companies act 2013 accounts and audit - sirc of...

TRANSCRIPT

Companies Act 2013

Accounts and audit

By

CA. S. Santhanakrishnan

July 6 2014

“ Some changes look negative on thesurface but you will soon realize that spacesurface but you will soon realize that space

is being created in your life for something

new to emerge.”

»Eckhart Tolle

Some basics

• These are strictly my views- not my firms nor my partners and

certainly not ICAI!

• The laws are evolving

– 282 sections (98+1+183) out of 470 in New act notified

• Out of these 10 sections of Old act still continue

• New Corporate governance guidelines of SEBI are not• New Corporate governance guidelines of SEBI are not

covered here (Effective Oct 1,14)

• For Mar 14 accounts and audit, 1956 act still applies (General

circular 8 dated 4 Apr 14)

• New clarifications /amendments are quite likely

• In most cases we will have guidance from ICAI soon

• ICAI also in the process of making some representations/or

done

Matters of Concern

• Mandatory rotation should not be retrospective S 139 and

Rule 6

• Relatives should only include dependents S 141 and Rule 10

• Limit of 20 cos per auditor should not apply to private cos and• Limit of 20 cos per auditor should not apply to private cos and

clarification required regarding branches /CFS S 141(3)g)

• Internal financial control system should be limited to those

related to financial statements (as done for Board) S 143

• Additional reporting like pending litigation, foreseeable losses

for Long term contracts and derivatives etc should be

dispensed with (rule 11 –chapter X)

Matters of Concern

• Reporting of fraud- auditor requires legislation protecting

auditor against criminal /civil liability; also should be limited to

frauds which have been investigated and concluded(S

143(12))

• Prohibited services for auditors-clarification required (S 144)

• Entire firm being debarred by NFRA should be reconsidered (S

132(4))

• Auditor should not be responsible to ‘any other person’. (S147(3)(ii))

Understanding Grandfathering

• A grandfather clause is a provision in which an old rulecontinues to apply to some existing situations, while anew rule will apply to all future cases.

• Wikipedia

• This is one main issue with the New companies act and• This is one main issue with the New companies act andRules

• Some clarifications have come like accounts, audit,Section 180 regarding Borrowing powers etc

• But in many cases this is the fundamental doubt

• Is old rule applicable or new!?

SOME KEY PROVISIONS –AUDIT-CHAPTER X

OF RULES

New audit landscape

• Some will lose existing audits

• Most will gain audits and do other work

• We will all benefit by the CHANGE

– Change anyway is the only constant in the world– Change anyway is the only constant in the world

Loss of audit to one/ gain to another-1

1. Because a member of auditor ’ s HUF, spouse, father/s,

mother/s, son/s, son’s wife, daughter, daughter’s husband,brother/s, sister/s (/s for step)

• acquires /holds security >Rs 1 lakh face value

• Becomes indebted to company/subsidiary, holding,

associate, co-subsidiary for >Rs 5 lakhs

• Gives guarantee /provides security to above for >Rs 1

lakh

– And don’t take corrective action in 60 days

» Rule 10 –section 141(3)

Loss of audit to one/ gain to another-2

2. Because the auditor has business relationship with Company,

subsidiary, holding co, associate , associate or subsidiary of

holding co. and not in ordinary course, at arm’s length

– (he can use mobile service provider, travel in a plane, get

admitted in a hospital, stay in a hotel room /eat in a

restaurant of any of the above cos or do such other similarrestaurant of any of the above cos or do such other similar

business. he can also do what is permitted by ICAI)

• S 141(3) –Rule 10

Loss of audit to one/ gain to another-3

3. Because the auditor has a relative who is a CFO or Company

secretary (being KMP) in the Company

• S 141

Loss of audit to one/ gain to another-4

4. Because he has over 20 audits , he has two choices now

� leave the not so remunerative ones to smaller firms

� better still bring in a new partner!

– Best provision to help

• SMP auditors• SMP auditors

• that manager in the firm who has slogged for 20 years-

who can get a partnership now!

– S 141

Loss of audit to one/ gain to another-5

5. Because the private limited consulting firm where he has

significant influence does Management services (one of the

prohibited services) for the holding co or subsidiary

– (If existing work he has one year to comply)

• S 144• S 144

Loss of audit to one/ gain to another-6

6. Because he has been an auditor from generation to

generation in a 112 year old co (formed originally under 1913

act- listed or with Public borrowing >=Rs 50cr, or Public co

with PUC >=Rs 10cr, or Private co with PUC>=Rs 20cr) he has

to retire after 3 more years!

(and he has to wait on the wings only for 5 years to get– (and he has to wait on the wings only for 5 years to get

back!)

• S 139(2)

Loss of audit to one/ gain to another-7

7. Because the members of the Company say let’s have a jointauditor because of the size of the Company and as existing

auditor has to retire in 3 years

• S 139(5)

8. Because the members do not ratify his appointment after say8. Because the members do not ratify his appointment after say

the second AGM even though appointed for 5 years.

• Explanation to Rule 3(7)

Loss of audit to one/ gain to another-8

9. Because the firm where he practices is no longer a majority

CA firm (when multi-disciplinary firms are allowed) and

thankfully an MBA cannot sign FS as auditor!

• Proviso to S 141(1)

I am not considering normal removal, resignation etc.I am not considering normal removal, resignation etc.

Thus there are 9 different ways (may be more?) in which audits

will get distributed across a larger CA population and audits will

get a new look

To me that looks GOOD!

THE LEGAL PROVISIONS RELATING TO

AUDIT-NOT COVERED SO FAR

Auditor Appointment

- S 139 - (S 224)

• Audit appointment till conclusion of 6th AGM (againstconclusion of next AGM)

– Ratification at AGM every year by ordinary resolution

• If not ratified, Board shall appoint another auditor

• Company to inform auditor and ROC (auditor was filing F23B); inform ROC in form ADT-123B); inform ROC in form ADT-1

• Audit committee to recommend auditor to Board and Boardin turn recommend to AGM

• Consecutive years mean all preceding financial years untilthere has been a break by 5 years or more

Auditor Appointment

- S 139 - (S 224) contd...

• Rotation of auditors in listed and other prescribed cos

(contd.)

– No audit firm with common partner of firm whose tenure

has expired, to be appointed for 5 years

– For existing cos/auditors 3 years’ time provided to comply

– Members of Co. may decide on audit partner/ team– Members of Co. may decide on audit partner/ team

rotation and joint audit

– Prohibition applies to

• A partner who certifies FS resigns and joins another firm ,

the latter firm

• Other firms whose name, trade name, or brand is used

by the firm or any of its partners

– If Joint audit, all auditors not to complete term in same

year

• What will happen if auditor resigns after say 8 years and

not 10 – will the cooling period of 5 years still apply?

Auditor Appointment

- S 141 - (S 224(1B)/ 226)

• Additional disqualifications:

– Partner can’t hold security or interest in company in theCompany/ subsidiary /holding co/ associate/ subsidiary ofholding co

– Person convicted by a court of

an offence involving fraud for 10 yearsan offence involving fraud for 10 years

– Provision of specialized services u/s 144

• Previous extension of disqualification of an auditor disqualifiedin subsidiary or holding company or a co-subsidiary –isremoved now

Auditor Appointment

- S 141 - (S 224(1B)/ 226) contd..

• Issues:

– The list is too long

– Relative or partner can’t owe money or hold shares butcan have business relations!

– As auditor includes firm , firm cannot hold shares or have

debts due also (expl. 2 S 140)

Independent Auditors Report

- S 143 - (S 227)

• Enquiry by auditor

– Good old 6 clauses u/s 227(1A) still there!

• Holding company auditor to have access to subsidiary

records so far as it relates to consolidation

– SA 600 is not yet mandatory in India but does this mean– SA 600 is not yet mandatory in India but does this mean

holding co auditor is responsible for subsidiary also even if

audited by another CA?

– Auditor does not have access to associate/JV company

books still

Independent Auditors Report

- S 143 - (S 227) contd…

• Italics /Bold for qualifications no longer exists

• Report to have additionally:

– Observation or comments on financial transactions or matters which

have any adverse effect on functioning of the Company

– Any qualification, reservation or adverse remark relating to the

maintenance of accounts and other matters connected therewith

– Whether company has adequate internal financial control system in

place and the operating effectiveness of such controls (Back door entryplace and the operating effectiveness of such controls (Back door entry

to SOX?)

• Under Rule 11 to report further:

– Whether company had disclosed impact, if any, of pending litigations

on its financial position in financial statements

– Whether company had made provision as required under any law or

accounting standards for material foreseeable losses if any on long term

contracts including derivative contracts

– Whether there has been any delay in transferring amounts to IEPF by

company

Reporting fraud to Central Government

- S 143 rw Rule 12/ 13 (S 227)

• Applies to main auditor as well as branch auditor

• Presently only in respect of money laundering there is a

requirement to report to CG (Implementation of S 51A of

Unlawful activities (Prevention) Act 1969 ICAI circ. dated 22

Apr 2010)

• Now if an auditor has reason to believe that an offence

involving fraud is being or has been committed against the

company by officers or employees of the company he shall

report it to CG

• No duty of auditor regarded as contravened if such reporting

done in good faith

How to report fraud to CG

- S 143 rw Rule 12/ 13 (S 227)

• Time - Within 60 days

• In - Form ADI 4

• How?

– Auditor to forward report to Board/AC of Co. seeking reply within

45 days

– Forward his report and reply with his comments to CG within 15

days of receipt of replydays of receipt of reply

– If no reply, auditor to forward his report to CG with a note

containing details of report forwarded to Board or AC

• To - Secretary, MCA

• By registered post ack due or speed post followed by email

• Branch auditor to have same duty related to the concerned

branch audited (Rule 12)

Reporting fraud to CG

- S 143 rw Rule 12/ 13 (S 227)

• Are we opening a Pandora’s box?

• Will aggrieved auditors report/ send reports to CG to take

revenge on management and not accept replies of

management?

• Board/ AC may call for the auditor after the report goes to

them and ‘persuade’ him aggressively

• No materiality is mentioned here!

• What about past frauds?

• Officers will include directors also!

Independent Auditors Report

- S 143 - (S 227)

• Other Issues:

– Equivalent of CARO u/s 227(4A) – S 143(11) what it will

contain we need to wait and see

– Observations on adverse effect on functioning of co- does

it mean propriety audit? Does it extend auditit mean propriety audit? Does it extend audit

responsibility?

– Reporting on adequacy of IC and effectiveness of IC is

going to be Herculean task! Not required anywhere in the

world! SA also does not require this! (Caro talked of only 2 –

sales and purchase)

Non audit services

- S 144 - new

• Directly or indirectly to Company/ Holding /Subsidiary:

– To be approved by Board or audit committee other than following

which are banned:

• Accounting; Internal audit; Design and implementation of

Financial info system; Actuarial services; Investment advisory

;Outsourced financial services; Management services*; Others as

prescribed

– Existing work- To comply with before closure of first FY

– Prior approval does not seem necessary but what if Board

/Ac fail to approve after the event?

– Forensic audit does not seem prohibited?

– ICAI rule of fees for other services would still apply?

• Applies to auditor, firm, partners, parent, subsidiary/ associate/ any

other entity where firm/partner has significant influence/ control or

common trade mark/ brand

* ICAI has stated what are permitted Management services

Non audit services

- S 144 - new – contd…

• Issues:

– List is too long but associate is not covered

– IFAC / IESBA code do not prohibit these services in all

companies; stricter rules apply to only Public interest

entities- so this is harsher than International standards

– If Company or subsidiary abroad obviously the restriction– If Company or subsidiary abroad obviously the restriction

can’t apply?

– What is management services? S141(3)(i) talks of

consulting and specialized services

– indirect recognition to multi national firms? (trade

mark/brand)

Penal provisions

• Penalties /prison time go up sky high! (In S 185/186 it is fine plusimprisonment)

• Refund of remuneration/ paying damages etc contemplated

• Liability extends to concerned partner/ partners who haveacted in a fraudulent manner or abetted or as the case maybe colluded in the fraud (R 9).

– Will it cover, for instance, an engagement quality control– Will it cover, for instance, an engagement quality controlreviewer who may not have the full facts?

• Joint and several liability to firm/partners

• Action by NFRA/ Tribunal provided for

• Class action suits arrive in India

• Will an LLP help at all?

• Will audit be a very onerous and thankless job?

SOME KEY PROVISIONS-ACCOUNTS

Securities premium:

- S 52 - (S 78)

• For prescribed class of companies following set off against

securities premium will not be permitted:

– Issue of fully paid preference shares

– w/off expenses /commission/discount on preference

shares/debentures

– W/off of preliminary expenses– W/off of preliminary expenses

– Providing premium payable on redemption of redeemable

preference shares /debentures

Depreciation

- S 123- (S 205)

Schedule II Schedule xiv

Useful life and residual value

prescribed (generally not more

than 5%); where these differ

disclose justification in FS

Minimum Depreciation rate

prescribed

Useful lives

increased/decreased as

Generally lower rates;

increased/decreased as

compared to Sch xiv- ex. ocean

going liners 25 years (20);

Furniture 10(15) –higher charge

will result in general esp. when

assets nearing end of life

Componentisation required

(note 4)

Componentisation was not

required; allowed under AS 10

Depreciation

- S 123- (S 205) contd..

Schedule II Schedule xiv

No 100% depreciation 100% depreciation for

assets costing less than Rs

5000

No ESA rate- 50% more for 2 shifts;

100% more for 3 shifts for period

Rates specified for ESA

More sub divisions in individual assets

like for Buildings ; separate rates for

some industries;

Less sub divisions and less

industries

Where remaining useful life nil charge

to Opening retained earnings

Always to Statement of

P&L

Revalued assets –depreciation to

P&L

The differential

depreciation was taken to

revaluation reserve

Consolidated Financial statements (CFS) -

S 129- Ch ix (S 211)• Where any company has a subsidiary (which definition includes

associate or JV Co)

– CFS to be prepared and laid before AGM along with standalone FS

(now for all cos)

• If no subsidiary but associate/ JV is there, will consolidation

apply?

– Option to prepare under IFRS per listing agreement goes– Option to prepare under IFRS per listing agreement goes

• CGmay provide rules for consolidation of accounts

– Statement containing salient features also continues! Form AOC 11-

(R5)

• Will apply to associates and JV also now

• Proviso to Rule 6 “In the case of a co. covered u/s 129(3)which is notrequired to prepare CFS under AS, it shall be sufficient if the Co.

complies with provisions of CFS provided in Sch III of the Act.” Thispossibly means only the additional information at the end of Sch III

need be provided; however not clear

Consolidated Financial statements (CFS) -

- S 129 (S 211) – contd..

• Total Share capital is Paid up equity share capital plus

Convertible preference share capital (Ch 1-R 2(r))

– What about partly convertible preference?

– Is it only Compulsorily convertible preference?

• Conflict between Co law and Accounting standard:• Conflict between Co law and Accounting standard:

• Subsidiary definition in S 2(87) states ‘control of more

than one-half of total share capital’ whereas in AS 21 it

is “one-half of the voting power”

• Also S 2 (87) talks of control of composition of board of

directors only, whereas AS 21 has in addition “to

obtain economic benefits from its activities”

Consolidated FS issues

- S 129 (S 211)

• Do we have to give all disclosures per Sch III in CFS also?

– May be not.

• as Sch III states the schedule will be followed mutatis,

mutandis (ie with necessary changes)

• Also AS 21 gives exemption from statutory information

(Cl 6 exp c of AS 21)(Cl 6 exp c of AS 21)

• Such information on an aggregate basis may not really

help users of FS but confuse them!

– For instance: what is the earthly use of aggregating

audit fee of all group cos or disparate information

like raw materials or goods purchased which make

sense only for standalone cos; or imports and

expenditure in foreign currency of foreign

subsidiaries?

Reopening/recasting of accounts

- S 130 / S131 – new

• Court/Tribunal order (S 130) / Voluntary (S 131):

• Who can apply?

– CG

– IT authorities

– SEBI

– Any other statutory/regulatory authority– Any other statutory/regulatory authority

– Board/Company- S 131

• To

– Court /Tribunal – S 130

– Tribunal – S 131

Reopening/recasting of accounts

- S 130 / S131 – new – contd…

• Conditions for reopening S 130

– Accounts prepared in fraudulent manner

– Affairs of the company was mismanaged during the

relevant period casting a doubt on reliability of FS

• Conditions S 131• Conditions S 131

– FS or Board report not in compliance with S 129/S 134

Reopening/recasting of accounts

- S 130 / S131 – new – contd…

• Notice to same authorities only viz CG, IT, SEBI, other statutory

regulatory body S 130

• Notice to CG, IT S 131

• Reopening/recasting only on order by court/Tribunal S 130 /• Reopening/recasting only on order by court/Tribunal S 130 /

Tribunal S 131

• Accounts so recast shall be final S 130

Reopening/recasting of accounts

- S 130 / S131 – new – contd…

• S 131 – revision of FS/Board report

– Revision for any of the 3 preceding FY

– Not more than once in a FY

– Detailed reasons to be disclosed in Board report

– Where already filed with ROC revision to be confined to

correction to the extent of non compliance with S 129/Scorrection to the extent of non compliance with S 129/S

134 and consequential corrections

– CG to frame rules including functions of company auditor

• Recently SEBI issued circular which empowers it to order

revision of FS –thus there are 3 ways

• SEBI has power only to ask company to restate results and

file same with Stock exchanges and company has to give

impact to this in the next year as prior period items

Reopening/recasting of accounts

- S 130 / S131 – new – contd…

• Questions that arise:

– How many years can be reopened not clear in S 130?

– For application by authorities nothing provided for

opportunity of being heard to Company! S 130?

– Finality is provided in S 130 not in S 131!?

– S 131 revisions every year possible!?

– Revision of CFS possible?

National Financial Reporting Authority

(NFRA) - S 132 – (S 210A)

• NACAS becomes NFRA

• Reach extends to audit standards and overview of audit

profession also

• NFRA has powers to investigate professional or other• NFRA has powers to investigate professional or other

misconduct

– Suo moto or on reference by CG

– ICAI can ’ t initiate/ continue any proceedings whereNFRAS initiates action

– Misconduct of CFO/Co. officials also covered

• NFRA has powers of civil court

NFRA

- S 132 – (S 210A) – contd…

• Penalty action if member(CA) proved guilty

– Penalty not < Rs 1Lakh upto 5 times fees received for

individual

– Penalty not < Rs 10 lakhs upto 10 times fees received for

firms

• Fees for how many years?• Fees for how many years?

– Debarring member or firm min. 6 months max. 10 years

• Appeal to Appellate authority possible

Corporate Social Responsibility (CSR)

- S 135 CSR rw CSR rules dtd 27 feb 14

• Spend

– At least 2% of average net profit of 3 immediately

preceding FY (per S 198)

– Excluding

• Profit from overseas branches• Profit from overseas branches

• Dividend received from other companies in India

complying with S 135 (avoids double counting)

Corporate Social Responsibility (CSR)

- S 135

• Limit of 5% on own personnel and implementation agencies –

R 4(6)

• Rule 4(1) excludes activities undertaken in pursuance of

company’s normal course of business.

– So for inst. a hospital cannot extend healthcare services.– So for inst. a hospital cannot extend healthcare services.

• Schedule III requires

– Disclosure of CSR expenses

• Disclose reasons if amount not spent.

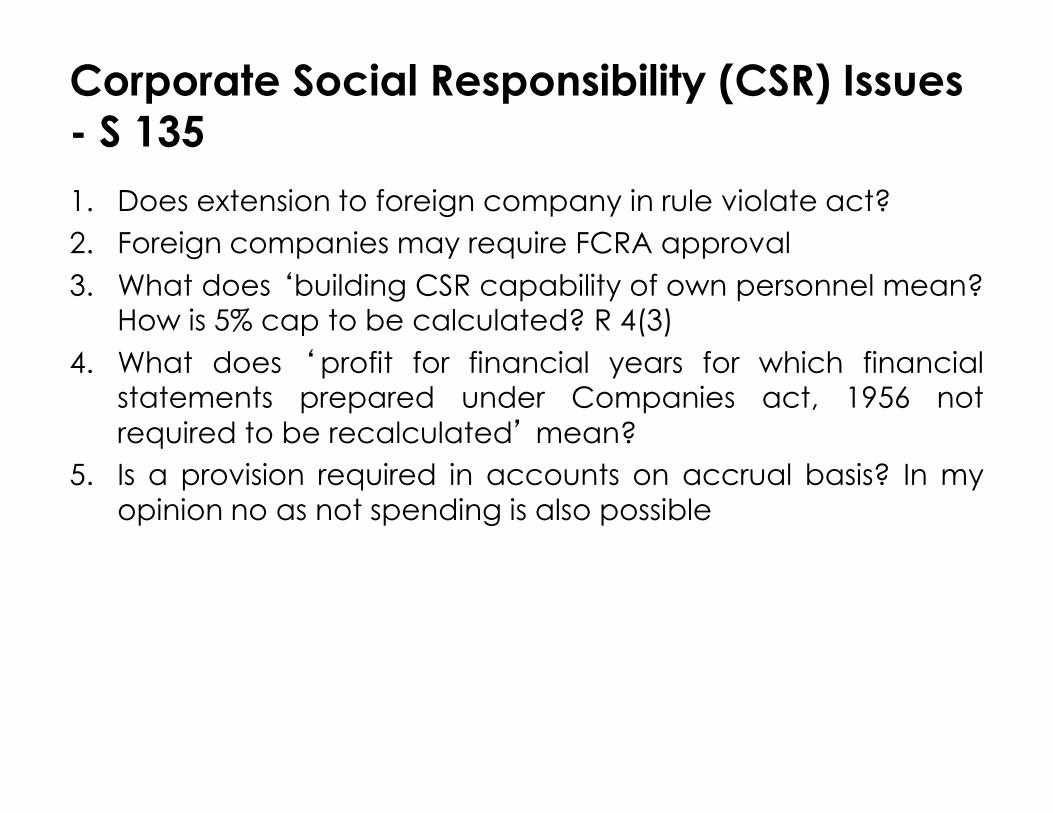

Corporate Social Responsibility (CSR) Issues

- S 135

1. Does extension to foreign company in rule violate act?

2. Foreign companies may require FCRA approval

3. What does ‘building CSR capability of own personnel mean?How is 5% cap to be calculated? R 4(3)

4. What does ‘profit for financial years for which financialstatements prepared under Companies act, 1956 notstatements prepared under Companies act, 1956 not

required to be recalculated’ mean?

5. Is a provision required in accounts on accrual basis? In my

opinion no as not spending is also possible

S 136, 137 ( S 219, 220)

• Copies of FS /filing:

– CFS also to be sent to members etc

– Listed co can send statement containing salient features

to members etc provided it makes them available for

inspection at regd office (in view of cl 32 they can’t sendabridged CFS)

– Listed cos to place CFS and standalone FS on website

– Electronic dispatch of FS under certain circumstances

– All companies with subsidiary need to place separate

audited a/cs of subsidiary/ies on website

• Thus unlisted cos having subsidiary need a website?

and

• Need not place the holding co a/cs or cfs on website!

S 138 rw Ch IX rule 13

• Internal auditor

– Required for

• Listed cos

• All companies with TO Rs 200cr or more or o/s loans and

borrowings from Banks/FI Rs 100cr or more

• Unlisted public cos with Share capital Rs 50cr or more or• Unlisted public cos with Share capital Rs 50cr or more or

Public deposits Rs 25 cr or more

– Shall appoint a

• CA /cost accountant; can be firm of internal auditors;

– 6 months time for compliance

– AC or Board in consultation with IA to formulate scope,

functioning, periodicity and methodology of IA

SOME OTHER KEY PROVISIONS RELEVANT

FOR AUDIT

Net worth

- S 2(57)

• Reserves created out of

• Write back of depreciation and amalgamation Excluded

– As auditors we need to note this carefully.

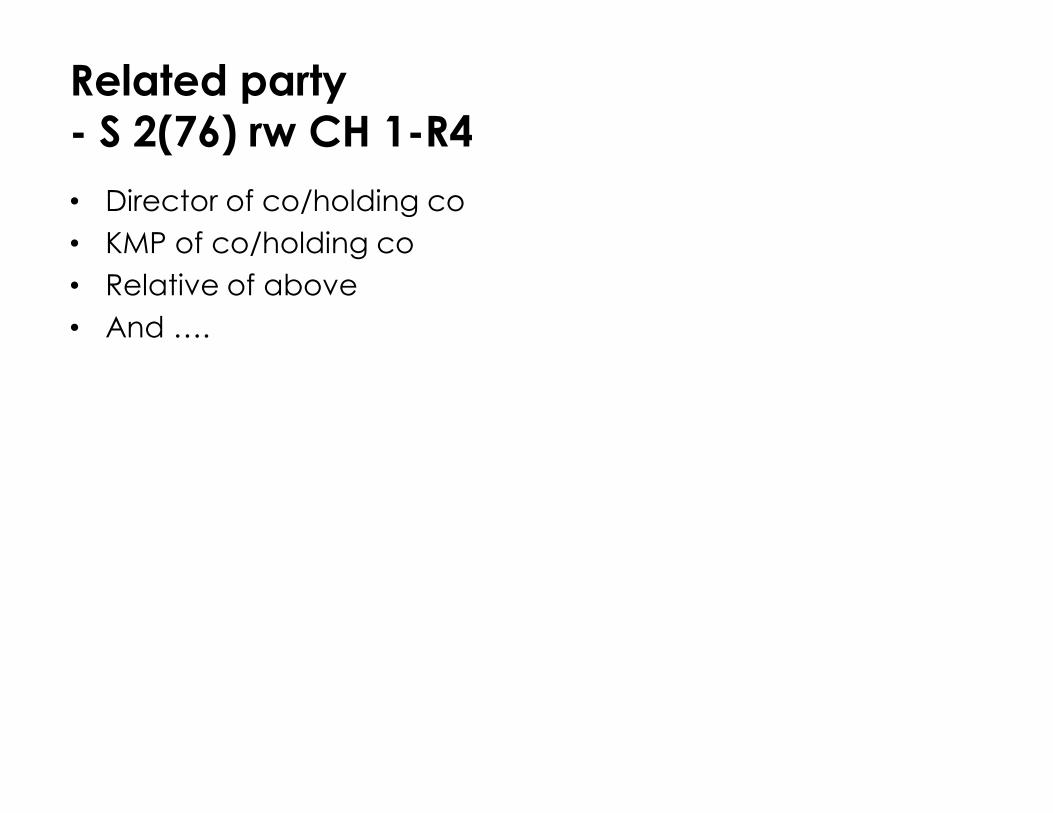

Related party

- S 2(76) rw CH 1-R4

• Director of co/holding co

• KMP of co/holding co

• Relative of above

• And ….

Related party new co law

New Companies Act

S 276 read with MCA Rule 3 of chapter I Rules

“related party”, with reference to a company, means

(i) a director or his relative;

(ii) a key managerial personnel or his relative;

(iii) a firm, in which a director, manager or his relative is a partner;

(iv) a private company in which a director or manager is a

member or director;

(v) a public company in which a director or manager is a director

or holds along with his relatives, more than two per cent. of its

paid-up share capital;

(vi) any body corporate whose Board of Directors, managing

director or manager is accustomed to act in accordance with the

advice, directions or instructions of a director or manager;

Related party new co law contd.

(vii) any person on whose advice, directions or instructions a

director or manager is accustomed to act:

Provided that nothing in sub-clauses (vi) and (vii) shall apply to the

advice, directions or instructions given in a professional capacity;

(viii) any company which is—(viii) any company which is—

(A) a holding, subsidiary or an associate company of such

company; or

(B) a subsidiary of a holding company to which it is also a

subsidiary;

(ix) such other person as may be prescribed; (Rule 3 of Chapter I)

A director or KMP of the Holding Co or his Relative with ref to a

co.

Related party Cos act Vs AS

S 276 read with MCA Rule 3 of

chapter I Rules AS

Holding Company Holding Company 2(76) VIII A

Subsidiary Subsidiary 2(76) VIII A

Fellow Subs

Fellow Subs - 2(76) VIII B a subs

of holding company to which it

is also a subsidiary.

Associate includes JV Company Associate 2(76) VIII A

KMP & Relatives KMP & Relative 2(76) II

Entrenchment

- S 5(3) -New

• The articles can now contain provisions for entrenchment –

– ie. specified provisions of the articles may be altered only if

conditions or procedures that are more restrictive than

those applicable in the case of a special resolution, are

met or complied with

• We should as auditors to ensure that If there is such a provision

in articles, resolutions passed are as prescribed

• Similarly if Board meeting called at short notice and no

independent director present, whether independent director

has ratified decisions later (S 173(3)

Special resolution required

- S 180/181/182 (S 293/293A)

• The clause regarding investment in trust securities now

applies to compensation received by company as a result of

merger or amalgamation

• Donations now for bona fide charitable and other funds

above 5% of average net profits for 3 immediately preceding

years will require prior permission of company in general

meeting. (Rs 50000 lower limit removed)meeting. (Rs 50000 lower limit removed)

• Political parties donation hiked to 7.5% from 5%

– For both above profit means profit (after tax?) and link to

managerial remuneration profits goes

• If existing borrowing limit u/s 293(1)(d) is sufficient, no need for

a special resolution again. If limit exceeded under New act

for new borrowings , charge registration, Special resolution to

be taken before 11 Sep 14. (Circular 4/14)

Loans to directors etc.

- S 185- (S295)

• Loans /guarantees /providing security to director or any

other person in whom director interested prohibited (director

of lending co or holding co or partner/relative of such

director; any firm where such director or relative is

partner; private co of which such director is director or

member; any BC where over 25% voting powermember; any BC where over 25% voting power

exercised by such director/directors together; or where

Board is accustomed to act according to instruction of

board or directors of lending co)

– Except for

• loan to MD/WTD as part of service condition extended

to all employees or per scheme approved by members

by special resolution

• Loans in the ordinary course at rates of interest not less

than bank rate

Loans/investments

- S 186 - (S 372A)

• Only two layers of investment companies

– Unless acquiring another company out of India

– Subsidiary having investment subsidiary to meet

requirements of any law

• Giving of loans/guarantee/security extended to any

person/body corporate (not only corporates)person/body corporate (not only corporates)

• Prior approval by special resolution needed if limits exceeded

for loans/Guarantee/security/Investment (i.e 60% of PUC/Free

reserves/Securities premium or 100% of free reserves incl.

securities premium)

• Rule 11 Ch XII

– Loans/guarantee/providing security to WOS/JV exempt

– Guarantees to Subsidiaries exempt if a)to banks /FI; b)

used for subsidiary’s principal activities

– Investments in WOS exempt.

Loans/investments

- S 186 - (S 372A) contd..

• No loans /investments if in default of repayment of deposits

• Rate of interest not less than prevailing yield on 1 year/3

years/ 5 years /10 years Government security, closest to tenor

of loan (previously bank rate)

– What about Forex loans?– What about Forex loans?

• Disclose in FS details of loans / investments / guarantee/

security, purpose

– No exemptions for private cos, etc

– One year time given to get approvals

– Omnibus resolutions possible

Related party transactions

- S 188 - (S 297)

• Related party definition widened

• Prior Special resolution required for RPTs (previously CG

approval if PUC over Rs 1cr) if not at arm’s length

– No vote by related party gives enormous powers to non

related parties for material transactions!

– How to take care in fellow subsidiaries/JV cos?- deadlock– How to take care in fellow subsidiaries/JV cos?- deadlock

situations?

• New items now brought under RPTs if not on an arm’s lengthbasis:

– Leasing of property; selling/buying property; appointment

of agents for purchase/sale of materials/service/property;

appointment to office or place of profit in

Company/Holding co.; underwriting securities/ derivatives

• Arm’s length V IT department Transfer pricing?

• How to determine arm’s length? And document?

Related party transactions covered

- S 188Transactions covered under new Act Transactions covered under Old Act

188(1)

a)sale purchase or supply goods or

materials

297 1 a sale purchase or supply

goods or materials

b) Selling or otherwise disposing off or

buying, property of any kind

Not Covered

c) Leasing of property of any kind Not covered

d) Availing or rendering of any services 297 1 a – for supply of any servicesd) Availing or rendering of any services 297 1 a – for supply of any services

e) appointment of any Agent for purchase

or sale of goods materials services or

property

Sole selling agents 294 -

f) such related parties appointment to any

office or place of profit in the company or

subsidiary or associate co.

314 -

g) underwriting of subscription any

securities or derivatives thereof of the co.

297 1 b for underwriting the sub of

any shares in or deb of the co.

RPT requiring prior approval of members-

majority of minority- if not at arm’’’’s length

• Chapter XII Rule 15 (3) –Prior approval of members – by special Resolution

– Provided further that no member of the company shall vote on such

special resolution, to approve any contract or arrangement which may

be entered into by the company, if such member is a related party

– The Co having paid up share capital of over Rs 10 cr or

– .

– sale purchase supply of goods or materials exceeding 25% of

annual TOannual TO

– selling or disposing of or buying property exceeding 10% of

networth

– leasing of property exceeding 10% of networth or 10% of TO

– availing or rendering of service exceeding 10% of the net worth.

• iii) appointment to any office or place of profit in the co or subsidiary or

associate at a monthly remuneration exceeding Rs 2.5 lacs

• iv) remuneration for underwriting the subscription of derivatives exceeding

1% of Net worth.

• Does it mean if paid up capital is over Rs 10 Cr, none of the other

conditions help?

Non cash transactions – directors

- S 192-

• Director of company/holding/subsidiary/associate co. or

person connected with him (not defined) requires prior

approval of Company in GM (also GM of holding co if

director of holding co) for:

– Acquiring assets from Company or

– For Company to acquire from the above

• for consideration other than cash

Minimum managerial remuneration

- S197/ SchV

Slabs for Effective Capital Limits on yearly

remuneration not exceeding

(can be double if approved by

Special resolution)

Negative or less than Rs. 5 crores Rs. 30 lakhs

Rs. 5 crores and above but less Rs. 42 lakhsRs. 5 crores and above but less

than Rs. 100 crores

Rs. 42 lakhs

Rs.100 crores and above but

less than Rs. 250 croresRs. 60 lakhs

Rs. 250 crores and above Rs. 60 lakhs plus 0.01% of the

effective capital in excess of Rs.

250 crores

Freezing of assets

- S 221 -New

• The Tribunal, on reference made to it by the Central

Government or in connection with any inquiry or investigation

into the affairs of a company or on any complaint made by

such number of members as specified or a creditor having Rs

1 lakh amount outstanding against the company or any other

person

• having a reasonable ground to believe that the removal,• having a reasonable ground to believe that the removal,

transfer or disposal of funds, assets, properties of the company

is likely to take place in a manner that is prejudicial to the

interests of the company or its shareholders or creditors or in

public interest,

• it may by order direct that such transfer, removal or disposal

shall not take place during such period not exceeding three

years as may be specified in the order or may take place

subject to such conditions prescribed

OTHER PROVISIONS-ACCOUNTS/AUDITING

Financial Year

- S 2 (41)

• Uniformly Mar 31

• A holding/ subsidiary of foreign co. can follow different FY

with permission of Tribunal

– Two years time for conversion to Mar 31

• Result:• Result:

– More work for companies and auditors due to peaking up

Free Reserves

- S 2 (43)

(i) any amount representing unrealised gains, notional gains or

revaluation of assets, whether shown as a reserve or

otherwise, or

(ii) any change in carrying amount of an asset or of a liability

recognised in equity, including surplus in profit and loss

account on measurement of the asset or the liability at fairaccount on measurement of the asset or the liability at fair

value,

– shall not be treated as free reserves;

• The underlined parts are going to pose lot of

challenges!

Free reserves

- to take care

• S 123 – no dividend to be declared from reserves other than

free reserves.

– New declaration of dividends out of reserves rules (chapter

VIII) clearly states amount drawn from accumulated profits

shall first be utilised to set off losses incurred in the financial

year in which dividend is declared.year in which dividend is declared.

– Hence the previous option of declaration out of ‘surplus’in P&L is no longer there.

Free reserves

- to take care

• S 180 on restrictions on powers of Board

– Borrowing moneys exceeding paid up share capital and

free reserves –here free reserves would mean only those

available for distribution as dividend and after reducing

unrealised gains and surplus on measurements of assets

and liabilities at fair value.

Special resolution to be taken before 11 Sep 14 if– Special resolution to be taken before 11 Sep 14 if

borrowing is more than limit (Circular 4/14)

• S 179 rw Rule 8(6) Chapter 12 –Board resolution required in

meeting and to be filed with ROC

– Buy sell investment held by company (non trade)

constituting 5% or more of Paid up capital and free

reserves of investee company.

Share application money–to take care

• Companies acceptance of deposits

Rules 2014 makes it compulsory to

issue shares within 60 days of receipt

of share application money or refundof share application money or refund

it within 15 days.

• Else this will be treated as deposit with serious consequences.

–Esp. for private limited companies.

Small Company

- S 2 (85) new

• Paid up share capital- Rs 50 lacs to Rs 5cr as prescribed

• Turnover per last P&L –Rs 2cr to Rs 20cr as prescribed (Rs 50cr

under AS)

– Exempt:

• Holding or subsidiary

• S 8 co• S 8 co

• Cos under special act

• Issues:

– Definition different from AS for SMC

– So cash flow statement becomes applicable for

companies with turnover per cos act limit which is smaller;

– What about companies with Turnover less than co. law

limit but borrowings exceeding Rs 10cr?

Section 71 rw rule 18 Chapter IV

• Company is now required to create DRR equivalent to 50% of

amount raised through the debenture issue before

redemption commences (sub rule 7 (b))

• This is more than current requirement in some cases

– In my opinion new rule applies to debentures issued after

Apr 1, 14 only

Dividends

- S 123 (S 205)

• Transfer of current profits to reserves rule go- transfer will be at

discretion of company

• No power to declare dividend without providing for

depreciation with CG approval

• Interim dividend:

– Out of surplus in P&L and out of profits of the FY– Out of surplus in P&L and out of profits of the FY

– If loss during CY upto previous quarter , rate not to be

higher than average dividends during immediately

preceding 3 FY

• Declaration of dividend out of reserves to be as per rules

• No dividend if S 73/74 (deposits acceptance and

repayment) not complied with

Type/details:

• Recognises electronic mode

•No details of account books like money received, expended , assets and liabilities and cost of material and labor (S 209(1)(d)) in new act

Branch:

• Branch returns periodically (previously not more than 3 months)

Books of accounts

- S 128 (S 209)

Inspection:

• Inspection of subsidiary books by a person

authorised by a resolution of Board

Preservation of books:

• In case of investigation under ch xiv, CG may

direct longer period than 8 years

Books of accounts

- S 128 (S 209) contd…

• When books not maintained:

– No longer to have defense that a competent and reliable

person was charged with the duty

– Willful offense not required for imprisonment

• Responsible person:• Responsible person:

– Director (where no MD) and every officer removed

– Now it is MD, WTD and CFO or any other person charged

by Board with the duty

Authentication of FS

- S 134 (S 215-217)

• Chairperson where authorised by Board or Two directors

including MD/CEO director

• CFO (need not be director)

– New /onerous requirement for all companies;

– Previously only in listed companies he was required to sign– Previously only in listed companies he was required to sign

a certificate that FS are free from material misstatement.

• Secretary

• Does this mean if Chairperson is authorised by Board he only

need sign FS?

Directors Report

- S 134 (S 215-217)

• Board report to also include:

� Extract of annual return

� Number of meetings of Board

� Director’s responsibility statement

� Statement on declaration by independent directors

� Policy on director’s appointment and remuneration� Policy on director’s appointment and remuneration

Directors Report

- S 134 (S 215-217) contd…

• Explanation by board on qualifications etc in secretarial audit

report

• Contracts/arrangements with related parties

• Risk management policy including elements of risk which

may threaten existence of company

– Previously this was restricted to listed cos– Previously this was restricted to listed cos

• CSR initiatives

• For listed and other prescribed cos

– Annual evaluation of performance of board, committees

and directors

• Others as may be prescribed

– Board report to include summary of CFS results also?

Directors Report

- S 134 (S 215-217) contd…

• Internal financial controls

• Policies and procedures adopted by the Company for

ensuring orderly and efficient conduct of its business including

• adherence to company’s policies,

• safeguarding of its assets ,

• the prevention/detection of frauds and errors ,• the prevention/detection of frauds and errors ,

• the accuracy and completeness of accounting records,

and

• the timely preparation of financial statements

• Rule 8(5)(viii) Ch ix talks of Internal financial controls wrt

financial statements in Director’s report –hence only ICFR and

not all Internal controls

Directors Report

- Other sections

• Board report to include:

– Every contract/arrangement with related party along with

justification (including non cash transactions)

• Form AOC -2 Ch IX Accounts

– This is going to be a long list!– This is going to be a long list!

Directors’’’’ responsibility Statement- S 134

• Applicable AS followed

• Selection and application of accounting policies, making

reasonable and prudent judgments and estimates to give

true and fair view of FS

• Proper /sufficient care for maintenance of adequate

accounting records for safeguarding assets and for

preventing/detecting fraud/ irregularities

• Prepared accounts on going concern basis

Directors’’’’ responsibility Statement- S 134 contd…

• Proper systems to ensure compliance with provisions of all

applicable laws and such systems were adequate and

running effectively

• Constitution of CSR committee where applicable ; disclose

CSRP and reasons for not spending 2% of avg profits on CSR

(S 135)(S 135)

• In listed company,

– Laid down internal financial controls to be followed by the

company (for orderly and efficient conduct of business)

– These internal financial controls are adequate and

operating effectively

Auditor removal

- S 140 (S 225)

• Special resolution and previous approval of CG required

• By Tribunal suo moto or application made, if it is satisfied thatauditor has directly or indirectly acted in a fraudulent manneror abetted or colluded in any fraud by or in relation tocompany or its directors or officers

• By Tribunal if application is made by CG

• If Tribunal passes order, auditor debarred for 5 years and alsoliable for action u/s 447

• Liability of firm and every partner who acted in fraudulentmanner or abetted or colluded in the fraud

Auditor resignation

- S 140 (S 225)

• Auditor to file a statement indicating reasons for resignation

within 30 days

• Resigning auditor to file form ADT-3 with ROC

• Fine not filing- Rs 50k to Rs 5 lakhs!

• Even resignation is not easy!

S 447 (new)

• S 447 defines fraud and hence is very important from

auditor’s view point.

• “ fraud” in relation to affairs of a company or any bodycorporate, includes any act, omission, concealment of any

fact or abuse of position committed by any person or any

other person with the connivance in any manner, with intent

to deceive, to gain undue advantage from, or to injure theto deceive, to gain undue advantage from, or to injure the

interests of, the company or its shareholders or its creditors or

any other person, whether or not there is any wrongful gain or

wrongful loss;

• “wrongful gain ” means the gain by unlawful means ofproperty to which the person gaining is not legally entitled;

• “wrongful loss” means the loss by unlawful means of propertyto which the person losing is legally entitled.