Download - The 2016 Contact Centre Benchmarking Report

accelerate your ambition

Dimension Data’s 2016 Global Contact Centre Benchmarking Report

21 June 2016

Asia Pacific summary

The Global Contact Centre

Benchmarking Report

Launched in 1997 by Merchants,

Dimension Data’s

subsidiary contact

centre specialist.

Annual global

research study of multichannel

interactions and

the contact centre

Supported by over 40of the world’s leading industry

groups and associations

19 yearsof trends, performance

analysis and best

practice techniques

6core review areasspanning CX strategy,

innovative technologies, and

best practice approaches on

phone and digital solutions

About the

2016 Report

6 chapters,

700+ data points,

80+ result charts

1320 companies from 81 countries

contributed to this year’s research.

388 participants from Asia Pacific (Inc ANZ)

Analysis with context

and recommendationson best practices

16 new questions

and existing

survey expanded

to include digital

25 country/regional

highlights summary

reports

5 vertical reports

Online portal and

bespoke reportbuilder via CX website

What’s included?

Customer Analyticscustomer segmentation

single view of customer

customer intelligence

service determinants

process re-engineering

internal SLAs

Contact centreoperationscustomer satisfaction

contact quality

management information

contact statistics

contact resolution

performance management

Workforce optimisationstaffing models

training

competency management

employee engagement

human resources

workforce management

Technology solutionstechnology trends

technology readiness

ownership

contact centre deployments

application functionality

service management

CX strategy and innovationcontact channels

centre maturity

market trends

financial positioning

location planning

strategic performance

innovation

Digital servicesself-service capability

self-service priorities

customer behaviours

contact statistics

process reviews

channel development

The Benchmarking Report provides a unique global

perspective on and the contact centre

We don’t just observe research results, we provide

context

Provides guidance toward best practice standards on

all aspects of CX and digital channel management

The big picture…

w e l i v e i n a w o r l d

d o m i n a t e d b y d i g i t a l

t e c h n o l o g i e s

accelerate your ambition 7

74,5

84,8

74,0

86,4

87,5

Reduction in contact volumes

Increased company revenue/profits

Increased employee engagement

Reduction in costs

Increased customer loyalty (incl. value)

Improved customer experience: benefits

What business benefits can your centre evidence as a result of an improving CX capability?

Customer loyalty

recognised as top

benefit of CX

85% can show increase

revenues/profits from

improved CX

accelerate your ambition 8

2,2

8,1

10,8

28,1

31,9

33,0

33,5

34,1

37,8

80,5

Other

Customer effort scores (ease of doing…

Transition to digital interactions

Complaint levels

Productivity and cost to serve (incl.…

Customer advocacy or loyalty (e.g. NPS*)

Employee engagement

Sales revenue and profits

First contact resolution (right first time)

Customer experience

Most important strategic performance measures

What are the top three most important strategic performance measurements according to your company’s board/executive team

*Net Promoter, NPS and Net Promoter Score are trademarks of Satmetrix Systems Inc., Bain & Company and Fred Reichheld

CX again top strategic

indicator of

performance

Focus on cost to serve

drops to 6th spot as

organisations buy into

benefits of CX

Much more than a contact centre

Telephone-premised CX Digital-premised CX

Contact2000s

Channel migration

for cost reduction

Broadening

channel access

1990s

CallReplacing

face-to-face

Provide improved

customer access

2010s

MultichannelPart of a

multiple channel experience

Supporting other channels

- not always first choice

Omnichannel2016 – 2018

Focused on resolving user

issues ‘in-channel’

Providing assisted support for

integrated digital channels

Digital analytics

Technology enablement

2016-2020s

Personalisation & proactive CX

accelerate your ambition 10

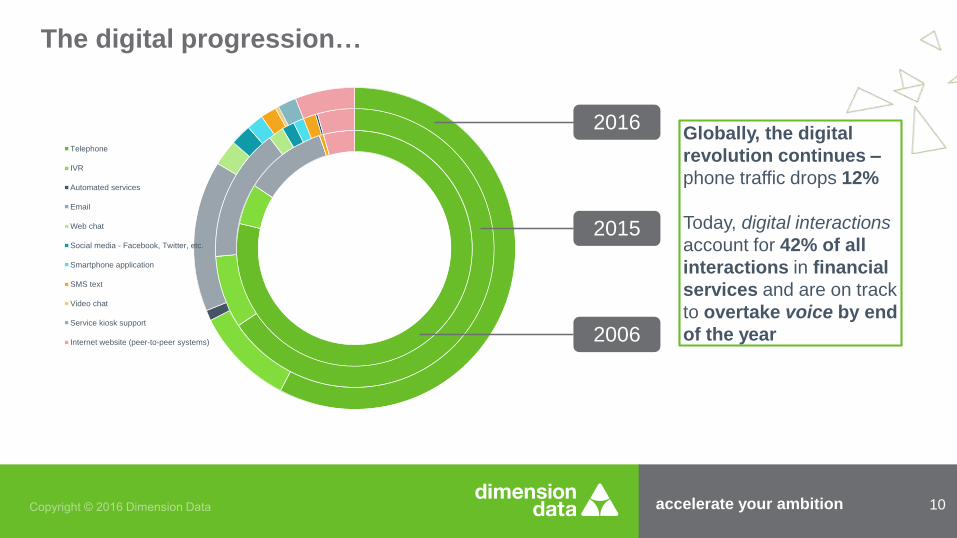

The digital progression…

Telephone

IVR

Automated services

Web chat

Social media - Facebook, Twitter, etc.

Smartphone application

SMS text

Video chat

Service kiosk support

Internet website (peer-to-peer systems) 2006

2015

2016Globally, the digital

revolution continues –

phone traffic drops 12%

Today, digital interactions

account for 42% of all

interactions in financial

services and are on track

to overtake voice by end

of the year

accelerate your ambition 11

Popularity of channel type by age group

Which contact channel is most popular with the following age groups?

Percentage of centres that do track channel popularity by age profile

% of N Under 25 yearsBetween 25 and

34 years

Between 35 and

54 years

Between 55 and

70 yearsOver 70 years

Social media 38.9 13.7 2.2 0.6 0.4

Mobile application 27.2 23.7 6.3 0.8 0.5

Email 12.2 26.8 32.7 8.8 0.8

Telephone 11.5 18.4 51.7 87.0 93.2

Web chat 9.4 16.5 6.3 1.1 0.3

Other 0.7 0.9 0.9 1.7 4.7

1st

2nd 3rd 4th

5th

6th

5th 5th6th

2nd 5th

3rd 1st 2nd 2nd 3rd

4th 3rd 1st 1st 1st

5th 4th 3rd 4th

6th 6th 6th 3rd 2nd

Mobile apps a top 3

choice for everyone

under 55

Social media top choice

for those under 25

Email preferred option for

those aged 25-34 years

accelerate your ambition 12

Contacts handled by channel

What’s the percentage split of interactions being handled across the channels offered to your customers?

2015 2016

Telephone 65.7 55.7

Email 15.5 14.3

IVR (touch-tone/speech) 8.4 14.2

Internet website (incl. knowledge portals, peer-to-peer systems

etc)4.3 4.6

Web chat (incl. instant messaging, co-browse) 1.8 1.7

Social media (Facebook, Twitter, etc.) 1.4 2.5

Service kiosk support (i.e. branch walk-ins) Not asked 2.0

Mobile applications (smartphone, tablets apps) 1.2 1.3

SMS text 1.5 2.3

Automated services (e.g. push messages, auto updates, etc) Not asked 0.7

Video chat 0.2 0.6

Phone contacts in

Asia Pac are already

amongst lowest

seen globally.

Phone has dropped

from 65.7% to 55.7%

in space of a year,

as digital revolution

picks up pace.

Digital split still

dominated by

traditional email and

IVR, but new

channel choices

growing

accelerate your ambition 13

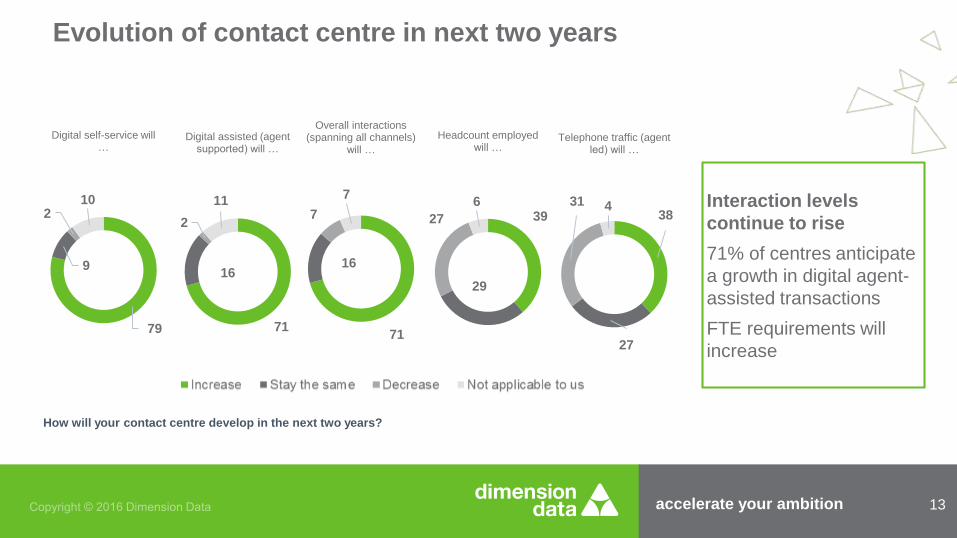

79

9

210

Digital self-service will …

Evolution of contact centre in next two years

How will your contact centre develop in the next two years?

71

16

2

11

Digital assisted (agent supported) will …

71

16

7

7

Overall interactions (spanning all channels)

will …

38

27

31 4

Telephone traffic (agent led) will …

39

29

27

6

Headcount employed will …

Interaction levels

continue to rise

71% of centres anticipate

a growth in digital agent-

assisted transactions

FTE requirements will

increase

accelerate your ambition 14

4,3

12,3

16,3

25

32,6

31,5

29,9

29,9

40,8

29,9

45,1

Other

Speed of change - can't keep up

Access to new technologies (incl.…

Security risks and compliance

Data analytics (incl. big data)

Interaction optimisation/automation

Commitment to customer…

Multiskilling/increased complexity

Changing user behaviours (mobile,…

Migrating traffic to digital

Omnichannel strategies (connected…

Industry trends affecting contact centre

What are the top three industry trends affecting your CX capability?

Connected

(omnichannel)

customer journeys

taking precedence

More so than migration of

traffic to alternative

channels

accelerate your ambition 15

5,5

16,6

77,9

14,9

61,9

23,2

Not integrated

Partially integrated

Fully integrated

Now Within 2 years

Omnichannel integration

Which of the following best describes the level of integration across your service channels?

Over 1/5 have

omnichannel capability

It’s on the horizon for

another 78%

Clear focus on achieving

full, not partial, integration

across channels

The challenge…

The digital revolution is being held back

- human touch is missing

User inputs to

technology

requirements low

Testing and

approvals scarce

Design

Consistent and

proven phone mgt

techniques not

applied to digital

Objectives not

aligned

Management

Responsibility and

focus to business

case objectives is

often missing

Silo approach to

channel mgt

Ownership

accelerate your ambition 18

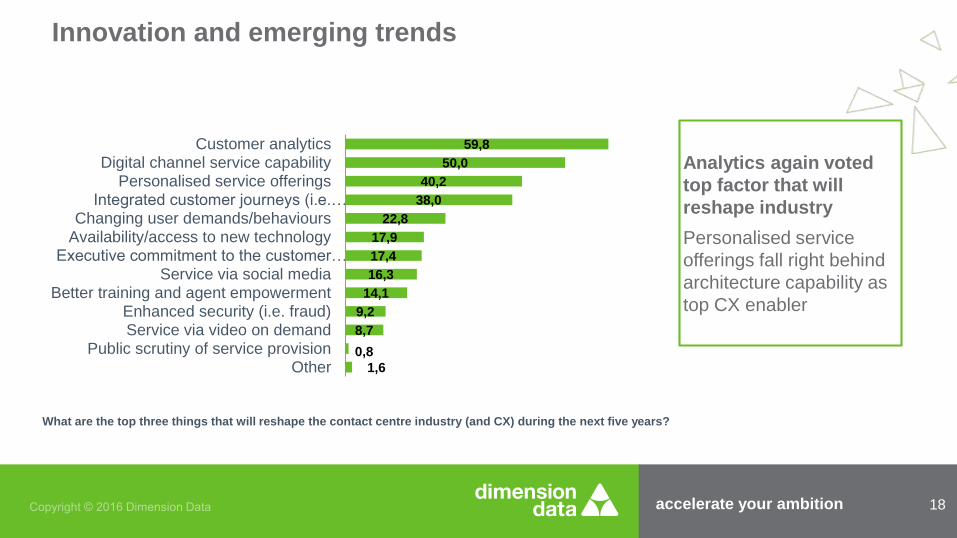

1,6

0,8

8,7

9,2

14,1

16,3

17,4

17,9

22,8

38,0

40,2

50,0

59,8

OtherPublic scrutiny of service provision

Service via video on demandEnhanced security (i.e. fraud)

Better training and agent empowermentService via social media

Executive commitment to the customer…Availability/access to new technologyChanging user demands/behaviours

Integrated customer journeys (i.e.…Personalised service offerings

Digital channel service capabilityCustomer analytics

Innovation and emerging trends

What are the top three things that will reshape the contact centre industry (and CX) during the next five years?

Analytics again voted

top factor that will

reshape industry

Personalised service

offerings fall right behind

architecture capability as

top CX enabler

accelerate your ambition 19

30,4

21,3

21,9

32,0

41,4

Other

We can't track the customer journey

Blockage points in processes (that affectthe CX) can be located

Key decision points can be identified

Interactions can be tracked across multiplechannels

Tracking customer journeys

How well can you track the customer journey across your service channels?

Just 41% can track a

customer journey that

spans multiple

channels

Just 21% can locate

problem hotspots that

impact CX

accelerate your ambition 20

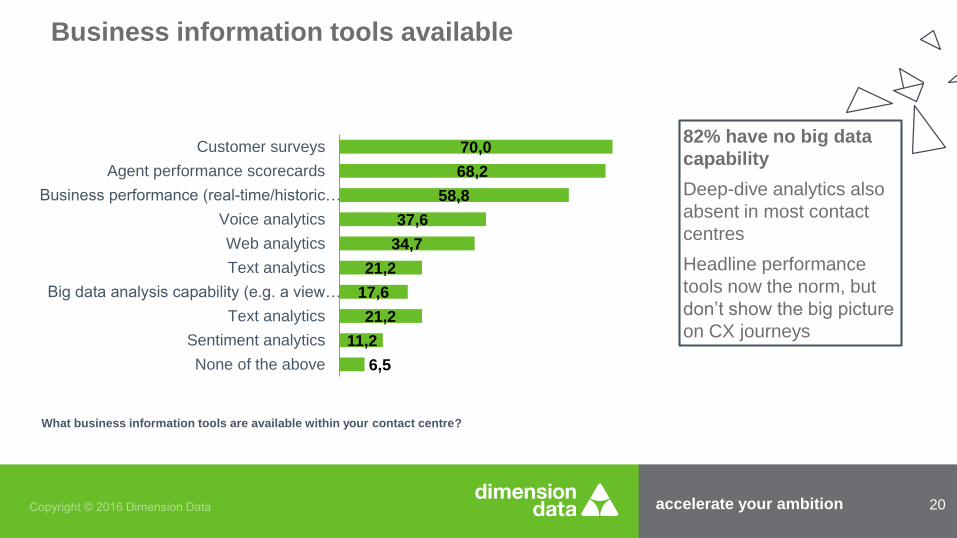

6,5

11,2

21,2

17,6

21,2

34,7

37,6

58,8

68,2

70,0

None of the above

Sentiment analytics

Text analytics

Big data analysis capability (e.g. a view…

Text analytics

Web analytics

Voice analytics

Business performance (real-time/historic…

Agent performance scorecards

Customer surveys

Business information tools available

What business information tools are available within your contact centre?

82% have no big data

capability

Deep-dive analytics also

absent in most contact

centres

Headline performance

tools now the norm, but

don’t show the big picture

on CX journeys

accelerate your ambition 21

Contact by channel: Actual split versus desired split

What is your desired versus actual split of customer interactions by channel grouping?

4…

3…

1…

Desired

5…

2…

2…

Actual

Desired split still

some way to go

before actual target

numbers achieved

Self-service presents

the largest gap and

significant opportunity

accelerate your ambition 22

4,4

8,1

19,2

31,3

37,0

Assisted services - single channel

Assisted services - multiple channels

Telephone and assisted services -blended channels

Telephone - single skill group

Telephone - multiple skill group (incl.inbound and outbound)

Dedicated versus cross-skilled agents

What percentage of your agents are dedicated to a single versus multiple skills/channels?

68% of agents continue

to be dedicated to

telephone

27% handle multiple

channels; 37% have

multiple skills

accelerate your ambition 23

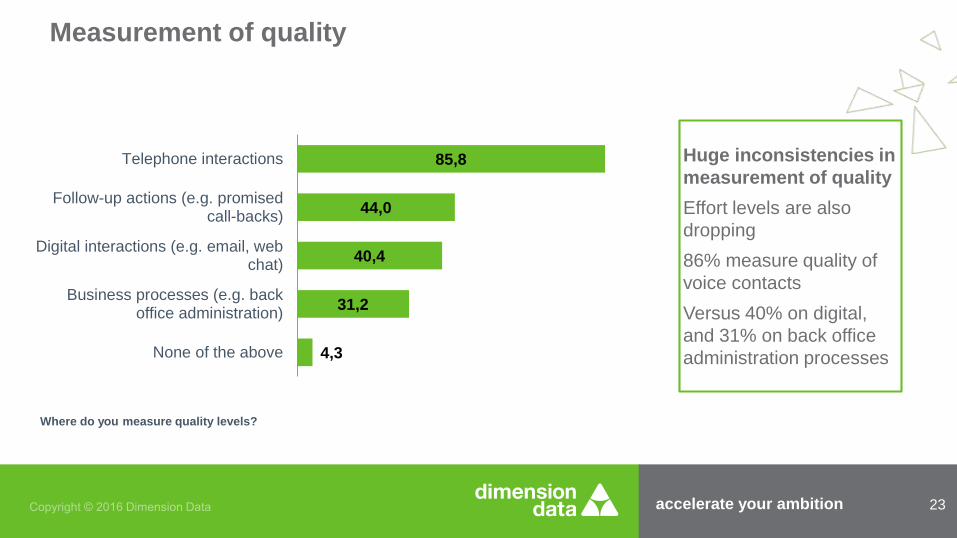

4,3

31,2

40,4

44,0

85,8

None of the above

Business processes (e.g. backoffice administration)

Digital interactions (e.g. email, webchat)

Follow-up actions (e.g. promisedcall-backs)

Telephone interactions

Measurement of quality

Where do you measure quality levels?

Huge inconsistencies in

measurement of quality

Effort levels are also

dropping

86% measure quality of

voice contacts

Versus 40% on digital,

and 31% on back office

administration processes

accelerate your ambition 24

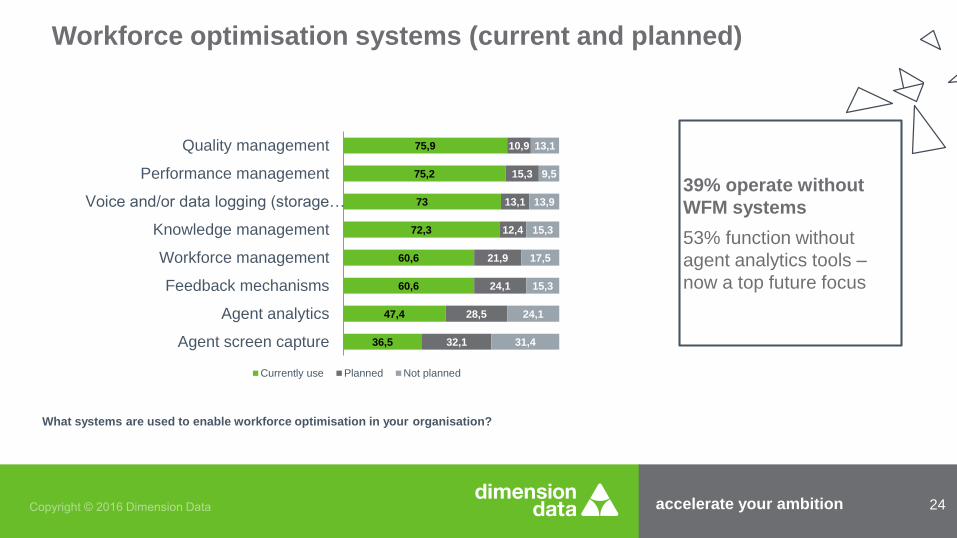

36,5

47,4

60,6

60,6

72,3

73

75,2

75,9

32,1

28,5

24,1

21,9

12,4

13,1

15,3

10,9

31,4

24,1

15,3

17,5

15,3

13,9

9,5

13,1

Agent screen capture

Agent analytics

Feedback mechanisms

Workforce management

Knowledge management

Voice and/or data logging (storage…

Performance management

Quality management

Currently use Planned Not planned

Workforce optimisation systems (current and planned)

What systems are used to enable workforce optimisation in your organisation?

39% operate without

WFM systems

53% function without

agent analytics tools –

now a top future focus

accelerate your ambition 25

48,2

13,9

19

24,8

28,5

24,1

24,8

19,7

34,3

38,7

51,8

53,3

54

65,7

None of the above

Agent satisfaction with workforce…

Management satisfaction with workforce…

Alignment of shift patterns to contact…

Forecast accuracy - resource…

Schedule adherence levels

Forecast accuracy - contact volumes

Telephone Assisted-service

Workforce management effectiveness (targets and measurements)

What targets are in place to measure the effectiveness of the workforce management team?

Large disparity between

phone and assisted-

service channels in

application of WFM

process

Almost half of centres are

failing to track WFM

performance across

digital service channel

accelerate your ambition 26

10,1

10,9

15,5

30,9

33,6

37,3

36,8

32,9

32,6

22,2

22,6

14,6

Sourcing stage

Approvals stage

Design stage

Independently responsible Fully involved Partially involved Not involved

Contact centre involvement in IT sourcing and design decisions

How involved is the contact centre across each stage of the technology decision-making process?

47% are only partially

involved or have no say

in the design of

technology

>½ have no input in the

approval process

Still the biggest inhibitor

to maximising systems

effectiveness

accelerate your ambition 27

16,8

17,3

18,2

18,7

22,0

24,2

29,8

31,3

44,4

40,8

59,5

41,4

50,0

58,3

50,5

54,3

38,8

41,9

22,3

39,9

28,0

17,6

19,7

14,4

Knowledge management systems

Analytics systems

Business support systems (HR/Finance…

Digital channel systems

Interaction optimisation systems…

Security systems (e.g. fraud prevention,…

Telephony systems - automated (e.g. IVR)

Telephony systems - agent-led…

Meets current and future needs Meets current needs Doesn't meet current needs

How does technology meet current and future needs?

How well do the following infrastructure items meet your current and future needs?

2 in 5 say digital

systems fail current

needs

78% fear systems won’t

meet future requirements

<1/2 of overall systems

meet current demands

accelerate your ambition 28

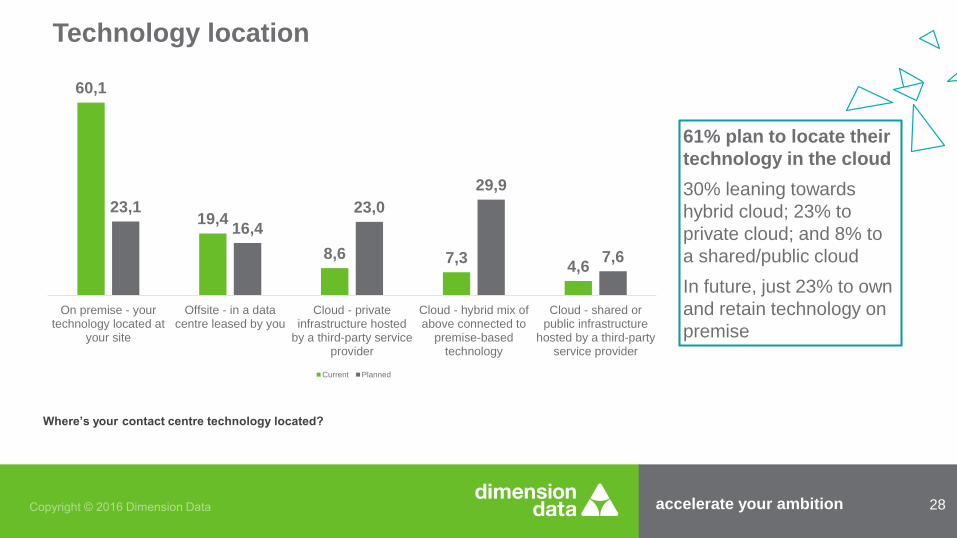

Technology location

Where’s your contact centre technology located?

60,1

19,4

8,6 7,34,6

23,1

16,4

23,0

29,9

7,6

On premise - yourtechnology located at

your site

Offsite - in a datacentre leased by you

Cloud - privateinfrastructure hosted

by a third-party serviceprovider

Cloud - hybrid mix ofabove connected to

premise-basedtechnology

Cloud - shared orpublic infrastructure

hosted by a third-partyservice provider

Current Planned

61% plan to locate their

technology in the cloud

30% leaning towards

hybrid cloud; 23% to

private cloud; and 8% to

a shared/public cloud

In future, just 23% to own

and retain technology on

premise

83.2% of companies recognise

CX as a competitive

differentiator

80.4% recognise CX as the

most important strategic

performance measure

Personalisation of

services will be key

and enabled by

analytics – voted

top trend that will

change the

industry in the next

5 years – 82.4%

have no big picture

view

86.4% can evidence

cost savings via

improved CX

84.4% say it

increases company

revenue/profits

Connected

customer

journeys, CX and

contact resolution

top focus as most

contact centres

head to 9 channel

options

Omnichannel top

trend for 2016

Integration

capability set to

increase from

23.2% to 77.9% in

next two years

CX is now top

reason for

offering self-

/assisted-service

channels (ahead of

cost reduction)

But digital

channels being

hindered by

absence of focus

Cloud in some

form now a must

for contact centres

58.2% planning for

it. Just 20.1% will

retain technology

on premise

Hybrid solutions

set to treble and

enable a single

integrated platform

Mobile apps

A top three choice for

CS with everyone under

35 yrs

2 in 5 say digital tech

not meeting business

needs as demand soars

AsiaPac at a glance…

5 things we’ve

learned

about Asia Pacific

from the 2016

results

Digital strategies now being defined by

CX rather than cost

Self-service capability 12% short of

desired split (assisted-service on track)

Omnichannel top focus, but 59%

can’t track customer journey that span

multiple channels

Analytics top enabler that will change

industry in next 5 years and is helping

validate CX investment

Over half 51% say digital technology isn’t

meeting current needs; WFO neglected

companiesbenchmark

Why Pinpoint

problems

Identify best

practice

Validate

performance

Get buy-in

to change

Support

business cases

Understand

trends

Benchmark Comparison

Portal

Dynamically

Filter All of the data in the

Benchmarking

Report by 8 levels

Further information2016 Global Contact Centre Benchmarking Report

Contact us:

www.dimensiondatacx.com

@DiDataCX | #CCBenchmarking

Global Contact Centre Benchmarking Discussion Group

Dimension Data Contact Centres Showcase Page