insurance rate making using data mining - … · data mining for rate making! the insurance...

TRANSCRIPT

Copyright © 2000 SAS EMEA

Bernd DrewesSAS EMEA

Insurance Rate MakingUsing Data Mining

Copyright © 2000 SAS EMEA

… or: Dollars from your Data

Copyright © 2000 SAS EMEA

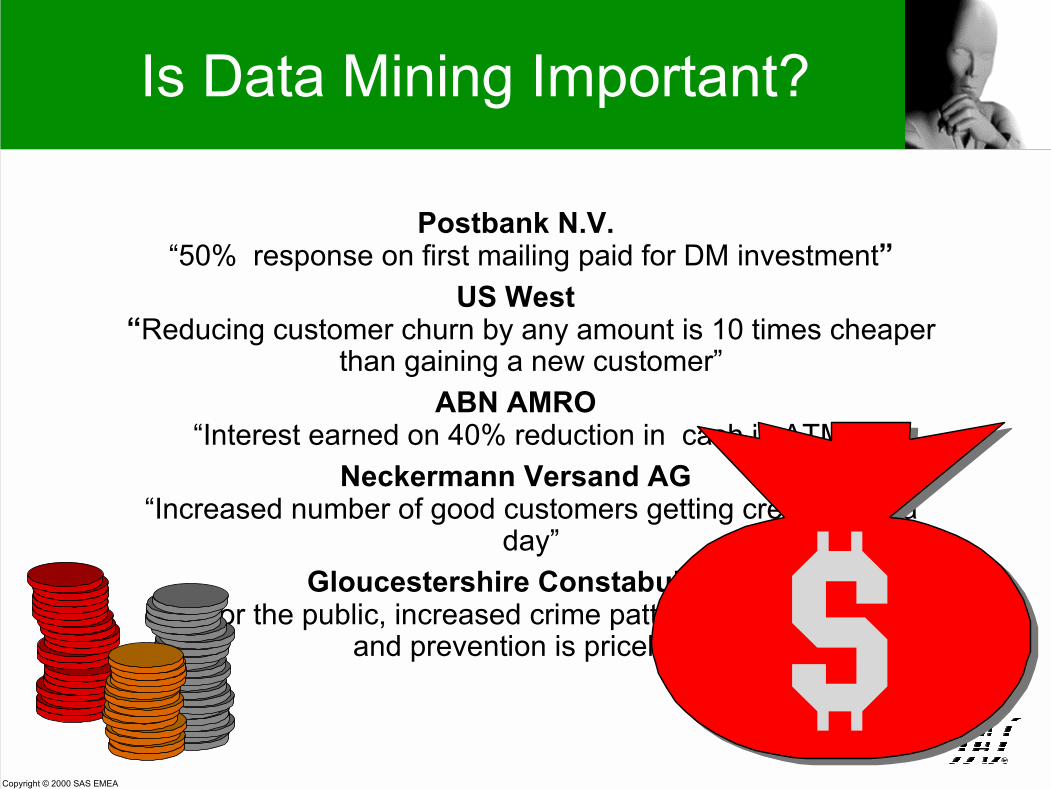

Is Data Mining Important?

Postbank N.V.“50% response on first mailing paid for DM investment”

US West“Reducing customer churn by any amount is 10 times cheaper

than gaining a new customer”ABN AMRO

“Interest earned on 40% reduction in cash in ATMs”Neckermann Versand AG

“Increased number of good customers getting credit by 80 aday”

Gloucestershire Constabulary“For the public, increased crime pattern identification

and prevention is priceless”

Copyright © 2000 SAS EMEA

Drivers for Data Mining

! Companies feel ‘datarich, information poor’

! Customer related dataoffer a competitiveadvantage

Copyright © 2000 SAS EMEA

Business DriversMarketing - CRM Relation! Target Marketing! Customer Acquisition! Customer Retention! Cross Selling/Up-selling! Customer Segmentation! Customer Profiling! Customer Profitability

Analysis

�� �� �� � � �

�� � �

�� �� � � ��

��� � � �

� � � � ���� � � � � � � �

�� � � � � �� ����� �

Copyright © 2000 SAS EMEA

Business DriversFinance

! Credit RiskManagement

! Fraud Detection! Funds

Management! Optimal Pricing! Optimal Rates! Individualized Risk

Copyright © 2000 SAS EMEA

Data Mining

! Data Mining is theprocess of selecting,exploring and modeling

! large amounts of data! to uncover previously

unknown patterns forbusiness advantage

Copyright © 2000 SAS EMEA

The Integrated SAS Solution

TransformData into

Information

Act on Information

BusinessQuestion

Data WarehouseDBMS

Data MiningProcessing

EIS, BusinessReporting,

OLAP

Identify Problem

MeasureResults

Copyright © 2000 SAS EMEA

The SAS InstituteData Mining Solution

Enterprise Miner

SAS Institute DataMining ProjectMethodology

Business SolutionsSAS Institute andPartners

Copyright © 2000 SAS EMEA

Enterprise Miner TM

Characteristics:! Integration of data warehousing

and data mining! Co-operation of business, IT and

data miners! Covers all stages of the DM

process! Process flow orientation! Enables companies to gain

competitive advantage

Copyright © 2000 SAS EMEA

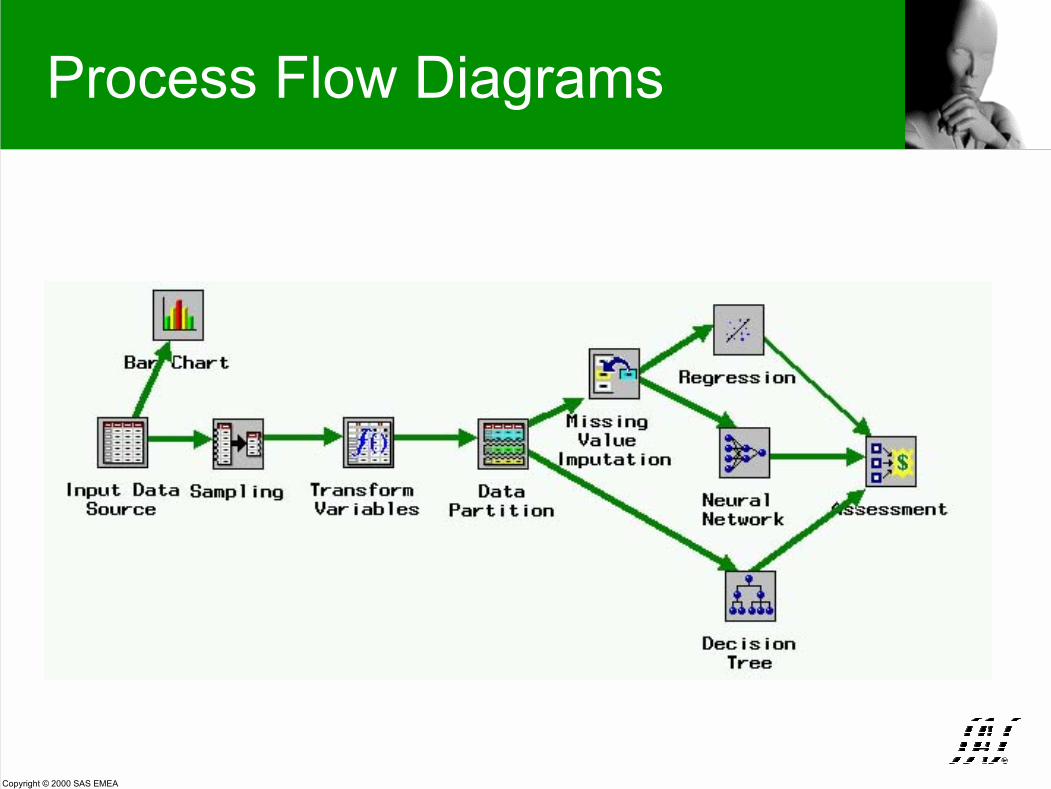

Process Flow Diagrams

Copyright © 2000 SAS EMEA

Data Mining for Rate Making

! The Insurance Industry in Change! The Business Problem! Examples of Data Mining Approaches to

the Business Problem! Rate Making Using Pure Premium! Rate Making Using Loss Ratio! Refining an Existing Rate Structure

Copyright © 2000 SAS EMEA

The Insurance Industry inChange

! Globalization! no safe home markets any more

! Deregulation! many more players, new rules

! New channels, new modes of business! retailers, E-insurance

! Result: Much higher competition and! increased focus: customers, attrition/loyalty,

prices/rates, direct marketing/profiling

Copyright © 2000 SAS EMEA

The Business Problem

! Rate Making:! competitive rates, increased profitability! Need to use correct pricing methodology

based on correct levels of risk exposure, and! need to move away from rigid rates and

provide a flexible price structure! Implications on customer relations

! attract good clients, discourage bad ones! client retention, cross selling other prod’s

Copyright © 2000 SAS EMEA

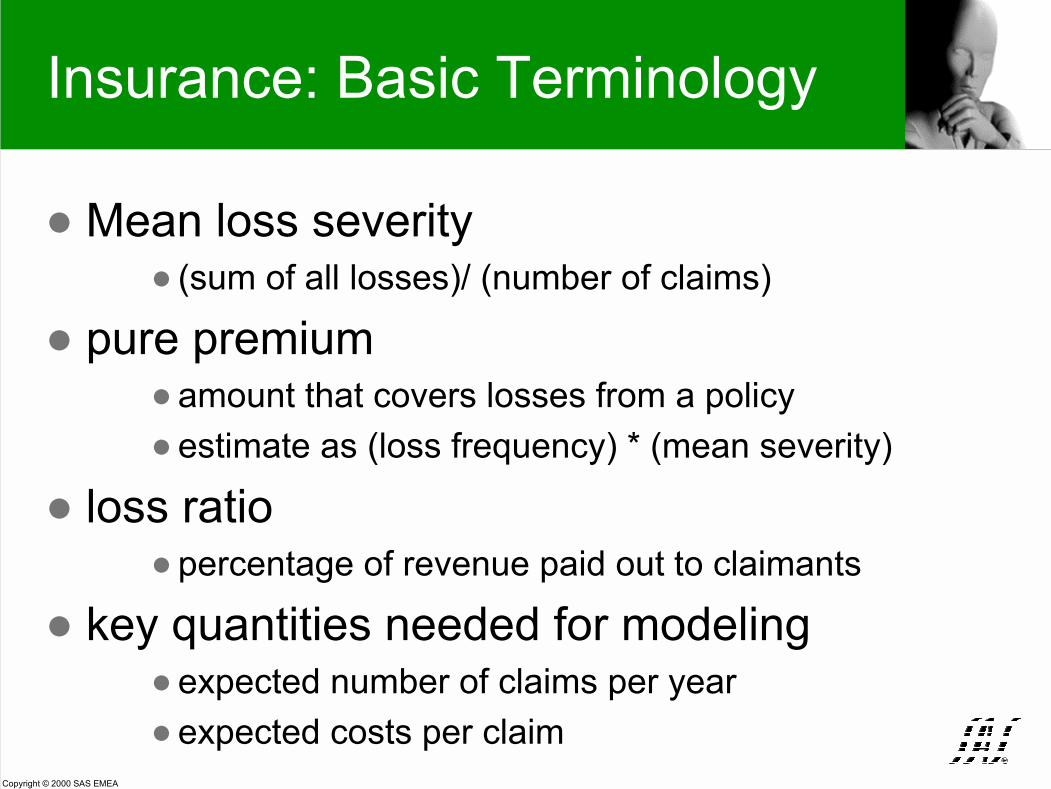

Insurance: Basic Terminology

! Mean loss severity! (sum of all losses)/ (number of claims)

! pure premium! amount that covers losses from a policy! estimate as (loss frequency) * (mean severity)

! loss ratio! percentage of revenue paid out to claimants

! key quantities needed for modeling! expected number of claims per year! expected costs per claim

Copyright © 2000 SAS EMEA

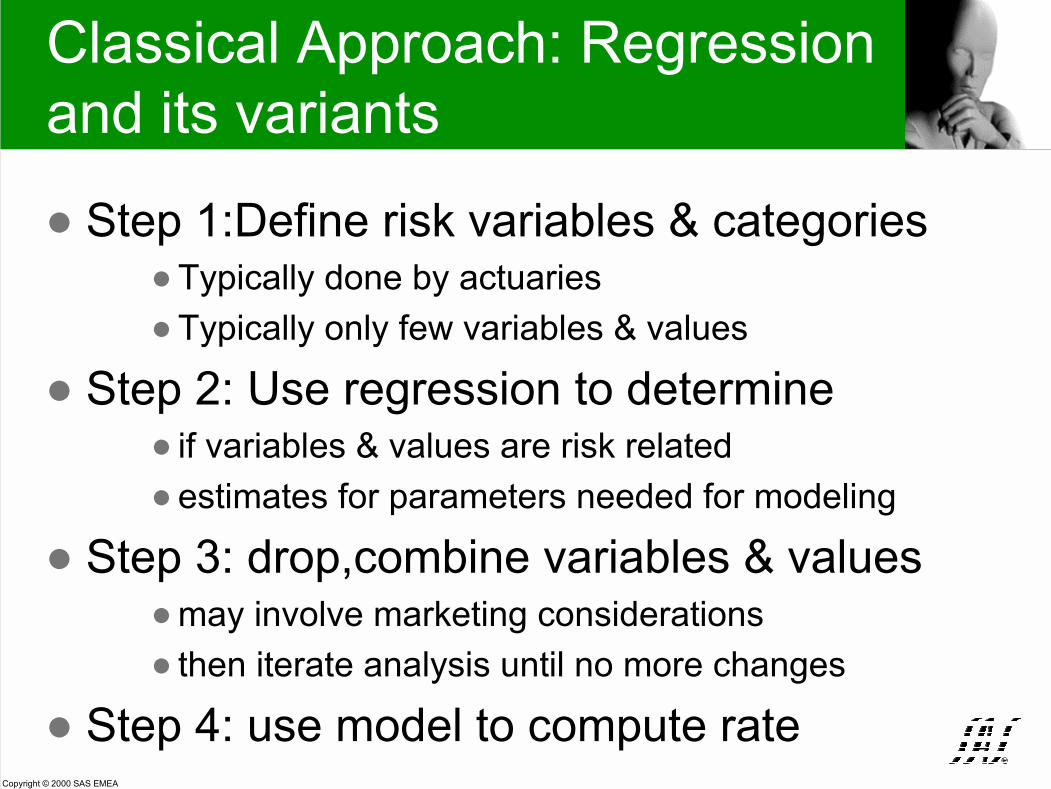

Classical Approach: Regressionand its variants

! Step 1:Define risk variables & categories! Typically done by actuaries! Typically only few variables & values

! Step 2: Use regression to determine! if variables & values are risk related! estimates for parameters needed for modeling

! Step 3: drop,combine variables & values! may involve marketing considerations! then iterate analysis until no more changes

! Step 4: use model to compute rate

Copyright © 2000 SAS EMEA

Example: Automobile Insurance

! start with age, car_age, car_power,value, region

! define intervals for each variable! based on experience and practice, not just data

! cross product of intervals defines risks! now each customer falls into a risk class! Use statistics to build a model for

! accident likelihood! mean cost per claim

Copyright © 2000 SAS EMEA

Claim frequency: Model results

Source Deviance NDF DDF F PrF ChiSquare PrChi

1 INTERCEPT 357.2690 0 76 . . . .

2 TARIF_ID 341.5579 1 76 11.9241 0.0009 11.9241 0.0006

3 AGE_ID 131.1380 1 76 159.7009 0.0001 159.7009 0.0001

4 VALUE_ID 128.5264 2 76 0.9911 0.3759 1.9821 0.3712

5 POWER_ID 124.4280 2 76 1.5553 0.2178 3.1106 0.2111

6 CAR_AGES 100.1366 4 76 4.6091 0.0022 18.4362 0.0010

Copyright © 2000 SAS EMEA

Rate Making Using DataMining: Overview

! Step 1: Collect ALL relevant data! store in single table! check & clean data, e.g. false & missing values

! Step 2: Explore data! determine relationships & trends! transform values and define derived variables

! Step 3: Compute several models! decision tree, regression, neural nets

! Step 4: Assess results! from technical and business perspective

Copyright © 2000 SAS EMEA

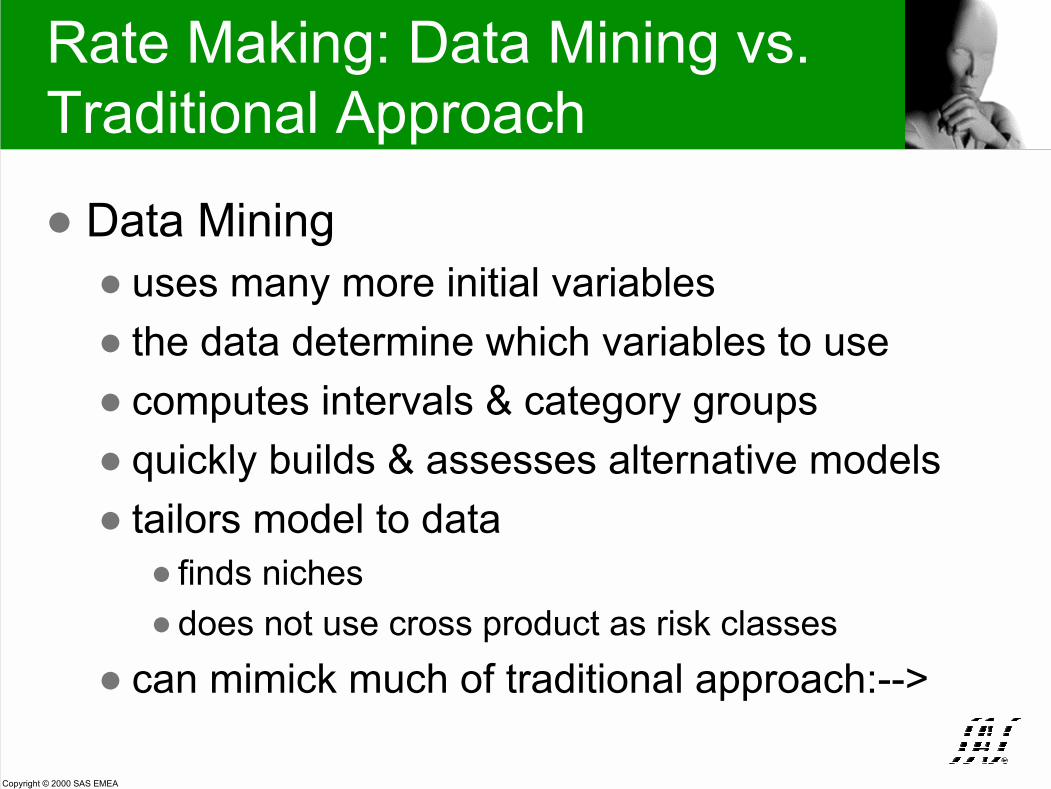

Rate Making: Data Mining vs.Traditional Approach

! Data Mining! uses many more initial variables! the data determine which variables to use! computes intervals & category groups! quickly builds & assesses alternative models! tailors model to data

! finds niches! does not use cross product as risk classes

! can mimick much of traditional approach:-->

Copyright © 2000 SAS EMEA

Example: Claim FrequencyPrediction with Data Mining

! When starting with same variables:region, age, value, power, car_age

! Decision Tree analysis finds these rules! IF Age < 32.5 THEN ACCID’s: 70.9%

No_ACCID’s: 29.1%! IF Car category based on power < 7.5 AND

32.5 <= Age < 35.5 THEN ACCID’s: 40.4%No_ ACCID’s: 59.6%

! IF Age of the car < 11.5 AND 35.5 <= Age< 50.5 THEN ACCID’s: 16.9%

No_ACCID’s: 83.1%

Copyright © 2000 SAS EMEA

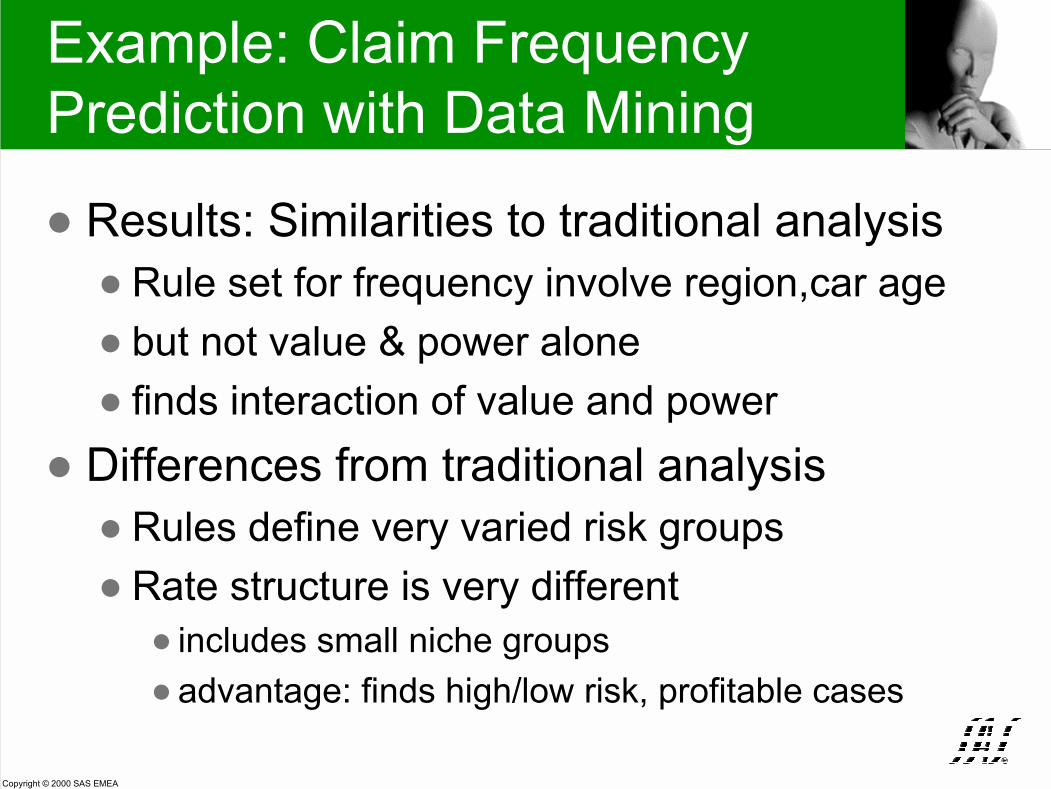

Example: Claim FrequencyPrediction with Data Mining

! Results: Similarities to traditional analysis! Rule set for frequency involve region,car age! but not value & power alone! finds interaction of value and power

! Differences from traditional analysis! Rules define very varied risk groups! Rate structure is very different

! includes small niche groups! advantage: finds high/low risk, profitable cases

Copyright © 2000 SAS EMEA

Getting more detailed: SpecificData Mining Approaches

! Approaches! 1. identify winning & loosing segments

2. generate new rating structure:! by focussing on loss ratio! by focussing on pure premiums

3. refine existing rating structure

! Additionally! Find most highly predicting variables! Find best splits and optimal groupings! Use Data Mining Results for statistics input

Copyright © 2000 SAS EMEA

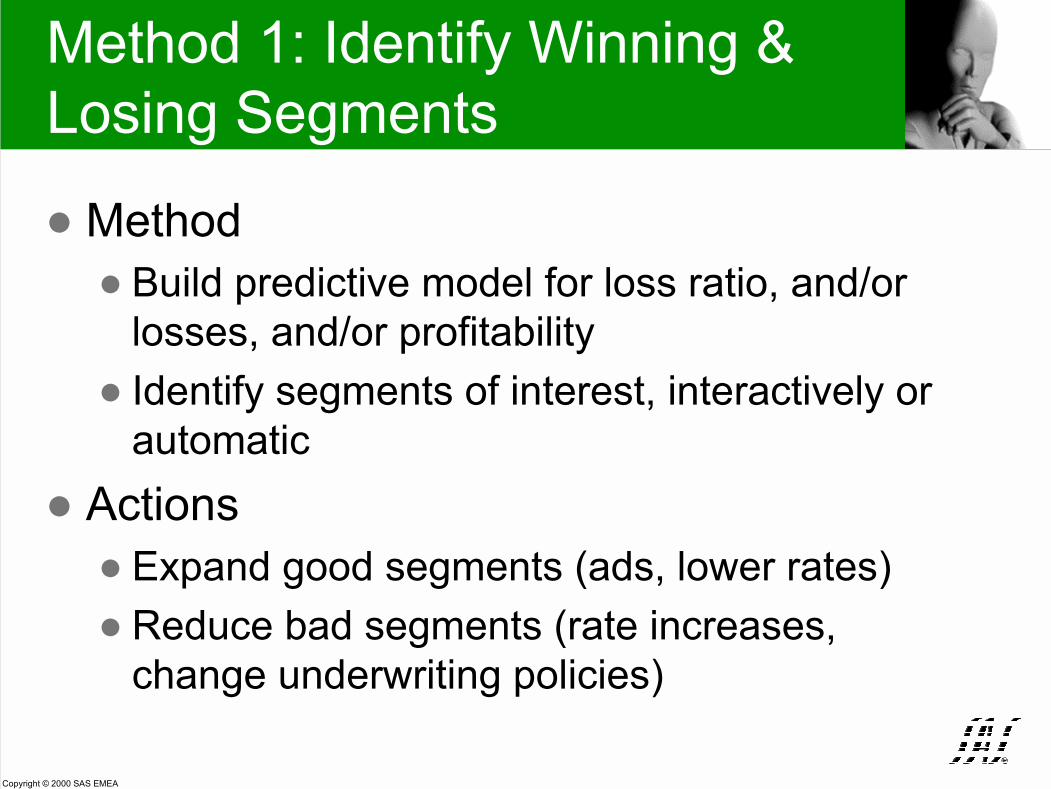

Method 1: Identify Winning &Losing Segments

! Method! Build predictive model for loss ratio, and/or

losses, and/or profitability! Identify segments of interest, interactively or

automatic! Actions

! Expand good segments (ads, lower rates)! Reduce bad segments (rate increases,

change underwriting policies)

Copyright © 2000 SAS EMEA

Method 2: Reduce Variance ofLoss Ratio

! Build predictive model for loss ratio! percentage of premiums paid out to claimants

! Consider resulting segments with a highvariance in loss ratio

! mixed behavior, some subgroups much better! good customers paying for bad ones

! Interactively partition segment! Discard or increase rate for poor subsegments

! Results in entirely new rating structure! Can only be done occasionally

Copyright © 2000 SAS EMEA

Method 3: Refine RatingStructure

! Goal:subdivide existing rating classes forimproved profitability

! Method:! label clients by unique rating class identifier! do supervised classification on risk identifier! identify segments to be refined! do loss ratio reduction method on segments! inspect resulting segments: raise rates on high

loss ratio, then if feasible, lower rates on others! Assess, iterate if necessary! Result: modification of existing rate structure

Copyright © 2000 SAS EMEA

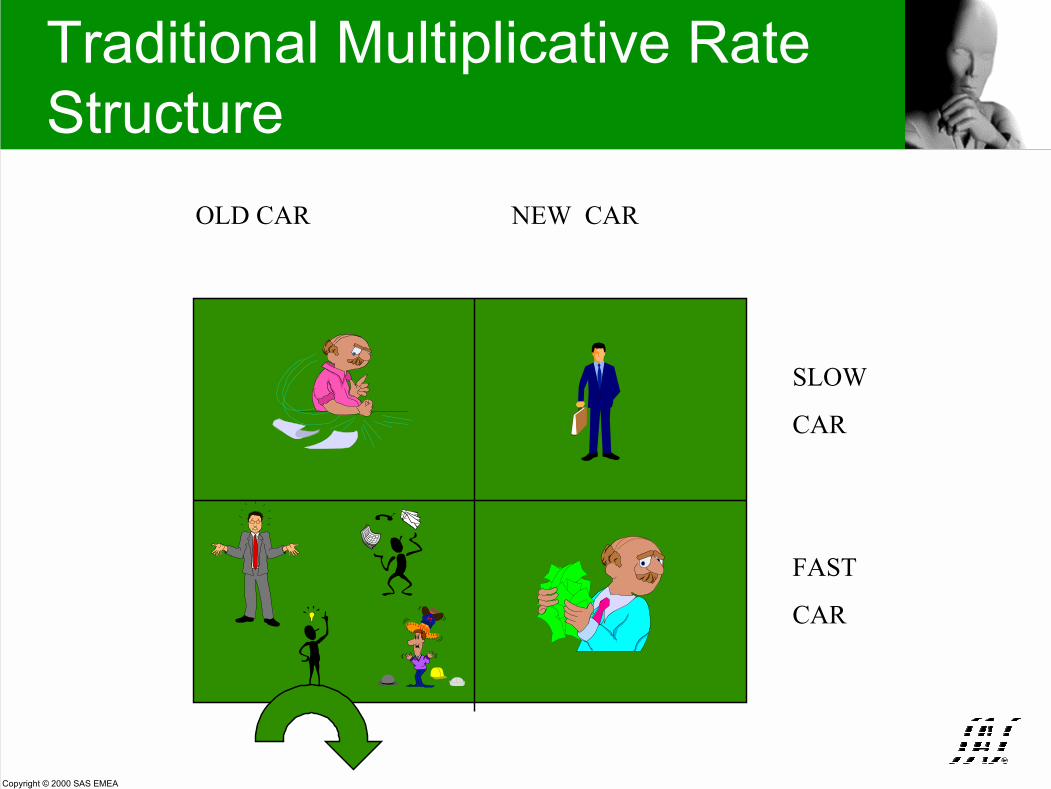

Traditional Multiplicative RateStructure

OLD CAR NEW CAR

SLOW

CAR

FAST

CAR

Copyright © 2000 SAS EMEA

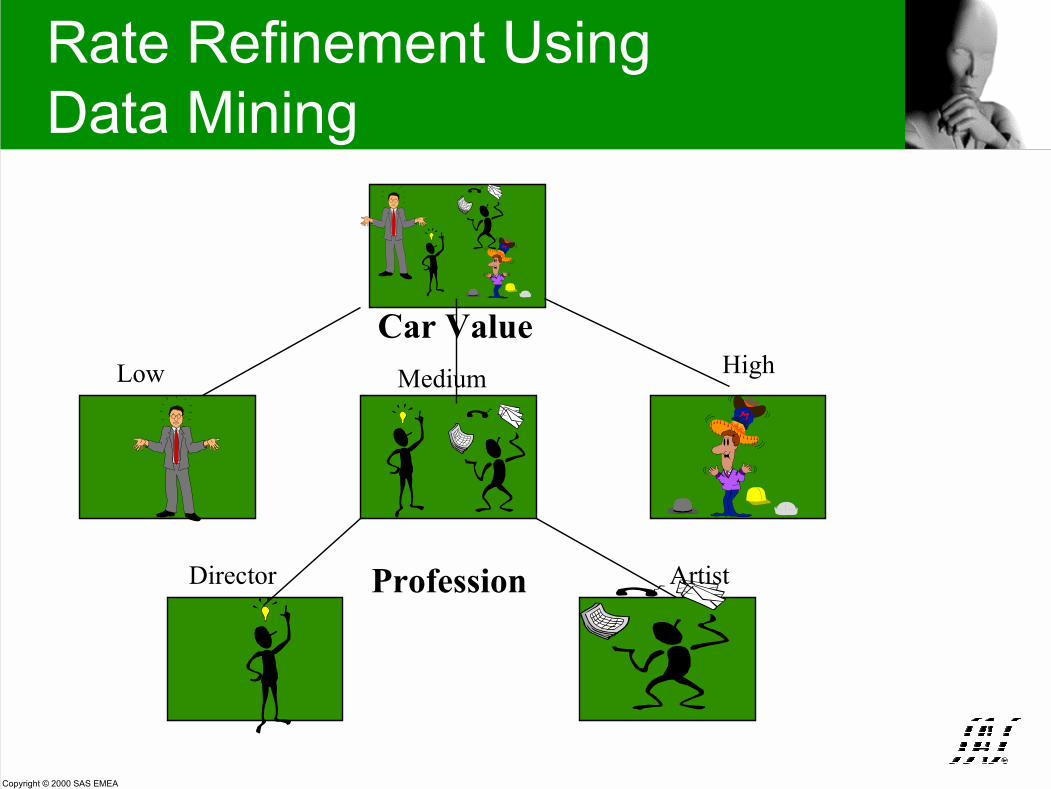

Rate Refinement UsingData Mining

Car Value MediumLow High

Profession Artist Director

Copyright © 2000 SAS EMEA

Summary: Rate Making withData Mining

! Data Mining allows! refinement of existing rate structures

! interactive exploration of rate groups

! almost individualized rate setting:! let the data define the rating categories

! building alternative models quickly! complexity reduction:

! optimal groupings for variables! Finding profitability and loss niches

Copyright © 2000 SAS EMEA

Conclusion:Beyond Rate Making

! Data Mining focuses on customers! Identifies customer groups & niches! focus is on understanding rate structure,

business implications, underwriting rules! Results may extend beyond rate making

! Cross selling (other insurance, investments)! improve customer retention! may consider life time value of customer

Copyright © 2000 SAS EMEA

References: Zurich Insurance

! Application Description: NeuralNetwork (EM) Application to detectsignificant Attributes of Policy-Holdersand determine Risk-Adequacy as well asLifetime Profitability & future Cash flows.

! Need to be able to do Customer-basedPricing to target profitable Segments ofthe Insurance Market.

! Some key directions: -->

Copyright © 2000 SAS EMEA

Zurich Insurance(see Lechner, SEUGI ‘98)! ���������������� ������������������� ����

�������������� ������ ��� ������ �������

! � ��� ����� ����������� � ����������� ���

������� ����������� �������������� �� ����

�� �������������������� ������ �������� ������

! � � ���� � ��� ���� ��� ��������������� ��

����� ��� ������� � �� ����� ����� ������� ���� ��

������ � ���� �� ��� �� �� ������� ��� ������

����� ����� �� � ������������ ��� ���

� � ���� ����

Copyright © 2000 SAS EMEA

References: Old Mutual

! !"#$%&'("#)*+&',-$%&).)"$$#)',)/,,0(')#('()(*%,&&)&$1$%(/)#2-$"&2,"&3)'4$*+&',-$%&)'4$-&$/1$&5)'4$)6%,#+*'&'4$7)4,/#),%)#,)",')4,/#5)("#)'4$)&(/$&*4(""$/

! ,8'$")9("')"$:('21$)(&)9$//)(&)6,&2'21$*%2'$%2();)&+*4)(&)<942*4)*+&',-$%&94,)-$$')'4$&$)*4(%(*'$%2&'2*&)#,)",'4(1$)$2'4$%)6%,#+*')=),%)6%,#+*')>?

! -,%$)&6$*282*&)..@

Copyright © 2000 SAS EMEA

Old Mutual (SEUGI 98)

! "$$#)42&',%2*)#('(),")'4$)*+&',-$%ABCD! *+&',-$%)2"8,%-('2,")E7)4,+&$4,/#

! consistent adresses, coherent product view! customer attrition

! which customers to make offers, which to let go! patterns for repeat purchases! life time value of customers

Copyright © 2000 SAS EMEA

References on Rates & PricesUsing Enterprise Miner

! GIE AXA (F)! Pricing, targeting, segmentation

! Allianz Subalpina (I)! motor rate analysis

! Societa’Reale Mutua di Assicurazioni (I)! correct pricing

Copyright © 2000 SAS EMEA

References on Enterprise Minerin Insurance

! Allianz (AU):! Rate Making, Customer Segmentation, Churn

! mainly doing Rate Making, but also CustomerSegmentation, Database Marketing,Churn Prediction

! GIE MMA SI (F)! Application Description: using EM for

strategic marketing decisions : loyaltyanalysis, retention analysis, profiling,targeting.

Copyright © 2000 SAS EMEA

References on Enterprise Minerin Insurance

! Winterthur (CH)! Marketing, Behavioral

Analysis

! AGIS (CH)! Database Marketing

! AXA Colonia (D)! EM-based CRM &

DWH

! Victoria AG (D)! churn & cancellation

analysis

! Finax (DK)! Credit scoring

Copyright © 2000 SAS EMEA

References on Enterprise Minerin Insurance

! GIE MMA SI (F)! loyalty & retention

analysis, profiling

! SACCEF (F)! credit scoring

! ARCA VITA (I)! database marketing

! ACHMEA HOLDINGNV (NL)

! Direct Mail, crossselling, profiling, LTV

! London&EdinburghInsurance Group(GB)

! Credit risk analysis

! Eagle Star (GB)

Copyright © 2000 SAS EMEA

Competition

! Data Mining Vendors! IBM: consulting package, generic tool, virtual

product

! Software/Consulting Companies! TRICAST! LARSEN & Partners

Copyright © 2000 SAS EMEA

Opportunity

! SAS has tools for traditional solutions! … for data mining solutions! …. Has good references! …. Not very much competition! customer is under market pressure

! --> good sales opportunity! customer needs to develop own

approach

Copyright © 2000 SAS EMEA

Applying Data Mining for RateMaking:Some Examples

! Identify niches of profits & losses! Refining rate structure! Interactively modify risk structure, e.g.

minimize loss ratio (Demo)

Copyright © 2000 SAS EMEA

Identifying Niches:(1) Find Rate Structure

Copyright © 2000 SAS EMEA

Identifying Niches:(2) Analyze Bottom Line

GROUP N Premium-Pure Premium8 931 -558,4729 1065 6505,42810 1237 768,677511 546 3445,33612 104 14644,713 47 6257,00114 73 18199,0815 16 27253,4

Copyright © 2000 SAS EMEA

Demo: Refining an ExistingRate Structure

Copyright © 2000 SAS EMEA

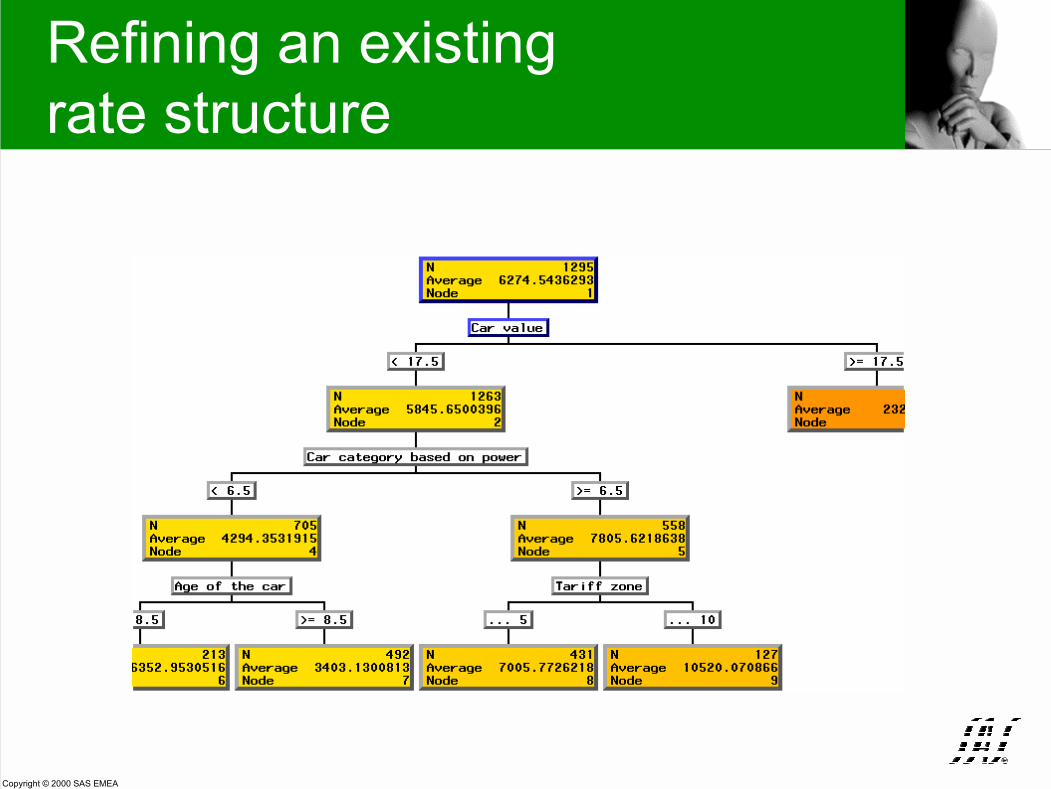

Refining an existingrate structure

Copyright © 2000 SAS EMEA

Refining an Existing RateStructure: Segment 3

OLD: Node 3 IF 17.5 <= Car valueTHEN NODE: 3, AVE : 23202.4, SD : 9753.32

NEW1. IF 17.5 <= Car value AND IF Tariff zone IS ONE OF: 8 9 10 THEN NODE: 3, AVE: 30293.9, SD: 104782.IF 17.5 <= Car value AND IF Age of the car < 8.5 AND

Tariff zone IS ONE OF: 2 3 4 5 6 7 THEN NODE: 4, AVE: 22460.2 , SD: 6779.283.IF 17.5 <= Car value AND IF 8.5 <= Age of the car

AND Tariff zone IS ONE OF: 2 3 4 5 6 7 THEN NODE: 5, AVE: 15637, SD: 6464

Copyright © 2000 SAS EMEA

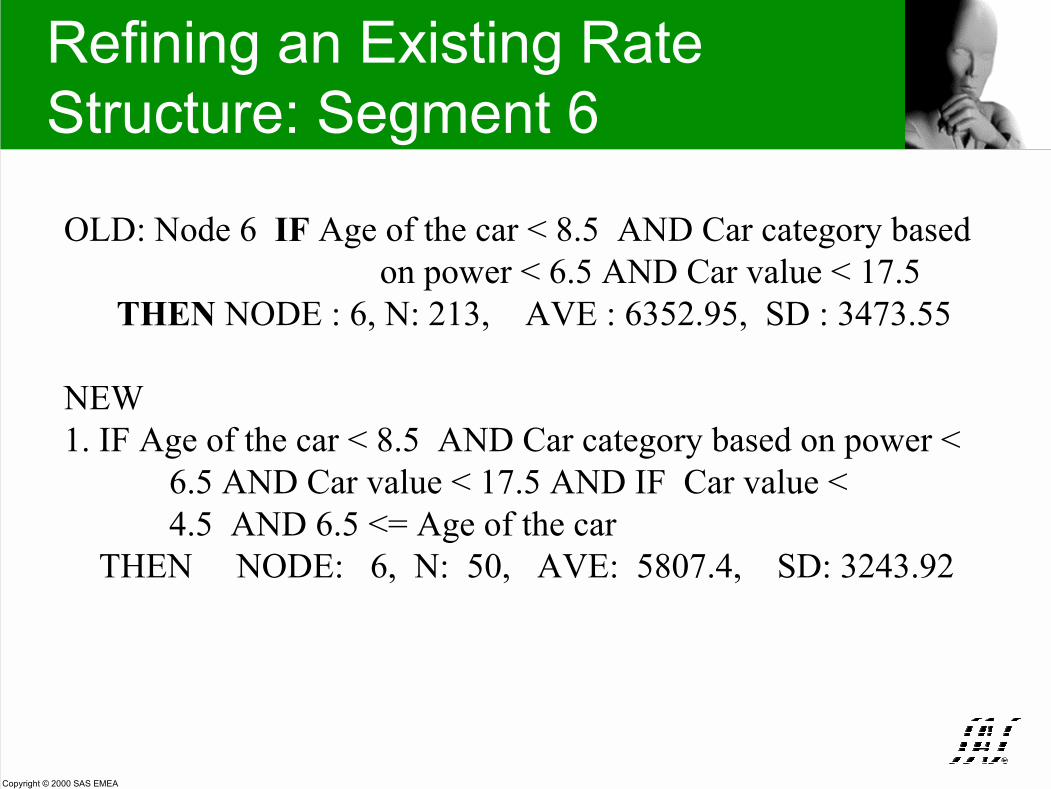

Refining an Existing RateStructure: Segment 6

OLD: Node 6 IF Age of the car < 8.5 AND Car category basedon power < 6.5 AND Car value < 17.5

THEN NODE : 6, N: 213, AVE : 6352.95, SD : 3473.55

NEW1. IF Age of the car < 8.5 AND Car category based on power <

6.5 AND Car value < 17.5 AND IF Car value <4.5 AND 6.5 <= Age of the car

THEN NODE: 6, N: 50, AVE: 5807.4, SD: 3243.92

Copyright © 2000 SAS EMEA

Refining an Existing RateStructure: Segment 6

2. IF Age of the car < 8.5 AND Car category based on power < 6.5AND Car value < 17.5 AND IF Age < 36 AND Tariffzone IS ONE OF: 1 2 3 4 AND Age of the car < 6.5

THEN NODE : 8, N: 14, AVE: 8372.93, SD: 3081.97

3. IF Age of the car < 8.5 AND Car category based on power < 6.5AND Car value < 17.5 AND IF 36 <= Age AND Tariff zoneIS ONE OF: 1 2 3 4 AND Age of the car < 6.5

THEN NODE : 9, N: 51, AVE: 4440.06, SD: 1458.214. IF Age of the car < 8.5 AND Car category based on power < 6.5

AND Car value < 17.5 AND IF Age < 40.5 AND Tariffzone IS ONE OF: 5 6 7 8 9 10 AND Age of the car < 6.5

THEN NODE: 10, N: 15, AVE: 8539.47, SD: 3664.78

Copyright © 2000 SAS EMEA

Refining an Existing RateStructure: Segment 6

5. IF Age of the car < 8.5 AND Car category based on power < 6.5AND Car value < 17.5 AND IF 40.5 <= Age AND Tariff zone IS ONE OF: 5 6 7 8 9 10 AND Age of the car < 6.5

THEN NODE: 11, N: 35, AVE: 6562.66, SD: 3375.426. IF Age of the car < 8.5 AND Car category based on power < 6.5

AND Car value < 17.5 AND IF Tariff zone IS ONE OF: 1 2 3 4 AND 4.5 <= Car value AND 6.5 <= Age of the car

THEN NODE: 12, N: 28, AVE: 6715, SD: 4768.797. IF Age of the car < 8.5 AND Car category based on power < 6.5

AND Car value < 17.5 AND IF Tariff zone IS ONE OF: 5 6 7 8 9 10 AND 4.5 <= Car value AND 6.5 <= Age of the car

THEN NODE: 13, N: 20, AVE: 8667, SD: 2477.46

Copyright © 2000 SAS EMEA

Epilogue

! Many more specialized rules with datamining

! rules almost impossible to find withclassical analysis

! creative tool in hands of creative analyst! validate hypotheses statistically! more approaches than shown: interactive

modifications of premiums, etc.