投資宏觀概覽 -...

TRANSCRIPT

2012年第三季季度報告

- 投資宏觀概覽 3 - 16

- STI 產品績效回顧 17 – 20

- 績效觀察:DFSP Series 21 - 24

- STI 產品展望 25 - 29

目錄

- Global Macro Investment 30 - 43

- STI Products Performance Review 44 - 47

- Performance: DFSP Series 48 - 51 - STI Products Outlook 52 - 56

Table of Contents

2

3

投資宏觀概覽

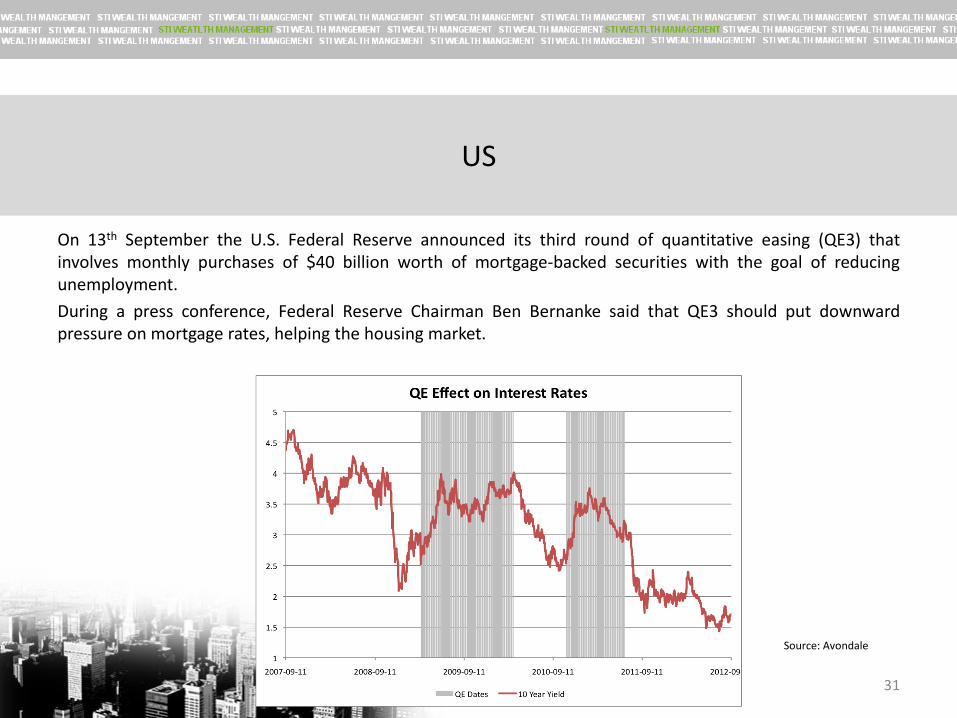

9月13日,聯邦儲備局宣布其第三輪數量寬鬆政策(QE3),每月將購買價值400億美元的抵押擔保證券(mortgage-backed securities) ,目標為增加就業。 在新聞發布會上,聯儲局主席伯南克表示,QE3應可以把加大住房抵押貸款利率下調的壓力,從而幫助房地產市場。

美國

4

資料來源: Avondale

在歐洲,市場焦點在西班牙。西班牙政府剛提交了其2013年的財政預算案,其確認了七月公佈的財政目標:2012財政年度的赤字為GDP的6.3%,及2013年4.5%。

標準普爾10月10日調降了西班牙的債務評級從BBB+至BBB-,是稍高於垃圾債券級別,並警告可能再作進一步下調;標普給予的展望為負面。

歐洲

5

資料來源:彭博

西班牙10年期國債孳息率

在歐盟第四大經濟體西班牙被連降兩級後,第二天環球股市表現各異,歐洲錄得溫和升幅,但亞洲卻下跌。

歐洲

6

資料來源:彭博

摩根士丹利資本國際世界指數

儘管歐元區解體的市場恐懼似乎消退了一段短時間,但要完全排除其可能性卻仍言之過早。希臘的脫歐仍可想像,尤其是如果其對第三次援助的需求越來越明顯。風險是,第三次救助極有可能不受一些核心成員國議會的支持。如是者,希臘可能會決定離開歐盟。

儘管我們認為歐元區解體是一個嚴重的政策失誤,這將帶來不可估計的負面影響,但機會仍然不能被排除;在今年剩下來的幾個月市場恐懼可能再度浮現。

預測

7

至於美國,我們認為其財政懸崖正為經濟增加一個新的威脅。財政懸崖是關於一系列的政策變化,相關法律將在2013年1月1日生效。

到當日,所有前總統喬治·布殊的減稅政策將會到期,即是:

• 社會保障的工資稅額的2個百分點扣減將到期;

• 政府將在未來十年削減總值的在1.2兆美元的開支。

如美國在到期前不能解決財政懸崖的問題,我們預測財政緊縮的推行將令美國國內生產總值收縮 4%左右。

這將令美國人的收入減少以至影響社會整體的消費;由此美國很可能會陷入經濟衰退,產量有可能於2013 年下降0.5%,失業率再上升到9%。美國大選的結果極可能推遲化解財政懸崖的對策,影響經濟增長和市場情緒。

預測

8

在十月初,國際貨幣基金(IMF),將今年全球經濟增長預測由3.5%降低至3.3%;其對2013年的預測為3.6%,對比3個月前的3.9%亦有所下降。

在歐洲、美國、以至全世界旳前景仍不明朗下,我們相信傳統的股票市場將再難為投資者提供穩定而持續的回報;或許,投資者是時候考慮一些傳統股票以外的投資。

預測

9

對於傳統只持長倉的股票投資策略,投資者就像被“戴上手銬”似的,因該策略在三種可能的市場情況下 (即上升,持平及下降) 只有一種會使投資者獲利。這種投資策略的主要風險是,除了高波幅外,在如最近幾年的熊市下,策略可以面臨大幅下挫,又或持續長時間錄得虧損。

相比之下,另類投資的基金經理進行可以進行對沖和賣空,所有這些選擇都可以讓投資組合相較市場表現呈低相關、不相關或甚至負相關。另類投資基金經理並沒“戴上手銬”,他們可以賣空估值過高的資產,並使用精煉的策略管理風險。

傳統股票投資 vs. 另類投資

10

我們看到的趨勢是,另類投資在現今萎靡不振的市場中正變得越來越普遍及重要。很多機構投資者當在另類投資中獲得更多的經驗,以及認識到它們的優勢後,已逐步將他們的投資分散至另類投資產品。

由“傳統”至“另類”

11

資料來源:彭博

道瓊斯瑞信對沖基金指數

在另類投資世界中,全球宏觀投資策略則是一個自由度最大的投資策略,可捕捉在經濟、金融活動或政府干預中所出現的一切可獲利的機會。

全球宏觀投資:

• 利用宏觀經濟的原則確定所有的資產價格錯位

• 不受地區限制,可在世界上的任何地方尋求價格錯位

全球宏觀投資不限於特定的市場或產品,不像其他的對沖投資有一定的約束力。全球宏觀投資有更廣泛的投資權限,基於其靈活性,使宏觀投資策略在重大的國際政治和經濟事件,仍然可能獲取很高的經風險調整後回報。

標普500指數

另類投資:全球宏觀投資策略

12

• 從上而下的投資分析是全球宏觀投資的主要方法之一,用來尋找全球可能的獲利機會。

• 全球宏觀基金採立多種投資策略,其投資目標是實現豐厚的正投資收益,全球宏觀投資策略利用槓桿,投資於範圍廣泛的投資工具和金融市場,包括股票,股票相關工具,貨幣,商品,固定收益和其他債務工具及衍生工具等等。

標普500指數 全球宏觀策略

13

全球宏觀交易分類如下:

單向趨勢交易:預測價格走勢

– 看漲美元時單一買入美元指數

雙向相對值交易:對類似的兩個資產同時買入和賣出來捕捉相對值之間的差價

– 購買美國指數和賣空歐洲指數

典型例子:

• 1992年索羅斯狙擊英鎊,透過賣空超過100億英鎊,最終逼使英國央行讓英鎊貶值。這堪稱全球宏觀投資策略的典範。有人估計,索羅斯在此役中獲得了約10億美元的利潤。

標普500指數

全球宏觀策略

14

為什麼全球宏觀策略

• 在金融危機後,市場是由國際新聞主導而不是基本因素帶動。

• 市場很容易受到全球性活動影響,投資者波動情緒觸使傳統股票型基金經理將難以為投資者帶來穩定回報

• 單純的長期持有策略已不能適應市場變化,只有靈活的全球投資宏觀才能應對市場的發展。

標普500指數 全球宏觀策略

15

VIX波動率指數

資料來源:彭博

恆生指數和美國經濟衰退時間(以紅色突出顯示)

全球宏觀投資策略

• 全球宏觀投資策略有更廣泛的投資範疇,可提供更大的靈活性來捕捉高波動性的市場中所出現的機會,可讓投資人從升市、跌市或波動市中獲利。

• 著眼於宏觀的發展和有能力利用各種投資工具,在控制下行風險的同時創造回報。

標普500指數 概括

16

STI 產品績效回顧

17

18

POWERFUND – 持續為投資人提供穏定回報

POWERFUND於第三季表現符合基金經理於年初所訂立之目標,基金價格於第三

季升1.4%,年初至今上升6.83%。

每月基金回報率都有約0.5%,符合基金所成立之目標,即透過與傳統資產的低相

關性,為投資者提供多元化好處。

19

20

績效觀察 : DFSP Series

21

STI旗下DFSP美元基金於本年第三季錄得正報酬率,淨資產升值2.17%。無論金融

市場走向為何,DFSP系列基金仍維持穩定報酬率。

STI旗下DFSP歐元基金於2012年第三季上升4.37%,回報主要受惠於套利操作上的

表現。相對於傳統的股票基金,本基金更能分散風險,獲得更令人滿意的回報/

風險比率。

22

Diversified FX Trading Segregated Portfolio (USD/EUR)

23

24

STI 產品展望

• 儘管美聯儲會宣布啟動新一輪數量寬鬆,投資者關注其他央行也遵循美聯儲的腳步,從而為美元帶來支撐。

• 我們認爲美元將在目前水準整固,因為美聯儲將繼續採用開放式資產政策。

• 長期來看,我們期待更令人鼓舞的經濟數據在2012年的最後一個季度出現,我們相信美元持續向上。

STI 產品展望

美元指數–過去一年走勢圖

• 在第三季,歐元從低位反彈,便一直維持其上升軌。因爲歐洲信貸風險緩和市場價格已經消化所有不利消息。

• 短期來看,我們預期歐元有可能會維持其上升軌是因爲市場預期西班牙會接受救市援助和歐洲央行購買短期西班牙的債務。

• 然而,我們並不預期進一步大幅反彈,因為歐洲經濟數據持續偏弱。

STI 產品展望

歐元兌美元–過去一年走勢圖

市場預期之外,日本央行推出進一步的貨幣刺激手段來壓制日圓上升,但是日本央行對日元匯率的干預並沒有造成實質性的影響。我們認為日圓將在目前水平整固,因為越來越多的政治壓力在驅動日本央行擺脫日本通貨緊縮的問題,央行可能因而再行干預。我們期待日圓在未來幾個月內走弱。

我們繼續維持對鎊看淡的觀點,因為英國的公共部門和私營企業都經歷了一連串的裁減槓桿。英國整體經濟數據預測中仍是薄弱,在2012年更有收縮的可能性。我們預計今年英倫銀行會有進一步放寬貨幣政策。

STI 產品展望 歐元兌美元–過去一年走勢圖

美元兌日圓–過去一年走勢圖

主要來說,基金維持美元和歐元逐步上升趨勢的看法,因為經濟數據會逐漸改善。然而美聯儲會將繼續採用開放式資產回購政策,這因素將會阻止美元大幅反彈。但我們看到其他央行可能為了抵禦強勢地方貨幣而進行干預,以抵消QE3的效果,最終引發新一輪貨幣戰爭。

STI 產品展望

30

The Global Macro Investment

On 13th September the U.S. Federal Reserve announced its third round of quantitative easing (QE3) that involves monthly purchases of $40 billion worth of mortgage-backed securities with the goal of reducing unemployment.

During a press conference, Federal Reserve Chairman Ben Bernanke said that QE3 should put downward pressure on mortgage rates, helping the housing market.

US

31

Source: Avondale

In Europe, the focus was on Spain. The Spanish government has presented its 2013 Budget, which confirmed the fiscal targets announced in July: a 2012 fiscal deficit of 6.3% of GDP and of 2013’s 4.5%.

Standard & Poor's lowered Spanish debt rating from BBB+ to BBB- on 10th Oct, just a level above junk bond, and warned of possible further downgrades. The ratings company left the country with a negative outlook.

EU

32

Source: Bloomberg

Spanish Government Generic Bonds-10 Year Note

World stock markets were mixed the next day with Europe recorded modest gains while Asia slumped, after Spain, the fourth-largest Euro economy, was slapped with the two-notch credit downgrade.

EU

33

Source: Bloomberg

MSCI World Index

We think that while break-up fears have been subsided for a short period, it would still be premature to eliminate the scenario of the Euro-zone break-up entirely. The exit of Greek remains conceivable, especially if it becomes clear that Greece will need a third bailout. There is a significant risk that another bailout would not be supported in some of the core countries’ parliaments. If so, Greece might decide to leave in order to devalue and get its way out of the crisis.

While we think Euro breakup would be a severe policy mistake with inestimable negative consequences, divorce still cannot be ruled out and break-up fears may possibly resurface in the remaining months of the year.

Outlook

34

For U.S., we think the fiscal cliff adds a new threat to the U.S economic growth. The fiscal cliff describes a series of policy changes that current law will put into effect at 1st January, 2013.

Till the day, all the tax cuts passed by former president George W. Bush will be expired; i.e.

• the expiration of a temporary 2 percentage point reduction in social security payroll taxes; and

• indiscriminate spending cuts worth $1.2tn over the next decade.

If the US fails to resolve the problem before it gets worse, we expect the automatic fiscal tightening policies will cut about 4% of its GDP.

We see that a withdrawal of income from the economy that will affect spending, and so the US is likely to suffer a recession, with the output falling 0.5% in 2013 and the unemployment rate rise again to 9%. Uncertainty of U.S. election outcome could delay the resolution of the cliff, hit growth and market sentiment.

35

Outlook

On early October, the International Monetary Fund reduced its growth forecast for the world economy this year to 3.3% from 3.5%. The forecast for growth for 2013 is 3.6%, down from the 3.9% three months ago.

With Europe, U.S., and the world’s outlook remains uncertain, we believe that the traditional stock market will be difficult to provide investors a stable and continuous positive return in the future. Perhaps, it is time for investors to consider some other investments than traditional equities.

36

Outlook

For the traditional long-only equity strategy, investors are “handcuffed” in the sense that the strategy only profits from one of three possible market scenarios, i.e., rise, flat, and declining. The key risks of long-only equity investments are that they are highly volatile and, in bear market trend like recent few years, they have the potential for either large drawdowns and negative returns for prolonged periods of time.

Alternative investments, by contrast, give portfolio managers the flexibility to hedge, short-sell and utilize options, all of which can lead to an aggregate investment profile that is less correlated, uncorrelated or even negatively correlated to the market and other risk assets. Managers of alternative investments are not handcuffed by the restrictions imposed on long-only investments. They are free to short overvalued assets and use sophisticated tools to manage volatility.

Traditional Equity Investments vs. Alternatives

37

Alternative investments, while more challenging to understand and evaluate, are nonetheless becoming more prevalent and more important in current markets’ malaise. Large institutions are allocating an increasing portion of their assets to alternatives as they gain more experience with these investments and recognize their significant advantages.

Going from “Traditional” into “Alternative”

38

Source: Bloomberg

Dow Jones Credit Suisse Hedge Fund Index

In the alternative investment universe, Global Macro strategy is perceive as one of the most flexible investment strategy, which could capture the arising opportunities from economic, financial activities or policy intervention.

Generally, Global Macro Funds are operated under two main investment objective:

I. utilize macroeconomic principles to identify the dislocation in all asset prices.

II. Dislocations are sought anywhere in the world

Unlike other hedge funds which are limited by certain constraints Global Macro funds are not limited to particular market or product. The broad mandate would allow macro funds generate large return even in major international political and economic events because of their flexibility moving from market to market.

標普500指數

Alternative Investment: The Global Macro Strategy

39

• Emphasizes on top-down approach with global themes and focuses on dislocation of major markets

• A Global Macro strategy is not limited to certain markets or products, apply multi-strategies approach to generate outsized positive returns by making leverage bets on price movements in wide range of instruments and markets, including, but not limited to equities, indexes, currencies, commodities, fixed-income and other debt-related instruments and derivative instruments.

標普500指數 Global Marco Strategy

40

Global Macro trades are classified as:

Outright Directional: forecast on price movements

-Long US Dollar Index, while bullish dollar

Relative Values: similar assets are paired on long and short side to capture a perceived relative mispricing

- Long US Indexes vs. short European Indexes

Real Case Example:

• A classic example would be currency speculation by George Soros in 1992, a global macro hedge-fund manager, became well-known for breaking the Bank of England by sold short more than $10 billion in pounds, the fund netted $1 billion in profits by betting that BoE would be forced to devalue the pound.

標普500指數

Global Marco Strategy

41

Why Global Macro?

• After the financial crisis, the markets has been driven more by news headline than fundamentals.

• The markets are susceptible to global events; wide swing in sentiment would be difficult for traditional equity funds mangers to generate high returns for investors.

• The pure buy and hold strategy is no longer suit the rapid changing market conditions, only the Global Macro could capture the macro economic developments.

標普500指數 Global Marco Strategy

42

VIX Volatility Index Hang Seng Index/Time Frame of US Recession (highlighted in Red)

Global Macro

• Broader mandate would provide the flexibility for managers to seek absolute returns for investors, while accommodate high volatility of the market.

• Focus on the macro development of the world and ability to participate in any markets or instrument, usually take positions that have limited downside risk and potentially large rewards.

標普500指數 To Sum Up…

43

STI Products Performance

44

45

The Q3 performance of POWERFUND was in line with the expectation of the fund manger. The fund’s NAV was up 1.4% in the third quarter, bringing the YTD return to 6.83%. The monthly returns were about 0.5%, in line with our target, i.e. diversification through correlations with traditional assets.

POWERFUND – Stable and Persistent Positive Return

46

47

Performance Review: DFSP Series

48

DFSP USD Fund rose 2.17% in Q3 of 2012. Regardless of the market conditions, DFSP Serial Fund

is able to deliver a stable return.

DFPS EUR Fund of STI rose 4.37% in Q3 of 2012. The return mainly derived from the

performance in arbitrary operation. Comparing to traditional equity fund, the Fund

demonstrates its capability to disperse risk and attain higher return-to-risk ratio.

49

Diversified FX Trading Segregated Portfolio (USD & EUR)

50

51

STI Products Outlook

• Despite the announcement of further quantitative easing by the Fed, the Dollar found support with investors’ concern on the possibility of central banks following similar footsteps of the Fed.

• We believe the USD will consolidate at the current level, with the continued open-ended asset by the Fed.

• In longer-term, we expect more encouraging economic data to roll out in the last quarter of 2012, we believe USD would form an upward trend.

STI Products Outlook

US Dollar Index Future Daily Price Chart

• The Euro has rallied from its low in the third quarter, as European credit risk eases and the markets have priced in all of the downside news.

• In short-term, the Euro would likely to gain with markets continue to expect a Spanish bailout and ECB to buy short-term Spanish debt.

• However, we do not anticipate a further substantial rally in Euro as European data are expected to be soft.

STI Products Outlook

EURUSD Daily Price Chart

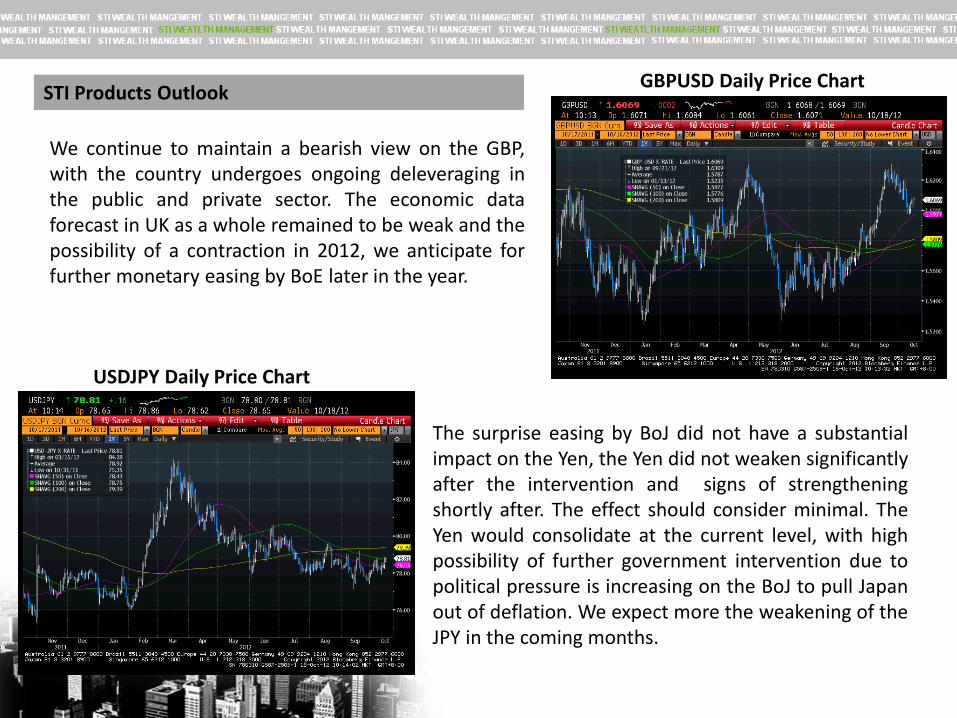

The surprise easing by BoJ did not have a substantial impact on the Yen, the Yen did not weaken significantly after the intervention and signs of strengthening shortly after. The effect should consider minimal. The Yen would consolidate at the current level, with high possibility of further government intervention due to political pressure is increasing on the BoJ to pull Japan out of deflation. We expect more the weakening of the JPY in the coming months.

We continue to maintain a bearish view on the GBP, with the country undergoes ongoing deleveraging in the public and private sector. The economic data forecast in UK as a whole remained to be weak and the possibility of a contraction in 2012, we anticipate for further monetary easing by BoE later in the year.

STI Products Outlook GBPUSD Daily Price Chart

USDJPY Daily Price Chart

In general, we believe the Dollar and Euro would maintain a gradual upward trend with more

improving economic data. However, the continued open-ended buying program by the Fed

would prevent the Dollar forming a substantial rally, but we see the possible intervention by

other central banks to offset the effect of QE3 and eventually turning to currency wars.

STI Products Outlook

詳情請聯絡

網址:www.stiwealth.com

重要聲明:

本文件僅供討論使用,可能不適用於任何投資人。在任何情況下,本文件不構成報價。本文所呈現的資料、觀點或意見乃來自整個社會大眾的許多不同消息來源及撰稿人。請注意,文件內容不一定代表或反映出STI WEALTH MANAGEMENT或其關係企業的觀點與意見。

For further information, please contact

E-mail: [email protected]

Web : www.stiwealth.com

Important Notice :

This documentation is for discussion purpose only and may not be appropriate for any investor. Without limitation, this document does not constitute an offer. Information, views or opinions expressed in this presentation originates from many different sources and contributors throughout the general community. Please note that the contents do not necessarily represent or reflect the views and opinions of STI WEALTH MANAGEMENT or their affiliates.