international business practice

DESCRIPTION

International Business Practice. Syllabus for International Business Practice September 2005 – January 2006. Major Textbook. 黎孝先, 2004 , 国际贸易实务(第三版) ,北京:对外经济贸易大学出版社. Course Topics. 课程介绍、授课计划及要求、第一章概述( WEEK 1) 第二章 国际贸易术语 ( WEEKS 2-4) 第三章 国际货物买卖合同的标的物 ( WEEKS 6-7) - PowerPoint PPT PresentationTRANSCRIPT

International Business Practice

Syllabusfor International Business

PracticeSeptember 2005 – January 2006

Major Textbook

• 黎孝先, 2004 ,国际贸易实务(第三版),北京:对外经济贸易大学出版社

Course Topics

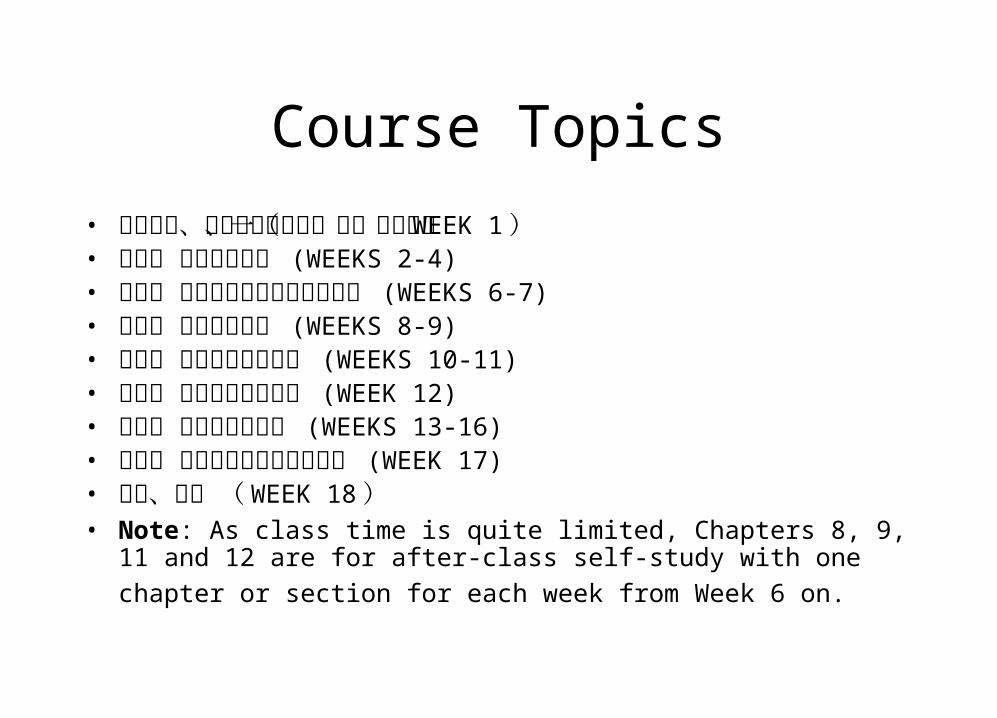

• 课程介绍、授课计划及要求、第一章概述( WEEK 1 )• 第二章 国际贸易术语 (WEEKS 2-4) • 第三章 国际货物买卖合同的标的物 (WEEKS 6-7)• 第四章 国际货物运输 (WEEKS 8-9)• 第五章 国际货物运输保险 (WEEKS 10-11)• 第六章 进出口商品的价格 (WEEK 12)• 第七章 国际货款的收付 (WEEKS 13-16)• 第十章 国际货物买卖合同的商订 (WEEK 17)• 复习、考试 ( WEEK 18 )• Note: As class time is quite limited, Chapters 8, 9, 11 and 12 are for after-

class self-study with one chapter or section for each week from Week 6

on.

List of Books for Course Reading

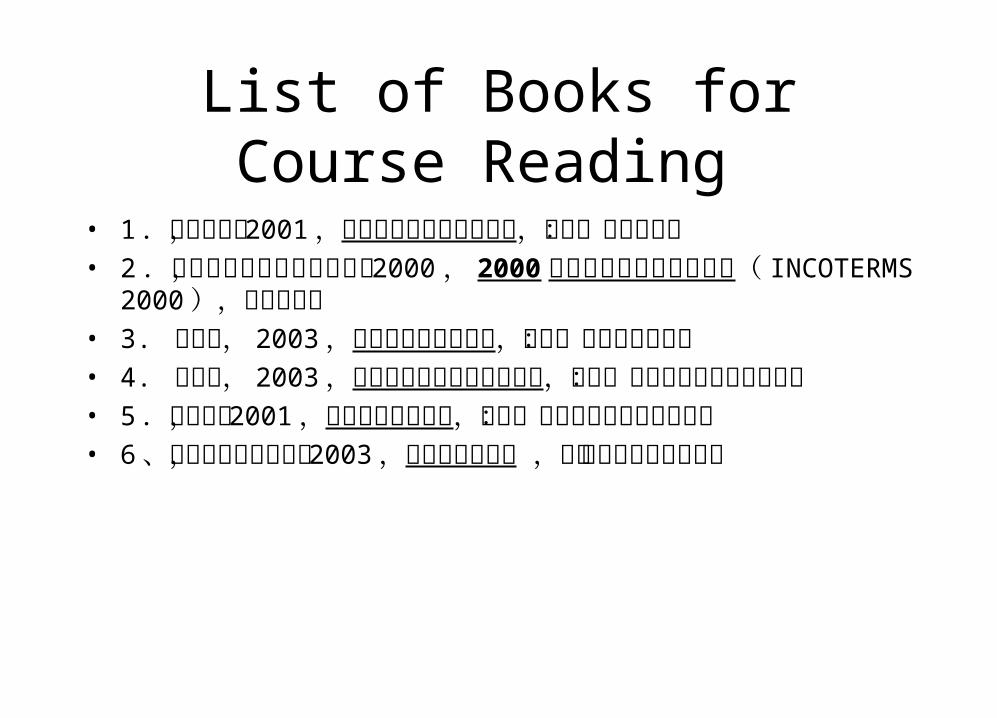

• 1 .胡庚申等, 2001 ,国际商务合同起草与翻译,北京:外文出版社

• 2 .国际商会中国国家委员会, 2000 , 2000年国际贸易术语解释通则( INCOTERMS 2000 ),中信出版社

• 3. 吴百福, 2003 ,进出口贸易实务教程,上海:上海人民出版社• 4. 黎孝先, 2003 ,进出口合同条款与案例分析,北京:对外经济贸

易大学出版社• 5 .赵承壁, 2001 ,国际货物买卖合同,北京:对外经济贸易大学

出版社• 6 、上海对外贸易协会, 2003 ,进出口单证实务 ,中国对外经济贸

易出版社

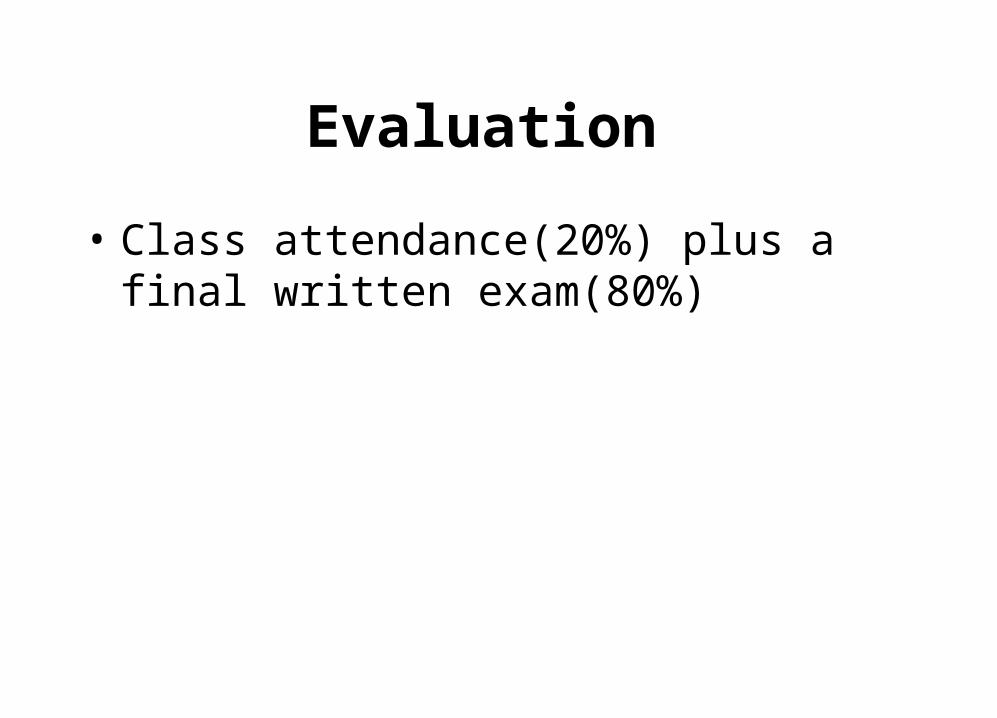

Evaluation

• Class attendance(20%) plus a final written exam(80%)

Introduction

• 1. Nature of International Business: International business(IB) refers to all business transactions that involve two or more countries or regions.It is also called international trade or foreign trade or cross-border trade.

• 2. Reasons why we should study international business: IB comprises a large portion of the world’s business; A company that enters the IB will engage in exportation and/or importation. Thus a better understanding of IB may help us to make better decisions and operate more effectively.

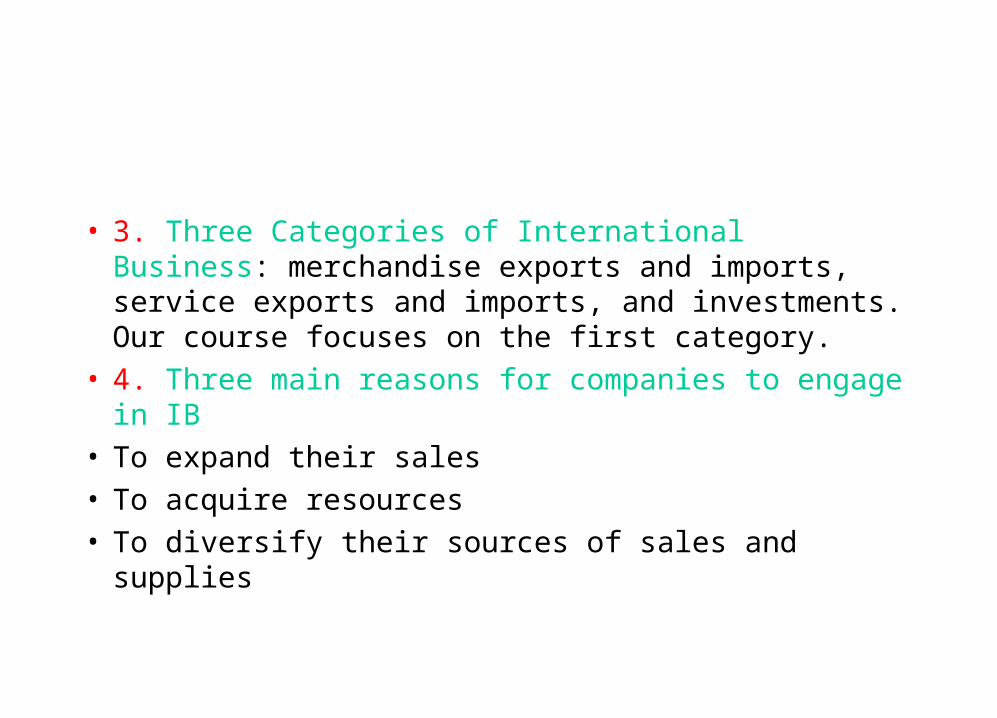

• 3. Three Categories of International Business: merchandise exports and imports, service exports and imports, and investments. Our course focuses on the first category.

• 4. Three main reasons for companies to engage in IB• To expand their sales• To acquire resources• To diversify their sources of sales and supplies

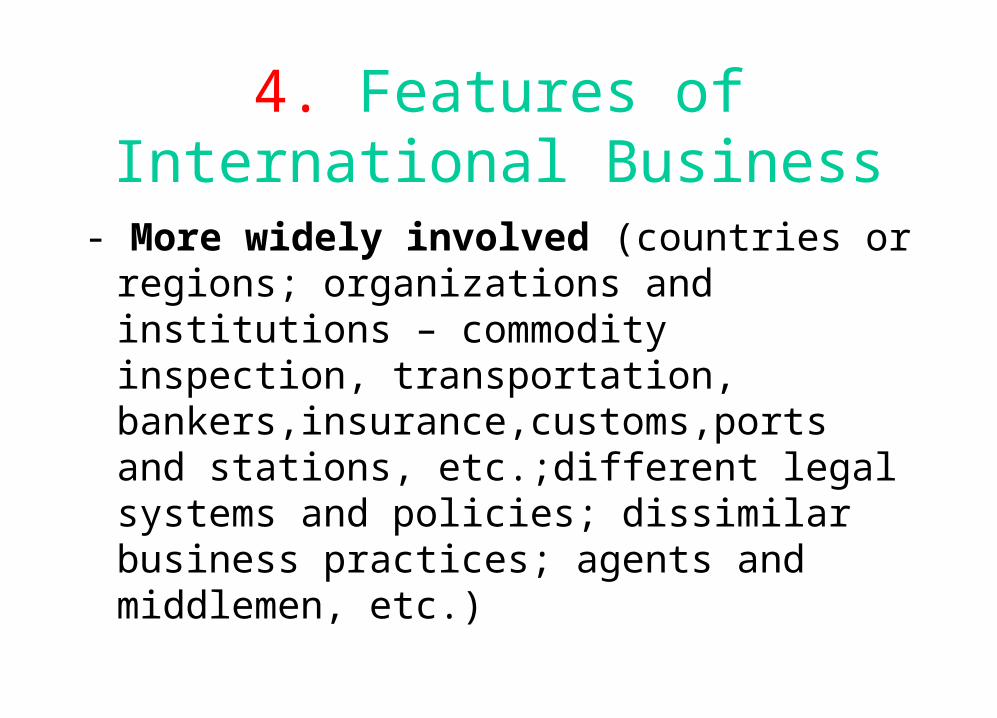

4. Features of International Business

- More widely involved (countries or regions; organizations and institutions – commodity inspection, transportation, bankers,insurance,customs,ports and stations, etc.;different legal systems and policies; dissimilar business practices; agents and middlemen, etc.)

- More difficult to handle (factors contributing to the unstableness of international trade -- changes in government trade policies and economic situations, turbulence in international political situation, keen competition for international market share, trade friction among nations, frequent fluctuations in exchange rate and commodity price,etc.)

- Riskier (large quantities, long-distance transportation, natural calamities or fortuitous accidents, wars, terrorist activities, etc.).

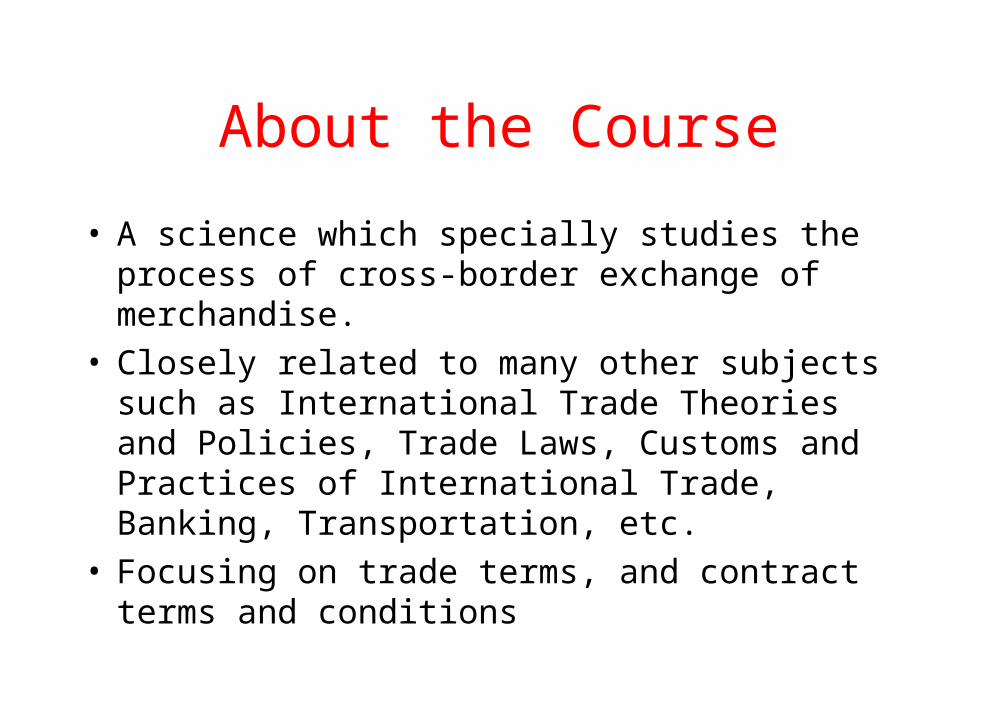

About the Course

• A science which specially studies the process of cross-border exchange of merchandise.

• Closely related to many other subjects such as International Trade Theories and Policies, Trade Laws, Customs and Practices of International Trade, Banking, Transportation, etc.

• Focusing on trade terms, and contract terms and conditions

Laws and Customs Applicable to Contracts for International Sale and Purchase of Merchandise

• Domestic laws

• Customs of international trade

• International treaties or conventions: • e.g. United Nations Convention on Contracts for the International Sale of

Goods. 《联合国国际货物销售合同公约》

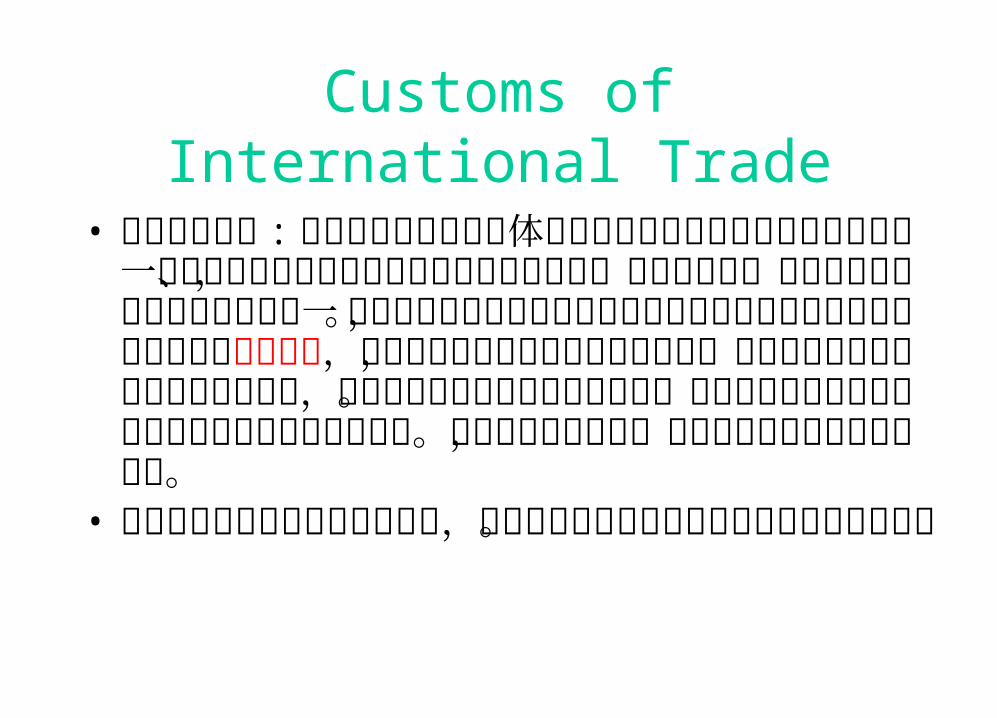

Customs of International Trade

• 国际贸易惯例 : 由国际组织或商业团体根据国际贸易长期实践中逐渐形成的一般贸易习惯做法而制定成文的国际贸易规则、通则和准则,它是国际贸易法律的重要渊源之一。国际贸易惯例的适用是以当事人的意思自治为基础的,因为惯例本身不是法律,它对合同当事人没有普遍的约束力,只有当事人在合同中规定加以采用时,才对合同当事人具有法律约束力。故买卖双方有权在合同中做出与某项惯例不符的规定。只要合同有效成立,双方均要遵照合同的规定履行。

• 国际贸易惯例虽然不具有强制性,但它对国际贸易实践的指导作用却不容忽视。

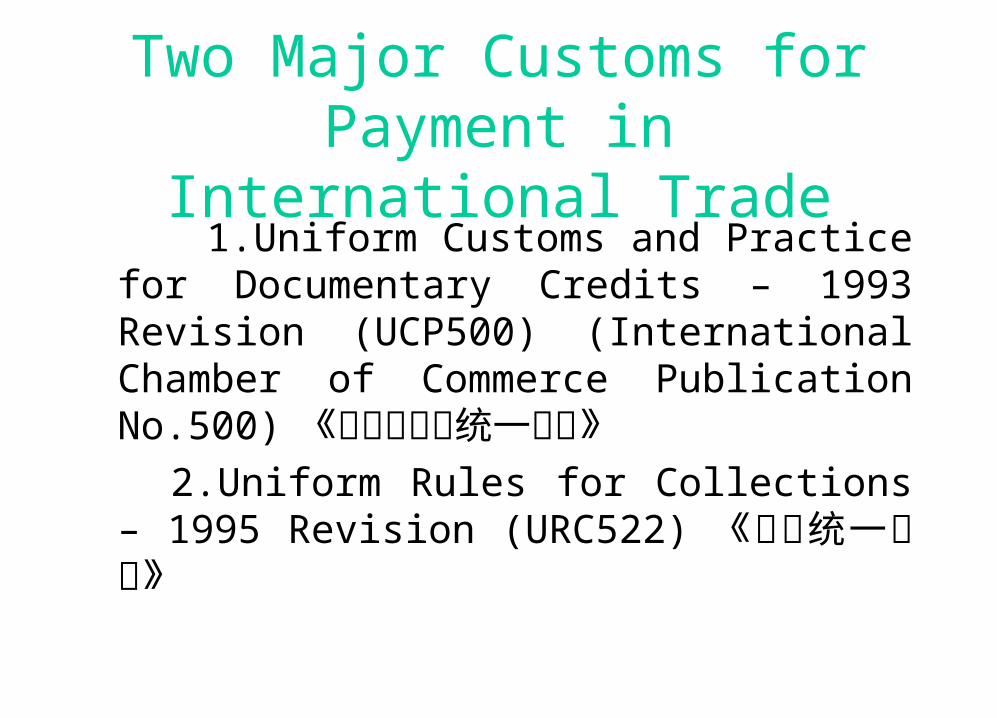

Two Major Customs for Payment in International Trade

1.Uniform Customs and Practice for Documentary Credits – 1993 Revision (UCP500) (International Chamber of Commerce Publication No.500) 《跟单信用证统一惯例》

2.Uniform Rules for Collections – 1995 Revision (URC522) 《托收统一规则》

Three Major Customs for Trade Terms in International Trade

1.Warsaw-Oxford Rules 1932 (laid down by International Law Association in 1932 providing explanations for contracts on CIF terms) 《华沙——牛津规则 , 是国际法协会专门为解释 CIF 合同而制定的。

2. Revised American Foreign Trade Definitions 1941 《 1941 年美国对外贸易定义修订本》

3. International Rules for the Interpretation of Trade Terms - 2000 (INCOTERMS 2000) (ICC Publication No. 560) 《 2000 年国际贸易术语解释通则》

INCOTERMS 2000

• International Commercial Terms 1936 (53-67-76-80-90-00 )

• Grouped in four basically different categories: Groups E, F, C and D

• Trade Terms /Trade Conditions/Price Terms• Trade terms are to divide the risks, liabilities and

costs between the sellers and the buyers.(Please refer to the Chinese definition on Page 16 of the textbook.)

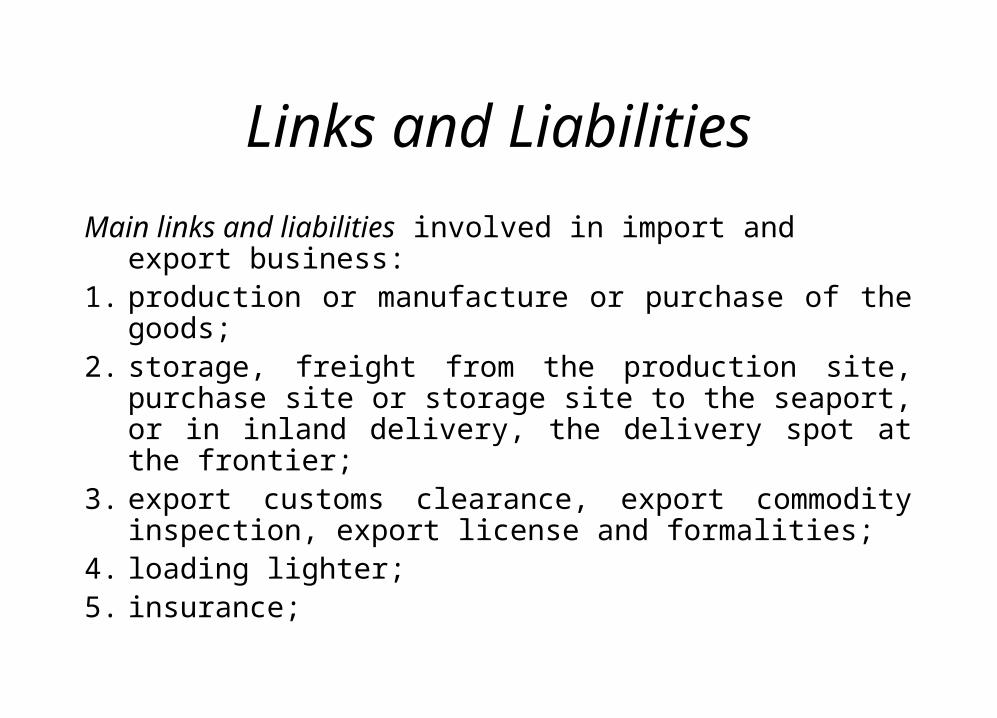

Links and Liabilities

Main links and liabilities involved in import and export business:

1. production or manufacture or purchase of the goods;2. storage, freight from the production site, purchase site

or storage site to the seaport, or in inland delivery, the delivery spot at the frontier;

3. export customs clearance, export commodity inspection, export license and formalities;

4. loading lighter;5. insurance;

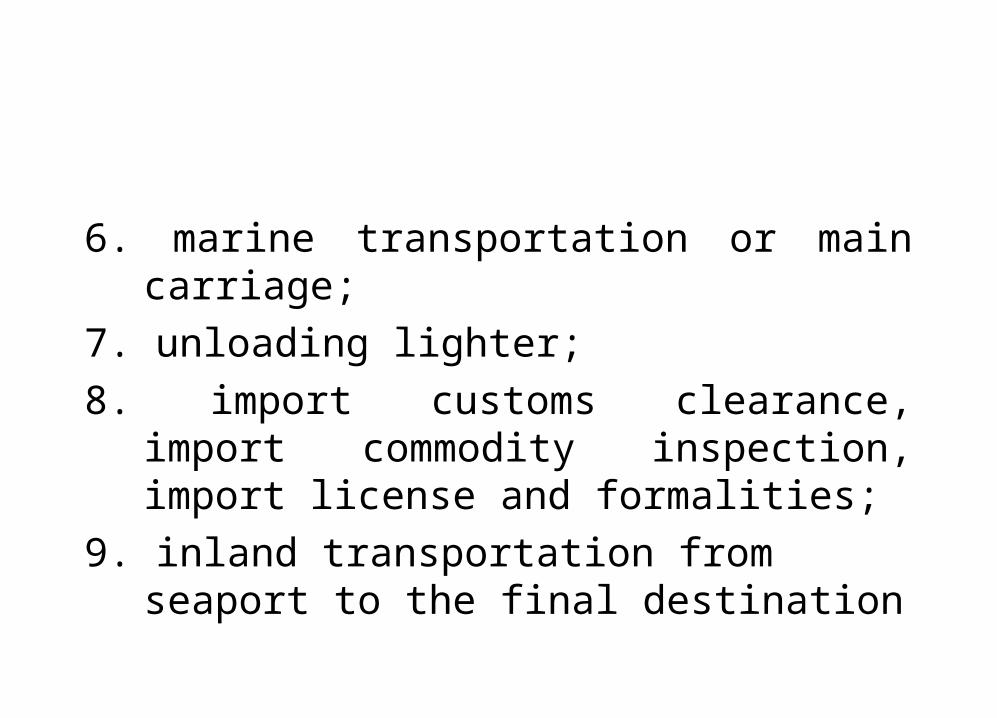

6. marine transportation or main carriage;

7. unloading lighter;

8. import customs clearance, import commodity inspection, import license and formalities;

9. inland transportation from seaport to the final destination

Three Frequently Used Trade Terms (三种常用的装运港交货

贸易术语 )• FOB

• CFR

• CIF

FOB (Free On Board)

• FOB Free On Board …( named port of shipment )船上 交 货 ( … … 指 定 装 运 港 ) (only applicable to sea or inland waterway transport) e.g. FOB Shanghai

• Free on Board means that the seller fulfils his obligation to deliver when the goods have passed over the ship’s rail within the stipulated time of shipment at the named port of shipment. This means the buyer has to bear all costs and risks of loss of or damage to the goods from that point. 指卖方在合同规定的装运港和规定的期限内,将货物装上买方指派的船只,并及时通知买方。货物在装船时越过船舷,风险即由卖方转移至买方。货物在装运港装船时越过船舷后的其它责任、费用也都由买方负担。

• 风险划分点:装运港船舷 (ship’s rail)

Particular Points about Sales under FOB Terms

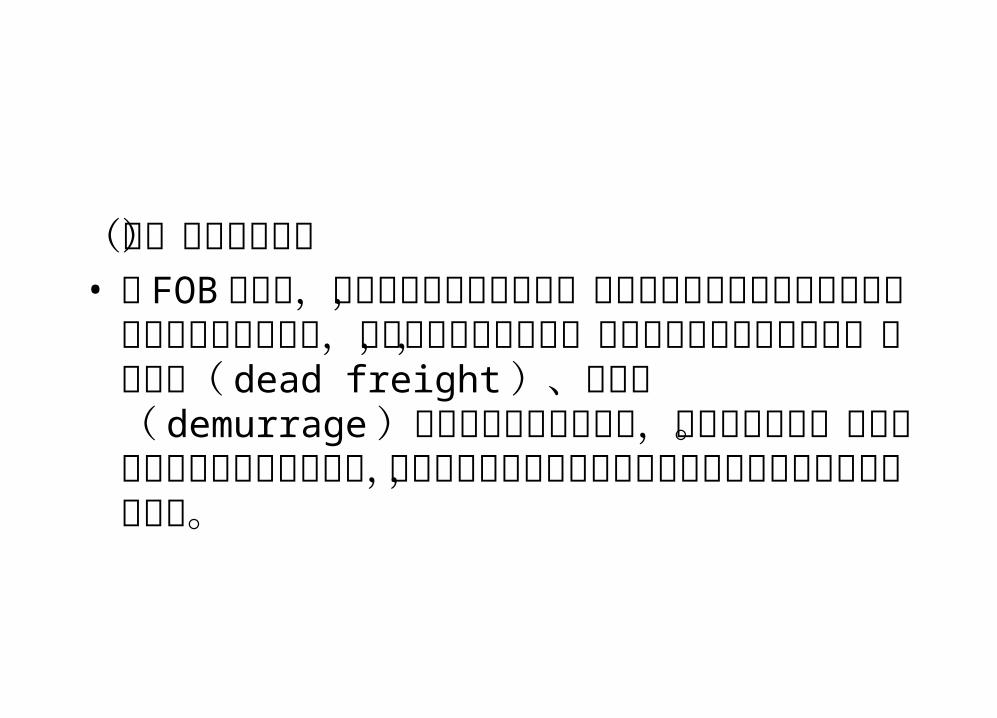

• ( 一 ) “ 船 舷 为 界 ” 的 确 切 含 义 Taking the ship’s rail as the point for division of risks

• 以装运港船舷作为划分买卖双方所承担风险的界限是 FOB 、 CIF 、 CFR 同其它贸易术语的重要区别之一。“船舷为界”表明货物在装上船之前的风险,包括在装船时货物跌落码头或海中所造成的损失,均由卖方承担。以船舷为界只是说明风险划分的界限 , 并不表示买卖双方的责任和费用划分的界限。

(二)船货衔接问题• 在 FOB条件下,如果买方未能按时派船,这包括未经对方同意提前将船派到和延迟派到装运港,卖方都有权拒绝交货,而且由此产生的各种损失,如空舱费( dead freight )、滞期费( demurrage )及卖方增加的仓储费等,均由买方负担。买方指派的船只按时到达装运港,而卖方却未能备妥货物,由此产生的上述费用则由卖方承担。

Variants of FOB

(三)装船费用的负担问题 Loading, trimming, stowing charges

• 为了说明装船费用的负担问题 ,往往在 FOB 术语后加列附加条件 , 形成了 FOB 的变形 , 它们主要有:

• 1 、 FOB Liner Terms (班轮条件)。是指装船费用按照班轮的做法来办,由船方或买方承担,即卖方不负担装船的有关费用。

• 2 、 FOB Under Tackle (吊钩下交货)。指卖方将货物交到买方指定船只的吊钩所及之处 (to have placed the goods under the tackle) ,即吊装入舱以及其它各项费用概由买方负担。

• 3 、 FOB Stowed (理舱费在内)。指卖方负责将货物装入船舱并承担包括理舱费在内的装船费用 (The seller is to bear the cost of stowing as well as loading) 。理舱费是指货物入舱后进行安置和整理的费用。

• 4 、 FOB Trimmed (平舱费在内)。指卖方负责将货物装入船舱并承担包括平舱费在内的装船费用 (The seller is to bear the cost of trimming as well as loading) ,平舱费是指对装入大舱的散装货物进行平整所需要的费用。

• 5 、 FOB Stowed and Trimmed , FOBST, 表明卖方承担包括理舱费和平舱费在内的各项装船费用。

• FOB 的上述变形只是为了表明装船费用由谁负担问题而产生的,它们并不改变FOB 的交货地点以及风险划分的界限。

(四)个别国家对 FOB 的不同解释

• 按照美国的《定义》的解释,买卖双方划分风险的界限不是在船舷 , 而 是 在 船 上 。 American or Canadian businessmen often use “FOB vessel”, which has different implications from those of INCOTERMS 20000. First, the risk dividing point is not the ship’s rail but the board of the ship. Second, the seller is not obliged to implement customs clearance(关于办理出口手续问题上也存在分歧 ).

• 鉴于上述情况,对美国、加拿大等国家的业务中,采用 FOB 成交时,应对有关问题做出明确规定,以免发生误会。特别是进口业务中,除应在 FOB 后注明“ Vessel” 外,还应明确提出由卖方负责取得出口许可证,并支付一切出口税捐及费用 。或在合同中注明“ FOB INCOTERMS 2000” or “This Contract/Confirmation is subject to INCOTERMS 2000, ICC Publication No.560.”)

CFR (Cost and Freight)

• CFR Cost and Freight …( named port of destination )成本加运费(……指定目的港) (only applicable to sea or inland waterway transport)

• Cost and Freight means that the seller must pay the costs and freight necessary to bring the goods to the named port of destination but the risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time the goods have been delivered on board the vessel, is transferred from the seller to the buyer when the goods pass the ship’s rail in the port of shipment.

• 指卖方在合同规定的装运港和规定的期限内,将货物装上船,并及时通知买方。货物在装船时越过船舷,风险即从卖方转移至买方。卖方要负责租船订舱、支付到指定目的港的运费,包括装船费用以及定期班轮公司可以在订约时收取的卸货费用。但从装运港至目的地的货运保险由买方负责办理,保险费由买方负担。

• 按照 CFR 术语成交,需要特别注意的问题是,卖方在货物装船之后必须及时向买方发出装船通知,以便买方办理投保手续

• 风险划分点:装运港船舷

CIF (Cost, Insurance and Freight)

CIF Cost, Insurance and Freight …( named port of destination )成本加保险费、运费(……指定目的港) (only applicable to sea or inland waterway transport)

• Cost, Insurance and Freight means that the seller has the same obligations as under CFR but with the addition that he has to procure marine insurance against the buyer’s risk of loss of or damage to the goods during the carriage. The seller contracts for insurance and pays the insurance premium. 卖方的基本义务是负责按通常的条件租船订舱 (to charter the ship or to book shipping space) ,支付到目的港的运费,并在规定的装运港和装运期内将货物装上船,装船后及时通知买方。卖方还要负责办理从装运港到目的港的海运货物保险 , 支付保险费。

• 风险划分点:装运港船舷

Some Particular Points about CIF

• (一)保险险别问题• Under the CIF term the seller is only required to obtain

insurance on minimum coverage. 卖方应按照合同的规定办理投保 (to effect insurance) 。投保最低的险别,但在买方要 求 时 , 并 由 买 方 承 担 费 用 的情况下 (at the buyer’s expense) ,可加 保战争、罢工、暴乱和 民变险 ( war, strikes, riots and civil commotion risks )。 (risks to cover, the insured amount)

• (二)租船订舱问题• 采用 CIF 术语成交,卖方的基本义务之一是租船订舱,办理从装运港至目的港的运输事项。

Variants of CIF

• ( 三 )卸货 费 用 负 担问题 (Unloading charges)(Please refer to Page 25 of the textbook)

• 1 、 CIF Liner Terms (班轮条件)。• 2 、 CIF Landed (卸至岸上)。• 3 、 CIF Ex Tackle (吊钩下交接 )• 4 、 CIF Ex Ship’s Hold (舱底交接)• CIF的变形也只是为了说明卸货费用的负担问题,并不改变 CIF的交货地点和风险划分的界限。

Symbolic Delivery

• ( 四 ) 象 征 性 交 货 问 题 (Symbolic Delivery or Documentary Transactions.)

• Under CIF, the seller is obliged to effect insurance but he does not bear the risk of loss or damage to the goods during transit. Once he delivered the goods and acquire the necessary documents, he is entitled to the payments of the goods even if the cargoes are lost. This is called Symbolic Delivery or Documentary Transactions. CIF 是一种典型的象征性交货。指卖方只要按期在约定地点完成装运,并向买方提交合同规定的 ( 包括物权凭证在内的 )有关单据,就算完成了交货义务,而无需保证到货。

• 有人称 CIF 为“到岸价”,这是一种误解。其实,按 CIF条件成交时,卖方是在装运港完成交货义务,他并不保证把货送到岸。卖方承担的风险也只限货物越过船舷之前的风险。货物越过船舷之后的风险,概由买方承担。

向承运人交货的三种贸易术语

• FCA (similar to FOB)

• CPT (similar to CFR)

• CIP (similar to CIF)

• Putting the goods into the carrier’s custody is taken as the point for division of risks

1. FCA (Free Carrier )

Free Carrier …( named place )货交承运人(……指定地点 ) (applicable to any mode of transport, including multi-model transport)

• Under FCA, the seller fulfils his obligations to deliver when he has handed over the goods, cleared for export, into the charge of the carrier named by the buyer at the named place

or point.

Some Particular Points about FCA

• FCA 术语适用于包括多式联运在内的各种运输方式。在使用 FCA 术语时,应注意以下几个问题:

• (一) FCA 在不同运输方式下有不同的交货条件• (二)注意 FCA条件下风险转移的问题• FCA 风险转移不是以船舷为界,而是以货交承运人处置时为界。

• (三)明确有关责任和费用的划分问题• 不论在何处交货,卖方都要自负风险和费用,取得出口许可证或其它官方批准证件,并办理货物出口所需的一切海关手续。

• (四) Under FCA, the seller has roughly the same liabilities as in the sales under FOB. The difference between FCA and FOB is that FOB is applicable only to waterway transport while FCA can be applied to all modes of transport.

2. CPT (Carriage Paid to)

Carriage Paid to …( named place of destination )运费付至(……指定目的地) (applicable to all modes of transport)

• The seller pays the freight for the carriage of the goods to the named destination. The risk of loss of or damage to the goods, as well as any additional costs due to events occurring after the time the goods have been delivered to the carrier, is transferred from the seller to the buyer when the goods have been delivered into the custody of the carrier.

• The seller bears roughly the same liabilities as in the sales under CFR.

• 卖方要自负费用订立将货物运往目的地指定地点的运输契约,并且负责按合同规定的时间将货物交给承运人。

• 货物自交货地点支至目的地的运输途中的风险是由买方承担,而不是卖方,卖方只承担货物交给承运人控制之前的风险。

• 从交货地点到指定目的地的正常运费由卖方负担,正常运费之外的其它有关费用,一般由买方负担。

3. CIP (Carriage and Insurance Paid to )

Carriage and Insurance Paid to …( named place of destination )运费、保险费付至(……指定目的地)

• Under CIP, the seller has the same obligations as under CPT but with the addition that he has to procure cargo insurance against the buyer’s risk of loss of or damage to the goods during the carriage. The seller contracts for insurance and pays the insurance premium.The only difference lies in that CIP is not only applicable to sea transport or inland waterway transport but also to other modes of transport. 卖方要负责订立运输契约并支付将货物运达指定目的地的运费,还要办理货物运输保险,支付保险费。卖方在合同规定的装运期内将货物交给承运人,或第一承运人的处置之下,即完成交货义务。交货后及时通知买方,风险也于交货后转移给买方。

其他贸易术语 • 1. EXW - Ex Works (… named place): --(applicable to all

modes of transport including multi-modal transport) The seller fulfils his obligation to deliver when he has made the goods available at his premises (i.e. works, factory, warehouse, etc) to the buyer. It may be written as follows: US$380 per dozen EX Works Shaoxing.

• 2. FAS – Free Alongside Ship( … named port of shipment): (only applicable to sea or inland waterway transport) The seller fulfils his obligation to deliver when the goods have been placed alongside the vessel on the quay or in the lighters at the named port of shipment. It requires the seller to clear the goods for export according to INCOTERMS 2000 version.

• 3. DAF – Delivered at Frontier (... named place): (applicable to all modes of transport, including multi-modal transport) The seller fulfils his obligation to deliver when he has made the goods available to the buyer, cleared for export, at the named point and place at the frontier, but before the customs border of the adjoining country. It may be written as “DAF Manzhouli”.

• 4. DES – Delivered Ex Ship (… named port of destination): (only applicable to sea or inland waterway transport) The seller fulfils his obligation to deliver when the goods have been made available to the buyer on board the ship, uncleared for import at the named port of destination.

• 5. DEQ – Delivered ex Quay (duty paid) (… named port of destination): : (only applicable to sea or inland waterway transport) The seller fulfils his obligation to deliver when he has made the goods available to the buyer on the quay at the named port of destination. Duties, taxes and other official charges payable upon importation are to be borne by the seller. The buyer is required under DEQ to clear the goods for importation.

• 6. DDU – Delivered Duty Unpaid (… named place of destination): (applicable to all modes of transportation) The seller fulfils his obligation to deliver when he has made the goods available to the buyer at the named place of destination. The buyer bears the duties, taxes and other charges payable upon importation and carries out customs formalities.

• 7. DDP – Delivered Duty Paid (… named place of destination): (applicable to all modes of transportation) The seller fulfils his obligation to deliver when he has made the goods available to the buyer at the named place in the country of destination. While Ex Work represents the minimum obligation for the seller, DDP represents the maximum

obligation for the seller.

Factors Affecting the Choice of Trade Terms

• It is necessary to take into consideration the following factors in deciding which one of the 13 trade terms is to be used in an international transaction:

• Mode of transport• Nature of commodity• Quantity of goods• Cost of freight/carriage(distance, transshipment, fluctuation

of freight, etc)• Risks• Customs clearance (including import and export)

Objectives of International Contracts

• “Objectives” here refers to common objectives of both parties to a commercial contract with regard to their rights and duties in the execution of the contract.

• Goods are dispensable to international trade. And whether visible or invisible, goods have their qualities, and the quality of a certain kind determines to a great degree its market and price. Hence the description (including the quality, quantity and packing) of the goods is among the main terms upon which a sales contract is based and constructed.

Name of Commodity

• Name of commodity must be

• definite and specific

• internationally recognized

• practical, realistic and truthful

• given for the sake of cost reduction and facilitation of customs clearance.

Quality of Goods

• The quality of the goods refers to the intrinsic attributes and the outer form or shape of the goods.

• The intrinsic properties mean the chemical composition, mechanical performance, biological features, and the like, while its outer form or shape is manifested in the modeling, structure, color, and luster (shiny appearance) of the goods.

• In another sense, a certain kind of goods possesses both natural and social attributes. From a narrow point of view, it possesses natural attributes, while from a broad point of view, it also includes its social attributes, that is, how it meets the subjective requirements and different tastes of its customers.

Methods Used to Express the Quality of Goods

• Different methods are employed to express the quality of different goods in IB. These methods include sales by inspection, by sample, by specification, by grade, by standard, by brand or trade mark, by description, by drawing or diagram, etc.

Sales by Inspection

• Sales by inspection is concluded with the spot inspection by the buyers or their agents and the quality is determined thereof. This method is of special necessity for particulars goods such as ornaments, jewels, paintings and artworks, etc. It is often used in consignment, auction, fairs and sales,etc.

• In many cases, the buyer may be advised to arrange for inspection of the goods before or at the time they are handed over by the seller for carriage (pre-shipment inspection or PSI). Unless the contracts stipulates otherwise, the buyer would himself have to pay the cost for such inspection that is arranged in his own interest.

Sales by Sample

• A sample is a product, often taken out from a whole lot of consignment or specially designed and processed. It is given for perspective customers to see and buy the product or set aside as the quality standard of the whole consignment. Garments, light industrial products, and agricultural native

produce are generally sold by sample. • Sales by sample falls into two categories: sales by seller’s

sample and sales by buyer’s sample.

Sales by Seller’s Sample

• Samples are usually provided by the seller. When the sample is accepted by the buyer in quality, the seller is obliged to deliver goods of the same quality as shown by the sample. In case the goods delivered by the seller do not correspond with the sample in quality, the buyer is entitled to claim compensation for losses or reject the goods. That is to say, the goods must be the same as its sample represents. Also, having sent a sample to the buyer, the seller should retain another sample of the same quality for later reference. This is called a duplicate sample. The exporter sometimes needs also to send another sample to the commercial inspection bureau if commercial inspection is needed for export.

• Some samples are marked as being “sample for your reference only”. They are then reference samples and are not binding upon the seller. They are for sales promotion only.

Sales by Buyer’s Sample

• Samples can also be provide by the buyer. They are given as the quality standard for the goods to be produced and delivered by the seller. Under such circumstances, to avoid future disputes over the quality of the goods, the seller usually first duplicates the sample and then sends the duplicate to the buyer for confirmation. This confirmed sample is called counter sample(“ 对等样品” or“回样” ).

• Before producing what the buyer’s sample requires, the seller should first make sure that he has the necessary technical and productive resources. Besides, it is necessary for the seller to declare in the contract that any disputes arising from property right shall be tackled by the buyer.

Particular Points about Sales by Sample

• 1. Under Sales by Sample, the quality of the goods delivered must be in exact conformity with that of the sample.

• 2. 以样品表示品质的方法,只能酌情采用。• 3.It is sometimes impossible to deliver the goods that is

exactly the same as the sample provided earlier, thus a flexible clause is found in a contract. For example, “Quality shall be about equal to the sample.” or “Quality is nearly the same as the sample.”