macroeconomic performance nbba post budget critique.doc - copy

TRANSCRIPT

i

qwertyuiopasdfghjklzxcvbnmqwertyuiopasqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmrtyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmqwertyuiopasdfghjklzxcvbnmrtyuiopasdfghjklzxcvbnmqwertyuiopa

UNITED REPUBLIC OF TANZANIA MINISTRY OF FINANCE AND ECONOMIC AFFAIRS

AN OVERVIEW OF MACROECONOMIC PERFORMANCE OF TANZANIA FOR THE PAST THREE YEARS

PAPER PRESENTED AT THE SEMINAR ON POST BUDGET

CRITIQUE AND PRE-BUDGET PROPOSALS FOR THE YEAR 2010/2011

By

Prof Handley Mpoki Mafwenga [PhD, MSc, PGDTM, ADTM]

Principal Finance Management Officer

JULY 2009

ii

Table of Contents

INTRODUCTION 1 OVERVIEW OF MACROECONOMIC PERFORMANCE FOR THE PAST THREE YEARS 2

2.1 GDP Growth 2 2.2 Inflation 3 Government Budget 4

Revenue 4 Expenditure 4

National Debt 6 2.4 External Sector 7 2.5 Money and Credit Developments 10

Money Supply 10 Credit Developments 10 Interest Rates 11

Exchange Rate 12 Foreign Reserves 12 Foreign Direct Investment 13

EMERGING MACROECONOMIC POLICY ISSUES AND CHALLENGES 14

3.1 Global Economic Crisis and the Economy 14 3.2 Fiscal Stimulus Initiatives in FY2009/10 15

MEDIUM-TERM MACROECONOMIC FRAMEWORK AND STRATEGIC DIRECTIONS 16

4.1 Growth Prospects 16 4.2 Medium Term Outlook 17

CONCLUSION 18

1

INTRODUCTION Tanzania’s macroeconomic performance continues to be strong in past three

years (2006, 2007 and 2008) despite major shocks caused by severe drought

experienced during 2005/06 rain season; high oil and fertilizer prices in 2007;

and the on-going financial and economic crisis, which has weakened

economic growth prospects for 2009 with the expected reduced demand for

our exports, lowering prices for primary commodities, tourism earnings and

contracting investment inflows. These developments have put pressure on

external balance of payments, exchange rate and official foreign exchange

reserves.

As a response to these challenges, the Government has taken several policy

measures to cushion the economy from further slide. Going forward, the

Government plan to further stimulate the economy through the budget for the

Financial Year 2009/10 to protect employment especially in sectors affected

with financial problems; taking precautions and mitigative measures due to

the global food shortage exacerbated by the crisis and bad weather; protect

basic social development programmes; and safeguard important investment

necessary for the country’s development. In line with mitigative measures,

the Government will remain focused on the raising long-term growth, expand

employment opportunities and empowerment programmes, reduce poverty

and promote regional development.

Notwithstanding these challenges, the Government remains committed to

attaining the goals of Tanzania National Development Vision 2025 and

National Strategy for Growth and Reduction of Poverty (MKUKUTA).

Tanzania’s economic foundation remains stable and supportive of accelerated

growth rates in the medium-to long term due to bold economic reforms

implemented in the recent past.

2

OVERVIEW OF MACROECONOMIC PERFORMANCE FOR THE PAST THREE YEARS Tanzania’s economic performance continues to be strong, despite the global

pressure on oil, food prices and economic recession. Economic growth has

been more resilient to shocks over three years with GDP growth averaging 7.0

percent between 2006 and 2008. This strong performance has been spurred

by sustained structural reforms coupled with prudent fiscal and monetary

policies and other interventions undertaken by the Government that have

focused on investment promotion, employment generation, export promotion,

infrastructure development, and human resource development.

2.1 GDP Growth

Tanzania continued to sustain good economic growth and macroeconomic

stability. During the year 2008, real GDP growth reached 7.4 percent

compared to actual growth rate of 7.1 percent and 6.7 percent in 2007 and

2006 respectively. The increase in economic growth rate was mainly

attributed to an increase in growth of agriculture; fishing and services

economic activities. The high growth rates were observed in communication

sub-activity; financial intermediation; and construction. However, industry

and construction contracted by 8.6 percent in 2008 compared with a growth

of 9.5 percent and 8.5 percent in 2007 and 2006 respectively. The share of

services to GDP increased by 43.7 percent in 2008 compared to 43.3 percent

in 2007 and 2006.

3

Source: National Bureau of Statistics

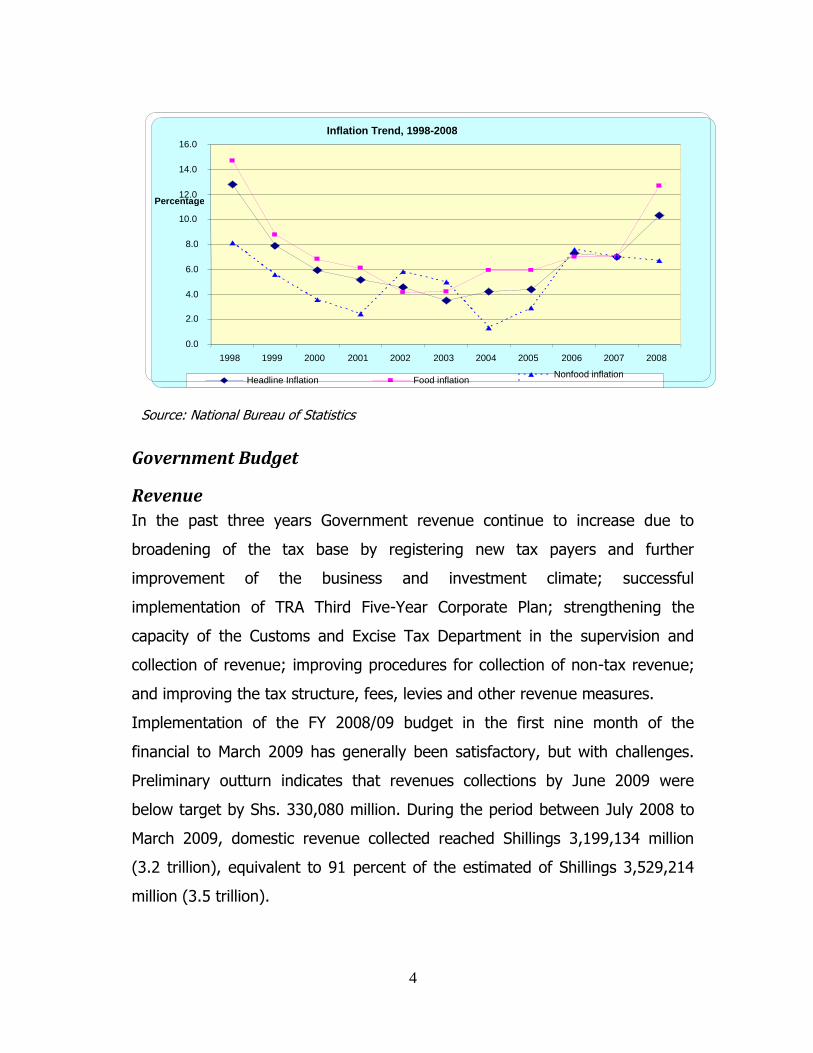

2.2 Inflation

Over the past decade, through reforms and stabilization measures,

Tanzania managed to subdue inflation to single digit levels. The recent upward

trend was however driven by pressures in the world oil and food prices leading

to double digit inflation level in 2008. The rate of inflation, as measured by the

Consumer Price Index (CPI), reached an annual average of 10.3% in 2008

compared to 7.0 percent and 7.3 percent recorded in 2007 and 2006

respectively. The high rate of inflation reflected rising power (electricity) tariffs

by a 21.7 percent as well as high world prices for oil and food stuffs. Annual

averaged food inflation was 12.7 percent while non-food inflation was 6.7

percent. Although world oil prices have fallen below their peak in 2008, the

local pump prices have not declined commensurately, thus triggering a

continued hike in food prices due high transport costs.

Real GDP Growth Rate, 2000, 4.9%

Real GDP Growth Rate, 2001, 6.0%

Real GDP Growth Rate, 2002, 7.2%

Real GDP Growth Rate, 2003, 6.9%

Real GDP Growth Rate, 2004, 7.8%

Real GDP Growth Rate, 2005, 7.4%

Real GDP Growth Rate, 2006, 6.7%

Real GDP Growth Rate, 2007, 7.1% Real GDP Growth Rate, 2008, 7.4%

Tsh

s. B

illio

n

GDP TREND (at Constant 2001 Prices)

Real GDP Real GDP Growth Rate

4

Source: National Bureau of Statistics

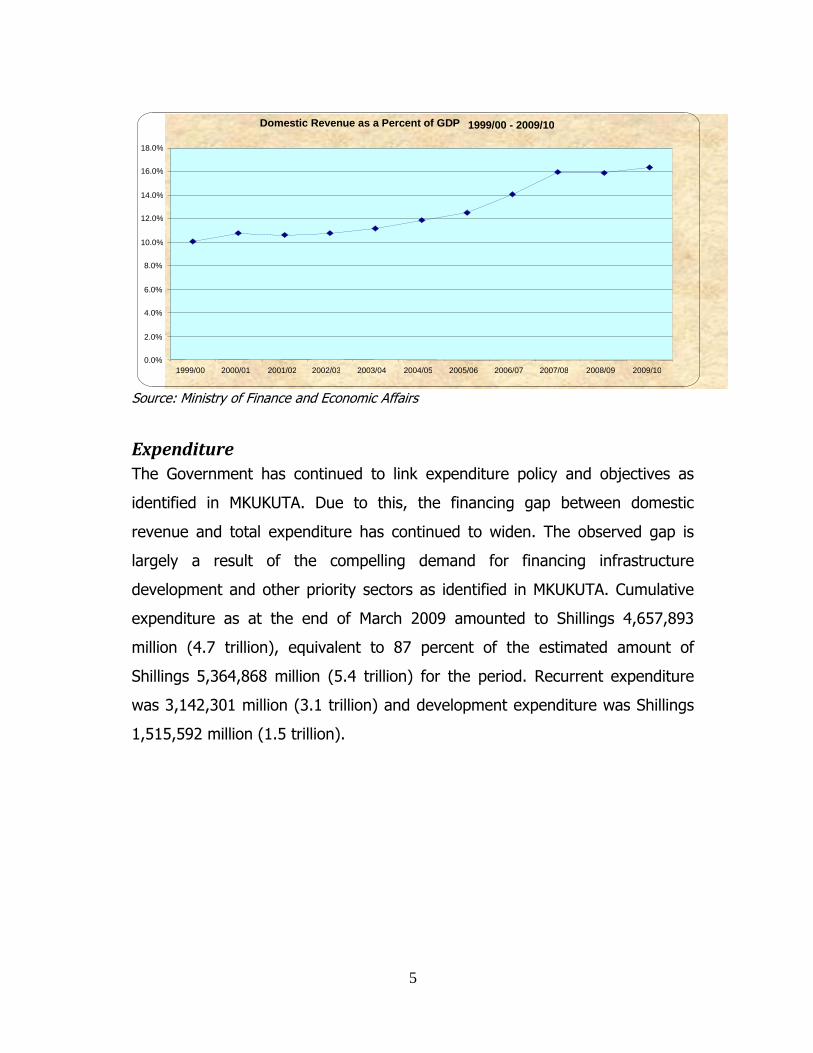

Government Budget

Revenue

In the past three years Government revenue continue to increase due to

broadening of the tax base by registering new tax payers and further

improvement of the business and investment climate; successful

implementation of TRA Third Five-Year Corporate Plan; strengthening the

capacity of the Customs and Excise Tax Department in the supervision and

collection of revenue; improving procedures for collection of non-tax revenue;

and improving the tax structure, fees, levies and other revenue measures.

Implementation of the FY 2008/09 budget in the first nine month of the

financial to March 2009 has generally been satisfactory, but with challenges.

Preliminary outturn indicates that revenues collections by June 2009 were

below target by Shs. 330,080 million. During the period between July 2008 to

March 2009, domestic revenue collected reached Shillings 3,199,134 million

(3.2 trillion), equivalent to 91 percent of the estimated of Shillings 3,529,214

million (3.5 trillion).

Inflation Trend, 1998-2008

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Percentage

Headline Inflation Food inflation Nonfood inflation

5

Source: Ministry of Finance and Economic Affairs

Expenditure

The Government has continued to link expenditure policy and objectives as

identified in MKUKUTA. Due to this, the financing gap between domestic

revenue and total expenditure has continued to widen. The observed gap is

largely a result of the compelling demand for financing infrastructure

development and other priority sectors as identified in MKUKUTA. Cumulative

expenditure as at the end of March 2009 amounted to Shillings 4,657,893

million (4.7 trillion), equivalent to 87 percent of the estimated amount of

Shillings 5,364,868 million (5.4 trillion) for the period. Recurrent expenditure

was 3,142,301 million (3.1 trillion) and development expenditure was Shillings

1,515,592 million (1.5 trillion).

Domestic Revenue as a Percent of GDP 1999/00 - 2009/10

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

1999/00 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10

6

Source: Ministry of Finance and Economic Affairs

National Debt

Despite the increase in the national debt, the trend shows that Tanzanian debt

is still sustainable. As at December, 2008, the National Debt was USD 6,329

million compared to USD 5,891.9 million in December 2007. This is equivalent

to 32.6 percent of GDP compared to 31.8 percent in 2007. Out of that amount,

external debt amounted to USD 4,822.0 million, while domestic debt was USD

1,507 million, equivalent to Shs. 1,929.3 billion. The external debt increased by

14.3 percent compared to USD 4,218.5 million in 2007. The increase in external

debt was largely due to accumulation of interest arrears, particularly for the

Non- Paris Club Member Countries, depreciation of the shilling and newly

contracted loans. Domestic debt for the period increased by Shs. 35 billion,

equivalent to an increase of 1.8 percent, compared to the period ending

December 2007.

Resource Gap, 1999/00-2009/10

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

1999/00 2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10

TSh Millions

Domestic revenue Total Expenditure (excl. Amortization)

Resource Gap

7

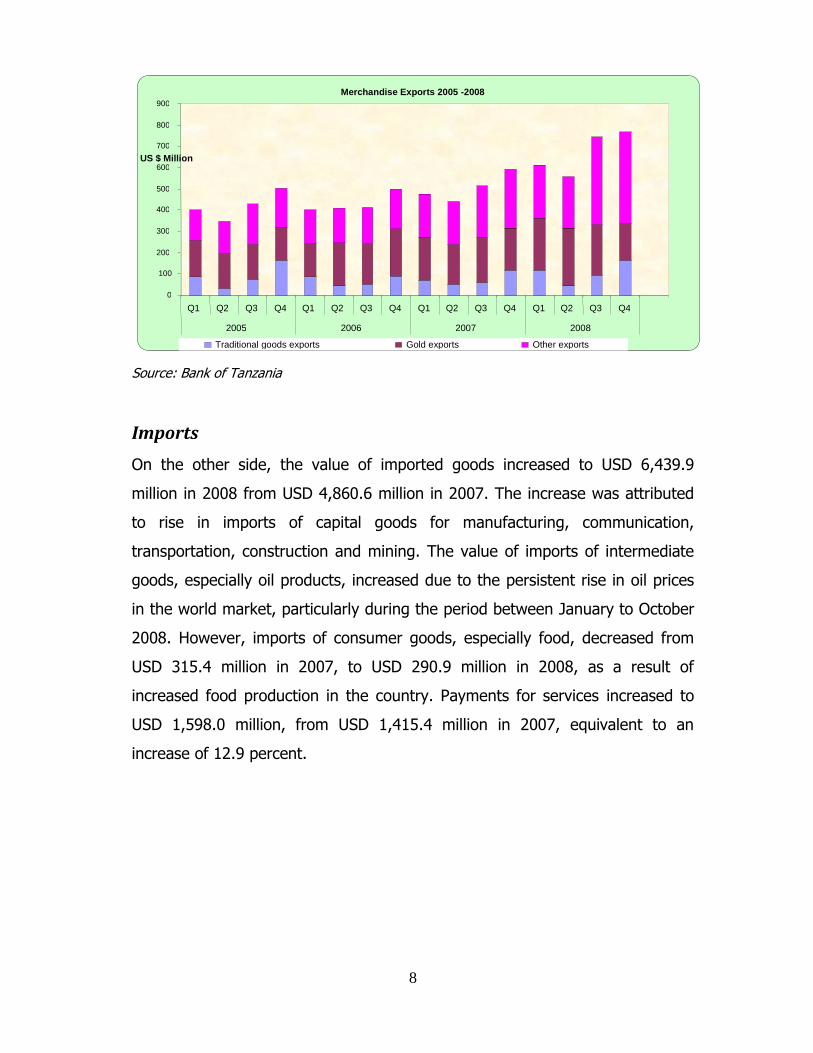

2.4 External Sector

Exports

The country’s balance on goods and services account has continued to worsen

due to an increase in imports over exports. Total export earnings (goods and

services) increased by 36.4 percent to USD 3,036.7 million from USD 2,226.6

million in 2007. The increase was mainly attributed to an increase in the export

of both traditional non-traditional goods. The value of traditional exports

including cotton, tea, tobacco, cashewnuts, coffee, sisal, and cloves increased

to USD 418.4 million in 2008, compared to USD 319.7 million in 2007. The

value of non - traditional exports was USD 2,270.6 million in 2008, compared

to USD 1,704.5 million in 2007, equivalent to an increase of 28.8 percent. The

increase was mainly attributed to the increase in exports of manufactured

goods, particularly cotton yarn and sisal products. The value of manufactured

exports increased by 113.8 percent, from USD 309.8 million in 2007 to USD

662.3 million in 2008. Likewise, receipts from service exports including tourism,

transport and others increased to USD 2,168.9 million, from USD 1,875.7

million in 2007, equivalent to an increase of 15.6 percent. In addition, during

2008, the value of exports to the European Union (EU) and Switzerland

increased by 26.1 percent; to the East African Community (EAC) by 82.6

percent; to SADC countries by 47.3 percent; and to other African countries by

56.4 percent. The value of goods exported to China, Japan, India, Hong Kong

and United Arab Emirates increased by 61.5 percent and to the Americas by

51.1 percent.

8

Source: Bank of Tanzania

Imports

On the other side, the value of imported goods increased to USD 6,439.9

million in 2008 from USD 4,860.6 million in 2007. The increase was attributed

to rise in imports of capital goods for manufacturing, communication,

transportation, construction and mining. The value of imports of intermediate

goods, especially oil products, increased due to the persistent rise in oil prices

in the world market, particularly during the period between January to October

2008. However, imports of consumer goods, especially food, decreased from

USD 315.4 million in 2007, to USD 290.9 million in 2008, as a result of

increased food production in the country. Payments for services increased to

USD 1,598.0 million, from USD 1,415.4 million in 2007, equivalent to an

increase of 12.9 percent.

Merchandise Exports 2005 -2008

0

100

200

300

400

500

600

700

800

900

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2005 2006 2007 2008

US $ Million

Traditional goods exports Gold exports Other exports

9

Source: Bank of Tanzania

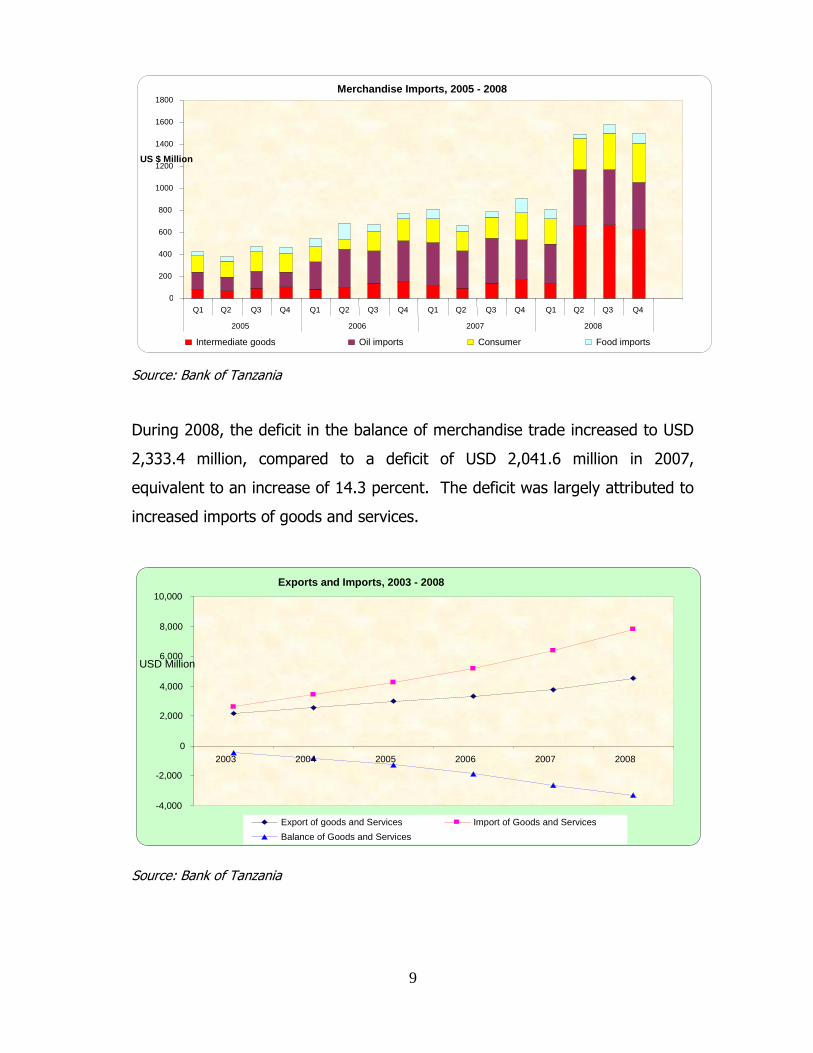

During 2008, the deficit in the balance of merchandise trade increased to USD

2,333.4 million, compared to a deficit of USD 2,041.6 million in 2007,

equivalent to an increase of 14.3 percent. The deficit was largely attributed to

increased imports of goods and services.

Source: Bank of Tanzania

Merchandise Imports, 2005 - 2008

0

200

400

600

800

1000

1200

1400

1600

1800

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 2005 2006 2007 2008

US $ Million

Intermediate goods Oil imports Consumer Food imports

Exports and Imports, 2003 - 2008

-4,000

-2,000

0

2,000

4,000

6,000

8,000

10,000

2003 2004 2005 2006 2007 2008

USD Million

Export of goods and Services Import of Goods and Services Balance of Goods and Services

10

2.5 Money and Credit Developments

Money Supply

In the year ending December, 2008, broad money supply (M2)1 grew by 29.7

percent, compared to 27.0 percent and 24.5 percent in December 2007 and

2006 respectively. The broad extended money supply (M3) grew by 24.0

percent for the period ending December 2008, compared to 21.4 percent and

24.2 percent in December, 2007 and 2006 respectively. The increase in M2 was

attributed to the increase in commercial bank credit to the private sector as

well as an increase in special demand deposits.

Credit Developments

There has been substantial expansion of financial sector over the years and

currently 36 commercial banks and 18 insurance companies are operating in

the country. The expansion in the banking sector has led to expansion of credit

to private sector growing at a above 35 percent per annum. This mainly

reflects Government efforts to reduce domestic borrowing for financing the

budget and promotion of a conducive environment for private sector

participation in economic activities. Credit extended to the private sector

increased to Shs. 4,376.4 billion in the year ending December, 2008 compared

to Shs. 2,976.3 billion extended in December, 2007, equivalent to an increase

of 47.0 percent. The increase in credit is largely due to Government reduction

in domestic bank borrowing, increased compliance in repayment of loans,

increase in credit guarantee schemes as well as an increase in corporate

borrowing. Most of the credit was extended to trade (16.1 percent);

manufacturing (13.1 percent); transport and communication (8.7 percent);

agriculture (8.3 percent); and private credit by (19.6 percent).

1 M0 is currency in circulation outside the banking system

M1 = M0 + Demand Deposits

M2 = M1 + Time and Savings Deposits

M3 = M2 + Foreign Currency Deposits

11

Source: Bank of Tanzania

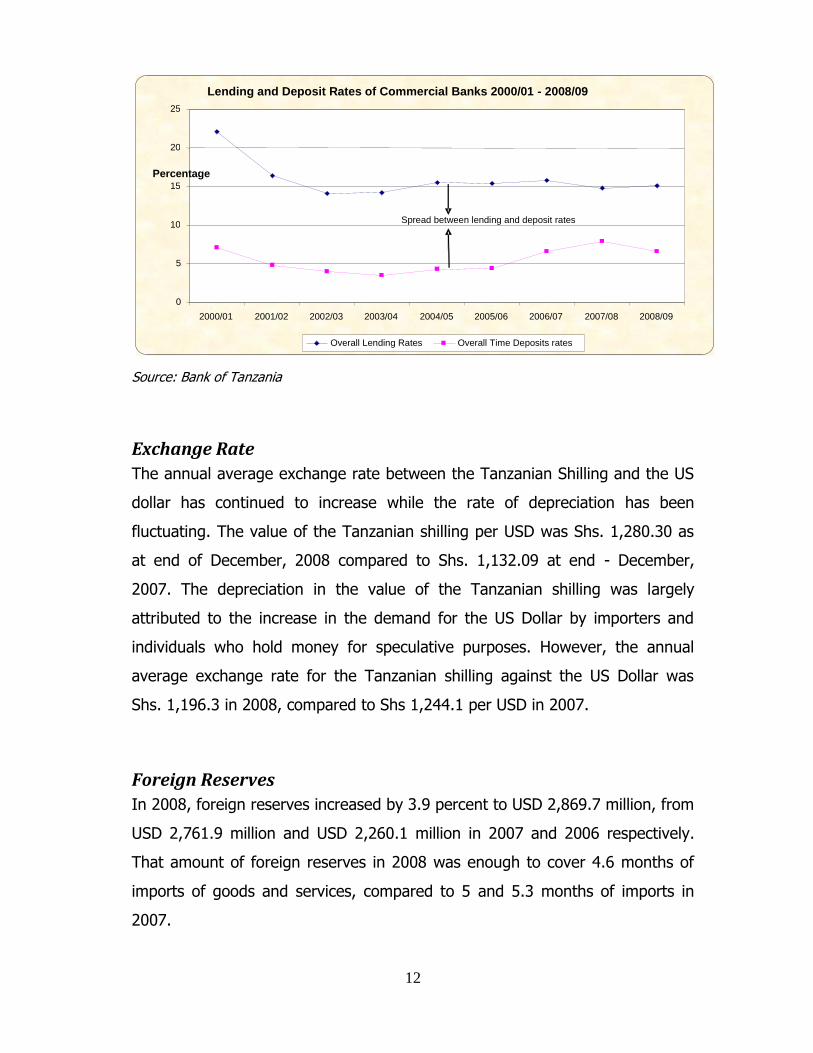

Interest Rates

There has been a notable narrowing in the spread between lending and deposit

rates of commercial banks between 2006/07 – 2008/09. This partly indicates

that commercial banks are gradually building confidence in their borrower and

it also reflects reduction of risk due to Government efforts to guarantee

commercial banks against risky borrowers, particularly for agricultural activities.

The average interest rate offered by various commercial banks continued to

exhibit wide interest rates spreads. The average lending rates by commercial

banks increased from 15.25 percent in December, 2007 to 16.05 percent in

December, 2008. Likewise, the interest rates on deposits increased from 2.65

in December, 2007 to 2.68 in December, 2008.

Commercial Banks Credit to Private Sector - April, 2009

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

Jun-97 Jun-98 Jun-99 Jun-00 Jun-01 Jun-02 Jun-03 Jun-04 Jun-05 Jun-06 Jun-07 Jun-08 Apr-09

Tshs. Billion

0%

10%

20%

30%

40%

50%

60%

Credit to private sector (TShs) Growth of credit to private sector

12

Source: Bank of Tanzania

Exchange Rate

The annual average exchange rate between the Tanzanian Shilling and the US

dollar has continued to increase while the rate of depreciation has been

fluctuating. The value of the Tanzanian shilling per USD was Shs. 1,280.30 as

at end of December, 2008 compared to Shs. 1,132.09 at end - December,

2007. The depreciation in the value of the Tanzanian shilling was largely

attributed to the increase in the demand for the US Dollar by importers and

individuals who hold money for speculative purposes. However, the annual

average exchange rate for the Tanzanian shilling against the US Dollar was

Shs. 1,196.3 in 2008, compared to Shs 1,244.1 per USD in 2007.

Foreign Reserves

In 2008, foreign reserves increased by 3.9 percent to USD 2,869.7 million, from

USD 2,761.9 million and USD 2,260.1 million in 2007 and 2006 respectively.

That amount of foreign reserves in 2008 was enough to cover 4.6 months of

imports of goods and services, compared to 5 and 5.3 months of imports in

2007.

Lending and Deposit Rates of Commercial Banks 2000/01 - 2008/09

0

5

10

15

20

25

2000/01 2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09

Percentage

Overall Lending Rates Overall Time Deposits rates

Spread between lending and deposit rates

13

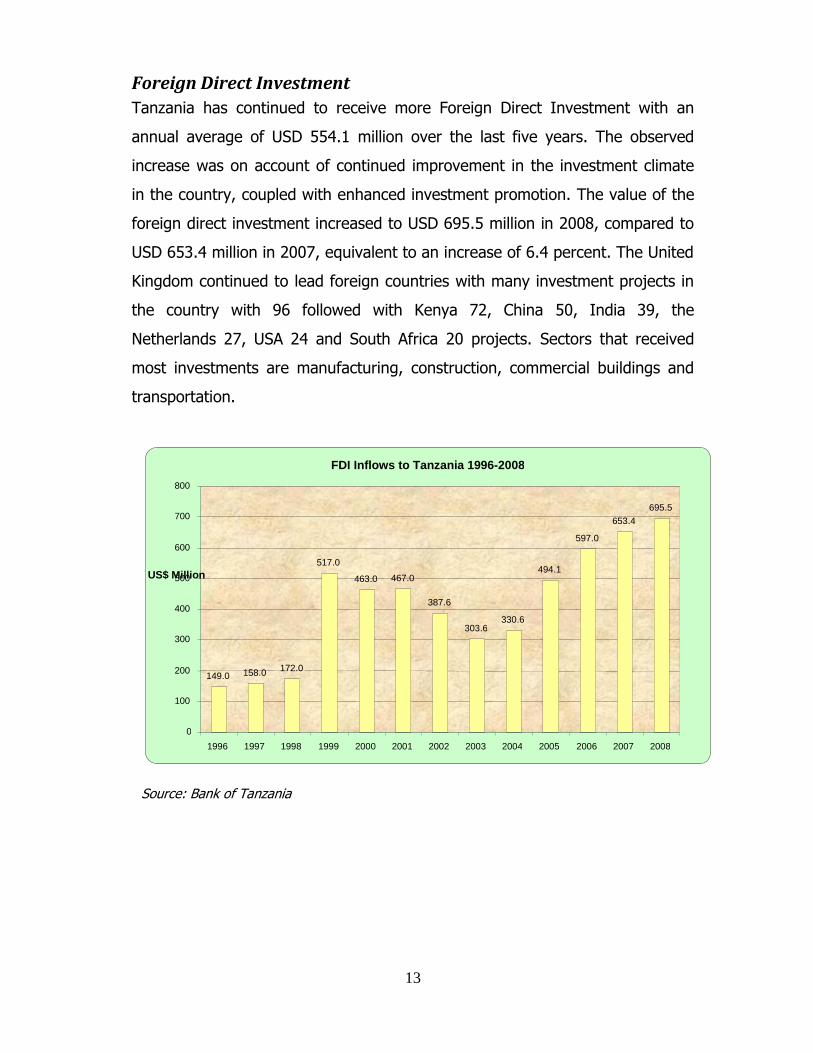

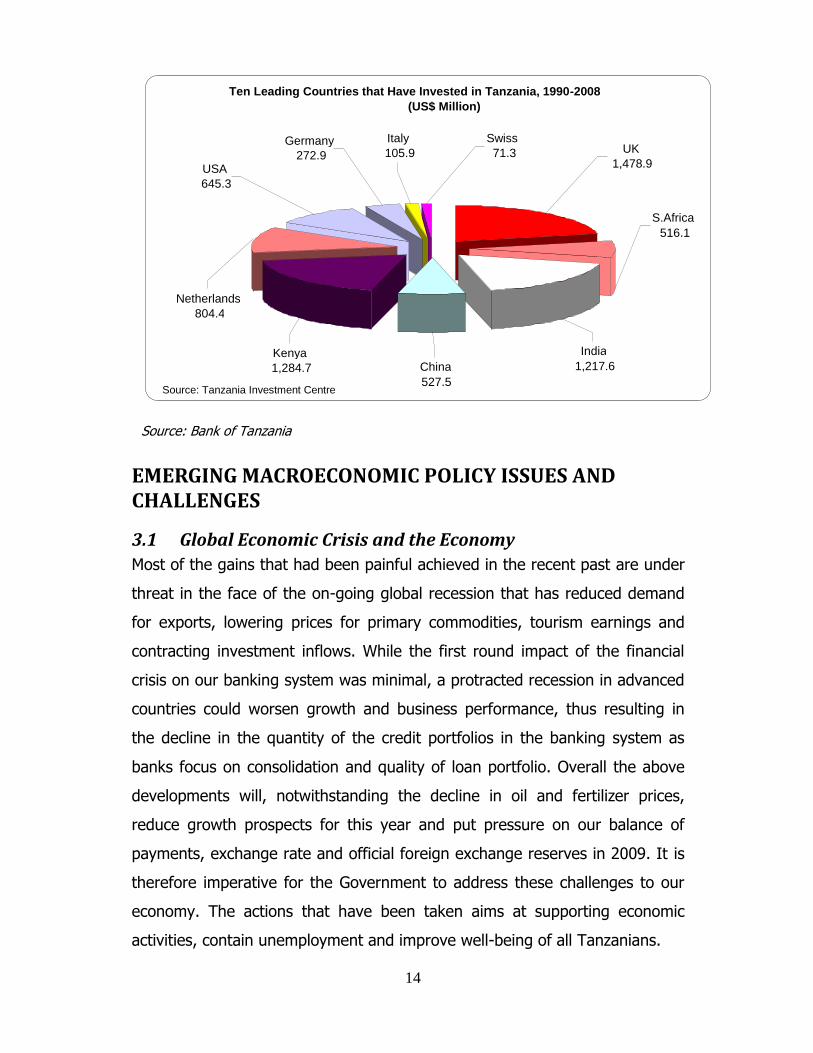

Foreign Direct Investment

Tanzania has continued to receive more Foreign Direct Investment with an

annual average of USD 554.1 million over the last five years. The observed

increase was on account of continued improvement in the investment climate

in the country, coupled with enhanced investment promotion. The value of the

foreign direct investment increased to USD 695.5 million in 2008, compared to

USD 653.4 million in 2007, equivalent to an increase of 6.4 percent. The United

Kingdom continued to lead foreign countries with many investment projects in

the country with 96 followed with Kenya 72, China 50, India 39, the

Netherlands 27, USA 24 and South Africa 20 projects. Sectors that received

most investments are manufacturing, construction, commercial buildings and

transportation.

Source: Bank of Tanzania

FDI Inflows to Tanzania 1996-2008

149.0 158.0 172.0

517.0 463.0 467.0

387.6

303.6 330.6

494.1

597.0 653.4

695.5

0

100

200

300

400

500

600

700

800

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

US$ Million

14

Source: Bank of Tanzania

EMERGING MACROECONOMIC POLICY ISSUES AND CHALLENGES

3.1 Global Economic Crisis and the Economy

Most of the gains that had been painful achieved in the recent past are under

threat in the face of the on-going global recession that has reduced demand

for exports, lowering prices for primary commodities, tourism earnings and

contracting investment inflows. While the first round impact of the financial

crisis on our banking system was minimal, a protracted recession in advanced

countries could worsen growth and business performance, thus resulting in

the decline in the quantity of the credit portfolios in the banking system as

banks focus on consolidation and quality of loan portfolio. Overall the above

developments will, notwithstanding the decline in oil and fertilizer prices,

reduce growth prospects for this year and put pressure on our balance of

payments, exchange rate and official foreign exchange reserves in 2009. It is

therefore imperative for the Government to address these challenges to our

economy. The actions that have been taken aims at supporting economic

activities, contain unemployment and improve well-being of all Tanzanians.

Ten Leading Countries that Have Invested in Tanzania, 1990-2008 (US$ Million)

UK 1,478.9

S.Africa 516.1

India 1,217.6 China

527.5

Kenya 1,284.7

Netherlands 804.4

USA 645.3

Germany 272.9

Italy 105.9

Swiss 71.3

Source: Tanzania Investment Centre

15

3.2 Fiscal Stimulus Initiatives in FY2009/10

In the face of unfavorable global economic environment and the need to

protect the livelihood of the poor and create employment, the Government

budget has outlined key actions to boost economic recovery to the growth

trajectory envisaged under the Vision 2025. This will be done through a fiscal

stimulus package that is more targeted, flexible and sufficient given the

magnitude of the likely impact of the crisis on our economy. Key element of the

proposed stimulus package includes:

To compensate the losses incurred by the buyers of crops during the

fiscal year 2008/09, including cooperatives and private companies which

sold cotton and coffee products at a loss;

Rescheduling of outstanding loans;

To provide working capital at concessional terms. Under the plan, the

Government will provide soft loan facilities for on-lending to businesses

whose operations have been adversely affected by the economic crisis;

To strengthen the Export Credit Guarantee Scheme (ECGS) and the

Small and Medium Enterprises (SMEs) Guarantee Scheme;

Import farm implement in order to improve production and productivity

in the agriculture sector;

Extending a loan to Artumas to enable the company to continue with

power generation project for Mtwara and Lindi regions to improve power

generation in those regions;

Seeking loans from multilateral and bilateral development partners to

finance operations of Tanzania Rail Limited (TRL); and

Establish special docks in the ports with required facilities for handling

cruise liners in order to encourage such vessels carrying tourists to make

stopovers in our country.

16

MEDIUM-TERM MACROECONOMIC FRAMEWORK AND STRATEGIC DIRECTIONS

4.1 Growth Prospects

The on-going global economic recession is expected to reduce demands for

exports, receipts from tourism and remittance, and capital inflows. It will also

lead to a decline in world prices of key export commodities, hence worsening

Tanzania’s terms of trade. While the Government has taken measures in

terms of the stimulus package to mitigate these challenges, growth prospects

in 2009 and the medium-term is likely to be reduced if the recovery in global

economy is protracted. In the midst of less favourable external environment,

real GDP growth is expected to slow down to 5.0 percent in 2009 from 7.4 in

2008. However, the impact of this crisis is assumed to be short-lived, and

thus, real GDP growth is expected to rebound thereafter. The

macroeconomic projections and policy targets for the period 2009/10–

2011/12 are as follows:

(i) Attain a real GDP growth rate of 5.0 percent in 2009, 5.7 percent in

2010, 7.2 percent in 2011 and 7.5 percent by 2012;

(ii) Control Inflation at below 10.0 percent by end-June, 2010;

(iii) Increase domestic revenue collection to equivalent of 15.9 percent of

GDP expected in 2009/10, 16.4 percent in 2009/10, 17.2 percent in

2010/11 and 18.3 in 2011/12;

(iv) Contain the growth rate of money supply (M2) consistent with GDP

growth and inflation targets;

(v) Maintain adequate official foreign reserves sufficient to cover a minimum

of five months worth of imports of goods and non-factor service;

(vi) Maintain a market determined realistic exchange rate; and

(vii) Remove bottlenecks in the financial sector in order to facilitate credit

availability to the private sector.

17

4.2 Medium Term Outlook

Looking further ahead, it is expected that a global economic will recover

sooner than later with the on-going actions to stabilize the financial markets

and resuscitate growth in advanced countries. On the domestic fronts, in the

medium-term, key macroeconomic strategic directions will focus on:

(a) Accelerating and sustaining economic growth through

macroeconomic stability and strengthening the financial sector to

ensure low but stable interest rates, a low inflation and a stable

currency;

(b) To increase investments in areas which have sectoral linkages,

particularly agriculture, infrastructure, manufacturing and energy,

as well as enhancing participation of the private sector in those

areas;

(c) To increase availability of credit facilities particularly for the

agriculture sector by establishing an agricultural bank and a bank

for women;

(d) To improve collection of domestic revenue in order to meet a bigger

portion of government expenditure and enhance accountability in

the use and management of public funds;

(e) To improve economic empowerment programmes and increase

employment generation; and

(f) To finalize the survey of village lands.

18

CONCLUSION The world economy is in a severe recession since World War II, following the

negative impact of the second and third wave of global financial crisis.

Despite the various policy measures including fiscal stimulus plans and

liquidity injections by advanced countries, financial strain remain acute,

impacting negatively on the real economy. The negative impact of global

recession will also be felt in Sub-Saharan Africa, Tanzania included. Looking

at the recent global developments, we note that economic foundation laid in

the past has not been eroded is still intact. What we need is to gather

courage, adopt a positive spirit, and commit ourselves to moving forward.

Above all, we should find strength, unity of purpose and resolve to urgently

and decisively confront the immediate challenges facing us, while at the

same time focusing on our long-term growth and development objectives in

line with Vision 2025. In order to reduce the suffering to the people from the

impact of the global economic recession, the Government will remain focused

on the raising long-term growth, expand employment opportunities and

empowerment programmes, reduce poverty and promote regional

development.