preparation and presentation of financial statements ... · preparation and presentation of...

TRANSCRIPT

1

copy 2005-13 Nelson Consulting Limited 1

Preparation and Presentation of Financial Statements ndash Part 2 24 September 2013

LAM Chi Yuen Nelson 林智遠MBA MSc BBA ACA ACS CFA CPA(US) CTA FCCA FCPA FCPA(Aust) FHKIoD FTIHK MHKSI MSCA

copy 2005-13 Nelson Consulting Limited 2

Operating Segments (IFRS 8)

p ( )Non-current Assets Held for Sale and Discontinued Operations (IFRS 5)

Todayrsquos Agenda

Interim Financial Reporting (IAS 34)

Simple but Comprehensive

Recap and key issues

Real Life Cases and Examples

2

copy 2005-13 Nelson Consulting Limited 3

Non-current Assets Held for Sale and Discontinued Operations (IFRS 5)

copy 2005-13 Nelson Consulting Limited 4

Todayrsquos Agenda

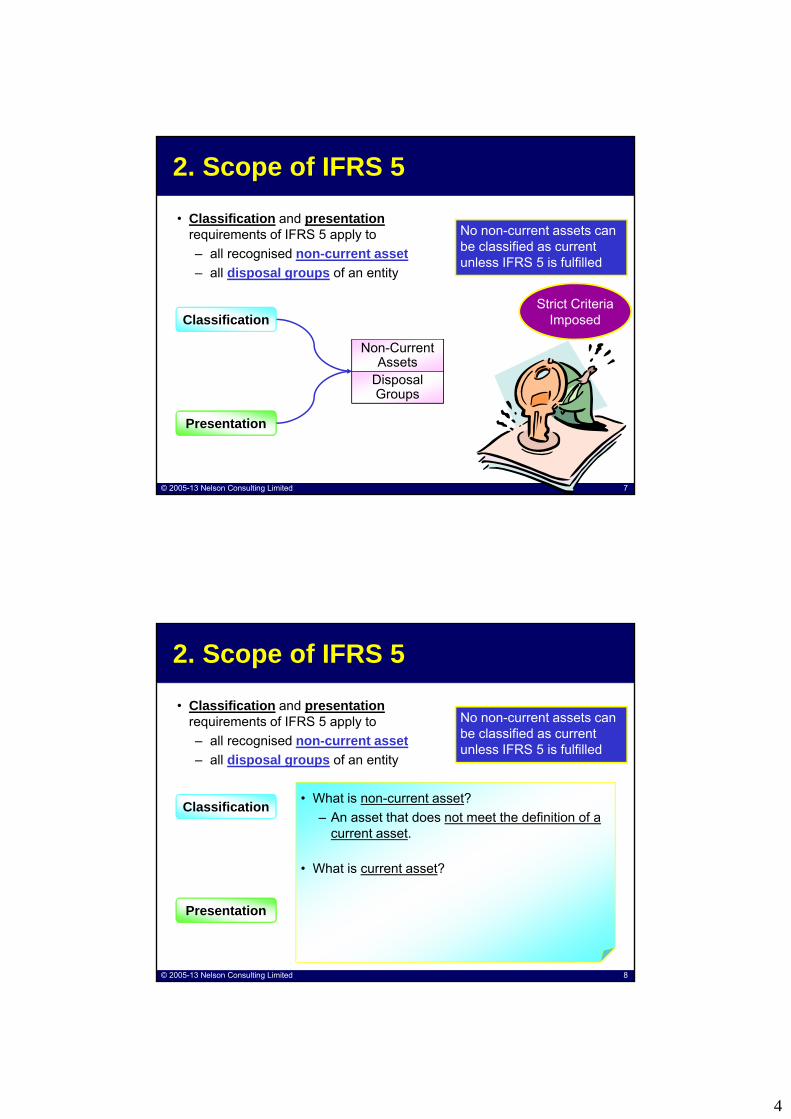

1 Objective of IFRS 5

2 Scope of IFRS 5

3 Classification

4 Measurement

5 Presentation

3

copy 2005-13 Nelson Consulting Limited 5

1 Objective of IFRS 5

bull To specify

Classification

Measurement

Presentation

bull The accounting forassets held for sale

bull The presentation and disclosureof discontinued operations

Non-Current Assets

Disposal Groups

PresentationDiscontinued Operations

Disposal Group may be Discontinued Operation if it is an operation

copy 2005-13 Nelson Consulting Limited 6

1 Objective of IFRS 5 (Summary)

bull To specify

bull The accounting forassets held for sale

bull The presentation and disclosureof discontinued operations

bull In particular to requirendash asset that meet the criteria to be

classified as held for sale to bebull measured at

ndash the lower of carrying amount andfair value less costs to sell and

ndash depreciation on such assets to cease andbull presented separately in the statement of

financial position andndash the results of discontinued operations to be

presented separately in the statement of comprehensive income

Classification

Measurement

Presentation

Strict Criteria Imposed

4

copy 2005-13 Nelson Consulting Limited 7

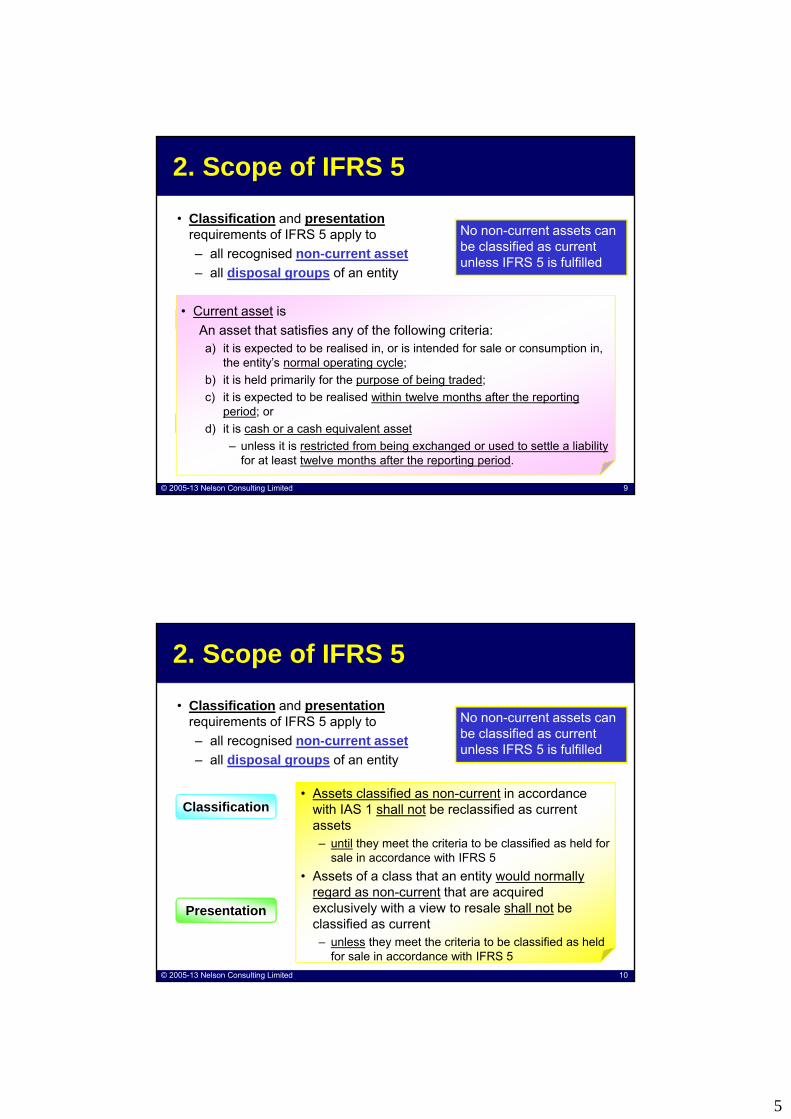

2 Scope of IFRS 5

Classification

Presentation

bull Classification and presentationrequirements of IFRS 5 apply to

ndash all recognised non-current asset

ndash all disposal groups of an entity

Non-Current Assets

Disposal Groups

No non-current assets can be classified as current unless IFRS 5 is fulfilled

Strict Criteria Imposed

copy 2005-13 Nelson Consulting Limited 8

2 Scope of IFRS 5

Classification

Presentation

bull Classification and presentationrequirements of IFRS 5 apply to

ndash all recognised non-current asset

ndash all disposal groups of an entity

No non-current assets can be classified as current unless IFRS 5 is fulfilled

bull What is non-current asset

ndash An asset that does not meet the definition of a current asset

bull What is current asset

5

copy 2005-13 Nelson Consulting Limited 9

2 Scope of IFRS 5

Classification

Presentation

bull Classification and presentationrequirements of IFRS 5 apply to

ndash all recognised non-current asset

ndash all disposal groups of an entity

No non-current assets can be classified as current unless IFRS 5 is fulfilled

bull Current asset is

An asset that satisfies any of the following criteriaa) it is expected to be realised in or is intended for sale or consumption in

the entityrsquos normal operating cycle

b) it is held primarily for the purpose of being traded

c) it is expected to be realised within twelve months after the reporting period or

d) it is cash or a cash equivalent asset

ndash unless it is restricted from being exchanged or used to settle a liabilityfor at least twelve months after the reporting period

copy 2005-13 Nelson Consulting Limited 10

2 Scope of IFRS 5

Classification

Presentation

bull Classification and presentationrequirements of IFRS 5 apply to

ndash all recognised non-current asset

ndash all disposal groups of an entity

bull Assets classified as non-current in accordance with IAS 1 shall not be reclassified as current assetsndash until they meet the criteria to be classified as held for

sale in accordance with IFRS 5

bull Assets of a class that an entity would normally regard as non-current that are acquired exclusively with a view to resale shall not be classified as currentndash unless they meet the criteria to be classified as held

for sale in accordance with IFRS 5

No non-current assets can be classified as current unless IFRS 5 is fulfilled

6

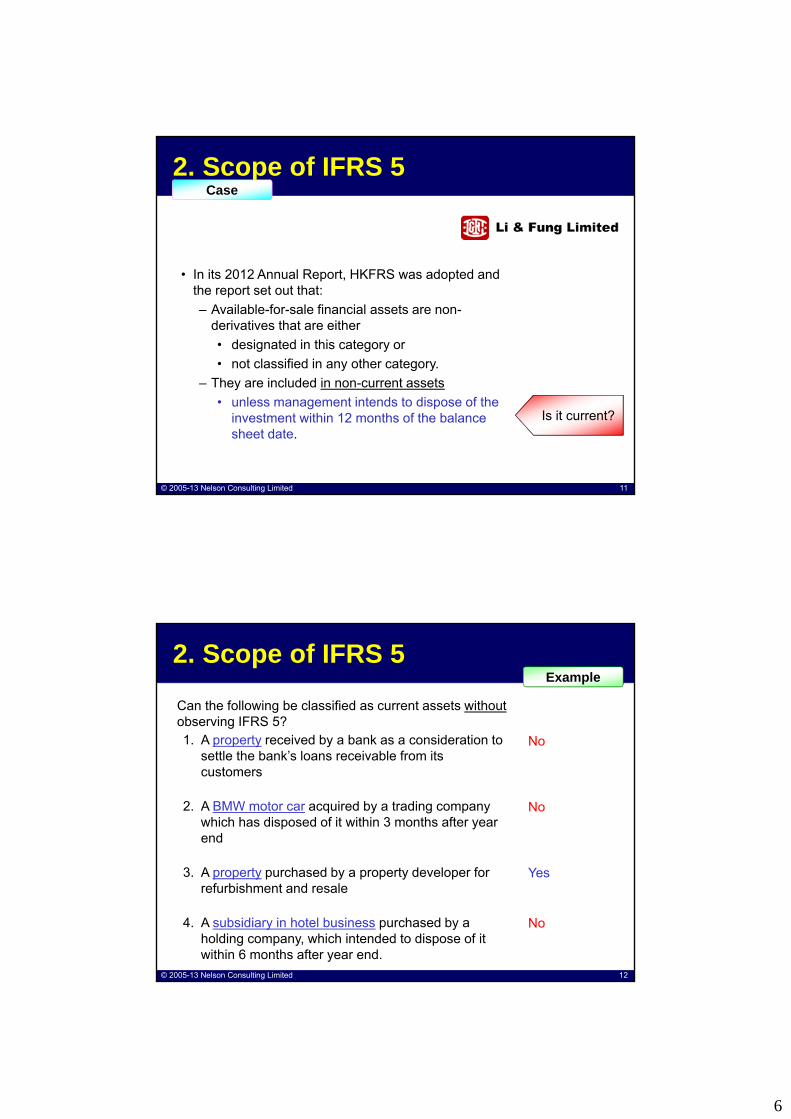

copy 2005-13 Nelson Consulting Limited 11

Is it current

2 Scope of IFRS 5

bull In its 2012 Annual Report HKFRS was adopted and the report set out that

ndash Available-for-sale financial assets are non-derivatives that are either

bull designated in this category or

bull not classified in any other category

ndash They are included in non-current assets

bull unless management intends to dispose of the investment within 12 months of the balance sheet date

Case

copy 2005-13 Nelson Consulting Limited 12

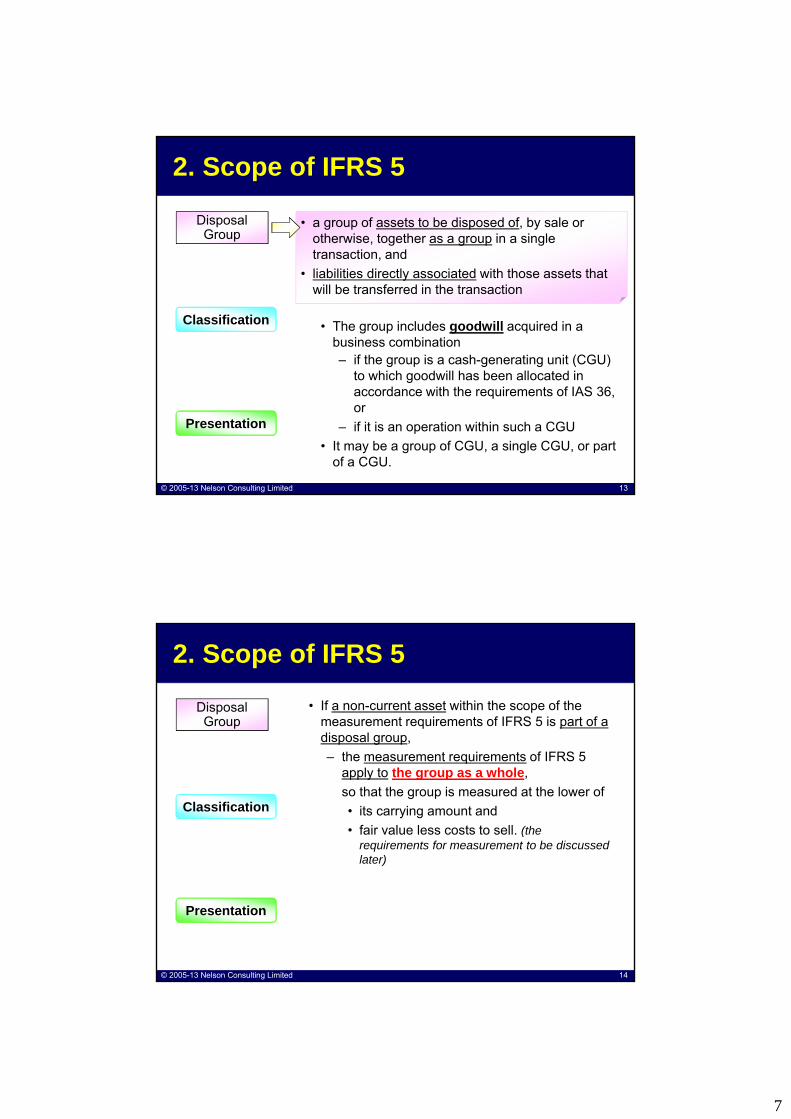

2 Scope of IFRS 5

Can the following be classified as current assets withoutobserving IFRS 51 A property received by a bank as a consideration to

settle the bankrsquos loans receivable from its customers

2 A BMW motor car acquired by a trading company which has disposed of it within 3 months after year end

3 A property purchased by a property developer for refurbishment and resale

4 A subsidiary in hotel business purchased by a holding company which intended to dispose of it within 6 months after year end

Example

No

No

Yes

No

7

copy 2005-13 Nelson Consulting Limited 13

2 Scope of IFRS 5

Classification

Presentation

bull a group of assets to be disposed of by sale or otherwise together as a group in a single transaction and

bull liabilities directly associated with those assets that will be transferred in the transaction

Disposal Group

bull The group includes goodwill acquired in a business combinationndash if the group is a cash-generating unit (CGU)

to which goodwill has been allocated in accordance with the requirements of IAS 36 or

ndash if it is an operation within such a CGU

bull It may be a group of CGU a single CGU or part of a CGU

copy 2005-13 Nelson Consulting Limited 14

2 Scope of IFRS 5

Classification

Presentation

Disposal Group

bull If a non-current asset within the scope of the measurement requirements of IFRS 5 is part of a disposal group

ndash the measurement requirements of IFRS 5 apply to the group as a whole

so that the group is measured at the lower of

bull its carrying amount and

bull fair value less costs to sell (the requirements for measurement to be discussed later)

8

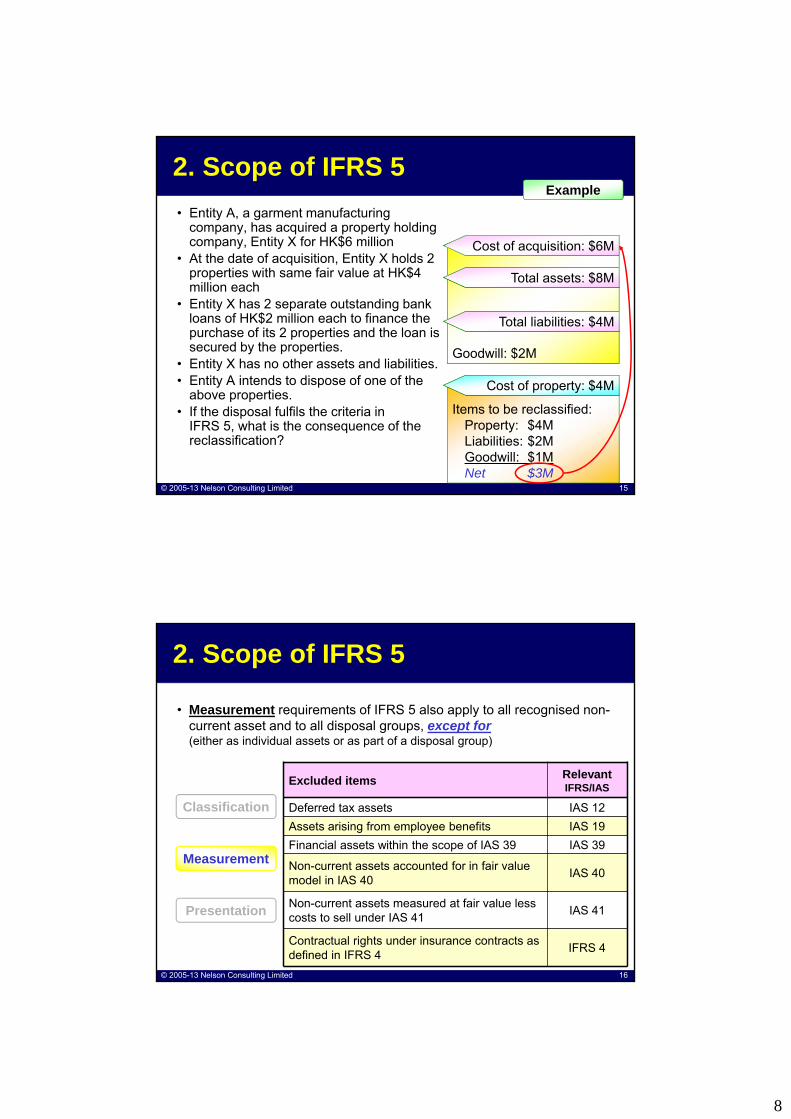

copy 2005-13 Nelson Consulting Limited 15

Items to be reclassifiedProperty $4MLiabilities $2MGoodwill $1MNet $3M

Goodwill $2M

2 Scope of IFRS 5Example

bull Entity A a garment manufacturing company has acquired a property holding company Entity X for HK$6 million

bull At the date of acquisition Entity X holds 2 properties with same fair value at HK$4 million each

bull Entity X has 2 separate outstanding bank loans of HK$2 million each to finance the purchase of its 2 properties and the loan is secured by the properties

bull Entity X has no other assets and liabilitiesbull Entity A intends to dispose of one of the

above propertiesbull If the disposal fulfils the criteria in

IFRS 5 what is the consequence of the reclassification

Cost of acquisition $6M

Total assets $8M

Total liabilities $4M

Cost of property $4M

copy 2005-13 Nelson Consulting Limited 16

2 Scope of IFRS 5

bull Measurement requirements of IFRS 5 also apply to all recognised non-current asset and to all disposal groups except for(either as individual assets or as part of a disposal group)

Classification

Measurement

Presentation

Excluded items Relevant IFRSIAS

Deferred tax assets IAS 12

Assets arising from employee benefits IAS 19

Financial assets within the scope of IAS 39 IAS 39

Non-current assets accounted for in fair value model in IAS 40

IAS 40

Non-current assets measured at fair value less costs to sell under IAS 41

IAS 41

Contractual rights under insurance contracts as defined in IFRS 4

IFRS 4

9

copy 2005-13 Nelson Consulting Limited 17

2 Scope of IFRS 5

bull The classification presentation and measurement requirements in IFRS 5 applicable to a non-current asset (or disposal group) that is classified as held for sale apply also to

ndash a non-current asset (or disposal group) that is classified as held for distribution to owners acting in their capacity as owners (held for distribution to owners) (IFRS 55A)

bull While IFRS 5 specifies the disclosures required in respect of non-current assets (or disposal groups) classified as held for sale or discontinued operations

ndash disclosures in other IFRSs do not apply to such assets (or disposal groups)unless those IFRSs require

a) specific disclosures in respect of non-current assets (or disposal groups) classified as held for sale or discontinued operations or

b) disclosures about measurement of assets and liabilities within a disposal group that are not within the scope of the measurement requirement of IFRS 5 and such disclosure are not already provided in the other notes to the financial statements (IFRS 55B)

copy 2005-13 Nelson Consulting Limited 18

Classification

Measurement

Presentation

For this to be the caseFor this to be the case

3 Classification as Held For Sale

Classification

Measurement

Presentation

bull An entity shall classify a non-current asset (or disposal group) as held for sale if

ndash its carrying amount will be recovered principally

bull through a sale transaction

bull rather than through continuing use

bull the asset (or disposal group) must beavailable for immediate sale

bull its sale must be highly probable

Available for Immediate Sale

Highly Probable

10

copy 2005-13 Nelson Consulting Limited 19

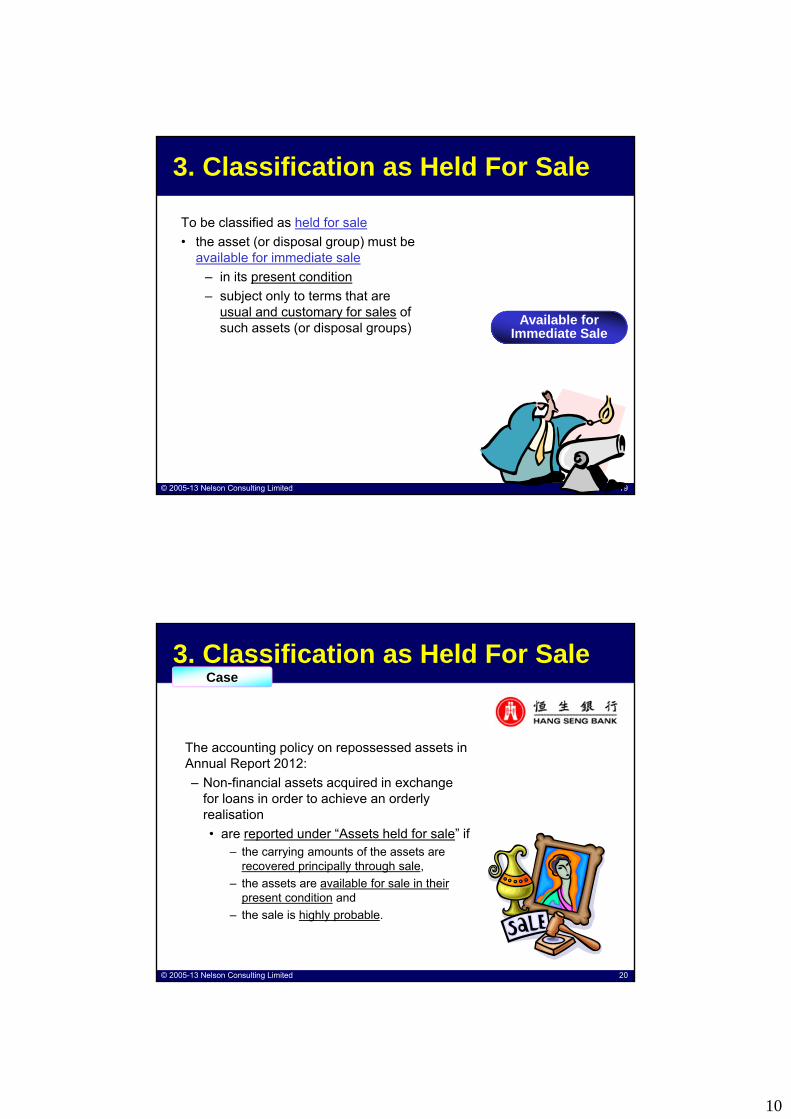

3 Classification as Held For Sale

Available for Immediate Sale

To be classified as held for sale

bull the asset (or disposal group) must be available for immediate sale

ndash in its present condition

ndash subject only to terms that are usual and customary for sales of such assets (or disposal groups)

copy 2005-13 Nelson Consulting Limited 20

3 Classification as Held For SaleCase

The accounting policy on repossessed assets in Annual Report 2012

ndash Non-financial assets acquired in exchange for loans in order to achieve an orderly realisation

bull are reported under ldquoAssets held for salerdquo if ndash the carrying amounts of the assets are

recovered principally through sale

ndash the assets are available for sale in their present condition and

ndash the sale is highly probable

11

copy 2005-13 Nelson Consulting Limited 21

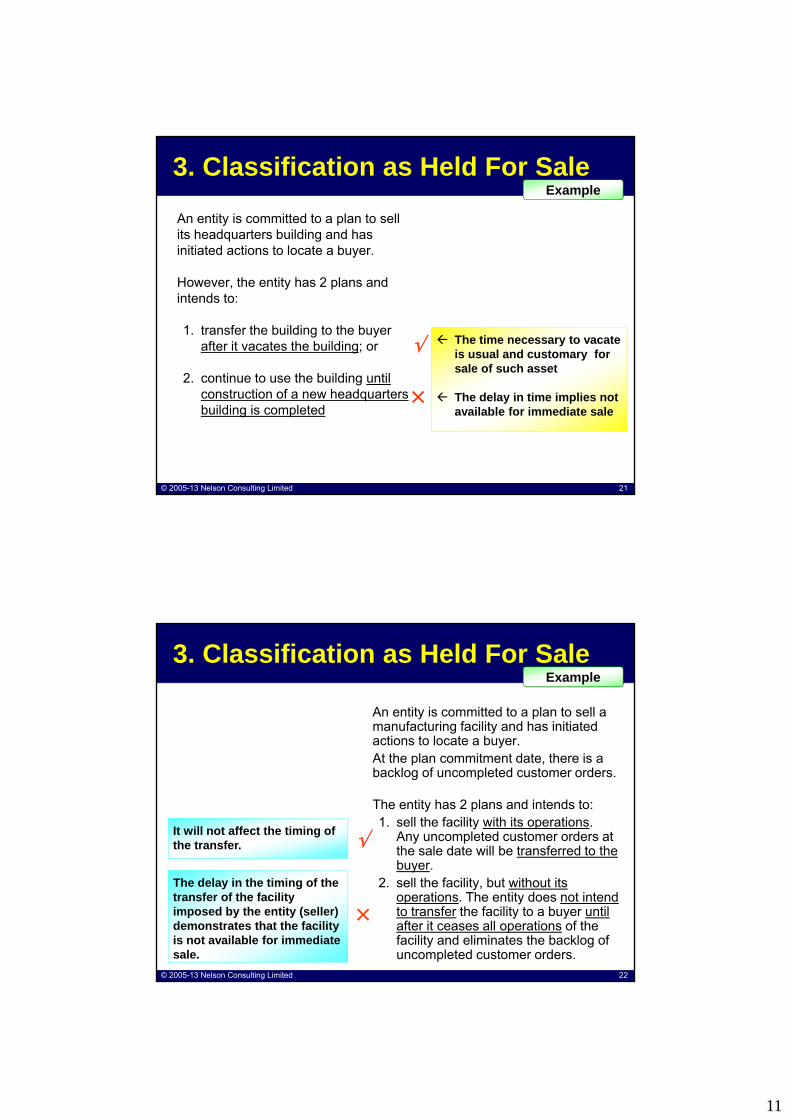

An entity is committed to a plan to sell its headquarters building and has initiated actions to locate a buyer

However the entity has 2 plans and intends to

1 transfer the building to the buyer after it vacates the building or

2 continue to use the building untilconstruction of a new headquartersbuilding is completed

3 Classification as Held For SaleExample

The time necessary to vacate is usual and customary for sale of such asset

The delay in time implies not available for immediate sale

copy 2005-13 Nelson Consulting Limited 22

An entity is committed to a plan to sell a manufacturing facility and has initiated actions to locate a buyerAt the plan commitment date there is a backlog of uncompleted customer orders

The entity has 2 plans and intends to1 sell the facility with its operations

Any uncompleted customer orders at the sale date will be transferred to the buyer

2 sell the facility but without its operations The entity does not intend to transfer the facility to a buyer until after it ceases all operations of the facility and eliminates the backlog of uncompleted customer orders

3 Classification as Held For SaleExample

It will not affect the timing of the transfer

The delay in the timing of the transfer of the facility imposed by the entity (seller) demonstrates that the facility is not available for immediate sale

12

copy 2005-13 Nelson Consulting Limited 23

3 Classification as Held For Sale

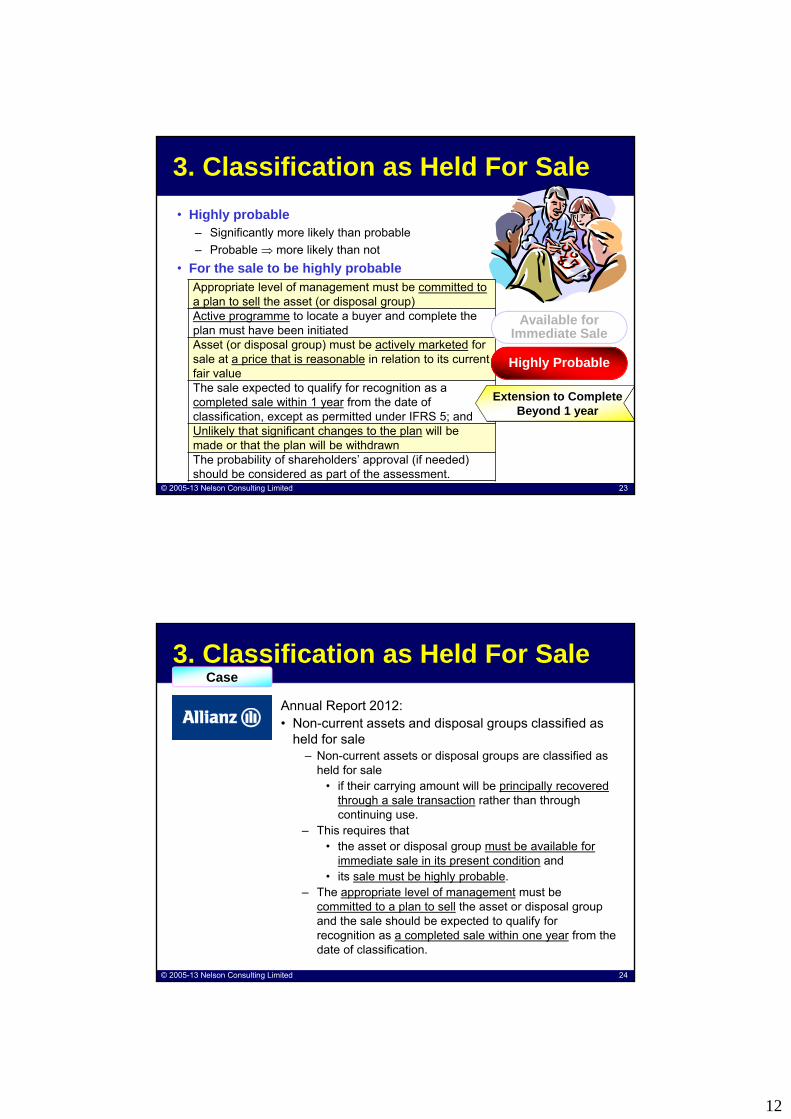

bull Highly probablendash Significantly more likely than probable

ndash Probable more likely than not

bull For the sale to be highly probableAppropriate level of management must be committed to a plan to sell the asset (or disposal group)Active programme to locate a buyer and complete the plan must have been initiatedAsset (or disposal group) must be actively marketed for sale at a price that is reasonable in relation to its current fair valueThe sale expected to qualify for recognition as a completed sale within 1 year from the date of classification except as permitted under IFRS 5 andUnlikely that significant changes to the plan will be made or that the plan will be withdrawnThe probability of shareholdersrsquo approval (if needed) should be considered as part of the assessment

Extension to Complete Extension to Complete Beyond 1 year

Highly Probable

Available for Immediate Sale

copy 2005-13 Nelson Consulting Limited 24

3 Classification as Held For Sale

Annual Report 2012bull Non-current assets and disposal groups classified as

held for salendash Non-current assets or disposal groups are classified as

held for salebull if their carrying amount will be principally recovered

through a sale transaction rather than through continuing use

ndash This requires that bull the asset or disposal group must be available for

immediate sale in its present condition and bull its sale must be highly probable

ndash The appropriate level of management must be committed to a plan to sell the asset or disposal group and the sale should be expected to qualify for recognition as a completed sale within one year from the date of classification

Case

13

copy 2005-13 Nelson Consulting Limited 25

3 Classification as Held For Sale

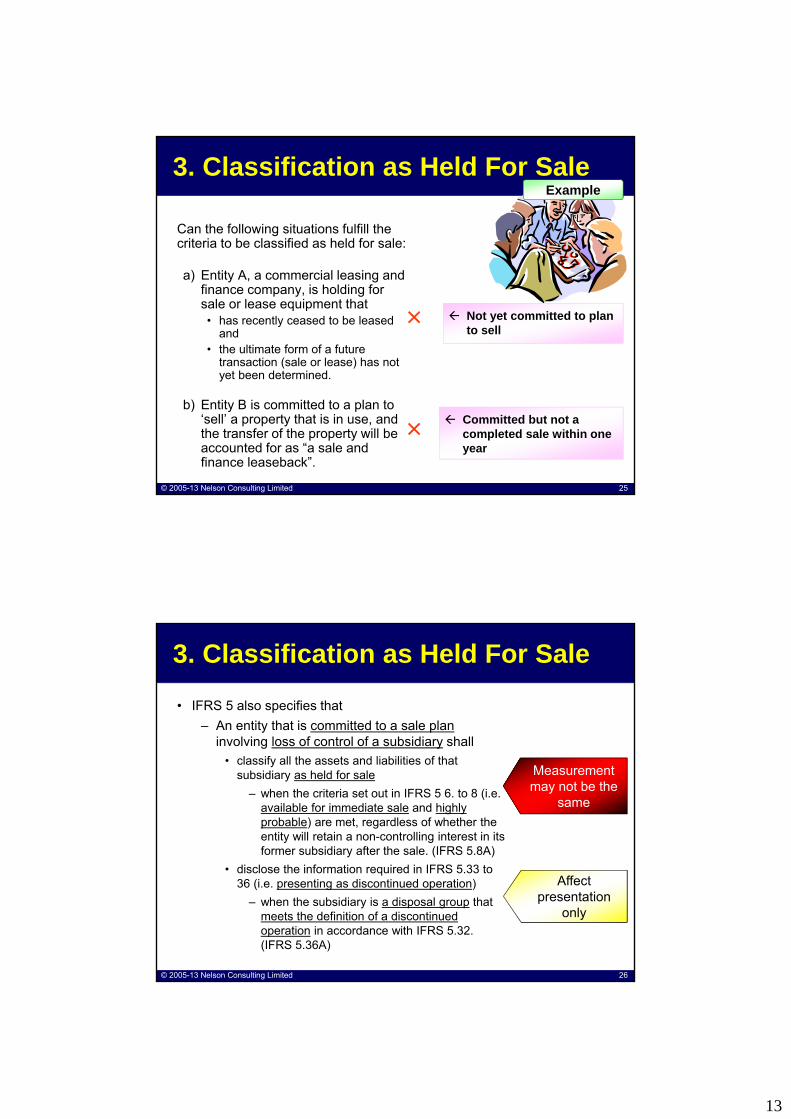

Can the following situations fulfill the criteria to be classified as held for sale

a) Entity A a commercial leasing and finance company is holding for sale or lease equipment thatbull has recently ceased to be leased

andbull the ultimate form of a future

transaction (sale or lease) has not yet been determined

b) Entity B is committed to a plan to lsquosellrsquo a property that is in use and the transfer of the property will be accounted for as ldquoa sale and finance leasebackrdquo

Example

Not yet committed to plan to sell

Committed but not a completed sale within one year

copy 2005-13 Nelson Consulting Limited 26

3 Classification as Held For Sale

bull IFRS 5 also specifies that

ndash An entity that is committed to a sale planinvolving loss of control of a subsidiary shall

bull classify all the assets and liabilities of that subsidiary as held for sale

ndash when the criteria set out in IFRS 5 6 to 8 (ie available for immediate sale and highly probable) are met regardless of whether the entity will retain a non-controlling interest in its former subsidiary after the sale (IFRS 58A)

bull disclose the information required in IFRS 533 to 36 (ie presenting as discontinued operation)

ndash when the subsidiary is a disposal group that meets the definition of a discontinued operation in accordance with IFRS 532 (IFRS 536A)

Measurement may not be the

same

Affect presentation

only

14

copy 2005-13 Nelson Consulting Limited 27

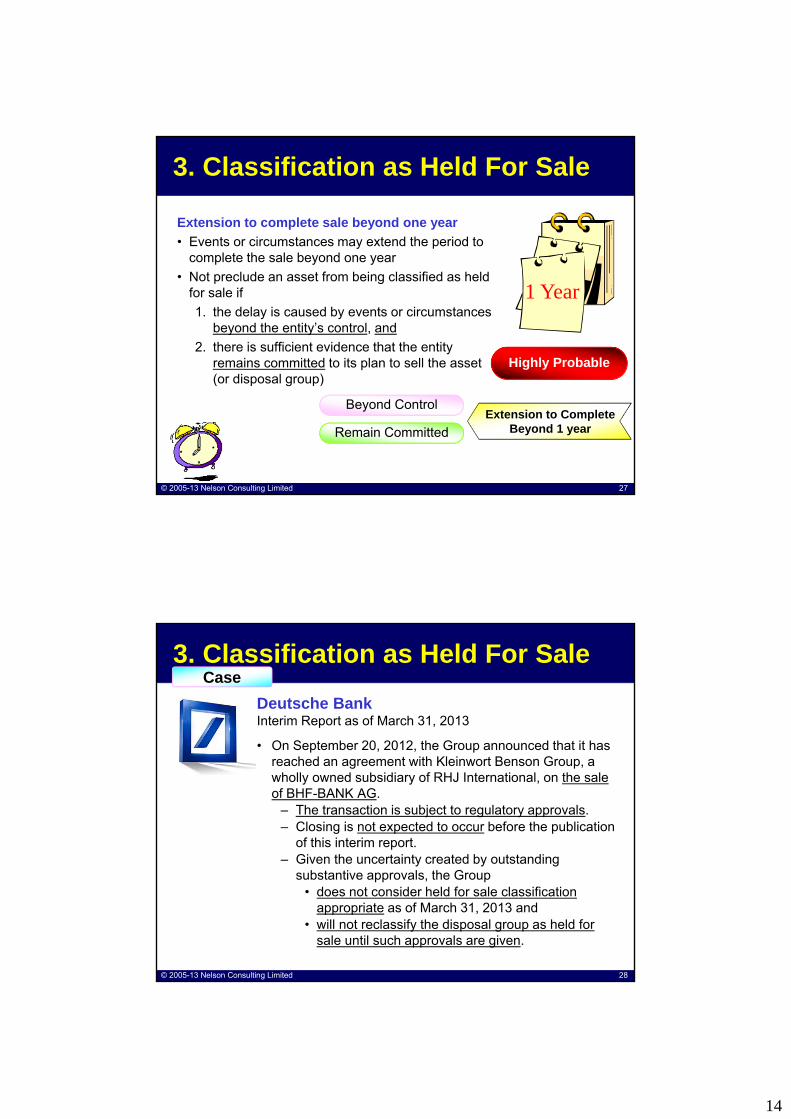

3 Classification as Held For Sale

Extension to Complete Beyond 1 year

Highly Probable

Extension to complete sale beyond one year

bull Events or circumstances may extend the period to complete the sale beyond one year

bull Not preclude an asset from being classified as held for sale if

1 the delay is caused by events or circumstances beyond the entityrsquos control and

2 there is sufficient evidence that the entity remains committed to its plan to sell the asset (or disposal group)

Beyond Control

Remain Committed

1 Year

copy 2005-13 Nelson Consulting Limited 28

3 Classification as Held For SaleCase

bull On September 20 2012 the Group announced that it has reached an agreement with Kleinwort Benson Group a wholly owned subsidiary of RHJ International on the sale of BHF-BANK AG

ndash The transaction is subject to regulatory approvals ndash Closing is not expected to occur before the publication

of this interim report ndash Given the uncertainty created by outstanding

substantive approvals the Group bull does not consider held for sale classification

appropriate as of March 31 2013 andbull will not reclassify the disposal group as held for

sale until such approvals are given

Deutsche BankInterim Report as of March 31 2013

15

copy 2005-13 Nelson Consulting Limited 29

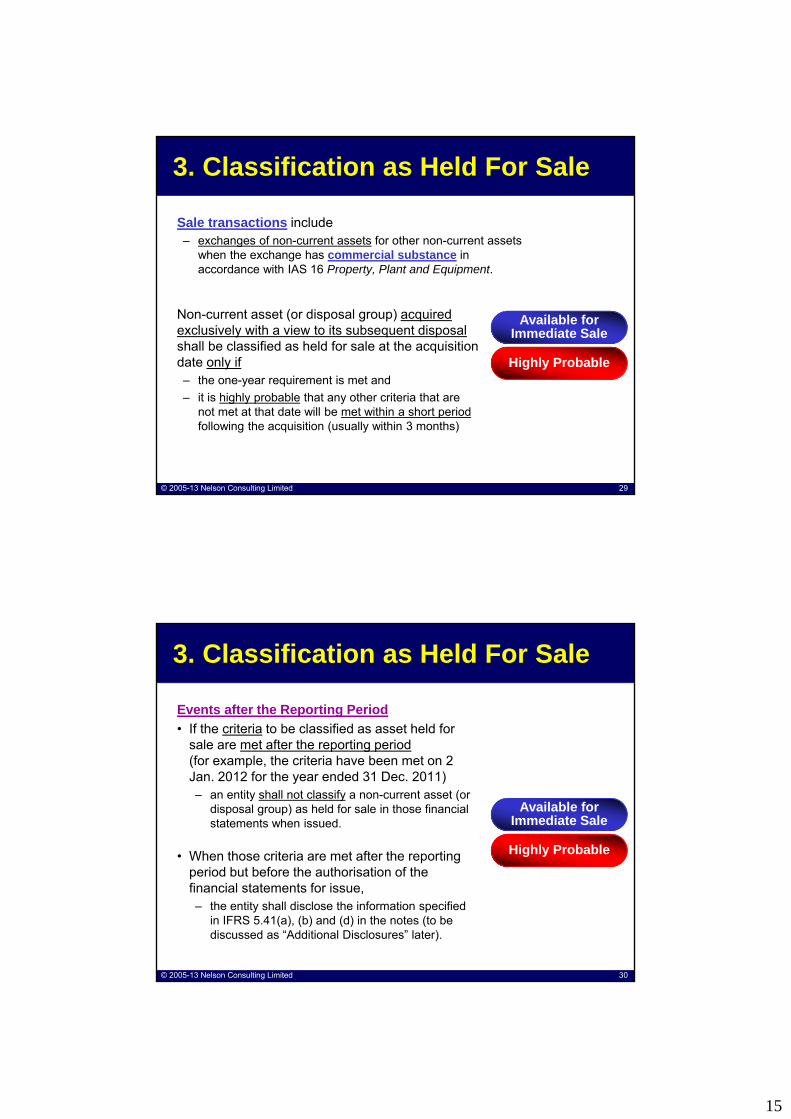

Sale transactions includendash exchanges of non-current assets for other non-current assets

when the exchange has commercial substance in accordance with IAS 16 Property Plant and Equipment

3 Classification as Held For Sale

Available for Immediate Sale

Highly Probable

Non-current asset (or disposal group) acquired exclusively with a view to its subsequent disposalshall be classified as held for sale at the acquisition date only ifndash the one-year requirement is met and

ndash it is highly probable that any other criteria that are not met at that date will be met within a short periodfollowing the acquisition (usually within 3 months)

copy 2005-13 Nelson Consulting Limited 30

Events after the Reporting Period

bull If the criteria to be classified as asset held for sale are met after the reporting period(for example the criteria have been met on 2 Jan 2012 for the year ended 31 Dec 2011)ndash an entity shall not classify a non-current asset (or

disposal group) as held for sale in those financial statements when issued

bull When those criteria are met after the reporting period but before the authorisation of the financial statements for issue ndash the entity shall disclose the information specified

in IFRS 541(a) (b) and (d) in the notes (to be discussed as ldquoAdditional Disclosuresrdquo later)

3 Classification as Held For Sale

Available for Immediate Sale

Highly Probable

16

copy 2005-13 Nelson Consulting Limited 31

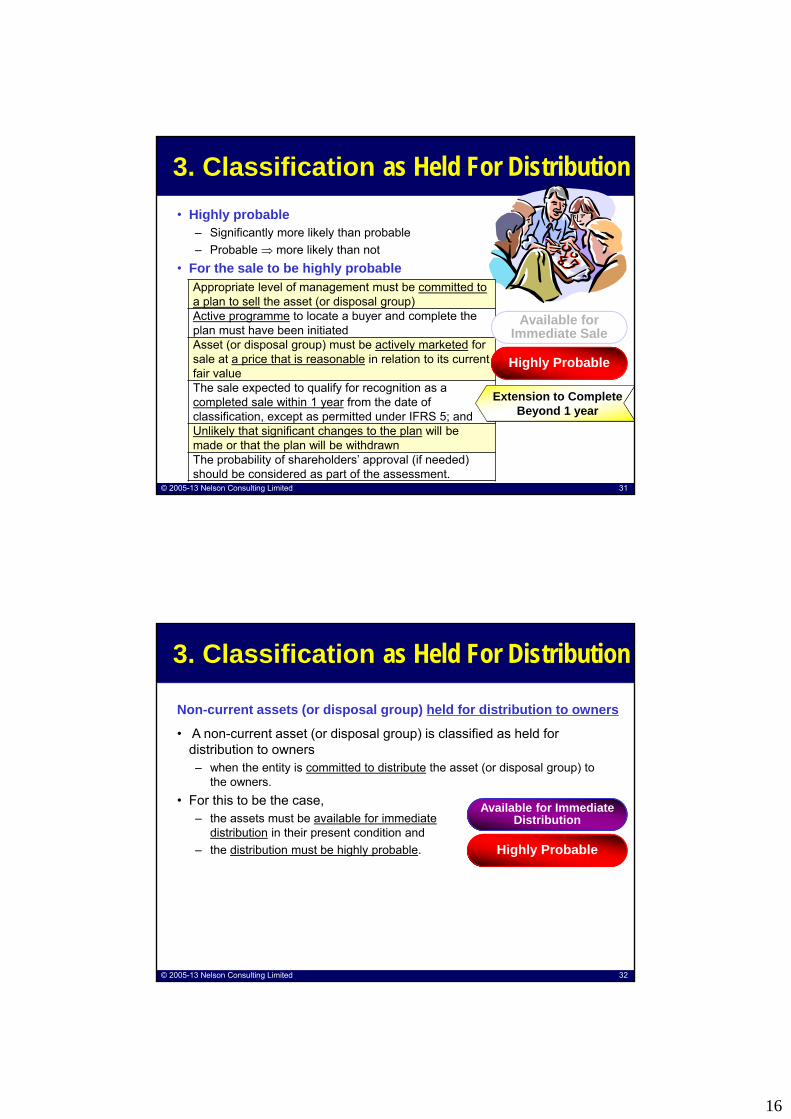

3 Classification as Held For Distribution

bull Highly probablendash Significantly more likely than probable

ndash Probable more likely than not

bull For the sale to be highly probableAppropriate level of management must be committed to a plan to sell the asset (or disposal group)Active programme to locate a buyer and complete the plan must have been initiatedAsset (or disposal group) must be actively marketed for sale at a price that is reasonable in relation to its current fair valueThe sale expected to qualify for recognition as a completed sale within 1 year from the date of classification except as permitted under IFRS 5 andUnlikely that significant changes to the plan will be made or that the plan will be withdrawnThe probability of shareholdersrsquo approval (if needed) should be considered as part of the assessment

Extension to Complete Extension to Complete Beyond 1 year

Highly Probable

Available for Immediate Sale

copy 2005-13 Nelson Consulting Limited 32

3 Classification as Held For Distribution

Non-current assets (or disposal group) held for distribution to owners

bull A non-current asset (or disposal group) is classified as held for distribution to owners ndash when the entity is committed to distribute the asset (or disposal group) to

the owners

bull For this to be the case ndash the assets must be available for immediate

distribution in their present condition and

ndash the distribution must be highly probable

Available for Immediate Distribution

Highly Probable

17

copy 2005-13 Nelson Consulting Limited 33

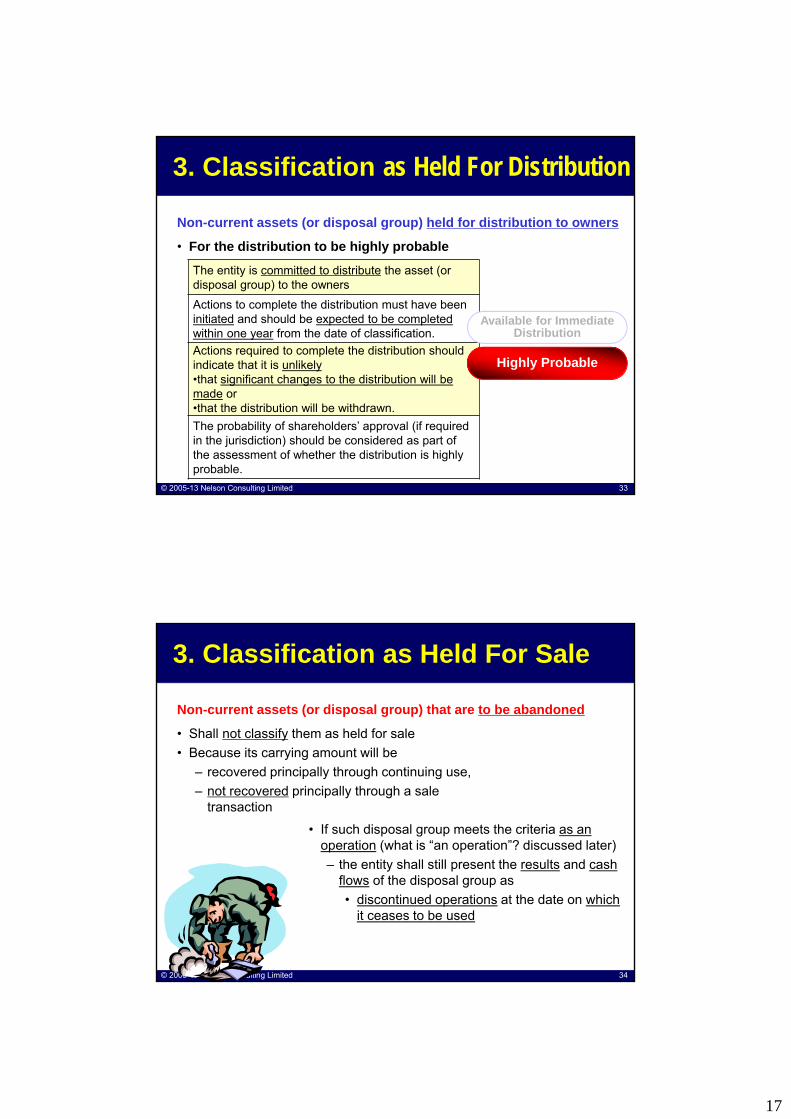

3 Classification as Held For Distribution

Non-current assets (or disposal group) held for distribution to owners

bull For the distribution to be highly probable

The entity is committed to distribute the asset (or disposal group) to the owners

Actions to complete the distribution must have been initiated and should be expected to be completed within one year from the date of classification

Actions required to complete the distribution should indicate that it is unlikelybullthat significant changes to the distribution will be made or bullthat the distribution will be withdrawn

The probability of shareholdersrsquo approval (if required in the jurisdiction) should be considered as part of the assessment of whether the distribution is highly probable

Available for Immediate Distribution

Highly Probable

copy 2005-13 Nelson Consulting Limited 34

3 Classification as Held For Sale

Non-current assets (or disposal group) that are to be abandoned

bull If such disposal group meets the criteria as an operation (what is ldquoan operationrdquo discussed later)

ndash the entity shall still present the results and cash flows of the disposal group as

bull discontinued operations at the date on which it ceases to be used

bull Shall not classify them as held for sale

bull Because its carrying amount will be

ndash recovered principally through continuing use

ndash not recovered principally through a sale transaction

18

copy 2005-13 Nelson Consulting Limited 35

3 Classification as Held For Sale

Non-current assets (or disposal group) that are to be abandoned

bull Non-current assets (or disposal groups) to be abandoned include

ndash non-current assets (disposal group)

bull used to the end of their economic life

bull closed rather than sold

bull An entity shall not account for a non-current asset thathas been temporarily taken out of use as if it had been abandoned

Not within IFRS 5

copy 2005-13 Nelson Consulting Limited 36

4 Measurement

bull An entity shall measure non-current asset (or disposal group) classified as held for sale at the lower of itsbull Carrying amount and

bull Fair value less costs to sell (IFRS 515)

bull When the sale is expected to occur beyond one year

ndash the entity shall measure the costs to sell at their present value

bull Any increase in the present value of the costs to sell that arises from the passage of time shall be presented in profit or loss as a financing cost

Classification

Measurement

Presentation

Classification

Measurement

Presentation

Any implication on

ndash newly acquired assets

ndash assets acquired under business combination

bull An entity shall measure a non-current asset (or disposal group) classified as held for distribution to owners at the lower of itsbull Carrying amount and

bull Fair value less costs to distribute (IFRS 515A)

19

copy 2005-13 Nelson Consulting Limited 37

4 Measurement

bull An entity shall not depreciate (or amortise) a non-current asset while

ndash it is classified as held for sale or

ndash while it is part of a disposal group classified as held for sale

bull Interest and other expenses attributable to the liabilities of a disposal group classified as held for sale

ndash shall continue to be recognised

copy 2005-13 Nelson Consulting Limited 38

4 Measurement

Annual Report 2012 ndash Notes to financial statements Assets acquired in exchange for loansndash Non-financial assets acquired in exchange for loans as part of an orderly

realisation are recorded as assets held for sale and reported in lsquoOther assetsrsquo if bull the carrying amounts of the assets are recovered principally through sale bull the assets are available for sale in their present condition and bull their sale is highly probable

ndash The asset acquired is recorded at the lower ofbull its fair value less costs to sell and bull the carrying amount of the loan (net of impairment allowance) at the date of

exchange ndash No depreciation is charged in respect of assets held for sale ndash Any subsequent write-down of the acquired asset to fair value less costs to sell

is recognised in the income statement in lsquoOther operating incomersquondash Any subsequent increase in the fair value less costs to sell to the extent this

does not exceed the cumulative write-down is also recognised in lsquoOther operating incomersquo together with any realised gains or losses on disposal

Case

20

copy 2005-13 Nelson Consulting Limited 39

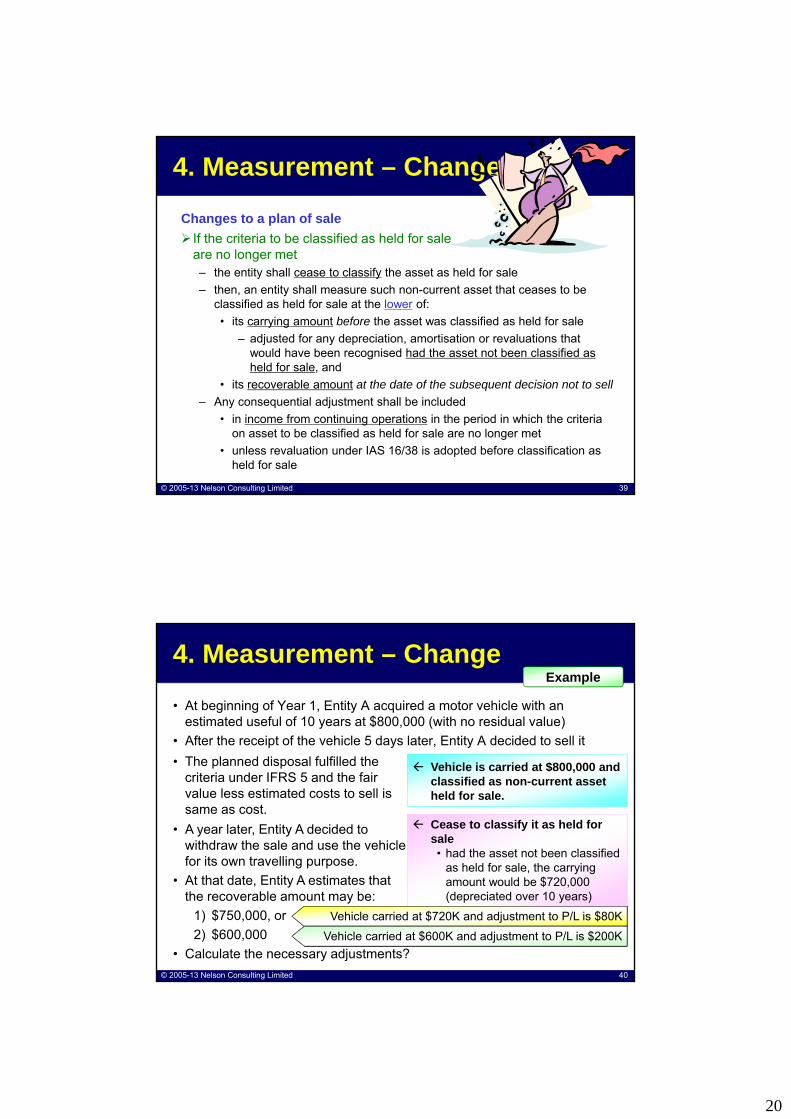

4 Measurement ndash Change

Changes to a plan of sale

If the criteria to be classified as held for saleare no longer metndash the entity shall cease to classify the asset as held for sale

ndash then an entity shall measure such non-current asset that ceases to be classified as held for sale at the lower of

bull its carrying amount before the asset was classified as held for sale

ndash adjusted for any depreciation amortisation or revaluations that would have been recognised had the asset not been classified as held for sale and

bull its recoverable amount at the date of the subsequent decision not to sell

ndash Any consequential adjustment shall be included

bull in income from continuing operations in the period in which the criteria on asset to be classified as held for sale are no longer met

bull unless revaluation under IAS 1638 is adopted before classification as held for sale

copy 2005-13 Nelson Consulting Limited 40

bull At beginning of Year 1 Entity A acquired a motor vehicle with an estimated useful of 10 years at $800000 (with no residual value)

bull After the receipt of the vehicle 5 days later Entity A decided to sell it

4 Measurement ndash ChangeExample

Vehicle is carried at $800000 and classified as non-current asset held for sale

Cease to classify it as held for salebull had the asset not been classified

as held for sale the carrying amount would be $720000 (depreciated over 10 years)

bull A year later Entity A decided to withdraw the sale and use the vehicle for its own travelling purpose

bull At that date Entity A estimates that the recoverable amount may be

1) $750000 or

2) $600000

bull Calculate the necessary adjustments

bull The planned disposal fulfilled the criteria under IFRS 5 and the fair value less estimated costs to sell is same as cost

Vehicle carried at $720K and adjustment to PL is $80K

Vehicle carried at $600K and adjustment to PL is $200K

21

copy 2005-13 Nelson Consulting Limited 41

4 Measurement ndash Change

Changes to a plan of sale

Removal from disposal group

bull If an entity removes an individual asset or liabilityfrom a disposal group classified as held for salendash the remaining assets and liabilities of the disposal group to be sold

shall continue to be measured as a group only if

bull the group (as a whole) meets the criteria on asset to be classified as held for sale

ndash Otherwise the remaining non-current assets of the group that individually meet the criteria to be classified as held for sale

bull shall be measured individually at the lower of their carrying amounts and fair values less costs to sell at that date

ndash Any non-current assets that do not meet the criteria shall cease to be classified as held for sale

copy 2005-13 Nelson Consulting Limited 42

5 Presentation

2 Presenting discontinued operations

3 Additional disclosuresClassification

Measurement

Presentation

Classification

Measurement

Presentation

1 Presenting non-current asset(or disposal group) held for sale

22

copy 2005-13 Nelson Consulting Limited 43

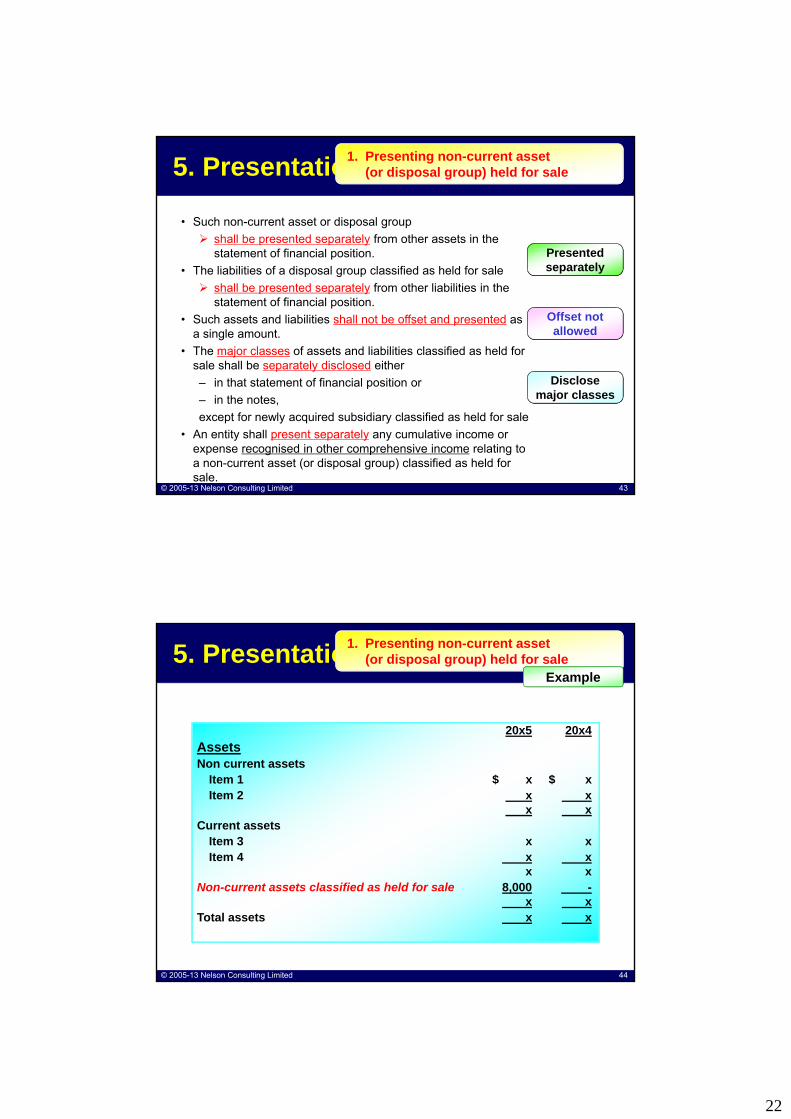

5 Presentation

bull Such non-current asset or disposal group

shall be presented separately from other assets in the statement of financial position

bull The liabilities of a disposal group classified as held for sale

shall be presented separately from other liabilities in the statement of financial position

bull Such assets and liabilities shall not be offset and presented as a single amount

bull The major classes of assets and liabilities classified as held for sale shall be separately disclosed either

ndash in that statement of financial position or

ndash in the notes

except for newly acquired subsidiary classified as held for sale

bull An entity shall present separately any cumulative income or expense recognised in other comprehensive income relating to a non-current asset (or disposal group) classified as held for sale

1 Presenting non-current asset(or disposal group) held for sale

Presented separately

Offset not allowed

Disclose major classes

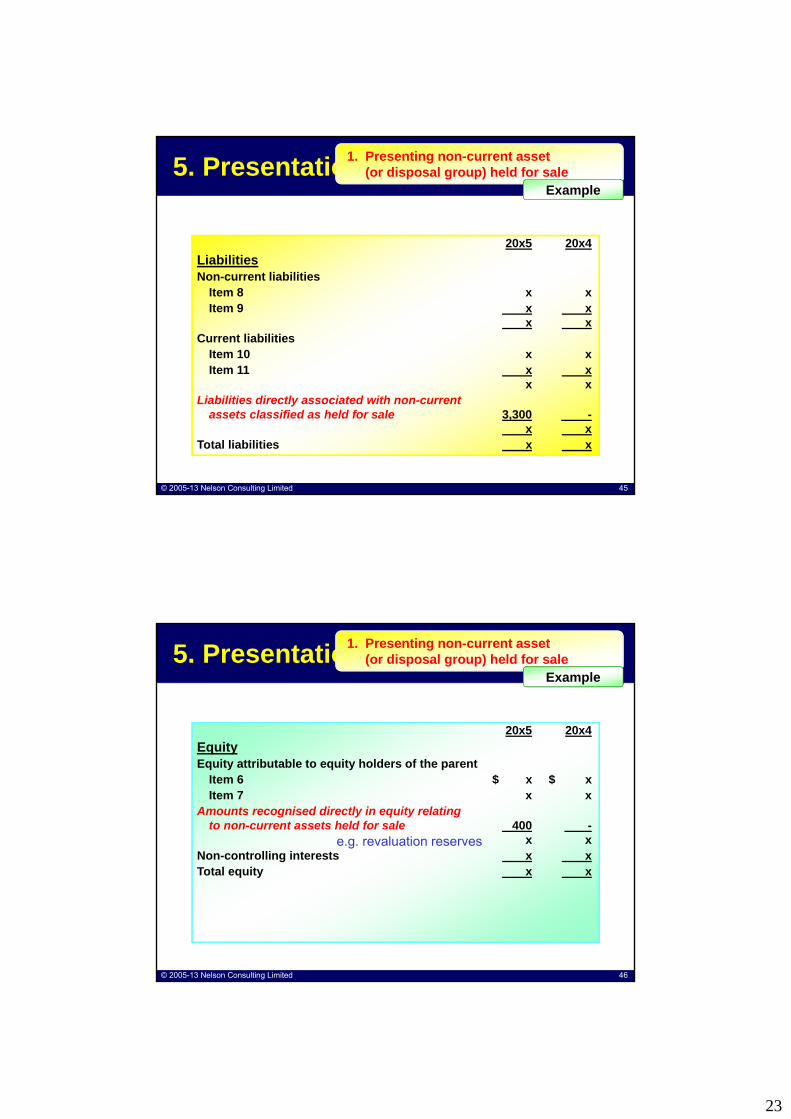

copy 2005-13 Nelson Consulting Limited 44

5 Presentation

20x5 20x4

AssetsNon current assets

Item 1 $ x $ xItem 2 x x

x xCurrent assets

Item 3 x xItem 4 x x

x xNon-current assets classified as held for sale 8000 -

x xTotal assets x x

1 Presenting non-current asset(or disposal group) held for sale

Example

23

copy 2005-13 Nelson Consulting Limited 45

20x5 20x4

LiabilitiesNon-current liabilities

Item 8 x xItem 9 x x

x xCurrent liabilities

Item 10 x xItem 11 x x

x xLiabilities directly associated with non-current

assets classified as held for sale 3300 -x x

Total liabilities x x

5 Presentation1 Presenting non-current asset

(or disposal group) held for saleExample

copy 2005-13 Nelson Consulting Limited 46

20x5 20x4

EquityEquity attributable to equity holders of the parent

Item 6 $ x $ xItem 7 x x

Amounts recognised directly in equity relatingto non-current assets held for sale 400 -

x xNon-controlling interests x xTotal equity x x

5 Presentation

eg revaluation reserves

1 Presenting non-current asset(or disposal group) held for sale

Example

24

copy 2005-13 Nelson Consulting Limited 47

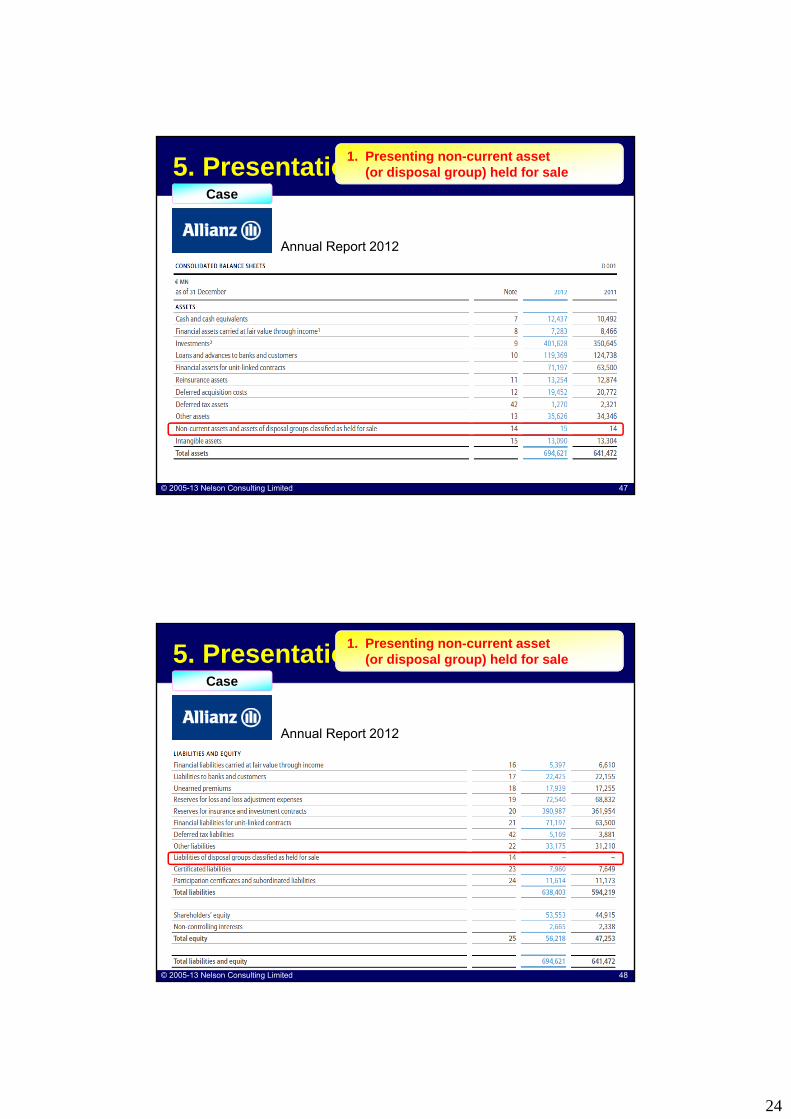

Annual Report 2012

5 PresentationCase

1 Presenting non-current asset(or disposal group) held for sale

copy 2005-13 Nelson Consulting Limited 48

Annual Report 2012

5 PresentationCase

1 Presenting non-current asset(or disposal group) held for sale

25

copy 2005-13 Nelson Consulting Limited 49

5 Presentation

bull If the disposal group is a newly acquired subsidiary that meets the criteria to be classified as held for sale on acquisition disclosure of the major classes of assets and liabilities

is not required

1 Presenting non-current asset(or disposal group) held for sale

Presented separately

Offset not allowed

Disclose major classes

bull Prior periodrsquos presentation shall not be revised An entity shall not reclassify or re-present amounts

presented for non-current assets (or for the assets and liabilities of disposal groups) classified as held for sale in the statements of financial position for prior periods to reflect the classification in the statement of financial position for the latest period presented

(except for associate and jointly controlled entitiesaccounted for under equity method or proportionate consolidation)

Any special

copy 2005-13 Nelson Consulting Limited 50

5 Presentation

bull An investment in an associate (jointly controlled entities) shall not be accounted for using the equity method (andor proportionate consolidation) when

ndash the investment is classified as held for sale in accordance with IFRS 5

bull Such investments described above

ndash shall be accounted for in accordance with IFRS 5

1 Presenting non-current asset(or disposal group) held for sale

However when they are NOT finally

disposed of or met IFRS 5 again helliphellip

Specific requirements on associate and jointly controlled entity

26

copy 2005-13 Nelson Consulting Limited 51

5 Presentation

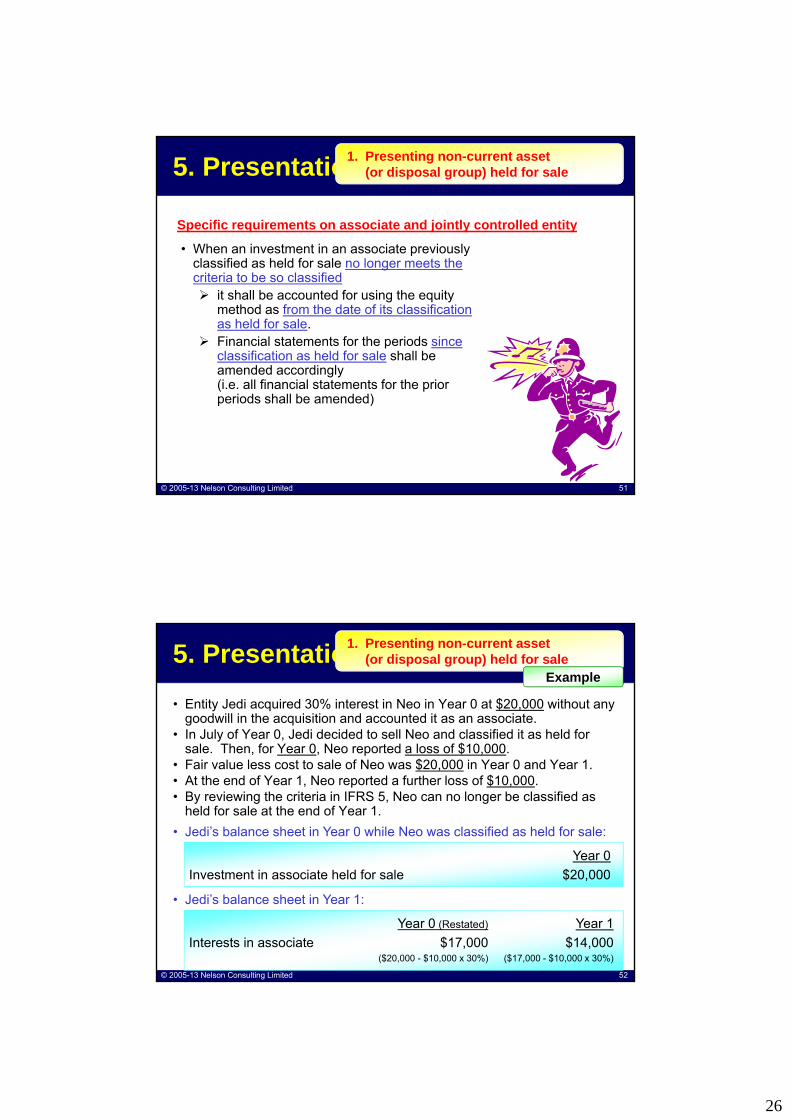

bull When an investment in an associate previously classified as held for sale no longer meets the criteria to be so classified it shall be accounted for using the equity

method as from the date of its classification as held for sale

Financial statements for the periods since classification as held for sale shall be amended accordingly(ie all financial statements for the prior periods shall be amended)

1 Presenting non-current asset(or disposal group) held for sale

Specific requirements on associate and jointly controlled entity

copy 2005-13 Nelson Consulting Limited 52

bull Entity Jedi acquired 30 interest in Neo in Year 0 at $20000 without any goodwill in the acquisition and accounted it as an associate

bull In July of Year 0 Jedi decided to sell Neo and classified it as held for sale Then for Year 0 Neo reported a loss of $10000

bull Fair value less cost to sale of Neo was $20000 in Year 0 and Year 1bull At the end of Year 1 Neo reported a further loss of $10000bull By reviewing the criteria in IFRS 5 Neo can no longer be classified as

held for sale at the end of Year 1

5 Presentation

Year 0

Investment in associate held for sale $20000

bull Jedirsquos balance sheet in Year 0 while Neo was classified as held for sale

Year 0 (Restated) Year 1

Interests in associate $17000 $14000($20000 - $10000 x 30) ($17000 - $10000 x 30)

bull Jedirsquos balance sheet in Year 1

1 Presenting non-current asset(or disposal group) held for sale

Example

27

copy 2005-13 Nelson Consulting Limited 53

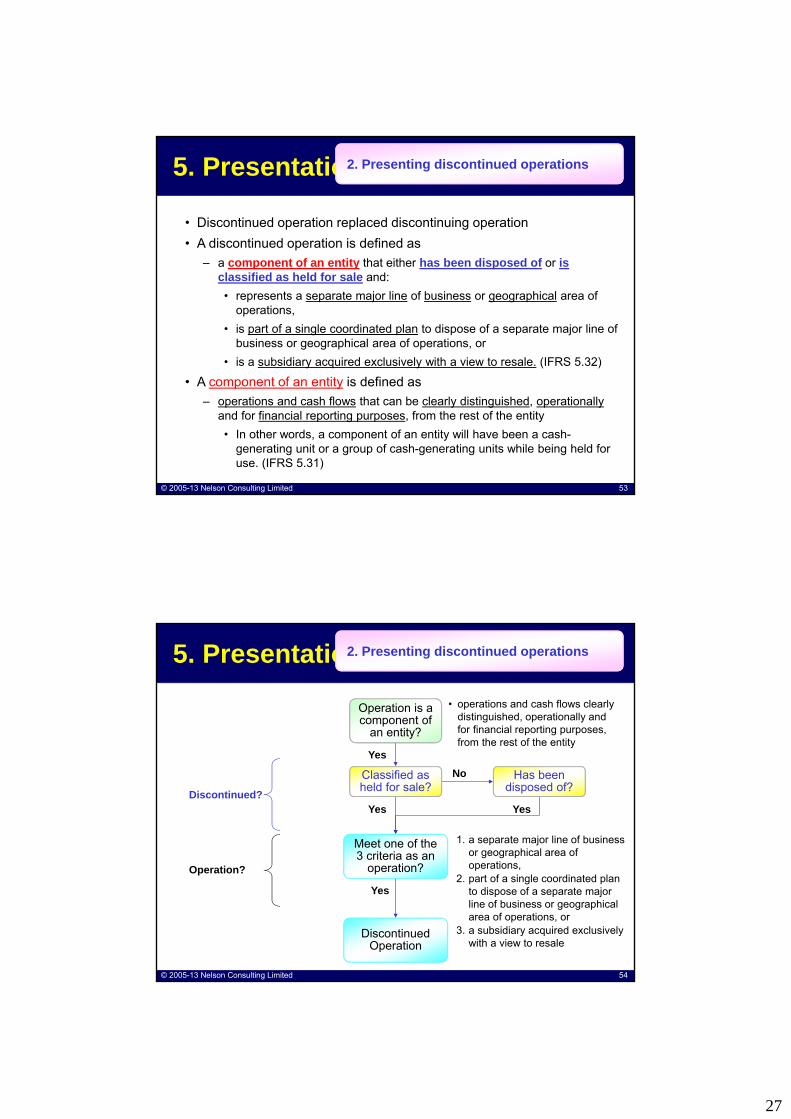

5 Presentation2 Presenting discontinued operations

bull Discontinued operation replaced discontinuing operation

bull A discontinued operation is defined as

ndash a component of an entity that either has been disposed of or is classified as held for sale and

bull represents a separate major line of business or geographical area of operations

bull is part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations or

bull is a subsidiary acquired exclusively with a view to resale (IFRS 532)

bull A component of an entity is defined as

ndash operations and cash flows that can be clearly distinguished operationallyand for financial reporting purposes from the rest of the entity

bull In other words a component of an entity will have been a cash-generating unit or a group of cash-generating units while being held for use (IFRS 531)

copy 2005-13 Nelson Consulting Limited 54

5 Presentation

Operation is a component of

an entity

2 Presenting discontinued operations

Has beendisposed of

Classified asheld for sale

Meet one of the 3 criteria as an

operation

Discontinued Operation

YesYes

bull operations and cash flows clearly distinguished operationally and for financial reporting purposes from the rest of the entity

1 a separate major line of business or geographical area of operations

2 part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations or

3 a subsidiary acquired exclusively with a view to resale

Yes

No

Yes

Discontinued

Operation

28

copy 2005-13 Nelson Consulting Limited 55

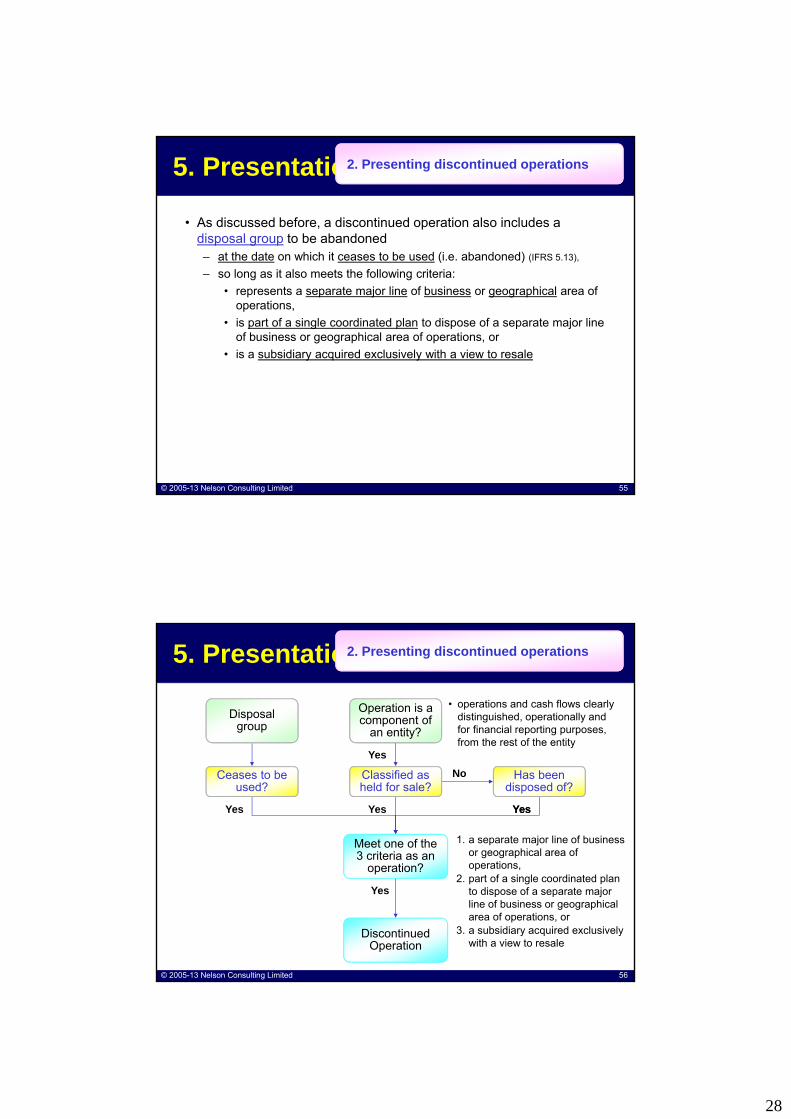

5 Presentation

bull As discussed before a discontinued operation also includes a disposal group to be abandonedndash at the date on which it ceases to be used (ie abandoned) (IFRS 513)

ndash so long as it also meets the following criteria

bull represents a separate major line of business or geographical area of operations

bull is part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations or

bull is a subsidiary acquired exclusively with a view to resale

2 Presenting discontinued operations

copy 2005-13 Nelson Consulting Limited 56

5 Presentation

Operation is a component of

an entity

2 Presenting discontinued operations

Has beendisposed of

Classified asheld for sale

YesYes

Disposal group

Ceases to be used

Yes

bull operations and cash flows clearly distinguished operationally and for financial reporting purposes from the rest of the entity

No

Yes

Meet one of the 3 criteria as an

operation

Discontinued Operation

Yes

1 a separate major line of business or geographical area of operations

2 part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations or

3 a subsidiary acquired exclusively with a view to resale

Yes

29

copy 2005-13 Nelson Consulting Limited 57

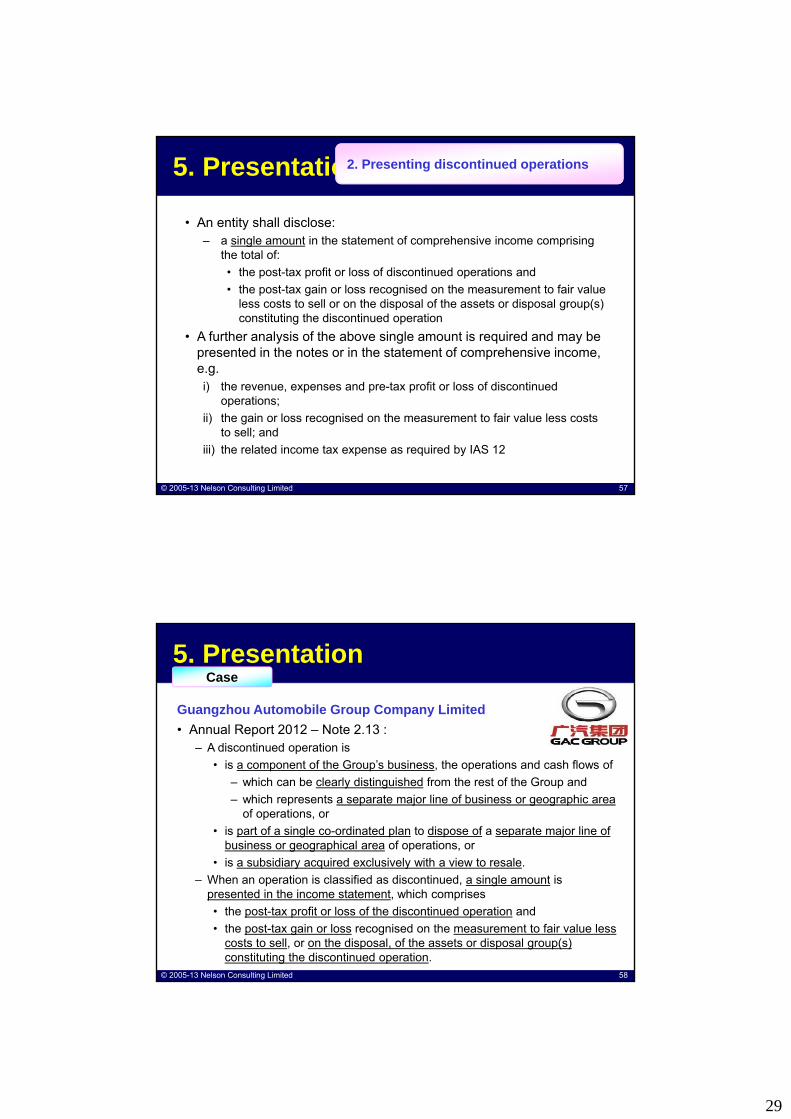

5 Presentation

bull An entity shall disclosendash a single amount in the statement of comprehensive income comprising

the total of

bull the post-tax profit or loss of discontinued operations and

bull the post-tax gain or loss recognised on the measurement to fair value less costs to sell or on the disposal of the assets or disposal group(s) constituting the discontinued operation

bull A further analysis of the above single amount is required and may be presented in the notes or in the statement of comprehensive income egi) the revenue expenses and pre-tax profit or loss of discontinued

operations

ii) the gain or loss recognised on the measurement to fair value less costs to sell and

iii) the related income tax expense as required by IAS 12

2 Presenting discontinued operations

copy 2005-13 Nelson Consulting Limited 58

5 Presentation

Guangzhou Automobile Group Company Limited

Case

bull Annual Report 2012 ndash Note 213 ndash A discontinued operation is

bull is a component of the Grouprsquos business the operations and cash flows of

ndash which can be clearly distinguished from the rest of the Group and

ndash which represents a separate major line of business or geographic area of operations or

bull is part of a single co-ordinated plan to dispose of a separate major line of business or geographical area of operations or

bull is a subsidiary acquired exclusively with a view to resale

ndash When an operation is classified as discontinued a single amount is presented in the income statement which comprises

bull the post-tax profit or loss of the discontinued operation and

bull the post-tax gain or loss recognised on the measurement to fair value less costs to sell or on the disposal of the assets or disposal group(s) constituting the discontinued operation

30

copy 2005-13 Nelson Consulting Limited 59

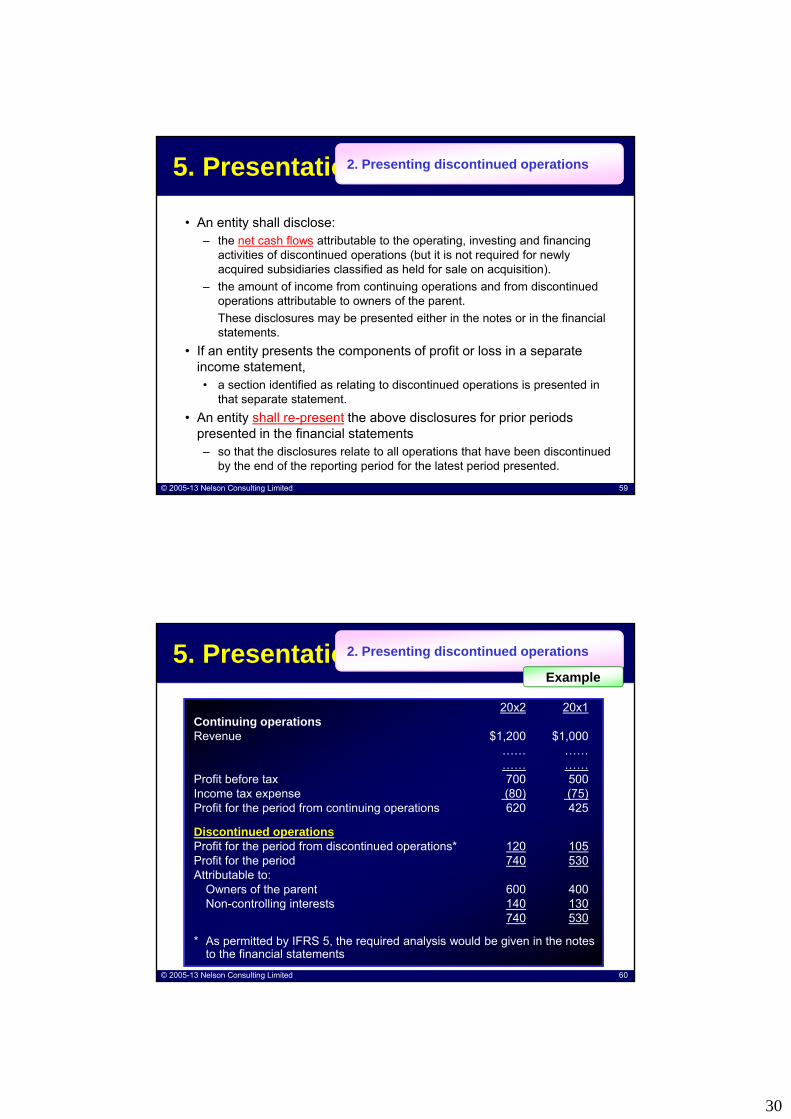

5 Presentation

bull An entity shall disclosendash the net cash flows attributable to the operating investing and financing

activities of discontinued operations (but it is not required for newly acquired subsidiaries classified as held for sale on acquisition)

ndash the amount of income from continuing operations and from discontinued operations attributable to owners of the parent

These disclosures may be presented either in the notes or in the financial statements

bull If an entity presents the components of profit or loss in a separate income statementbull a section identified as relating to discontinued operations is presented in

that separate statement

bull An entity shall re-present the above disclosures for prior periods presented in the financial statementsndash so that the disclosures relate to all operations that have been discontinued

by the end of the reporting period for the latest period presented

2 Presenting discontinued operations

copy 2005-13 Nelson Consulting Limited 60

5 Presentation

20x2 20x1Continuing operationsRevenue $1200 $1000

helliphellip helliphelliphelliphellip helliphellip

Profit before tax 700 500Income tax expense (80) (75)Profit for the period from continuing operations 620 425

Discontinued operationsProfit for the period from discontinued operations 120 105Profit for the period 740 530Attributable to

Owners of the parent 600 400Non-controlling interests 140 130

740 530

As permitted by IFRS 5 the required analysis would be given in the notes to the financial statements

2 Presenting discontinued operations

Example

31

copy 2005-13 Nelson Consulting Limited 61

5 Presentation

bull Prohibit retroactive classification of an operation as discontinued

ndash when the criteria for that classification are not met until after the reporting period

2 Presenting discontinued operations

copy 2005-13 Nelson Consulting Limited 62

5 Presentation

Adjustments in current period relating to amounts previously presented in discontinued operations

ndash Such adjustments (if directly related to the disposal of a discontinued operation in a prior period) shall be classified separately in discontinued operations

ndash The nature and amount of such adjustments shall be disclosedbull Examples of circumstances in which these adjustments may arise

include the resolution of uncertainties

ndash that arise from the terms of the disposal transaction(say resolution of purchase price adjustments)

ndash arise from and are directly related to the operations of the component before its disposal(say environmental and product warranty obligations)

2 Presenting discontinued operations

32

copy 2005-13 Nelson Consulting Limited 63

5 Presentation

Subsidiary is a disposal group that meets the definition of a discontinued operation

ndash An entity that is committed to a sale plan involving loss of control of a subsidiary shall disclose the information required in IFRS 533-36

bull when the subsidiary is a disposal group that meets the definition of a discontinued operation in accordance with IFRS 532 (IFRS 536A)

2 Presenting discontinued operations

copy 2005-13 Nelson Consulting Limited 64

5 Presentation

Gains or Losses Relating to Continuing Operations

bull Any gain or loss on the remeasurement of a non-current asset (or disposal group) classified as held for sale that does not meet the definition of a discontinued operation

shall be included in profit or loss from continuing operations

2 Presenting discontinued operations

33

copy 2005-13 Nelson Consulting Limited 65

Non-Current Assets Held for Sale and Discontinued Operationsndash Net income (loss) from discontinued operations includes

bull the net total of net income (loss) before tax from discontinued operations and discontinued operations tax expense

ndash Similarly the net cash flows attributable to the operating investing and financing activities of discontinued operations have to be presented separately

ndash The comparative income statement and cash flow information is re-presented for discontinued operations

Deutsche Bank ndash Annual Report 2012

5 Presentation2 Presenting discontinued operations

Case

copy 2005-13 Nelson Consulting Limited 66

5 Presentation3 Additional disclosures

bull An entity shall disclose the following information in the notes in the period in which a non-current asset (or disposal group) has been either classified as held for sale or solda) a description of the non-current asset (or disposal group)

b) a description of the facts and circumstances of the sale or leading to the expected disposal and the expected manner and timing of that disposal

c) the gain or loss recognised in respect of the impairment loss (or reversal) and if not separately presented on the statement of comprehensive income the caption in the statement of comprehensive income that includes that gain or loss

d) if applicable the reportable segment in which the non-current asset (or disposal group) is presented in accordance with IFRS 8 Operating Segments

34

copy 2005-13 Nelson Consulting Limited 67

Operating Segments(IFRS 8)

copy 2005-13 Nelson Consulting Limited 68

Background

bull IFRS 8 arises from the IASBrsquos consideration of ndash FASB Statement No 131 Disclosures about Segments of

an Enterprise and Related Information (SFAS 131 of United States) issued in 1997 compared with IAS 14 Segment Reporting which is similar to IAS 14

bull IFRS 8 achieves convergence with the requirements of SFAS 131ndash The wording of IFRS 8 is the same as that of SFAS 131

except for changes necessary to make the terminology consistent with that in other IFRSs

35

copy 2005-13 Nelson Consulting Limited 69

2 Operating Segments

4 Disclosure

1 Core Principle and Scope

Todayrsquos Agenda

3 Reportable Segments

5 Measurement

6 Entity-Wide Disclosures

copy 2005-13 Nelson Consulting Limited 70

1 Core Principle and Scope

Core Principle

bull An entity shall disclose information to enable users of its financial statements to evaluate

ndash the nature and financial effects of the business activities in which it engages and

ndash the economic environments in which it operates

36

copy 2005-13 Nelson Consulting Limited 71

1 Core Principle and Scope

Scope

bull IFRS 8 applies tondash the separate or individual financial statements of

an entity with listed debt and equity

ndash the consolidated financial satements of a group with a parent with listed debt and equity

ndash The segment information of an entity which chooses to follow IFRS 8

bull If a financial report contains both the parentrsquos consolidated financial statements and separate financial statements

ndash segment information is required only in the consolidated financial statements

copy 2005-13 Nelson Consulting Limited 72

2 Operating Segments

bull An operating segment is a component of an entity

a) that engages in business activities from which it mayearn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity)

b) whose operating results are regularly reviewed by the entityrsquos chief operating decision maker to

bull make decisions about resources to be allocated to the segment and

bull assess its performance and

c) for which discrete financial information is available

A business activity might have not yet earned any revenue

For example CEO COO or a group of executive directors

bull Not every part of an entity is necessarily an operating segment or part of an operating segment say corporate headquarter

Operating Segments

Not necessary be geographical areas or products

37

copy 2005-13 Nelson Consulting Limited 73

Interim Report 2009

bull HKFRS 8 requires segment disclosure

ndash to be based on the way the Grouprsquos chief operating decisionmaker regards and manages the Group

ndash with the amounts reported for each reportable segment being the measures reported to the Grouprsquos chief operating decision maker for the purposes of assessing segment performance and making decisions about operating matters

bull This contrasts with the presentation of segment information in prior years which was based on a disaggregation of the Grouprsquos financialstatements into segments based on related services

bull The adoption of HKFRS 8 has resulted in the presentation of segment information in a manner that is more consistent with internal reporting provided to the Grouprsquos most senior executive management

2 Operating SegmentsCase

IFRS 8

IAS 14

copy 2005-13 Nelson Consulting Limited 74

3 Reporting Segments

bull An entity shall report separately information about each operating segment that

a) has been identified as operating segment or results from aggregating two or more of those segments under the aggregation criteria and

b) exceeds the quantitative thresholds(ldquo10 or more testrdquo)

bull There are also other situations in which separate information about an operating segment shall be reported

Reportable Segment

Aggregation Criteria

Operating Segments

Quantitative Thresholds

Other Situations

38

copy 2005-13 Nelson Consulting Limited 75

3 Reporting Segments

bull Operating segments often exhibit similar long-term financial performance if they have similar economic characteristics

ndash For example similar long-term average gross margins for two operating segments would be expected if their economic characteristics were similar

Aggregation Criteria

copy 2005-13 Nelson Consulting Limited 76

Aggregation Criteria

bull Two or more operating segments may be aggregated into a single operating segment if ‒ aggregation is consistent with the core principle of

IFRS 8

‒ the segments have similar economic characteristics and

‒ the segments are similar in each of the following respects

a) the nature of the products and services

b) the nature of the production processes

c) the type or class of customer for their products and services

d) the methods used to distribute their products or provide their services and

e) if applicable the nature of the regulatory environment eg banking or public utilities

3 Reporting Segments

Aggregate segments if desired

39

copy 2005-13 Nelson Consulting Limited 77

3 Reporting Segments

bull An entity shall report separately information about an operating segment that meets any of the following quantitative thresholds

a) Its reported revenue (including both sales to external customers and intersegment sales or transfers) is 10 or more of the combined revenue(internal and external) of all operating segments

b) The absolute amount of its reported profit or loss is 10 or more of the greater in absolute amount of

i) the combined reported profit of all operating segments that did not report a loss and

ii) the combined reported loss of all operating segments that reported a loss

c) Its assets are 10 or more of the combined assetsof all operating segments

Quantitative Thresholds

copy 2005-13 Nelson Consulting Limited 78

3 Reporting Segments

Combination of Segments

bull An entity may combine information (combine information about operating segments that do not meet the quantitative thresholds with information about other operating segments that do not meet the quantitative thresholds) to produce a reportable segment

ndash only if the operating segments

bull have similar economic characteristics and

bull share a majority of the aggregation criteria

bull If the total external revenue reported by operating segments constitutes less than 75 of the entityrsquos revenue

ndash additional operating segments shall be identified as reportable segments (even if they do not meet the quantitative thresholds) until at least 75 of the entityrsquos revenue is included in reportable segments

Other Situations

40

copy 2005-13 Nelson Consulting Limited 79

3 Reporting Segments

Not Reportable Segments

bull Information about other business activities and operating segments that are not reportable

ndash shall be combined and disclosed in an ldquoall other segmentsrdquo category separately from other reconciling items in the reconciliations required by IFRS 828

bull The sources of the revenue included in the ldquoall other segmentsrdquo category shall be described

bull If management judges that an operating segment identified as a reportable segment in the immediately preceding period is of continuing significance

ndash information about that segment shall continue to be reported separately in the current period even if it no longer meets the criteria for reportability

Other Situations

copy 2005-13 Nelson Consulting Limited 80

4 Disclosure

bull To give effect to the core principle an entity shalldisclose the following for each period for which an income statement is presented

a) general information as described in IFRS 8

b) information about

bull reported segment profit or loss including specified revenues and expenses included in reported segment profit or loss

bull segment assets and

bull the basis of measurement and

c) reconciliations of the totals of

bull segment revenues

bull reported segment profit or loss

bull segment assets and

bull other material segment items

to corresponding entity amounts

General Information

Other Information

Reconciliations

41

copy 2005-13 Nelson Consulting Limited 81

4 Disclosure ndash General Information

bull An entity shall disclose the following general information

a) factors used to identify the entityrsquos reportable segments including the basis of organisationfor example

bull whether management has chosen to organise the entity around differences in products and services geographical areas regulatory environments or a combination of factors and

bull whether operating segments have been aggregated and

b) types of products and services from which each reportable segment derives its revenues

General Information

copy 2005-13 Nelson Consulting Limited 82

4 Disclosure ndash Other Information

bull An entity shall report a measure of profit or loss and total assets for each reportable segment

bull An entity shall report a measure of liabilities for each reportable segment if such an amount is regularly provided to the chief operating decision maker

Other Information

42

copy 2005-13 Nelson Consulting Limited 83

4 Disclosure ndash Other Information

bull An entity shall also disclose the following about each reportable segment if the specified amounts are included in the measure of segment profit or loss reviewed by the chief operating decision maker or are otherwise regularly provided to the chief operating decision maker even if not included in that measure of segment profit or loss

a) revenues from external customers

b) revenues from transactions with other operating segments of the same entity

c) interest revenue

d) interest expense

e) depreciation and amortisation

f) material items of income and expense disclosed in accordance with IAS 1

g) the entityrsquos interest in the profit or loss of associates and joint ventures accounted for by the equity method

h) income tax expense or income and

i) material non-cash items other than depreciation and amortisation

Other Information

copy 2005-13 Nelson Consulting Limited 84

4 Disclosure ndash Reconciliations

bull Reconciliations of the amounts in the statement of financial position for reportable segments

ndash to the amounts in the entityrsquos statement of financial position are required for each dateat which a statement of financial position is presented

bull Previously reported information for prior periods shall be restated

Reconciliations

43

copy 2005-13 Nelson Consulting Limited 85

5 Measurement

bull The amount of each segment item reported shall be the measure reported to the chief operating decision maker

ndash for the purposes of making decisions about allocating resources to the segment and assessing its performance

bull Compared with IAS 14

ndash IAS 14 required segment information to be prepared in conformity with the accounting policies adopted for preparing and presenting the financial statements of the consolidated group or entity

ndash IAS 14 defines segment revenue segment expense segment result segment assets and segment liabilities

ndash IFRS 8 does not define these terms but requires an explanation of how segment profit or loss segment assets and segment liabilities are measured for each reportable segment

copy 2005-13 Nelson Consulting Limited 86

5 Measurement

bull Adjustments and eliminations made in preparing an entityrsquos financial statements and allocations of revenues expenses and gains or losses shall be included in determining reported segment profit or loss only if

ndash they are included in the measure of the segmentrsquos profit or loss that is used by the chief operating decision maker

bull Similarly only those assets and liabilities that are included in the measures of the segmentrsquos assets and segmentrsquos liabilities that are used by the chief operating decision maker shall be reported for that segment

bull If amounts are allocated to reported segment profit or loss assets or liabilities those amounts shall be allocated on a reasonable basis

44

copy 2005-13 Nelson Consulting Limited 87

5 Measurement ndash Reconciliations

bull If an entity changes the structure of its internal organisation in a manner that causes the composition of its reportable segments to change

ndash the corresponding information for earlier periods including interim periods shall be restated unless the information is not available and the cost to develop it would be excessive (for each individual item of disclosure)

bull Following a change in the composition of its reportable segments

ndash an entity shall disclose whether it has restated the corresponding items of segment information for earlier periods

copy 2005-13 Nelson Consulting Limited 88

5 Measurement ndash Reconciliations

bull If an entity has changed the structure of its internal organisation in a manner that causes the composition of its reportable segments to change and if segment information for earlier periods including interim periods is not restated to reflect the change

ndash the entity shall disclose in the year in which the change occurs segment information for the current period on both the old basis and the new basis of segmentation unless the necessary information is not available and the cost to develop it would be excessive

45

copy 2005-13 Nelson Consulting Limited 89

6 Entity-Wide Disclosures

bull All entities subject to IFRS 8 including those that have a single reportable segment are also required to have certain entity-wide disclosures includingndash the revenues from external customers for each

product and service or each group of similar products and services

ndash certain geographical information

ndash information about the extent of its reliance on its major customers

Products and Services

Geographical Areas

Major Customers

copy 2005-13 Nelson Consulting Limited 90

Interim Financial Reporting(IAS 34)

46

copy 2005-13 Nelson Consulting Limited 91

Points for Sharing

1 Scope and Definitions

2 Content of an Interim Financial Report

3 Disclosure in Annual Financial Statements

4 Recognition and Measurement

5 Restatement of Previously Reported Interim Periods

copy 2005-13 Nelson Consulting Limited 92

1 Scope and Definition

bull IAS 34 does not mandatendash which entities should be required to publish interim financial

reports

ndash how frequently or

ndash how soon after the end of an interim period

bull However governments securities regulators stock exchanges and accountancy bodies often require entities whose debt or equity securities are publicly traded to publish interim financial reports

bull IAS 34 appliesndash if an entity is required or elects to publish an interim

financial report in accordance with IFRSs (IAS 341)

47

copy 2005-13 Nelson Consulting Limited 93

1 Scope and Definition

bull Interim periodndash is a financial reporting period shorter than a full financial

year

bull Interim financial report means a financial report containing either ndash a complete set of financial statements (as described in IAS

1 Presentation of Financial Statements) or

ndash a set of condensed financial statements (as described in IAS 34) for an interim period (IAS 344)

copy 2005-13 Nelson Consulting Limited 94

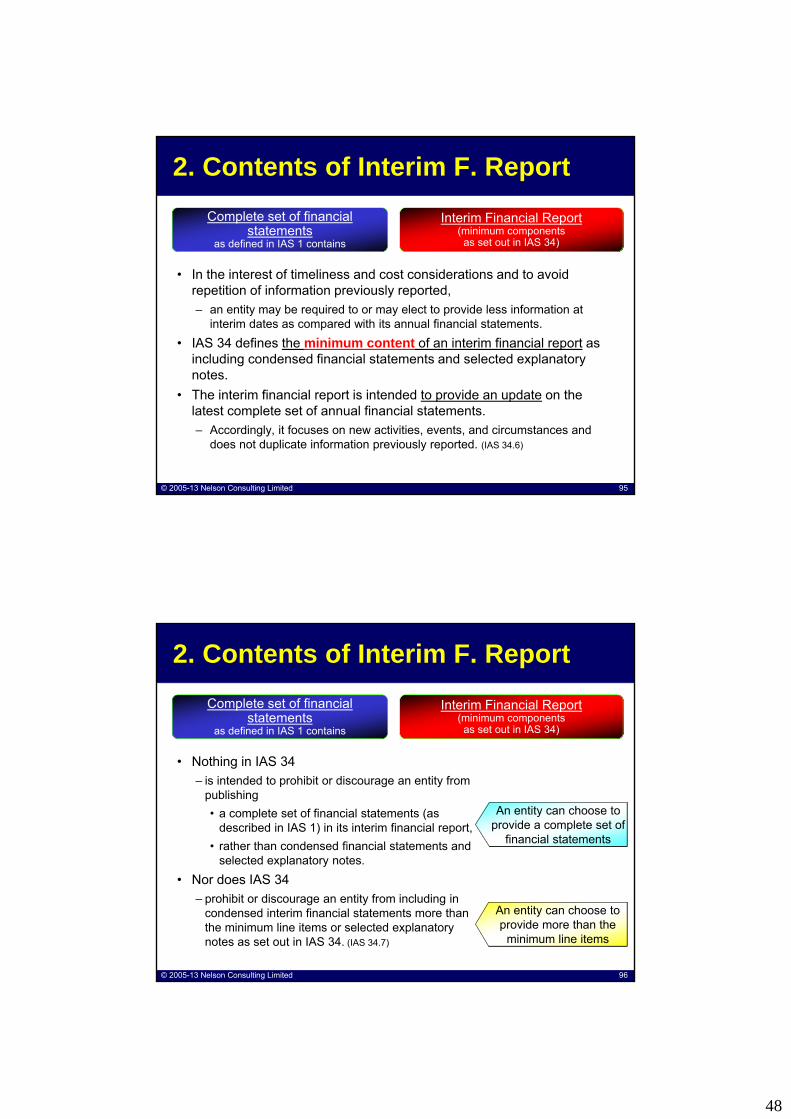

2 Contents of Interim F Report

a a statement of financial position

b a statement (or statements) of profit or loss (PL) and other comprehensiveincome (OCI) for the period

c a statement of changes in equity

d a statement of cash flows

e notes (comprising other information) and

ea comparative information and

f a statement of financial position as at the beginning of the earliest comparative preceding period (as required by IAS 1) (IAS 345)

Condensed statement of fin position

Condensed statement (or statements)of PL and OCI

Condensed statement of changes in equity

Condensed statement of cash flows

Selected explanatory notes

Complete set of financial statements

as defined in IAS 1 contains

Interim Financial Report(minimum components

as set out in IAS 34)

48

copy 2005-13 Nelson Consulting Limited 95

2 Contents of Interim F Report

bull In the interest of timeliness and cost considerations and to avoid repetition of information previously reported

ndash an entity may be required to or may elect to provide less information at interim dates as compared with its annual financial statements

bull IAS 34 defines the minimum content of an interim financial report as including condensed financial statements and selected explanatory notes

bull The interim financial report is intended to provide an update on the latest complete set of annual financial statements

ndash Accordingly it focuses on new activities events and circumstances and does not duplicate information previously reported (IAS 346)

Complete set of financial statements

as defined in IAS 1 contains

Interim Financial Report(minimum components

as set out in IAS 34)

copy 2005-13 Nelson Consulting Limited 96

2 Contents of Interim F Report

bull Nothing in IAS 34

ndash is intended to prohibit or discourage an entity from publishing

bull a complete set of financial statements (as described in IAS 1) in its interim financial report

bull rather than condensed financial statements and selected explanatory notes

bull Nor does IAS 34

ndash prohibit or discourage an entity from including in condensed interim financial statements more than the minimum line items or selected explanatory notes as set out in IAS 34 (IAS 347)

provide a complete set of An entity can choose to

provide a complete set of financial statements

An entity can choose to provide more than the

minimum line items

Complete set of financial statements

as defined in IAS 1 contains

Interim Financial Report(minimum components

as set out in IAS 34)

49

copy 2005-13 Nelson Consulting Limited 97

2 Contents of Interim F Report

bull The recognition and measurement guidance in IAS 34 applies also to

ndash complete financial statements for an interim period and such statements would include all of the disclosures required by IAS 34 (particularly the selected note disclosures in IAS 3416) as well as those required by other IFRSs (IAS 347)

Complete set of financial statements

as defined in IAS 1 contains

Interim Financial Report(minimum components

as set out in IAS 34)

copy 2005-13 Nelson Consulting Limited 98

2 Contents of Interim F Report

bull An interim financial report shall include at a minimum the following components

a a condensed statement of financial position

b a condensed statement (or statements) of PL and OCI

c a condensed statement of changes in equity

d a condensed statement of cash flows and

e selected explanatory notes (IAS 348)

Condensed statement of fin position

Condensed statement of changes in equity

Condensed statement of cash flows

Selected explanatory notes

bull If an entity presents the items of profit or loss in a separate statement as described in IAS 110A (as amended in 2011) it presents interim condensed information from that statement (IAS 348A)

Condensed statement (or statements)of PL and OCI

Interim Financial Report(minimum components

as set out in IAS 34)

50

copy 2005-13 Nelson Consulting Limited 99

2 Contents of Interim F Report

bull If an entity publishes a complete set of financial statements in its interim financial report

ndash the form and content of those statements shall conform to the requirements of IAS 1 for a complete set of financial statements (IAS 349)

bull If an entity publishes a set of condensed financial statements in its interim financial report

ndash those condensed statements shall include at a minimum

bull each of the headings and subtotals that were included in its most recent annual financial statements and

bull the selected explanatory notes as required by IAS 34 (IAS 3410)

Additional line items or notes shall be included

bull if their omission would make the condensed interim financial statements misleading (IAS 3410)

Complete set of financial statements

as defined in IAS 1 contains

Interim Financial Report(minimum components

as set out in IAS 34)

copy 2005-13 Nelson Consulting Limited 100

2 Contents of Interim F Report

bull In the statement that presents the items of profit or loss for an interim period

ndash an entity shall present basic and diluted earnings per share for that period when the entity is within the scope of IAS 33 Earnings per Share (IAS 3411)

bull If an entity presents the items of profit or loss in a separate statement as described in IAS 110A (as amended in 2011)

ndash it presents basic and diluted earnings per share in that statement (IAS 3411A)

Present in the condensed statement of profit or loss

Complete set of financial statements

as defined in IAS 1 contains

Interim Financial Report(minimum components

as set out in IAS 34)

51

copy 2005-13 Nelson Consulting Limited 101

2 Contents of Interim F Report

Significant Events and Transactions

bull An entity shall include in its interim financial report

ndash an explanation of events and transactions that are significant to an understanding of the changes in financial position and performance of the entity since the end of the last annual reporting period

ndash Information disclosed in relation to those events and transactions shall update the relevant information presented in the most recent annual financial report (IAS 3415)

bull A user of an entityrsquos interim financial report will have access to the most recent annual financial report of that entity

bull Therefore it is unnecessary for the notes to an interim financial report to provide relatively insignificant updates to the information that was reported in the notes in the most recent annual financial report (IAS 3415A)

copy 2005-13 Nelson Consulting Limited 102

2 Contents of Interim F Report

bull The following is a list of events and transactions for which disclosures would be required if they are significant (the list is not exhaustive)a the write-down of inventories to net realisable value and the reversal of

such a write-down

b recognition of a loss from the impairment of financial assets property plant and equipment intangible assets or other assets and the reversal of such an impairment loss

c the reversal of any provisions for the costs of restructuring

d acquisitions and disposals of items of property plant and equipment

e commitments for the purchase of property plant and equipment

f litigation settlements

g corrections of prior period errors

h changes in the business or economic circumstances that affect the fair value of the entityrsquos financial assets and financial liabilities whether those assets or liabilities are recognised at fair value or amortised cost

Example

52

copy 2005-13 Nelson Consulting Limited 103

2 Contents of Interim F Report

bull The following is a list of events and transactions for which disclosures would be required if they are significant (the list is not exhaustive)i any loan default or breach of a loan agreement that has not been

remedied on or before the end of the reporting period and

j related party transactions

k transfers between levels of the fair value hierarchy used in measuring the fair value of financial instruments

l changes in the classification of financial assets as a result of a change in the purpose or use of those assets and

m changes in contingent liabilities or contingent assets (IAS 3415B)

Example

copy 2005-13 Nelson Consulting Limited 104

2 Contents of Interim F Report

bull Interim reports shall include interim financial statements (condensed or complete) for periods as follows

a) statement of financial position

bull as of the end of the current interim period and

a comparative statement of financial position

bull as of the end of the immediately preceding financial year

Periods for which Interim Financial Statements are Required to be Presented

53

copy 2005-13 Nelson Consulting Limited 105

2 Contents of Interim F Report

bull Interim reports shall include interim financial statements (condensed or complete) for periods as follows

b) statements of profit or loss and other comprehensive income

bull for the current interim period and

bull cumulatively for the current financial year to date with

comparative statements of profit or loss and comprehensive income

bull for the comparable interim periods (current and year-to-date) of the immediately preceding financial year

ndash As permitted by IAS 1 (as amended in 2011) an interim report may present for each period a statement or statements of profit or loss and other comprehensive income

Periods for which Interim Financial Statements are Required to be Presented

copy 2005-13 Nelson Consulting Limited 106

2 Contents of Interim F Report

bull Interim reports shall include interim financial statements (condensed or complete) for periods as follows

c) statement of changes in equity

bull cumulatively for the current financial year to date with

a comparative statement

bull for the comparable year-to-date period of the immediately preceding financial year

d) statement of cash flows

bull cumulatively for the current financial year to date with

a comparative statement

bull for the comparable year-to-date period of the immediately preceding financial year (IAS 3420)

Periods for which Interim Financial Statements are Required to be Presented

54

copy 2005-13 Nelson Consulting Limited 107

2 Contents of Interim F Report

Entity A will report the following in its interim financial report

Current Comparative

Statement of financial position as at 3092013 31122012

Statement of PL and OCIFor 3-month period 172013 to 3092013 172012 to 3092012For 9-month period 112013 to 3092013 112012 to 3092012

Statement of changes in equity For 9 month period 112013 to 3092013 112012 to 3092012

Statement of cash flowsFor 9-month period 112013 to 3092013 112012 to 3092012

Example

bull Entity A ends its financial statement at 31 Dec and proposes to report an interim financial report for the three-month period ended 3092013

copy 2005-13 Nelson Consulting Limited 108

2 Contents of Interim F Report

bull For an entity whose business is highly seasonal financial information for the twelve months ending on the interim reporting date and comparative information for the prior twelve-month period may be useful

ndash Accordingly entities whose business is highly seasonal are encouraged to consider reporting such information in addition to the information called for in IAS 34

Periods for which Interim Financial Statements are Required to be Presented

55

copy 2005-13 Nelson Consulting Limited 109

2 Contents of Interim F Report

bull In deciding how to recognise measure classify or disclose an item for interim financial reporting purposes

ndash materiality shall be assessed in relation to the interim period financial data

bull In making assessments of materiality it shall be recognised that interim measurements may rely on estimates to a greater extent than measurements of annual financial data (IAS 3423)

Materiality

copy 2005-13 Nelson Consulting Limited 110

3 Disclosures in Annual Fin S

bull lf an estimate of an amount reported in an interim period is changed significantly during the final interim period of the financial year but a separate financial report is not published for that final interim period

ndash the nature and amount of that change in estimate shall be disclosed in a note to the annual financial statements for that financial year (IAS 3426)

56

copy 2005-13 Nelson Consulting Limited 111

4 Recognition and Measurement

bull An entity shall apply the same accounting policiesin its interim financial statements as are applied in its annual financial statements

ndash except for accounting policy changes made after the date of the most recent annual financial statements that are to be reflected in the next annual financial statements

bull However the frequency of an entityrsquos reporting (annual half-yearly or quarterly) shall not affect the measurement of its annual results

bull To achieve that objective measurements for interim reporting purposes shall be made on a year-to-date basis (IAS 3428)

copy 2005-13 Nelson Consulting Limited 112

5 Restatement of Previously Reports

bull A change in accounting policy other than one for which the transition is specified by a new Standard or Interpretation shall be reflected by

a) restating the financial statements of prior interim periods of the current financial year and the comparable interim periods of any prior financial years that will be restated in the annual financial statements in accordance with IAS 8 or

b) when it is impracticable to determine the cumulative effect at the beginning of the financial year of applying a new accounting policy to all prior periods adjusting the financial statements of prior interim periods of the current financial year and comparable interim periods of prior financial years to apply the new accounting policy prospectively from the earliest date practicable (IAS 3443)

57

copy 2005-13 Nelson Consulting Limited 113

Preparation and Presentation of Financial Statements ndash Part 2 24 September 2013

LAM Chi Yuen Nelson 林智遠nelsonnelsoncpacomhkwwwNelsonCPAcomhkwwwFacebookcomNelsonCPA

Full set of slides in PDF can be found in wwwNelsonCPAcomhktraining

copy 2005-13 Nelson Consulting Limited 114

Preparation and Presentation of Financial Statements ndash Part 2 24 September 2013

QampA SessionQampA Session

LAM Chi Yuen Nelson 林智遠nelsonnelsoncpacomhkwwwNelsonCPAcomhkwwwFacebookcomNelsonCPA

Full set of slides in PDF can be found in wwwNelsonCPAcomhktraining

2

copy 2005-13 Nelson Consulting Limited 3

Non-current Assets Held for Sale and Discontinued Operations (IFRS 5)

copy 2005-13 Nelson Consulting Limited 4

Todayrsquos Agenda

1 Objective of IFRS 5

2 Scope of IFRS 5

3 Classification

4 Measurement

5 Presentation

3

copy 2005-13 Nelson Consulting Limited 5

1 Objective of IFRS 5

bull To specify

Classification

Measurement

Presentation

bull The accounting forassets held for sale

bull The presentation and disclosureof discontinued operations

Non-Current Assets

Disposal Groups

PresentationDiscontinued Operations

Disposal Group may be Discontinued Operation if it is an operation

copy 2005-13 Nelson Consulting Limited 6

1 Objective of IFRS 5 (Summary)

bull To specify

bull The accounting forassets held for sale

bull The presentation and disclosureof discontinued operations

bull In particular to requirendash asset that meet the criteria to be

classified as held for sale to bebull measured at

ndash the lower of carrying amount andfair value less costs to sell and

ndash depreciation on such assets to cease andbull presented separately in the statement of

financial position andndash the results of discontinued operations to be

presented separately in the statement of comprehensive income

Classification

Measurement

Presentation

Strict Criteria Imposed

4

copy 2005-13 Nelson Consulting Limited 7

2 Scope of IFRS 5

Classification

Presentation

bull Classification and presentationrequirements of IFRS 5 apply to

ndash all recognised non-current asset