training workshop on accounts management

TRANSCRIPT

BASIC FINANCIAL ACCOUNTING

Presented by: Ligaya T. Bato, CPA

Business Entity Forms

Sole Proprietorship

Sole Proprietorship PartnershipPartnership CorporationCorporation

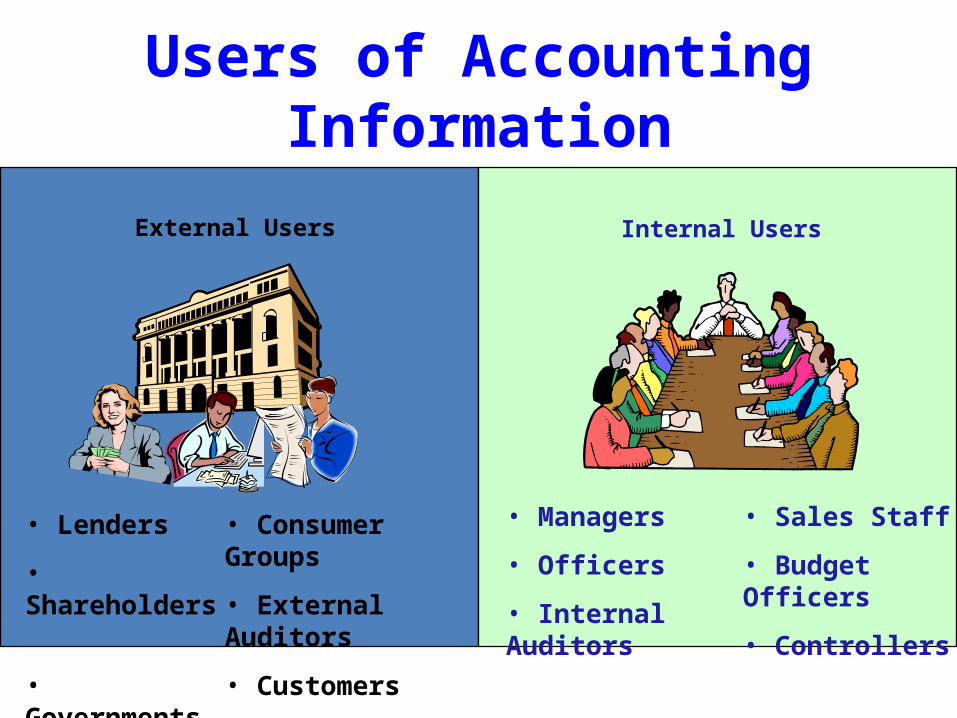

Users of Accounting Information

External Users

• Lenders

• Shareholders

• Governments

• Consumer Groups

• External Auditors

• Customers

Internal Users

• Managers

• Officers

• Internal Auditors

• Sales Staff

• Budget Officers

• Controllers

Users of Accounting Information

External Users

Financial accounting provides external users with financial

statements.

Internal Users

Managerial accounting provides information needs for internal

decision makers.

What is the relation between Accounting and Bookkeeping?

• Bookkeeping is the recording of financial transactions and events, either manually or electronically.

• Accounting is much more. It includes identifying, measuring, recording, reporting, and analyzing business events and transactions, and helps information users to make economic decisions.

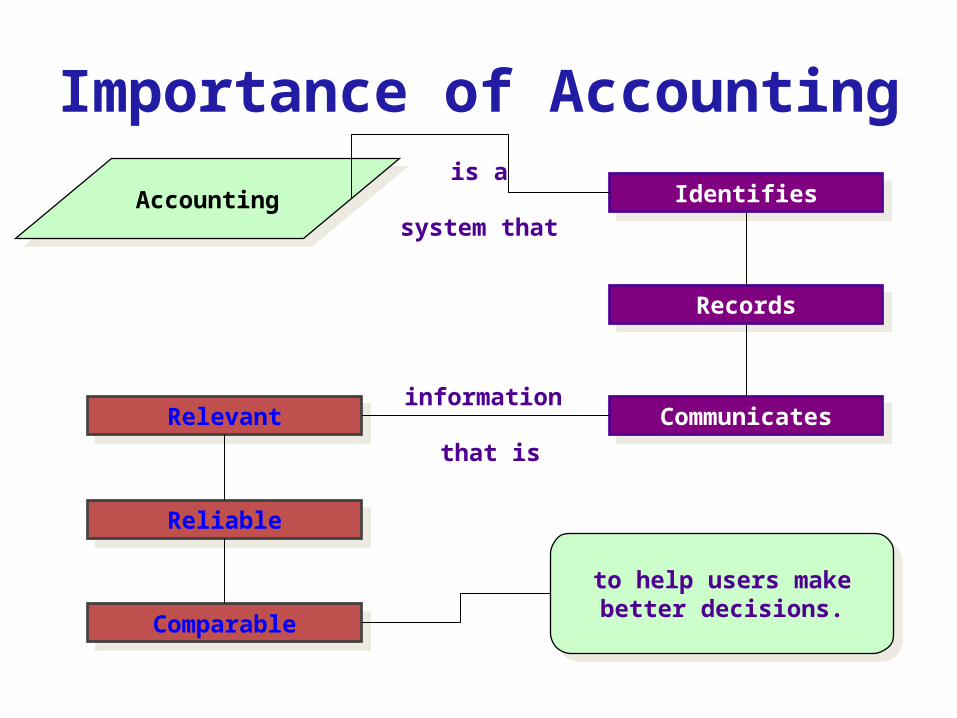

IdentifiesIdentifies

RecordsRecords

CommunicatesCommunicatesRelevantRelevant

ReliableReliable

ComparableComparable

Importance of Accounting

AccountingAccountingis a

system that

information

that is

to help users make better decisions.

to help users make better decisions.

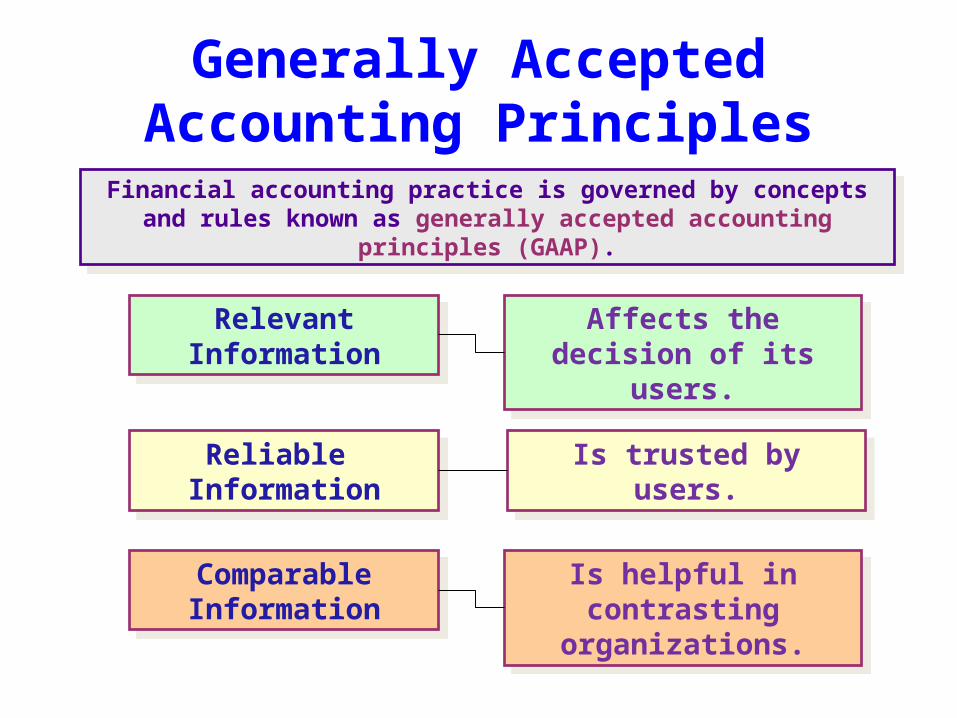

Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP).

Financial accounting practice is governed by concepts and rules known as generally accepted accounting principles (GAAP).

Generally Accepted Accounting Principles

Relevant Information

Relevant Information

Affects the decision of its users.

Affects the decision of its users.

Reliable InformationReliable Information Is trusted by users.Is trusted by users.

Comparable Information

Comparable Information

Is helpful in contrasting organizations.

Is helpful in contrasting organizations.

Identifying Business Activities

RecordingClassifying

Summarizing Business Activities

CommunicatingAnalyzing

Business Activities

Accounting Activities

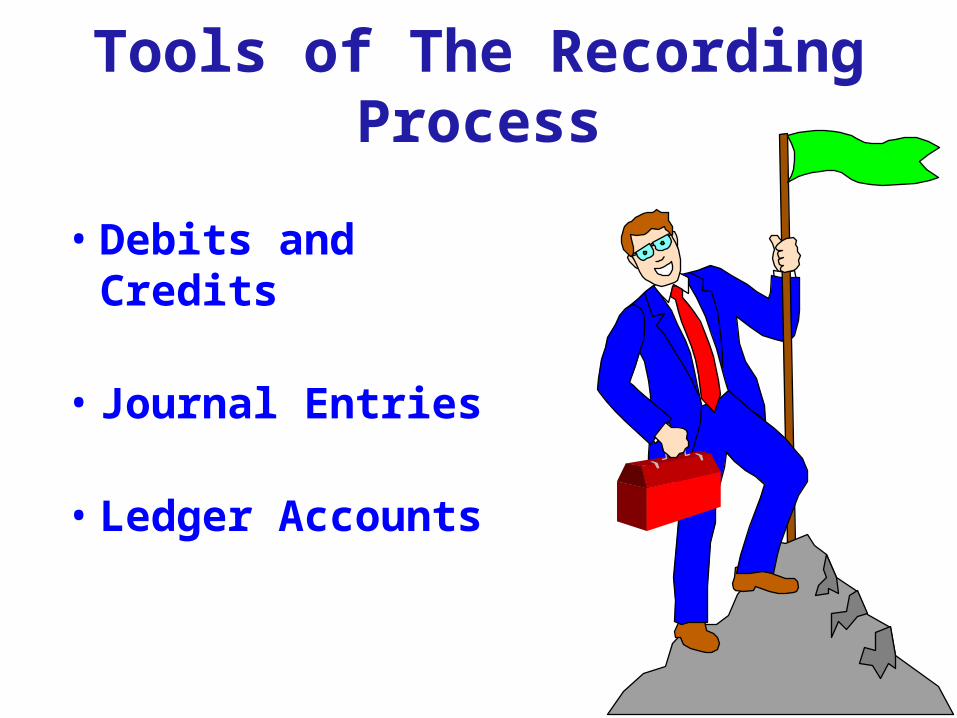

Tools of The Recording Process

• Debits and Credits

• Journal Entries

• Ledger Accounts

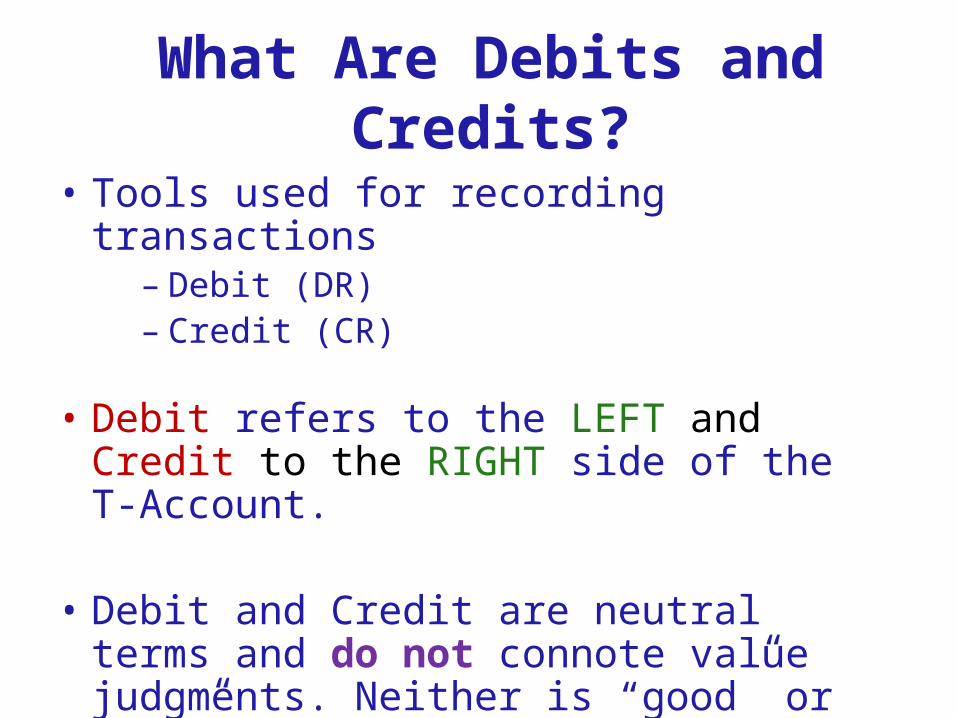

What Are Debits and Credits?

• Tools used for recording transactions– Debit (DR)– Credit (CR)

• Debit refers to the LEFT and Credit to the RIGHT side of the T-Account.

• Debit and Credit are neutral terms and do not connote value judgments. Neither is “good” or “bad”!

• Again, debits and credits are used to increase or decrease account balances.

• Determining whether to use a debit or credit to record an increase or decrease depends on the type of account in question.

• The Balance Sheet Equation OR Balance Sheet Model is the basis for the determination.

Using Debits and Credits

Assets Liabilities + Equity

Accounting Equation

LiabilitiesLiabilities EquityEquityAssetsAssets = +

1-12

Normal Balances

The normal balances for each of the FIVE types of accounts are as follows:

Account Name

Debit Balance Credit BalanceAssets Expenses

Liabilities Stockholders’ Equity Revenues

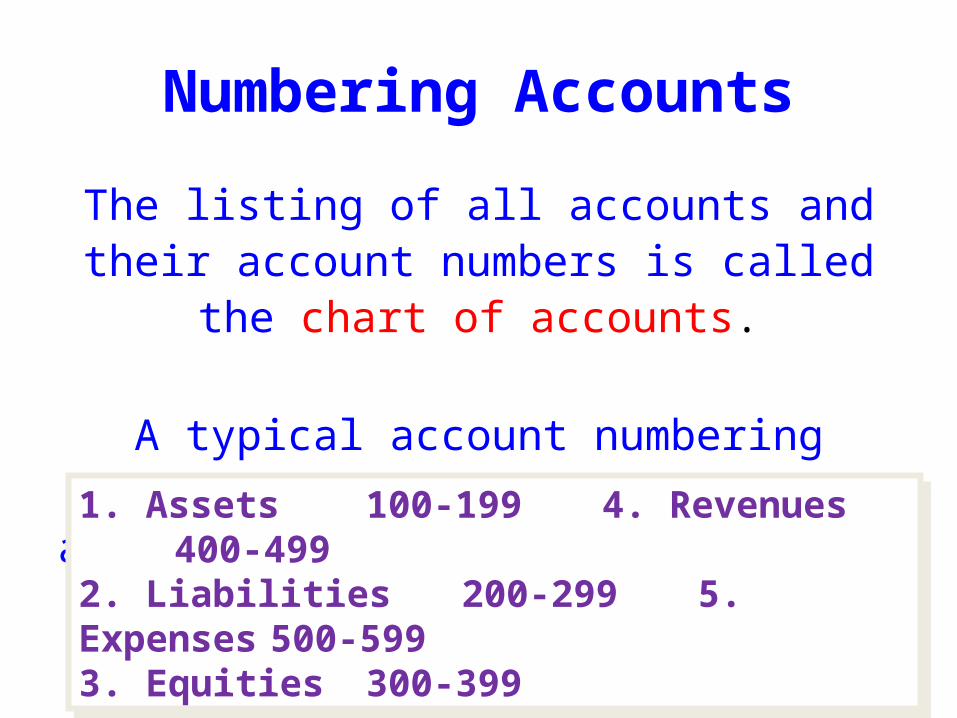

Numbering Accounts

The listing of all accounts and their account numbers is called the chart of accounts.

A typical account numbering scheme of the Five types of accounts might appear as follows:

1. Assets 100-199 4. Revenues 400-4992. Liabilities 200-299 5. Expenses 500-5993. Equities 300-399

1. Assets 100-199 4. Revenues 400-4992. Liabilities 200-299 5. Expenses 500-5993. Equities 300-399

Recording Transactions

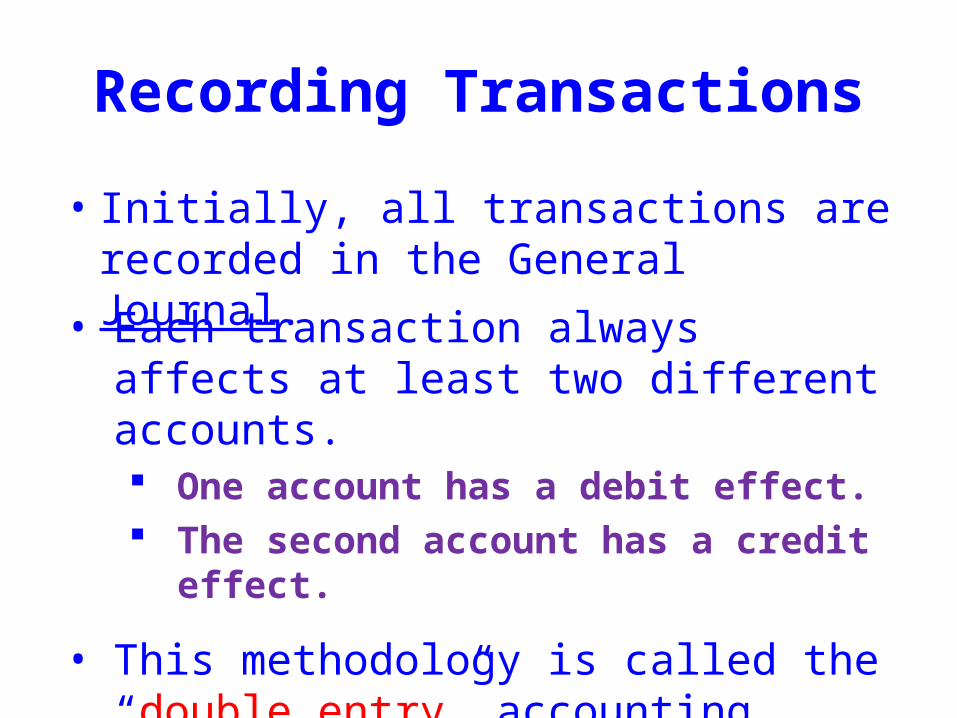

• Each transaction always affects at least two different accounts. One account has a debit effect. The second account has a credit effect.

• This methodology is called the “double entry” accounting.

• Initially, all transactions are recorded in the General Journal.

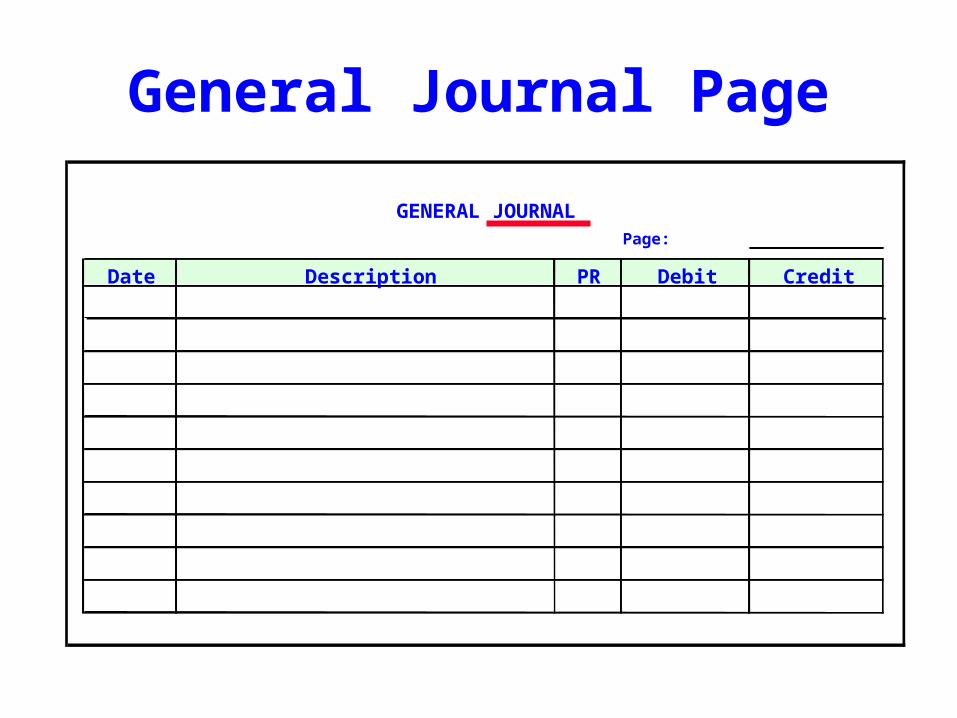

General Journal Page

GENERAL JOURNALPage:

Date Description PR Debit Credit

SAMPLE JOURNAL ENTRIES

Debit Credit

The General Ledger AccountA ledger account is a tool used for

classifying and summarizing information about increases, decreases, and balances of financial statements items.

– Think of it as a storage container like a bucket.

– Pesos (or applicable monetary currencies), which are used to measure economic transactions, are “poured” into and out of the container.

Assets

Liabilities

Stockholders’ Equity

Revenues

Expenses

Assets

Liabilities

Stockholders’ Equity

Revenues

Expenses

Types of Ledger Accounts

Categories of General Ledger Accounts

The five types of accounts fall into one of two categories:

• Real Accounts

• Nominal Accounts

Real Accounts

• This category includes Assets, Liabilities, and Stockholders’ Equities (i.e., Balance Sheet accounts)

• Accounts are permanent.

• Account balances are carried forward from one fiscal year to the next.

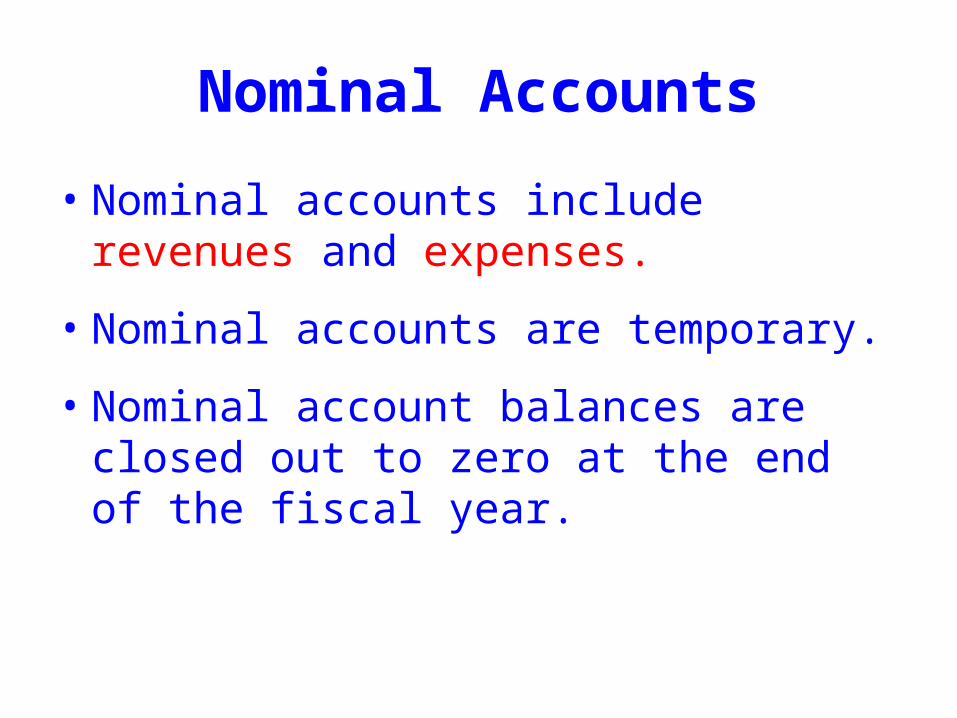

Nominal Accounts

• Nominal accounts include revenues and expenses.

• Nominal accounts are temporary.

• Nominal account balances are closed out to zero at the end of the fiscal year.

General Ledger Account Formats

Three-Amount Column Format (Debit, Credit, Balance) – Used in general ledgers in the business world

T-Account Format– Used primarily for teaching and analysis of complex transactions

General Ledger AccountThree-Amount Column Format

10/01 90,000

10/24 Salaries from Oct 01-15, 2013 45,0000 135,000

Salaries & Wages Account No.

Date Description PR Debit Credit Balance

The T-Account

Increases to the T-account are

recorded on one side of the

T-account, and Decreases are

recorded on the other side.

Debit Credit

Account Name

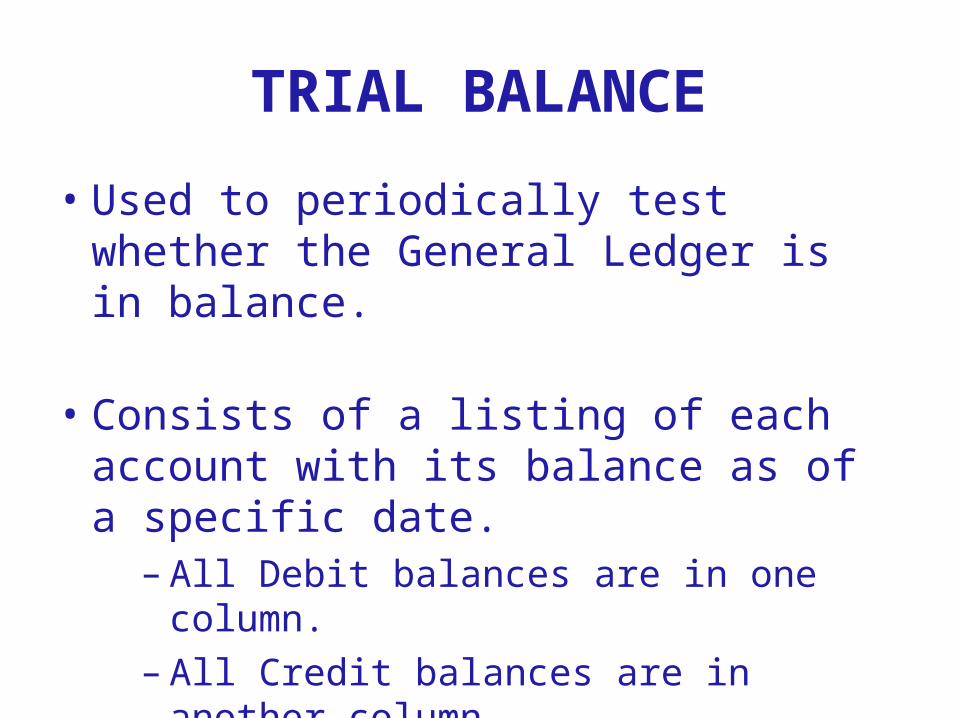

TRIAL BALANCE

• Used to periodically test whether the General Ledger is in balance.

• Consists of a listing of each account with its balance as of a specific date.

– All Debit balances are in one column.– All Credit balances are in another column.

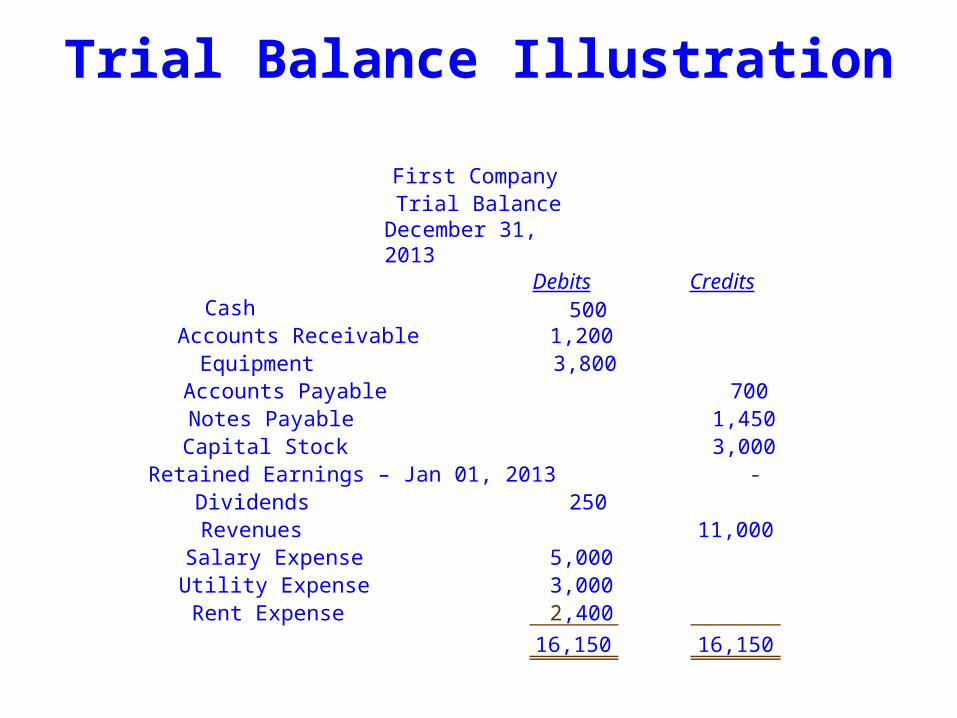

Trial Balance Illustration

First CompanyTrial Balance

December 31, 2013

Debits CreditsCash 500 Accounts Receivable 1,200 Equipment 3,800 Accounts Payable 700 Notes Payable 1,450 Capital Stock 3,000 Retained Earnings – Jan 01, 2013 - Dividends 250 Revenues 11,000 Salary Expense 5,000 Utility Expense 3,000 Rent Expense 2,400

16,150 16,150

Content and Purpose of Financial Statements

• Accountants communicate with users through four financial statements

• Income Statement

• Retained Earnings Statement

• Balance Sheet

• Statement of Cash Flows

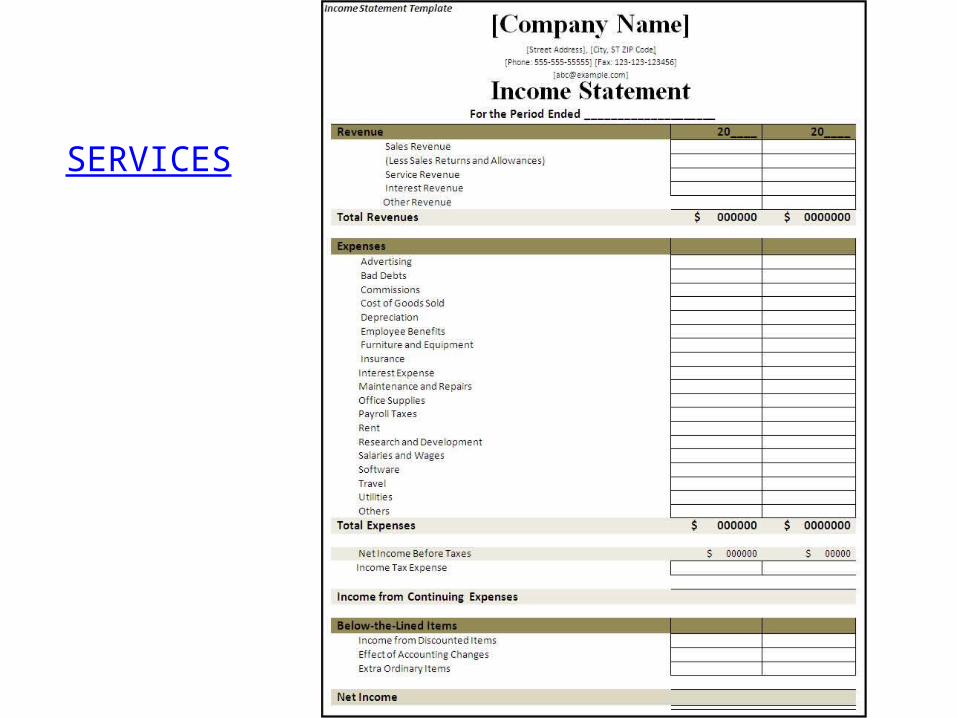

Income Statement

• Reports operating success or failure for a period.

• Summarizes revenues and expenses for period: month, quarter, or year.

• If revenue > expense = Net Income.

GOODS

SERVICES

Essential Elements of an Income Statement

1. Revenues/Sales 2. Expenses 3. Net Income before Taxes 4. Provision for Income Tax

5. Net Income after Taxes

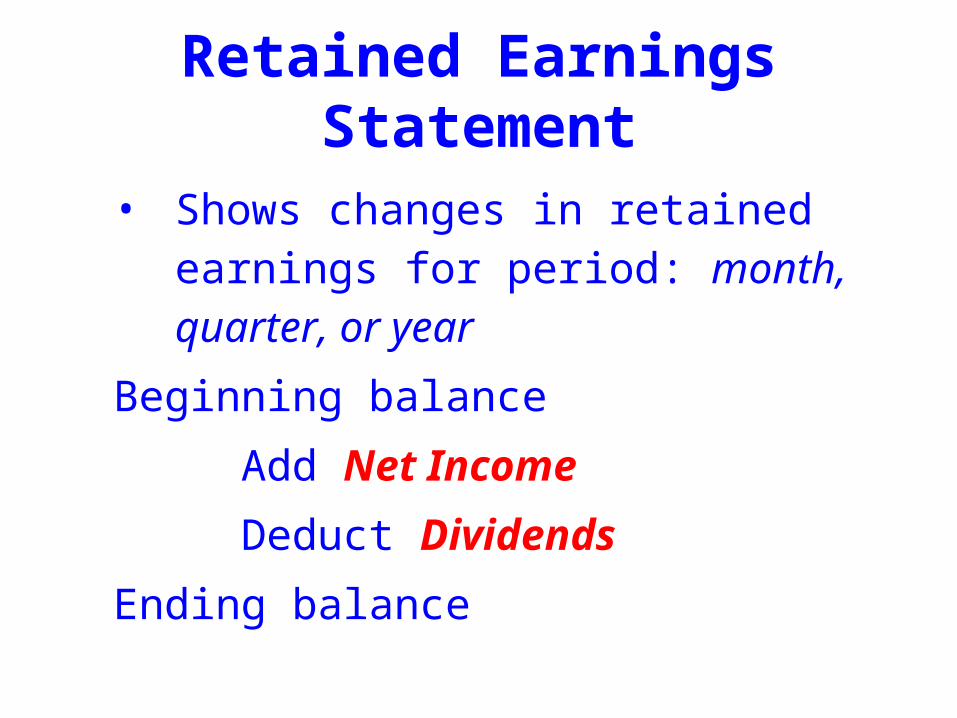

Retained Earnings Statement

• Shows changes in retained earnings for period: month, quarter, or year

Beginning balance

Add Net Income

Deduct Dividends

Ending balance

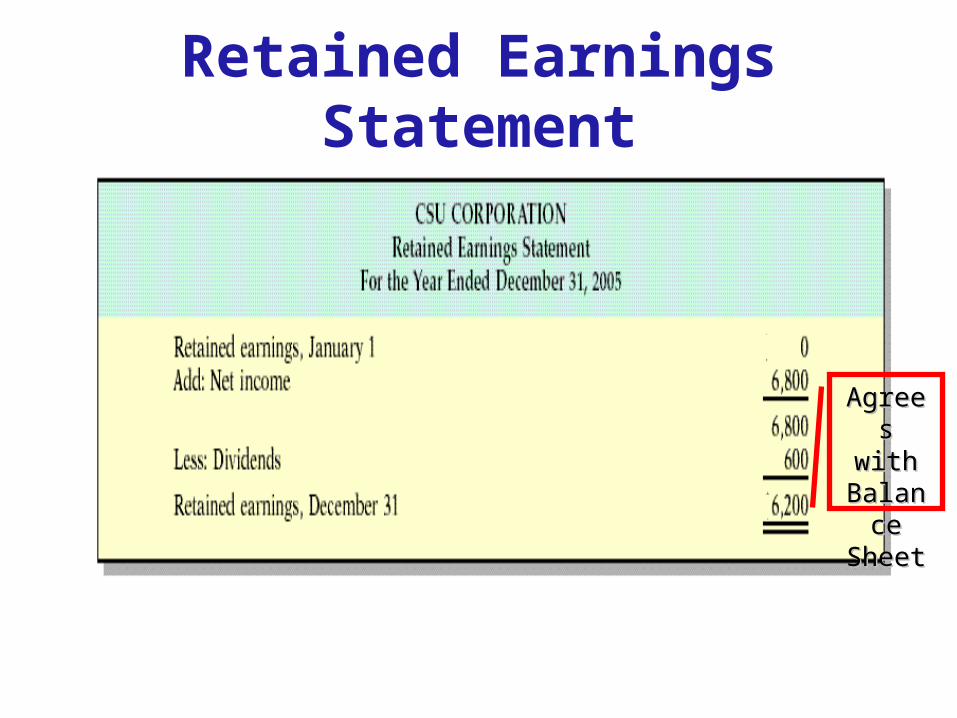

Retained Earnings Statement

Agrees Agrees with with

Balance Balance SheetSheet

ABC COMPANYSTATEMENT OF INCOME AND RETAINED EARNINGS

FOR THE YEAR ENDING DECEMBER 31, 2014

Revenues/Sales xxx Less Expenses (xxx) Net (Loss) Income before Taxes xxxProvision for Income Tax (xxx) Net Income (Loss) after Taxes xxxRetained Earnings (Deficit), Beginning xxxLess Dividend etc. (xxx) Retained Earnings (Deficit), End xxx

Agrees Agrees with with

Balance Balance SheetSheet

Balance Sheet

Income and Income and Retained Retained Earnings Earnings

StatementStatement

Balance Sheet

• Reports assets and claims to assets.

• Claims of creditors, liabilities.

• Claims of owners, stockholders’ equity.

• Assets = Liabilities + Stockholders’ Equity

• Specific date – one point in time!

Essential Elements of a Balance Sheet 1. Assets (owns) - Current Assets - Non Current Assets - Total Assets

2. Liabilities (owes) - Current Liabilities - Long-term Liabilities - Total Liabilities

3. Stockholders’ Equity (net worth) - Capital Stock - Retained Earnings (Deficit) - Total Stockholders’ Equity

LandLand

EquipmentEquipment

BuildingsBuildings

CashCash

VehiclesVehiclesStore Supplies

Store Supplies

Notes Receivable

Notes Receivable

Accounts Receivable

Accounts Receivable

Resources owned or controlled by a companyResources owned or controlled by a companyASSETS

1-40

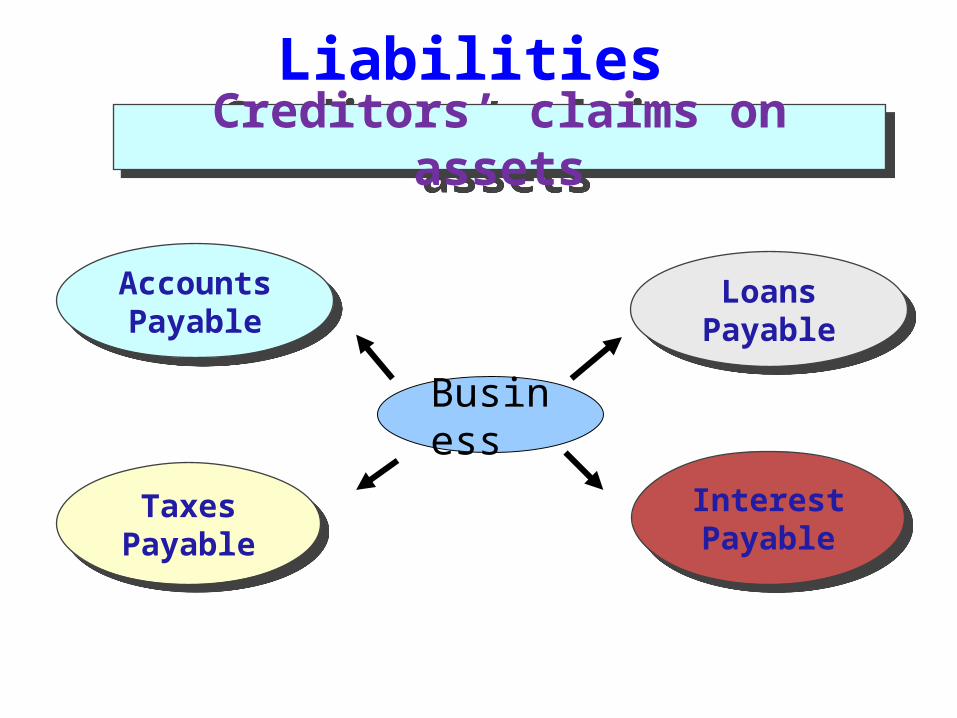

Business

Taxes Payable

Taxes Payable

Interest Payable

Interest Payable

Loans Payable

Loans Payable

Accounts Payable

Accounts Payable

Creditors’ claims on assetsCreditors’ claims on assets

Liabilities

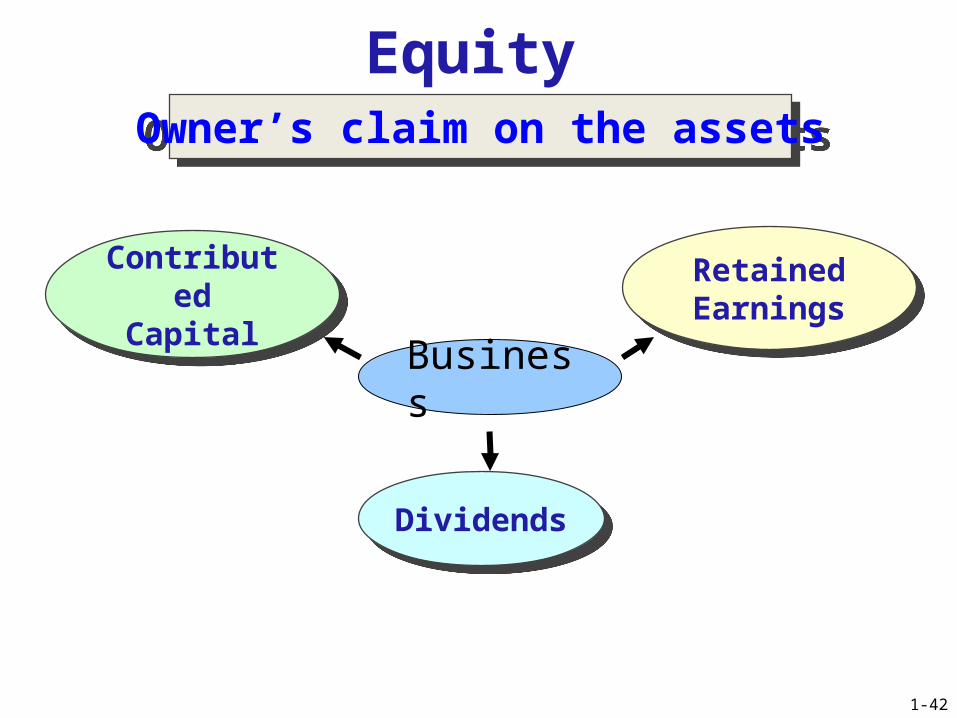

Business

Owner’s claim on the assetsOwner’s claim on the assets

DividendsDividends

Contributed Capital

Contributed Capital

Retained Earnings

Retained Earnings

Equity

1-42

Business

ACCOUNT FORM (T-ACCOUNT)

REPORT FORM (VERTICAL)

Note 1

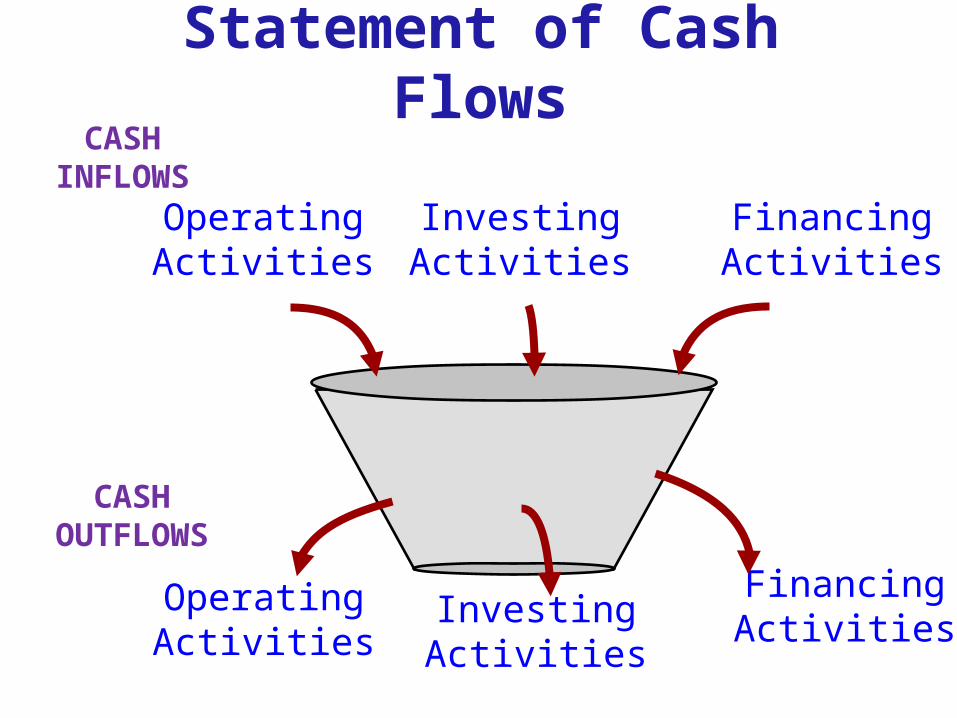

Statement of Cash Flows

• Provides information about cash receipts and cash payments

• Summarizes for period: month, quarter, or year.

• Cash effects of operating, investing, and financing activities.

Statement of Cash Flows

Agrees Agrees withwith

Balance Balance SheetSheet

Classification of Cash Flows• Operating activities – Transactions and

events that enter into the determination of net income.

• Investing activities – Transactions and events that involve the purchase and sale of securities, property, plant, equipment, and other assets not generally held for resale, and the making and collecting of loans.

• Financing activities – Transactions and events whereby resources and obtained from, or repaid to, owners and creditors.

Operating Activities

Cash Inflow• Sale of goods or

services • Sale of investments

in trading securities• Interest revenue• Dividend revenue

Cash Outflow• Inventory payments• Interest payments• Wages• Utilities, rent • Taxes

Investing Activities

Cash Inflow• Sale of plant assets• Sale of securities,

other than trading securities

• Collection of principal on loans

Cash Outflow• Purchase of plant

assets• Purchase of securities,

other than trading securities

• Making of loans to other entities

Financing Activities

Cash Inflow• Issuance of own stock• Borrowing

Cash Outflow• Dividend payments• Repaying principal on

borrowing• Treasury stock

purchase

CASH OUTFLOWS

OperatingActivities

FinancingActivitiesInvesting

Activities

CASH INFLOWS

FinancingActivities

OperatingActivities

InvestingActivities

Statement of Cash Flows

Statement of Cash Flows AnalysisOperating Investing Financing General Explanation

Building up pile of cash,Possibly looking forAcquisition

Operating cash flow beingUsed to buy fixed assetsAnd pay down debt

Operating cash flow and sale of fixed assets being used to pay down debt.

Operating cash flow and borrowed money being used to expand

1.

2.

3.

4.

+

+

+

+

+

─

+

─

+

─

─

+

The Accounting Operations/Processes

JOURNAL ENTRIES

POST TO LEDGER

TRIAL BALANCE

IDENTIFY AND ANALYZE TRANSACTIONS

ADJUSTMENTS/CLOSING ENTRIES

ADJUSTED TRIAL BALANCE

FINANCIAL STATEMENTS

ANNUAL REPORT

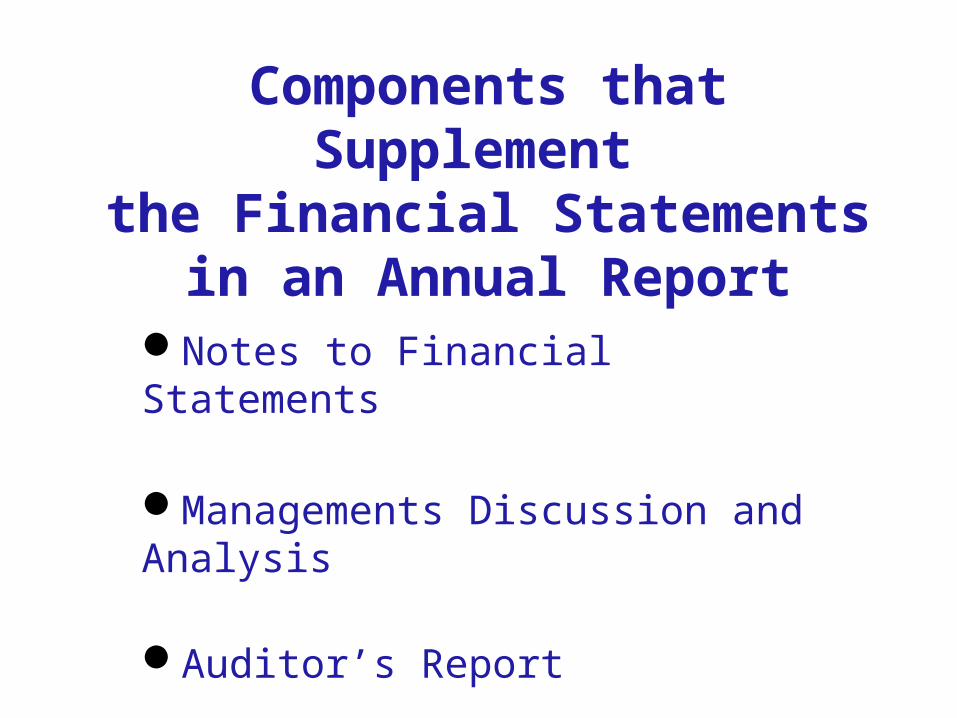

Typically, an Annual Report will contain the following sections:-Financial Highlights-Letter to the Shareholders-Narrative Text, Graphics and Photos-Financial Statements-Notes to Financial Statements-Management's Discussion and Analysis-Auditor's Report-Summary Financial Data-Corporate Information

Components that Supplement the Financial Statements

in an Annual Report

Notes to Financial Statements

Managements Discussion and Analysis

Auditor’s Report

Note 1

Management’s Discussion and Analysis

Auditor’s Report

generally acceptedaccounting principles.

THANK YOU VERY MUCH

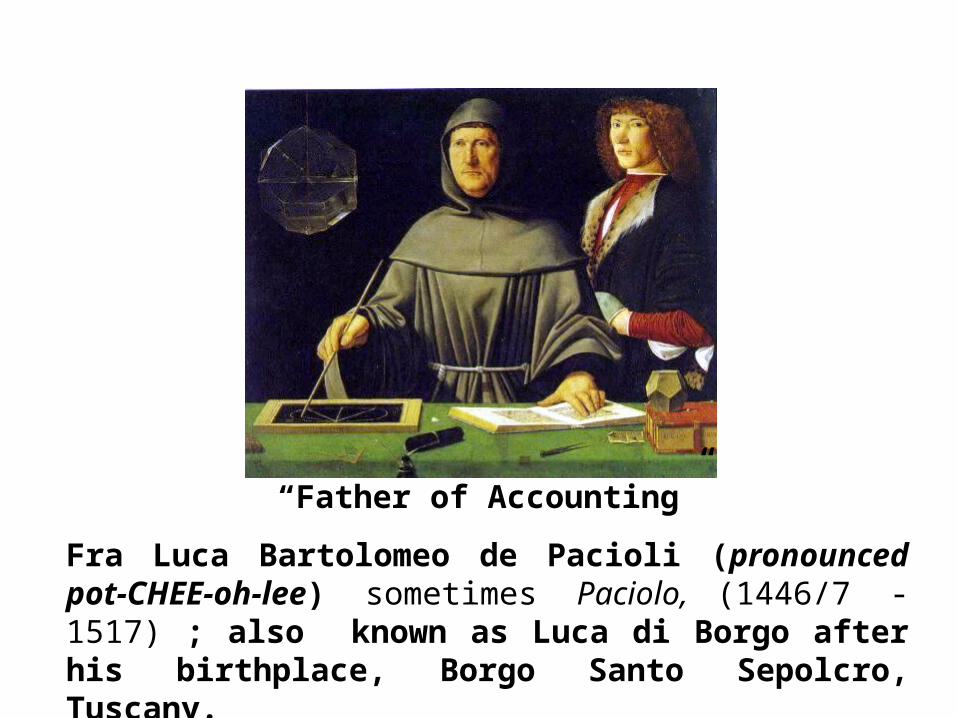

“Father of Accounting”

Fra Luca Bartolomeo de Pacioli (pronounced pot-CHEE-oh-lee) sometimes Paciolo, (1446/7 - 1517) ; also known as Luca di Borgo after his birthplace, Borgo Santo Sepolcro, Tuscany.

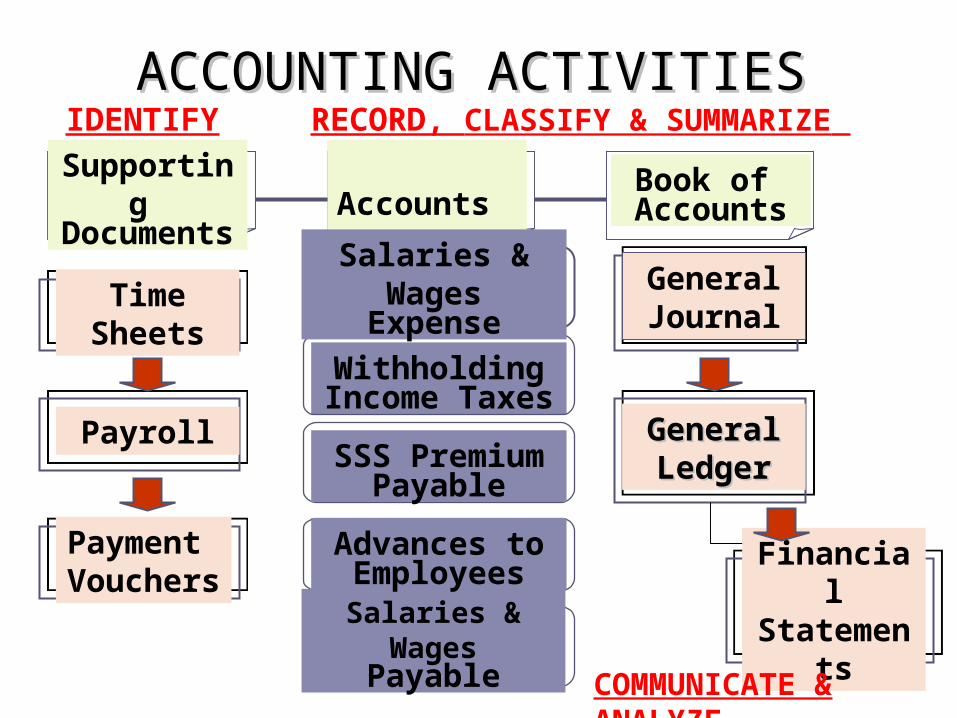

Supporting Documents

Book of Accounts

Accounts

ACCOUNTING ACTIVITIESACCOUNTING ACTIVITIES

WithholdingIncome Taxes

SSS PremiumPayable

Salaries & WagesPayable

Salaries & WagesExpense

Advances toEmployees

General Journal

Payroll

Payment Vouchers

TimeSheets

General General LedgerLedger

Financial Statements

IDENTIFY RECORD, CLASSIFY & SUMMARIZE

COMMUNICATE & ANALYZE

Implications Of Debits And Credits

Debits and Credits are used to indicate that something happened to an account.

Interpreting its implications requires an analysis of the entire journal entry.

Statement of Cash Flows Analysis

Operating Investing Financing General Explanation

Operating cash flow problems covered by sale of fixed assets, borrowing and owner contributions.

Rapid growth, short falls in operating cash flow; purchase of fixed assets.

Sale of fixed assets is financing operating cash flow shortages.

Company is using reserves to finance cash flow short falls.

5.

6.

7.

8.

─

─

─

─

+

─

+

─

+

+

─

─