morgan stanley mufg for the teleconference, 28th july · pdf file ·...

TRANSCRIPT

JFE GroupCapturing Growth Opportunities

in Greater East Asian Market

JFE Holdings, Inc.July 2010

1

Morgan Stanley MUFG for the Teleconference,Morgan Stanley MUFG for the Teleconference,2828thth July 2010July 2010

2

Contents

1. Financial Results for the First Quarter

ending March 31, 2011…………………………………….3

2. Financial Forecast for the FY10 …………………………6

3. Interim Dividends…………………………………………11

4. Capturing Growth Opportunities in Greater East Asian

Market……………………………………………………..13

5. Appendix……………………..……………………………40

This presentation material is for information and discussion purposes only.Any statements in the presentation which are not historical facts are future projections based on certain assumptions and currently available information. Please note that actual performance may vary significantly due to various factors.

1.Financial Results for the First Quarter ending March 31, 2011

3

JFE Holdings

4

Financial Results for the First Quarter ending March 31, 2011

JFE Holdings

(billion yen)FY2009 FY2010Apr-Jun Apr-Jun

Net Sales 589 755 166Ordinary Profit -61 53 115

Other loss -6 -2 4Ordinary Profit -67 51 119

Extraordinary loss 0 -5 -5Income before income taxesand minority interests(loss) -67 46 113Tax expense and Minority

Interest 26 -18 -44Net Income(loss) -42 28 69

Change

5

Financial Results for the First Quarter ending March 31, 2011Sales/Recurring Profit by Business Segment

(billion yen)FY2009 FY2010Apr-Jun Apr-Jun

Steel 476 657 181Engineering 51 46 -5Shipbuilding 68 53 -16Urban Development 5 5 0LSI 5 6 1Eliminations and Corporate -17 -13 4

589 755 166Steel -77 46 123Engineering 0 -1 -1Shipbuilding 7 7 1Urban Development -0 -1 -1LSI -0 0 1Eliminations and Corporate 3 -1 -4

-67 51 119

Change

Net Sales

Ordinary Income

JFE Holdings

6

2. Financial Forecast for FY10

77

Financial Forecast for FY10

(billion yen)Change

Full Year Full Year (Y/Y)

Steel 2,281 2,960 679

Net Sales 2,844 3,420 576

Operating Income 89 230 141Steel 32 200 168

Ordinary Income 69 220 151

Net Income 46 120 74

FY10(e)FY09(A)

88

* Forex Rate : ¥90.0/US$ (c.f. FY09 avg.: ¥93/US$)

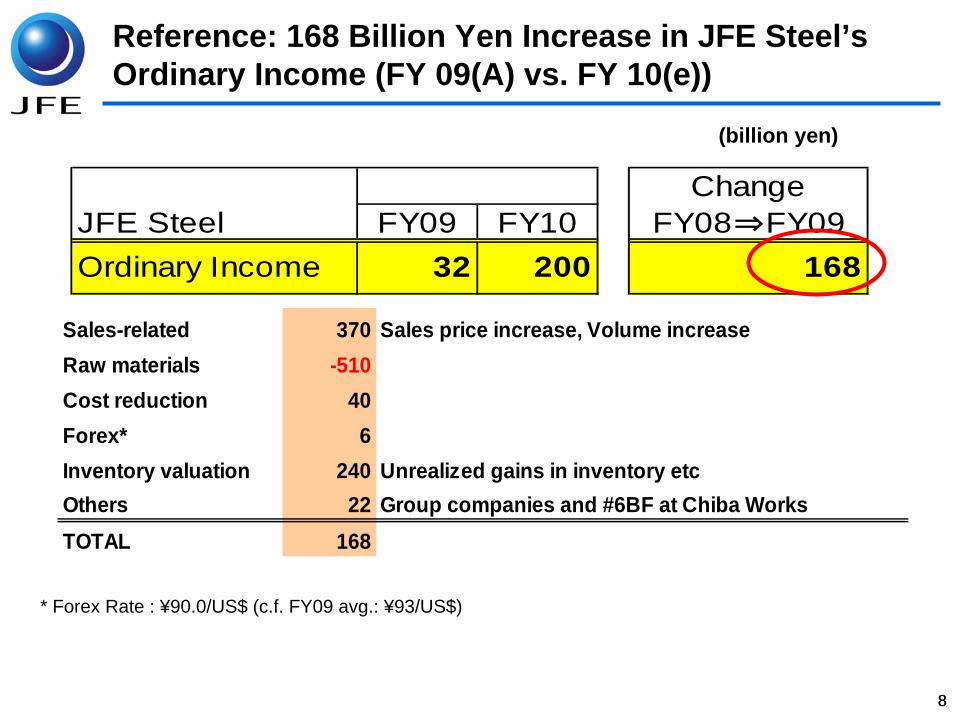

ChangeJFE Steel FY09 FY10 FY08⇒FY09Ordinary Income 32 200 168

Sales-related 370 Sales price increase, Volume increaseRaw materials -510Cost reduction 40Forex* 6Inventory valuation 240 Unrealized gains in inventory etcOthers 22 Group companies and #6BF at Chiba WorksTOTAL 168

Reference: 168 Billion Yen Increase in JFE Steel’s Ordinary Income (FY 09(A) vs. FY 10(e))

(billion yen)

9

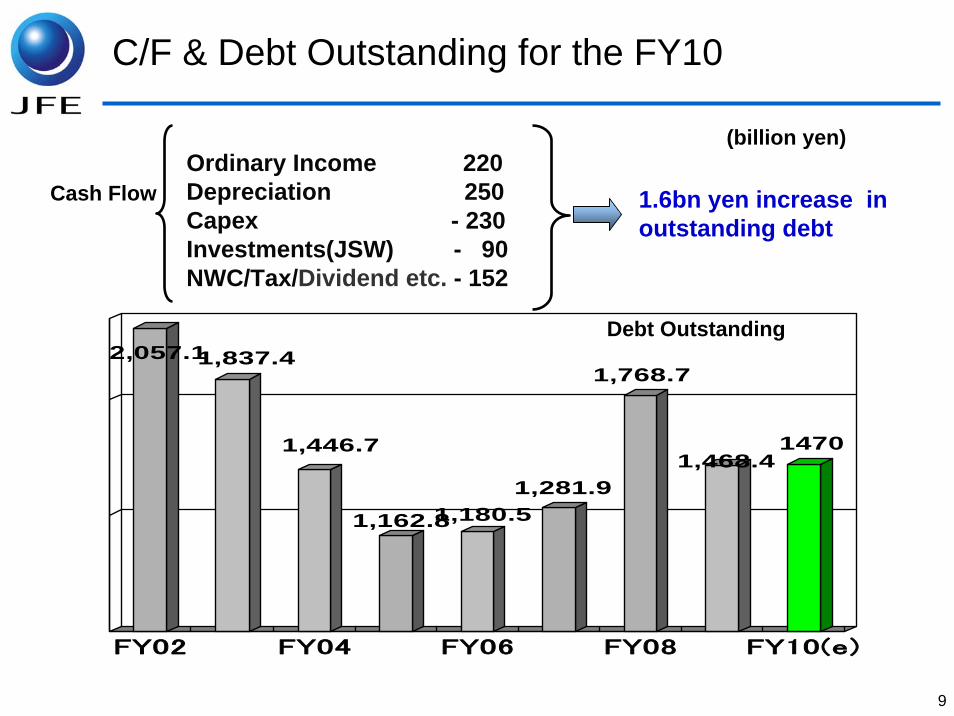

C/F & Debt Outstanding for the FY10

Ordinary Income 220Depreciation 250Capex - 230Investments(JSW) - 90NWC/Tax/Dividend etc. - 152

2,057.11,837.4

1,446.7

1,162.81,180.51,281.9

1,768.7

1,468.41470

FY02 FY04 FY06 FY08 FY10(e)

Cash Flow

Debt Outstanding

(billion yen)

1.6bn yen increase in outstanding debt

10

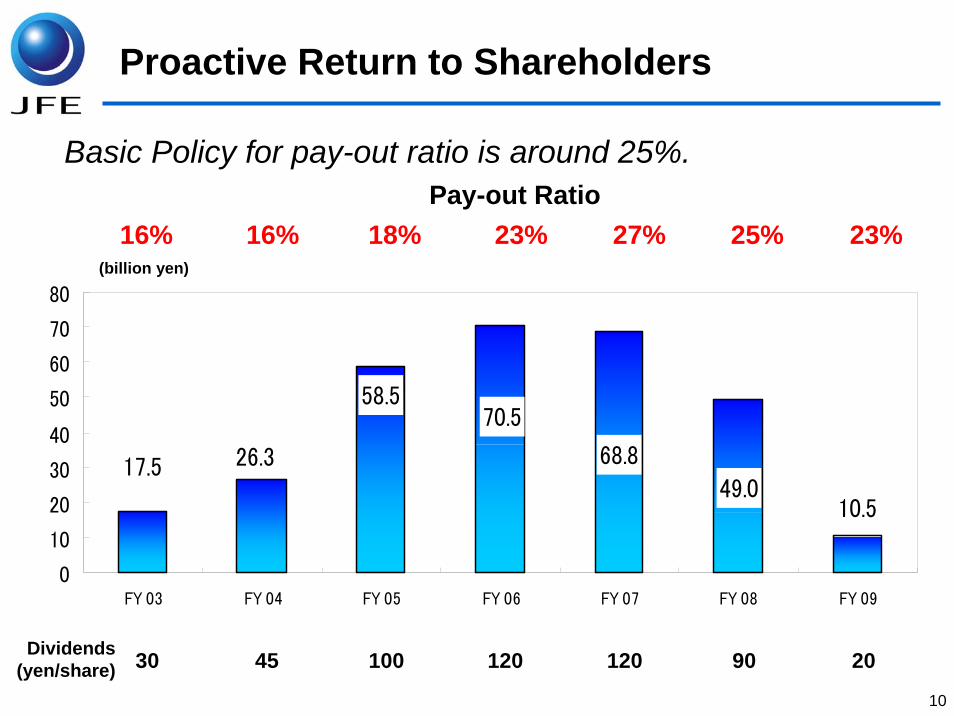

10.5

17.5 26.3

58.570.5

68.8

49.0

0

10

20

30

40

50

60

70

80

FY 03 FY 04 FY 05 FY 06 FY 07 FY 08 FY 09

Dividends(yen/share)

(billion yen)

30 45 100 120 120 90 20

Proactive Return to Shareholders

Pay-out Ratio16% 16% 18% 23% 27% 25% 23%

Basic Policy for pay-out ratio is around 25%.

3.Interim Dividend

11

12

Interim Dividend

The company intends to propose payment of an interim dividend of 20 yen per share for the current fiscal year.(Pay-out Ratio=21%)

Payment of an year-end dividend is not determined at this time.

13

4. Capturing Growth Opportunities in Greater East Asian Market

14

(1) Advantages of JFE Steel

1515

3.73.9

5.46.06.8

7.67.7

7.918.1

0.0 5.0 10.0 15.0 20.0

JFE Steel West Japan

Nippon Steel Kimitsu

JFE Steel East Japan

Nippon Steel Oita

Sumitomo Metals Kashima

Nippon Steel Nagoya

Kobe Steel Kakogawa

Sumitomo Wakayama

Nippon Steel Yawata

Million tons

Crude Steel Production by Steelworks in FY ended March 2010

Cost competitiveness of JFE Steel based on we have consolidated large steelworksat two location.

Sharing infrastructure, JFE’s steelworks are operated at energy-efficient way, need no transferring cost of slabs to the other works and fixed cost of those are relatively lower.

Advantages of JFE Steel (1):Economies of Scale

16

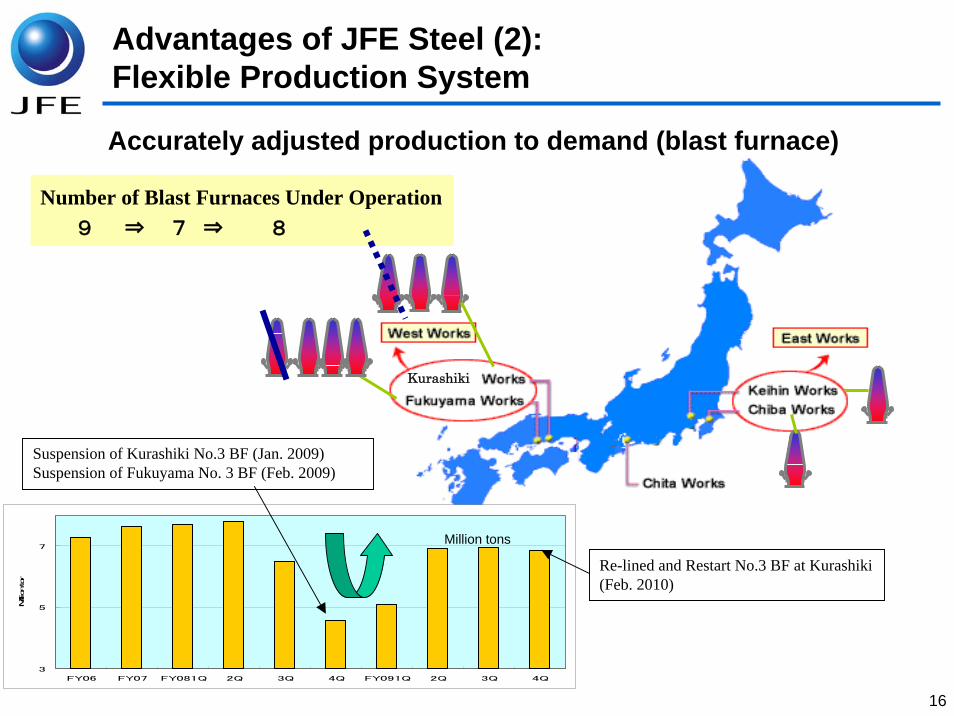

Number of Blast Furnaces Under Operation9 ⇒ 7 ⇒ 8

3

5

7

FY06 FY07 FY081Q 2Q 3Q 4Q FY091Q 2Q 3Q 4Q

Million ton

Suspension of Kurashiki No.3 BF (Jan. 2009)Suspension of Fukuyama No. 3 BF (Feb. 2009)

Kurashiki

Re-lined and Restart No.3 BF at Kurashiki (Feb. 2010)

Accurately adjusted production to demand (blast furnace)

Million tons

Advantages of JFE Steel (2):Flexible Production System

1717

Thailand10%

China18%

Other Asian22%

Other6%Americas

5%

S. Korea39%

Autos30%

Construction10%Shipbuilding

19%Machinery

8%

Containers 4%

Secondary processing

16%

Dealers13%

Advantages of JFE Steel (3): Stable Customer Bases both Domestic and Asia

FY 09

Domestic Shipments by Customer

Exports by Destination

Exports by Customer

Allied steelmakers43%

Contract customers(autos, appliances &

shipbuilding)32%

Only One and Number Oneproducts, etc. 25%

: Prices usually negotiated on annual basis. With the customer overseas, price negotiation be done mainly by semi-annual or quarterly basis.

Domestic45%

Exports 55%

18

Reference : Alliances with Overseas SteelmakersReference : Alliances with Overseas SteelmakersReference : Alliances with Overseas Steelmakers

GreeceGreece・・Corinth Corinth PipeworksPipeworks

CanadaCanada・・DJGDJG

U.S.A.U.S.A.・・CSICSI・・AK SteelAK Steel

South Korea・Dongkuk Steel・Hyundai HYSCO・Dongbu Steel

South KoreaSouth Korea・・DongkukDongkuk SteelSteel・・Hyundai HYSCOHyundai HYSCO・・DongbuDongbu SteelSteel

JFE SteelJFE Steel

ThailandThailand・・TCR, TCSTCR, TCS・・TTPTTP

ColombiaColombia・・HolasaHolasaIndonesiaIndonesia

・・SermaniSermani SteelSteel

MalaysiaMalaysia Vietnam Vietnam ・・PerstimaPerstima・・MycronMycron, , SunscoSunsco

GermanyGermany・・ThyssenKruppThyssenKrupp・・GeorgsmarienhuetteGeorgsmarienhuette

ChinaChina・・BohaiBohai NKK Drill PipeNKK Drill Pipe・・Fujian SinoFujian Sino--Japan MetalJapan Metal・・Hainan Hainan HaiwooHaiwoo TinplateTinplate・・Guangzhou JFE SheetGuangzhou JFE Sheet

Taiwan Taiwan ・・TonTon--yiyiIndiaIndia

・・JSW SteelJSW Steel

1919

Reference : Capturing growing demand for high-end steel in Asian markets.

80

90

100

110

120

130

140

FY03/1H

FY03/2H

FY04/1H

FY04/2H

FY05/1H

FY05/2H

FY06/1H

FY06/2H

FY07/1H

FY07/2H

FY08/1H

FY08/2H

FY09/1H

FY09/2H

Shipments to Allied Steelmakers (FY03/1H = 100)

Shipments to allied steelmakers, following a temporary decrease due to the global economic crisis triggered by the collapse of Lehman in FY2008, grew at solid half-year rates of 10–30% in FY 2009, as the company captured growing demand for high-end steel in Asian markets.

20

(2) Target Market Greater East Asia as our “Home Market”

21

China(6.79 mil tons)

South Western Asia(4.13 mil tons)

Middle and Near East(7.89 mil tons)

Hot-rolled sheet

Cold-rolled sheet

Plate

Regional Import Volumes in 2008(see legend)

2.74

1.28

3.87

0.64

1.382.12

Strategies to Expand ExportsOrganization

Make extended visits to develop sales

Restructure sales: 10 departments & 15 sections 13 departments & 18 sections

Strengthen overseas offices

Strengthen alliances

Export Expansion Focusing on Asia

6.84

4.15

4.23

East Asia(15.22 mil tons)

679240

1,522

537

413

789

0

500

1,000

1,500

2,000

2,500

3,000

3,500

Total imports Exports from Japan

34.03 mil tons 8.33 mil tons

China

Middle and Near East

South Western Asia

East Asia

Legend

1.340.92

4.53

22

Business Models that Respond to Each Market

Localization

Distance from Japan

Korea China Thai East Asia

India Middle East

North America

South America

Europe

Export

CSI

AK

Steel

Vertical Alliance(Export of semi-finished goods)

Dongkuk Hyundai

HyscoTongbu

GJSSTin

PlateMill

TCR

TCS

Tin PlateMill

Tin PlateMill

Localiza

tion

Study feasibility of Integrated Steel Work Projects

Study feasibility of Slab Projects

TKS

GMH

AKSteel

(USS)

Dongkuk

Hyundai Hysco

Technological

Alliance

(JSW)

Expanding Sales

◆Further Strengthen the established relationship ◆Seek New Alliance in New Market

2323

Equipment Shipments(operating) (1,000t/p.a.)

High-end SteelAuto (GA) 600

400Under Construction Electric (GI) 200

Auto (CRC) 500

1,800 400 Electric (CRC) 200

CRC 200

900

CAL

PL-TCM No.2 CGL

No.1 CGL

Expansion of Capacity in Guangzhou, China

Guangzhou JFE Steel Sheet (JFE ownership: 50%)Phase 1: Started operating #1 CGL (March 2006)Phase 2: Start operating expanded line (mid-2011)

Providing HRC

JFE Steel

24

Expansion of Alliances

Mycron Steel [announced Feb. 2010]Made 3% capital investment (179 million ringgits, or about 4.9 billion yen)Supply automotive technology and EG substrateIncrease supply of hot-rolled coil after Mycron’s introduction of new cold reduction mill Increase supply of hot rolled steel to 200,000 tons/year by around 2012

Mycron Steel [announced Feb. 2010]Made 3% capital investment (179 million ringgits, or about 4.9 billion yen)Supply automotive technology and EG substrateIncrease supply of hot-rolled coil after Mycron’s introduction of new cold reduction mill Increase supply of hot rolled steel to 200,000 tons/year by around 2012

SUNSCO [announced Feb. 2010]Made 8% capital investment (US$ 130 million, or about 11.7 billion yen). Major shareholder

is Maruichi Steel (64.3%).Increase hot rolled steel supply to 50,000 tons/year in 2010 and then 100,000–150,000

tons/year in 2011

SUNSCO [announced Feb. 2010]Made 8% capital investment (US$ 130 million, or about 11.7 billion yen). Major shareholder

is Maruichi Steel (64.3%).Increase hot rolled steel supply to 50,000 tons/year in 2010 and then 100,000–150,000

tons/year in 2011

Strategic collaboration with JSW Steel, India’s major steel maker [announced Nov. 2009]Help JSW Steel expand crude steel capacity from current 7.8 million tons to 11 million tons in

2011 and then to 32 million tons in 2020.Collaborate on steel products for automobiles (supply production technology, substrate

and cooperative services)Others (participate in West Bengal project, make joint capital investments, etc.)

Strategic collaboration with JSW Steel, India’s major steel maker [announced Nov. 2009]Help JSW Steel expand crude steel capacity from current 7.8 million tons to 11 million tons in

2011 and then to 32 million tons in 2020.Collaborate on steel products for automobiles (supply production technology, substrate

and cooperative services)Others (participate in West Bengal project, make joint capital investments, etc.)

IndiaIndia

MalaysiaMalaysia

VietnamVietnam

25

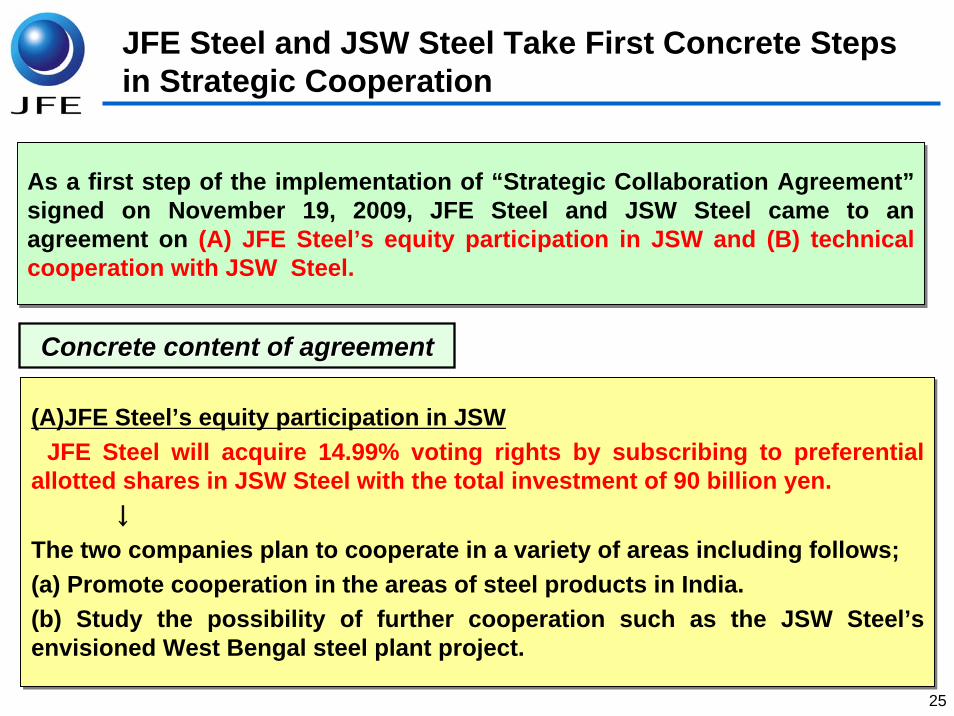

JFE Steel and JSW Steel Take First Concrete Steps in Strategic Cooperation

(A)JFE Steel’s equity participation in JSW JFE Steel will acquire 14.99% voting rights by subscribing to preferential allotted shares in JSW Steel with the total investment of 90 billion yen. ↓

The two companies plan to cooperate in a variety of areas including follows; (a) Promote cooperation in the areas of steel products in India.(b) Study the possibility of further cooperation such as the JSW Steel’s envisioned West Bengal steel plant project.

(A)JFE Steel’s equity participation in JSW JFE Steel will acquire 14.99% voting rights by subscribing to preferential allotted shares in JSW Steel with the total investment of 90 billion yen. ↓

The two companies plan to cooperate in a variety of areas including follows; (a) Promote cooperation in the areas of steel products in India.(b) Study the possibility of further cooperation such as the JSW Steel’s envisioned West Bengal steel plant project.

As a first step of the implementation of “Strategic Collaboration Agreement”signed on November 19, 2009, JFE Steel and JSW Steel came to an agreement on (A) JFE Steel’s equity participation in JSW and (B) technical cooperation with JSW Steel.

As a first step of the implementation of “Strategic Collaboration Agreement”signed on November 19, 2009, JFE Steel and JSW Steel came to an agreement on (A) JFE Steel’s equity participation in JSW and (B) technical cooperation with JSW Steel.

Concrete content of agreementConcrete content of agreement

26

(B) JFE Steel’s technical assistance for JSW

(a) Cooperation in the Automotive Steel

【Objective of Agreement】 Through newly announced agreements, JFE Steel looks forward to deepening its collaboration with JSW Steel to establish a solid base for production and sales and thereby grow its market in India.

【Essential point of Agreement】JFE Steel will provide JSW Steel with technology for the production of hot-rolled coils and

cold-rolled coils for automotive use,JFE Steel will supply JSW Steel with substrates, andThe two companies will jointly provide automotive customers with services including

engineering and product development.

(B) JFE Steel’s technical assistance for JSW

(a) Cooperation in the Automotive Steel

【Objective of Agreement】 Through newly announced agreements, JFE Steel looks forward to deepening its collaboration with JSW Steel to establish a solid base for production and sales and thereby grow its market in India.

【Essential point of Agreement】JFE Steel will provide JSW Steel with technology for the production of hot-rolled coils and

cold-rolled coils for automotive use,JFE Steel will supply JSW Steel with substrates, andThe two companies will jointly provide automotive customers with services including

engineering and product development.

JFE Steel and JSW Steel Take First Concrete Steps in Strategic Cooperation

27

(b) Technical Assistance for operational improvements of JSW’s Vijayanagar Works

The two companies agreed on the areas of JFE Steel’s technical assistance forJSW’s Vijayanagar Works’ operational improvements, such as

Energy reduction/ environmental protectionImprovement of production process quality and yieldProduction capacity analysis and indices benchmarking

(b) Technical Assistance for operational improvements of JSW’s Vijayanagar Works

The two companies agreed on the areas of JFE Steel’s technical assistance forJSW’s Vijayanagar Works’ operational improvements, such as

Energy reduction/ environmental protectionImprovement of production process quality and yieldProduction capacity analysis and indices benchmarking

JFE Steel and JSW Steel Take First Concrete Steps in Strategic Cooperation

28

(Reference) JFE STEEL & JSW STEEL COME TOGETHER IN A STRATEGIC COLLABORATION [announced on Nov. 19th , 2009]

○○・・・Concluded agreements in the equity participation and technical cooperation agreement signed July 27th , 2010

(A) Collaboration for Automotive Steel Production:・ Supply of substrate materials for hot rolled, cold rolled and galvanized products.

・Joint service activities including application engineering and product development for automotive customers.

(B) Further Collaboration in the near future: ・Production of steel products other than automotive steel.

・Energy reduction programmes ・Environmental programmes ・Quality and yield improvement programmes

・Performance audit of JSW facilities・Benchmarking of techno-economic parameters between the parties・Procurement of raw materials both in and outside of India ・Project for building and operating an integrated steel production facility in

JSW’s West Bengal Steel Project・Mutual Stockholding

(3) Expansion of Production Capacity

30

Production Capacity Expand to 33 million tons (JFE Steel non-consolidated basis)

27

30

2627

29

31

33

20

25

30

35

FY05 FY06 FY07 FY08 FY09 FY10(E) FY11(F)

Trends of Crude Steel Production(stand-alone basis)

Crude SteelProduction

(Consolidated)30 33 34 29 28 33

(Mt)

As JFE Steel re-lined and restart #3BF at Kurashiki, 11th Feb. 2010, production volume will increase to 30-31Mt in the FY2010. (Eight BF are under operation)

30

Nine BF were under operation

3

5

7

FY06 FY07 FY081Q 2Q 3Q 4Q FY091Q 2Q 3Q 4Q

Million ton

31

8.5 10.0

23.0

30.033.0

21.5

Current Capacity for33 million tons/yr

East Japan Works

West Japan Works

Crude steel production (million tons/yr)

• Construction of new continuousslab caster, increase in degassingcapacity, and addition of slabfinishing equipment at Fukuyama

• Relining #3 BF at Kurashiki• Expansion of oxygen plant at

Fukuyama• Relining #3 BF at Fukuyama

(Increase furnace volume to 4,300m3 . Construction will be completed in May 2010 )

Primary investments

• Construction of new degassingequipment and expansion ofNo.1 continuous caster at Keihin

• Increase in steel plate capacityat Keihin

Reference: Expand Capacity by Reducing Bottlenecks

32

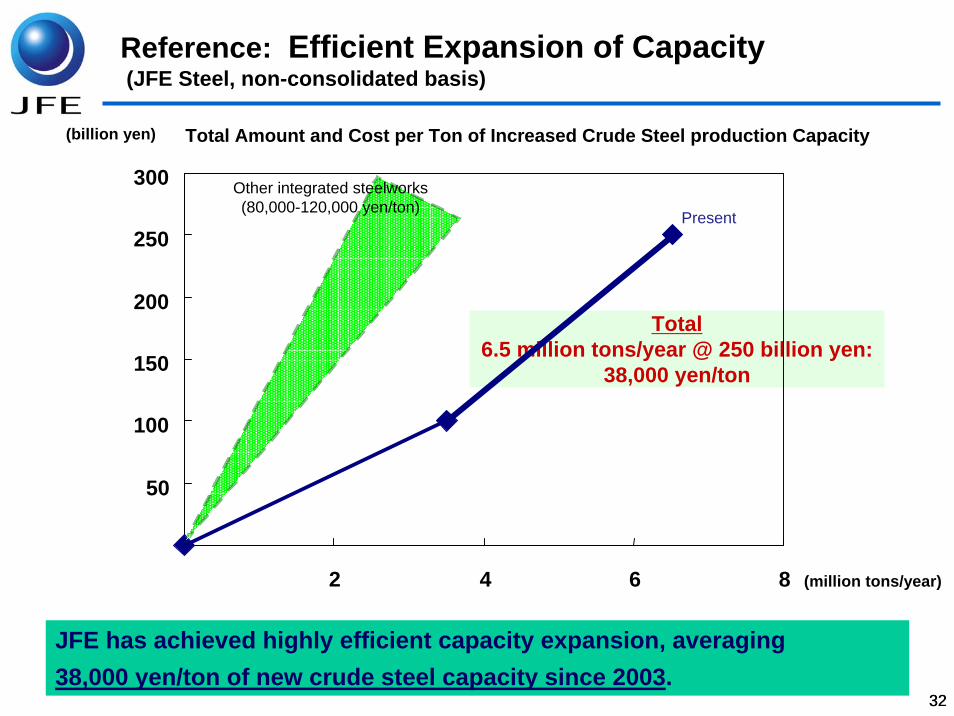

JFE has achieved highly efficient capacity expansion, averaging 38,000 yen/ton of new crude steel capacity since 2003.

Reference: Efficient Expansion of Capacity (JFE Steel, non-consolidated basis)

(billion yen)

Total6.5 million tons/year @ 250 billion yen:

38,000 yen/ton

(million tons/year)

50

100

150

200

250

300

2 4 6 8

Present

Other integrated steelworks(80,000-120,000 yen/ton)

Total Amount and Cost per Ton of Increased Crude Steel production Capacity

32

33

(4) Price Trends of Raw Materials

33

34

020406080

100120140160180200220240260280300

03 04 05 06 07 08 09 10-1Q 10-2Q SPOT

(US$/ton)

Australian premium hard coking coal

Australian fine ore (62% Fe)

300.0

89.7

Main Raw Material Prices

129

60.1

Raw Materials

Raw Materials

200(+55%)

120(+100%)

225(+12.5%)

147(+22.5%)

118

198

35

(5) More Self Sufficiency for Raw Materials

35

3636

Mining Interests & Operations Overseas

Philippine Sinter CorporationSinter

Minas da Serra Geral S/AJV with Vale

Iron ore

Nova Era Silicon S/AFerro-silicon

Erdos Manganese Alloys Co., Ltd.Silico-manganese

JFE Steel Corporation

Capital investment in 7 coal mines

(including JFE group companies)Coking coal

JFE Western 4 (Yandi)

JV with BHP BillitonIron ore

Cato Ridge Alloys (PTY) Ltd.Ferro-manganese

3737

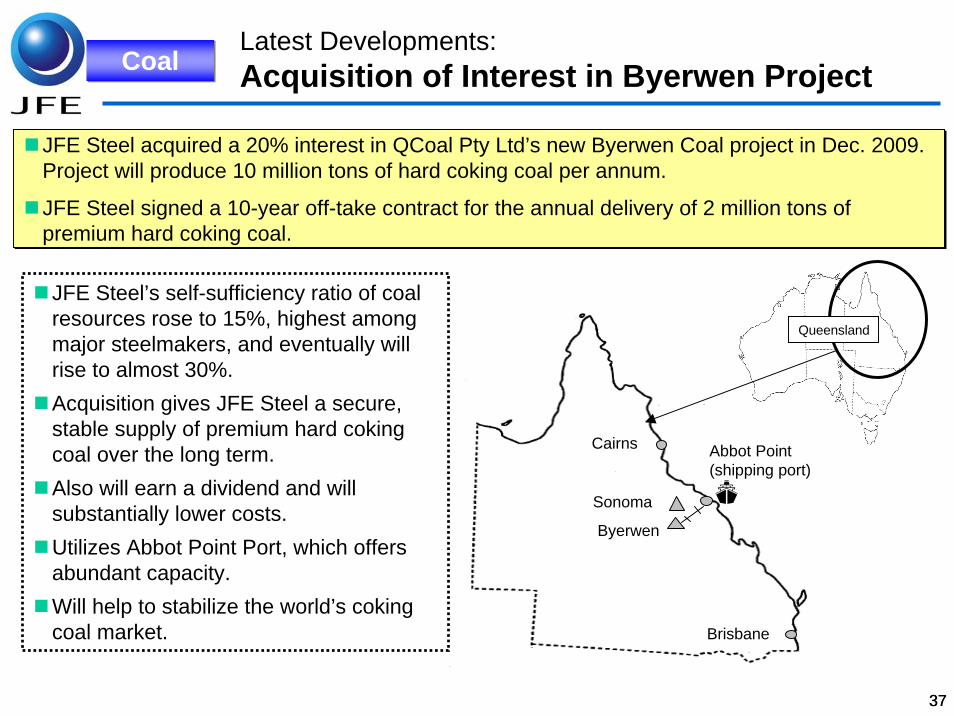

Latest Developments: Acquisition of Interest in Byerwen Project

JFE Steel acquired a 20% interest in QCoal Pty Ltd’s new Byerwen Coal project in Dec. 2009. Project will produce 10 million tons of hard coking coal per annum.

JFE Steel signed a 10-year off-take contract for the annual delivery of 2 million tons of premium hard coking coal.

JFE Steel acquired a 20% interest in QCoal Pty Ltd’s new Byerwen Coal project in Dec. 2009. Project will produce 10 million tons of hard coking coal per annum.

JFE Steel signed a 10-year off-take contract for the annual delivery of 2 million tons of premium hard coking coal.

Cairns

Brisbane

Sonoma

Byerwen

JFE Steel’s self-sufficiency ratio of coal resources rose to 15%, highest among major steelmakers, and eventually will rise to almost 30%.Acquisition gives JFE Steel a secure, stable supply of premium hard coking coal over the long term.Also will earn a dividend and will substantially lower costs. Utilizes Abbot Point Port, which offers abundant capacity.Will help to stabilize the world’s coking coal market.

Queensland

Abbot Point(shipping port)

CoalCoal

38

Latest Developments:

NAMISA Project in Brazil

Self-sufficiency ratio of 15% (Iron Ore)TOP-Ranked among competitors

• Investment: December 2008• Owners: CSN & Japan–Korea consortium• Projected sales: 38 MT/year in FY2013

Iron OreIron Ore

39

Increasing Self-Sufficiency Ratio

15%

30%

0%

10%

20%

30%

40%

Current In the Next Two Years

・A steady, secure supply of raw materials is a source of competitive strength.

・Consequently, JFE Steel acquires resource rights where there is a clear economic rationale for doing so. ・Aim at increasing the self-sufficiency ratio from 15% to 30% in some two years.

5. Appendix

41

(1) Steel Business Environment

42

58.1%

85.7% 83.4%

50.0%

55.0%

60.0%

65.0%

70.0%

75.0%

80.0%

85.0%

90.0%Ju

l-08

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov

-09

Jan-

10

Mar

-10

Source :WSA

ExportExport World Steel Capacity Utilization Ratio

...recovering to the robust levels as before the “Lehman Shock”.

43

ExportExport

Source :WSA : World Steel Short Range Outlook Spring, 2010

Demand Increase in Asia Apparent Steel Use in Asia

0

100

200

300

400

500

600

700

800

900

1,000

CY07 CY08 CY09 CY10(f) CY11(f)

millio

n t

ons

Others

India

Korea

China

Japan

+64Mt(y/y)

Source : OECD*Figures converted to steel products

Capacity Increase in Asia(09⇒10)

0

200

400

600

800

1,000

1,200

CY09/3E CY10/3E(e)

millio

n t

ons

Crude SteelProduction

Othes

India

Korea

China

Japan

+67Mt(y/y)*

Utilization Ratio(77%)

Utilization Ratio(78%)

Demand and Supply Trends in Asia (2010)

Healthy demand and supply trends in Asia will continue throughout the year 2010

44

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Ja

n-

08

Ap

r-0

8

Ju

l-0

8

Oc

t-0

8

Ja

n-

09

Ap

r-0

9

Ju

l-0

9

Oc

t-0

9

Ja

n-

10

Ap

r-1

0

mill

ion

tons

◆Quick estimate of world crude steel production in June : 118.8 million tons •Change from previous month: -5.4 million tons / Year-on-year change: + 18%

■ Production in China in June : 53.8 million tons•Change from previous month: -2.3 million tons / Year-on-year change: + 9%

Source :WSA

Crude Steel Production

China

EU27

Korea

USJapan

ExportExport

45

Auto Sales in Key Countries

Upward momentum continues in Asian Region. Keep rising y/y.

-40%

0%

40%

80%

120%

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-May

Korea China

FY2006 FY2007 FY2008 FY2009

-60%

-40%

-20%

0%

20%

40%

60%

80%

100%

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-Jun

Jul-S

ept

Oct

-Dec

Jan-

Mac

Apr

-May

Indonesia Thailand India

Automobile Sales in Key Countries (YoY changes)

* S. Korea figures include export sales

FY2006 FY2007 FY2008 FY2009

ExportExport

million unitsCY07 CY08 CY09 CY10

Jan-Mac Apr-Jun Jul-Set Oct-Dec Jan-Mac Apr-MayChina 8.8 9.4 2.7 3.4 3.6 4.0 4.6 3.0 0.73 32%Korea 4.1 3.8 0.7 0.9 0.9 1.1 0.9 0.7 0.19 35%Thailand 0.6 0.6 0.1 0.1 0.1 0.1 0.2 0.1 0.04 50%Indonesia 0.4 0.6 0.1 0.1 0.1 0.2 0.2 0.1 0.06 86%India 2.0 2.0 0.5 0.5 0.6 0.6 0.7 0.5 0.16 48%

y/y Change

46Source: General Administration of China Customs

China’s Export and Import of Steel Products (Including Semi-finished Products)(thousand tons)

China’s Export and Import of Steel Products

5680

1490

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep-

08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep-

09

Nov

-09

Jan-

10

Mar

-10

May

-10

ExportImport Last-minute shipment before the

abolishment of export tax rebate.

Export rebates will be scrapped for steel products after 15th July. (cf. Tax rebate for HRC will be reduced from 9% to zero)

ExportExport

47

0500

1,0001,5002,0002,5003,000

Jan

-0

8

Apr

-0

8

Ju

l-0

8

Oc

t-0

8

Jan

-0

9

Apr

-0

9

Ju

l-0

9

Oc

t-0

9

Jan

-1

0

Apr

-1

0

(thousand tons)Inventories of Steel Sheet in East China (Public Warehouses)

Hot rolled

Cold rolled

Hot dipped

Tin plate

Thin plate

Only inventory of hot rolled sheet is showing a rising trend.

China’s Steel Sheet InventoriesExportExport

48

Source: Production, exports and imports:-Japan Iron and Steel Federation, “China Steel Statistics”

Consumer Goods Production(Year-on-year growth)

Production in ChinaExport

Steel Production by Product

Export

0

5

10

15

20

25

30

35

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

mill

ion

to

ns

0%

50%

100%

150%

200%

250%

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

Automobiles(Sales, including commercial)

TV

Airconditioners

Refrigerators

Bar Steel

Steel Sheet

Plate & Thin plate

Pipe and etc.

49

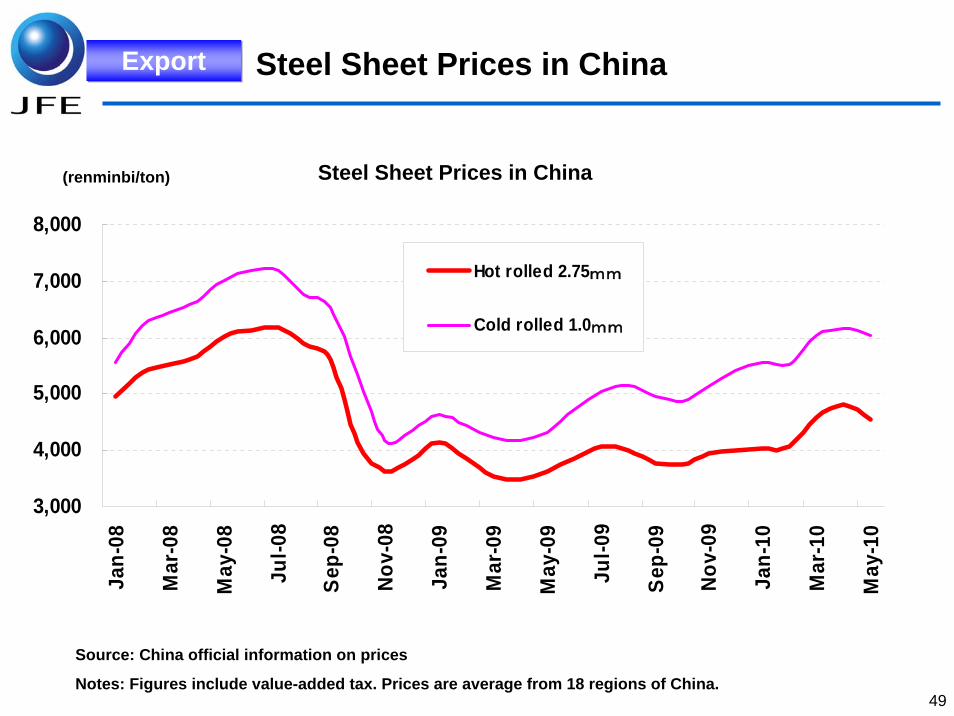

Steel Sheet Prices in China(renminbi/ton)

Source: China official information on prices

Notes: Figures include value-added tax. Prices are average from 18 regions of China.

Steel Sheet Prices in ChinaExportExport

3,000

4,000

5,000

6,000

7,000

8,000

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov-

08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Nov-

09

Jan-

10

Mar

-10

May

-10

Hot rolled 2.75mm

Cold rolled 1.0mm

50

Production Volume of Automobiles

2.61 2.582.74

2.972.79

2.983.13 3.18

2.88 2.91

2.59

1.611.71

2.14

2.47 2.54

2.30

2.74 2.992.73 2.76

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Apr-Jun Jul-Sept Oct-Dec Jan-Mac

milli

on u

nits

FY05(10.9M) FY06(11.5M) FY07(11.8M)FY08(10.0M) FY09(8.9M) FY10(9.3M)

DomesticDomestic

51

Combined Inventories of HR, CR and Surface-treated Steel Sheet

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000Ja

n-08

Apr

-08

Jul-0

8

Oct

-08

Jan-

09

Apr

-09

Jul-0

9

Oct

-09

Jan-

10

Apr

-10

thou

sand

tons

Maker Wholesaler Coil center

DomesticDomestic

52

Inventory of Sheared plate

200

250

300

350

400

450

500

550

60005

/3 906

/3 907

/3 7 9 1108

/1 3 5 7 9 1109

/1 3 5 7 9 1110

/1 3 5

thou

sand

tons

1

1.5

2

2.5

3

mon

ths

Inventory of sheared plate

Inventory ratio

DomesticDomestic

53

Inventory of Wide Flange Shapes

0

50

100

150

200

250

300

Jun-

08

Aug

-08

Oct

-08

Dec

-08

Feb-

09

Apr

-09

Jun-

09

Aug

-09

Oct

-09

Dec

-09

Feb-

10

Apr

-10

Jun-

10

thou

sand

tons

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

mon

ths

Inventory (left axis) Shipment (left) Inventory Ratio (right)

DomesticDomestic

54

Business Environment

Overall: The gradual recovery since FY 2009 will continue, but demand from construction sector will remain at low levels.

DomesticDomestic

Steel Demand from Manufacturing Industry

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

FY08

/1Q

FY08

/2Q

FY08

/3Q

FY08

/4Q

FY09

/1Q

FY09

/2Q

FY09

/3Q

FY09

/4Q

FY10

/1Q

(e)

FY10

/2Q

(e)

FY10

/3Q

(e)

FY10

/4Q

(e)

thousand t

ons

Shipyards Automobiles Others

Steel Demand from Construction Sector

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,000

FY08

/1Q

FY08

/3Q

FY09

/1Q

FY09

/3Q

FY10

/1Q

(e)

FY10

/3Q

(e)

thousa

nd t

ons

Construction

Civil Construction

55

(2) Others

56

JFE Engineering Results: Changes between FY 2009 and FY 2010

Y on Y

Engineering

Notes: Main Factors behind Changes 3.5 billion yen decrease in earnings due to weaker sales, 7.8 billion yen decrease in gross margin due to lower sales prices, 3 billion yen increase by cost reduction, and 2 billion yen increase in equity method earnings, etc.

※1

(billion yen)Change

1H Total 1H Total

Orders 157 279 130 310 31

Net Sales 117 294 110 270 ▲ 24

Operating Income 3 13 △1 5 ▲ 8

Ordinary Income 3 13 0 7 ▲ 6

FY09 FY10(e)

57

Shipbuilding Business Results: Changes between FY 09 and FY 10

Shipbuilding

Y on Y

※

Notes: Main Factors behind Changes¥5.8 billion : Cost reductions ¥2.5 billion : Forex rates & steel price changes

- 19.3 billion : Difference caused by booking reversal of the allowance for losses on construction contracts.

(billion yen)Change

1H Total 1H Total

Orders 14 59 64 110 51

Net Sales 139 287 110 210 ▲ 77

Oprating Income 10 21 8 11 ▲ 11

Single year income/loss ▲ 3 4 9 13 8

Changes of allowance forlosses on constructioncontract

15 21 1 1 ▲ 19

Goodwill amotzaron ▲ 2 ▲ 4 ▲ 2 ▲ 4 0

Ordinary Income 10 22 8 11 ▲ 11

FY09 FY10(e)

58

020406080

100120140160180200220240260280300

03 04 05 06 07 08 09 10-1Q 10-2Q SPOT

(US$/ton)

Australian premium hard coking coal

Australian fine ore (62% Fe)

300.0

89.7

Main Raw Material Prices

129

60.1

200(+55%)

120(+100%)

225(+12.5%)

147(+22.5%)

118

198

Raw Materials

Raw Materials

59

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Apr

-05

Jul-

05

Oct-

05

Jan

-06

Apr

-06

Jul-

06

Oct-

06

Jan

-07

Apr

-07

Jul-

07

Oct-

07

Jan

-08

Apr

-08

Jul-

08

Oct-

08

Jan

-09

Apr

-09

Jul-

09

Oct-

09

Jan

-10

Apr

-10

Jul-

10

(Yen/t)

Trends in Scrap Price Raw Materials

Raw Materials

Metals

Ferromanganese

400

800

1200

1600

2000

2400

2800

3200

3600

05/04

05/08

05/12

06/04

06/08

06/12

07/04

07/08

07/12

08/04

08/08

08/12

09/04

09/08

09/12

10/4

U$/T

Ferrosilicon

500

700

900

1100

1300

1500

1700

1900

2100

2300

2500

05/04

05/08

05/12

06/04

06/08

06/12

07/04

07/08

07/12

08/04

08/08

08/12

09/04

09/08

09/12

10/4

U$/T

Ferrochromium

30

50

70

90

110

130

150

170

190

210

230

05/04

05/08

05/12

06/04

06/08

06/12

07/04

07/08

07/12

08/04

08/08

08/12

09/04

09/08

09/12

10/4

¢/lb

Molybdenum

0

5

10

15

20

25

30

35

40

05/04

05/07

05/10

06/01

06/04

06/07

06/10

07/01

07/04

07/07

07/10

08/01

08/04

08/07

08/10

09/01

09/04

09/07

09/10

10/1

10/4

U$/lb

Raw Materials

Raw Materials

61

0

20

40

60

80

100

120

140

160

03/1

03/4

03/7

03/1

004

/104

/404

/704

/10

05/1

05/4

05/7

05/1

006

/106

/406

/706

/10

07/1

07/4

07/7

07/1

008

/108

/408

/708

/10

09/1

09/4

09/7

09/1

010

/110

/410

/7

50

150

250

350

450

550

650

750

850

WTI Crude Oil

Bunker oil

(Crude oil:$/bbl) (BUnker:$/T)

Crude Oil and Bunker OilRaw Materials

Raw Materials

62

0

50,000

100,000

150,000

200,000

250,000

05/4

05/7

05/10

06/1

06/4

06/7

06/10

07/1

07/4

07/7

07/10

08/1

08/4

08/7

08/10

09/1

09/4

09/7

09/10

10/1

10/4

10/7

Spot Prices for Vessel Chartering

($/day)

Raw Materials

Raw Materials

63

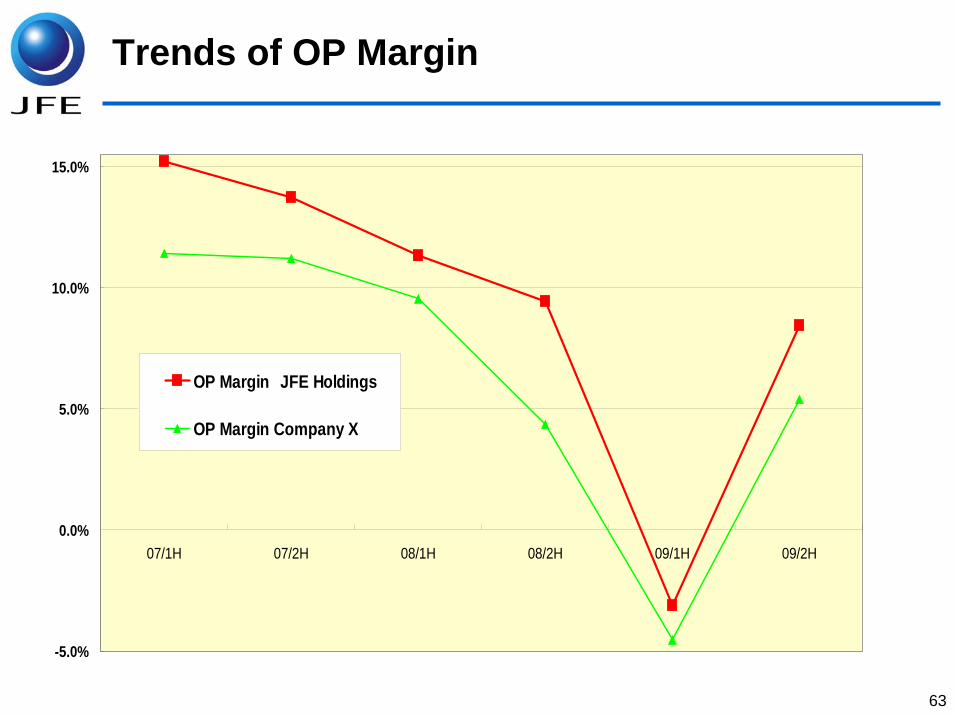

Trends of OP Margin

-5.0%

0.0%

5.0%

10.0%

15.0%

07/1H 07/2H 08/1H 08/2H 09/1H 09/2H

OP Margin JFE Holdings

OP Margin Company X

Main Financial Data

* For hybrid bonds issued in March 2008, 75% of the 300 billion yen issue price is deemed to be capital.

FY 2003 FY 2004 FY 2005 FY 2006 FY 2007 FY 2008 FY 2009 FY 2010(e)

Main financial indicators

Ordinary income(billion yen) 218 461 517 514 503 401 69 220

ROS 8.8% 16.4% 16.7% 15.8% 14.2% 10.2% 2.4% 6.4%

ROE 15.9% 18.7% 28.6% 21.3% 17.5% 13.7% 3.3% 8.2%

ROA 6.5% 13.1% 14.6% 14.1% 13.0% 10.0% 2.2% 6.0%

D/E ratio 246.2% 149.4% 88.7% 78.6% 85.7% 132.4% 103.2% 98.0%

D/E ratio * 61.4% 98.9% 75.5% 72.2%

Shares

Net income (yen/share) 185.8 274.0 555.0 513.6 450.6 355.6 86.4 227.0

Dividends (yen/share) 30 45 100 120 120 90 20 20

Contact:Finance and Investor Relations Dept., JFE Holdings, Inc.

Koji Matsunaga (Mr.)ManagerPhone: +81-3-3597-4381E-mail: [email protected]

Hiroyuki Kuriahra (Mr.)Staff ManagerPhone: +81-3-3597-4382E-mail: [email protected]