new markets tax credit presentation - center for rural · pdf filenew markets tax credit the...

TRANSCRIPT

New Markets Tax Credit

The New Markets Tax Credit ("NMTC"), provided in Section 45D of the Internal Revenue Code, provides federal tax credits with respect to $15 billion in qualified investments made from 2001 to 2007.

What is the New Markets Tax Credit?

New Markets Tax Credit

Annual qualified investment pool which generates NMTCs: 2001 - $1 billion 2002 - $1.5 billion 2003 - $1.5 billion 2004 - $2 billion 2005 - $2 billion 2006 - $3.5 billion 2007 - $3.5 billion

New Markets Tax Credit The NMTC is equal to 39% of qualified

investments and is claimed over a seven year period starting on the date when the investment is made.

Investors may claim NMTCs equal to 5% of their investment in years one to three and 6% of their investment in years four to seven.

The NMTC has a present value of about 30%.

New Markets Tax Credit Example: A $1 million qualified investment in 2002

would generate NMTCs as follows: $50,000 in 2002 $50,000 in 2003 $50,000 in 2004 $60,000 in 2005 $60,000 in 2006 $60,000 in 2007 $60,000 in 2008

Total of $390,000 in NMTCs, with a present value of about $300,000.

New Markets Tax Credit

NMTCs are awarded by the Treasury Department to entities which qualify as Community Development Entities ("CDEs") and which apply for an allocation of credits.

A CDE can be owned or sponsored by either a for-profit or a non-profit entity, or both.

To qualify, the entity must have a primary mission of community development and must be accountable to the community. A CDE can meet these tests through its parent (for example, a CDC sponsor).

How Does the NMTC Work?

New Markets Tax Credit

Example: A community development corporation forms a limited partnership, limited liability company or subsidiary corporation to apply for CDE status and an allocation of NMTCs.

How Does the NMTC Work?

New Markets Tax Credit

Once a CDE receives tax credits, investors (such as local corporations, banks, insurance companies or individuals) invest in the CDE by contributing cash. No bridge financing is permitted.

The CDE uses cash from the investment to invest in qualifying businesses.

Investment in qualifying business may be in the form of capital or equity investment or loans to qualifying businesses.

Investment in the Community

New Markets Tax Credit

A wide range of businesses are eligible for assistance, including for-profit retail, manufacturing, service businesses and nonprofit businesses.

Residential rental housing is specifically excluded.

Qualifying Businesses

New Markets Tax Credit

A qualifying business must meet the following criteria: It must derive at least 50% of its total gross income from

activities in a low income community; A substantial portion of its tangible personal property must

be used in a low income community; Its employees must perform a substantial portion of their

services in a low income community; and Less than 5% of its property is attributable to:

Collectibles; and Nonqualified financial property

Qualifying Businesses

New Markets Tax Credit

A "low income community" is defined as a census tract where: the poverty rate exceeds 20%; or the median income is below 80% of the greater of:

Statewide median income; or Metropolitan area median income (for metropolitan

tracts only)

Qualifying Businesses

New Markets Tax Credit

The NMTC is intended to enhance investor returns. NMTCs alone do not generate sufficient returns to

make investing in CDEs attractive to investors. Thus, in addition to the tax credits, investors will

need substantial cash flow and/or capital appreciation to generate a reasonable return.

As illustrated in the prior example, a $1 million investment would yield only $390,000 in NMTCs, having a $300,000 present value.

Investor's Incentive

New Markets Tax Credit

The NMTC can be combined with other federal and state nontax subsidies.

However, the ability to combine the NMTC with other federal tax benefits will be limited. The NMTC cannot be combined with: Low-income housing tax credits Tax-exempt bonds

Combing the NMTC with Other Subsidies

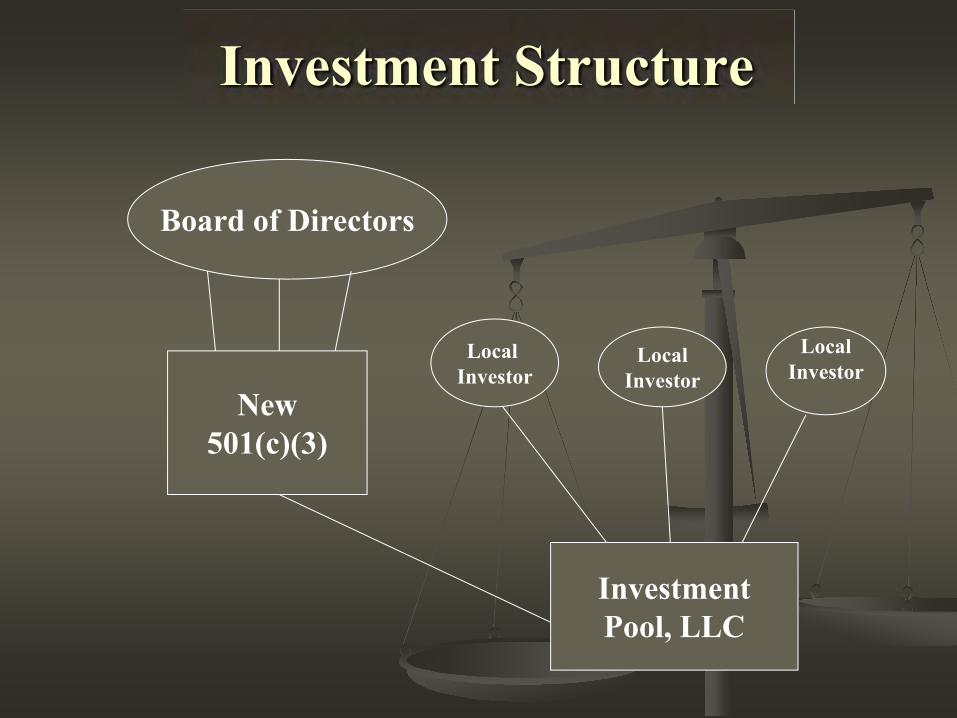

Investment Structure

Board of Directors

Local Investor

LocalInvestor

LocalInvestor

New501(c)(3)

InvestmentPool, LLC

Investment Structure(Example)

Investment: $1,200,000Admin fee to CDE (7%) ( 84,000)Reserve held by CDE ( 116,000)

Net Loan to Grocery $1,000,000

Investment Structure(Example)

Investment: $1,200,000Admin fee to CDE (7%) ( 84,000)Reserve held by CDE ( 116,000)

Net Loan to Grocery $1,000,000

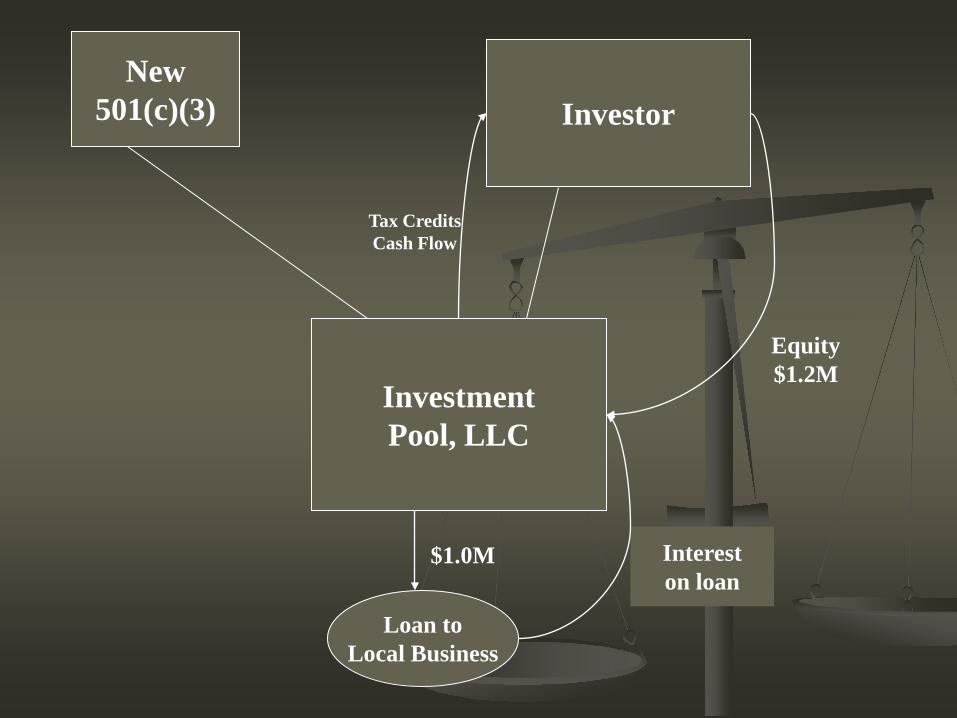

InvestmentPool, LLC

Loan toLocal Business

New501(c)(3) Investor

Tax CreditsCash Flow

Equity$1.2M

Intereston loan

$1.0M

Return to Investor

InvestmentYear Credits Interest Return

1,200,0001 50,000 30,000 6.67%2 50,000 30,000 6.67%

3 50,000 30,000 6.67%

4 60,000 30,000 7.50%

5 60,000 30,000 7.50%

6 60,000 30,000 7.50%

7 60,000 30,000 7.50%

* Principal/Reduction also begins in year 8

8 -0- 70,000 7%

9 -0- 70,000 7%

10 -0- 70,000 7%