atul ltd. research report

TRANSCRIPT

AtulLtdIndia|DyesandPigmentsIndustry|InitiatingCoverageAboutthecompany• Establishedsince1947,thiscompanyisoneoftheoldestandleadingplayers

intheindustry.• Theproductprofileofthecompanyisverybroadincludingaromatics,bulk

chemicalsandintermediates,colours,pharmaceuticalsandintermediates,cropprotection/agrochemicalsandpolymers.

• ThekeytoAtul’ssteady-goingfinancialperformanceisitsglobalpositioninginaromatics,ledbyP-cresolandderivatives,coloursbecauseofsulphurblackandvatdyesandpolymersepoxyandsulphonesandbycropprotectionthroughformulationof2,4D

MacroeconomicOutlook• Sizeofworldchemicalindustryis4.4trillion$anditgrewby2%in2015:Indian

Chemicalindustry(sizeUS$103bn)grewby3%,butisstillranked7afterChina(sizeUS$1.5tn),theUSA(sizeUS$630bn),Germany(sizeUS$198bn),Japan(sizeUS$190bn),SouthKorea(sizeUS$165bn)andFrance(sizeUS$107bn).Accordingtoaleadingconsultingfirm,IndiahasthepotentialtogrowitsSpecialityChemicalsindustryat9%.

• Thechemicalindustryisheavilydependentonoilandoilproductsasrawmaterial.Alotofproductsarecommoditiesandlackpricingpower.CompanieswhichspendonR&DandareabletogeneratesustainableholdonValueproductslikespecialtychemicals,createanedgeoverothers.

• SomeGrowthDriversfortheindustryare:

1. Rise in global GDP and purchasing power worldwide, leading to increasedconsumptionandrelatedproducts

2. Low cost manufacturing , refining processes to cut costs, also environmentrelatedcompliancesandcosts

3. 100%FDIbringinginmoreinvestment,infrastructureandtechnology4. Governmentsupportininfrastructure,policiesandR&D

DEMANDSIDEECONOMICS SUPPLYSIDEECONOMICS• Aschemicalisamajorinputinalot

industriesvaryingfromcropstoconstructiontoadhesivestoaromatics,itsdemandformostoftheproductsaredeterminedbytheindustrialgrowthdriversofgrowthinGlobalGDPandincreaseinconsumptionanddemandoftheseproducts.

• SpecificallyforATULltd.Upturninglobaleconomicscenarioplaysamajorroleas55%ofitssalesarefromExports.

• ButanindustryplayersuchasAtulcanincreasesalesandcreateamoat:

1. Creatingcomplex,valueaddedproductsthroughfocusonR&D.

2. CreatingmoreBrandstocreateproductdifferentiation

3. Enhancingcapacityandcostleadershipinthoseproductstokeepthemoatsustainable

• Crudeisthemaincomponentofrawmaterialandfluctuationinitspricesplaysanimportantroleintotalsales.

• Crudepricesfluctuatedbetween22$-66$in2015-2016.SuchlowlevelsofrawmaterialpricesresultedinlowerTotalSalesasAtulltd.wasnotabletoretaintheadvantageofdecreaseinvalueofrawmaterialsduetolackofpricingpowerinlargenumberofsegmentsandproducts,duetotheircommoditynature.

• Percentageimportofrawmaterialsis28%oftotalpurchasesindicatinglowerimpactofrupeedepreciationonitsrawmaterialcost.

• Furtherstabilityandupturninoilpriceswillboostsalesgrowth.

27August2016

SELLCMP:Rs.2118

COMPANYDATAO/SShares(Cr.) 3

MARKETCAP(RSCr.) 6284

52WKLOW/HIGH 1150-2299

PARVALUE(Rs.) 10

FY16 FY15 FY14

NETSALES 2601 2656 2458EBITDA 456 391 364NETPROFIT

269 226 220

D/E 0.3 0.3 0.4ROE 22.82 21.80 24.96

SHAREHOLDINGPATTERN

Dec‘15 Sep‘15 June‘15

Promoters 50.8 50.8 50.7FII/NRI 6.3 6.9 7.0FI/MF 13.0 13.6 13.4NONPRO 29.9 10.0 9.8PUBLIC&OTHERS

0.0 18.7 19.1

PORTER’SFIVEFORCES

THREATOFNEWENTRANTS-Lowtomoderate

• Hugecapitalrequiredtostart• Patentprotectionbycompaniesaddsgreatvaluetovariousproductsdevelopedbythem.• Varioussafetymeasurestofollowwhicharecostlyandtoughtoimplement• Theindustryasawholehavehighentrybarriers,complexproductsandprocesses,Manycomplex

productsaremanufacturedthroughR&Dandincludestoughprocesseswhicharehardtooperate• R&Dandpollutioncontrolprocessesneedgovernmentapprovalandsupport• Customerprocessandproductapprovalsystemarehighlyelongatedandtedious.Testingprocessto

finalapprovaltakes1-2years,thuscreatingstickycustomerbaseandwhichhelpinmaintainingstablemarginsandleadingtohighentrybarriers

THREATOFSUBSTITUTES-Low

• Buyersusuallyhaveaspecificchemicalrequirement.• Thusthereisnodirectsubstituteeventhoughit’sacommodity.• Also,specialtychemicalsprovide-

a) Valueadditionb) Productdifferentiation

COMPETITIVERIVALRY-High

• Chemicalindustryishighlyfragmented,cateringtovariousindustriesandcommoditizedproducts• Governmenthasallowed100%FDIinthissector,sonowtheyhavetocompetewithbothdomestic

andinternationalplayers.• ThereisathreatofthesecompaniesdumpingtheirproductsinIndiaatlowprices,reducingthe

demandfordomesticplayers.• MoreoverChinabeingtheleaderintheindustrycausesmajordisruptioninpricesanddemands

fromtimetotime.

BARGAININGPOWEROFSUPPLIERS-High

• Crudeisthemajorrawmaterialhere.• Itissuppliedmainlybyfewlargepetrochemicalplants.• Suppliershavehighbargainingpowergiventhefragmentedplayersinchemicalindustry.• Also,thereisnomajorsubstitutepresentfortherawmaterials.

BARGAININGPOWEROFBUYERS-High

• Sincethechemicalindustryisfragmented,thebuyershavealotofsuppliers.• Chemicalcommodityproductsarenotdifferentiated,thusgivingbigbuyersanupperhandat

negotiations.• Also,thesechemicalcompaniesaresometimesboundbylongtermcontractssotheyhaveveryless

chanceofmovingtoamoreprofitablesource.• However,somespecialtychemicalshavesomepricingpowerandsupplytonicheindustries,inthat.

LikevinatiorganicssuppliesATBSandisabletomaintainitspricing.

MajorProducts

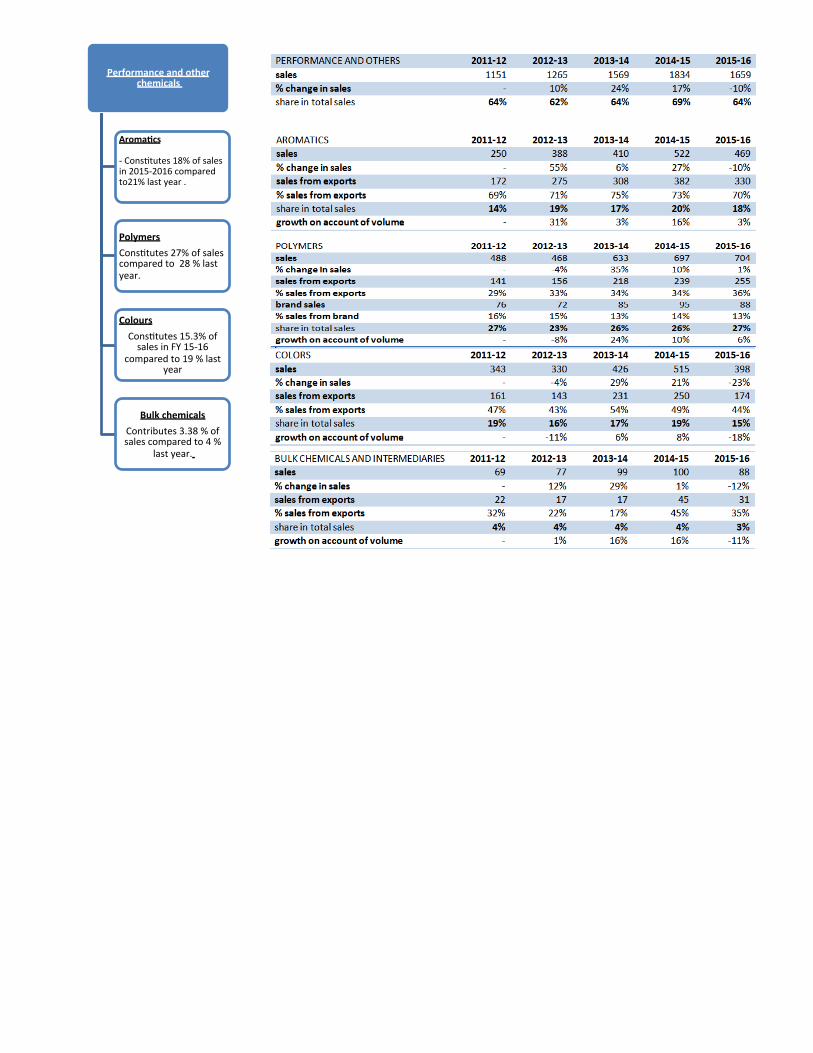

1. Aromatics:ThesizeofworldfragranceindustryisestimatedatUS$11bnandisgrowingatabout14%.ThoughearliertheproductusedtobemanufacturedonlyinUKandUSA,ChinaandIndiaarenowthemajorsuppliersoftheproduct.Themainuserindustries,namely –fragrance andpersonal care are growingwell becauseof improvingstandardofliving.KeyProductsp-cresolandderivativesmarkets:Atulisthelargestmanufacturerp-Cresolanditsderivativesincludingp-anisicaldehyde(p-AA)andP-anisolalcohol(p-AAI)intheworld.Exportsrevenuecontributestoover70%oftotalaromaticsales.Marketofpcresolisestimatedat63,000mtandisgrowingabout2%.PricingPowerThecompanyhoweverhasverylowpricingpowerasitisheavilydependentonoil.In2015-16,growthonaccountofvolumewas3%butthetotalsalesdeclineby10%total.ProjectsThe company completed 1 project under this head and has undertaken 1projectforimplementation.

2. PolymersandtheirbrandsWorldmarketforEpoxyResinsandHardenersisestimatedatUS$6.3bnandisgrowingatabout2%andIndianmarketisestimatedatUS$250mnandisgrowingatabout6%.WorldmarketforSulphones(ahardener)isestimatedatUS$320mnandisgrowingatabout4%.Theuserindustries,Construction,Defence,ElectricalandElectronics,PaintandCoatingsandWindEnergyaregrowingwell,particularlyinIndia.AtulisthelargestmanufacturerofsulphonesinworldandlargestmanufacturerofepoxyinIndia.ItalsohasanumberofBrandsunderthissegmentgivingitproductdifferentiationopportunitiesandbrandrecognition.Themajorproductof this segment runsunder thebrandnameofLapoxandPolygrip.

PricingPowerGrowth on account of volume was 6%, however the total increase in salesamounted to just 1%, which indicates the company’s low pricing power,thoughitisnotaslowasaromatics,showingbettermarginopportunitieshere.ProjectsThecompanycompleted3projectsunderthissegmentandundertook2moreprojectsforimplementation.

3. Cropprotection

Atulisamongtheworld'sfiveleadingmanufacturersof2,4dderivativesusedinherbicides.Ithascapacityof10,000tn.However,itlacksbargainingpower.TheindustryisestimatedatUS$52bnandisgrowingatabout4%.

Pricingpower

Thecompanyhoweverhaslowpricingpowerasthegrowthinvolumeis34%,butthetotalsaleshasincreasedby22%,showingthatthecompanyhadtoreducepricestomatchcompetitionandboostsales.

Projects

Thecompanycompleted3projectsunderthisheadandhasundertook1anotherforimplementation.Thecompanyisalsodeepeningitpresenceinothercountries,especiallyinAfricaandSouthAmerica.

4. Colours

AtulisthelargestmanufacturerofsulphurblackinIndiaandoneofthelargestmanufacturersofvatdyesintheworld.

ThesizeofworldDyestuffindustryisestimatedatUS$6bnandisgrowingatabout3.5%.WorldmarketforhighperformancepigmentsisestimatedatUS$4.3bnandisgrowingatabout2.7%.

Thisgroupcompromisesofaround550products.Green1,PRedandSulpharBlackaresomeofthekeyproducts.

PricingPower

Thecompanyhaslowpricingpowerbecausethecompanyfaceddecreaseinsaleof23%whereasdecreaseinvolumewas18%,showingareductioninprices.

ProjectsTheCompanycompleted4projectsandundertook2projectsforimplementationthisyear.

5. Pharma

ThesizeofworldAPIindustryisestimatedatUS$150bnandisgrowingatabout7%..

Thecompanyfaceddegrowthonaccountofvolumeof1%.

AtulBioscienceLtd,a100%subsidiaryofthecompanyfocusedonproductionofadvancedAPIintermediates,increaseditssalesby17%,from47to55crprimarilybecauseofvolumes.

PricingPower

Totalsalesdecreasedby1%.Degrowthonaccountofvolumewas1%.Thisindicatesthatthatpharmasegmenthassomeamountofpricingpowerandatleastmuchbetterthanothersegments.Breakthroughsinthissectorcancontributetomajorrevenuesinfuture.

Projects

ThecompanyhassuccessfullycompleteditssecuredUSFAinspectionforoneofitsproductsandisintheprocessofexpandingitsAPIplant.

Thecompanyundertook1projectforimplementation.

BusinessModel

AtulLtdconsistsof2segments:

i. LifeSciencesii. Performanceandotherchemicals

-

LifeScience

CropProtecjon-Consjtutes16%ofsalesinFY15-16comparedto14%lastyear.-Herbicidesegmentandformulajonssuchas2and4daremajorvariantsofcropprotecjon.

Pharma-Consjtutes12.6%ofsalesinFY15-16comparedto13%lastyear.-Itconsjtutesabout50productsincludinganjdepressants,anj–diabejc,anj-infecjve.

Performanceandotherchemicals

Aromafcs-Consjtutes18%ofsalesin2015-2016comparedto21%lastyear.

PolymersConsjtutes27%ofsalescomparedto28%lastyear.

ColoursConsjtutes15.3%ofsalesinFY15-16

comparedto19%lastyear

BulkchemicalsContributes3.38%ofsalescomparedto4%

lastyear.

FinancialPerformance

CapitalStructure

• Longtermdebt:hasbeendecreasingfrom2010andhascomedownto5%levelsofsalesfrom33%levelsofsales10yearsback.

• Shorttermdebts:havebeenincreasingconsiderably,theyarestilllowenoughtokeepthedebt/equityratioatonly0.3.ShorttermborrowingshavebeenIncreasingduetolowinventoryturnoverandthushighworkingcapitalrequirementsofthebusinessoveraperiodoftimeduetoincreasinglevelofsalesandWorkingcapitalneeds.weseefromthetableshorttermdebtas%ofsaleshasbeenfluctuatingbetween7%-10%,apartfrom2yearswhereworkingcapitalneedswerelessandthusnoworkingcapitalshorttermloanwastakenbythecompany.Moreoveritcanalsobeseen%ofshorttermloantoworkingcapitalisprettyinalmostalltheyears,indicatingthathighdemandofworkingcapitalanditsvolatilityaffectsshorttermdebt.

• Interestcoverageratio(EBIT/Interestcost):itisprettyhigh,showingCo.ismorethancapableofmeetingthem.Also,nocapitalizedinterestcostispresentinthebalancesheetofthecompany.

• Thecompanyrightnowis• expandingbyusingitsownearnings,itsCFO.• Ifthecompanyeverneedsdebttoexpandorrecoverfromsloweconomiccycles,theystillwill

haveadebtcapacityof1118cr.• Calculationssupportingtheabovementioned:

o Bank’susualinterestcoverageof3.DividingitbyEBITof428cro Givesaninterestexpenseof143cro Atul’scurrentloancostfromIndianbanks=6.99%to7.49%o Beingconservative,eventakingdebtcostas12%,thecompany’sdebtcapacityof1,118

cro Atulwithit’sconsistentprofitscanmanagetopaythisoff.

ReturnRatios

1.ROIC which measures efficiency of operatingassets (say core business quality) has been on theup consistently barring this year. We see a slightdeclineduetoincreaseinnetblockandcapitalWIPduetoCAPEXundertaken,butoverallthenumberisprettydecentat32.

2. ROE has also increased over the years to areasonably good level of 22.82 and importantlygrowth has not come from leverage effect butthrough consistently increasing net profit marginsand stable asset turnover. Also, some amount ofdebt is slightly beneficial as it is gives boost toequityholders returnandat thesametime isverymuchmanageable in case of fall in revenues to ahighextent.

3. ROA is increasing similar to ROE as it does nothaveahighpercentageofdebt.

4.ROIIC- In FY2008-2009 and 09-10 have seen bigreductioninoperatingcapemployed,thisisduetothe freeing up ofworking capitalwhich in turn isbecauseofdecreaseindebtorsin08-09anddrasticincrease in payables and short term borrowings in09-10. Despite reduced working capital, EBIT hasincreasedorremainedstable.

The ROIIC figure has shown a strong increasingtrend from FY12-13 to FY 14-15 suggesting evenfurther the efficient use of allocated incrementalcapital.ThiswasduetoincreasingsalesintheFY13-14 and in FY14-15 due to freeing up of workingcapital toa largeextentwhichwasbecauseof theincrease in creditors and short term borrowings.TheFY15-16thefigurehasgonedownduetoheavyCAPEXwhichhasbeenundertaken,otherwiseinthelast5yearsthecompanyhasseenhealthyreturnonincrementalinvestedcapital..

The RoIIC figures have been a bit volatile as thecompany’sbusiness isdependentoneconomyandconsumerdemand,making itcyclical, thusworkingcapitaldemands fluctuateasper thecyclicalneedsofthebusiness.

GrowthPercentages

Atulltd.hasshownconsistentYOYgrowthinnetsales.

ThemajorgrowthsinFY10-11majorlyduetonegativegrowthinpreviousyearwhichgivesitsmallerbaseandFY13-14dueglobalupturnindemands.

Thisyearhasseendegrowthafteralongtimemajorlyduetotworeasons:

1) Lowercrudepricesandunabletoretainduetocommoditynatureofproducts2) Globaleconomicdownturnandthuslowerdemand,sounabletoincreasevolumeto

offsetthedecreaseinprice.

ThoughthesaleshavedecreasedthisyeartheEBITDAandEBITgrowthhaveseenimprovementfrompreviousyear.ThoughitshouldbeseenthatthebaseofpreviousyearwascomparativelylowandthegrowthisstilllessFY12-13andFY13-14levels.Overallitstillshowsimprovingoperatingefficiency.NetprofitmarginshaveimprovedduetoreducingpercentageofLongtermdebtincomparisontosales.

HighnetprofitgrowthisvisibleinFY13-14andFY10-11duetosignificantincreaseinsales,EBITDAandEBITmarginswhichhavetrickleddowntoPAT.

MoreoverifwetakeAverageofEBITmarginsoveraperiodof5yearseachinthelast10yearswegetanaverageof5.62%fromtheperiodFY06-07toFY10-11andAveragemarginfromFY11-12toFY15-16standsat11.52%,Thehighermarginsaremorlyduetothelast3yearsofindicatingimprovedefficiencyaswellasmajorimpactofreductiononrawmaterialprices(ofwhichsomebenefitswereretained).Buthowlongwillthehighmarginsbesustainabledependsonthecrudeoilpricesandfurtherefficiencieswhicharelimited.ThusanaverageEBITmarginoflast10yearsof8.5%isanumberwhichshouldbegivenmoreweightageto.

SalesandoperatingPerformance

Itcanbeseenfromabovenumbersthatalltheprofitabilitymarginshavebeencontinuouslyandconsistentlyincreasing.WhileagoodincreaseinGrossProfitmargininFY15-16canbeattributedtolowpricesofcrude,thisisthemajorrawmaterialforthecompany.HoweverconsistentimprovementsinEBITmarginsreachingalmost15%thisyearshowsimprovingoperatingefficienciesandbettercostmanagementinalmostallareasofexpenditure.Netprofitmarginimprovementismajorlyduetodecreasinglongtermdebtovertheyearswhichhasgonedownconsiderablyduringthisperiod.

The,assetturnoverhasbeenmarginallyincreasingexceptFY15-16(whichwasdownduetolowersales)despiteofconsistentCAPEX.Despitetheincrementitisstillbetweentherangesof1.3to1.45inthelast5years,whichshowscapitalintensivenatureofthebusiness.

NetFixedAssetturnoverhaveshowngoodjumpinFY10-11andhavebeenincreasingsincethen,exceptthisfinancialyear(againduetolowsalesandrelativelyhighCAPEX),whichshowstheCo.HasbeenabletoboostuprevenuewithoutdoingalargeamountofCAPEXconsistently.AscanalsobeseenbyCAPEX/salesratiowhichhasbeenconsistentintherangeof5%-7%untilFY14-15.After10yearsthatisthisyearCAPEXhasalmostdoubledto14%asexpansionprojectsworth213cr.havebeencompletedandRs98cr.morehavebeenundertakentoboostupgrowthinexistingproducts.

Comingtoworkingcapitalmanagementasitcanbeseencashconversioncyclehasdeterioratedsincelast5years,whilethisincreaseisaconsequenteffectofincreaseinsales

levelfromFY11-12,itshouldalsobenotedthatbettermanagementofinventoryisneeded.DebtorturnoverdayshavebeendecreasingandthenconsistentsinceFY11-12andwellabovethedaysofpayables,thoughhavedecreasedbymajornumberssinceFY11-12.ThemajorareasofWorkingcapitalmanagementforAtulltd.Comesininventorymanagementwhichhasseenconsistenthighnumberofconversiondaysandhavesignificantlydeterioratedto117inFY15-16from107inpreviousyearandthusareamajorholdupintheimprovementofcashconversioncycleaswellasforfreeingupcashflow.

Toaddtoit,itshouldalsobenotedthatWorkingcapitalmanagementandspeciallyinventoryturnoverisprettylowforthewholespecialtychemicalindustry.ForreferenceifweseetheinventoryturnoverdaysofitspeerArtiltd.Italsocomescloseto110days.Buteventhoughmajorlybeinganindustryproblem,Atulltd.certainlyneedstobetteritsinventorymanagementforloweringshorttermborrowingcostsandfreeingupmorecash.

Atul’sbusinessmodelhasbeenabletoconvertprofitstocashascanbeseenbycomparingcumulativeCFO(cCFO)oflast10yearswithcumulativePAT(cPAT)oflast10years,withcCFObeing1586crandcPATbeing1168cr,indicatinghealthyconversionofprofitstocashoveralongperiod.

MoreoveritsCFO/EBITDAratiohas10yearaverageof0.8whichshowsahealthyconvergencebetweenprofitsandcashflowswiththedifferencemainlyduetoworkingcapitalchanges.

CFOhaveshownsignificantincrementfromFY13-14duetobetterprofits,thoughworkingcapitalmanagementhasbeenfluctuatingbetweenbadandgoodintheseyearsasWCchangeinFY13-14was-155crandhasimprovedinFY15-16to17cr.Withbetteringprofits,bettermanagementofworkingcapitalspeciallyinventorywouldfurtherboostupCFO.

AlltheseyearsCAPEXhasbeenself-fundedandtotheextentthattheyhavebeencoveredbyCFOitselfexceptthe2years,sofreecashflowsituationismostlypositiveandhealthybarring2years.ThusthisshowsAtulltd.canexpandevenfurtherwithouttheneedofanydebt.

Ø PROFITMARGINS:themarginforlifescienceshasbeenstableataround20%andperformancehasamarginofaround13%.

Ø SALES/ASSETS:thisratioforlifescienceshasdroppeddownby6%whereasforperformance,ithasdrasticallydroppedby22%.Thisindicatesthatperformancesegmentisonadeclineinabletoconvertit’sasset’sefficiencyintosales.

Ø SALES/ADDITONALCAPEX:thisratioindicatesastohowwelltheadditionalCAPEXisabletogeneratesalesinthefutureyears.Lifesciencesisdoingadecentjobwithastablerateof25times.But,performancesegmenthasdroppeddownsignificantlyby10%inthecurrentyear.

Ø KEYPOINT:ifAtulltdisabletoaddafewspecialtyandvalueaddedproductsinlifesciences,itcangeneratehighersaleshere.Currently,performanceholdsabout70%ofthetotalsalesrightnow.Itcanallocatecapitalinabalancedwaybetweenthe2sectors,itcanseeanincreaseinthevolumeandtotalsalesfigureaswell.Alsoifitcancreatemorespecialityandkeyproductsinlifesciences,thenitcouldfurtherboostupsalesduetobettermarginsinthatsector.

Ø OTHERSECTOR:thissectorincludesproductsthatarenotrelatedtothemajorproducts.Thefuturesalesfigurewillgiveusabetteroutlookonthissector.Also,thissectoraccountsforaveryminusclepercentageoftotalsalessoitisnotgoingtoaffectthegrowthsignificantly.

SegmentalPerformance

ManagementQuality

• Thecompanyhasnosignificantrelatedpartytransactions,noranyhugeamountshavebeenlenttoanyexecutiveoranyorganization,anexecutivemayberelatedwith.

• ThepromoterorhisfamilyareisnotrelatedtoasimilarbusinessoutsideAtulLtd.• Allthepatentsareunderthecompany’snameandeverythingisbeingprofessionally

run.• Thecapitalallocationforthecompanyhasbeendoneefficiently.• Thepromoterishighlyeducated,qualified,leadsasimplelifestyleandhasaclean

record.• Thepromoterwithdrawsatotalsalarywhichis240.06timesthemedian

remunerationoftheemployees;thistotalamounthoweverisnotmorethan4%PAT.• Themanagementiscompetentandhasbeencandidaboutitsmistakesand

performances.• Thepromotershareholdinghasafavourablenumberandtherehasbeennopledging

orissueofwarrants.• Thetopmanagementisquitestableandtheelectionofrevolvingdirectorsisbeing

carriedoutintime.• Therehasbeennodecisiontakenagainsttheminorityshareholders.

AdditionalPoints

1)Hedging:Atulltd.hedgedaround3.5crofforeignexposureinFY2015-2016andhasaround4.62cr.ofexposureunhedged.Regardingthehedgingofitsrawmaterials,asthepricesareveryvolatiletheCompanydoesnotgoforcommoditypriceriskhedgingactivitiesasitdoesnotexpectsignificantadvantageinmediumtolong-termhorizon.However,forminimisingprocurementriskforshortduration,itentersintoannualpurchasecontractsforkeyrawmaterialslinkedtoinputcosts2)Cyclicnatureofbusiness:Beingaproviderofindustrialproductswhichareenablersforotherindustries,thedemandforthechemicals,especiallyspecialitychemicalsthatcontributestoAtulLtd’smajorrevenuesaredependentondemandoftheendconsumerproductslikefragrances,paints,tyresetc.Thusbeingdrivenbyconsumerspendingandpurchasingpower,thecompanyfacescyclesofmedium,highgrowthandnegativegrowth.Moreovertheinputbeingacommodity(oil)alsohasamajorimpactoncompany’stotalsales,astrendoftotalsaleschangeswithchangesinthetrendofoil.(negativegrowthinsalesduetolowcrudeprices)Alsoasobservedfromthesalesfiguresabove,ina4-5yearcycle,thecompanyshows2-3yearsofmediumgrowth,followedby1-2yearsofgreatgrowthandthenayearofdegrowth.

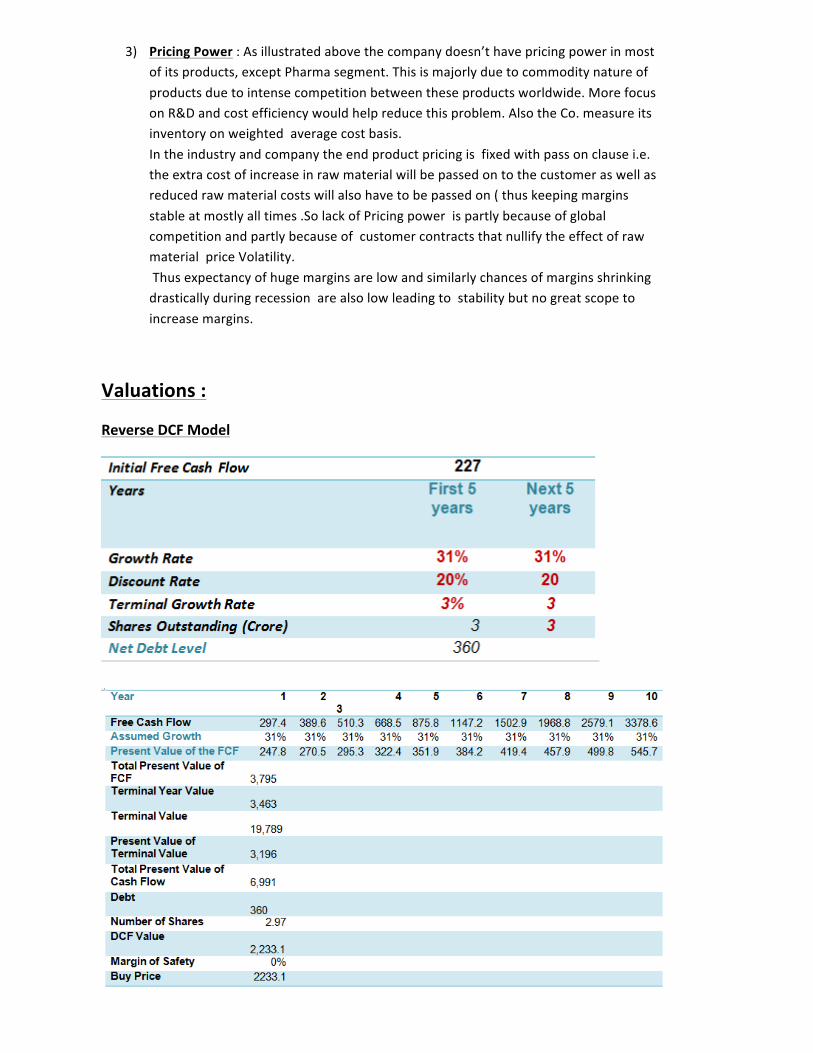

3) PricingPower:Asillustratedabovethecompanydoesn’thavepricingpowerinmostofitsproducts,exceptPharmasegment.Thisismajorlyduetocommoditynatureofproductsduetointensecompetitionbetweentheseproductsworldwide.MorefocusonR&Dandcostefficiencywouldhelpreducethisproblem.AlsotheCo.measureitsinventoryonweightedaveragecostbasis.Intheindustryandcompanytheendproductpricingisfixedwithpassonclausei.e.theextracostofincreaseinrawmaterialwillbepassedontothecustomeraswellasreducedrawmaterialcostswillalsohavetobepassedon(thuskeepingmarginsstableatmostlyalltimes.SolackofPricingpowerispartlybecauseofglobalcompetitionandpartlybecauseofcustomercontractsthatnullifytheeffectofrawmaterialpriceVolatility.Thusexpectancyofhugemarginsarelowandsimilarlychancesofmarginsshrinkingdrasticallyduringrecessionarealsolowleadingtostabilitybutnogreatscopetoincreasemargins.

Valuations:

ReverseDCFModel

Usinga31%growthrateforthenext10years,weseetheintrinsicvaluedrawclosetothecurrentmarketprice.Thisonlyshowshowthemarkethasaccordedanirrationallyhighgrowthtothecompany.Reviewingthemarket,thisindustryandcompanyinparticularwillwitnessdecentgrowthincoming2-3yearsbutahighgrowthrateof31%isbiasedtosomeextent.Asofnow,wewouldn’tenterthecompanybutwhenthemarkethasbrokenthisvalueandsubsequentlydrawsdownthepriceshowcasingagrowthbelow15-16%,thenthatwouldbeagoodtimetoenterthecompanyasthenitwouldprovidegoodreturnsalongwithmaintainingmarginofsafety.

ExitMultipleApproach

ThisapproachtakesintoP/Eof20,withanassumptionthatattheendof10yearsP/Eofcompanywillbearound20,thusifP/Ereratesdownfromcurrentlevelstoaround20,withaprojectedEPSandwithourexpectedgrowthof18%innext5yearsand12%forfurther5years,thenitwillvaluethecompanyatapprox.Rs7314after10years.

Giving13%CAGRfromthispricepointwhichisbelowourdesiredreturnof20%.Thuswewouldwaitforthemarkettocorrectpricestoattainaminimumofthatreturnontheinvestment,consideringthebusinesscyclicalityrisk.

BRIEFOUTLOOK:

GENERALOVERVIEW

• Atulltdmajorsincommoditymarketwhichhappenstobecyclicalinnature.So,itiscloselylinkedtotheeconomiccycle.Supportingtheabove,itisatabusinessendwhereanymotionintheotherendwillcauseturmoilinthiscompany.

• Thecompanyhaslowersalesfigureinthecurrentyearwhichisduetodecreaseininputpriceswhichithadtopassonduetolackofpricingpower.Also,theincreaseinvolumewasnotenoughtocanceltheeffect.(volumegrowththisyearwas3%ascomparedto5%oflastyear).

• Thecrudeoilpriceshavegonedownbutitdoesnotshowasustainableapproachtoconsideritfortheforecast.

• Theoperatingefficiencyseemsgoodasthemanagementwasabletoachieveahigherprofitmarginevenafterhavingadecreaseinsalesfigure.Tellsusthatthecompanyisgoodatcostcuttingbutwhichagainisnotsustainableforthelongterm.

• Thereisnomanipulationbythemanagementandinrelatedpartytransactions.• Theindustryasawholehavehighentrybarriers,complexproductsandprocesses,stable

returnsandmargins,lowdebt.Specialitychemicalsarehighvalue–lowvolumeproducts.(willgoinportersrule)

• Itisaknowledgebasedindustry,needspecializedknowledgeableprocess,establishedindustriesbetterpositionedtotakeadvantageofgrowthinincountrydemandandofexports.

• Customerprocessandproductapprovalsystemarehighlyelongated,tedious.Thusstickycustomerbaseandthushelpinmaintainingstablemargins.Testingprocesstofinalapprovaltakes1-2years,thussticky.Leadingtohighentrybarriers.(porter’srule)

• Supplementingtheabovewithvaluation,theCMPofAtulltdisR.2,120.Butaspervaluationthemarketiscurrentlygivingitgreatgrowthwhichinourviewisoverestimatedandthusthestockseemsovervalued.Asthegrowthpredictedbyusinthenext4-5yearsismaximumaround18%andbeyondthatatalevelofabout12%foranother5years

TREND(previous2-5years):

• Indianspecialitychemicalshavegrownat13%CAGRfrom2009-2014.Thegrowthinlast2yearshavebeenrelativelydownduetolowoilpricesandlackofglobaldemandtoo.

• Butinthelast3-4yearsIndianchemicalindustryhasbeengainingadvantageoverchina,whichisamajorcompetitor.Chinawasandstilltoalargeextentisfacingcostpressureduetohighcostsoflabour,fuel,power,andmostimportantlystricterenvironmentalregulations(2majorchemicalfactoriesofatwodifferentbigchemicalcompanieshavebeenrelocatedinrecentyears).Alsoappreciatingyuanhadbeendampeningtheirexportsduringthattime.

• Moreover , according to industry experts, the cost of production of India’s specialty chemicals works out to 10-15% lower than that in China after China’s investment in environmental protection

• WhetherthisadvantagewillsustainforlongfromthecurrenttimedependsonthegrowthofChineseeconomy,theirpoliciesregardingenvironmentandcurrency

devaluation.Thusitisdifficulttopredicthowlongwillsuchadvantageprevail,unlessIndiancompaniesbecomehugelycostefficientduringtheperiod.

• CurrencydepreciationaidedrevenuegrowthinFY13• CAPEXincreasedgraduallyfrom11-12TO14-15andzoomedin15-16forAtulLtd.and

itspeers–AartiLtd.andVinatiOrganics.• AllCAPEXhasbeendonethroughinternalsourcesi.e.surplusoftheyearsandthusdebthas

beenatconsistentlevelsforAtulLtd.,thusbringingdownD/Eataround0.3(surplushavebeenincreasingandaccumulatingduringtheperiod)

KeyGrowthDrivers:

• Indianspecialitychemicalsectorhasgrown13%inthelast5yearsandisexpectedtogrowat17%CAGRover2014-2015to2019-2020,duetohigherexports,strongerconsumermarketsinindiaandgainingcompetitiveadvantageoverchinaasperEmkayglobal’sreportonIndianSpecialitychemicalsectorpublishedinJune,2014.But,uptillnowthegrowthinthesegmenthasbeenmuchbelowthepredictedlevels,duetolowerpricesofcrudeandlowglobaldemands,thusthefigureneedstoberevisedasthegrowthhasbeendowntojust8%inFY14-15and-2%inFY15-16

• AlsoIndia'sshareinglobalspecialtychemicalindustryisestimatedtogrowfromabout2.8percentin2013to6-7percentin2023withmarketsizeintherangeof$80-100billion.ThusgrowthopportunitiesareprevalentforAtulLtd.inthenearfuture.

• Specialitychemicalsconsistof22%oftotalchemicalintheworld.ThisisexpectedtoincreasewithgreaterexportpenetrationbyIndianCompaniesandweakeningglobalcompetitioninshapeofChina.RightnowSpecialitychemicalsinindiaoccupyverysmallproportionofchemicalsascomparedtoglobalaverageandasqualityoflifeandstandardoflivingimproves,theirdemandwillincreasetoo.InthisaspectIndiamarketpresentsgreatgrowthpotentialduegrowingeconomy,increaseInconsumptionrate,improvingstandardsoflivinginthecountry,aidingitsdemand.ThiscouldbeachievedthroughincreasingapplicationsthroughR&Dandenhancingtheknowledgeofendconsumers.ThekeydriversforpickupinthepercapitaconsumptionareriseinGDPandpurchasingpowerwhichgenerateshugegrowthpotentialforthedomesticmarket,low-costmanufacturing,afocusonnewsegmentssuchasspecialty&knowledgechemicalsandWorld-classengineeringandstrongR&Dcapabilities.

• Govt.Initiativeslike100%FDIhasbeenallowed• Another advantage is India has better IPR laws than china, thus better protection and

promotion to R&D• Chemical sector to be major beneficiary of upcoming Smart Cities • On a macro-level, there are fivebroad critical elements of any Smart City - water

management systems, infrastructure,transportation and energy , all of which require large amount of speciality chemicals.

• Visible growth in user industries and brands, cushions polymer businessPolymers is Atul’s flagship segment with ~27. Polymer business is largely domestic market oriented and accounts for ~65% of total sales. SO for polymers domestic market is key, in which signs are positive as Indian economy and consumer spending are on up, so this is a segment which can see decent growth, also more penetration in exports will give good

performance though it lacks bargaining power, a10% CAGR for next 2 years can be expected in it.

• Aromatics being a key segment for Atul, is seen to bring value due to its leadership in p-cresol and derivatives.However, the recent economic slowdown impacted volumes while prices softened due to lower crude. Still, considering a likely gradual pick up in user industries (dyestuff, flavours & fragrance, pharma, personal care), a 10% CAGR for Atul’s aromatic sales over FY16�18 (of which over 80% is led by P�cresol)

MajorRisks&Downsides

• Intheindustryandcompanytheendproductpricingisdecidedwithpassonclausei.e.theextracostofincreaseinrawmaterialwillbepassedontothecustomeraswellasreducedrawmaterialcostswillalsohavetobepassedon(thuskeepingmarginsstableatmostlyalltimes).SolowPricingpowerispartlybecauseofglobalcompetitionandpartlybecauseofcustomercontractsthatnullifytheeffectofrawmaterialpriceVolatility.

• Thusexpectancyofhugemarginsarelowandsimilarlychancesofmarginsshrinkingdrasticallyduringrecessionarealsolowleadingtostabilitybutnogreatscopetoincreasemargins.

• Nomajorstructuralchangeisaworry,speciallyinglobalscenario,whilethepositiveisthattheincountrydemandmightrise,china’scompetitionandinabilitytolowercosttolowlevelspertainstheriskofdeclineinexports.

• AtulLtd.hasconsistentlybeenmakingitsoperationsmoreefficientthushavingabenefitsofoperatingleverage.Butlargescalefurtheroperatingleverageisunlikelyinnearfuture,saleswillbekeysourceofbottomlinegrowth.

• ColorsisanintegratedoperationforAtul,withleadingpositioninsulphurblackinIndiaandvatdyesintheworld.Thisdivisionsawhealthy25%CAGRinFY13-15primarilyledbyspikeinthepricesofdyesanddyeintermediatesandajumpintheexportvolumes.However,overalldyepriceshavesoftenedabitinFY16;simultaneously,exportsdemandforvatdyes(aleadingproductforAtul)seemstohavecorrectedmeaningfully,ledbyglobalslowdown,makingtheoutlookbleak.Indianexportofvatdyesfell~35%overthelast12months(verymuchdependentonglobalpricesandglobaldemands)

• Diversificationisstagnatinggrowthhere,assomesectorsareonupandcolorsandaromaticsareseeingdowntrend

• SpecialitychemicalsegmentandAtul’sgrowthwhichhadreallypickedupintheyears11-12to13-14,havereallydampenedinthelast2financialyears

• Theindustrybeingdependentuponthedemandofendproductsandcrudeoilbeingamajorrawmaterial,facescyclicalitywhichtranslatestofluctuatingrevenuegrowth

PeerAnalysis(AARTIINDUSTRIES)

Asageneralreview,AartiLtd’sfinancialsintherecent4yearsascomparedtoAtulLtd.showanequivalentlevelsofsales,withAartihavingslightlymoreatarounf2900crlevelsforFY2014-2015against2650cr.ofAtul’s.ThegrowthinsaleswerebetterinAartiLtdintheyearsascomparedtoAtul’ssalesgrowthofaround13%,20%and8%.YOYgrowthinEBIT,PAThasalsobeenbetterinAarti,partlybecauseofbettergrowthinSales.

Whenitcomestomargins,AtulLtd’smarginsaremuchbettertoAarti’sinallaspectsinthelast2years.WhileAartiLtd’smarginshavebeenconsistent,AtulLtd’shavebeenconsistentlyonanupwardstrendandhavebetteredAaarti’sinthelast2years,showingimprovingefficiencies.

Workingcapitalcycleofboththesecompanieshavelongcashconversioncyclesduetolowinventoryturnover.Thisismajorlyduetothetypeofindustrytheyoperatein.EventhenAtul’scashconversioncyclerangesbetween90-97days,whileAarti’shavebeensignificantlymore,showingpoormanagementinAtul’scomparision.

TheperformanceratiosshowsapicturewhereROEisalmostsameforboththecompanies,butthemajordifferenceisthatROEofAartiLtd.IsboostedbyhigherleverageascomparedtoAtul’swhichwaspredominantlyhigherduetomarginsandassetturnover.ThisisfurtherbackedbyROA,whichshowsabetterpictureinAtulltdinrecentyears.

Thus,eventhoughwithbettergrowththanAtul,AartiLtd.isnottobetteritsoperatingefficienciesasshownbylowerassetturnover,lowermargins,lowerinventoryturnoverandhigherlevelsofdebt.ThisshowsinthePATfiguresof(109,140,174,216)croresforAartiwhicharelowerthanAtul’sinthelast2years(95,128,220,226)croreseventhoughhavingabettersales,indicatingAtul’soperatingefficiencyimprovementwhichIslackinginAartiLtd.

Thusthoughthecompaniesarecloseinmanyaspects,themajordifferentiatingfactorswouldbe:1)Operatingefficiency2)Globaldemandoftheirkeyproductsbasedontheenduserdemandintheeconomyandconsumptionlevels.

Highlightsaboutthekeyproducts:

1. BENZENEBASEDINTERMEDIATESAARTIisamongstthelargestmanufacturerofBenzenebasedintermediatesinIndiawithproductsclassifiedintothefollowingcategories:

• CHLORINATIONofBenzeneintoMCB,ODCB,PDCB&TCB.AARTIpresentlyhasachlorinationcapacityof70,000tonsperannum-LargestinIndia.

• AMMONOLYSISofNitroChlorocompoundssuchasPNCB,ONCB.AARTIisthelargestmanufacturerofAminationproductsinIndiaandismakingvariousAminocompoundssuchasPNA,ONA,OCPNA,PCONA,etc.

2. SULPHURICACID&IT'SALLIEDPRODUCTS.AARTI'sSulphuricAcidplanthasacapacityof1,75,000tonsperannum.AARTIhasmostbackwardintegratedplantforDIMETHYLSULPHATE(thekeymethylatingagent)i.e.startingfromSulphur&Methanol.

3. ActivePharmaceuticalIngredient(API)-AARTImanufacturesvariousBulkPharmaceuticalsintherangeofAnti-asthma,Anti-hypertensive,Anticancer,CNS,DermatologyattheTarapurplant.TheplantisUSFDAapproved,EUGMPcertifiedbyTheGermanHealthAuthorityfromHamburgandalsohasAccreditationCertificateofForeignDrugManufacturerfromJapaneseHealthAuthorities.

4. BULKPHARMACEUTICALS:AARTIismakingvariousBulkPharmaceuticalsintherangeofAntidiarrhoeals,Antiinflammatory,Vitamins,Antiasthama,AntiHIV,Antijetlag/SleepDisorder,AceInhibitor,Antibiotics&Antidiabetics.

5. AGROCHEMICALS:ThesecompriseofQuinalphos&Carbendazim.

6. DYES:AARTIhasstartedgettingdyesmanufacturedoncontractbasisfromthelocalmanufacturersexclusivelyforexports.Theyareabletosupplychromiumfreedyesinpowder&liquidformforSwimmingPool&Spaapplications.Also,supplyliquiddyesinEcofriendlypackingofIBCTunner&powderinbiodegradablecorrugatedboxes.

Thus,thoughthespecialtychemicalscharacteristicofLowPricingpowerandCyclicityarepresentinboththecompanies,theproductsthattheyleadinaredifferentandusedfordifferentpurposes,thusmakingthemspecialty.Sointhelongtermwhichcompanyshowsasignificantbettergrowthoverotherisalittledifficulttosayasbothdependonconsumerspendingoftheirrespectiveproducts.Butitcanstillbesaidthatthegrowthinspecialtychemicalsaspredictedwillnotleadtoamassivedifferenceasbothhavesomenicheproductsthattheyareleadersin.

AARTIINDUSTRIESVALUATION

ThususingthereversedcfmodelforAarti,itisevidentthemarketisgivingitagrowthofabout30%forthenext10yearsandexpectingtoearn20%returnsfromthis,whichinourviewiscertainlyovervalued.AsAarti’sgrowthwillsomewherebearounfAtul’s,ratheralittleless,comparingtheproductprofile,managementefficiencyandhigherdebtonboththecompany’sbalancesheet.

Thoughbothofthesestocksareonthevergeofgrowthboostduetopredictedgrowthinspecialtychemicalsinthecomingyears,Atul’simprovingoperatingefficiencyandleadershipinvariousproductsgivesitabitofedgeoverAartiLtd.buttakingintothecyclicnatureofbusiness,ahighermarginofsafetyshouldbemaintainedaswellasbuyingshouldbedonewhenpricecorrectsitselftoagrowthrateofbelow13-14%.

Broaderpicture:

ViewingandanalyzingthecriticalaspectsofthespecialtychemicalindustryaswellasAtulLtd.,itcanseenthatthesectorasawholehascertainpotentialbenefitslikegrowingIndianEconomy,consumerdemandandimprovinglivingstandardsalongwithincreasingeffortstolowercostsbythecompany.Lowdebtsandgoodinternalaccrualsarealsoprettygoodsignsofstability.

Buttherevenuesbeingcyclicalduetoitbeingdependentonglobaldemandsandvolatileoilprices,diversificationcreatingtheneedformultiplefactorsinmultiplesegmentstogointhesamefavorabledirection,alongwithlowscopeofmarginexpansionduetoescalationandde-escalationclausesandwithnomajorstructuralchangeoracatalysttocreatethat,alongtermholdwouldnotbesuggestedbyusaswebelievelongtermreturnsofabout5-7yearswillbefluctuatingandwillnotgiveanyextraordinaryreturnsduetocyclicityandmutedgrowthduetodiversification.ThoughstablereturnscanbeexpectedasAtulhasbeenproducingthroughout,duetoefficientoperationsandgoodmanagementagreatoraboveaveragereturnsasexpectedfromlongtermholdingslookdifficult.Moreoverthecurrentvaluationsaresteepandthestockhasalreadygrownby128%inlast2years,discountingfuturegrowthwhichhasnottranslatedinthe2years.

Thusseeingalltheseaspectswerecommenda“SELL”asinourviewtherearelowchancesthatstockwouldgivethedesiredreturnoraconsiderableupsideonourminimumrequiredreturnforthelongterm(i.e.atleast20-25%returnsforalongtermonaconsistentbasis)

KeyTrackables–

• Structuralchangeindicatorslike,hugedomesticdemand,considerableincreaseinlivingstandardsofpeopleinIndia,gainingsustainableadvantageoverChinaandshiftofproductiondemandfromcountireslikeChinaandJapantoIndia

• AmountofCAPEXdonebycompanyandinwhichsegments.Potentiallyhighgrowthsegmentscanboostrevenue

• Aneyeonnewpatents,R&Defficienciesoraproductderivedwithgreatpotentialornewprocesseswhichcanbringgreaterefficienciesthancompetitors

• Growthinpaints,polymerandaromaticindustry,these3beingthebiggestcontributorsandnewadvancementsinPharmasegmentasithassomerelativepricingpower

• Directionincurrencymovements,continualdepreciationofcurrencyagainstdollarwouldbeverybeneficialforexports

• Acheckonmovementofoilpricesandanymajorchangesincontractswithsupplierswhichcouldleadtomajorchangeinmargins.

• Anymajorautomationofprocessestolowercosts,thatcanprovetobeabigdifferentiatorbetweenAtulanditscompetitorsworldwide.

Theabovereporton“AtulLtd.’’hasbeenpreparedby:

AkshaySahani,SrishtiAgarwal,SmitNaikandBansriJuneja

References&Sources:Annualreports,Emkayglobalfinancialservicesreport,PhilipCapitalreport,HDFCreportonIndianChemicalsector,Analystmeetpresentations