1 learning objectives when you complete this chapter, you should be able to : identify or define: ...

Post on 20-Dec-2015

218 views

TRANSCRIPT

1

Learning Objectives

When you complete this chapter, you should be able to :

Identify or Define:

Forecasting Forecasting

Types of forecasts Types of forecasts

Time horizons Time horizons

Approaches to forecastsApproaches to forecasts

2

Learning Objectives

When you complete this chapter, you should be able to :

Describe or Explain:

Moving averagesMoving averages

Exponential smoothingExponential smoothing

Trend projectionsTrend projections

Regression and correlation analysisRegression and correlation analysis

Measures of forecast accuracyMeasures of forecast accuracy

3

What is Forecasting?

Process of predicting a future event

??

4

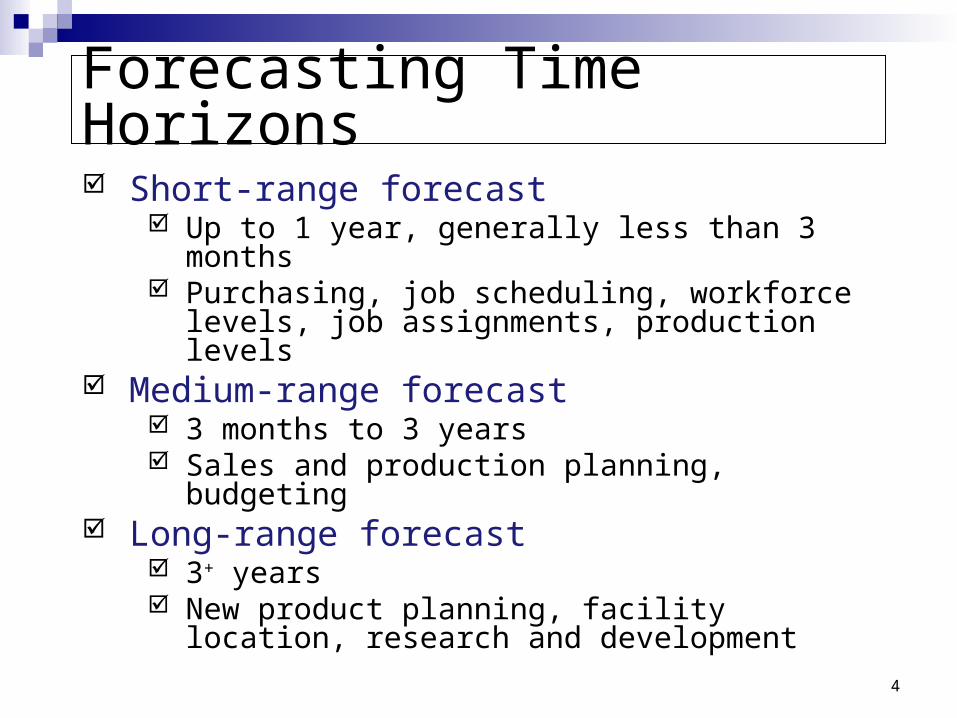

Short-range forecast Up to 1 year, generally less than 3 months Purchasing, job scheduling, workforce levels,

job assignments, production levels Medium-range forecast

3 months to 3 years Sales and production planning, budgeting

Long-range forecast 3+ years New product planning, facility location, research

and development

Forecasting Time Horizons

5

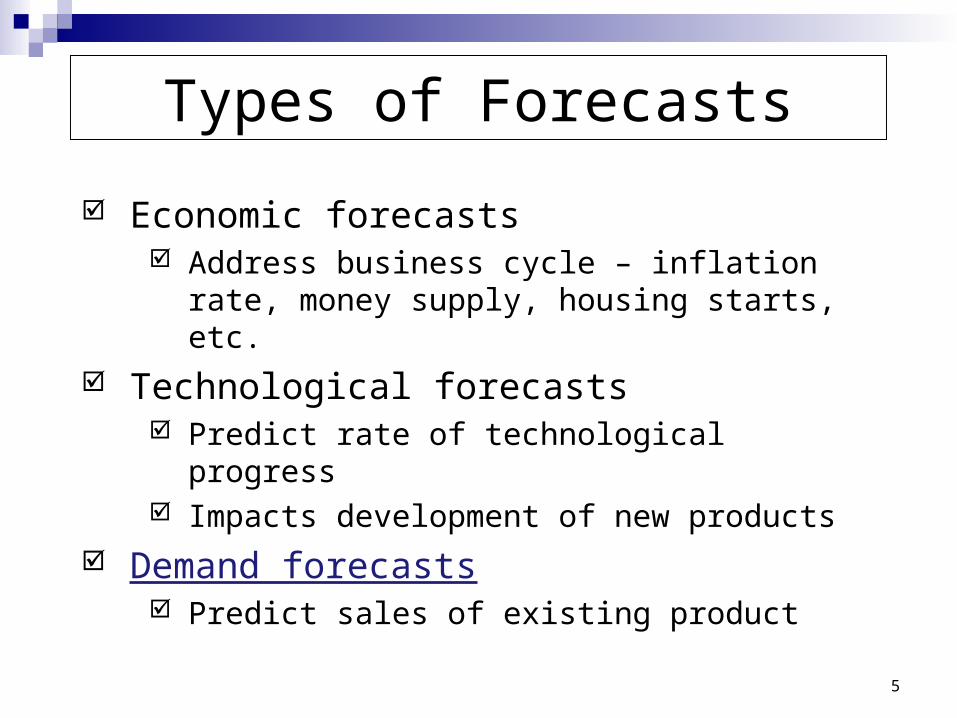

Types of Forecasts

Economic forecasts Address business cycle – inflation rate, money

supply, housing starts, etc.

Technological forecasts Predict rate of technological progress Impacts development of new products

Demand forecasts Predict sales of existing product

6

Strategic Importance of Forecasting

Human Resources – Hiring, training, Human Resources – Hiring, training, laying off workerslaying off workers

Capacity – Capacity shortages can Capacity – Capacity shortages can result in undependable delivery, loss result in undependable delivery, loss of customers, loss of market shareof customers, loss of market share

Supply-Chain Management – Good Supply-Chain Management – Good supplier relations and price advancesupplier relations and price advance

7

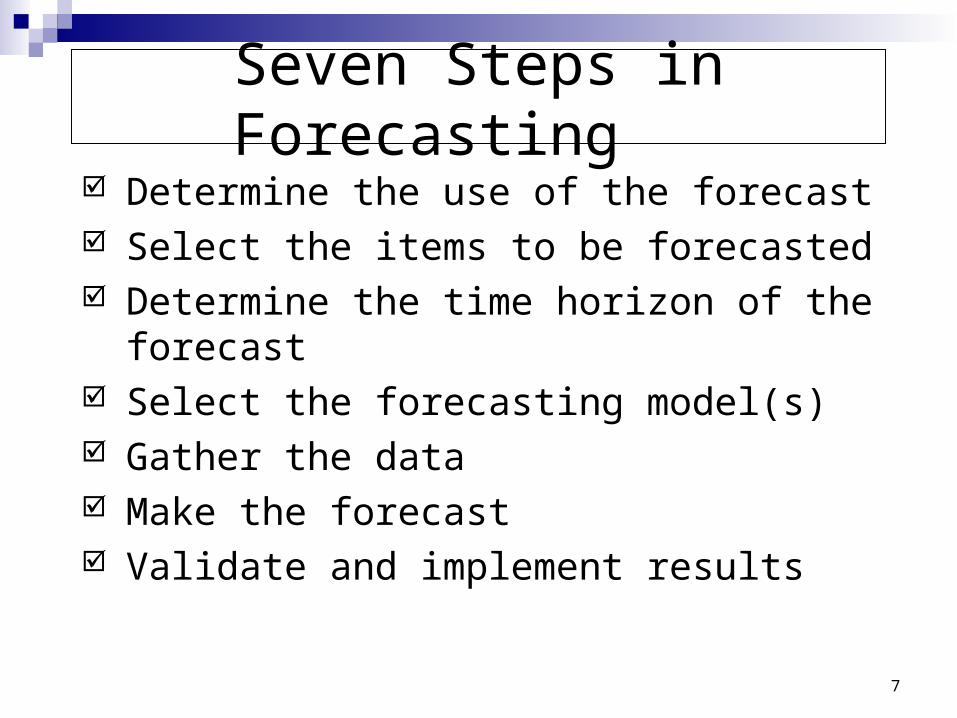

Seven Steps in Forecasting Determine the use of the forecast Select the items to be forecasted Determine the time horizon of the

forecast Select the forecasting model(s) Gather the data Make the forecast Validate and implement results

8

The Realities!

Forecasts are seldom perfectForecasts are seldom perfect

Most techniques assume an Most techniques assume an underlying stability in the systemunderlying stability in the system

Product family and aggregated Product family and aggregated forecasts are more accurate than forecasts are more accurate than individual product forecastsindividual product forecasts

9

Forecasting Approaches

Used when situation is vague and little data exist New products New technology

Involves intuition, experience e.g., forecasting sales on Internet

Qualitative MethodsQualitative Methods

10

Forecasting Approaches

Used when situation is ‘stable’ and historical data exist Existing products Current technology

Involves mathematical techniques e.g., forecasting sales of color

televisions

Quantitative MethodsQuantitative Methods

11

Overview of Qualitative Methods

Jury of executive opinion Pool opinions of high-level executives,

sometimes augment by statistical models Delphi method

Panel of experts, queried iteratively

12

Overview of Qualitative Methods

Sales force composite Estimates from individual salespersons are

reviewed for reasonableness, then aggregated

Consumer Market Survey Ask the customer

13

Involves small group of high-level managers Group estimates demand by working

together Combines managerial experience with

statistical models Relatively quick ‘Group-think’

disadvantage

Jury of Executive Opinion

14

Sales Force Composite

Each salesperson projects his or her sales

Combined at district and national levels

Sales reps know customers’ wants Tends to be overly optimistic

15

Delphi Method

Iterative group process, continues until general agreement is reached

3 types of participants Decision makers Staff Respondents

Staff(Administering

survey)

Decision Makers(Evaluate

responses and make decisions)

Respondents(People who can make valuable

judgments)

16

Consumer Market Survey

Ask customers about purchasing plans

What consumers say, and what they actually do are often different

Sometimes difficult to answer

17

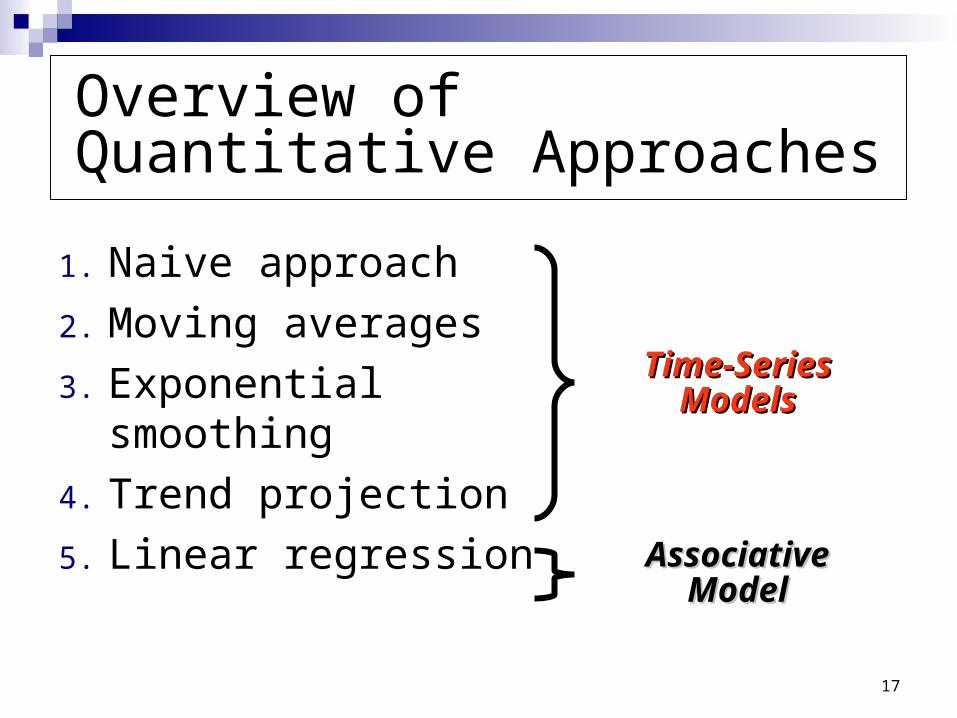

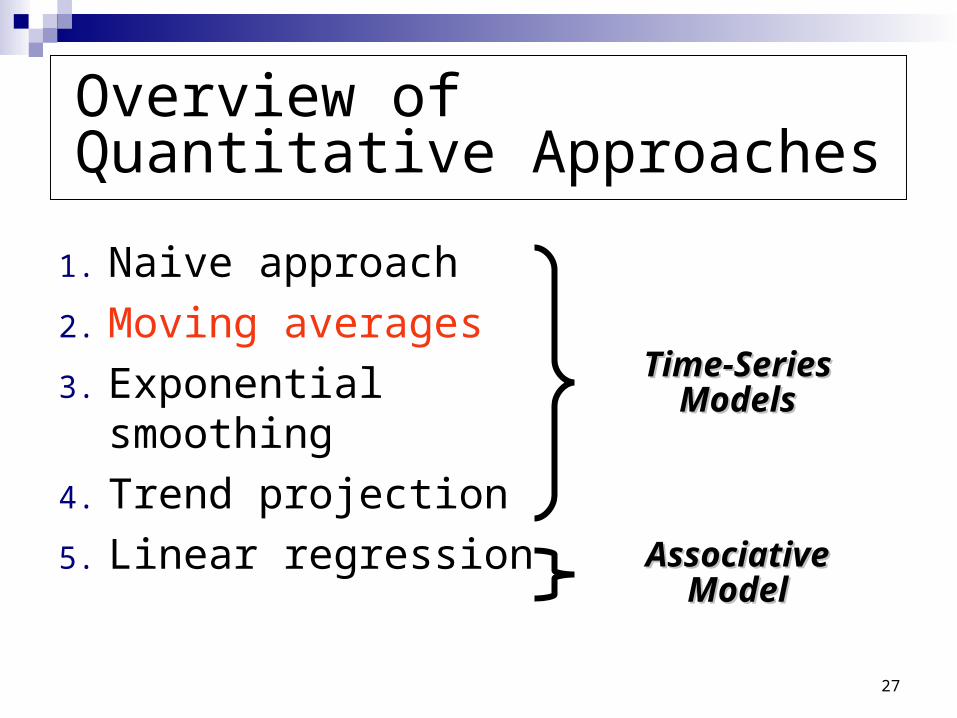

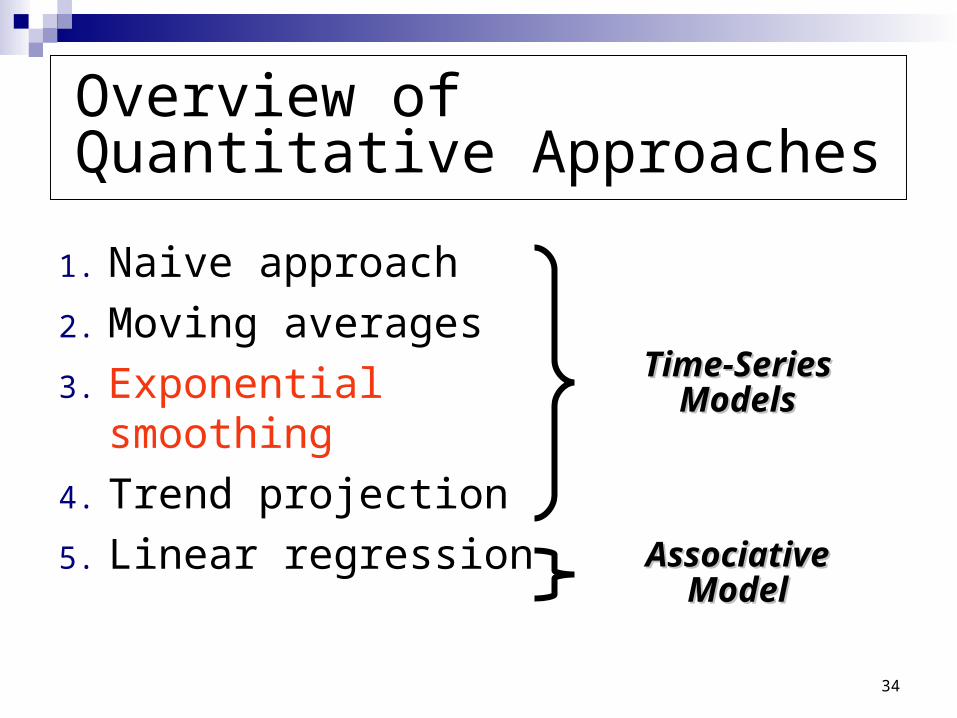

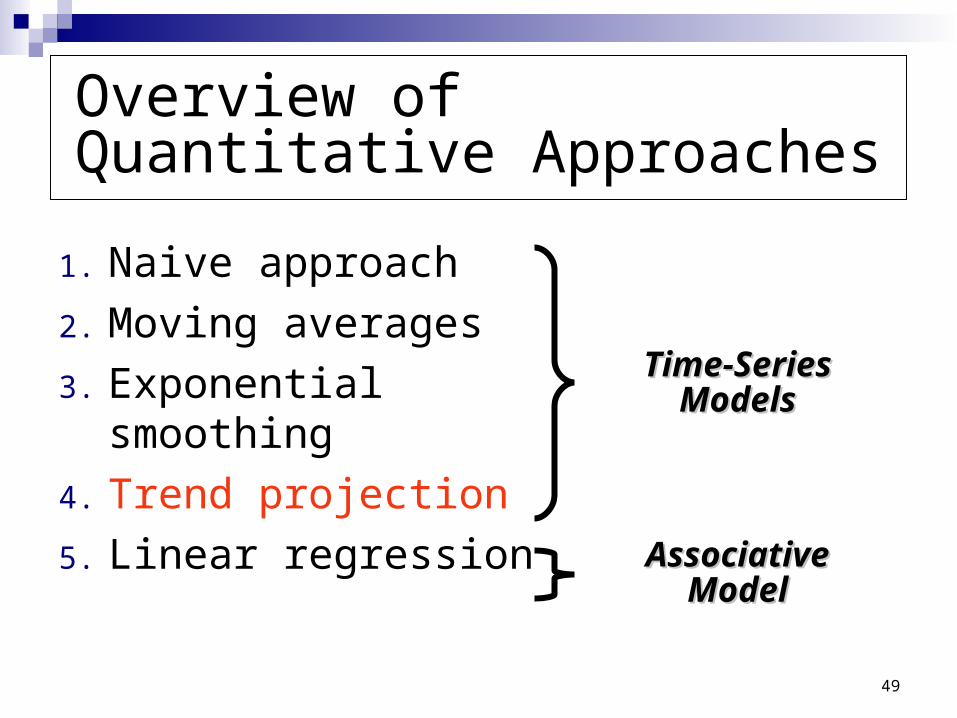

Overview of Quantitative Approaches

1. Naive approach

2. Moving averages

3. Exponential smoothing

4. Trend projection

5. Linear regression

Time-Series Time-Series ModelsModels

Associative Associative ModelModel

18

Set of evenly spaced numerical data Obtained by observing response

variable at regular time periods Forecast based only on past values

Assumes that factors influencing past and present will continue influence in future

Time Series Forecasting

19

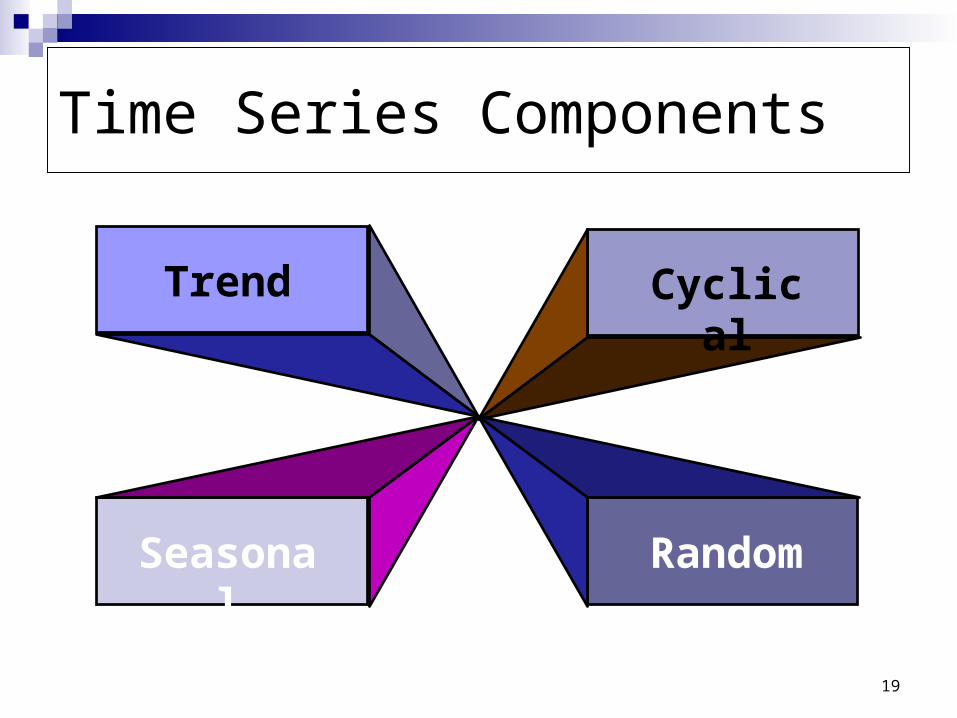

Trend

Seasonal

Cyclical

Random

Time Series Components

20

Components of DemandD

eman

d f

or

pro

du

ct o

r se

rvic

e

| | | |1 2 3 4

Year

Average demand over four years

Seasonal peaks

Trend component

Actual demand

Random variation

Figure 4.1Figure 4.1

21

Persistent, overall upward or downward pattern

Changes due to population, technology, age, culture, etc.

Typically several years duration

Trend Component

22

Regular pattern of up and down fluctuations

Due to weather, customs, etc. Occurs within a single year

Seasonal Component

Number ofPeriod Length Seasons

Week Day 7Month Week 4-4.5Month Day 28-31Year Quarter 4Year Month 12Year Week 52

23

Repeating up and down movements Affected by business cycle, political,

and economic factors Multiple years duration Often causal or

associative relationships

Cyclical Component

00 55 1010 1515 2020

24

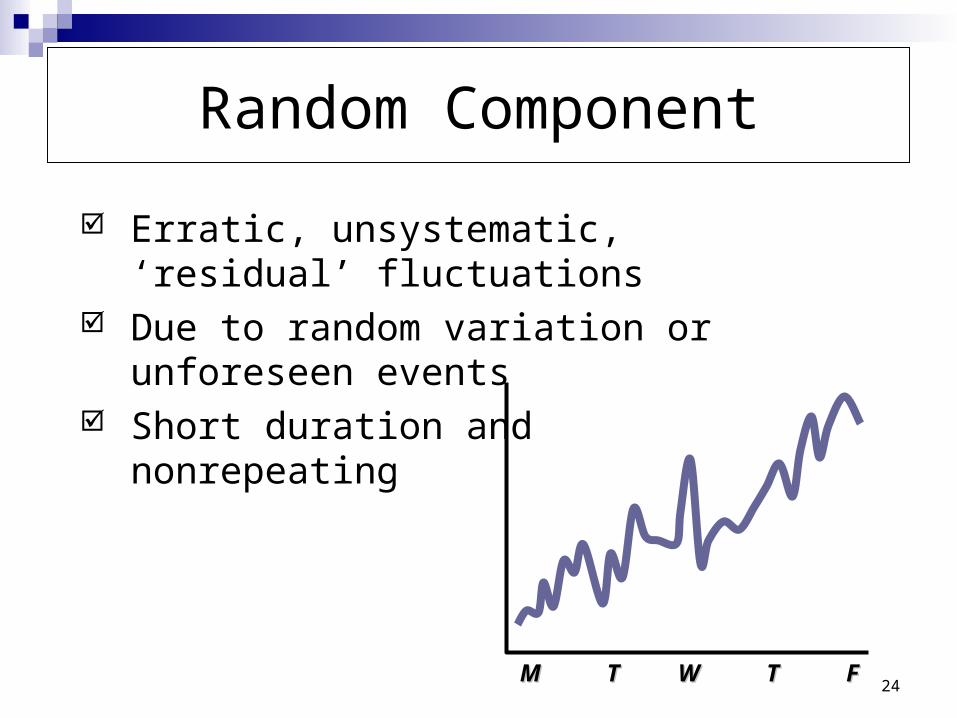

Erratic, unsystematic, ‘residual’ fluctuations

Due to random variation or unforeseen events

Short duration and nonrepeating

Random Component

MM TT WW TT FF

25

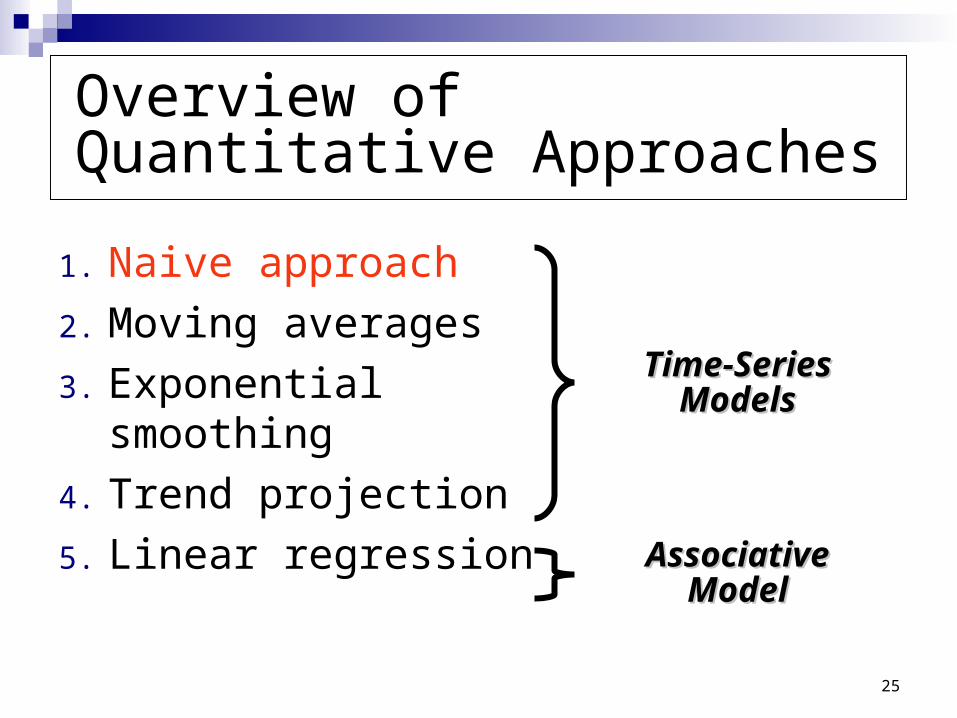

Overview of Quantitative Approaches

1. Naive approach

2. Moving averages

3. Exponential smoothing

4. Trend projection

5. Linear regression

Time-Series Time-Series ModelsModels

Associative Associative ModelModel

26

Naive Approach

Assumes demand in next period is the same as demand in most recent period e.g., If May sales were 48, then June

sales will be 48 Sometimes cost effective and

efficient

27

Overview of Quantitative Approaches

1. Naive approach

2. Moving averages

3. Exponential smoothing

4. Trend projection

5. Linear regression

Time-Series Time-Series ModelsModels

Associative Associative ModelModel

28

MA is a series of arithmetic means Used if little or no trend Used often for smoothing

Provides overall impression of data over time

Moving Average Method

Moving averageMoving average ==∑∑ demand in previous n periodsdemand in previous n periods

nn

29

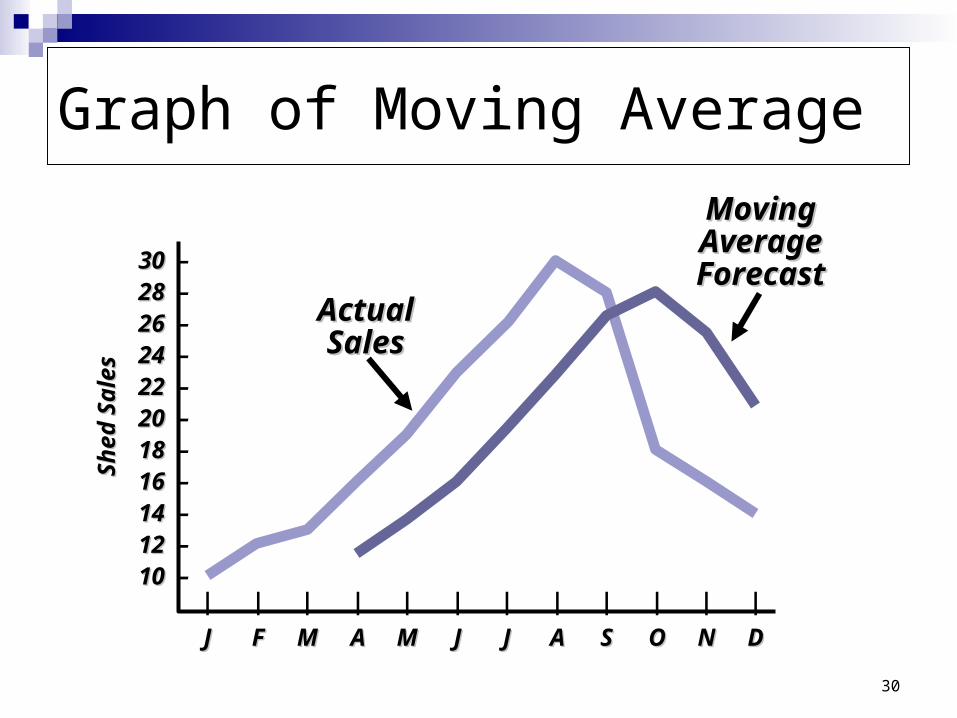

JanuaryJanuary 1010FebruaryFebruary 1212MarchMarch 1313AprilApril 1616MayMay 1919JuneJune 2323JulyJuly 2626

ActualActual 3-Month3-MonthMonthMonth Shed SalesShed Sales Moving AverageMoving Average

(12 + 13 + 16)/3 = 13 (12 + 13 + 16)/3 = 13 22//33

(13 + 16 + 19)/3 = 16(13 + 16 + 19)/3 = 16(16 + 19 + 23)/3 = 19 (16 + 19 + 23)/3 = 19 11//33

Moving Average Example

101012121313

((1010 + + 1212 + + 1313)/3 = 11 )/3 = 11 22//33

30

Graph of Moving Average

| | | | | | | | | | | |

JJ FF MM AA MM JJ JJ AA SS OO NN DD

Sh

ed S

ales

Sh

ed S

ales

30 30 –28 28 –26 26 –24 24 –22 22 –20 20 –18 18 –16 16 –14 14 –12 12 –10 10 –

Actual Actual SalesSales

Moving Moving Average Average ForecastForecast

31

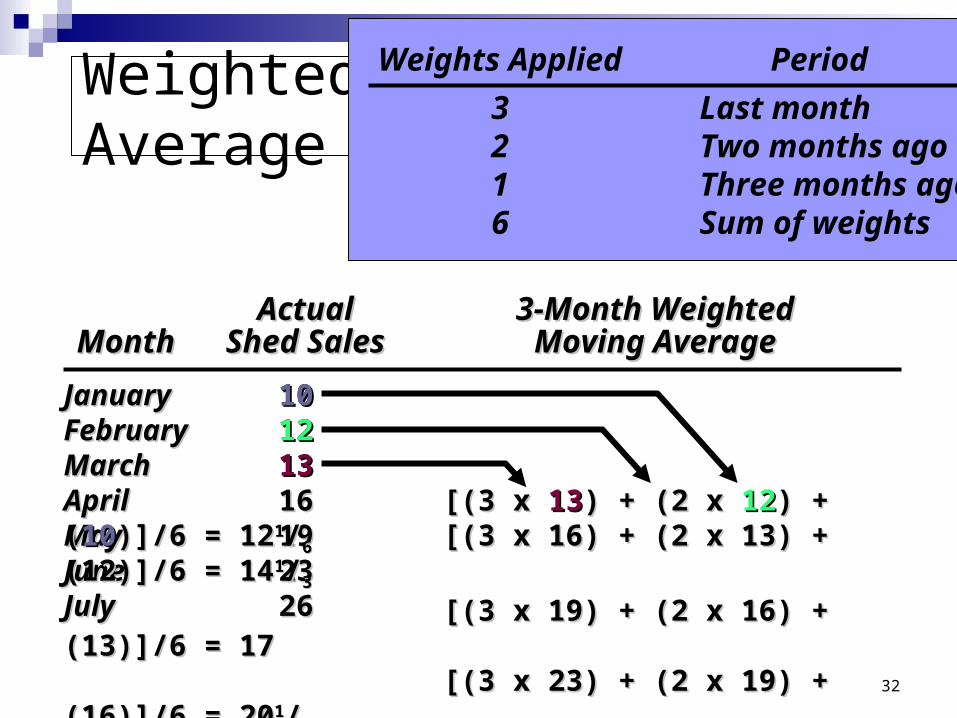

Used when trend is present Older data usually less important

Weights based on experience and intuition

Weighted Moving Average

WeightedWeightedmoving averagemoving average ==

∑∑ ((weight for period nweight for period n)) x x ((demand in period ndemand in period n))

∑∑ weightsweights

32

JanuaryJanuary 1010FebruaryFebruary 1212MarchMarch 1313AprilApril 1616MayMay 1919JuneJune 2323JulyJuly 2626

ActualActual 3-Month Weighted3-Month WeightedMonthMonth Shed SalesShed Sales Moving AverageMoving Average

[(3 x 16) + (2 x 13) + (12)]/6 = 14[(3 x 16) + (2 x 13) + (12)]/6 = 1411//33

[(3 x 19) + (2 x 16) + (13)]/6 = 17[(3 x 19) + (2 x 16) + (13)]/6 = 17[(3 x 23) + (2 x 19) + (16)]/6 = 20[(3 x 23) + (2 x 19) + (16)]/6 = 2011//22

Weighted Moving Average

101012121313

[(3 x [(3 x 1313) + (2 x ) + (2 x 1212) + () + (1010)]/6 = 12)]/6 = 1211//66

Weights Applied Period

3 Last month2 Two months ago1 Three months ago6 Sum of weights

33

Moving Average And Weighted Moving Average

30 30 –

25 25 –

20 20 –

15 15 –

10 10 –

5 5 –

Sa

les

de

man

dS

ale

s d

em

and

| | | | | | | | | | | |

JJ FF MM AA MM JJ JJ AA SS OO NN DD

Actual Actual salessales

Moving Moving averageaverage

Weighted Weighted moving moving averageaverage

Figure 4.2Figure 4.2

34

Overview of Quantitative Approaches

1. Naive approach

2. Moving averages

3. Exponential smoothing

4. Trend projection

5. Linear regression

Time-Series Time-Series ModelsModels

Associative Associative ModelModel

35

Exponential Smoothing

New forecast =New forecast = last period’s forecastlast period’s forecast+ + ((last period’s actual demand last period’s actual demand

– – last period’s forecastlast period’s forecast))

FFtt = F = Ft t – 1– 1 + + ((AAt t – 1– 1 - - F Ft t – 1– 1))

wherewhere FFtt == new forecastnew forecast

FFt t – 1– 1 == previous forecastprevious forecast

== smoothing (or weighting) smoothing (or weighting) constant constant (0 (0 1) 1)

36

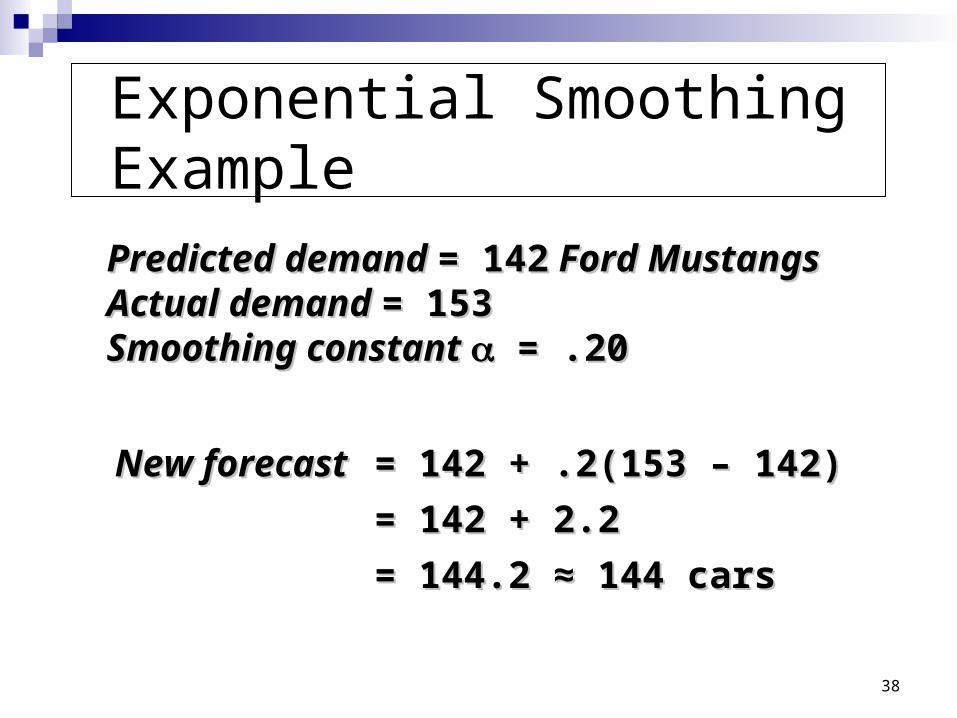

Exponential Smoothing Example

Predicted demand Predicted demand = 142= 142 Ford Mustangs Ford MustangsActual demand Actual demand = 153= 153Smoothing constant Smoothing constant = .20 = .20

37

Exponential Smoothing Example

Predicted demand Predicted demand = 142= 142 Ford Mustangs Ford MustangsActual demand Actual demand = 153= 153Smoothing constant Smoothing constant = .20 = .20

New forecastNew forecast = 142 + .2(153 – 142)= 142 + .2(153 – 142)

38

Exponential Smoothing Example

Predicted demand Predicted demand = 142= 142 Ford Mustangs Ford MustangsActual demand Actual demand = 153= 153Smoothing constant Smoothing constant = .20 = .20

New forecastNew forecast = 142 + .2(153 – 142)= 142 + .2(153 – 142)

= 142 + 2.2= 142 + 2.2

= 144.2 ≈ 144 cars= 144.2 ≈ 144 cars

39

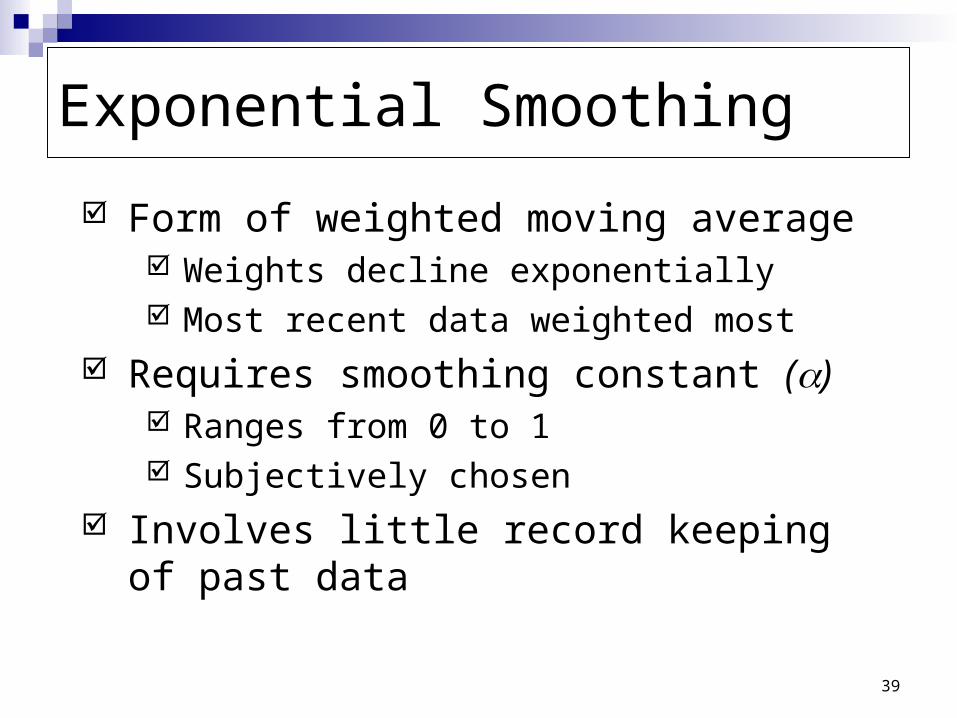

Form of weighted moving average Weights decline exponentially Most recent data weighted most

Requires smoothing constant () Ranges from 0 to 1 Subjectively chosen

Involves little record keeping of past data

Exponential Smoothing

40

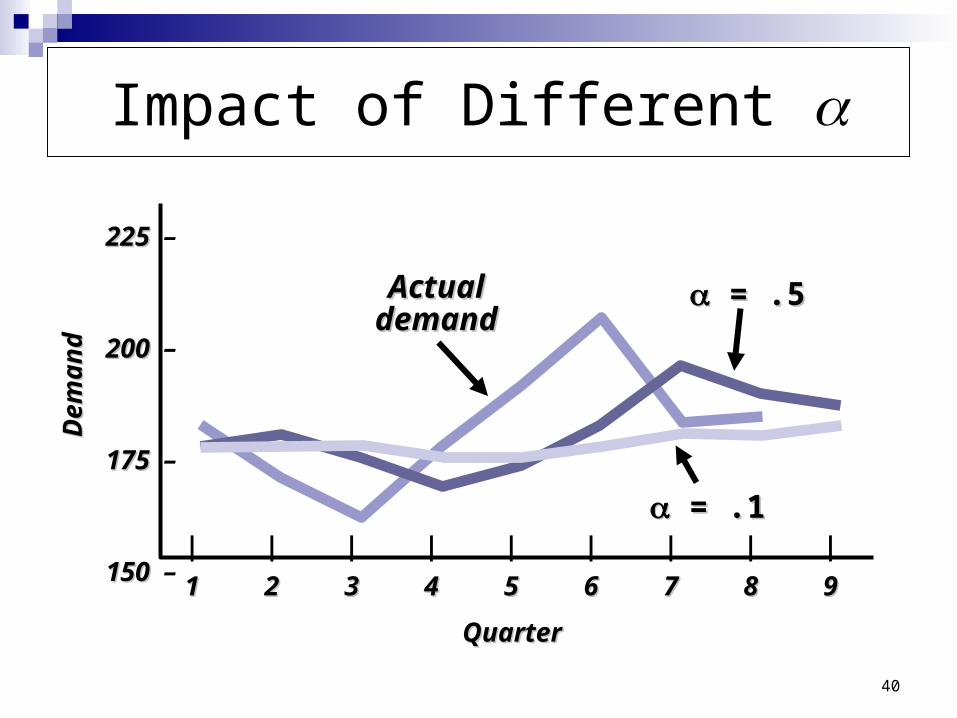

Impact of Different

225 225 –

200 200 –

175 175 –

150 150 –| | | | | | | | |

11 22 33 44 55 66 77 88 99

QuarterQuarter

De

ma

nd

De

ma

nd

= .1= .1

Actual Actual demanddemand

= .5= .5

41

Choosing

The objective is to obtain the most The objective is to obtain the most accurate forecast no matter the accurate forecast no matter the techniquetechnique

We generally do this by selecting the We generally do this by selecting the model that gives us the lowest forecast model that gives us the lowest forecast errorerror

Forecast errorForecast error = Actual demand - Forecast value= Actual demand - Forecast value

= A= Att - F - Ftt

42

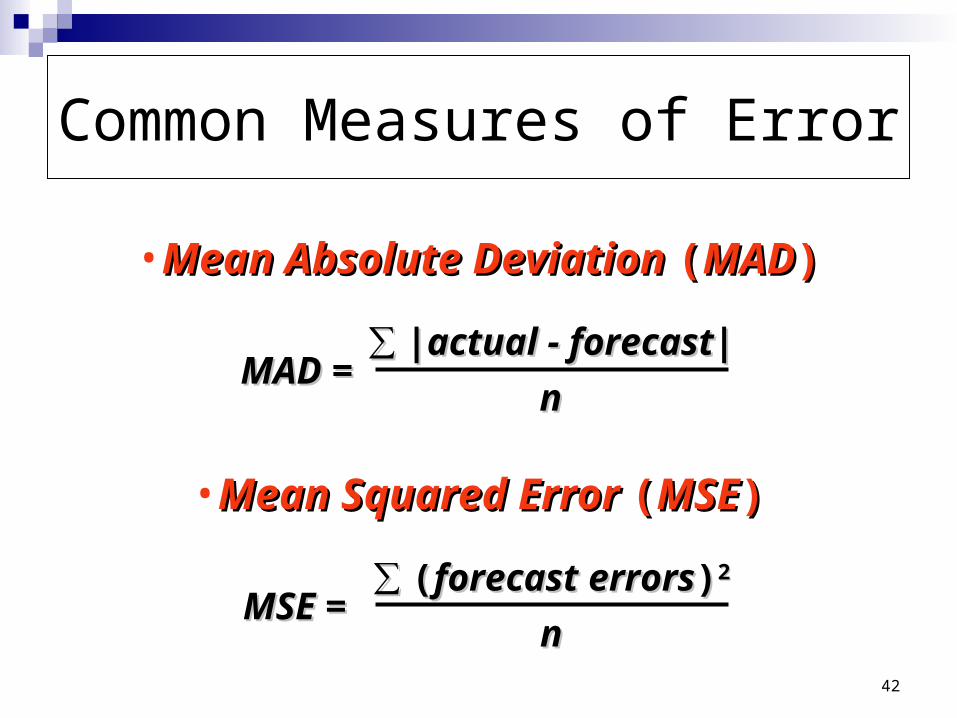

Common Measures of Error

•Mean Absolute Deviation Mean Absolute Deviation ((MADMAD))

MAD =MAD =∑∑ |actual - forecast||actual - forecast|

nn

•Mean Squared Error Mean Squared Error ((MSEMSE))

MSE =MSE =∑∑ ((forecast errorsforecast errors))22

nn

43

Common Measures of Error

Mean Absolute Percent Error Mean Absolute Percent Error ((MAPEMAPE))

MAPE =MAPE =100 100 ∑∑ |actual |actualii - forecast - forecastii|/actual|/actualii

nn

nn

i i = 1= 1

44

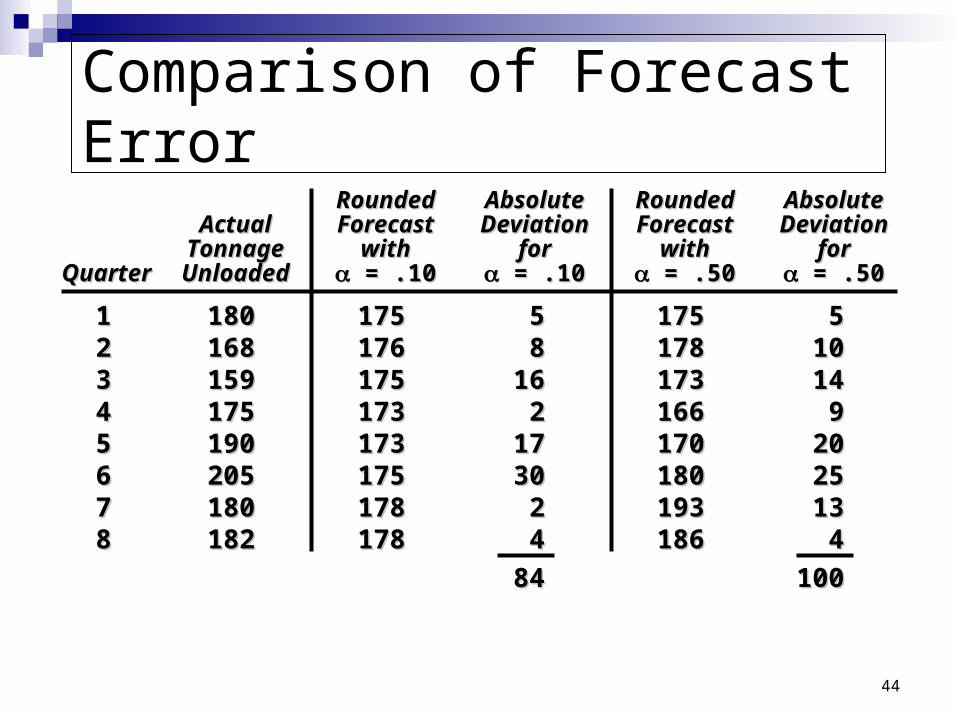

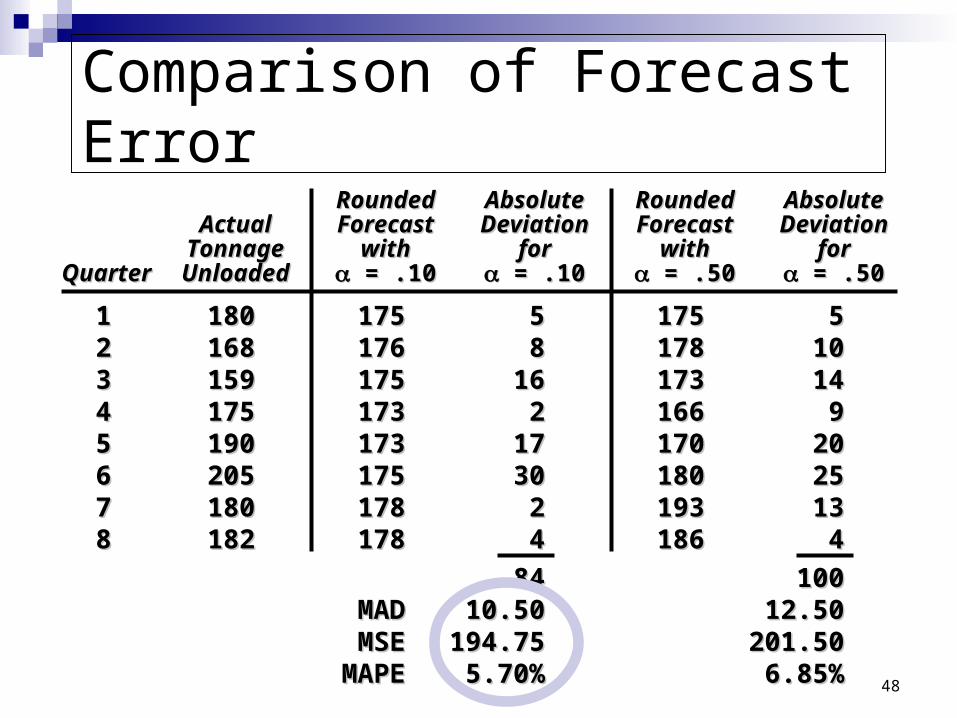

Comparison of Forecast Error

RoundedRounded AbsoluteAbsolute RoundedRounded AbsoluteAbsoluteActualActual ForecastForecast DeviationDeviation ForecastForecast DeviationDeviation

TonnageTonnage withwith forfor withwith forforQuarterQuarter UnloadedUnloaded = .10 = .10 = .10 = .10 = .50 = .50 = .50 = .50

11 180180 175175 55 175175 5522 168168 176176 88 178178 101033 159159 175175 1616 173173 141444 175175 173173 22 166166 9955 190190 173173 1717 170170 202066 205205 175175 3030 180180 252577 180180 178178 22 193193 131388 182182 178178 44 186186 44

8484 100100

45

Comparison of Forecast Error

RoundedRounded AbsoluteAbsolute RoundedRounded AbsoluteAbsoluteActualActual ForecastForecast DeviationDeviation ForecastForecast DeviationDeviationTonageTonage withwith forfor withwith forfor

QuarterQuarter UnloadedUnloaded = .10 = .10 = .10 = .10 = .50 = .50 = .50 = .50

11 180180 175175 55 175175 5522 168168 176176 88 178178 101033 159159 175175 1616 173173 141444 175175 173173 22 166166 9955 190190 173173 1717 170170 202066 205205 175175 3030 180180 252577 180180 178178 22 193193 131388 182182 178178 44 186186 44

8484 100100

MAD =∑ |deviations|

n

= 84/8 = 10.50

For = .10

= 100/8 = 12.50

For = .50

46

Comparison of Forecast Error

RoundedRounded AbsoluteAbsolute RoundedRounded AbsoluteAbsoluteActualActual ForecastForecast DeviationDeviation ForecastForecast DeviationDeviationTonageTonage withwith forfor withwith forfor

QuarterQuarter UnloadedUnloaded = .10 = .10 = .10 = .10 = .50 = .50 = .50 = .50

11 180180 175175 55 175175 5522 168168 176176 88 178178 101033 159159 175175 1616 173173 141444 175175 173173 22 166166 9955 190190 173173 1717 170170 202066 205205 175175 3030 180180 252577 180180 178178 22 193193 131388 182182 178178 44 186186 44

8484 100100MADMAD 10.5010.50 12.5012.50

= 1,558/8 = 194.75

For = .10

= 1,612/8 = 201.50

For = .50

MSE =∑ (forecast errors)2

n

47

Comparison of Forecast Error

RoundedRounded AbsoluteAbsolute RoundedRounded AbsoluteAbsoluteActualActual ForecastForecast DeviationDeviation ForecastForecast DeviationDeviationTonageTonage withwith forfor withwith forfor

QuarterQuarter UnloadedUnloaded = .10 = .10 = .10 = .10 = .50 = .50 = .50 = .50

11 180180 175175 55 175175 5522 168168 176176 88 178178 101033 159159 175175 1616 173173 141444 175175 173173 22 166166 9955 190190 173173 1717 170170 202066 205205 175175 3030 180180 252577 180180 178178 22 193193 131388 182182 178178 44 186186 44

8484 100100MADMAD 10.5010.50 12.5012.50MSEMSE 194.75194.75 201.50201.50

= 45.62/8 = 5.70%

For = .10

= 54.8/8 = 6.85%

For = .50

MAPE =100 ∑ |deviationi|/actuali

n

n

i = 1

48

Comparison of Forecast Error

RoundedRounded AbsoluteAbsolute RoundedRounded AbsoluteAbsoluteActualActual ForecastForecast DeviationDeviation ForecastForecast DeviationDeviation

TonnageTonnage withwith forfor withwith forforQuarterQuarter UnloadedUnloaded = .10 = .10 = .10 = .10 = .50 = .50 = .50 = .50

11 180180 175175 55 175175 5522 168168 176176 88 178178 101033 159159 175175 1616 173173 141444 175175 173173 22 166166 9955 190190 173173 1717 170170 202066 205205 175175 3030 180180 252577 180180 178178 22 193193 131388 182182 178178 44 186186 44

8484 100100MADMAD 10.5010.50 12.5012.50MSEMSE 194.75194.75 201.50201.50

MAPEMAPE 5.70%5.70% 6.85%6.85%

49

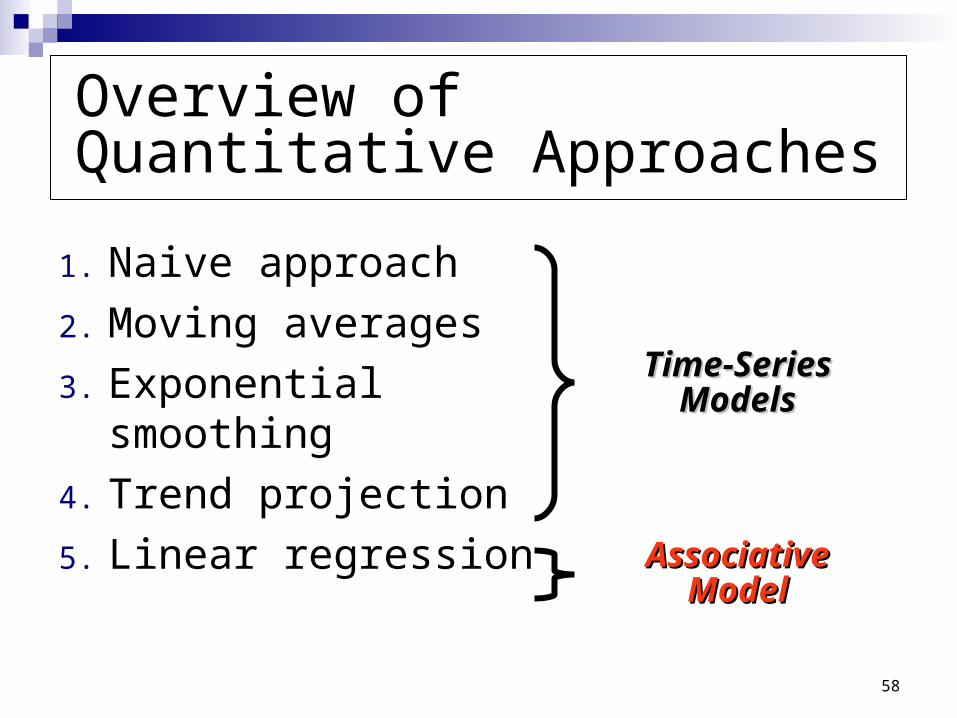

Overview of Quantitative Approaches

1. Naive approach

2. Moving averages

3. Exponential smoothing

4. Trend projection

5. Linear regression

Time-Series Time-Series ModelsModels

Associative Associative ModelModel

50

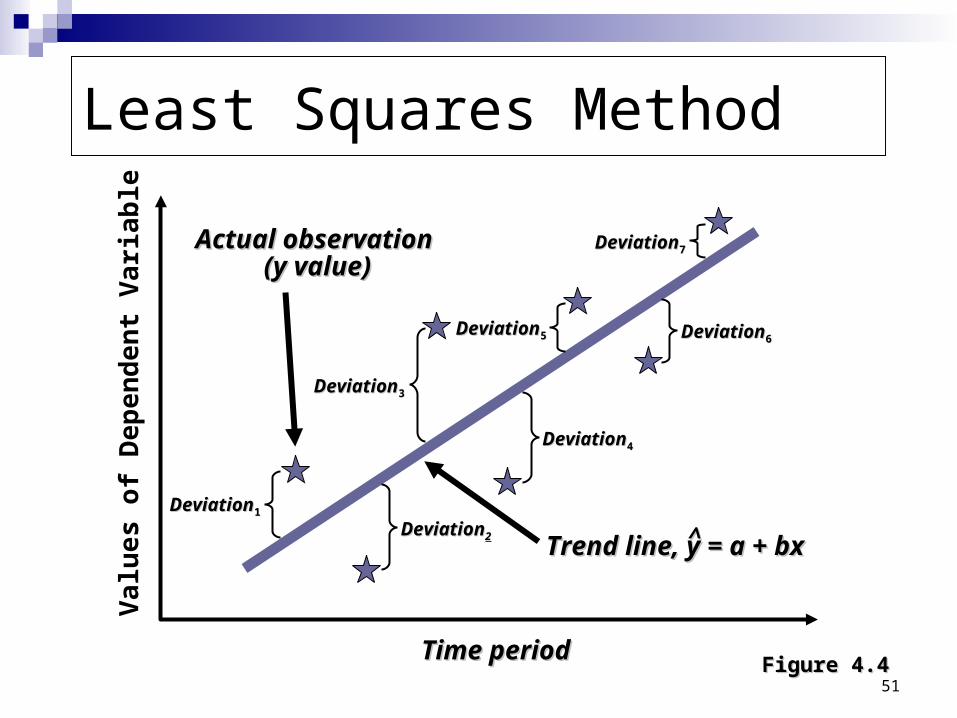

Trend Projections

Fitting a trend line to historical data points Fitting a trend line to historical data points to project into the medium-to-long-rangeto project into the medium-to-long-range

Linear trends can be found using the least Linear trends can be found using the least squares techniquesquares technique

y y = = a a + + bxbx^̂

where ywhere y= computed value of the = computed value of the variable to be predicted (dependent variable to be predicted (dependent variable)variable)aa= y-axis intercept= y-axis interceptbb= slope of the regression line= slope of the regression linexx= the independent variable (= the independent variable (in this in this case timecase time))

^̂

51

Least Squares Method

Time periodTime period

Va

lue

s o

f D

ep

end

en

t V

ari

able

Figure 4.4Figure 4.4

DeviationDeviation11

DeviationDeviation55

DeviationDeviation77

DeviationDeviation22

DeviationDeviation66

DeviationDeviation44

DeviationDeviation33

Actual observation Actual observation (y value)(y value)

Trend line, y = a + bxTrend line, y = a + bx^̂

52

Least Squares Method

Time periodTime period

Va

lue

s o

f D

ep

end

en

t V

ari

able

Figure 4.4Figure 4.4

DeviationDeviation11

DeviationDeviation55

DeviationDeviation77

DeviationDeviation22

DeviationDeviation66

DeviationDeviation44

DeviationDeviation33

Actual observation Actual observation (y value)(y value)

Trend line, y = a + bxTrend line, y = a + bx^̂

Least squares method minimizes the sum of the

squared errors (deviations)

53

Least Squares Method

Equations to calculate the regression variablesEquations to calculate the regression variables

b =b =xy - nxyxy - nxy

xx22 - nx - nx22

y y = = a a + + bxbx^̂

a = y - bxa = y - bx

54

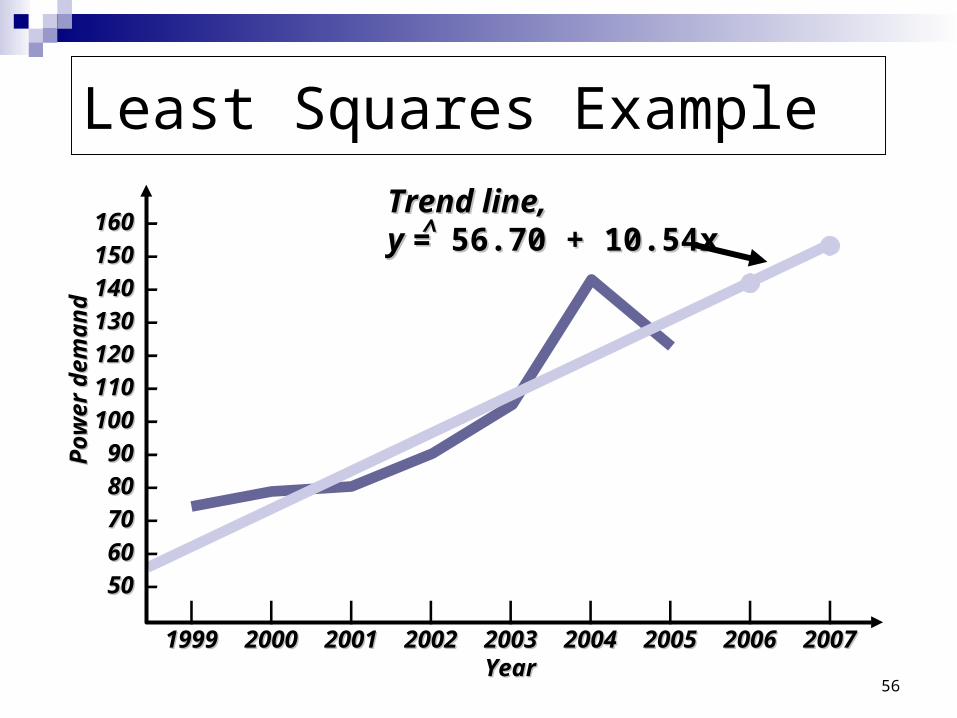

Least Squares Example

b b = = = 10.54= = = 10.54∑∑xy - nxyxy - nxy

∑∑xx22 - nx - nx22

3,063 - (7)(4)(98.86)3,063 - (7)(4)(98.86)

140 - (7)(4140 - (7)(422))

aa = = yy - - bxbx = 98.86 - 10.54(4) = 56.70 = 98.86 - 10.54(4) = 56.70

TimeTime Electrical Power Electrical Power YearYear Period (x)Period (x) DemandDemand xx22 xyxy

19991999 11 7474 11 747420002000 22 7979 44 15815820012001 33 8080 99 24024020022002 44 9090 1616 36036020032003 55 105105 2525 52552520042004 66 142142 3636 85285220052005 77 122122 4949 854854

∑∑xx = 28 = 28 ∑∑yy = 692 = 692 ∑∑xx22 = 140 = 140 ∑∑xyxy = 3,063 = 3,063xx = 4 = 4 yy = 98.86 = 98.86

55

Least Squares Example

b b = = = 10.54= = = 10.54xy - nxyxy - nxy

xx22 - nx - nx22

3,063 - (7)(4)(98.86)3,063 - (7)(4)(98.86)

140 - (7)(4140 - (7)(422))

aa = = yy - - bxbx = 98.86 - 10.54(4) = 56.70 = 98.86 - 10.54(4) = 56.70

TimeTime Electrical Power Electrical Power YearYear Period (x)Period (x) DemandDemand xx22 xyxy

19991999 11 7474 11 747420002000 22 7979 44 15815820012001 33 8080 99 24024020022002 44 9090 1616 36036020032003 55 105105 2525 52552520042004 66 142142 3636 85285220052005 77 122122 4949 854854

xx = 28 = 28 yy = 692 = 692 xx22 = 140 = 140 xyxy = 3,063 = 3,063xx = 4 = 4 yy = 98.86 = 98.86

The trend line is

y = 56.70 + 10.54x^

56

Least Squares Example

| | | | | | | | |19991999 20002000 20012001 20022002 20032003 20042004 20052005 20062006 20072007

160 160 –

150 150 –

140 140 –

130 130 –

120 120 –

110 110 –

100 100 –

90 90 –

80 80 –

70 70 –

60 60 –

50 50 –

YearYear

Po

wer

dem

and

Po

wer

dem

and

Trend line,Trend line,y y = 56.70 + 10.54x= 56.70 + 10.54x^̂

58

Overview of Quantitative Approaches

1. Naive approach

2. Moving averages

3. Exponential smoothing

4. Trend projection

5. Linear regression

Time-Series Time-Series ModelsModels

Associative Associative ModelModel

59

Associative Forecasting

Used when changes in one or more Used when changes in one or more independent variables can be used to predict independent variables can be used to predict

the changes in the dependent variablethe changes in the dependent variable

Most common technique is linear Most common technique is linear regression analysisregression analysis

We apply this technique just as we did We apply this technique just as we did in the time series examplein the time series example

60

linear regression analysis

Forecasting an outcome based on predictor Forecasting an outcome based on predictor variables using the least squares techniquevariables using the least squares technique

y y = = a a + + bxbx^̂

where ywhere y= computed value of the = computed value of the variable to be predicted (dependent variable to be predicted (dependent variable)variable)aa= y-axis intercept= y-axis interceptbb= slope of the regression line= slope of the regression linexx= the independent variable though = the independent variable though to predict the value of the to predict the value of the dependent variabledependent variable

^̂

61

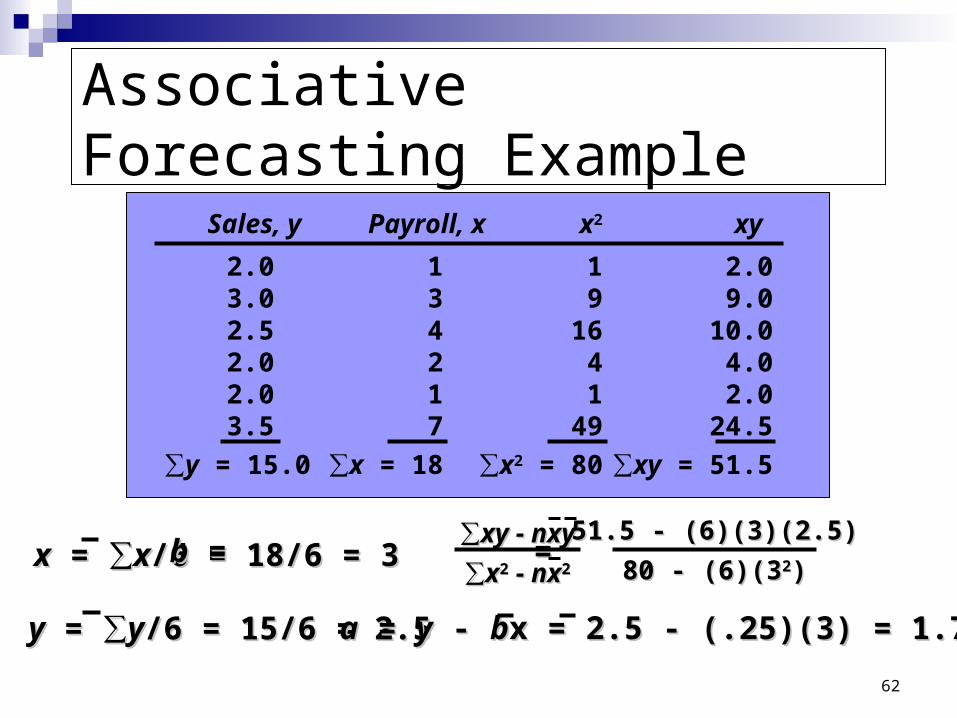

Associative Forecasting Example

SalesSales Local PayrollLocal Payroll($000,000), y($000,000), y ($000,000,000), x($000,000,000), x

2.02.0 113.03.0 332.52.5 442.02.0 222.02.0 113.53.5 77

4.0 –

3.0 –

2.0 –

1.0 –

| | | | | | |0 1 2 3 4 5 6 7

Sal

es

Area payroll

62

Associative Forecasting Example

Sales, y Payroll, x x2 xy

2.0 1 1 2.03.0 3 9 9.02.5 4 16 10.02.0 2 4 4.02.0 1 1 2.03.5 7 49 24.5

∑y = 15.0 ∑x = 18 ∑x2 = 80 ∑xy = 51.5

xx = = ∑∑xx/6 = 18/6 = 3/6 = 18/6 = 3

yy = = ∑∑yy/6 = 15/6 = 2.5/6 = 15/6 = 2.5

bb = = = .25 = = = .25∑∑xy - nxyxy - nxy

∑∑xx22 - nx - nx22

51.5 - (6)(3)(2.5)51.5 - (6)(3)(2.5)

80 - (6)(380 - (6)(322))

aa = = yy - - bbx = 2.5 - (.25)(3) = 1.75x = 2.5 - (.25)(3) = 1.75

63

Associative Forecasting Example

4.0 –

3.0 –

2.0 –

1.0 –

| | | | | | |0 1 2 3 4 5 6 7

Sal

es

Area payroll

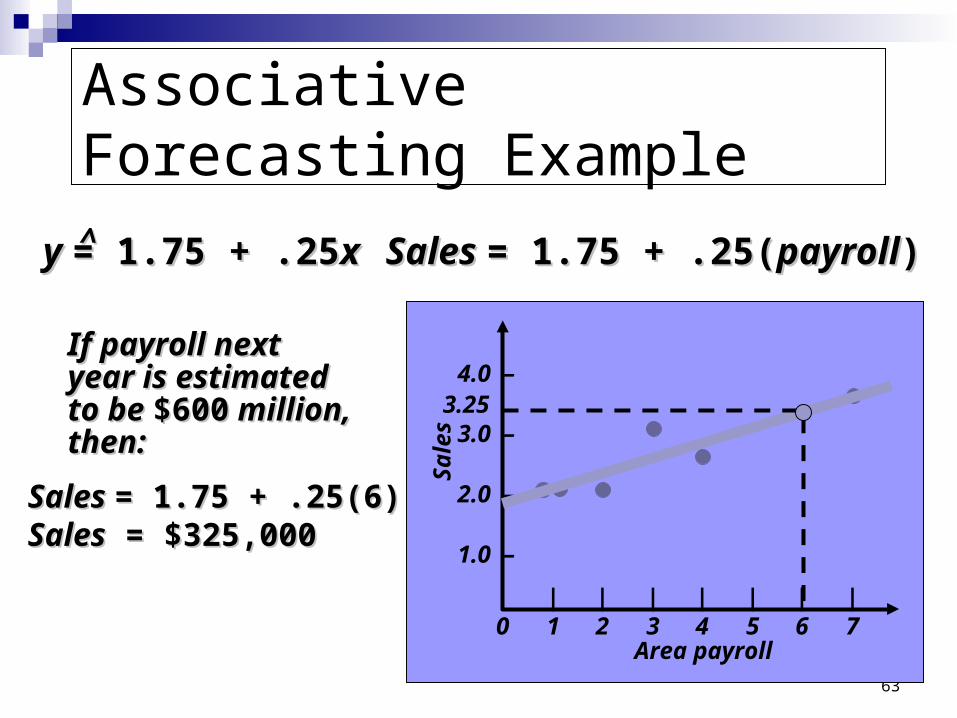

y y = 1.75 + .25= 1.75 + .25xx^̂ Sales Sales = 1.75 + .25(= 1.75 + .25(payrollpayroll))

If payroll next year If payroll next year is estimated to be is estimated to be $600$600 million, then: million, then:

Sales Sales = 1.75 + .25(6)= 1.75 + .25(6)SalesSales = $325,000 = $325,000

3.25

64

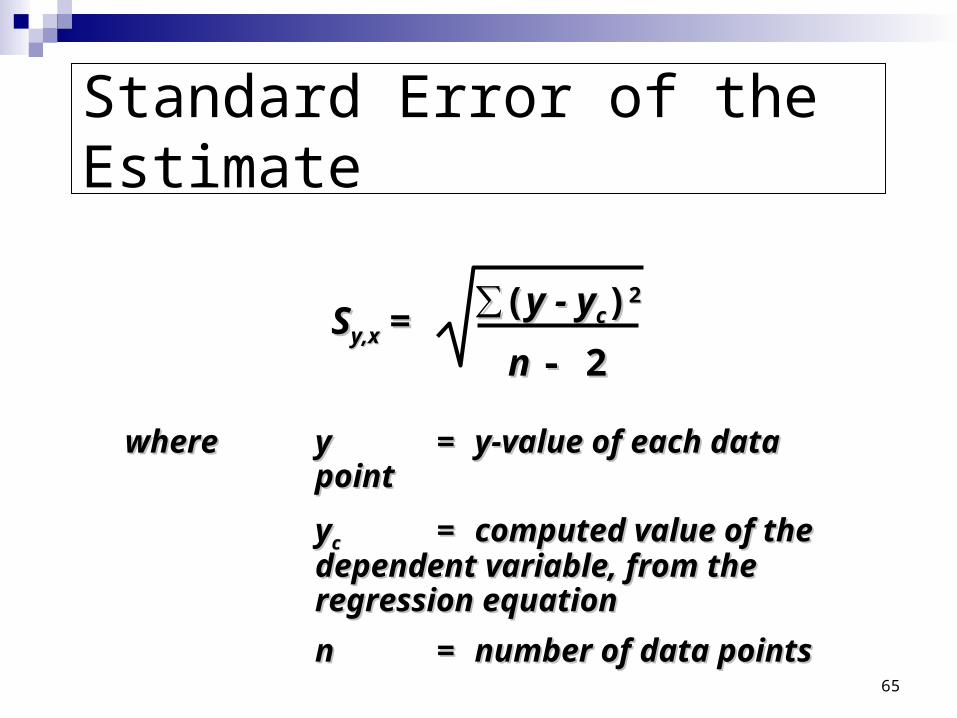

To measure the accuracy of the regression estimates, we must compute the standard error of the estimate, Sy,x.Sy,x.

This computation is called the standard deviation of the regression. It measures the error from the dependent variable y, to the regression line, rather than to the mean.

Standard Error of the Estimate

65

Standard Error of the Estimate

wherewhere yy == y-value of each data y-value of each data pointpoint

yycc == computed value of the computed value of the dependent variable, from the dependent variable, from the regression equationregression equation

nn == number of data pointsnumber of data points

SSy,xy,x = =∑∑((y - yy - ycc))22

n n - 2- 2

66

Standard Error of the Estimate

Computationally, this equation is Computationally, this equation is considerably easier to useconsiderably easier to use

We use the standard error to set up We use the standard error to set up prediction intervals around the prediction intervals around the

point estimatepoint estimate

SSy,xy,x = =∑∑yy22 - a - a∑∑y - by - b∑∑xyxy

n n - 2- 2

67

Associative Forecasting Example

Sales, y Payroll, x x2 xy

2.0 1 1 2.03.0 3 9 9.02.5 4 16 10.02.0 2 4 4.02.0 1 1 2.03.5 7 49 24.5

∑y = 15.0 ∑x = 18 ∑x2 = 80 ∑xy = 51.5

xx = = ∑∑xx/6 = 18/6 = 3/6 = 18/6 = 3

yy = = ∑∑yy/6 = 15/6 = 2.5/6 = 15/6 = 2.5

bb = = = .25 = = = .25∑∑xy - nxyxy - nxy

∑∑xx22 - nx - nx22

51.5 - (6)(3)(2.5)51.5 - (6)(3)(2.5)

80 - (6)(380 - (6)(322))

aa = = yy - - bbx = 2.5 - (.25)(3) = 1.75x = 2.5 - (.25)(3) = 1.75

68

Standard Error of the Estimate

4.0 –

3.0 –

2.0 –

1.0 –

| | | | | | |0 1 2 3 4 5 6 7

Sal

es

Area payroll

3.25

SSy,xy,x = = = =∑∑yy22 - a - a∑∑y - by - b∑∑xyxyn n - 2- 2

39.5 - 1.75(15) - .25(51.5)39.5 - 1.75(15) - .25(51.5)6 - 26 - 2

SSy,xy,x = = .306.306

The standard error The standard error of the estimate is of the estimate is $30,600$30,600 in sales in sales

69

coefficient of correlation

Regression line merely describe the relationship among variables.

Another way to evaluate the relationship between two variable is to compute the coefficient of correlation.

70

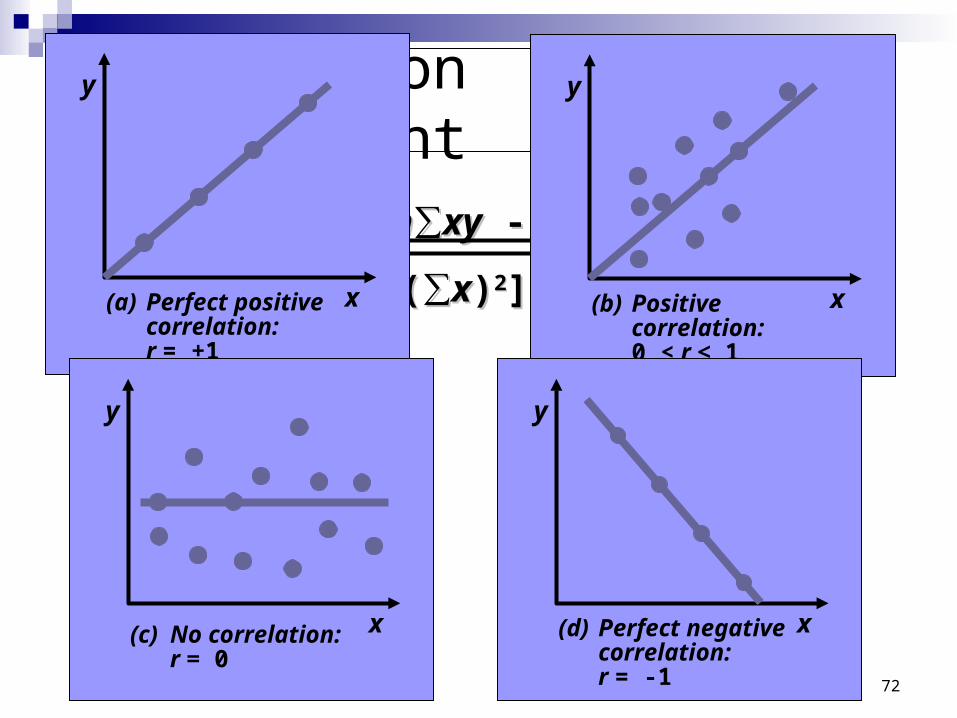

How strong is the linear relationship between the variables?

Correlation does not necessarily imply causality!

Coefficient of correlation, r, measures degree of association Values range from -1 to +1

Correlation

71

Correlation Coefficient

r = r = nnxyxy - - xxy y

[[nnxx22 - ( - (xx))22][][nnyy22 - ( - (yy))22]]

72

Correlation Coefficient

r = r = nn∑∑xyxy - - ∑∑xx∑∑y y

[[nn∑∑xx22 - ( - (∑∑xx))22][][nn∑∑yy22 - ( - (∑∑yy))22]]

y

x(a) Perfect positive correlation: r = +1

y

x(b) Positive correlation: 0 < r < 1

y

x(c) No correlation: r = 0

y

x(d) Perfect negative correlation: r = -1

73

Coefficient of Determination, r2, measures the percent of change in y predicted by the change in x Values range from 0 to 1 Easy to interpret

Correlation

For the Nodel Construction example:For the Nodel Construction example:

r r = .901= .901

rr22 = .81 = .81

74

Multiple Regression Analysis

If more than one independent variable is to be If more than one independent variable is to be used in the model, linear regression can be used in the model, linear regression can be

extended to multiple regression to extended to multiple regression to accommodate several independent variablesaccommodate several independent variables

y y = = a a + + bb11xx11 + b + b22xx22 … …^̂

Computationally, this is quite Computationally, this is quite complex and generally done on the complex and generally done on the

computercomputer

75

Multiple Regression Analysis

y y = 1.80 + .30= 1.80 + .30xx11 - 5.0 - 5.0xx22^̂

In the Nodel example, including interest rates in In the Nodel example, including interest rates in the model gives the new equation:the model gives the new equation:

An improved correlation coefficient of r An improved correlation coefficient of r = .96= .96 means this model does a better job of predicting means this model does a better job of predicting the change in construction salesthe change in construction sales

Sales Sales = 1.80 + .30(6) - 5.0(.12) = 3.00= 1.80 + .30(6) - 5.0(.12) = 3.00Sales Sales = $300,000= $300,000

76

Have nice day!