regional daily ytl power 1.500 (0.7) 31 -...

TRANSCRIPT

REGIONAL DAILY

December 26, 2012

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT.

MALAYSIA

Malaysia Daybreak | 3 June 2014

▌What’s on the Table…

——————————————————————————————————————————————————————————————————————

Strategy - 1Q14 results leave much to be desired

Despite the strong 1Q real GDP growth of 6.2%, the May results season was another disappointment as the revision ratio declined from 0.56x to 0.41x. Earnings misses came from across the board, including from the telco, oil & gas and banking sectors. No changes to our end-2014 KLCI target of 2,030 points, based on a bottom-up valuation. Our preference for the Economic Transformation Programme (ETP) winners remains, i.e. the oil & gas, construction and property sectors. We also believe smaller-cap stocks will continue to outperform.

Power - Track 4A has arrived

The Energy Commission (EC) announced that Track 4A has been awarded to a consortium of YTL Power, Tenaga and SIPP Energy. The project was awarded through direct negotiations, which is likely to raise eyebrows among the public. However, we think that the Energy Commission (EC) resorted to direct negotiations on the premise that the Malaysian power grid could be at risk of outages by 2018 and thus planting up should be fast-tracked. We believe that the award will not be seen as a lopsided agreement which would leave Tenaga and the public paying more as Tenaga is part of the consortium. We maintain our Overweight position on the sector.

YTL Power International - A comeback through 4A

YTL Power's involvement in the consortium that was awarded Track 4A is highly positive for the company as this implies that it will remain a Malaysian independent power producer (IPP) after the expiry of its existing power purchase agreement (PPA) in 2015. While details are still scarce, we estimate that once the plant is completed in 2018, it would contribute c.10-11% of additional earnings to YTL Power's bottomline, and boost its target price by RM0.25-0.40. We make no changes to our earnings forecasts and SOP-based target price for now. We think this win would likely act as a catalyst for the stock, for which we continue to have an Add call.

Star Publications - Expanding beyond print

Management remains upbeat about the group’s growth prospects driven by its various initiatives to expand beyond the print segment. In a briefing yesterday, the company shared its strategy to address the decline in print and its focus on the digital platform for growth. We maintain our Hold call on the stock with a higher target price of RM2.65, based on 13.7x CY15 P/E,(15% discount to our implied target market P/E of 16.1x (vs 20% previous), as we are seeing improving earnings diversification strategy from lowering its dependency on print and higher potential for earnings contribution from TV, radio and outdoor segments. The stock offers a decent FY14 yield of 5.7%. Switch to Astro for exposure to the media sector.

▌News of the Day…

——————————————————————————————————————————————————————————————————————

• EPF received six submissions for Project MX-1, the town centre in Kwasa Damansara

• Industry players question award of Track 4A power plant via direct negotiations

• Mah Sing increase GDV of Southville City@KL South project by 62% to RM8.3bn

• Alam Maritim shareholders green-light for the entry of Tan Sri Quek and Paul Poh

• Farm’s Best is “still working on” the proposed RTO by SHH (M) Holdings S/B

• US ISM factory index rose to 55.4 in May from 54.9 in Apr

Sources: CIMB. COMPANY REPORTS

Sources: CIMB. COMPANY REPORTS

Key Metrics

FBMKLCI Index

1,650

1,700

1,750

1,800

1,850

1,900

Jun-13 Aug-13 Oct-13 Dec-13 Feb-14 Apr-14 Jun-14

———————————————————————————

FBMKLCI

1864.25 -9.13pts -0.49%June Futures July Futures

1867 - (-0.53% ) 1868 - (1.00% )———————————————————————————

Gainers Losers Unchanged297 516 298

———————————————————————————

Turnover1331.66m shares / RM1953.907m

3m avg volume traded 1884.69m shares

3m avg value traded RM2143.72m———————————————————————————

Regional IndicesFBMKLCI FSSTI JCI SET HSI

1,864 3,302 4,912 1,441 23,082 ————————————————————————————————

Close % chg YTD % chg

FBMKLCI 1,864.25 (0.5) (0.1)

FBM100 12,546.09 (0.4) (0.3)

FBMSC 17,443.10 (0.1) 11.1

FBMMES 6,564.01 (0.3) 15.6

Dow Jones 16,743.63 0.2 1.0

NASDAQ 4,237.20 (0.1) 1.5

FSSTI 3,302.24 0.2 4.3

FTSE-100 6,864.10 0.3 1.7

Hang Seng 23,081.65 0.3 (1.0)

JCI 4,912.09 0.4 14.9

KOSPI 2,002.00 0.4 (0.5)

Nikkei 225 14,935.92 2.1 (8.3)

PCOMP 6,710.40 0.9 13.9

SET 1,440.94 1.8 11.0

Shanghai 2,039.21 (0.1) (3.6)

Taiwan 9,075.91 (0.4) 5.4————————————————————————————————

Close % chg Vol. (m)

SONA PETROLEUM 0.600 1.7 48.1YTL CORP BHD 1.630 0.0 44.1

HUBLINE BHD 0.050 0.0 39.2

SEAL INC 0.805 12.6 35.0

7-ELEVEN 1.610 5.2 31.8

YTL POWER 1.500 (0.7) 31.2

MAS 0.175 (2.8) 29.4

ASTRAL SUPREME 0.150 20.0 27.8————————————————————————————————

Close % chg

US$/Euro 1.3598 0.01RM/US$ (Spot) 3.2283 (0.05)

RM/US$ (12-mth NDF) 3.3014 (0.08)

OPR (% ) 2.97 (1.00)

BLR (% , CIMB Bank) 6.60 0.00

GOLD ( US$/oz) 1,244 (0.01)

WTI crude oil US spot (US$/barrel) 102.47 (0.23)

CPO spot price (RM/tonne) 2,399 (2.80)

Market Indices

Top Actives

Economic Statistics

————————————————————————————————————————

Terence WONG CFA T (60) 3 2261 9088 E [email protected]

Daybreak│Malaysia

June 3, 2014

2

Global Economic News…

The US Institute for Supply Management’s (ISM) factory index rose to 55.4 in May from 54.9 in Apr. (Bloomberg)

The final index of US manufacturing Purchasing Managers’ Index (PMI) by Markit increased to a three-month high of 56.4 in May from 55.4 in Apr. (Bloomberg)

Interest rate increases by the US Federal Reserve will depend on the economic outlook, potentially in 2015 or 2016, Chicago Fed President Charles Evans said. (WSJ)

Construction spending in US increased 0.2% mom to an annual rate of US$953.5bn in Apr (+0.6% mom in Mar). (Reuters)

Eurozone’s manufacturing PMI by Markit fell to 52.2 in Apr from 53.4 in Mar. (Bloomberg)

Japan’s capital expenditures climbed 7.4% yoy in 1Q14 (+4.0% yoy in 4Q13). (Bloomberg)

Japan’s manufacturing PMI came in at 49.9 in May (49.4 in Apr). (RTT)

India’s seasonally adjusted HSBC/Markit Manufacturing PMI was at 51.4 in May (51.3 in Apr). (WSJ)

Home-building approvals in Australia declined 5.6% mom in Apr (-4.8% mom in Mar). Building approvals rose 1.1% yoy in Apr (+20.9% yoy in Mar). (Bloomberg, WSJ)

South Korea’s May HSBC PMI fell to 49.5, against 50.2 in Apr. (WSJ)

South Korea's consumer prices (CPI) grew 1.7% yoy (+1.5% yoy in Apr) and rose 0.2% mom in May (+0.1% mom in Apr). Core inflation rose 2.2% yoy in May (+2.3% yoy in Apr). (Yonhap, Bloomberg)

Indonesia’s HSBC manufacturing PMI rose to a high of 52.4 in May from 51.1 in Apr. (WSJ)

Indonesia’s inflation rose 0.16% mom in May (-0.02% mom in Apr) and increased 7.32% yoy in May (7.25% yoy in Apr). Core inflation rose 4.825 yoy in May (4.66% yoy in Apr). (Antara News, Bloomberg)

Indonesia's trade balance slipped to a US$1.97bn deficit in Apr (US$669m surplus in Mar). Exports fell 3.16% yoy (+1.12% yoy in Mar) while imports eased 1.26% yoy in Apr (-2.44% yoy in Mar). (The Star)

Daybreak│Malaysia

June 3, 2014

3

Thailand's headline inflation rose 2.62% yoy in May (+2.45%% yoy in Apr). On month, inflation rose 0.40% mom in May (+0.50% mom in Apr). Core inflation increased 1.75% yoy in May (+1.66% yoy in Apr). (WSJ, Bloomberg)

The Thailand military junta has drawn up a list of emergency measures such as price caps on fuel and loan guarantees for small firms to kick-start an economy threatened by recession after months of political turmoil. The plan take in longer-term measures such as the development of special economic zones on the borders with Myanmar, Laos and Malaysia. (Reuters)

Vietnam’s PMI posted 52.5 in May, after climbing to a record high of 53.1 in Apr. (Thanh Nien News)

Malaysian Economic News…

Rural folk would benefit from increased development allocations for their areas with the implementation of the Goods and Services Tax (GST) from next year, said Prime Minister Datuk Seri Najib Tun Razak. He said with the implementation of GST, the government would be able to increase its revenue which could then be channelled for development purposes, especially in the rural areas. (Bernama)

Petronas' subsidiary, PRPC Water Sdn Bhd has signed a procurement, construction and commissioning contract with Konsortium Asia Baru - PPC JV (KAP) for the development of a raw water supply project in Pengerang, Johor.

The consortium, comprising Asia Baru Construction Sdn Bhd and Putra Perdana Construction Sdn Bhd, will build raw water supply facilities to support the needs of Petronas' Refinery and Petrochemical Integrated Development (RAPID) project and other facilities within its Pengerang Integrated Complex (PIC).

The water supply project known as 'PAMER' will supply 260 million litres of water per day (mld) to the PIC, of which 30 mld will be channeled for public consumption, Petronas.

PRPC Water's Director, Juniwati Rahmat Hussin this was the first major contract awarded for a project related to the PIC development after Petronas announced the final investment decision on RAPID and other facilities within the PIC on Apr 3, 2014. (Bernama)

Mydin, the supermarket chain, has assured that store-wide prices will not be raised after the implementation of the Goods and Services Tax (GST) on Apr 1, 2015. Managing Director of Mydin Mohamed Holdings Bhd Datuk Ameer Ali Mydin said a consultant has been appointed to look into all processes related to GST implementation and that prices remain unchanged. However, he said society must understand that GST at 6% would replace the Sales and Service Tax which was pegged at 16%. (Bernama)

The government is in the midst of attracting more international investments in biomedical engineering, said Secretary-General of the Ministry of International Trade and Industry (MITI), Datuk Dr Rebecca Fatima Sta Maria. "We must take advantage of our location (centre of the region), resources and the support we have from the government. "We are already the hub in Asia Pacific (for this technology). It is just a matter of encouraging more companies (to invest here)," she said. Rebecca said the development of the industry in

Daybreak│Malaysia

June 3, 2014

4

Malaysia is still at the preliminary stage and there was huge potential in various areas, specifically medical tourism. (Bernama)

Credit Guarantee Corporation Malaysia Bhd(CGC) has proposed an inital portfolio of RM30m for up to 600 SMEs as the first tranche of the BizMula-i scheme. The BizMula-i scheme extends financing to new businesses viewed as high-risk within the financial sector, CGC said. It will provide an uplift to the development of new businesses devoid of track records or collaterals. CGC President and Chief Executive Officer Datuk Wan Azhar Wan Ahmad said the Syariah-compliant scheme is unique as businesses will be directly financed by the company. Financing, he added, ranges from RM50,000 to RM300,000 with a repayment tenure of seven years. (Bernama)

The government intends to revise incentives for biogas to woo more investments in that sector and realise plans to become Asia’s biogas hub and channel more energy into the national power grid, the Malaysian Biotechnology Corporation (BiotechCorp) said.

BiotechCorp’s research revealed that the biogas industry will contribute around RM20bn to the country’s GDP growth. However, it’s contribution remains dependent on technology readiness in the next six years.

Malaysia has vast potential utilising biogas resources from palm oil mills, water treatment plants, landfills and agriculture farms. Coupling the advantages of the country’s sustainable biomass feedstock as well as the government’s focus on green and renewable technologies are the country’s strategic advantages.

The 1.9m cubic meters produced by palm oil mill effluent alone constituted 24% of Malaysia’s gas consumption. (Edge Financial Daily)

The Malaysian Plastics Manufacturers Association has submitted 10 proposals to the national Wage Consultative (NWCC) regarding the impending review of the Minimum Wage Order. The industry’s direct labour cost rose by 20-40% after implementation of the wage policy. The manufacturers were also suffering from increase in electricity tariff, transportation, raw materials, packaging and other operational costs which have resulted in the increase in total manufacturing cost by more than 10%. Majority of plastic manufacturers were unable to pass on the increase in cost to customers as the bulk of the plastic finished products were exported. (Edge Financial Daily)

The Johor government has garnered returns of RM171.1m in cash and RM2.8bn in kind from 71 privatisation projects signed up with the private sector since 1996 to develop the state, the state legislative assemble was told. Menteri Besar Datuk Seri Mohamed Khaled Nordin said the returns in kind included mixed, housing, commercial and infrastructure development. Meanwhile returns for new privatisation projects will be in cash to overcome the arrears in the returns in kind. (Edge Financial Daily)

The Federal Government is willing to negotiate Sarawak’s request to increase oil royalties from 5% to 20%, said Prime Minister Datuk Seri Najib Tun Razak. The Sarawak state assembly sitting in May approved a special motion to seek royalties from the state’s oil and gas revenue to be increased from 5% cent to 20%. (The Star)

Daybreak│Malaysia

June 3, 2014

5

Political News…

Malaysian of Chinese descent love Malaysia too, and their patriotism is reflected through daily activities, said PM Datuk Seri Najib Razak. Najib posted on his Mandarin Facebook page yesterday wishing all Malaysian Chinese a happy Rice Dumpling Festival. He also said that the Chinese here have contributed much to the country and he hopes that every Malaysian can unite and work hard for the betterment of the nation. (Star)

Corporate News…

Following Kwasa Land Sdn Bhd’s invitation to 20 prospective companies pre-qualified as tier-1 developers in March, the wholly-owned subsidiary of the Employees Provident Fund has received six submissions for Project MX-1, a town centre in the proposed Kwasa Damansara development. The entire development has a gross development value of RM50bn. Kwasa Land, the master developer of the 2,330 acres, said in a statement that the six companies with timely submission bids were Guocoland Malaysia Bhd, Malaysian Resources Corp Bhd, Putrajaya Holdings Sdn Bhd, S P Setia Bhd, UEM Sunrise Bhd and YTL Corp Bhd. These tier-1 developers are large-scale companies with shareholders’ funds or paid-up capital of RM1bn and above.

Kwasa Land said that under the qualitative evaluations, bidders were required to submit development concept and layout proposals for the MX-1 parcel based on approved plot ratio, development phasing, and unique features of the proposal complete with overall planning layout, three-dimensional massing and landscape plans.

Property sales for the whole development within the MX-1 land area should be fully completed within 12 years. Bidders were also required to submit the tender price on a per-sq-ft basis along with their financial feasibility analysis. (StarBiz)

Eco World Development Group may consider venturing into the UK, Australia, Singapore, China and Vietnam, emulating SP Setia's success in these markets since 2007. "If the opportunity comes along, why not? We have the expertise to venture overseas. We do like certain countries," said its CEO Datuk Chang Khim Wah. (BT)

Mah Sing Group Bhd has increased the gross development value (GDV) of its 428-acre (173.2ha) Southville City@KL South project in Bangi, Selangor by 62% to RM8.3bn from the initial RM5.13bn after it secured the approval of the authorities for the township's master plan, which now includes a 2km stretch of commercial development fronting the North-South Highway. The take-up rate has been encouraging for Phase 1 of Southville City@KL South, which includes the Savanna Executive Suites, with RM600m sales achieved, said Mah Sing in a statement yesterday. (The Edge)

Felda Global Ventures Holdings Bhd (FGV), via Twin Rivers Technologies-ETGO (TRT-ETGO), hopes to record around C$475m (RM1.4bn) in sales from its operations in Canada this year. “That is our target but it all depends on the commodity price,” said TRT-ETGO president and chief executive officer Karu Munusamy. Karu said the main focus is to expand the business across Canada and other key markets, and reduce operational cost. TRT-ETGO operates a canola and soyabean crushing and refining plant in Becancour Industrial Park, Quebec. (BT)

Daybreak│Malaysia

June 3, 2014

6

Industry players have questioned the award of the multi-billion ringgit Track 4A power plant project in Johor to a tripartite consortium via direct negotiations. They said if the Energy Commission insisted on awarding the contract without competitive bidding, Tenaga Nasional Bhd (TNB) alone can undertake the job, given its greater resources and fine credit standing. With assets worth nearly RM70bn, TNB is the largest power utility company in Malaysia and Southeast Asia. “I don't see any benefits of a multi-party consortium. TNB alone can do the job, given that the group has the land and AAA debt rating. I believe that the economic internal rate of return (EIRR), if TNB were to do it alone, is better than that by independent power producers (IPPs),” said a source. (StarBiz)

Malaysia Airlines is stepping up efforts to cut costs to survive, following the mysterious disappearance of its flight MH370. The second quarter this year is 'a challenge,' but the management wants to implement measures that, if successful, could enable the airline to break even in 2015. "I don't think there will be any sacred cows," said Hugh Dunleavy, the carrier's director of commercial operations. "Every part of the airline will have to be looked at carefully."

Dunleavy declined to comment on suggestions that MAS could be taken private or that it might sell off its engineering business, but he added that there were other things that the airline could do. These included cutting 'legacy costs' that have been in place for "the last 10 to 20 years", he said.

The cargo unit's business model is also being re-assessed, with the airline possibly selling some freighters if it can find a buyer. MAS had planned to order new passenger aircraft, including Airbus A330s and A350s, before MH370 went missing. That plan has been put on hold, although the airline could acquire some A330s on lease to replace ageing Boeing 777-200s, the sources said. The airline could also reconfigure the cabin to add more business class seats to increase revenue yield.

Revenues were hit after the MH370 disaster in part because the airline stopped all promotional and marketing activity. This resumed in the first week of May, and forward bookings have returned to pre-MH370 levels in most markets, said Dunleavy.

Average fare yields, however, remain under pressure due to competition from other full-service airlines in Asia and the Middle East, as well as low-cost carriers AirAsia and AirAsia X in Malaysia. The airline continues to burn cash, but Dunleavy said he remained confident that management can turn the business round. "We have to look at the business model that will allow us to be sustainable over the next 40 years," he said. (Reuters)

The International Air Transport Association (IATA) is planning to put aircraft tracking proposals to the UN's International Civil Aviation Organization (ICAO) in September, which in turn says a standard could be in place in two to three years. However, individual airlines could move sooner than that, Tyler said. "It is the sort of issue where before regulations actually start to bite, airlines will already have made arrangements, they aren't going to wait," Tony Tyler, director general of IATA said. Qatar Airways, hosting the meeting, said the technology to track planes was available today, citing the possible adaptation to tracking of the existing ACARS Aircraft Communications Addressing and Reporting System as an example, which can deliver communication in short bursts, although it is not continual. "Qatar is keen to explore this," Chief Executive Akbar al Baker told reporters. Industry sources also said Malaysia Airlines was already looking at options that it will implement as soon as possible across its fleet. For airlines though, a big issue will be ensuring costs for any technology do not spiral out of control, given the industry's already tight profit margins. (Reuters)

Daybreak│Malaysia

June 3, 2014

7

AirAsia Bhd has clarified that it is currently in the midst of obtaining the necessary approvals for its new office building at KLIA2 in Sepang, denying claims that the delay is due to funding issues. "AirAsia would like to clarify that we are in the midst of obtaining approvals from local authorities for our new office building at KLIA2 and do not face any funding issues," said Aireen Omar, CEO of AirAsia.

The airline explained that it had been requested to reduce the height of its new building when the control tower at KLIA2 was relocated to a new site upon instruction by the authorities. "As a result of the reduced height, the original site and plan for the new office building became structurally uneconomical. A new site had to be identified, and plans had to be redrawn and resubmitted for approval which had adjusted the timeline of the new office building significantly for AirAsia," the airline's statement said. (Financial Daily)

Supported by favorable export taxation to attract investment, Indonesia, the world’s largest palm oil producer, has the potential to become the production base for several downstream palm oil products, stakeholders say. The main potential lay in the surfactant industry, which could nearly triple added-value of crude palm oil (CPO), according to the Industry Ministry’s director general for agriculture and chemical industries, Panggah Susanto.

Surfactant is a chemical compound used in detergents, soaps and cosmetics. “We have the potential to serve as the manufacturing base for surfactants, but we are not yet in an optimal position to develop the product, despite the huge potential,” Panggah said. (Jakarta Post)

Malaysian palm oil futures fell for a seventh straight session on Monday to hit their lowest in nearly seven-and-a-half months, as weak soyoil prices and disappointing export data dragged on the tropical oil. The benchmark August contract on the Bursa Malaysia Derivatives Exchange fell to RM2,386 in early trade, its weakest since Oct. 18, 2013, before settling at RM2,389 (US$741) per tonne by the midday break, down 1.4%.

Market participants said although demand for palm oil improved in May compared to April, the export growth slowed down towards the end of the month, signalling dwindling demand for the tropical oil despite a major festival just around the corner. "Fundamentally, palm itself is not so bearish. But there are people who feel that the export pace has not been too friendly," said a trader with a foreign commodities brokerage. "We were expecting exports to maintain a very good pace until the end of the month. But the ITS number shows that it did not materialise," the Kuala Lumpur-based trader added.

Cargo surveyor Intertek Testing Services (ITS) reported that a total of 1,315,952 tonnes of Malaysian palm oil products were shipped in May, 7.8% higher month-on-month, but slower than the 23% jump recorded in the May 1-15 period. (Reuters)

Shareholders of Alam Maritim have green-lit the entry of banking tycoon Tan Sri Quek Leng Chan and his lieutenant Paul Poh as the second-largest shareholders of the offshore support vessel firm. Quek, via Associated Land Sdn Bhd, had agreed in late Apr to take up 60m new shares for RM81m and Poh’s Caprice Capital International Ltd 63m shares worth RM85.05m via a placement. They will hold a combined 15.53% interest, unseating Lembaga Tabung Haji as Alam's second-largest shareholder. The private placement of 123m shares at RM1.35 apiece will raise RM166.05m for Alam to buy a diving support ship and pare down borrowings. (Star)

Daybreak│Malaysia

June 3, 2014

8

Permodalan Nasional Bhd (PNB), which owns 47.7% of NCB Holdings Bhd, has been tipped to bag the proposed third container terminal project in Port Klang, Selangor, according to sources close to the matter. "The transport ministry is currently deciding whom the award should go to and NCB is regarded as being the strongest contender for the contract award," a source said. "The proposed third terminal is necessary, and the operator should be an experienced Port Klang operator and not an outsider," the source said. It is understood the award would grant NCB a 30-year concession to develop and operate the proposed third terminal. (Financial Daily)

Only those with a monthly income of below RM5,000 and cars with an engine capacity below 2,000cc will be entitled to unrestricted purchase of subsidised petrol under the new petrol subsidy system, according to a report by Sin Chew Daily. The report said the target is to launch the new system in 3Q14. Those who earn RM5,000-10,000 per month will only be able to purchase 300 litres of subsidised diesel and RON95 petrol per month. Those with a monthly income of RM10,000 and above will have to purchase RON97 petrol, which will be based on market prices and without an subsidy. In addition, foreigners and those with foreign registered cars will not be able to buy subsidised petrol. (Financial Daily)

A total of 200 companies have registered with Puncak Semangat Sdn Bhd to participate in the closed tender for various contracts for the Digital Terrestrial TV (DTTV) infrastructure and network facilities implementation, said its deputy project director Mohamed Redzwan Yahya. "About 200 companies have registered with us to participate in this tender. We will review their capacity," he told.

He said the 200 companies are interested in various packages, including 20 set-top box (STB) manufacturers who are looking to participate in the two million STBs that Puncak Semangat will provide to eligible recipients in rural areas. It was reported that the contracts include 16 packages spread under seven categories and only companies (local and international) offering products and services that suit Puncak Semangat's strategy will be invited for the closed tender. "We have specifications for the STBs.

Whoever is interested must meet our specifications. We have 20 STB manufacturers to supply the STBs. We'll shortlist, review and negotiate the prices," said Redzwan. (The Sun)

Puncak Semangat Sdn Bhd is investing RM2bn in capital expenditure (capex) and RM2.5bn in operational expenditure over 15 years to implement the Digital Terrestrial TV (DTTV) infrastructure and network facilities. Puncak Semangat project director Nik Abdul Aziz Nik Yaacob said it will spend RM1.5bn to RM1.6bn of the capex during the first seven years to set up the infrastructure and facilities including the set-top boxes (STB) and the remaining capex will be spent over the remaining eight years.

He said the bulk of the capex will be spent on new equipment for the transmitter sites and about 30% to 40% will be spent on the STBs. "For now we are funding it internally. As we move forward, we are definitely looking at all the possible funding avenues be it equity funding, borrowings and what not," he told. (The Sun)

Daybreak│Malaysia

June 3, 2014

9

Four groups, including MTD Capital Bhd, bid for a 35.4bn pesos (RM2.64bn) state contract to build and operate a toll road meant to decongest traffic in industrial zones south of Manila under a public-private partnership (PPP) programme, the Philippine government said. The winner of the contract, the Philippines’ most expensive road project under the PPP scheme so far, would be announced at a later date as bids would first be reviewed for technical evaluation, Public Works Secretary Rogelio Singson told investors during the auction yesterday.

Among those who submitted bids are a consortium formed by Ayala Corp and Aboitiz Equity Ventures Inc, and the grouping of Metro Pacific Investments Corp, DMCI Holdings Inc and Leighton Holdings Inc. Besides the two groupings, San Miguel Corp and Malaysia’s MTD also made bids.

The 35-year contract to finance, design, construct, and operate a 47km four-lane toll road connecting two expressways south of the capital is part of government efforts to address the South-East Asian nation’s infrastructure backlog. The Asian Development Bank said in a report last year that the country needs US$20bn (RM65bn) annually in infrastructure investment to sustain economic growth, attract direct investment and alleviate poverty. (StarBiz)

Protasco Bhd’s wholly-owned subsidiary HCM Engineering Sdn Bhd has bagged a RM21m contract from the Public Works Department to undertake maintenance works on federal roads in Zone 2A, Sarawak. The company said the award encompasses construction of overtaking lanes from Sibu to Bintulu and from Bintulu to Tatau. (StarBiz)

Farm’s Best Bhd is “still working on” the proposed reverse takeover (RTO) by SHH (M) Holdings Sdn Bhd, which will see its existing share base being reduced to 6.42% of its enlarged paid-up capital upon the completion of a series of corporate exercises. Firstly, 760m new shares of 50 sen each will be issued to SHH (M) Holdings. This will be followed by a special issuance of 130m shares at 50 sen each, which the company would utilise as part of its working capital.

SHH (M) Holdings would inject its poultry business in China through the RM380m transaction, while RM65m more would be raised via the special issuance. Farm’s Best corporate affairs general manager K. T. Hoh told StarBiz: “Currently, the company is in the midst of finalising the due diligence process on SHH (M) Holdings.” (StarBiz)

Taliworks Corp Bhd’s unit will secure higher fees for its wastewater treatment services in China’s Yinchuan city upon the completion of upgrading and expansion works for one of its plants there by mid-2015. The water infrastructure company said its unit, Taliworks (Yinchuan) Wastewater Treatment Co Ltd, had entered into a head of agreement (HoA) with the Yinchuan City Construction Bureau for the upgrading and expansion works on four of its wastewater treatment plants in the city in the Ningxia Hui Autonomous Region at a total investment of 900m yuan (RM464.5m).

Taliworks Yinchuan is a wholly-owned subsidiary of Taliworks International Ltd, which, in turn, is a wholly-owned subsidiary of Taliworks. Under the HoA, which was signed last Saturday, the improvement works on Yinchuan City Waste Water Treatment Plant Nos 1, 2, 3 and 4 would be carried out over four years, with stages of completion from January 2014 to Dec 2017. (StarBiz)

Daybreak│Malaysia

June 3, 2014

10

Credit Guarantee Corp Malaysia Bhd (CGC) has proposed an initial portfolio of RM30m for up to 600 small and medium enterprises (SMEs) as the first tranche of the BizMula-i scheme. The scheme extends financing to new businesses viewed as high risk within the financial sector, according to CGC in a statement. It will provide an uplift to the development of new businesses devoid of track record or collateral. Its underlying principal is to encourage and nurture budding businessmen with reliable business plans, satisfactory business insights and a high entrepreneurship drive. Financing ranges between RM50,000 to RM300,000 with a repayment tenure of seven years. (BT)

Bank Islam plans to raise RM1bn by selling Islamic bonds to fund organic growth as well as a potential acquisition in Indonesia, two people involved in the sale told Reuters . The sale of the Basel-III compliant Tier 2 sukuk is awaiting approval from the central bank by next week ahead of the final green light from the Securities Commission, said the person who declined to be identified as the matter was not yet public. (BT)

Daybreak│Malaysia

June 3, 2014

11

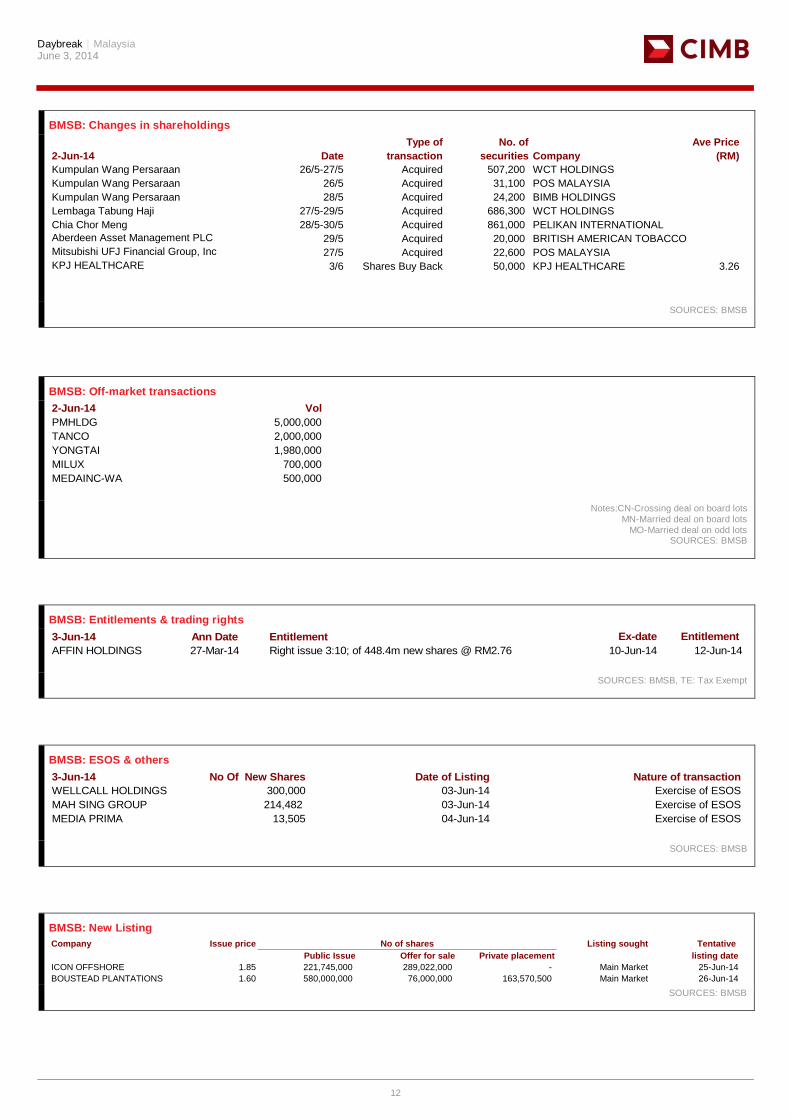

BMSB: Changes in shareholdings

Type of No of Ave Price

2-Jun-14 Date transaction securities Company (RM)

EPF 28/5 Disposed 4,548,600 PUBLIC BANK

EPF 28/5 Disposed 2,450,000 YTL CORPORATION

EPF 28/5 Disposed 2,356,300 SAPURAKENCANA PETROLEUM

EPF 28/5 Disposed 1,934,500 AMMB HOLDINGS

EPF 27/5-28/5 Disposed 1,341,300 CIMB GROUP

EPF 28/5 Disposed 1,283,400 SIME DARBY

EPF 28/5 Disposed 1,048,000 ALLIANCE FINANCIAL GROUP

EPF 28/5 Disposed 1,000,000 BURSA MALAYSIA

EPF 28/5 Disposed 897,500 FELDA GLOBAL VENTURES

EPF 28/5 Disposed 870,000 WAH SEONG CORPORATION

EPF 28/5 Disposed 800,000 BUMI ARMADA

EPF 28/5 Disposed 515,700 IJM LAND

EPF 28/5 Disposed 328,300 IJM CORPORATION

EPF 28/5 Disposed 201,200 IOI CORPORATION

EPF 28/5 Disposed 200,000 PRESTARIANG

EPF 28/5 Disposed 165,000 PETRONAS GAS

EPF 28/5 Disposed 111,100 AEON CO. (M)

EPF 28/5 Disposed 51,400 ORIENTAL HOLDINGS

EPF 28/5 Disposed 4,800 BIMB HOLDINGS

Kumpulan Wang Persaraan 27/5 Disposed 2,072,600 IJM CORPORATION

Kumpulan Wang Persaraan 26/5 Disposed 832,300 GAMUDA

Kumpulan Wang Persaraan 26/5-27/5 Disposed 491,000 TIME DOTCOM

Kumpulan Wang Persaraan 26/5-27/5 Disposed 220,300 PETRONAS GAS

Kumpulan Wang Persaraan 27/5 Disposed 53,600 BOUSTEAD HOLDINGS

Kumpulan Wang Persaraan 27/5 Disposed 49,300 KULIM (MALAYSIA)

Kumpulan Wang Persaraan 26/5-27/5 Disposed 49,100 FELDA GLOBAL VENTURES

Lembaga Tabung Haji 27/5-29/5 Disposed 395,900 FABER GROUP

GIC Private Limited 28/5-30/5 Disposed 3,372,374 PARKSON HOLDINGS

Aberdeen Asset Management PLC 29/5 Disposed 29,700 SHANGRI-LA HOTELS

Mitsubishi UFJ Financial Group, Inc 27/5 Disposed 119,400 CIMB GROUP

Mitsubishi UFJ Financial Group, Inc 27/5 Disposed 14,000 SHANGRI-LA HOTELS

Mitsubishi UFJ Financial Group, Inc 27/5 Disposed 500 BRITISH AMERICAN TOBACCO

EPF 2/5-22/5 Acquired 4,446,800 UMW OIL & GAS CORPORATION

EPF 28/5 Acquired 4,400,000 AXIATA GROUP

EPF 28/5 Acquired 3,731,500 TELEKOM MALAYSIA

EPF 28/5 Acquired 1,735,000 GAMUDA

EPF 28/5 Acquired 1,658,900 DIGI.COM

EPF 28/5 Acquired 1,460,600 AIRASIA

EPF 28/5 Acquired 1,374,200 IHH HEALTHCARE

EPF 28/5 Acquired 1,000,000 IOI PROPERTIES GROUP

EPF 28/5 Acquired 1,000,000 SUNWAY REIT

EPF 28/5 Acquired 1,000,000 UEM SUNRISE

EPF 28/5 Acquired 760,800 MAXIS

EPF 28/5 Acquired 499,700 HONG LEONG BANK

EPF 28/5 Acquired 434,700 MALAYAN BANKING

EPF 28/5 Acquired 335,500 KUALA LUMPUR KEPONG

EPF 28/5 Acquired 200,000 KPJ HEALTHCARE

EPF 28/5 Acquired 170,000 GENTING PLANTATIONS

EPF 28/5 Acquired 170,000 LAFARGE MALAYSIA

EPF 28/5 Acquired 133,100 AL-`AQAR HEALTHCARE REIT

EPF 28/5 Acquired 112,100 KOSSAN RUBBER INDUSTRIES

EPF 28/5 Acquired 99,000 AXIS REIT

EPF 28/5 Acquired 76,300 DIALOG GROUP

EPF 28/5 Acquired 65,100 TAN CHONG MOTOR

EPF 26/5 Acquired 56,000 LITRAK

EPF 28/5 Acquired 39,100 TIME DOTCOM

EPF 28/5 Acquired 34,100 TOP GLOVE CORPORATION

SOURCES: BMSB

Daybreak│Malaysia

June 3, 2014

12

BMSB: Changes in shareholdings

Type of No. of Ave Price

2-Jun-14 Date transaction securities Company (RM)

Kumpulan Wang Persaraan 26/5-27/5 Acquired 507,200 WCT HOLDINGS

Kumpulan Wang Persaraan 26/5 Acquired 31,100 POS MALAYSIA

Kumpulan Wang Persaraan 28/5 Acquired 24,200 BIMB HOLDINGS

Lembaga Tabung Haji 27/5-29/5 Acquired 686,300 WCT HOLDINGS

Chia Chor Meng 28/5-30/5 Acquired 861,000 PELIKAN INTERNATIONAL

Aberdeen Asset Management PLC 29/5 Acquired 20,000 BRITISH AMERICAN TOBACCO

Mitsubishi UFJ Financial Group, Inc 27/5 Acquired 22,600 POS MALAYSIA

KPJ HEALTHCARE 3/6 Shares Buy Back 50,000 KPJ HEALTHCARE 3.26

SOURCES: BMSB

BMSB: Off-market transactions

2-Jun-14 Vol

PMHLDG 5,000,000

TANCO 2,000,000

YONGTAI 1,980,000

MILUX 700,000

MEDAINC-WA 500,000

Notes:CN-Crossing deal on board lots

MN-Married deal on board lots MO-Married deal on odd lots

SOURCES: BMSB

BMSB: Entitlements & trading rights

3-Jun-14 Ann Date Entitlement Ex-date Entitlement

AFFIN HOLDINGS 27-Mar-14 Right issue 3:10; of 448.4m new shares @ RM2.76 10-Jun-14 12-Jun-14

SOURCES: BMSB, TE: Tax Exempt

BMSB: ESOS & others

3-Jun-14 No Of New Shares Date of Listing Nature of transaction

WELLCALL HOLDINGS 300,000 03-Jun-14 Exercise of ESOS

MAH SING GROUP 214,482 03-Jun-14 Exercise of ESOS

MEDIA PRIMA 13,505 04-Jun-14 Exercise of ESOS

SOURCES: BMSB

BMSB: New Listing

Company Issue price Listing sought Tentative

Public Issue Offer for sale Private placement listing date

ICON OFFSHORE 1.85 221,745,000 289,022,000 - Main Market 25-Jun-14

BOUSTEAD PLANTATIONS 1.60 580,000,000 76,000,000 163,570,500 Main Market 26-Jun-14

No of shares

SOURCES: BMSB

Daybreak│Malaysia

June 3, 2014

13

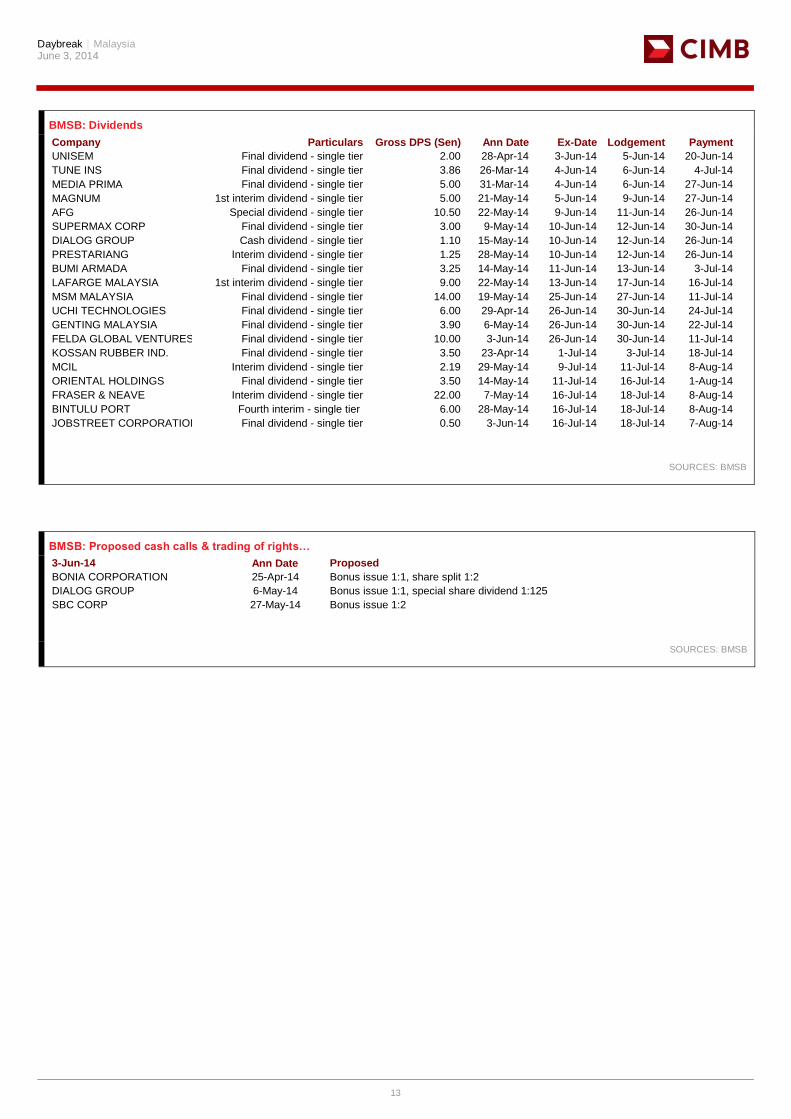

BMSB: Dividends

Company Particulars Gross DPS (Sen) Ann Date Ex-Date Lodgement Payment

UNISEM Final dividend - single tier 2.00 28-Apr-14 3-Jun-14 5-Jun-14 20-Jun-14

TUNE INS Final dividend - single tier 3.86 26-Mar-14 4-Jun-14 6-Jun-14 4-Jul-14

MEDIA PRIMA Final dividend - single tier 5.00 31-Mar-14 4-Jun-14 6-Jun-14 27-Jun-14

MAGNUM 1st interim dividend - single tier 5.00 21-May-14 5-Jun-14 9-Jun-14 27-Jun-14

AFG Special dividend - single tier 10.50 22-May-14 9-Jun-14 11-Jun-14 26-Jun-14

SUPERMAX CORP Final dividend - single tier 3.00 9-May-14 10-Jun-14 12-Jun-14 30-Jun-14

DIALOG GROUP Cash dividend - single tier 1.10 15-May-14 10-Jun-14 12-Jun-14 26-Jun-14

PRESTARIANG Interim dividend - single tier 1.25 28-May-14 10-Jun-14 12-Jun-14 26-Jun-14

BUMI ARMADA Final dividend - single tier 3.25 14-May-14 11-Jun-14 13-Jun-14 3-Jul-14

LAFARGE MALAYSIA 1st interim dividend - single tier 9.00 22-May-14 13-Jun-14 17-Jun-14 16-Jul-14

MSM MALAYSIA Final dividend - single tier 14.00 19-May-14 25-Jun-14 27-Jun-14 11-Jul-14

UCHI TECHNOLOGIES Final dividend - single tier 6.00 29-Apr-14 26-Jun-14 30-Jun-14 24-Jul-14

GENTING MALAYSIA Final dividend - single tier 3.90 6-May-14 26-Jun-14 30-Jun-14 22-Jul-14

FELDA GLOBAL VENTURES Final dividend - single tier 10.00 3-Jun-14 26-Jun-14 30-Jun-14 11-Jul-14

KOSSAN RUBBER IND. Final dividend - single tier 3.50 23-Apr-14 1-Jul-14 3-Jul-14 18-Jul-14

MCIL Interim dividend - single tier 2.19 29-May-14 9-Jul-14 11-Jul-14 8-Aug-14

ORIENTAL HOLDINGS Final dividend - single tier 3.50 14-May-14 11-Jul-14 16-Jul-14 1-Aug-14

FRASER & NEAVE Interim dividend - single tier 22.00 7-May-14 16-Jul-14 18-Jul-14 8-Aug-14

BINTULU PORT Fourth interim - single tier 6.00 28-May-14 16-Jul-14 18-Jul-14 8-Aug-14

JOBSTREET CORPORATION Final dividend - single tier 0.50 3-Jun-14 16-Jul-14 18-Jul-14 7-Aug-14

SOURCES: BMSB

BMSB: Proposed cash calls & trading of rights…

3-Jun-14 Ann Date Proposed

BONIA CORPORATION 25-Apr-14 Bonus issue 1:1, share split 1:2

DIALOG GROUP 6-May-14 Bonus issue 1:1, special share dividend 1:125

SBC CORP 27-May-14 Bonus issue 1:2

SOURCES: BMSB

Daybreak│Malaysia

June 3, 2014

14

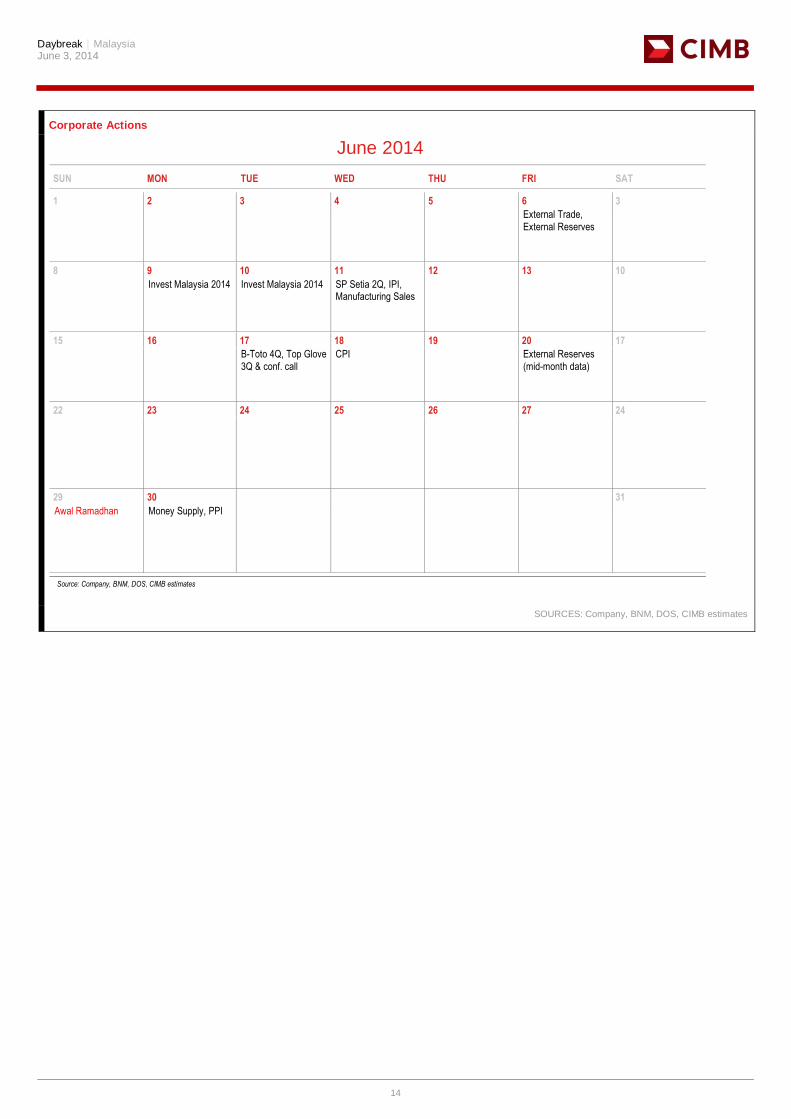

Corporate Actions

June 2014

SUN MON TUE WED THU FRI SAT

1 2 3 4 5 6 3

External Trade,

External Reserves

8 9 10 11 12 13 10

Invest Malaysia 2014 Invest Malaysia 2014 SP Setia 2Q, IPI, Manufacturing Sales

15 16 17 18 19 20 17

B-Toto 4Q, Top Glove

3Q & conf. call

CPI External Reserves

(mid-month data)

22 23 24 25 26 27 24

29 30 31

Awal Ramadhan Money Supply, PPI

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak│Malaysia

June 3, 2014

15

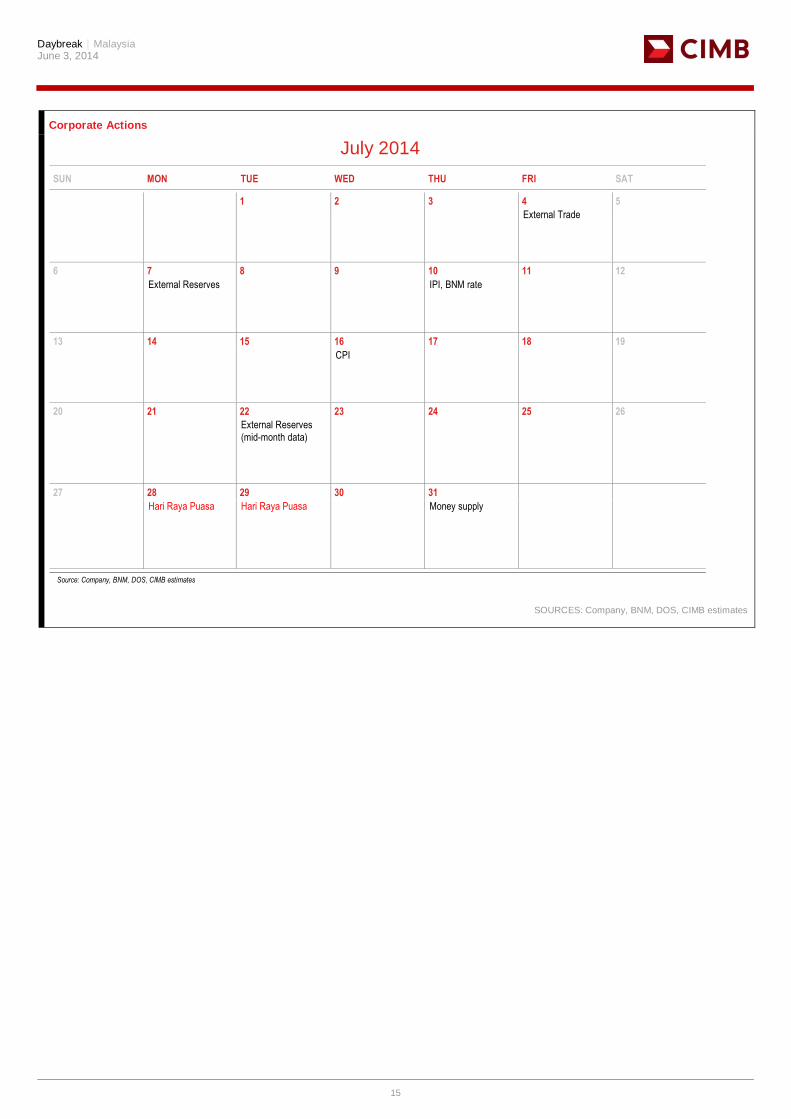

Corporate Actions

July 2014

SUN MON TUE WED THU FRI SAT

1 2 3 4 5

External Trade

6 7 8 9 10 11 12

External Reserves IPI, BNM rate

13 14 15 16 17 18 19

CPI

20 21 22 23 24 25 26

External Reserves

(mid-month data)

27 28 29 30 31

Hari Raya Puasa Hari Raya Puasa Money supply

Source: Company, BNM, DOS, CIMB estimates

SOURCES: Company, BNM, DOS, CIMB estimates

Daybreak│Malaysia

June 3, 2014

16

DISCLAIMER

This report is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

By accepting this report, the recipient hereof represents and warrants that he is entitled to receive such report in accordance with the restrictions set forth below and agrees to be bound by the limitations contained herein (including the ―Restrictions on Distributions‖ set out below). Any failure to comply with these limitations may constitute a violation of law. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this report may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

Unless otherwise specified, this report is based upon sources which CIMB considers to be reasonable. Such sources will, unless otherwise specified, for market data, be market data and prices available from the main stock exchange or market where the relevant security is listed, or, where appropriate, any other market. Information on the accounts and business of company(ies) will generally be based on published statements of the company(ies), information disseminated by regulatory information services, other publicly available information and information resulting from our research.

Whilst every effort is made to ensure that statements of facts made in this report are accurate, all estimates, projections, forecasts, expressions of opinion and other subjective judgments contained in this report are based on assumptions considered to be reasonable as of the date of the document in which they are contained and must not be construed as a representation that the matters referred to therein will occur. Past performance is not a reliable indicator of future performance. The value of investments may go down as well as up and those investing may, depending on the investments in question, lose more than the initial investment. No report shall constitute an offer or an invitation by or on behalf of CIMB or its affiliates to any person to buy or sell any investments.

CIMB, its affiliates and related companies, their directors, associates, connected parties and/or employees may own or have positions in securities of the company(ies) covered in this research report or any securities related thereto and may from time to time add to or dispose of, or may be materially interested in, any such securities. Further, CIMB, its affiliates and its related companies do and seek to do business with the company(ies) covered in this research report and may from time to time act as market maker or have assumed an underwriting commitment in securities of such company(ies), may sell them to or buy them from customers on a principal basis and may also perform or seek to perform significant investment banking, advisory, underwriting or placement services for or relating to such company(ies) as well as solicit such investment, advisory or other services from any entity mentioned in this report.

CIMB or its affiliates may enter into an agreement with the company(ies) covered in this report relating to the production of research reports. CIMB may disclose the contents of this report to the company(ies) covered by it and may have amended the contents of this report following such disclosure.

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his or her personal views and opinions about any and all of the issuers or securities analysed in this report and were prepared independently and autonomously. No part of the compensation of the analyst(s) was, is, or will be directly or indirectly related to the inclusion of specific recommendations(s) or view(s) in this report. CIMB prohibits the analyst(s) who prepared this research report from receiving any compensation, incentive or bonus based on specific investment banking transactions or for providing a specific recommendation for, or view of, a particular company. Information barriers and other arrangements may be established where necessary to prevent conflicts of interests arising. However, the analyst(s) may receive compensation that is based on his/their coverage of company(ies) in the performance of his/their duties or the performance of his/their recommendations and the research personnel involved in the preparation of this report may also participate in the solicitation of the businesses as described above. In reviewing this research report, an investor should be aware that any or all of the foregoing, among other things, may give rise to real or potential conflicts of interest. Additional information is, subject to the duties of confidentiality, available on request.

Reports relating to a specific geographical area are produced by the corresponding CIMB entity as listed in the table below. The term ―CIMB‖ shall denote, where appropriate, the relevant entity distributing or disseminating the report in the particular jurisdiction referenced below, or, in every other case, CIMB Group Holdings Berhad ("CIMBGH") and its affiliates, subsidiaries and related companies.

Country CIMB Entity Regulated by

Australia CIMB Securities (Australia) Limited Australian Securities & Investments Commission

Hong Kong CIMB Securities Limited Securities and Futures Commission Hong Kong

Indonesia PT CIMB Securities Indonesia Financial Services Authority of Indonesia

India CIMB Securities (India) Private Limited Securities and Exchange Board of India (SEBI)

Malaysia CIMB Investment Bank Berhad Securities Commission Malaysia

Singapore CIMB Research Pte. Ltd. Monetary Authority of Singapore

South Korea CIMB Securities Limited, Korea Branch Financial Services Commission and Financial Supervisory Service

Taiwan CIMB Securities Limited, Taiwan Branch Financial Supervisory Commission

Thailand CIMB Securities (Thailand) Co. Ltd. Securities and Exchange Commission Thailand

Information in this report is a summary derived from CIMB individual research reports. As such, readers are directed to the CIMB individual research report or note to review the individual Research Analyst's full analysis of the subject company. Important disclosures relating to the companies that are the subject of research reports published by CIMB and the proprietary positions by CIMB and shareholdings of its Research Analysts’ who prepared the report in the securities of the company(s) are available in the individual research report.

The information contained in this research report is prepared from data believed to be correct and reliable at the time of issue of this report. CIMB may or may not issue regular reports on the subject matter of this report at any frequency and may cease to do so or change the periodicity of reports at any time. CIMB is under no obligation to update this report in the event of a material change to the information contained in this report. This report does not purport to contain all the information that a prospective investor may require. CIMB or any of its affiliates does not make any guarantee, representation or warranty, express or implied, as to the adequacy, accuracy, completeness, reliability or fairness of any such information and opinion contained in this report. Neither CIMB nor any of its affiliates nor its related persons shall be liable in any manner whatsoever for any consequences (including but not limited to any direct, indirect or consequential losses, loss of profits and damages) of any reliance thereon or usage thereof.

This report is general in nature and has been prepared for information purposes only. It is intended for circulat ion amongst CIMB and its affiliates’ clients generally and does not have regard to the specific investment objectives, financial situation and the particular needs of any specific person who may receive this report. The information and opinions in this report are not and should not be construed or considered as an offer, recommendation or solicitation to buy or sell the subject securities, related investments or other financial instruments thereof.

Investors are advised to make their own independent evaluation of the information contained in this research report, consider their own individual investment objectives, financial situation and particular needs and consult their own professional and financial advisers as to the legal, business, financial, tax and other aspects before participating in any transaction in respect of the securities of company(ies) covered in this research report. The securities of such company(ies) may not be eligible for sale in all jurisdictions or to all categories of investors.

Australia: Despite anything in this report to the contrary, this research is provided in Australia by CIMB Securities (Australia) Limited (―CSAL‖) (ABN 84 002 768 701, AFS Licence number 240 530). CSAL is a Market Participant of ASX Ltd, a Clearing Participant of ASX Clear Pty Ltd, a Settlement Participant of ASX Settlement Pty Ltd, and, a participant of Chi X Australia Pty Ltd. This research is only available in Australia to persons who are ―wholesale clients‖ (within the meaning of the Corporations Act 2001 (Cth)) and is supplied solely for the use of such wholesale clients and shall not be distributed or passed on to any other person. This research has been prepared without taking into account the objectives, financial situation or needs of the individual recipient.

France: Only qualified investors within the meaning of French law shall have access to this report. This report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial instruments and it is not intended as a solicitation for the purchase of any financial instrument.

Hong Kong: This report is issued and distributed in Hong Kong by CIMB Securities Limited (―CHK‖) which is licensed in Hong Kong by the Securities and Futures Commission for Type 1 (dealing in securities), Type 4 (advising on securities) and Type 6 (advising on corporate finance) activities. Any investors wishing to purchase or otherwise deal in the securities covered in this report should contact the Head of Sales at CIMB Securities Limited. The views and opinions in this research report are our own as of the date hereof and are subject to

Daybreak│Malaysia

June 3, 2014

17

change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CHK has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CHK. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CHK. Unless permitted to do so by the securities laws of Hong Kong, no person may issue or have in its possession for the purposes of issue, whether in Hong Kong or elsewhere, any advertisement, invitation or document relating to the securities covered in this report, which is directed at, or the contents of which are likely to be accessed or read by, the public in Hong Kong (except if permitted to do so under the securities laws of Hong Kong).

India: This report is issued and distributed in India by CIMB Securities (India) Private Limited (―CIMB India‖) which is registered with SEBI as a stock-broker under the Securities and Exchange Board of India (Stock Brokers and Sub-Brokers) Regulations, 1992 and in accordance with the provisions of Regulation 4 (g) of the Securities and Exchange Board of India (Investment Advisers) Regulations, 2013, CIMB India is not required to seek registration with SEBI as an Investment Adviser.

The research analysts, strategists or economists principally responsible for the preparation of this research report are segregated from the other activities of CIMB India and they have received compensation based upon various factors, including quality, accuracy and value of research, firm profitability or revenues, client feedback and competitive factors. Research analysts', strategists' or economists' compensation is not linked to investment banking or capital markets transactions performed or proposed to be performed by CIMB India or its affiliates.

Indonesia: This report is issued and distributed by PT CIMB Securities Indonesia (―CIMBI‖). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBI has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBI. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBI. Neither this report nor any copy hereof may be distributed in Indonesia or to any Indonesian citizens wherever they are domiciled or to Indonesia residents except in compliance with applicable Indonesian capital market laws and regulations.

Malaysia: This report is issued and distributed by CIMB Investment Bank Berhad (―CIMB‖). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMB has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMB. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB.

New Zealand: In New Zealand, this report is for distribution only to persons whose principal business is the investment of money or who, in the course of, and for the purposes of their business, habitually invest money pursuant to Section 3(2)(a)(ii) of the Securities Act 1978.

Singapore: This report is issued and distributed by CIMB Research Pte Ltd (―CIMBR‖). Recipients of this report are to contact CIMBR in S ingapore in respect of any matters arising from, or in connection with, this report. The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBR has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only. If the recipient of this research report is not an accredited investor, expert investor or institutional investor, CIMBR accepts legal responsibility for the contents of the report without any disclaimer limiting or otherwise curtailing such legal responsibility. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBR.

As of June 2, 2014, CIMBR does not have a proprietary position in the recommended securities in this report.

South Korea: This report is issued and distributed in South Korea by CIMB Securities Limited, Korea Branch ("CIMB Korea") which is licensed as a cash equity broker, and regulated by the Financial Services Commission and Financial Supervisory Service of Korea.

The views and opinions in this research report are our own as of the date hereof and are subject to change, and this report shall not be considered as an offer to subscribe to, or used in connection with, any offer for subscription or sale or marketing or direct or indirect distribution of financial investment instruments and it is not intended as a solicitation for the purchase of any financial investment instrument.

This publication is strictly confidential and is for private circulation only, and no part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMB Korea.

Sweden: This report contains only marketing information and has not been approved by the Swedish Financial Supervisory Authority. The distribution of this report is not an offer to sell to any person in Sweden or a solicitation to any person in Sweden to buy any instruments described herein and may not be forwarded to the public in Sweden.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Taiwan: This research report is not an offer or marketing of foreign securities in Taiwan. The securities as referred to in this research report have not been and will not be registered with the Financial Supervisory Commission of the Republic of China pursuant to relevant securities laws and regulations and may not be offered or sold within the Republic of China through a public offering or in circumstances which constitutes an offer or a placement within the meaning of the Securities and Exchange Law of the Republic of China that requires a registration or approval of the Financial Supervisory Commission of the Republic of China.

Thailand: This report is issued and distributed by CIMB Securities (Thailand) Company Limited (CIMBS). The views and opinions in this research report are our own as of the date hereof and are subject to change. If the Financial Services and Markets Act of the United Kingdom or the rules of the Financial Services Authority apply to a recipient, our obligations owed to such recipient therein are unaffected. CIMBS has no obligation to update its opinion or the information in this research report.

This publication is strictly confidential and is for private circulation only to clients of CIMBS. This publication is being supplied to you strictly on the basis that it will remain confidential. No part of this material may be (i) copied, photocopied, duplicated, stored or reproduced in any form by any means or (ii) redistributed or passed on, directly or indirectly, to any other person in whole or in part, for any purpose without the prior written consent of CIMBS.

Corporate Governance Report:

The disclosure of the survey result of the Thai Institute of Directors Association (―IOD‖) regarding corporate governance is made pursuant to the policy of the Office of the Securities and Exchange Commission. The survey of the IOD is based on the information of a company listed on the Stock Exchange of Thailand and the Market for Alternative Investment disclosed to the public and able to be accessed by a general public investor. The result, therefore, is from the perspective of a third party. It is not an evaluation of operation and is not based on inside information.

The survey result is as of the date appearing in the Corporate Governance Report of Thai Listed Companies. As a result, the survey result may be changed after that date. CIMBS does not confirm nor certify the accuracy of such survey result.

Score Range 90 – 100 80 – 89 70 – 79 Below 70 or No Survey Result

Description Excellent Very Good Good N/A

United Arab Emirates: The distributor of this report has not been approved or licensed by the UAE Central Bank or any other relevant licensing authorities or governmental agencies in the United Arab Emirates. This report is strictly private and confidential and has not been reviewed by, deposited or registered with UAE Central Bank or any other licensing authority or governmental agencies in the United Arab Emirates. This report is being issued outside the United Arab Emirates to a limited number of institutional investors and must not be provided to any person other than the original recipient and may not be reproduced or used for any other purpose. Further, the information contained in this report is not intended to lead to the

Daybreak│Malaysia

June 3, 2014

18

sale of investments under any subscription agreement or the conclusion of any other contract of whatsoever nature within the territory of the United Arab Emirates.

United Kingdom and Europe: In the United Kingdom and European Economic Area, this report is being disseminated by CIMB Securities (UK) Limited (―CIMB UK‖). CIMB UK is authorised and regulated by the Financial Services Authority and its registered office is at 27 Knightsbridge, London, SW1X 7YB. This report is for distribution only to, and is solely directed at, selected persons on the basis that those persons: (a) are persons that are eligible counterparties and professional clients of CIMB UK; (b) have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the ―Order‖); (c) are persons falling within Article 49 (2) (a) to (d) (―high net worth companies, unincorporated associations etc‖) of the Order; (d) are outside the United K ingdom; or (e) are persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000) in connection with any investments to which this report relates may otherwise lawfully be communicated or caused to be communicated (all such persons together being referred to as ―relevant persons‖). This report is directed only at relevant persons and must not be acted on or relied on by persons who are not relevant persons. Any investment or investment activity to which this report relates is available only to relevant persons and will be engaged in only with relevant persons.

Only where this report is labelled as non-independent, it does not provide an impartial or objective assessment of the subject matter and does not constitute independent "investment research" under the applicable rules of the Financial Services Authority in the UK. Consequently, any such non-independent report will not have been prepared in accordance with legal requirements designed to promote the independence of investment research and will not subject to any prohibition on dealing ahead of the dissemination of investment research.

United States: This research report is distributed in the United States of America by CIMB Securities (USA) Inc, a U.S.-registered broker-dealer and a related company of

CIMB Research Pte Ltd, CIMB Investment Bank Berhad, PT CIMB Securities Indonesia, CIMB Securities (Thailand) Co. Ltd, CIMB Securities Limited, CIMB Securities

(Australia) Limited, CIMB Securities (India) Private Limited, and is distributed solely to persons who qualify as "U.S. Institutional Investors" as defined in Rule 15a-6 under the

Securities and Exchange Act of 1934. This communication is only for Institutional Investors whose ordinary business activities involve investing in shares, bonds and

associated securities and/or derivative securities and who have professional experience in such investments. Any person who is not a U.S. Institutional Investor or Major

Institutional Investor must not rely on this communication. The delivery of this research report to any person in the United States of America is not a recommendation to

effect any transactions in the securities discussed herein, or an endorsement of any opinion expressed herein. CIMB Securities (USA) Inc, is a FINRA/SIPC member and

takes responsibility for the content of this report. For further information or to place an order in any of the above-mentioned securities please contact a registered

representative of CIMB Securities (USA) Inc.

Other jurisdictions: In any other jurisdictions, except if otherwise restricted by laws or regulations, this report is only for distribution to professional, institutional or sophisticated investors as defined in the laws and regulations of such jurisdictions.

As at the time of publishing this report CIMB is phasing in an absolute recommendation structure for stocks (Framework #1). Please refer to all frameworks for a definition of any recommendations stated in this report.

CIMB Recommendation Framework #1 Stock Ratings Definition

Add The stock’s total return is expected to exceed 10% over the next 12 months. Hold The stock’s total return is expected to be between 0% and positive 10% over the next 12 months. Reduce The stock’s total return is expected to fall below 0% or more over the next 12 months.

The total expected return of a stock is defined as the sum of the: (i) percentage difference between the target price and the current price and (ii) the forward net dividend yields of the stock. Stock price targets have an investment horizon of 12 months.

Sector Ratings Definition Overweight An Overweight rating means stocks in the sector have, on a market cap-weighted basis, a positive absolute recommendation. Neutral A Neutral rating means stocks in the sector have, on a market cap-weighted basis, a neutral absolute recommendation. Underweight An Underweight rating means stocks in the sector have, on a market cap-weighted basis, a negative absolute recommendation.

Country Ratings Definition Overweight An Overweight rating means investors should be positioned with an above-market weight in this country relative to benchmark. Neutral A Neutral rating means investors should be positioned with a neutral weight in this country relative to benchmark.

Underweight An Underweight rating means investors should be positioned with a below-market weight in this country relative to benchmark.

CIMB Stock Recommendation Framework #2 * Outperform The stock's total return is expected to exceed a relevant benchmark's total return by 5% or more over the next 12 months. Neutral The stock's total return is expected to be within +/-5% of a relevant benchmark's total return.

Underperform The stock's total return is expected to be below a relevant benchmark's total return by 5% or more over the next 12 months. Trading Buy The stock's total return is expected to exceed a relevant benchmark's total return by 3% or more over the next 3 months. Trading Sell The stock's total return is expected to be below a relevant benchmark's total return by 3% or more over the next 3 months.

* This framework only applies to stocks listed on the Singapore Stock Exchange, Bursa Malaysia, Stock Exchange of Thailand, Jakarta Stock Exchange, Australian Securities Exchange, Taiwan Stock Exchange and National Stock Exchange of India/Bombay Stock Exchange. Occasionally, it is permitted for the total expected returns to be temporarily outside the prescribed ranges due to extreme market volatility or other justifiable company or industry-specific reasons. CIMB Research Pte Ltd (Co. Reg. No. 198701620M)

CIMB Stock Recommendation Framework #3 ** Outperform Expected positive total returns of 10% or more over the next 12 months. Neutral Expected total returns of between -10% and +10% over the next 12 months. Underperform Expected negative total returns of 10% or more over the next 12 months.

Trading Buy Expected positive total returns of 10% or more over the next 3 months. Trading Sell Expected negative total returns of 10% or more over the next 3 months. ** This framework only applies to stocks listed on the Korea Exchange, Hong Kong Stock Exchange and China listings on the Singapore Stock Exchange. Occasionally, it is

permitted for the total expected returns to be temporarily outside the prescribed ranges due to extreme market volatility or other justifiable company or industry-specific reasons.

Daybreak│Malaysia

June 3, 2014

19

Corporate Governance Report of Thai Listed Companies (CGR). CG Rating by the Thai Institute of Directors Association (IOD) in 2013. AAV – Good, ADVANC - Excellent, AMATA - Very Good, ANAN – Good, AOT - Excellent, AP - Very Good, BANPU - Excellent , BAY - Excellent , BBL - Excellent, BCH – Good, BCP - Excellent, BEC - Very Good, BGH - not available, BJC – Very Good, BH - Very Good, BIGC - Very Good, BTS - Excellent, CCET – Very Good, CENTEL – Very Good, CK - Excellent, CPALL - Very Good, CPF – Excellent, CPN - Excellent, DELTA - Very Good, DTAC - Excellent, EGCO – Excellent, GLOBAL - Good, GLOW - Very Good, GRAMMY – Excellent, HANA - Excellent, HEMRAJ - Excellent, HMPRO - Very Good, INTUCH – Excellent, ITD – Very Good, IVL - Excellent, JAS – Very Good, KAMART – not available, KBANK - Excellent, KKP – Excellent, KTB - Excellent, LH - Very Good, LPN - Excellent, MAJOR – Very Good, MAKRO – Very Good, MCOT - Excellent, MINT - Excellent, PS - Excellent, PSL - Excellent, PTT - Excellent, PTTGC - Excellent, PTTEP - Excellent, QH - Excellent, RATCH - Excellent, ROBINS - Excellent, RS – Excellent, SAMART – Excellent, SC – Excellent, SCB - Excellent, SCC - Excellent, SCCC - Very Good, SIRI – Very Good, SPALI - Excellent, STA - Good, STEC - Very Good, TCAP - Excellent, THAI - Excellent, THCOM – Excellent, TICON – Very Good, TISCO - Excellent, TMB - Excellent, TOP - Excellent, TRUE - Excellent, TTW – Excellent, TUF - Very Good, VGI – Excellent, WORK – Good.