potential of residue from sugar production for the ... · pdf filepotential of residue from...

TRANSCRIPT

www.renewables-made-in-germany.com

Potential of residue from sugar production

for the generation of Heat and Power in

Vietnam

Presenter: NGUYEN VAN LOC

Vice Chairman of the Vietnam Sugar Association

Deputy Chairman of the Board - Bien Hoa sugar JSC

Chairman of Sugar Committee, TTC Group

1. Overview of Viet Nam‘s sugar industry

2. Overview of bagasse co-generation of Viet nam‘s sugar industry

3. Current application of bagasse for co-generation heat and power in Vietnam

4. Legal framework for biomass power generation in Vietnam

5. Challenges and barriers

Agenda

• 41 Mills

• Mills capacity: 139,800 ton/day

• Plantation: 280,000 Ha

• Cane growers: 337,000 families

1. Overview of Viet Nam‘s sugar industry

Key figures at glance

1. Overview of Viet Nam‘s sugar industry

Area of sugar production

South Central Coast

& Central Highlands: No. of mills: 14

Total capacity (TCD): 52,100

Cane tonnage (1000T): 5,898

Cane Area (1000 Ha): 118

Mekong River Delta: No. of mills: 10

Total capacity (TCD): 25,150

Cane tonnage (1000T): 4,178

Cane Area (1000 Ha): 52

Northern (from yellow to

green): No. of mills: 11

Total capacity (TCD): 42,500

Cane tonnage (1000T): 4,984

Cane Area (1000 Ha): 137

Southeast: No. of mills: 5

Total capacity (TCD): 19,500

Cane tonnage (1000T): 2,261

Cane Area (1000 Ha): 34

Sugar season 2013/2014

COUNTRYNORTHER

NCENTRAL

SOUTHEAST

MEKONGRIVERDELTA

CANE 17.321.60 4.984.600 5.898.000 2.261.000 4.178.000

SUGAR 1.619.420 505.100 576.800 193.870 343.650

-

2.000.000

4.000.000

6.000.000

8.000.000

10.000.000

12.000.000

14.000.000

16.000.000

18.000.000

20.000.000

1. Overview of Viet Nam‘s sugar industry

Viet nam’s sugarcane development

1. Overview of Viet Nam‘s sugar industry

2000/01

2001/02

2002/03

2003/04

2004/05

2005/06

2006/07

2007/08

2008/09

2009/10

2010/11

2011/12

2012/13

cane area (ha) 303.0 309.9 315.0 287.0 280.0 265.0 310.0 306.6 270.6 265.1 271.4 283.2 283.0

cane yield (ton/ha) 49,8 49,2 50,1 50,5 51,8 50,9 54,8 54,1 50,0 51,7 60,5 61,7 63,5

0,0

10,0

20,0

30,0

40,0

50,0

60,0

70,0

240.000

250.000

260.000

270.000

280.000

290.000

300.000

310.000

320.000

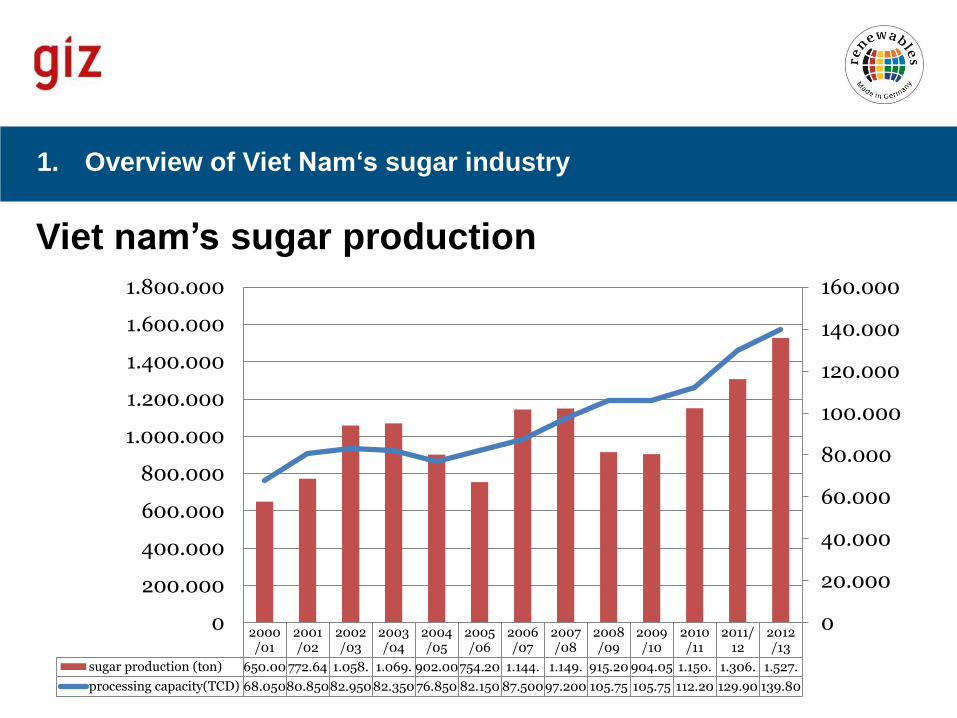

Viet nam’s sugar production

1. Overview of Viet Nam‘s sugar industry

2000/01

2001/02

2002/03

2003/04

2004/05

2005/06

2006/07

2007/08

2008/09

2009/10

2010/11

2011/12

2012/13

sugar production (ton) 650.00 772.64 1.058. 1.069. 902.00754.20 1.144. 1.149. 915.20 904.05 1.150. 1.306. 1.527.

processing capacity(TCD) 68.05080.85082.95082.350 76.850 82.150 87.50097.200 105.75 105.75 112.20 129.90 139.80

0

20.000

40.000

60.000

80.000

100.000

120.000

140.000

160.000

0

200.000

400.000

600.000

800.000

1.000.000

1.200.000

1.400.000

1.600.000

1.800.000

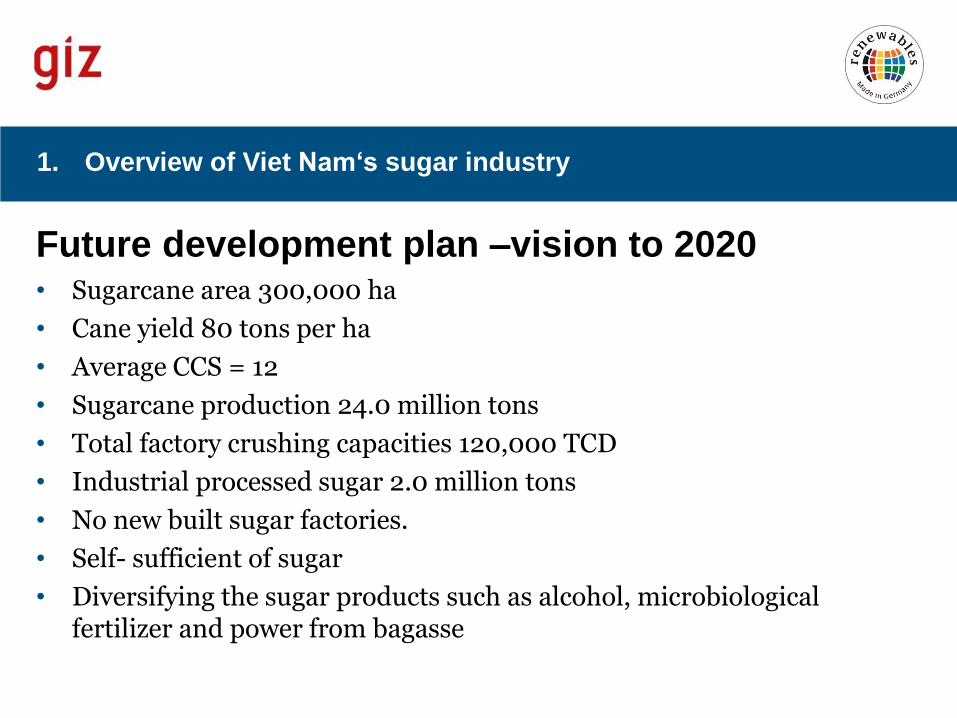

Future development plan –vision to 2020 • Sugarcane area 300,000 ha

• Cane yield 80 tons per ha

• Average CCS = 12

• Sugarcane production 24.0 million tons

• Total factory crushing capacities 120,000 TCD

• Industrial processed sugar 2.0 million tons

• No new built sugar factories.

• Self- sufficient of sugar

• Diversifying the sugar products such as alcohol, microbiological fertilizer and power from bagasse

1. Overview of Viet Nam‘s sugar industry

Restructuring sugar industry

Adjust, supplement and plan the sugarcane zones for each factory that are

suitable with the national planning.

The provincial people’s committee directs to carry out the projects of

investment and construction for infrastructure such as transportation,

irrigation that are suitable and synchronous with the projects of sugarcane

zone development.

Apply the overall agricultural solutions such as sugarcane seed, intensive

cultivation techniques, pest and insect prevention, mechanization, etc for

concentrate sugarcane zones to increase the sugarcane productivity and

quality.

Mainly focus on increasing productivity and production of sugar on each

hectare, not to enlarge the sugarcane cultivation area.

1. Overview of Viet Nam‘s sugar industry

Benefits of bagasse co-generation power in Vietnam

The sugar factory production in the dry season - the season of power shortage , water

shortage to hydropower factories.

Reduce CO2 emissions : estimates of world sugar ISO organization , for every ton of

bagasse will reduce 0.55 tons of CO2 emissions .

Decentralized power station ( in 41 sugar mills ) in rural areas : reduce loss of power

transmission from the central source ( as reported by EVN power loss of about 9-10 %

) . In India , 1MW electricity from bagasse equivalent concentration of 1.67 MW from

thermal coal .

Savings of fossil resources , a ton of 50 % moisture bagasse equal to 0.213 tons of oil

Saving money by burning oil in thermal power centers and purchase power from

China ( 2013 , expected lack of water for hydropower , EVN will have spent $ 5,542

billion to oil burning in thermal power centers and 5,000 billion to buy power from

China ) .

2. Overview of bagasse co-generation of Viet nam‘s sugar industry

Biomass availability in Vietnam

Sugar industry residue (bagasse) is only available in crushing season (120-

140 days)

There are other biomass residues available such as cane trash,rice husk, rice

straw, coconut pith, wood chip,coffee waste., etc

Such biomass are scattered and the residues are spread over a large area.

To extend the operation of biomass cogeneration facilities up to 280-300

days/year, a system needs to be developed where residues can be efficiently

collected and transported to a central power station or processing location.

2. Overview of bagasse co-generation of Viet nam‘s sugar industry

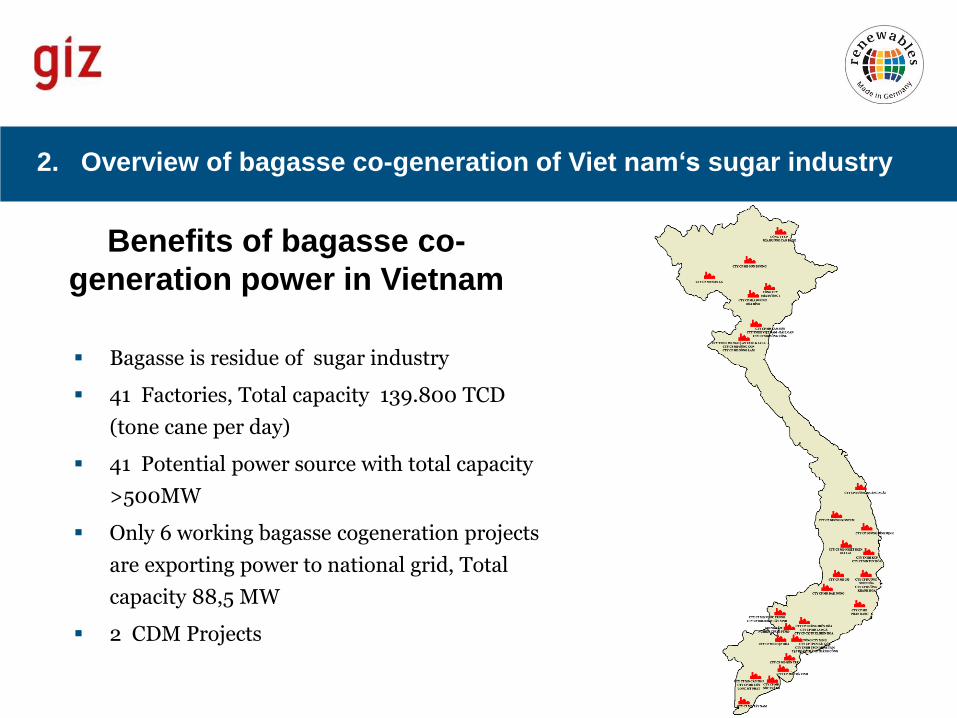

Benefits of bagasse co-

generation power in Vietnam

Bagasse is residue of sugar industry

41 Factories, Total capacity 139.800 TCD

(tone cane per day)

41 Potential power source with total capacity

>500MW

Only 6 working bagasse cogeneration projects

are exporting power to national grid, Total

capacity 88,5 MW

2 CDM Projects

2. Overview of bagasse co-generation of Viet nam‘s sugar industry

Energy savings in sugar factories

• Currently, Viet Nam sugar factories are in high energy consumption, Energy savings

in sugar process will increase the power export to the grid .

• Potential savings in sugar factory is very large , can reduce up to 25 % of total energy

consumption . power consumption of about 35-40 kWh / ton of cane can be reduced

to levels < 30 kWh / ton of cane , steam consumption in about 400-500 kg steam/ ton

cane can be reduced to 300-400 kg/ ton cane

• Should be Priority investment for a bagasse cogeneration project

• The area can reduce energy include : CANE MILLING , STEAM GENERATION ,

POWER GENERATION , SUGAR PROCESSING , LIGHTING SYSTEM .

• The solutions include: changes in operating parameters ( reduce bagasse moisture ,

reduce excess air in boiler, reducing blowdown,etc) , switching turbine to electric

motor, apply continuous technology , apply waste heat recovery system , insulation

against heat loss

2. Overview of bagasse co-generation of Viet nam‘s sugar industry

There are only 6 projects

BACKWARD technology including low pressure boiler <45 ata, and back pressure turbine resulting in low energy rate, just about 30 Kwh/ton cane

Seasonal working < 150 days.

Single fuel: bagasse only

Only 2 projects implement CDM and carbon credit sale

3. Current application of bagasse for co-generation heat

and power in Vietnam

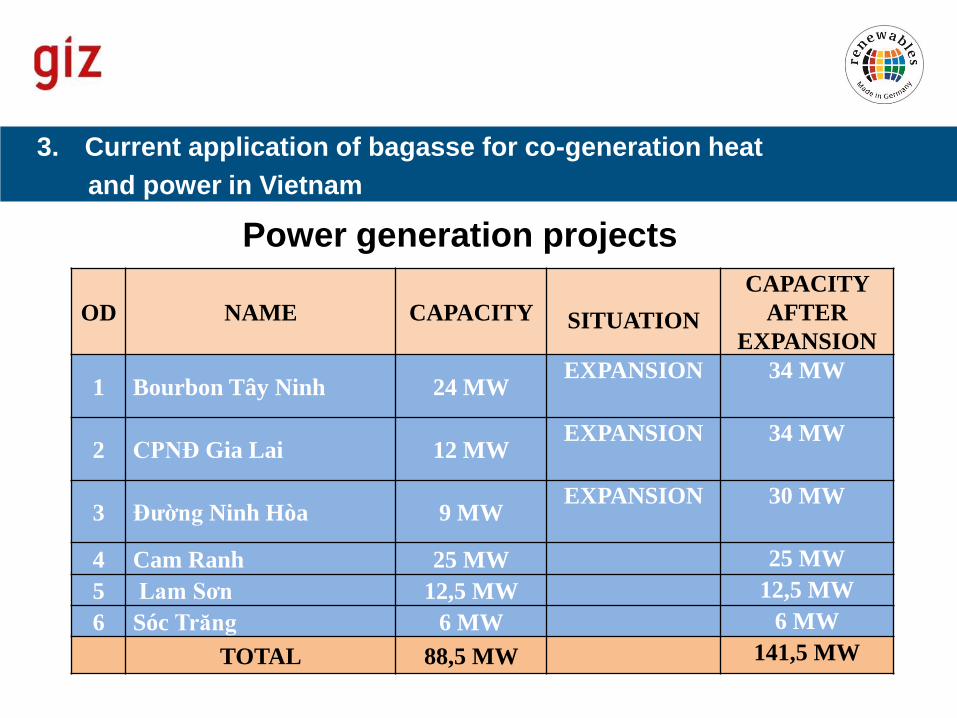

Power generation projects

3. Current application of bagasse for co-generation heat

and power in Vietnam

OD NAME CAPACITY

SITUATION

CAPACITY

AFTER

EXPANSION

1 Bourbon Tây Ninh 24 MW EXPANSION 34 MW

2 CPNĐ Gia Lai 12 MW EXPANSION 34 MW

3 Đường Ninh Hòa 9 MW EXPANSION 30 MW

4 Cam Ranh 25 MW 25 MW

5 Lam Sơn 12,5 MW 12,5 MW

6 Sóc Trăng 6 MW 6 MW

TOTAL 88,5 MW 141,5 MW

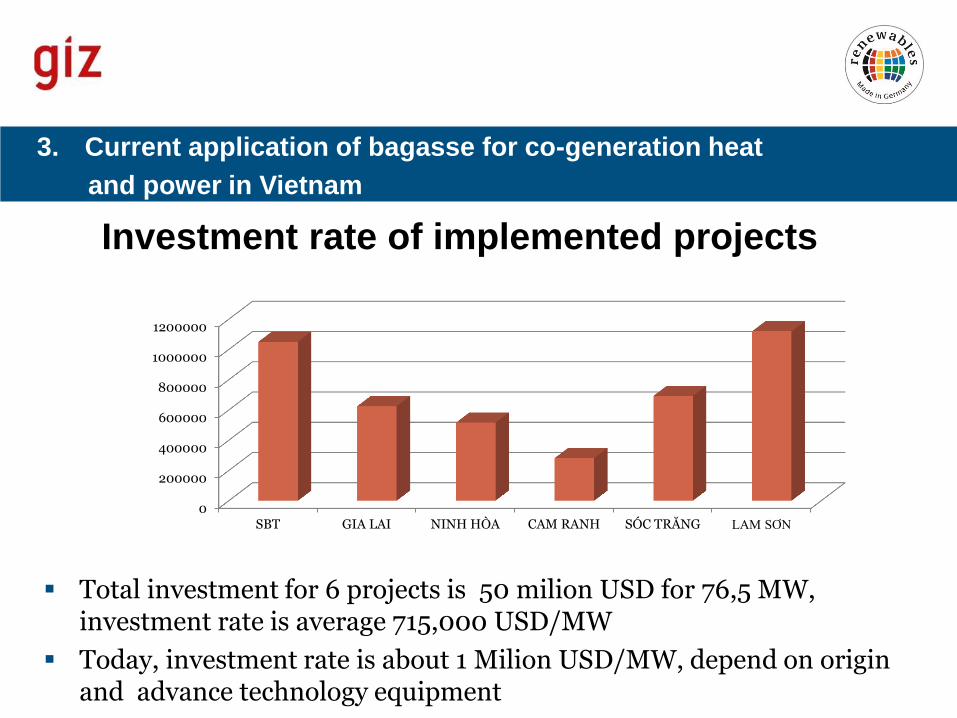

Investment rate of implemented projects

Total investment for 6 projects is 50 milion USD for 76,5 MW, investment rate is average 715,000 USD/MW

Today, investment rate is about 1 Milion USD/MW, depend on origin and advance technology equipment

3. Current application of bagasse for co-generation heat

and power in Vietnam

0

200000

400000

600000

800000

1000000

1200000

SBT GIA LAI NINH HÒA CAM RANH SÓC TRĂNG LAM SƠN

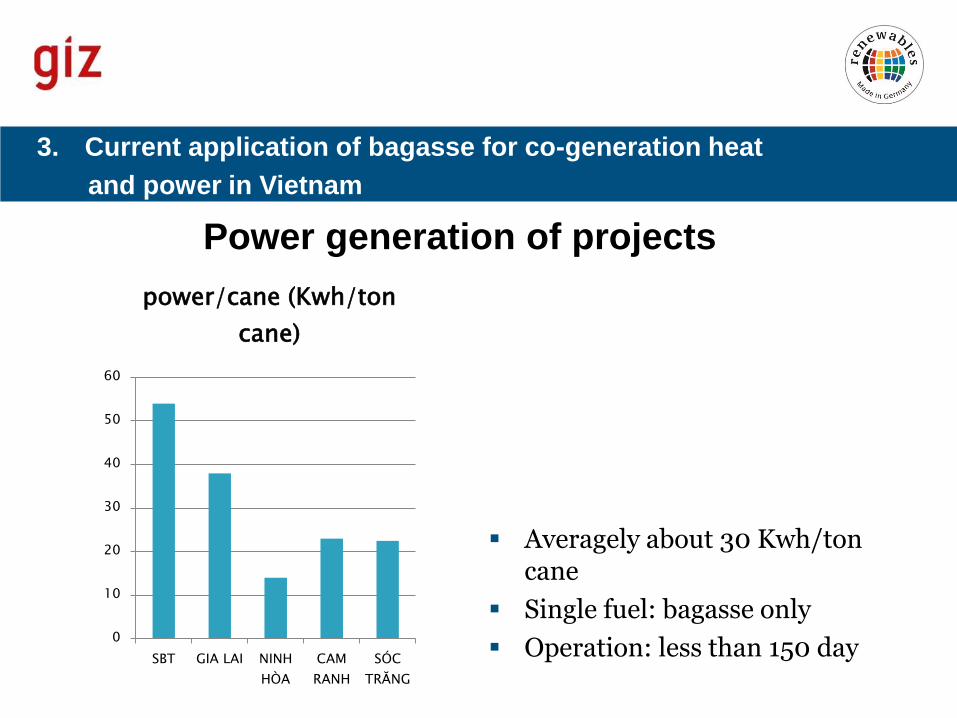

Power generation of projects

3. Current application of bagasse for co-generation heat

and power in Vietnam

Averagely about 30 Kwh/ton cane

Single fuel: bagasse only

Operation: less than 150 day

0

10

20

30

40

50

60

SBT GIA LAI NINH

HÒA

CAM

RANH

SÓC

TRĂNG

power/cane (Kwh/ton

cane)

Potential and Scenarios of Viet Nam bagasse

cogeneration development Targeting 500MW in 2020

3. Current application of bagasse for co-generation heat

and power in Vietnam

Cane

production

(mil ton)

Export power 30Kwh/tc

(current)

Export power

70Kwh/tc (medium

pressure)

Export power 130

Kwh/tc (high pressure,

advanced tecnology)

Export unit

(GWH)

Export

capacity

(MW)

Export unit

(GWH)

Export

capacity

(MW

Export unit

(GWH)

Export

capacity

(MW

16 (2015) 480 133

1.120

311

2080

577

20 (2020) 600 166

1400

388

2600

722

• Electricity Act 2004 ( adjusted 2012): interest and capital support for electricity from renewable energy projects in rural and mountainous areas

• 2005 Investment Law : investment incentives for renewable energy projects , in areas of investment incentives

• Law encouraging domestic investment in 2003 :

• Environmental Protection Act 2005 and support incentives for renewable energy projects

• Decree 04/2009/ND-CP on incentives , support environmental protection activities : preferential support for import of renewable energy and renewable energy production .

• Government Decree No. 151/2006/ND-CP of 20/12 , 2006, the investment credit and export credit

4. Legal framework for biomass power generation in Vietnam

Decree No. 61/2010/ND-CP : The power project from bagasse cogeneration power is renewable energy projects in the agricultural sector LIST SPECIAL INVESTMENT INCENTIVES

Decision No. 1855/QD-TTg , 27/12/2007 Energy Development Strategy of Vietnam National 2020 vision 2050

Decision No. 130/2007/QĐ-TTg dated 02/8/2007 mechanisms and policies for investment projects under the clean development mechanism ( CDM )

Decision 1208/QD-TTg ( or Master Plan 7 ) . Objectives power from bagasse cogeneration power plants in sugar will reach a total capacity of 500MW , and by 2030 will reach 2000MW

Decision 24/2014/QD-TTg mechanism to support the development of biomass power project in Vietnam

4. Legal framework for biomass power generation in Vietnam

Development Orientation according to Decision 24/2014

The MoIT shall be responsible for preparing the national biomass energy utilization

and development master plan and submitting for the Prime Minister’s approval.

The Purchaser shall be responsible for purchasing all electric power produced by the

grid-connected biomass power generation plant under its jurisdiction.

Projects of biomass power project should be in the form of independent entity to

fully enjoy the preferential treatment . ( 10 % corporate tax exemption for 5 years

reduction in the next several years v / v ..... ).

For combined heat and power projects: the Purchaser is obligated to purchase entire

redundant electricity generated from combined heat and power projects using

biomass energy at the delivery point at 1,220 VND/kWh (excluding VAT, equivalent to

5.8 US cents/kWh).

For other biomass power projects, which are not combined heat and power projects:

The electricity purchase price shall apply the avoided cost mechanism.

4. Legal framework for biomass power generation in Vietnam

5.1 Transmission line

The investor of a biomass power project shall be responsible for investing, operating

and maintaining the transmission line and transformer station (if any) from the

Seller’s power plant to the connection point as agreed with the Purchaser.

Distance from sugar factory (where bagasse fuel is available) to connection point as

agreed with purchaser is normally quite far, because the sugar factory is normally in

the rural area and far from connection point. The investment cost for transmission

line could be remarkable in some cases.

Voltage of transmission line: higher voltage means higher investment but it could

reduce the loss of power transmission. Lower voltage could reduce the reliable of

exporting power.

5. Challenges and barriers

5.2 Knowledge level

There is a lack of updated information on bio-energy technologies

Information of high efficiency energy conversion technologies in the sugar

cane industry such as GSTIG – gasifier steam injected gas turbin (or

Biomass Integrated Gasifier Gas Turbine Technology -BIG GT), multiple –

fuel steam generator, at reasonable investment cost.

Opportunities of Carbon Funding through CDM or VGS systems is too

complicated and unknown.

5. Challenges and barriers

5.3 Capital financing

Cogeneration systems are capital intensive projects and the sources of

capital financing is an important consideration.

Sugar companies, the investors of bagasse cogeneration project, are in

difficult time due to the situation of sugar industry: low prices, excess

supply.

So the self-financing is limited and unfeasible

The borrowing could be an alternative providing the project is high rate of

return and require certain equity and guarantee

Other alternatives such as leasing, third party financing is not familiar with

Viet Nam investors

5. Challenges and barriers

5.4 High investment cost of equipment

• Decision on the origin of the

equipment : China , India ,

Europe , Japan , ..

• Decision on single or multiple-

fuel boiler

• Decision on back pressure or

condensing steam turbine

• System storage and

transportation of sugarcane

bagasse

• System supply and water

treatment

• The environmental issues

• Advanced technology and high

efficiency equipment is preferd

• But modern technology is high

investment cost

• The selling price of product

(power) is fixed at

5.8UScents/kWH

• Strugling between payback (IRR)

and reliability of invested

equipment

5. Challenges and barriers

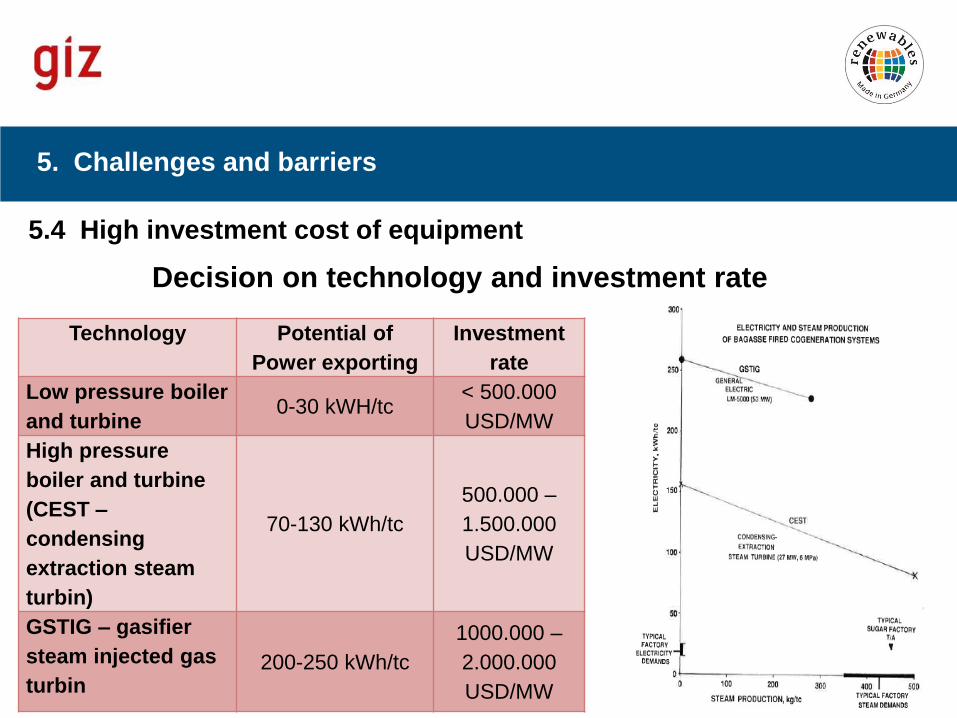

Decision on technology and investment rate

Technology Potential of

Power exporting

Investment

rate

Low pressure boiler

and turbine 0-30 kWH/tc

< 500.000

USD/MW

High pressure

boiler and turbine

(CEST –

condensing

extraction steam

turbin)

70-130 kWh/tc

500.000 –

1.500.000

USD/MW

GSTIG – gasifier

steam injected gas

turbin 200-250 kWh/tc

1000.000 –

2.000.000

USD/MW

5. Challenges and barriers

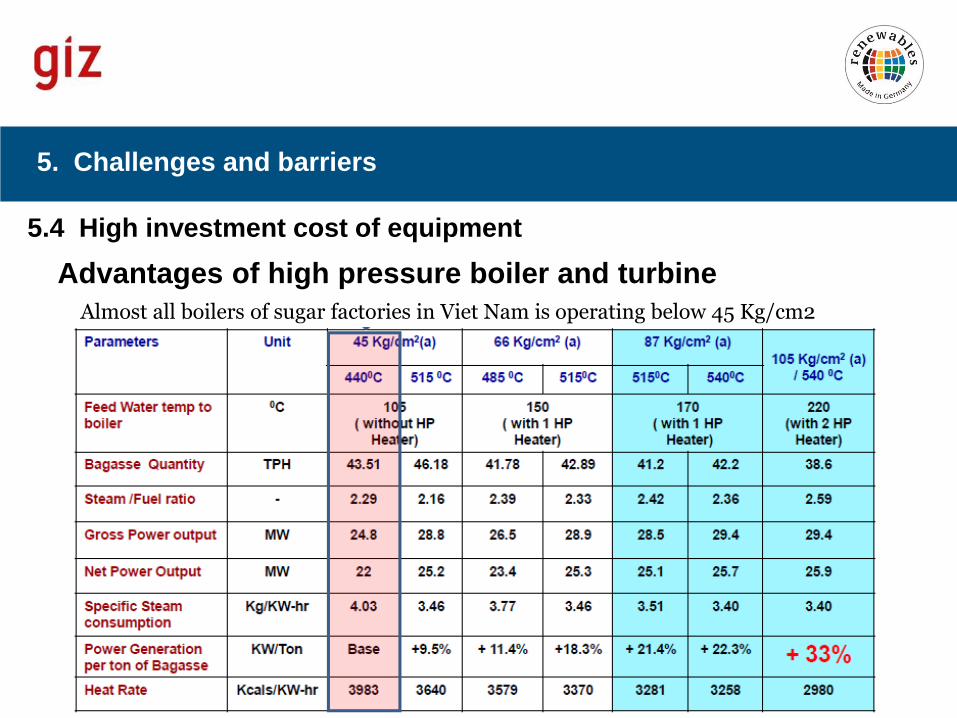

5.4 High investment cost of equipment

Advantages of high pressure boiler and turbine

Almost all boilers of sugar factories in Viet Nam is operating below 45 Kg/cm2

5. Challenges and barriers

5.4 High investment cost of equipment