 2000 2025 2050Industrial Roundwood

Tropical Regions 0,019 0,023 0,035 0,043Temperate Regions 0,119 0,127 0,139 0,139

Boreal Regions 0,143 0,150 0,163 0,163SubTotal Global Area 0,281 0,300 0,337 0,345Fuelwood and Charcoal

Tropical Regions 0,069 0,085 0,132 0,171Temperate Regions 0,037 0,042 0,049 0,051

Boreal Regions 0,003 0,003 0,003 0,003SubTotal Global Area 0,109 0,130 0,184 0,225Total Global Area 0,390 0,430 0,521 0,570TOTAL FOREST AREA 3,4-4,1 2,5-3,1

Total Potential FuelwoodEnergy (EJ/yr) 562,33 400,3

Required Area to Fulfill Wood Demand Using Planted Fuelwood & Fast Growing Trees for Roundwood 1990 Data

(109 ha)

Country Area Yield Production Price Value** Total Value Area Yield Production Price Value Total Value(Mha) (t/ha) (Mt) (LC)* (US$/ha) (MUS$) (Mha) (t/ha) (Mt) (LC) (US$/ha) (MUS$)

BRAZIL 14 2,68 38,8 162 573,52 8303,2 12,8 3,24 41,5 112 324 4150USA 30 2,49 75 214 532,86 16050 28 8,38 235 100CHINA 8,7 1,72 15 23,5 4,7 110INDIA 6 0,93 56 6,6 1,82 12WORLD 85 2,25 187 163 4,29 711

* Local Currency**Uses the US market value. The assumption is not always commercially feasible.

Country Area Yield Production Price Value Total Value Area Yield Production Price Value* Total Value(Mha) (t/ha) (Mt) (LC) (US$/ha) (MUS$) (Mha) (t/ha) (Mt) (LC) (US$/ha) (MUS$)

BRAZIL 3,2 3,23 10,3 177 516,8 1648 2,3 0,78 1,8 1037 780 1800USA 1,3 7,01 9,1 160 0 1,45 0,0038 5780CHINA 28,5 6,35 18,1 NA 1,36 0,0075INDIA 44,5 2,96 13,2 0,31 0,97 0,301WORLD 180 3,85 58,5 11,7 0,62 73

*Coffee value in Brazil is much lower than in US. A value of US1000/tonne was assumed

SOYBEANS

RICE

Largest Crops in Brazil Compared with Some Other Important Agricultural Producers

MAIZE

COFFEE

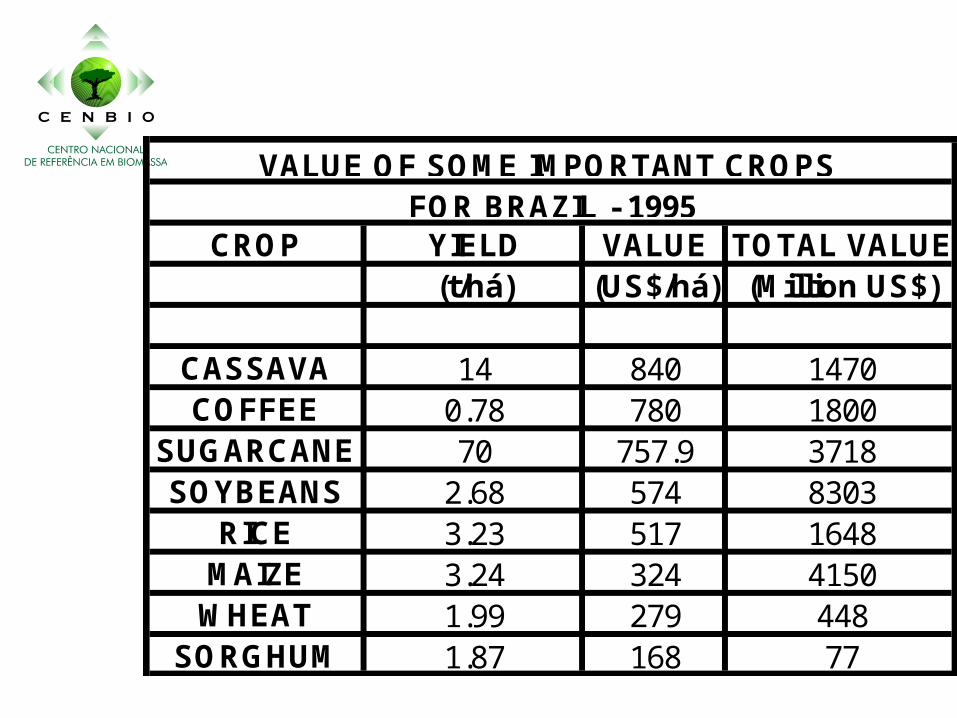

CROP YIELD VALUE TOTAL VALUE(t/há) (US$/há) (Million US$)

CASSAVA 14 840 1470COFFEE 0.78 780 1800

SUGARCANE 70 757.9 3718SOYBEANS 2.68 574 8303

RICE 3.23 517 1648MAIZE 3.24 324 4150

WHEAT 1.99 279 448SORGHUM 1.87 168 77

VALUE OF SOME IMPORTANT CROPS FOR BRAZIL - 1995

HARVESTED AREAS FOR SOME MAJOR CROPS

0

50

100

150

200

250

BRAZIL USA CHINA INDIA WORLD

COUNTRIES

MH

A

SOYBEANS

MAIZE

SUGARCANE

RICE

COFFEE

CASSAVA

WHEAT

SORGHUM

AMOUNT OF BIOMASS HARVESTED- MAJOR CATEGORIES- 2001

0

500

1000

1500

2000

2500

3000

BRAZIL USA CHINA INDIA WORLD

COUNTRIES

MT

/YR

ALL CEREALS

SUGARCANE+"BARBOJO"

SUGARCANE

WOODFUEL(Comm.+NonComm.)

INDUSTRIAL ROUNDWOOD

WHEAT

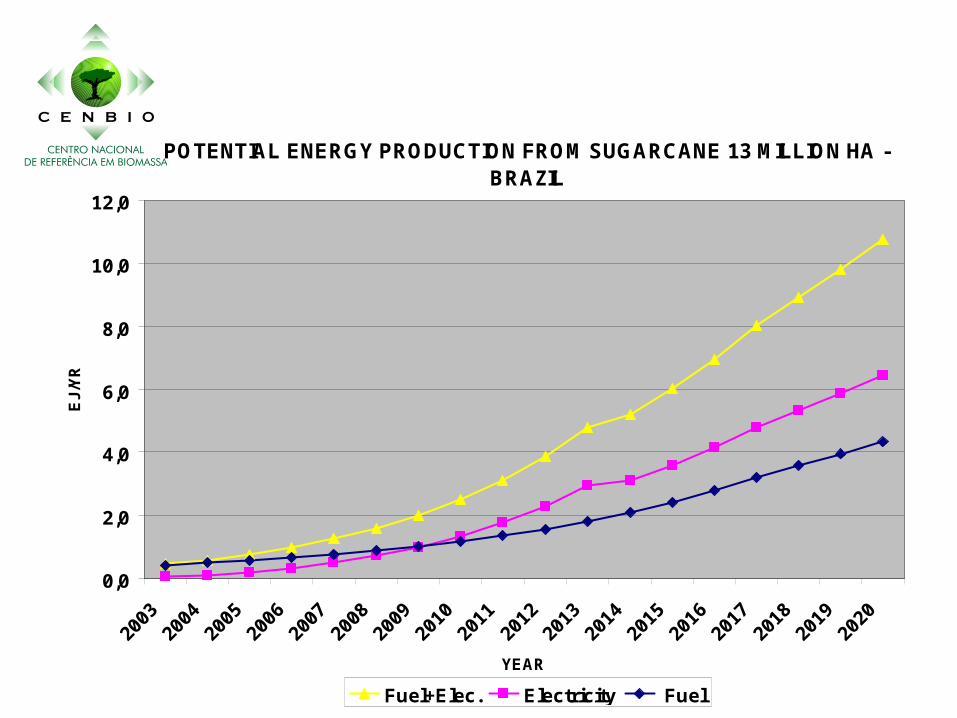

ENERGY PRODUCTION FROM SUGARCANE PLANTATION- AREA EQUIVALENT TO SOYBEANS CROP - BRAZIL 2002/2020

YEAR AREA YIELD TOTAL PRODUCTION

(Mha) (t/ha) (Mt/yr) (EJ) (Mboe/day) (TWh/yr) (EJ) (EJ) (Mboe/day)2003 2,60 70 182 0,429 0,239 9,1 0,064 0,492 0,2742004 2,86 74 210 0,495 0,276 11,6 0,081 0,576 0,3212005 3,15 77 243 0,572 0,318 26,7 0,187 0,759 0,4222006 3,46 81 280 0,661 0,368 46,3 0,324 0,985 0,5482007 3,81 85 324 0,763 0,425 71,3 0,499 1,262 0,7022008 4,19 89 374 0,881 0,490 102,9 0,720 1,601 0,8912009 4,61 94 432 1,018 0,566 142,6 0,998 2,016 1,1222010 5,07 98 499 1,176 0,654 192,1 1,345 2,521 1,4022011 5,57 103 576 1,358 0,756 253,6 1,775 3,133 1,7432012 6,13 109 666 1,568 0,873 329,5 2,307 3,875 2,1562013 6,74 114 769 1,811 1,008 422,9 2,960 4,772 2,6552014 7,42 120 888 2,092 1,164 444,1 3,108 5,201 2,8942015 8,16 126 1026 2,417 1,345 512,9 3,590 6,007 3,3422016 8,98 132 1185 2,791 1,553 592,4 4,147 6,938 3,8602017 9,87 139 1368 3,224 1,794 684,2 4,789 8,013 4,4582018 10,86 140 1521 3,582 1,993 760,3 5,322 8,904 4,9542019 11,95 140 1673 3,940 2,192 836,3 5,854 9,794 5,4492020 13,14 140 1840 4,334 2,412 919,9 6,439 10,774 5,994

Increase 5,05 2 10,11 10,109 10,109 101,1 101,089 21,878 21,878

TOTAL 2000* 39 13000TOTAL 2020* 68 22000* SOURCE: US-EIA, International Energy Outlook

TOTAL ENERGYFuel+Elec. Fuel Electricity

ENERGY PRODUCTION ENERGY PRODUCTION

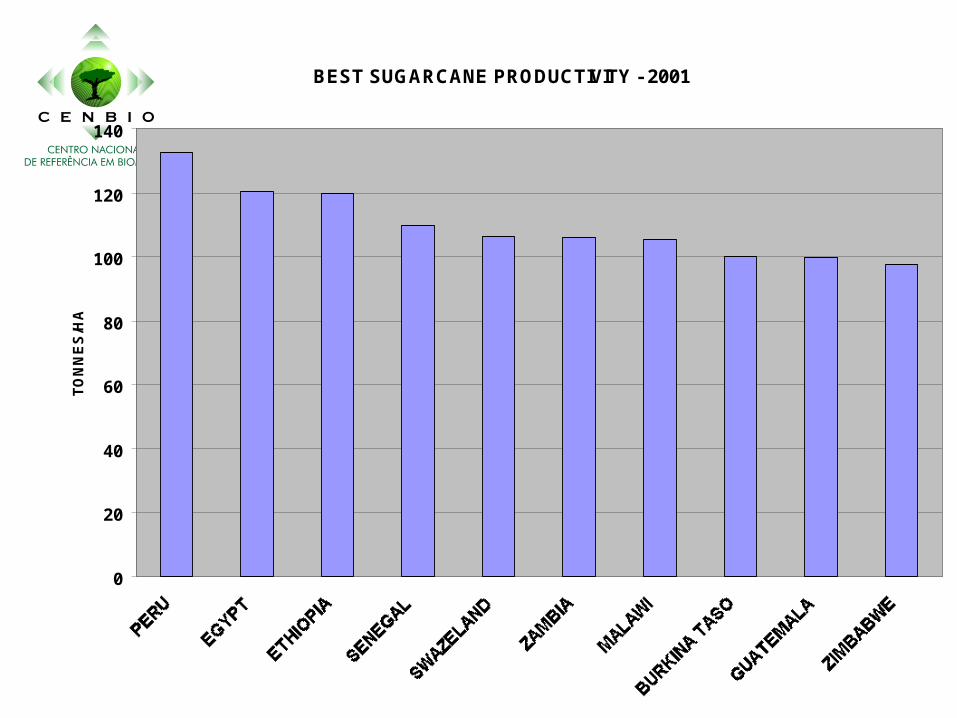

BEST SUGARCANE PRODUCTIVITY - 2001

0

20

40

60

80

100

120

140

TO

NN

ES

/HA

POTENTIAL ENERGY PRODUCTION FROM SUGARCANE 13 MILLION HA - BRAZIL

0,0

2,0

4,0

6,0

8,0

10,0

12,0

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YEAR

EJ

/YR

Fuel+Elec. Electricity Fuel

WORLD BRAZIL USA INDIA CHINA

Agricultural Area (1000Ha) 4,961,289 250.2 418.3 180.8 535.36Arable & Permanent Crops (1000Ha) 1,501,452 65.2 179 169.7 135.36

SOURCE: FAO, 2002

LAND AVAILABILITY AND LAND USE FOR CROPSSELECTED COUNTRIES - 1999

WORLD FEASIBLE SUGARCANE PLANTATION -LARGE EFFORT SCENARIO- 2020

COUNTRY POTENTIAL AREA (Mha) (EJ) (Mboe/day) (TWh/yr) (EJ) (EJ) (Mboe/day)

BRAZIL 20 6,596 3,6700793 1400 9,8 16,396 9,1227797USA 10 3,298 1,8350397 700 4,9 8,1981 4,5613899INDIA 10 3,298 1,8350397 700 4,9 8,1981 4,5613899CHINA 10 3,298 1,8350397 700 4,9 8,1981 4,5613899MEXICO 4,8 1,583 0,880819 336 2,352 3,9351 2,1894671CENTRAL AM 4,8 1,583 0,880819 336 2,352 3,9351 2,1894671SOUTH AM 16 5,277 2,9360634 1120 7,84 13,117 7,2982238SOUTH ASIA 16 5,277 2,9360634 1120 7,84 13,117 7,2982238AUSTRALIA 16 5,277 2,9360634 1120 7,84 13,117 7,2982238AFRICA 16 5,277 2,9360634 1120 7,84 13,117 7,2982238OTHER 20 6,596 3,6700793 1400 9,8 16,396 9,1227797TOTAL 143,6 47,36 26,351169 10052 70,36 117,72 65,501559

TOTAL 2000* 39 13000TOTAL 2020* 68 22000

* SOURCE: US-EIA, International Energy Outlook

PRODUCTION PRODUCTION PRODUCTIONFUEL+ELECTR.FUEL ELECTRICITY

PRODUCTION OF SOME BIOMASS IN 2000 COMPARED WITH SUGARCANE POTENTIAL PRODUCTION IN 2020

0

5000

10000

15000

20000

25000

30000

WORLD

MT

/YE

AR

SUGARCANE+"BARBOJO" - LARGEEFFORT SCEN. - 2020

SUGARCANE+"BARBOJO"

WOODFUEL (Comm.+NonComm.)

INDUSTRIAL ROUNDWOOD

WHEAT

FUEL CONSUMPTION ON THE TRANSPORTATION SECTOR - BRAZIL 1974-1999

0

5000

10000

15000

20000

25000

30000

35000

YEAR

MIL

LIO

N O

F C

UB

IC M

ET

ER

CONSUMPTION GASOLINE + ALCOHOL DIESEL CONSUMPTION

GASOLINE CONSUMPTION ALCOOL CONSUMPTION

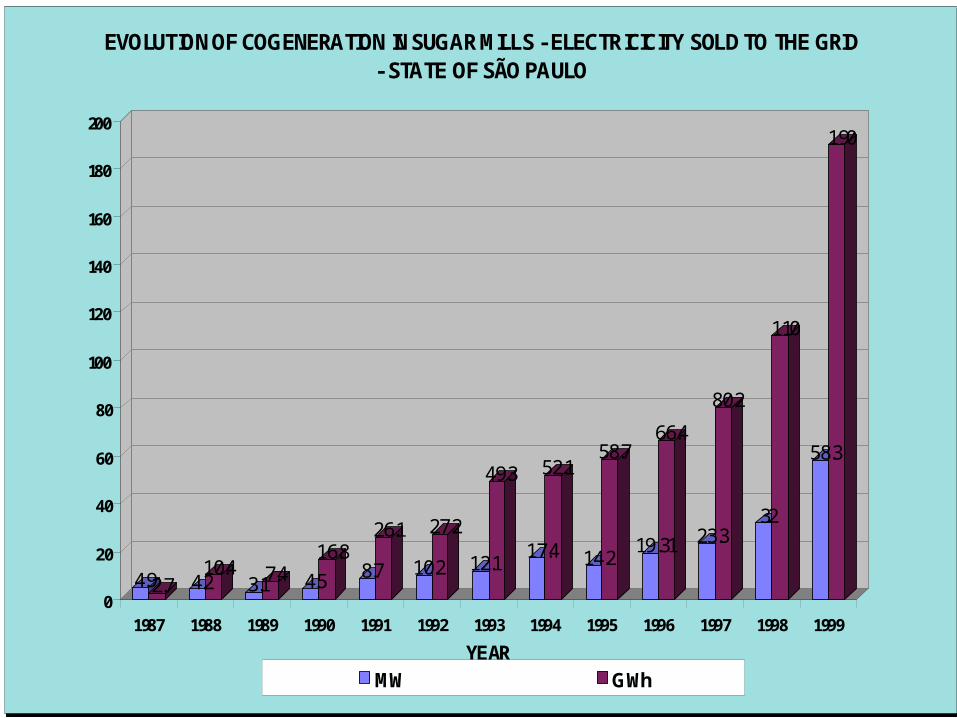

4.92.7 4.210.4

3.17.4 4.5

16.88.7

26.1

10.2

27.2

12.1

49.3

17.4

52.1

14.2

58.7

19.31

66.4

23.3

80.2

32

110

58.3

190

0

20

40

60

80

100

120

140

160

180

200

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999

YEAR

EVOLUTION OF COGENERATION IN SUGAR MILLS - ELECTRICICITY SOLD TO THE GRID - STATE OF SÃO PAULO

MW GWh

Car

bon

effi

cien

cy

Time

Market potentialEconomic potential

Socio-economic potential

Technological potential

Thermodynamic potential

Barriers to achieving the potential of technologies

Market failures

Values, attitudes, social barriers

High costs

Knowledge gap

SOCIO-ECONOMIC ISSUES

What are the main barriers to reach the (socio-)economic potential?

• Data, information, knowledge, awareness• Access to capital, especially smaller firms• Risk aversion in financial institutions, incl MDB’s• Trade barriers such as tariffs or export restrictions • Human and institutional capabilities • Missing codes and standards for EST’s • Low, subsidised conventional energy prices • Absence of full-cost pricing • Individual preferences/ lifestyle• Poverty

MITIGATION POTENTIAL TILL 2020

Source: Moomaw et al, IPCC, 2001

Compare to: 300-1500 Gt to be avoided over 100 years

A spokeswoman for the Mossman Central Mill-Australia said: 1) The Queensland and Federal Governments committed more than $10 million to the ethanol pilot plant project earlier this year; 2) Ethanol does not just have the potential to benefit cane growers but the environment and fuel consumers as well.

Peter Sheedy - Manager Herbert River District Canegrowers said:1) An ethanol blend offers a cleaner burning fuel; 2) Ethanol would also cut Australia's dependence on fossil fuel; 3) Ethanol has constantly to be kept on our radar screens.

Australian Cane Farmers Association chairman Warren Martin has: 1) Called for an immediate expansion of Australia's ethanol industry; 2) Stated many European countries already have mandatory ethanol-blend fuel; 3) Ethanol may ultimately provide the answer to more environmental issues than just greenhouse gas abatement," he said; 4) Additionally it will assist Australia to fill its own energy needs and rely less on imports.

Edition: ; Page: 001; Section: News

Japan eyes ethanol to cut greenhouse gas emissions Aya Takada (Reuters) Tokyo, December 20 , 2001

Japan, under pressure to cut greenhouse gas emissions, blamed for global warming, is considering introducing a policy of blending ethanol with gasoline.

Giant trading house Mitsui & Co is backing ethanol's introduction to the Japanese fuel market.

Estimate of the potential size of Japan's ethanol market is nearly six million kilolitres a year, based on the assumption that Japan would adopt an ethanol-to-gasoline blending ratio of 10 percent," said Mitsui biomass project manager Norimichi Okuda.

The Japanese have not used ethanol as fuel because they have not had any compelling need for an alternative But Japan has turned serious about using "green" energy.

From WWP- REPORT ON OIL GAS & PETROCHEMICALS

IN THE DEV, August 1st, 2001

Thailand is currently promoting the use of ethanol as an alternative

fuel.

It can be used as a substitute for the gasoline additive (MTBE).

As a results, the governments of Thailand and Austria are

considering a plan to set up 5 ethanol plants in Thailand.

The Austrian government's has proposed to Thailand that an

investment of around $22,000,000 to $44,000,000 could be made

for building each of the plants...

ENERGY RELATED CO2 EMISSIONS BY SECTOR - WORLD 1971-1995

1140 1273 1450 1542 1646 1732 1820 1913 2011 2113 2221

1653 1796 2094 2110 2293 2340 2387 2435 2484 2534 2586

672 760 862 925 1078 1215 1368 1540 1734 1952 2198

103 120 159 186 210 217 224 230 237 245 252

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1971 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020

Building industry Transportation Agriculture

ECONOMIC ISSUES

Retail Wholesale ------- Retail Wholesale

Brazil -- 15 Russia 33 22

Australia 35 United States 43 27

EU 60 -- Japan 73 48

Cuba 8 -- South Korea -- 36

Thailand 13 12 Canada 30 16

Guatemala -- 22 Iran NA NA

South Africa -- 22 Malaysia 18 17

Colombia -- 27 Algeria -- --

Mauritius -- -- Indonesia -- --

Mexico 23 21 Egypt 21 18Sources: USDA attached reports, F.O. Licht, PROMAR International

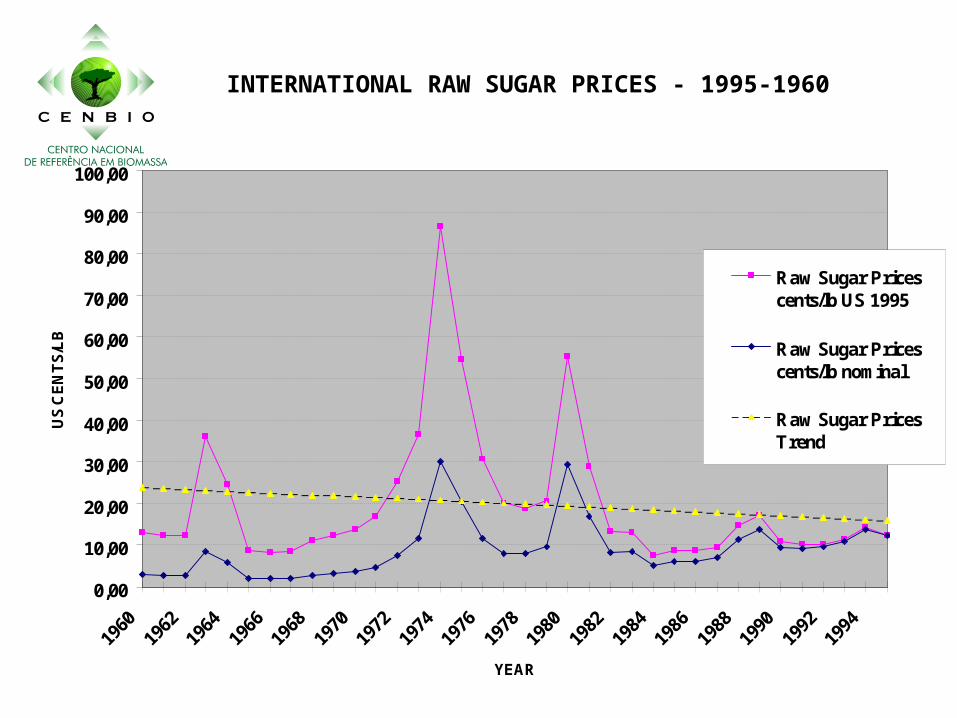

Sugar Prices in the Leading Sugar Trading Nations

Net Exporters Net Importers (U.S. cents per pound of white sugar)

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

90,00

100,00

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

YEAR

US

CE

NT

S/L

B

Raw Sugar Pricescents/lb US 1995

Raw Sugar Pricescents/lb nominal

Raw Sugar PricesTrend

INTERNATIONAL RAW SUGAR PRICES - 1995-1960

0,00

10,00

20,00

30,00

40,00

50,00

60,00

70,00

80,00

90,00

YEAR

US

$/B

L

GasolinePrices US$/blUS$ 1995

GasolinePricesCurrentUS$/bl

GasolinePrices Trend

GASOLINE PRICES IN ROTERDAN

GASOLINE PRICES IN USA AND BRAZIL, AND ETHANOL PRICES IN BRAZIL

0.605 0.665

0.988

0.5860.710

0.7900.859

0.7320.888

0

0.2

0.4

0.6

0.8

1

1.2

Refinery

gate

199

9

Refinery

gate

200

0

Competit

ive P

rice U

SA-Conv.

Eng.

Competiv

e Pric

e USA-H

igh C

omp. E

ng.

Refinery

gate

200

1

Competiv

e Pric

e BRAZI

L-Conv.

Eng.

Competit

ive P

rice B

RAZIL-H

igh c

omp. E

ng.

Hydra

ted p

rice a

t mill

-200

1

Potentia

l Anhyd

rous p

rice a

t mill

-200

1

US$/gallon

GAS USA

ETHANOL

GAS BRAZIL

ETHANOL 2001

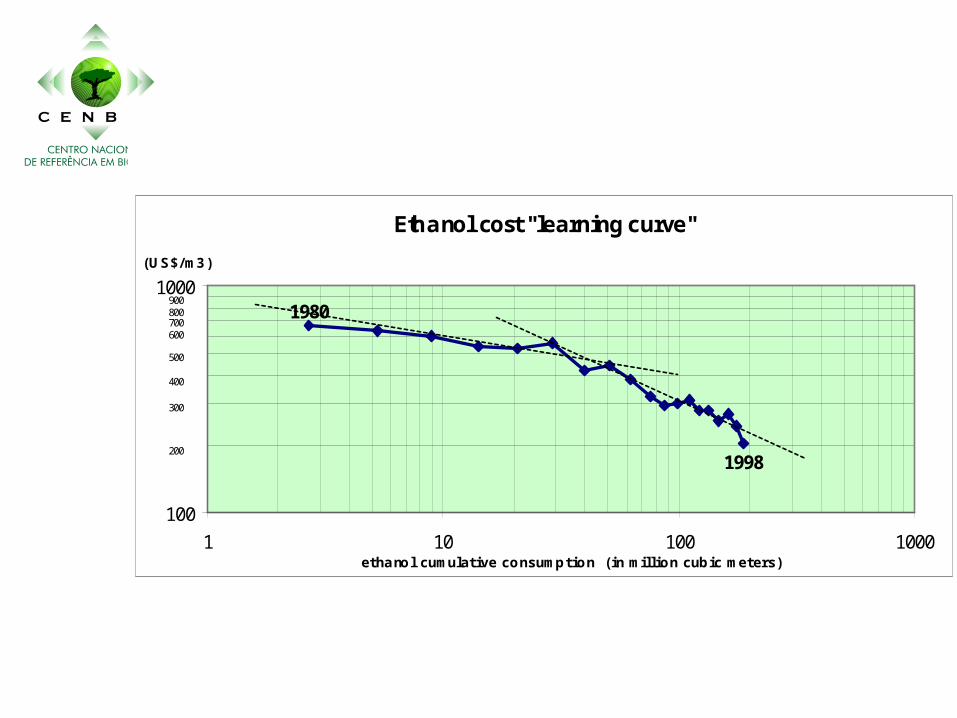

Ethanol cost "learning curve"

100

1000

1 10 100 1000e t ha no l c umulat ive c o ns ump t io n ( in millio n c ub ic me t e rs )

( US $/ m3 )

1980

1998200

300

400

500

600700800900

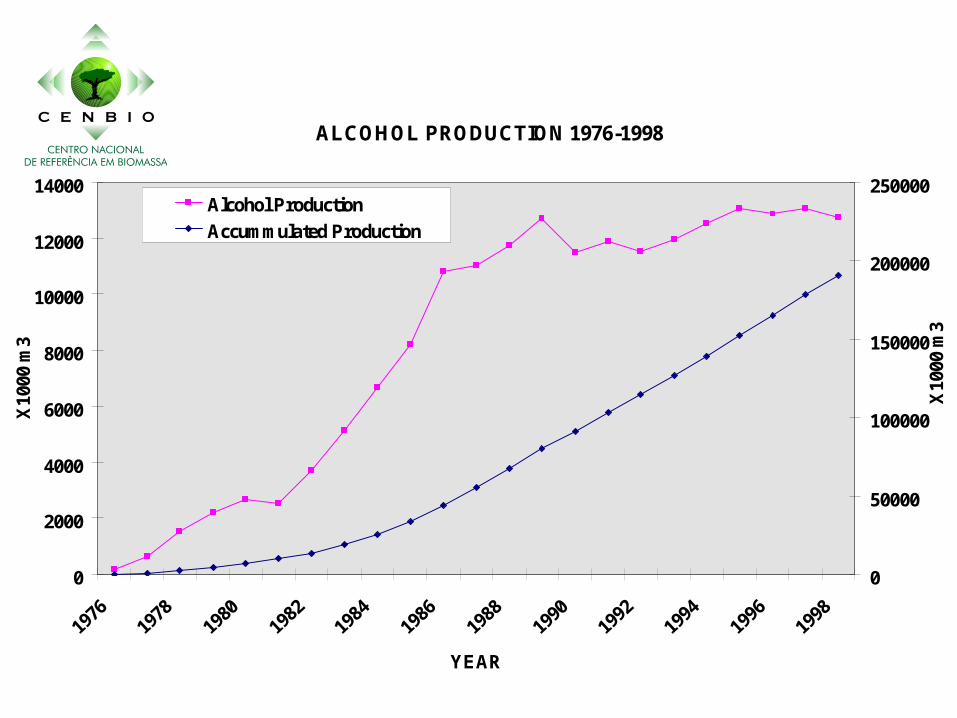

ALCOHOL PRODUCTION 1976-1998

0

2000

4000

6000

8000

10000

12000

14000

19761978

19801982

19841986

19881990

19921994

19961998

YEAR

X10

00 m

3

0

50000

100000

150000

200000

250000

X10

00 m

3

Alcohol Production

Accummulated Production

Carbon Credit Value:Two Scenarios

0

100

200

300

400

500

600

2003

2005

2007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

Year

US

$/t

C

High Price

Low Price

SMALL HYDRO PROJECT Internal Rate of Return

0%

2%

4%

6%

8%

10%

12%

14%

16%

No CarbonCredits

Low Price High Price

0

200

400

600

800

1000

1200

1400

1600

1800

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YEAR

MtC

Fuel+Elect. Cummulative(MtC)

Fuel Cummulative (MtC)

Elect. Cummulative (MtC)

POTENTIAL C ABATEMENT FROM THE USE OF SUGARCANE FOR FUEL AND ELECTRICITY

PRODUCTION - BRAZIL - 13 MILLION HA

0

20

40

60

80

100

120

140

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

YEAR

C Abatement/Area Sugarcane(tC/há)

AREA (Mha)

Cummulative C Abatement/AreaForest Sink (tC/há)

POTENTIAL CARBON ABATEMENT PER UNIT OF HARVESTED AREA - SUGARCANE - BRAZIL - 13 MHA

EXTERNAL DEBT IMPACT OF ALCOHOL EXPORTATION BRAZIL - 1979/1992

02 04 06 08 0

1 0 01 2 01 4 01 6 0

7 8 7 9 8 0 8 1 8 2 8 3 8 4 8 5 8 6 8 7 8 8 8 9 9 0 9 1 9 2

Y E A R

US$ B

illio

n E x t . d e b t

E x t . D e b t w . E th a n .

E x p . E th a n o l

E x p o r ta t io n

EXTERNAL DEBT IMPACT OF ALCOHOL EXPORTATION

BRAZIL 1979/1992

EXTERNAL DEBT WITH AND WITHOUT SUGARCANE EXPORTATION FOR BRAZIL - 13 MILLION HA 1994-2020

0

100

200

300

400

500

600

700

800

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

2015

2017

2019

YEAR

BIL

LIO

N U

S$

Ext. Debt CV

Ext. Deb. Ethanol Exp CV

Ext. Deb. Ethanol Exp. LowInterest CV

Ethanol Export.