ravi bharti axa

TRANSCRIPT

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 1/84

SUMMER TRAINING PROJECT REPORT

BHARTI AXA LIFE INSURANCE

SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENT OFBACHELOR OF BUSINESS ADMINISTRATION (BBA)

GURU NANAK DEV UNIVERSITY, AMRITSAR

A STUDY ON MARKETING STRATEGIES INVOLVED IN

SELLING LIFE INSURANCE

TRAINING SUPERVISOR SUBMITTED BY

PARAG AGGAWAL RAVI MISHRA

BRANCH MANAGER Enrollment No.

SESSION 2006-2009

GURU NANAK DEV UNIVERSITY, AMRITSAR

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 2/84

PREFACE

The insurance industry plays a number of important roles in India’s booming

economy.

Insurance is necessary to protect enterprises against risks such as theft, fire and

natural disasters. Individuals require insurance services in such areas as health care and

life. They also require insurance against property, theft, fire and natural calamities. The

insurance industry also provides crucial financial intermediary services, transferring funds

from the insured to various sectors of economy for capital formation, a critical need for

India's continued economic expansion.

Chapter one highlights the Origin of Insurance in world and in India. Chapter two puts

forth the research methodology. Chapter three brings to the readers concept of Business

Development Strategies and its application in Insurance Industry. This is followed by data

analysis and recommendation.

This project is going to be helpful to Bharti axa in analysing the Marketing Strategies.

2

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 3/84

ACKNOWLEDGEMENT

I wish to express my gratitude to my organizational guide and project in charge

Mr. Parag Aggarwal for his valuable guidance and providing me an opportunity to do this

project. This project was a great source of learning and a good experience as it has made

me aware of the professional culture and conducts that exists in an organization.

I express my deep sense of gratitude to our faculty of marketing. His experience helped me

a lot in completing this project successfully in time.

I would like to express my innate sense of gratitude to my parents and friends who

encouraged me a lot during the project and without their assistance and affection this

project would not have been completed. It thanks them for being there.

The help provided to me by the entire sales division of Bharti axa also obliges me.

RAVI MISHRA

3

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 4/84

ABSTRACT

Someone has greatly said that practical knowledge is far better than classroom teaching.

During this project I fully realized this and come to know about the present real world

scenario of Life Insurance in India.

The topic of my project report was “A Study on Marketing Strategies involved in selling

Life Insurance” with reference to Bharti Axa I have done this by applying various tools like

through direct interaction with advisors and sales managers, by consulting with marketing

department, by filling up the Questionnaire, etc.

The report contains first of all brief introduction about the company. Then it contains the

complete description of the job done and in the last the growth opportunities and

suggestions.

The undertaken project is aimed at the learning & experimenting all the guidelines and

factors that a Life Insurance Company must consider for selling its products. The study was

mostly concerned with the study and implementation of Marketing Strategies i.e. various

steps undertaken by the company to increase its sale and thus increasing its market share.

In the starting of the project the scope of the project was decided as:

• To study all the factors related to marketing of the products of a life insurance

company.

• To find various criteria for selecting a particular strategy.

• To design a theoretical and applicative framework of How to sell life insurance by

achieving competitive advantage.

• To study the factors which contribute major role in selling Life Insurance.

4

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 5/84

Main objective of the project is to consider all the factors related to strategies involved in

selling of life insurance with different modes & methods and then to come up with

different scenarios in which a particular way of selling the insurance product is best suited.

Also the proposed models and scenarios are stated in a way to help the company in

selection of the particular strategy to fulfill some specific orders.

The methodology for the project was the study of literature available on Internet, library

and other sources and its application directly on the process.

5

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 6/84

CONTENTS

CHAPTAR NO. TITLE PAGE NO.

1. INTRODUCTION 1

1.1 OVERVIEW OF THE INDUSTRY

1.2 PROFILE OF THE ORGANIZATION

1.3 PROBLEMS OF THE ORGANIZATION

1.4 COMPETITION INFORMATION

1.5 S.W.O.T. ANLYSIS

2. RESEARCH METHODOLOGY 26

2.1 SIGNIFICANCE

2.2 MARGINAL USEFULNESS OF THE STUDY

2.3 OBJECTIVE OF THE STUDY

2.4 SCOPE OF THE STUDY

2.5 METHODOLOGY

3. CONCEPTUAL DISCUSSION 31

4. DATA ANALYSIS 52

5. CONCLUSION AND RECOMMENDATIONS 61ANNEXURES 66

BIBLIOGRAPHY 69

6

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 7/84

7

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 8/84

Chapter 1

INTRODUCTION

1

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 9/84

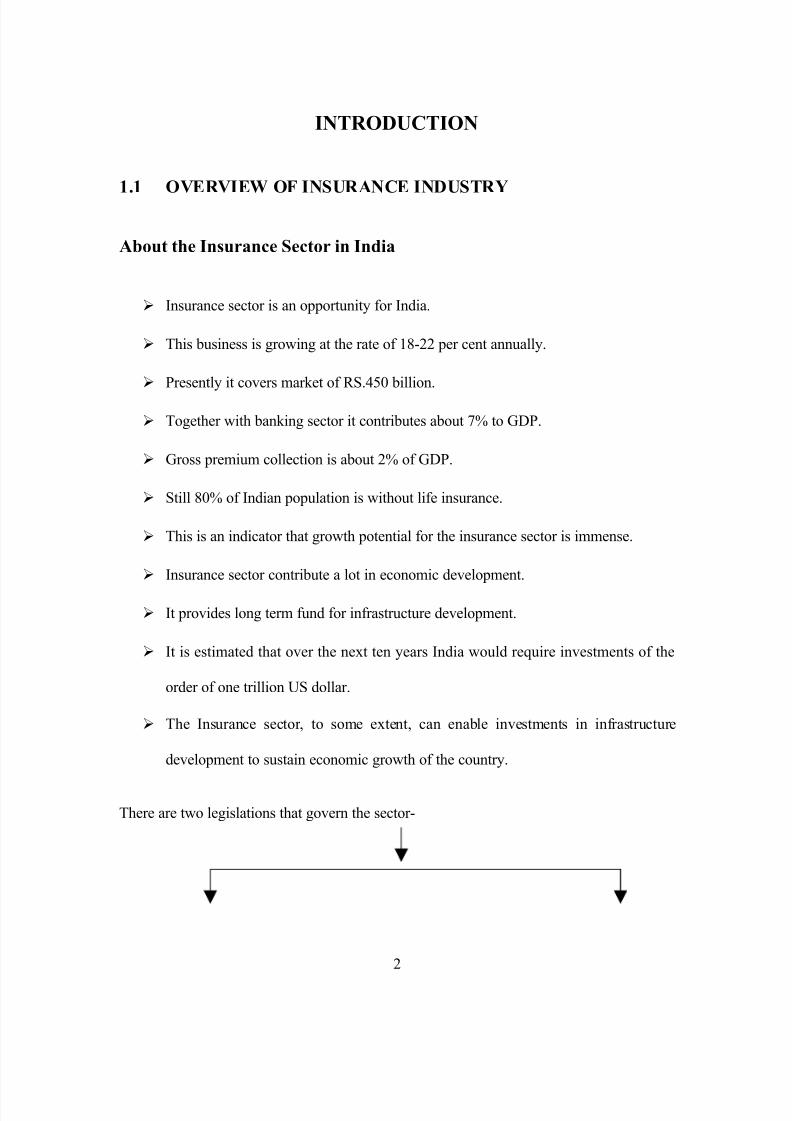

INTRODUCTION

1.1 OVERVIEW OF INSURANCE INDUSTRY

About the Insurance Sector in India

Insurance sector is an opportunity for India.

This business is growing at the rate of 18-22 per cent annually.

Presently it covers market of RS.450 billion.

Together with banking sector it contributes about 7% to GDP.

Gross premium collection is about 2% of GDP.

Still 80% of Indian population is without life insurance.

This is an indicator that growth potential for the insurance sector is immense.

Insurance sector contribute a lot in economic development.

It provides long term fund for infrastructure development.

It is estimated that over the next ten years India would require investments of the

order of one trillion US dollar.

The Insurance sector, to some extent, can enable investments in infrastructure

development to sustain economic growth of the country.

There are two legislations that govern the sector-

2

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 10/84

The Insurance Act- 1938 The IRDA Act- 1999.

3

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 11/84

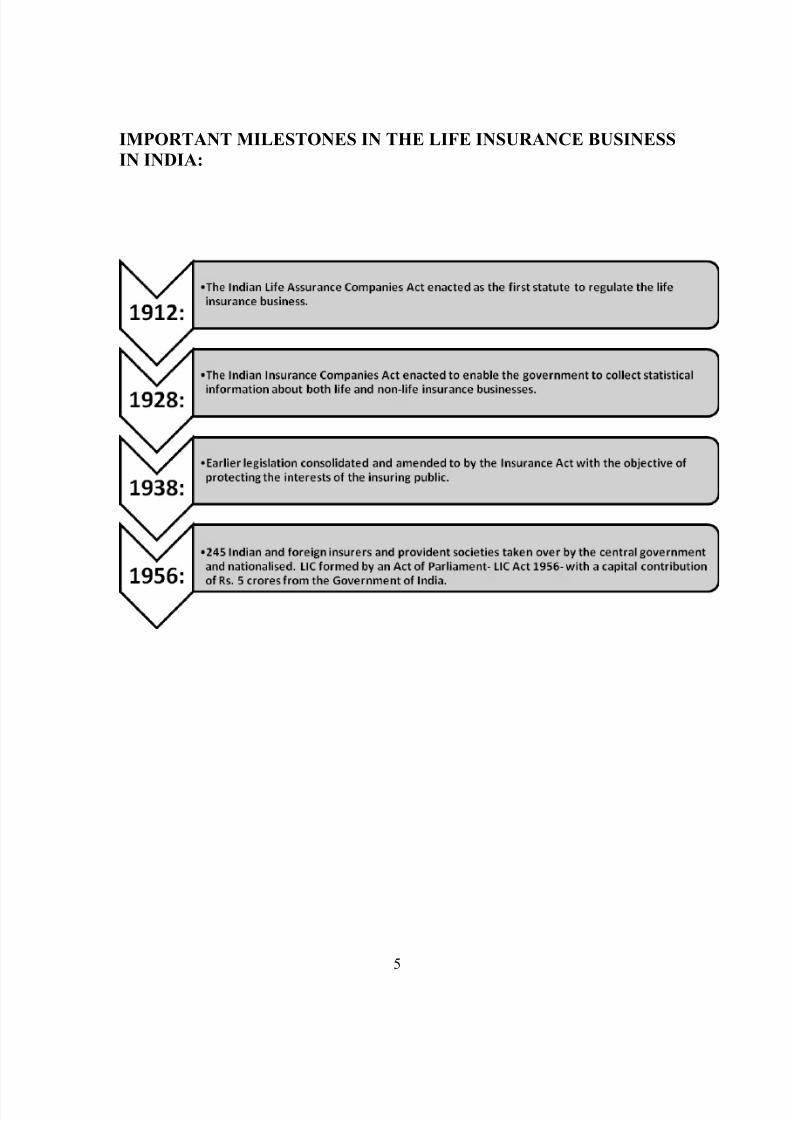

HISTORICAL PERSPECTIVE

In 1818 it was conceived as a means to provide for English Widows.

The Bombay Mutual Life Insurance Society started its business in 1870.

It was the first company to charge same premium for both Indian and non-Indian

lives.

The Oriental Assurance Company was established in 1880.

Till the end of nineteenth century insurance business was almost entirely in the

hands of overseas companies.

Insurance regulation formally began in India with the passing of the Life Insurance

Companies Act of 1912 and the provident fund Act of 1912.

Several frauds during 20's and 30's sullied insurance business in India.

By 1938 there were 176 insurance companies.

The first comprehensive legislation was introduced with the Insurance Act of 1938

that provided strict State Control over insurance business.

The insurance business grew at a faster pace after independence.

The Government of India in 1956, brought together over 240 private life insurers

and provident societies under one nationalized monopoly corporation and Life

Insurance Corporation (LIC) was born.

Nationalization was justified on the grounds that it would create much needed funds

for rapid industrialization.

4

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 12/84

IMPORTANT MILESTONES IN THE LIFE INSURANCE BUSINESS

IN INDIA:

5

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 13/84

INSURANCE SECTOR REFORMS

In 1993, Malhotra Committee- headed by former Finance Secretary and RBI Governor

R.N. Malhotra- was formed to evaluate the Indian insurance industry and recommend its

future direction. The Malhotra committee was aimed at creating a more efficient and

competitive financial system suitable for the requirements of the economy keeping in mind

the structural changes currently underway and recognising that insurance is an important

part of the overall financial system where it was necessary to address the need for similar

reforms. In 1994, the committee submitted the report and some of the key

recommendations included:

i) Structure: Government stake in the insurance Companies to be brought down to 50%.

Government should take over the holdings of GIC and its subsidiaries so that these

subsidiaries can act as independent corporations. All the insurance companies should be

given greater freedom to operate.

ii) Competition: Private Companies with a minimum paid up capital of Rs.1bn should be

allowed to enter the sector. No Company should deal in both Life and General Insurance

through a single entity. Foreign companies may be allowed to enter the industry in

collaboration with the domestic companies. Postal Life Insurance should be allowed to

operate in the rural market. Only one State Level Life Insurance Company should be

allowed to operate in each state.

6

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 14/84

iii) Regulatory Body: The Insurance Act should be changed. An Insurance Regulatory

body should be set up. Controller of Insurance- a part of the Finance Ministry- should be

made independent

iv) Investments: Mandatory Investments of LIC Life Fund in government securities to be

reduced from 75% to 50%. GIC and its subsidiaries are not to hold more than 5% in any

company (there current holdings to be brought down to this level over a period of time)

v) Customer Service: LIC should pay interest on delays in payments beyond 30 days.

Insurance companies must be encouraged to set up unit linked pension plans.

Computerization of operations and updating of technology to be carried out in the

insurance industry.

The committee felt the need to provide greater autonomy to insurance companies in order

to improve their performance and enable them to act as independent companies with

economic motives. For this purpose, it had proposed setting up an independent regulatory

body- The Insurance Regulatory and Development Authority.

Reforms in the Insurance sector were initiated with the passage of the IRDA Bill in

Parliament in December 1999. The IRDA since its incorporation as a statutory body in

April 2000 has fastidiously stuck to its schedule of framing regulations and registering the

private sector insurance companies. Since being set up as an independent statutory

body the IRDA has put in a framework of globally compatible regulations. The other

decision taken simultaneously to provide the supporting systems to the insurance sector and

in particular the life insurance companies was the launch of the IRDA online service for

7

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 15/84

issue and renewal of licenses to agents. The approval of institutions for imparting training

to agents has also ensured that the insurance companies would have a trained workforce of

insurance agents in place to sell their products.

PRESENT SCENARIO

The Government of India liberalized the insurance sector in March 2000 with the passage

of the Insurance Regulatory and Development Authority (IRDA) Bill, lifting all entry

restrictions for private players and allowing foreign players to enter the market with some

limits on direct foreign ownership. Under the current guidelines, there is a 26 percent

equity cap for foreign partners in an insurance company. There is a proposal to increase

this limit to 49 percent.

The opening up of the sector is likely to lead to greater spread and deepening of insurance

in India and this may also include restructuring and revitalizing of the public sector

companies. In the private sector 15 life insurance companies have been registered. A host

of private Insurance companies operating in life segments have started selling their

insurance policies since 2001. Table shows the current market players in the life Insurance

Industry (Source IRDA).

LIFE INSURANCE SCENARIO IN INDIA

Since 1956, with the nationalization of insurance industry, the state-run LifeInsurance Corporation of India (LIC) has held the monopoly in country’s life

insurance sector. General Insurance Corporation of India (GIC), with its four

subsidiaries, was its counterpart in the casualty sector. Over the time, taking

advantages of its monopoly and virtual prerogative in establishing premiums, LIC

8

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 16/84

has evolved into a monolith. With around 60,000 agents in every nook and corner of

the vast country, it has created an enviable brand name, particularly among the rural

population of the country. It has around $40 billion as its financial sector. However,

on the qualitative side, it has every little to take pride in. And there lies the potentialfor players to challenge this behemoth.

As is typical with monopolies, the premium rates charged LIC are among the

highest in the world, and its track record in customer service can at best be called

shabby. With a huge unionized, rigid workforce mostly in the clerical category, LIC

run the risk of high fixed cost, which will be the deciding factor productivity in the

competitive scenario. While boasting full-scale automation of its operation, the truth

is that its technology is outdated. The new players, with the state-of-the –art

technology under the belt, will be in advantageous position. 80% of LIC’s business

is procured by 20% of its ill-trained agent force. The foreign player, with the

domestic partner’s string band value, can test the unconventional distribution

channels like brokers, the Internet, the banking distribution system etc., although

foreign players may be tempted to keep their operations in big cities for the ‘cream

layer’ of the society, the real market lies in rural India, which accounts for the lion’sshare of LIC’s present business.. The foreign companies need to know the “ground

realities” to the details.

PRIVATIZATION OF INSURANCE

The Indian Insurance sector has finally opened up and it is with much anticipation

that new players are awaiting their share of market. License have been issued to

both Indian and foreign players- Reliance, HDFC-Standard Life, Max India-New

York, Royal Sundaram Alliance, Bharti Axa Life Insurance, IFFCO-Tokyo Marine,

Bajaj Allianz, Birla Sun life, Tata AIG, AVIVA Life Insurance, SBI Life, OM

Kotak Mahindra are some of the entrants into the newly liberalized Indian Insurance

market.

9

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 17/84

ICICI Prudential Life Insurance and HDFC-Standard Life have issued their life

policies-the first from the private sector after 45 years. The first move for the

liberalization came with the Malhotra Committee Report in 1993 which

recommended the privatization of insurance, setting of an insurance regulatoryauthority and restructuring the government monopoly LIC and GIC and its

subsidiaries. IRDA Act passed in November 1999 had set ball rolling for the entry

of private players in domestic sector.

IRDA

The insurance sector has been opened up in India, as there was an urgent need. The

international experience indicates those country with a liberalized insurance sector

have witnessed a rapid growth in premium volumes enhancing the domestic saving

rate. This happened in China, Malaysia and Singapore where a competitive market

has led to improvement in services and quicker settlement of claims.

It is also important to note that competition will bring about advancement in

information, communication and technology. And rightly therefore a decision was

taken by the Government of India to open up insurance sector. The establishment of

IRDA in the month of April 2000 has been important development in this direction,

making the end of monopoly in the insurance sector.

The IRDA Governs the critical aspect of insurance sector including:

The number and role of Private sector operates including-Roman area

intermediaries.

Regulate covering investment, solvency norms etc.

Product range.

10

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 18/84

Accounting practices.

Consumer protection norms.

Ensuring the rural and health insurance are developed.

Fixing of license fee.

Perhaps of all the most critical regulation is the 26% equity Capital for foreign

Insurers. This regulation bring in issues regarding management control and one of

the reasons for joint venture breaking up Cubb-Kotak, Liberty-Dabur, All State-

Dabur, Manu Life-UTI are some of the broken up alliances.

LIBERALIZATION OF INSURANCE SECTOR

Liberalization commitment of the country to help in disciplining future economic

policies will include the insurance reforms. When world over insurance market has

been opened up. India cannot remain in isolation. History has shown that it is very

difficult to prosper in isolation.

Globalization is the new economic reality, which is here to stay, heralding a new era

of insurance in India.

With the opening of the insurance industry, India stands to gain with the following

major advantages.

⇒

Globalization will provide opportunities to the customer for the better production. With more reasonable and affordable pricing.

⇒ The customer will get quicker services.

⇒ It will enhance the saving rate.

11

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 19/84

⇒ Long term funds for infrastructure development will be available to the country.

⇒ It will secure for India larger inflow of foreign capital need to sustain our GDP

growth.

ADVANTAGES OF LIBERALIZATION

⇒ The opening up will enable the country to save more and invest more for the

development in infrastructure.

⇒ With new insurance intermediaries and more distribution channels the market

is bound to develop by leaps and bounds.

⇒ In the next few years it is established that the Indian insurance sector will

develop a better understanding of consumer requirement leading to more

satisfaction of consumers.

⇒ The world class technology will be available in the market bringing about

tremendous improvement in servicing.

⇒ Choice of price will be available to the customers.

⇒ Lead to increase in employment.

⇒ Social and rural obligations will also be served as IRDA has come out with

clear regulation in this regard, which makes the development in this area

mandatory.

⇒ Global competitors will help in building expertise with their global practice.

⇒ Unlike west, in India, insurance is sold as the instrument of saving. About

18%of the policies are sold as death risk consideration. Impression about LIC is

12

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 20/84

that they are not meant for the market requirements. They are only intended to

find customers. Insurance awareness is therefore low. Unit linked insurance

products are not available. Insurance covers are expensive and returns are low.

Turn over the agent is high. The choice available to the insuring public isinadequate in terms of services, products and prices. These are the areas of

weakness, which may act as opportunities for new players who may work to

offer policies to the customer with the value additions at a competitive premium

with much improved servicing.

INSURANCE IN INDIA

Only 22% of the insurance population has been extended cove r. Market penetration

is low and the potential to exploit is high. Insurance premium per capita is very low.

Lack of comprehensive social system benefit and welfare means that demand for

pension products is high. Huge middle class of approximately 300 million.

EXISTING INSURANCE COMPANY SCORE LOW ON CUSTOMER

SERVICE FRONT

The insurance market registered growth in the Asian region even though India’s

share in global insurance premium is less than 0.5% (1998) as compared to USA

(24.2%) and Japan (21%). Studies have revealed that in an emerging market, as

disposable income rises, Insurance premium as a ratio of GDP shoots up. The

confederation of Indian Industry projected a growth of life insurance premiums from

Rs. 350 billion at present to Rs. 140 billion. The growth of non-life insurance

premium is expected to increase from 75 billion to 375 billion. Out of which, only

10% is tapped by the existing insurer.

Insurance even more than banking is a volume game. A very exclusive approach in

view is unlikely to provide meaningful numbers. Currently, insurance is bought for

13

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 21/84

the purpose of tax-benefits. A higher percentage of business is in the rural market.

The share of rural new business insurance total new business is 55% in terms of

policies and 47% in terms of sum assured. However, this needs to be viewed in the

light of some recent issues that have been raised regarding as to what constitutes therural market. Therefore, private insurers will be best served by middle market

approach, targeting the customer segments that are presently unexploited.

How many Indians are aware that LIC has more than 60 products and GIC has more

than 180 products. Not only there is a reduction in the premiums of life insurance

products have long overdue since Indian mortality rate has decreased three folds in

the last 50 years. There is also scope to increase the yield on life insurance policies

(presently 6%) with proper risk management in place.

It is been debated that insurance business does not produce profit in the first five

years cross subsidization is a feature of Indian market. Even the first portfolio vote

that is considered profitable, cross subsidizes the other departments. Tariff reduction

is likely to reduce profits, further insurers have to institute proper claims

management progress in order to extract efficiencies. At present life insurance

business in the country is taxed at 12.5% of the profit in financial year. The

government is soon to present a new model of taxing life insurance companies at

international rates.

New entrants should be well advised to look ahead to the stage where brand strength

will be a competitive advantage and sketch their alliances accordingly. In fact, we

believe that alliance related to distribution rather than to products and technology

will prove most valuable.

The stages where brand strength will be competitive advantage and sketch their

world accordingly. In fact we believe that alliance related to distribution rather than

to produce or technology will prove most valuable in the long run.

14

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 22/84

Banks and financial companies will emerge, as attractive distribution channel for

this insurance trend will be led by two factors, which already apply in other world

markets. First Banking food insurance, fund management and other financial

services companies are being to increase their profitability and provide maximumvalue to their customers. Therefore, they are themselves looking for a range of

products to distribute.

In other market notably Europe; this has resulted in bank assurance. Bank entering

into the insurance business in India to bank hope to maximize expensive existing

network by selling a range of products more of a loss alliance between insurance

and bank than a formal ownership. Some Indian entrants like ICICI, HDFC, Bharti

Axa and reliance hope to ride their existing network and customer bases.

1.2 COMPANY PROFILE

Bharti AXA Life Insurance is a joint venture between Bharti, one of India’s leading

business groups with interests in telecom, agri business and retail, and AXA, world leader

in financial protection and wealth management. The joint venture company has a 74%

stake from Bharti and 26% stake of AXA.

The company launched national operations in December 2006. Today, we have over 5200

employees across over 12 states in the country. Our business philosophy is built around the

promise of making people "Life Confident".

As we expand our presence across the country to cater to your insurance and wealth

management needs with our product and service offerings, we continue to bring 'life

confidence' to customers spread across India. Whatever your plans in life, you can be

confident that Bharti AXA Life will offer the right financial solutions to help you achieve

them.

15

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 23/84

VISION

To be a leader and the preferred company for financial protection and wealth management

in India

VALUES

• Professionalism

• Innovation

• Team Spirit

• Pragmatism

• Integrity

STRATEGY

• To achieve a top 5 market position in India through a multi-distribution, multi-

product platform

• To adapt AXA's best practice blueprints as a sound platform for profitable growth

• To leverage Bharti's local knowledge, infrastructure and customer base

• To deliver high levels of shareholder return

• To build long term value with our business partners by enhancing the proposition to

their customers

• To be the employer of choice to attract and retain the best talent in India

• To be recognised as being close and qualified by our customers

16

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 24/84

Strategic Differentiators

• Strong partner Bharti - provides access to customer base of more than 20 million

• Multi channel execution capability

• Current Asia product range which is a strong match to products sold to the mass

and mass affluent

• Global scale providing cost effective and speedy re-use of systems, products and

business capability

•

Strong AXA and Bharti brands which can be leveraged to attract and retain a highquality management team

PRODUCTS

Bharti AXA Life Dream Life Pension

Dream Life Pension, Bharti AXA Life Insurance’s unique pension product ensures that

your retirement life is your Dream Life.

Live your Dreams! Be Life Confident!

Key Benefits:

• Unmatched flexibility for retirement wealth creation

o Pay one time lump sum or regular premiums

o At the inception systematically increase your premiums by 5 % or 8% each

year with the Accumulator Option

o Increase/decrease premiums any time after the 2nd policy year

17

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 25/84

o Add top up premiums any number of times after the 1st policy year

• Dream Life Pension enhances your retirement kitty by providing special addition,

starting from the end of 10th policy year

• Change your planned retirement age any time during the policy term

• Obtain tax benefits as per the prevailing tax laws on the premiums paid and the

benefits received under the policy.

Annuity –Return of Capital

Bharti AXA Life Insurance presents “Immediate Annuity” product, to help secure your golden years. At your vesting age, you have an option to buy annuity from Bharti AXA

Life Insurance or any other annuity provider in India.

Bharti AXA Life Aspire life

Aspire Life helps you create a pool of wealth to meet your long-term needs, while also

providing you adequate protection in case the need arises.

Key Benefits:

• Allocation rates as high as 100% i.e. no allocation charges for premiums greater

than or equal to Rs.50,000 on your investment in the unit-linked fund from year 2 -

to maximize your investment returns.

• Up to 175% of the first year premium paid by you is returned as Guaranteed

Special Addition, at maturity of the policy or on unfortunate event of death of the

Life Insured.

• 3 investment fund options as per your investment preferences.

18

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 26/84

• Flexibility of partial withdrawals after fifth Policy Year, premium holiday option

after seven policy years and facility to switch amongst the investment funds as per

your investment objectives.

• Protection benefit which provides high Sum Assured for longer policy terms.

• Tax benefits under section 80C and 10(10D) of Income Tax Act.

Invest Confident

Presenting Invest Confident, a unique single premium, unit linked investment and

protection product which not only strives to maximise your investment returns but also

gives you an enhanced flexibility to suit it according to your protection needs, because we

at Bharti AXA Life Insurance, believe that your hard earned money deserves nothing but

the best.

Key Benefits:

• Convenient single premium product with policy benefit period till the age of 70.

•

Unique special additions starting from the end of 5th policy year and thereafter atthe end of every 5 years till the maturity date.

• 3 investment fund options as per your investment preferences.

• Basic Sum Assured of five times the single premium.

• Unique option of investing additional amount at your convenience through Top Up

Premiums.

• Flexibility of partial withdrawals after the third Policy Year

• Additional benefit of Rs.5, 00,000 in the event of death due to an accident.

• Tax benefits under section 80C and 10(10D) of Income Tax Act.

19

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 27/84

Bharti AXA Life Wealth Confident

Wealth Confident, a unit-linked investment cum protection product, with its limited

period premium payment facility of 5 years, premium payment flexibility, higher allocation

of your premium for investment, unique special additions and life insurance benefit, not

only makes your money grow but also provides your investment the special treatment that

it deserves.

Key Benefits:

• Pay premium for five years, while your policy continues for ten years.

• Higher allocation of your premium up to 88% for investment.

• Special additions of units added every year from 6th Year for incremental wealth

creation.

• Choose from four different investment funds to meet your financial objectives.

• Five times the life cover of your annual premium.

• Tax benefit under 80C and 10(10D).

Future Confident

"Future Confident is a complete financial solution that serves you in building wealth for

your long-term needs, but most importantly, provides comprehensive financial protection

to your loved ones, against all odds."

Key Benefits:

• Life insurance benefit of up to 420 times the monthly premium.

• Comprehensive overall protection through "Protection Enhancers" in the form of

riders.

20

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 28/84

• Wealth creation for your long term financial needs.

• Special additions at regular intervals, starting from 7th year, to enhance your

wealth.

• Four different investment funds to meet your financial objectives.

• Tax benefit under 80C and 10(10D).

Future Confident II

"Future Confident II is a complete financial solution that serves you in building wealth for

your long-term needs, but most importantly, provides comprehensive financial protectionto your loved ones, against all odds."

Key Benefits:

• Build Wealth for your long term financial needs with enhanced financial protection.

• Sum assured up to 420 times the monthly premium.

• Life insurance benefit as Sum assured PLUS Policy fund value.

• Four different investment funds to meet your financial objectives.

• Comprehensive overall protection through "Protection Enhancers" in the form of

riders.

• Special additions at regular intervals, starting from the end of 7th year, to enhance

your wealth.

• Tax benefit under sections 80C and 10(10D) of Income Tax Act.

21

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 29/84

Save Confident

Save Confident, a traditional money back insurance product, offers you a perfect

combination of liquidity, long term savings and life insurance benefit.

Save Confident with its unique liquidity feature of guaranteed payment for 10 continuous

years, annually compounded bonus accumulation, and a guaranteed life insurance benefit

offers a perfect three-in-one solution for your financial needs.

Key Benefits:

• Traditional money back product with payment term of 10 years.

• Get guaranteed amount back on specified intervals, starting from 6th policy year till

maturity.

• Amount equal to 110% of Sum Assured paid across 10 years.

• Secured growth on savings with Annual Reversionary Bonus, if declared, every

year.

• Savings enhanced by Terminal Bonus, if any, payable at maturity.

• Total protection for your family with guaranteed sum assured plus accrued bonuses.

• Added protection in the event of death due to an accident with payment of

additional amount equal to the basic Sum Assured, subject to maximum of Rs 10

Lakh.

• Tax benefit under sections 80C and 10(10D) of Income Tax Act, 1961.

Secure Confident

All of us desire to maximise the happiness for our family at all times, irrespective of the

circumstances. The thought of unfortunate events befalling us may cause us anxiety about

22

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 30/84

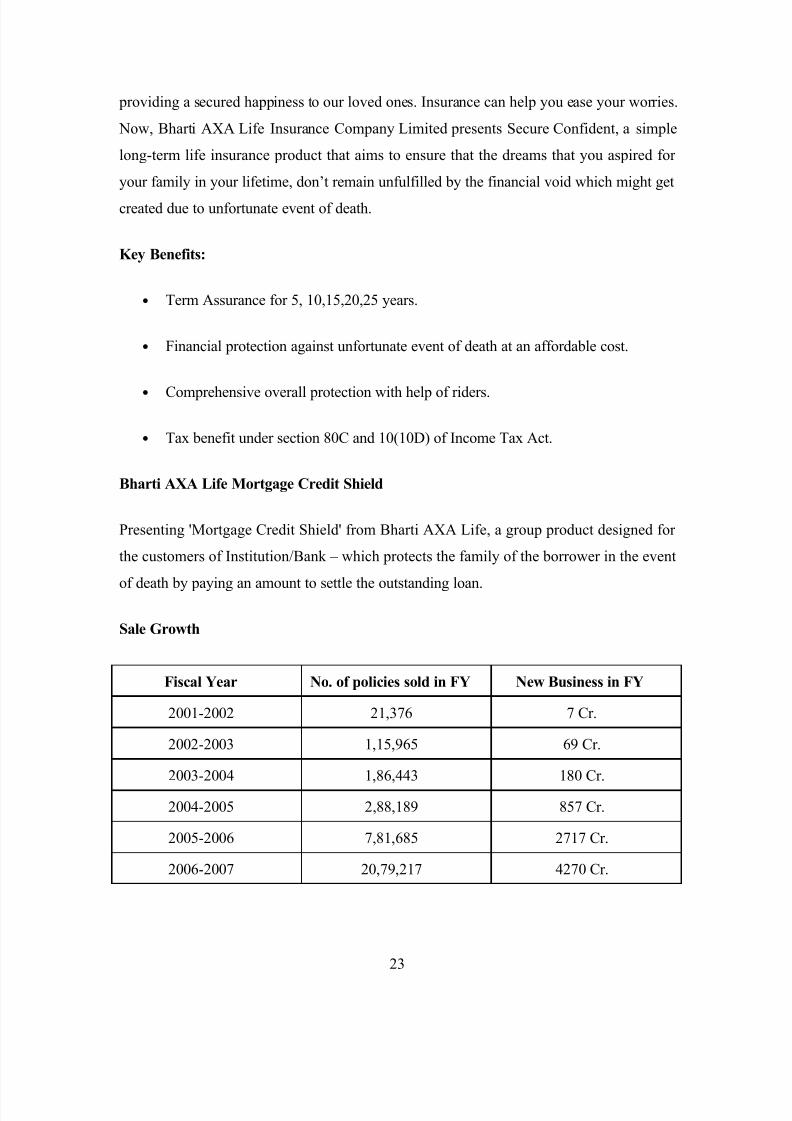

providing a secured happiness to our loved ones. Insurance can help you ease your worries.

Now, Bharti AXA Life Insurance Company Limited presents Secure Confident, a simple

long-term life insurance product that aims to ensure that the dreams that you aspired for

your family in your lifetime, don’t remain unfulfilled by the financial void which might get

created due to unfortunate event of death.

Key Benefits:

• Term Assurance for 5, 10,15,20,25 years.

• Financial protection against unfortunate event of death at an affordable cost.

• Comprehensive overall protection with help of riders.

• Tax benefit under section 80C and 10(10D) of Income Tax Act.

Bharti AXA Life Mortgage Credit Shield

Presenting 'Mortgage Credit Shield' from Bharti AXA Life, a group product designed for

the customers of Institution/Bank – which protects the family of the borrower in the event

of death by paying an amount to settle the outstanding loan.

Sale Growth

Fiscal Year No. of policies sold in FY New Business in FY

2001-2002 21,376 7 Cr.

2002-2003 1,15,965 69 Cr.

2003-2004 1,86,443 180 Cr.

2004-2005 2,88,189 857 Cr.

2005-2006 7,81,685 2717 Cr.

2006-2007 20,79,217 4270 Cr.

23

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 31/84

ORGANIZATION STRUCTURE

DIRECTOR

VICE PRESIDENT

SR. BRANCHMANAGER

BRANCH MANAGER

ASSISTANT BRANCH

MANAGER

SR. SALES MANAGER

ASSISTANT

MANAGER

MANAGEMENT

TRAINEE

SALES MANAGER

24

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 32/84

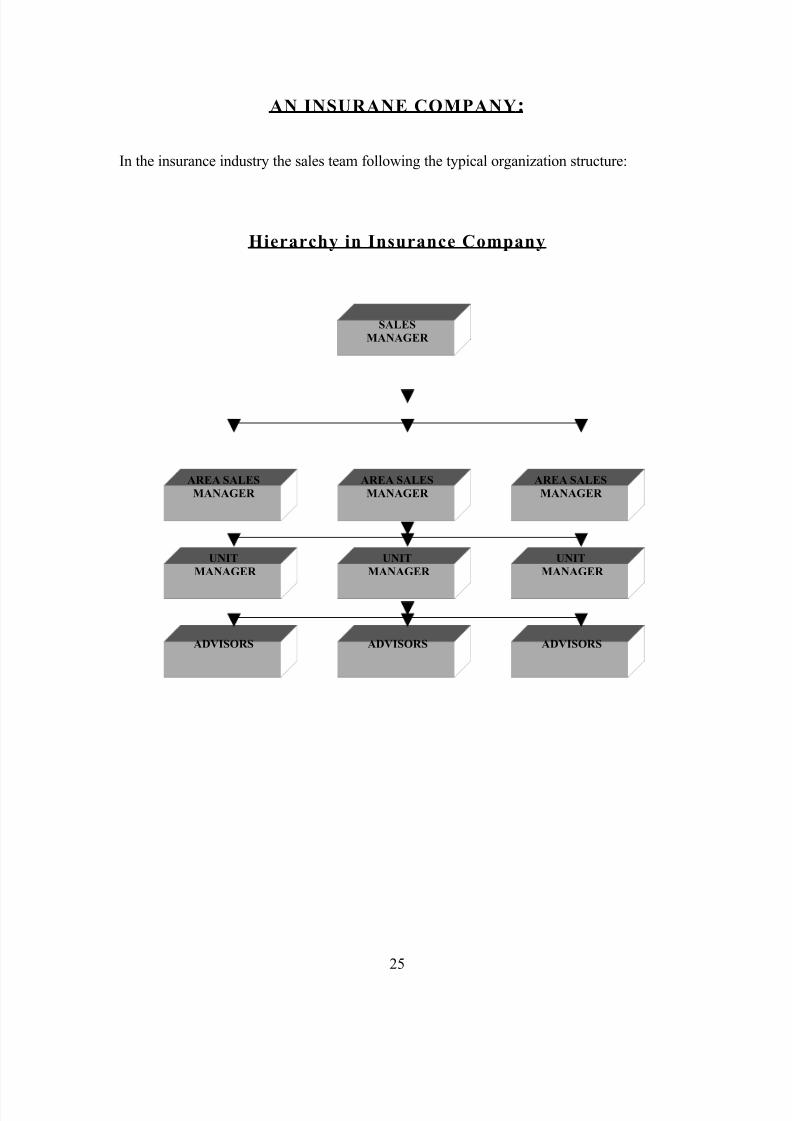

AN INSURANE COMPANY :

In the insurance industry the sales team following the typical organization structure:

Hierarchy in Insurance Company

SALES

MANAGER

AREA SALES

MANAGER

AREA SALES

MANAGER

AREA SALES

MANAGER

UNIT

MANAGER

UNIT

MANAGER

UNIT

MANAGER

ADVISORS ADVISORS ADVISORS

25

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 33/84

FUTURE PLAN OF THE ORGANISATION

Reliance Life Insurance promises to provide higher returns in higher investments.

The plans smart assure will help the customer in wealth creation and is aimed at providing

efficiency affordability and flexibility to customer needs. The product offer the customer a

choice of allocating up to 100% of premium paid beyond specified premium bracket. As

the premium goes up, the allocation charges keep on decreasing with no allocation charges

levied on premium upward rupees 3 lakhs.

26

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 34/84

1.3 PROBLEMS OF THE ORGANIZATION

• Service delivery / Logistics perception is weak

• Negative Environment

• Top management takes large amount of time to approve high value loan borrowers.

1.4 COMPETITORS INFORMATION

Sr. No. Name of the Company

1 Bajaj Allianz Life Insurance Co. Limited

2 HDFC Standard Life Insurance Co. Ltd

3 ICICI Prudential Life Insurance Co. Ltd

4 ING Vysya Life Insurance Co. Ltd.

5 Life Insurance Corporation of India

6 Max New York Life Insurance Co. Ltd

7 Met Life India Insurance Co. Pvt. Ltd.

8 Kotak Mahindra Old Mutual Life Insurance Ltd.

9 SBI Life Insurance Co. Ltd.

10 Tata AIG Life Insurance Co. Ltd.

11 Reliance Life Insurance Co. Ltd.

12 Aviva Life Insurance Co. India Pvt. Ltd.

13 Sahara India Life Insurance Co. Ltd.

14 Shriram Life Insurance Co. Ltd.

15 Bharti AXA Life Insurance Co. Ltd.

27

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 35/84

1.5 SWOT Analysis

STRENGTHS

Premiums are increasing and so are commissions.

The variety of products is increasing.

Transparency in working is followed.

Fund charges are less i.e. 0.8%

Stronger financial base.

Employee centric organization.

WEAKNESSES

Strong competitors like LIC, ICICI Pru, Birla Sun Life etc.

Premium is priced high as compared top the market leader.

Infrastructure cost is high.

Less expenditure on promotion.

Products not customized for lower segment.

OPPORTUNITIES

The ability to cross sell financial services barely being tapped.

Technology is improving to the point that paperless transactions are available.

28

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 36/84

The client's increasing need for an "insurance consultant" can open new ways to

service the client and generate income.

THREATS

Government regulations on issues like health care, mold and terrorism can quickly

change the direction of insurance.

The increasing expenses and lower profit margins. Intense competition from LIC.

29

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 37/84

Chapter 2

RESEARCH METHODOLOGY

30

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 38/84

RESEARCH METHODOLOGY

2.1 SIGNIFICANCE

The main significance of the project is to find out various efforts that an insurance

company has to do in selling its life insurance products.

For any business venture, Business Development Strategies go hand in hand. Opportunities

come and go but business comes from the ones, which are handled properly in terms of

leads. Leads for any new opportunity are very important for it to turn out a profitableventure.

Business Development Strategies work hand in hand for leads.

Promotion plays a very important role in both the departments. Promotion helps us to

market a product properly and also helps in increasing the sale of the product as compared

to competitors.

2.2 MANAGERIAL USEFULNESS OF THE STUDY

This project is very useful to find out the different strategies involved in selling life

insurance products and to know how these factors influence the success of a Private

Insurance Company.

Our sturdy Helps to have sale experience, deal with different customers, overcome the

objections of the customers and It provides a platform where managerial role can be played

effectively and efficiently

31

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 39/84

2.3 RESEARCH OBJECTIVE

• To find out various efforts that an insurance company has to do in selling its life

insurance products.

• To find out different strategies involved in selling life insurance products.

• To get the information about the major factor i.e. Agents and Advisors that

contributes more to the sale of life insurance products.

• To know how these factors influence the success of a PRIVATE insurance

company.

2.4 SCOPE OF THE STUDY

• To study all the factors related to marketing of the products of a life insurance

company.

• To find various criteria for selecting a particular strategy.

• To design a theoretical and applicative framework of How to sell life insurance by

achieving competitive advantage.

• To study the factors which contribute major role in selling Life Insurance.

2.5 METHODOLOGY ADOPTED

The methodology of research indicates the general pattern for organizing the procedure

to assemble effective data for the problems to understudy. The study tries to find out the

kind of strategies and methods that would further enhance the insurance business.

Insurance business mainly aims at recruiting the insurance and advisors who have

entrepreneurial skills and necessary drive to survive and flourish in the present competitive

and ever increasing insurance industry.

32

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 40/84

DATA SOURCE

The universe of study was limited to a particular region that created some problems

while collecting data. The universe was divided in different segments. The process of

segmentation was primarily aimed at simplifying the universe into smaller parts so each

segment can be handled according to its unique features.

Further these segments were divided into several sub-segments because there is

heterogeneity in population of respective areas that needs different marketing strategies to

be adopted in selling insurance products. These were:

• Education of person

• Income of person

• Living style

• Influence of social factors, etc.

These factors were considered at the time of collecting the data and information.

Data Source:

Primary Data collection:

• Direct interaction with marketing and sale department of Bharti Axa

• Questionnaires were used to collect individual’s data, etc.

Secondary Data Collection:

• Bharti Axa’s journals

• Internet

33

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 41/84

• Books on Insurance marketing

• Yellow Pages

34

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 42/84

Chapter 3

CONCEPTUAL DISCUSSION

35

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 43/84

CONCEPTUAL DISCUSSION

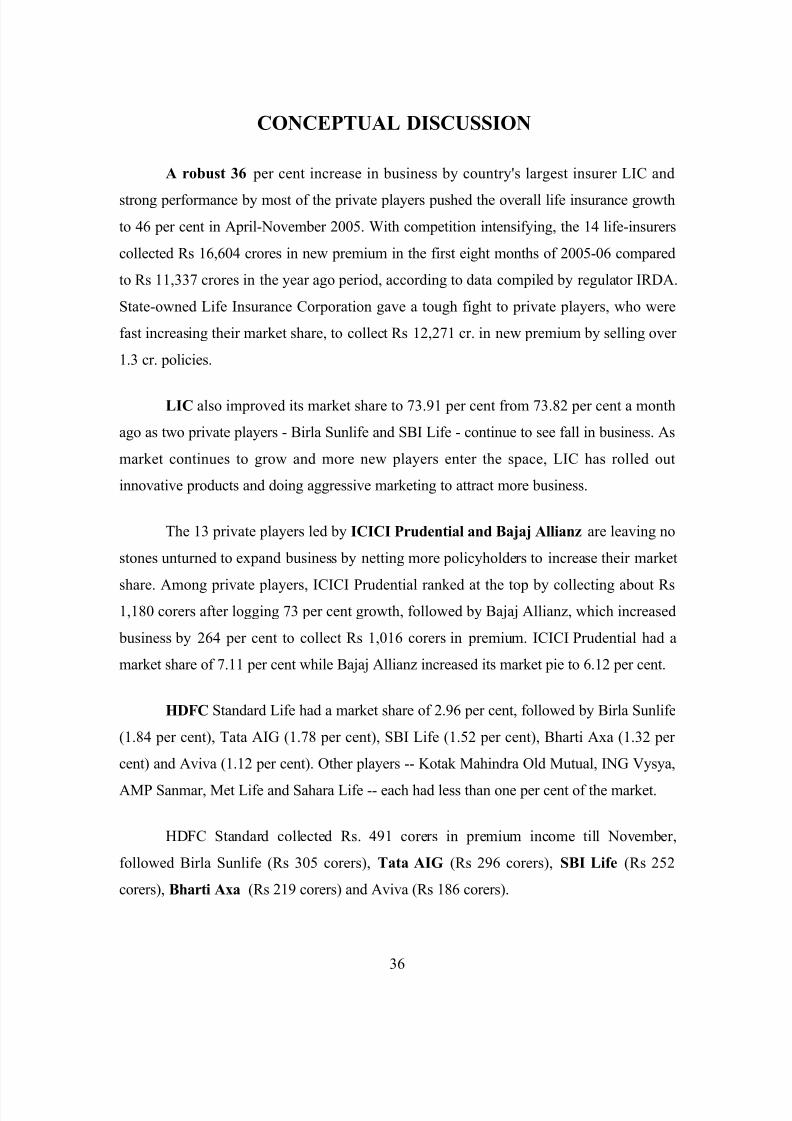

A robust 36 per cent increase in business by country's largest insurer LIC and

strong performance by most of the private players pushed the overall life insurance growth

to 46 per cent in April-November 2005. With competition intensifying, the 14 life-insurers

collected Rs 16,604 crores in new premium in the first eight months of 2005-06 compared

to Rs 11,337 crores in the year ago period, according to data compiled by regulator IRDA.

State-owned Life Insurance Corporation gave a tough fight to private players, who were

fast increasing their market share, to collect Rs 12,271 cr. in new premium by selling over

1.3 cr. policies.

LIC also improved its market share to 73.91 per cent from 73.82 per cent a month

ago as two private players - Birla Sunlife and SBI Life - continue to see fall in business. As

market continues to grow and more new players enter the space, LIC has rolled out

innovative products and doing aggressive marketing to attract more business.

The 13 private players led by ICICI Prudential and Bajaj Allianz are leaving no

stones unturned to expand business by netting more policyholders to increase their market

share. Among private players, ICICI Prudential ranked at the top by collecting about Rs1,180 corers after logging 73 per cent growth, followed by Bajaj Allianz, which increased

business by 264 per cent to collect Rs 1,016 corers in premium. ICICI Prudential had a

market share of 7.11 per cent while Bajaj Allianz increased its market pie to 6.12 per cent.

HDFC Standard Life had a market share of 2.96 per cent, followed by Birla Sunlife

(1.84 per cent), Tata AIG (1.78 per cent), SBI Life (1.52 per cent), Bharti Axa (1.32 per

cent) and Aviva (1.12 per cent). Other players -- Kotak Mahindra Old Mutual, ING Vysya,

AMP Sanmar, Met Life and Sahara Life -- each had less than one per cent of the market.

HDFC Standard collected Rs. 491 corers in premium income till November,

followed Birla Sunlife (Rs 305 corers), Tata AIG (Rs 296 corers), SBI Life (Rs 252

corers), Bharti Axa (Rs 219 corers) and Aviva (Rs 186 corers).

36

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 44/84

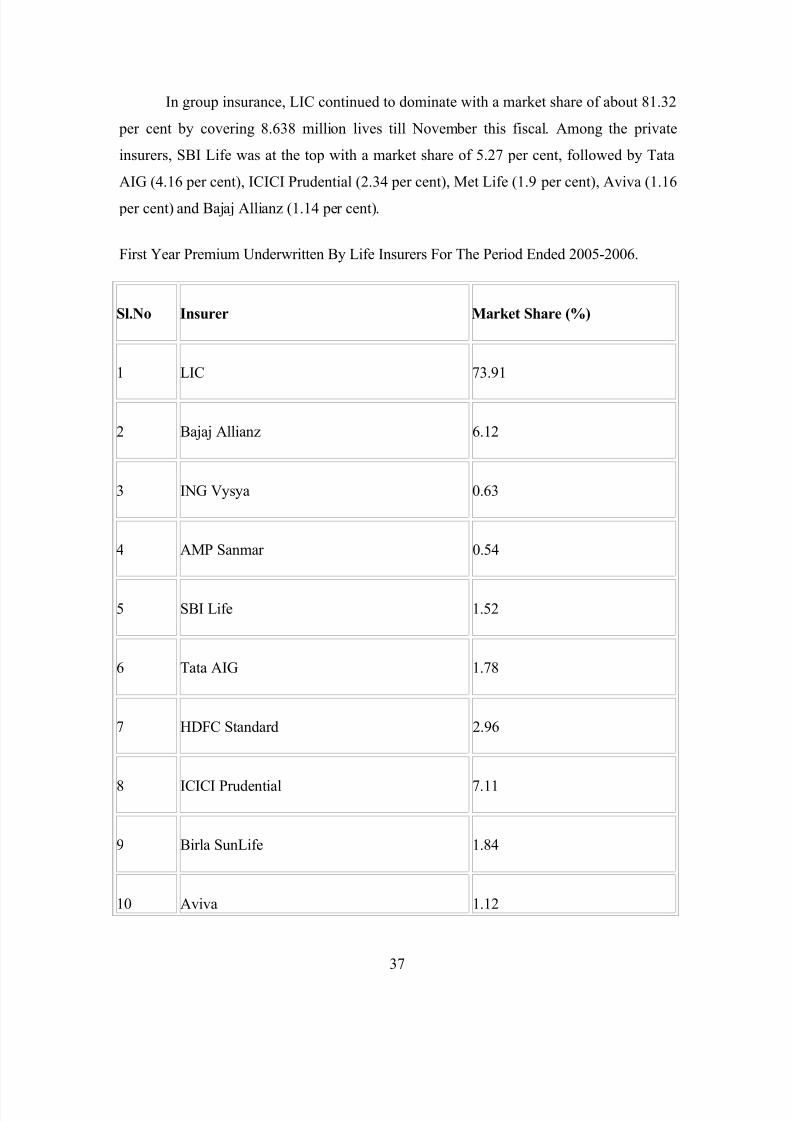

In group insurance, LIC continued to dominate with a market share of about 81.32

per cent by covering 8.638 million lives till November this fiscal. Among the private

insurers, SBI Life was at the top with a market share of 5.27 per cent, followed by Tata

AIG (4.16 per cent), ICICI Prudential (2.34 per cent), Met Life (1.9 per cent), Aviva (1.16

per cent) and Bajaj Allianz (1.14 per cent).

First Year Premium Underwritten By Life Insurers For The Period Ended 2005-2006.

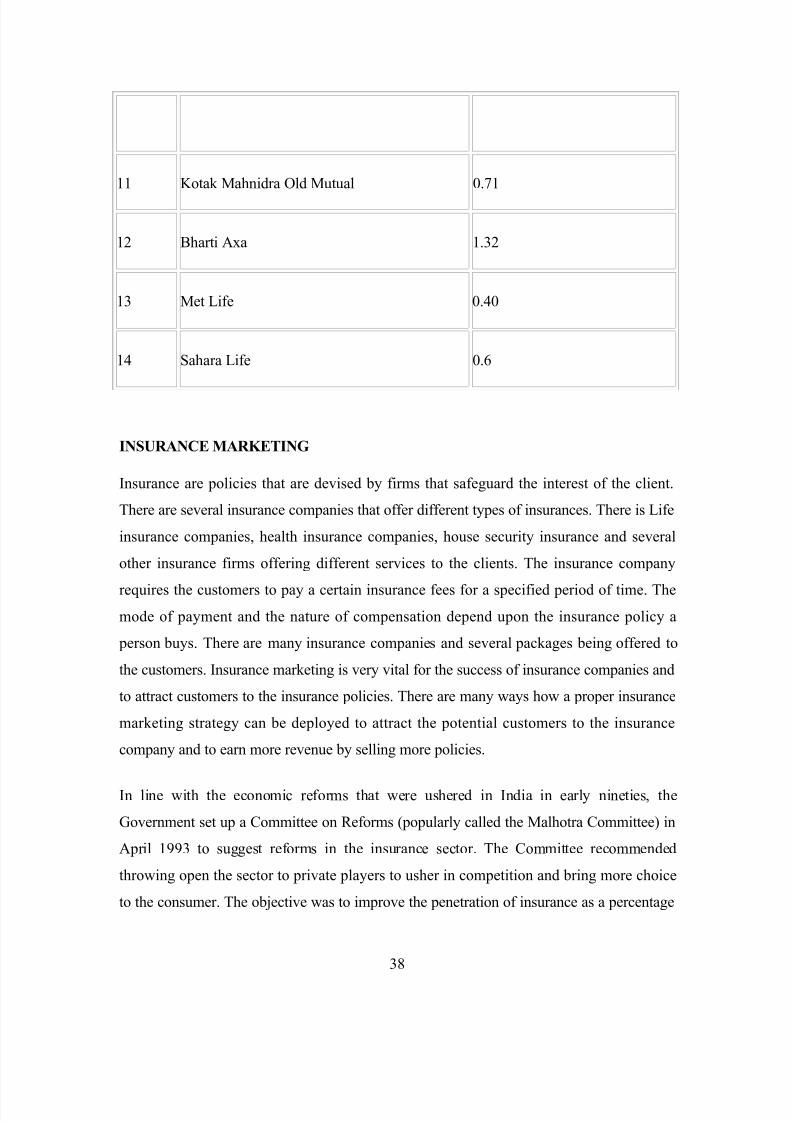

Sl.No Insurer Market Share (%)

1 LIC 73.91

2 Bajaj Allianz 6.12

3 ING Vysya 0.63

4 AMP Sanmar 0.54

5 SBI Life 1.52

6 Tata AIG 1.78

7 HDFC Standard 2.96

8 ICICI Prudential 7.11

9 Birla SunLife 1.84

10 Aviva 1.12

37

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 45/84

11 Kotak Mahnidra Old Mutual 0.71

12 Bharti Axa 1.32

13 Met Life 0.40

14 Sahara Life 0.6

INSURANCE MARKETING

Insurance are policies that are devised by firms that safeguard the interest of the client.

There are several insurance companies that offer different types of insurances. There is Life

insurance companies, health insurance companies, house security insurance and several

other insurance firms offering different services to the clients. The insurance company

requires the customers to pay a certain insurance fees for a specified period of time. The

mode of payment and the nature of compensation depend upon the insurance policy a

person buys. There are many insurance companies and several packages being offered to

the customers. Insurance marketing is very vital for the success of insurance companies and

to attract customers to the insurance policies. There are many ways how a proper insurance

marketing strategy can be deployed to attract the potential customers to the insurance

company and to earn more revenue by selling more policies.

In line with the economic reforms that were ushered in India in early nineties, the

Government set up a Committee on Reforms (popularly called the Malhotra Committee) in

April 1993 to suggest reforms in the insurance sector. The Committee recommended

throwing open the sector to private players to usher in competition and bring more choice

to the consumer. The objective was to improve the penetration of insurance as a percentage

38

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 46/84

of GDP, which remains low in India even compared to some developing countries in Asia.

Reforms were initiated with the passage of Insurance Regulatory and Development

Authority (IRDA) Bill in 1999. IRDA was set up as an independent regulatory authority,

which has put in place regulations in line with global norms. So far in the private sector, 12

life insurance companies and 9 general insurance companies have been registered.

39

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 47/84

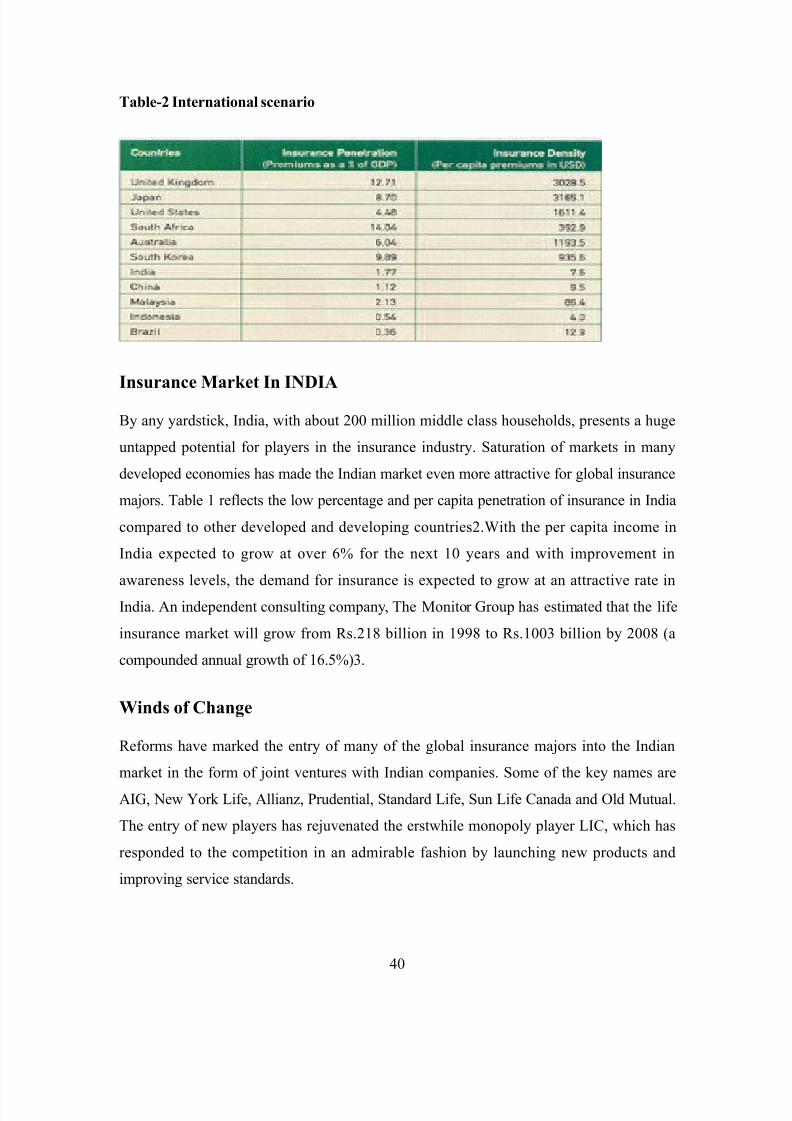

Table-2 International scenario

Insurance Market In INDIA

By any yardstick, India, with about 200 million middle class households, presents a huge

untapped potential for players in the insurance industry. Saturation of markets in many

developed economies has made the Indian market even more attractive for global insurance

majors. Table 1 reflects the low percentage and per capita penetration of insurance in India

compared to other developed and developing countries2.With the per capita income in

India expected to grow at over 6% for the next 10 years and with improvement in

awareness levels, the demand for insurance is expected to grow at an attractive rate in

India. An independent consulting company, The Monitor Group has estimated that the life

insurance market will grow from Rs.218 billion in 1998 to Rs.1003 billion by 2008 (a

compounded annual growth of 16.5%)3.

Winds of Change

Reforms have marked the entry of many of the global insurance majors into the Indian

market in the form of joint ventures with Indian companies. Some of the key names are

AIG, New York Life, Allianz, Prudential, Standard Life, Sun Life Canada and Old Mutual.

The entry of new players has rejuvenated the erstwhile monopoly player LIC, which has

responded to the competition in an admirable fashion by launching new products and

improving service standards.

40

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 48/84

The following are the key winds of change brought about by privatization:

Market Expansion: There has been an overall expansion in the market. This has been

possible due to improved awareness levels thanks to the large number of advertising

campaigns launched by all the players. The scope for expansion is still unlimited as

virtually all the players are concentrating on large cities and towns - except by LIC to an

extent there was no significant attempt to tap the rural markets.

New Product Offerings: There has been a plethora of new and innovative products

offered by the new players, mainly from the stable of their international partners.

Customers have tremendous choice from a large variety of products from pure term (risk)

insurance to unit-linked investment products. Customers are offered unbundled products

with a variety of benefits as riders from which they can choose. More customers are buying products and services based on their true needs and not just traditional money-back

policies, which is not considered very appropriate for long-term protection and savings.

However, there are still some key new products yet to be introduced - e.g. health products.

Customer Service: Not unexpectedly, this was one area that witnessed the most significant

change with the entry of new players. There is an attempt to bring in international best

practices in service and operational efficiency through use of latest technologies. Advice

and need based selling is emerging through much better trained sales force and advisors.

There is improvement in response and turnaround times in specific areas such as delivery

of first policy receipt, policy document, premium notice, final maturity payment, settlement

of claims etc. However, there is a long way to go and various customer surveys indicate

that the standards are still below customer expectation levels.

Channels of Distribution: Till two years back, the only mode of distribution of life

insurance products was through Agents. While agents continue to be the predominant

distribution channel, today a number of innovative alternative channels are being offered to

consumers. Some of them are banc assurance, brokers, the Internet and direct marketing.

Though it is too early to predict, the wide spread of bank branch network in India could

lead to banc assurance emerging as a significant distribution mechanism.

41

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 49/84

Table 3 below gives a snapshot of the performance for 2003-04 (up to October) of the 13

life insurance payers in India based on the first year premium figures4.

STRATEGIC ALTERNATIVES

If one analyses the history of growth of the insurance industry since reforms, it is marked

by all-round growth of all players. More or less all players (including the market leader

LIC) have aggressively recruited and trained advisors, appointed agents, launched new

products, improved customer service standards and revamped/expanded their distribution

networks. If at all there was any major difference between players it was only in time lag in

launching of services. Every player would like the customers to believe that its service

standards are the best or that its agents are the most informed and ethical, but is debatable

whether there are any significant differences. In other words, each company is trying to be

‘everything to everybody’.

Our argument is that the strategy of being everything to everybody is risky. Some players

justify the above strategy on the basis that the Indian market is huge and it can

accommodate everybody. Still, in a market where it is difficult to distinguish oneself

sufficiently on service or any other parameter to be able to charge a premium, it will lead to

unmitigated price competition to the detriment of all players. One may achieve sales

turnover, but margins and profitability will suffer severely. In the insurance industry where

large amounts of capital are required, this is risky.

While there is room for a few scale players with a finger in every pie, it is profitable for

other players to focus on different segments to survive and thrive in a multi-firm open

environment. While each company has to choose its own unique positioning based on its

unique strengths, the below-mentioned generic positioning alternatives5 appear worth

considering. Needless to say the positioning choices discussed here are not mutuallyexclusive and can be overlapping.

42

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 50/84

Variety-based Positioning

This type of positioning is based on varieties in products and services rather than customer

segments. It is a sensible strategy for those companies who have distinctive advantages or

strengths in offering certain products and services.

In the insurance industry too, it is possible to achieve a unique position by focusing on

certain category of products. One such example is Birla Sun life Insurance, which has been

placing particular focus on investment-related products since its launch in India6. Through

its superior fund management capabilities, the insurance company can deliver better returns

on its investment-linked products and thereby carve for itself a leadership position in this

segment.

Then there is the entire category of pension products that is widely touted to have immense

growth potential in India due to imminent pension reforms. It is possible to achieve

profitable positioning by focusing and excelling in only pension products.

Needs-based Positioning

This is the most commonly understood positioning and is based on the differing needs of

different groups of consumers. This can be done successfully if a company has unique

strengths to service a group of customer needs better than others.

The insurance needs of customers vary significantly for different groups of customers. The

insurance needs of young family with small children will be quite different from that of a

family in which the income-earner is close to retirement. However, in India most of the life

insurance companies have a wide variety of products tailored for different customer needs

and there is no company focusing on a particular customer need.

An example would be a life insurance company that focuses only on High Net-worth

Individuals (HNIs). The needs of HNIs would be quite different from those of a general

consumer and would require an entirely different marketing mix right from the type of

products offered and the way they are distributed, to the promotion methods employed.

43

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 51/84

Access-based Positioning

Positioning of customers can also be done by the way they are accessible. That is different

groups of customers may be accessible in different ways even though they may have

similar needs. Access is typically a function of customer geography or customer scale.

There is excellent opportunity in the insurance industry to employ access-based positioning

by targeting the rural insurance sector. The rural market for life insurance is very different

from the urban market in terms of needs, income levels and distribution (seasonality, for

example), penetration of media and so on. So far except for LIC, no other player has paid

any attention or focus on the rural sector. Contrary to common perception it is a big

opportunity as emphasized repeatedly by such eminent strategists like C.K. Prahlad7. Rural

market can be a highly profitable position if one is able to carefully plan and tailor an entire

set of low-cost activities of advertising, distribution, and product design etc. to successfully

exploit the potential.

CHOOSING THE RIGHT STRATEGY

The right strategic choice is not a matter of positioning choice alone. It involves the very

way a company organizes itself to do business. It is the configuration of the entire value

chain of the company through a different set of activities to deliver unique value to

consumers. The set of activities cover all upstream and downstream activities, from the

selection of the product mix, the way the products are priced, promoted, the type of

distribution mechanism used, the way customers are serviced and so on.

Some life insurance companies focusing on rural markets have adopted innovative means

of distribution. Instead of appointing agents as is done typically, they have used grosbeaks

in different villages across the country to promote life insurance and act as their sales arm.

This enabled them to tap into their special knowledge of their local.

The best way for insurance marketing is to analyze the target audience for the insurance.

This will help the insurance company to focus on a specific audience only and would

increase sales of your insurance policy. There are many different insurance companies with

an assortment of insurance policies. Only proper insurance marketing helps in propelling

44

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 52/84

the insurance business and give it an edge over other insurance corporation.

There are several insurance marketing strategies and the proper implementation of the

insurance marketing strategies helps the insurance company to build up a proper name in

the market. The insurance company with poor planning and insurance marketing policies

cannot propel in the market.

Some of the most important insurance marketing strategies include the following

plans:

One of the most basic methods for insurance marketing is to promote the industry

in general public through sales letters and banners. Some insurance company even issues

weekly or monthly sales letter with different insurance policies and benefits for the clients.Having such promotional strategy is very advantageous for the insurance marketing and

helps in getting more clients for the business.

Web promotion is also a very good insurance marketing strategy. All the insurance

policies can be listed on the internet and market to the online customers. In the advance

world of today a webpage is consider to be the life-line of any insurance organization.

Building a proper referral system also helps in boosting insurance sales and in

making more clients. There are several associations with whom the insurance company can

built a referral system with. For example if the insurance company is providing health

insurance then it could affiliate itself with hospitals. This form of insurance marketing is

very beneficial for insurance company as it helps in building a good name for the insurance

company and to add more clients.

Another insurance marketing technique that most insurance agencies deploy is to

organize seminars and dinners for general public. They also maintain proper contacts with

the customers and also send them promotional gifts as a mean to build a strong client base

for the insurance policy.

45

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 53/84

SELLING LIFE INSURANCE: HOW IS IT DONE?

Techniques for marketing and selling date back to man's earliest awareness of trade. This is

because in order to gain anything in return, man had to turn in what assets of his were in

demand. For this, he had to determine t ha value of his possessions and what he could offer others. In exchange for what he could offer, people turned in what they could afford to. A

similar concept is also followed today when insurance companies sell insurance. They offer

you all that they can in exchange for your investment in them. They will take on your risks

if they can afford to do so and cover you in case of accidental death, injury, etc.

In order to sell people things, you need to know your product well. Insurance agents or any

successful tradesman of the past would need to market products to the best of his or her

ability based on the sole knowledge of his or her product. Having proper knowledge of a

product is an immense weapon in sales and marketing.

Marketing and selling products also require one to do so effectively and in the most

affordable manner. In selling insurance, it is known that most affordable methods have

always been used. This is because of the fact that the funds for marketing insurance come

from the investors' pockets. This is proof in itself that their investments are not being over-

spent or misused.

In the olden times, individuals who were interested in obtaining insurance cover for their

families and businesses would basically have to get in touch with a suitable insurance

company or insurance agent, who would offer the best insurance coverage. In the event of

individuals undergoing a major loss of costly equipment, insurance agents would carefully

carry out an analysis of the damaged equipment and settle the insurance claim with the

insurance company.

There are various types of insurance coverage being sold by insurance sales agents. Some

of these include disability, life, health, and property, accidental, dental and medical

insurance. Insurance agents involved in selling life insurance also offer a certain retired

income to individuals. Insurance agents specialize in numerous insurance packages. They

46

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 54/84

will discuss or rather have one on one consultation with their respective clients or

customers about how much they are willing to pay and take time to review the cost of the

damaged property or equipment. Prior to this insurance agent may then have to involve

themselves in a lot of paper work. In most cases they will have to chalk out a detailed

invoice, stating details of the prices of the damaged goods.

INTERNET

With the use of the Internet nowadays, there are various ways to advertise for insurance in

a more economical way. The Internet with the span of time is growing into a major source

of advertising for cheap insurance coverage. Major insurance companies and various other

online insurance companies are providing attracting discounts to their online customers,

provided they buy the insurance cover. There is a growing trend for people all over the

United Kingdom purchasing motor insurance from online companies.

ADVERTISING

There are numerous amounts of companies offering cheap insurance packages, to help

serve the needs of the individuals according to their needs and budgets. Through the

frequent use of newsletters and brochures, companies can advertise for insurance policies

effectively.

Advertisements covering certain insurance policies such as auto, medical group and health

insurance, can be advertised through the use of brochures, business cards, bulletin boards in

public shopping or postcards which are issued out to customers. Insurance companies

wishing to sell their insurance at rated discounts can advertise for these insurance packages,

through setting up flyers and advertisement boards, at public and social places. These

include the libraries, hair salons, parking lots and grocery stores.

WORD OF MOUTH

Advertising for insurance through word of mouth is another least expensive way of

advertising. All one needs is creativity and a few marketing strategies to target a specific

customer audience. Insurance companies interested in advertising for insurance online, can

benefit from the advantages of link exchanging. Linking to other WebPages and third party

47

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 55/84

websites is a way, of improving an insurance company's online image. It helps in

accelerating the number of customers logging onto their insurance website. Other non

expensive ways to advertise for insurance on the web could include the use of electronic

magazines or e-zones, in the insurance company's website. This will increase the number of

customers towards logging onto the respective insurance website.

Insurance companies can also benefit from the use of e-mail marketing and the advantages

it has to offer. It is a relatively more effective approach as compared to offline direct

marketing.

PRICING & DISTRIBUTION OF LIFE INSURANCE

PRICING OF LIFE INSURANCE

Pricing of insurance product is a complex task as premium rates to be charged depend upon

variety of factors namely, expected losses, operating expenses, income from investments

and profit margin of the insurance company.

Pricing refers to the methods used to calculate rate of premium to be charged on insurance products.

Premium is a price for which the insurer is willing to accept the risk.

Actuaries employed by the insurer calculate and determine the premium rates to be charged

for different policies and from people of different age. If the premium charged is very low,

the company would not be able to collect sufficient amount to pay claims, bear expenses

and earn some profit. On the other hand, excessively high premium charged will result in

loss of prospective clients of the insurance company because company may lose the

prospective insurer to its competitors in the market.

Pricing also depends on the market forces of demand and supply of insurance products.

48

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 56/84

The payment of premium by the proposer is acceptance of the price charged by the insurer

for providing the life insurance cover.

PRICING OBJECTIVES

The following are the objectives kept in mind while deciding upon the pricing of various

insurance products:

ADEQUACY OF RATES

The premium rates fixed by the insurance company should be adequate in order to pay the

benefits promised to the policyholders and meet all the operating expenses. In other words

the rates charged must be sufficient to collect the premium incomes the insurance company

required to pay various operating expenses, to pay the claims and at some profit margin.

Insurers do conduct periodic reviews to assess whether the initial premium levels

established are equitable and not too high i.e. adequate.

FAIRNESS AND RATE EQUITY

The insurance rates must be fair and equitable. The rates charged to the Policyholders with

the same expected losses and other costs should be equal.

49

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 57/84

This is known as rate equity. It means that the insurance company should Charge

premiums in accordance with the expected payment of benefits and

expenses. The rates must be same for homogenous groups and must not be

same for heterogeneous groups (say of different age groups).If the two

individuals of different ages, say one 25 years and other 50 years intend to

purchase same policy for the same time period with same terms, the

insurer will be charging the higher rate of premium from the person who is

50 years old as there is comparatively higher death probability of the older

client.

In the case of the young person of 25 years the company cannot associate very high death

probability.

If there are two persons of the same age who want to take same policy with same terms and

conditions but one person is chronically ill, the insurer must charge them different rates as

the ill person has higher probability of dying at a certain age (so should be giving higher

premium).

REASONABLENESS

The rates of the premium charged to the policyholders should not be too high because it

will lead to loss of insurance business to the competitors in the industry. Charging

excessive premium is therefore unfair to the customers.

SIMPLICITY

The premium rates charged should be simple to understand and should not change very

frequently.

LIFE INSURANCE PRICING ELEMENTS

Following are the elements of life Insurance Pricing:

1. Rate of death of large number of insured persons.

50

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 58/84

2. Administration cost and other expenses of the insurer.

3. Income from investment of premium.

RATE OF DEATH OF LARGE NUMBER OF INSURED PERSONS:

The mortality rates depend on the age, occupation, life style, and medical history of the

insured. The premium rates charged are calculated on the basis of rate of deaths of very

large number of persons insured, i.e., the past experience of large number of cases is taken

into consideration before deciding on mortality rate.

51

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 59/84

ADMINISTRATION COST AND OTHER EXPENSES OF THE

INSURER:

Every insurer incurs certain expenses or administrative costs related to the service

provided. The administration cost incurred may depend on frequency of payment of

premium and the volume of records kept. If the premium is paid annually, cost is lesser as

compared to quarterly and half yearly or monthly payments.

INCOME FROM INVESTMENT OF PREMIUM:

Premium collected by the insurance company from various policyholders is again invested

and the income earned on the same helps the insurance company to bear various expenses

incurred and benefits given to policyholders.

CHANNELS OF DISTRIBUTION

Marketing includes all those activities carried on to transfer the goods and services from

manufacturer to the consumer.

Marketing mix is a unique combination of basic ingredients of marketing viz.

1. Product

2. Price

3. Place (channels of distribution)

4. Promotion

It is designed for the best realization of the objectives of marketing management. In

marketing management the term place is used to refer to channels of distribution i.e.

intermediaries which fetch products/services from the place of the manufacture to the place

of ultimate consumers. The channel of distribution (place) is an important ingredient of

marketing mix as however useful the product might be and how so ever suitable its price

52

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 60/84

be, unless and until the products/services are mad available to consumers at ‘centers of

convenient buying’ the consumers will not be buying the same.

Insurance being a service business requires marketing department to play a key role in

delivery of service. The marketing department conducts research for identification of target

customers, help in maintaining and promoting the distribution system and also plays an

active role in development of new products. It is the most vibrant department in an

insurance organization since it has to necessarily deal with all the other department of the

organization.

Insurance business is business of law of large numbers. The law requires the insurer to

attract a sufficient number of exposures to allow credible ratio prediction. The major task

of sales managers in charge of the sales section of insurance company is the supervision of

the sales functions of the branches. This section is also responsible for spreading awareness

among the general public about the benefits of life Insurance. Sales training section is

entrusted with responsibility for training in product, in selling and sales planning in the

personnel such as development officers and agents. The agents of insurance company

mainly sell insurance policies.

We can take example of Bharti Axa in particular to understand sales and distributionfunction of the corporation.

JOB DESCRIPTION

What does an agent or broker do?

Most people have their first contact with an insurance company through an insurance agent.

These workers help individuals, families, and businesses select insurance policies that

provide the best protection for their lives, health, and property. Insurance sales who agents

work exclusively for one insurance company are referred to as captive agents. Independent

insurance agents or brokers represent several companies and place insurance policies of

their clients with the company that offers the best rate and coverage. In either case, agent

prepares reports, maintain records, seek out new clients, and in the event of a loss, help

53

7/31/2019 Ravi Bharti Axa

http://slidepdf.com/reader/full/ravi-bharti-axa 61/84

policyholders settle their insurance claims. Increasingly, some are also offering their client

financial analysis or advice on ways the clients can minimize risk.

Insurance sales agents commonly referred to as “producers” in the insurance industry offer