chapter three security markets. 证券市场的功能 n 优化资源配置 n 筹集资金...

TRANSCRIPT

CHAPTER THREE

SECURITY MARKETS

证券市场的功能 优化资源配置 筹集资金

•筹集的资金长期稳定•可以连续筹资•筹资的规模和速度大大提高

资产定价•有利于证券价格的统一和定价的合理

提供证券的流动性

证券市场的参与者

证券市场主体•证券发行人

包括政府、金融机构、企业•证券投资者

个人投资者、机构投资者(投资基金公司、信托投资公司、证券公司、信托基金、退休基金、养老基金、年金等社会福利团体)

证券市场的参与者 证券市场中介

• 证券承销商和证券经纪商• 证券交易所以及证券交易中心• 具有证券律师资格的律师事务所• 具有证券从业资格的会计师事务所或审计事务所• 资产评估机构• 证券评级机构• 证券投资咨询与服务机构

证券市场的参与者

自律性组织•中国证券业协会和中国国债协会

证券监管机构•证监会

证券市场的结构 按照功能划分:

•一级市场—证券发行市场•二级市场—证券交易市场

按照交易的证券品种划分:•股票市场•债券市场•基金市场•衍生证券市场

二级市场的结构 场内交易市场

• 由证券交易所为代表的集中有形交易市场• 具有固定的场地和交易时间• 符合规定的证券经批准上市买卖

场外交易市场• 柜台交易市场、第三市场、第四市场• 不在证券交易所内进行交易• 价格、时间灵活、佣金、手续费低廉、无场地限制• 相对投机性强、风险度大

证券交易所

由经纪人和证券商组成的进行证券集中交易的场所。

为证券交易提供固定的场所、人员和设施,对证券交易进行组织和管理。

封闭的组织

场外市场

柜台市场、店头市场 在证券交易所外部通过证券商之间或证

券商与客户间完成证券交易的市场。 包括未上市的证券和一些上市的证券。 二板市场—创新型中小企业 NASDAQ

第三、四市场

第三市场•在场外市场上从事已在交易所挂牌上市的证

券交易。•最低佣金的限制促进了第三市场的发展。

第四市场•买卖双方直接交易的市场•美国:计算机自动报价和撮合成交或电话商

谈。

TYPES OF SECURITY MARKETS

CALL MARKETS•have posted hours for trading only

•“called” securities are for sale to those buyers or sellers

TYPES OF SECURITY MARKETS CONTINUOUS MARKETS

•trading may occur at any time during a regular trading day

•dealers (market makers)provide liquidity to brokers who cannot

find a suitable buyer or sellerusually are temporary positions

MAJOR U.S. SECURITY MARKETS THE NEW YORK STOCK EXCHANGE

(NYSE)•established as a corporation, with a

charter and regulations for membership

•approximately 1,366 members

•Board of Directors: 26 elected

MAJOR U.S. SECURITY MARKETS NYSE SEATS:

•purchased from a current member

•give privileges to members to execute trades

•held by individuals as well as brokerage firms

MAJOR U.S. SECURITY MARKETS LISTED SECURITIES: Some criteria

to list•the degree of national interest

•relative position and stability in the industry

•prospects of maintaining its relative position

TRADING HALTS

THE EXCHANGE MAY IMPOSE TRADING HALTS AND CIRCUIT BREAKERS•Trading Halts:

are temporary suspensions of trading in a listed firm’s shares

TRADING HALTS

•Circuit Breakers: Rule 80Arule states that if the Dow Jones

Industrial Average (DJIA) moves 50 or more points from a previous closing price, all index arbitrage orders will be subject to the “tick test.”

TRADING HALTS

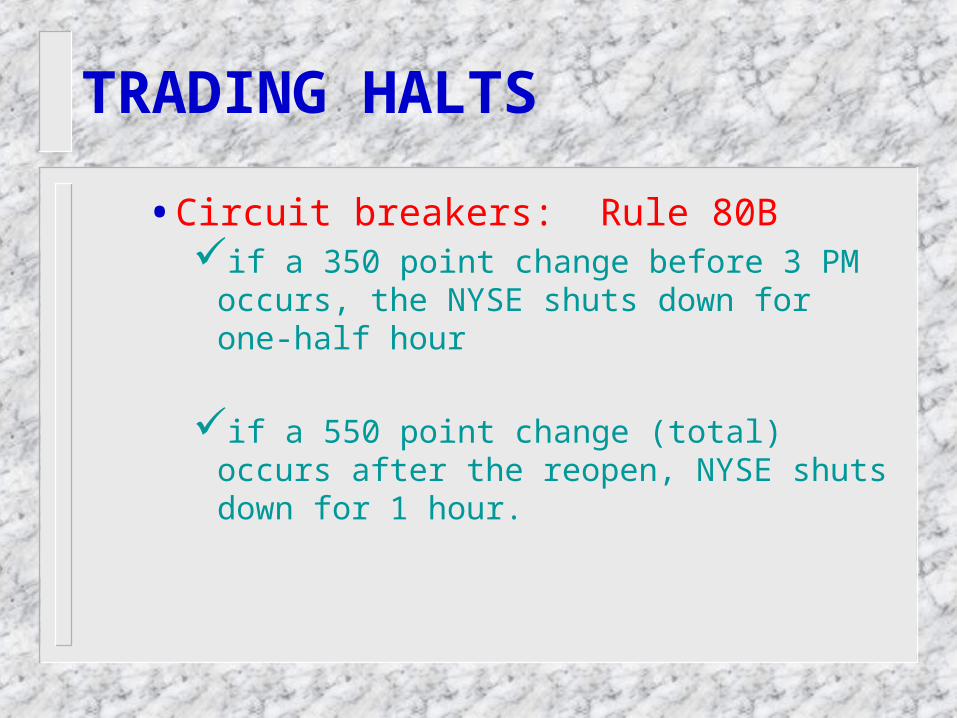

•Circuit breakers: Rule 80Bif a 350 point change before 3 PM

occurs, the NYSE shuts down for one-half hour

if a 550 point change (total) occurs after the reopen, NYSE shuts down for 1 hour.

PLACING AN ORDER

4 TYPES OF NYSE MEMBERSHIPS:•commission brokers:

earn commission for their brokerage firms•floor brokers:

assist commission brokers during overload periods•floor traders:

trade only for themselves•specialists:

keep unfilled limit orders/act as market makers

PLACING AN ORDER

LARGE ORDERS:•Found in blocks of at least 10,000

shares

•Usually place by institutional investors

•Handled mostly by upstairs dealer market

PLACING AN ORDER

SMALLER ORDERS:•in the past these orders were often

overlooked in favor of larger orders

PLACING AN ORDER

•to correct this oversight the SuperDOT system was create

•stands for Super Designated Order Turnaround:handles smaller orders involving 30,999 or fewer shares

orders sent directly to trading post specialist for immediate exposure and execution

facilitates the trading technique known as program trading

OTHER EXCHANGES

THE AMERICAN STOCK EXCHANGE:•Lists stocks of smaller-sized

companies

OTHER EXCHANGES

REGIONAL EXCHANGES:•Boston

•Cincinnati

•Chicago

•Pacific

•Philadelphia

OTHER EXCHANGES

REGIONAL EXCHANGES:•Options

Chicago Board Options Exchange– one of the largest

•FuturesThe Chicago Mercantile Exchange

– offers interest rate, commodities, and index futures contracts

OVER-THE-COUNTER MARKET NASDAQ is an o-t-c market:

•created by the National Association of Securities Dealers (NASD)

•the NASD created the NASD automated quotation system (NASDA) to clear transactionsa nationwide communication network

allows instant access to all major dealers

OVER-THE-COUNTER MARKET NASDAQ CLASSIFICATION OF

STOCKS:•National Market System (NMS)

stocks with larger trading volumesstocks that are eligible for margin and

short transactionsSmall Cap Issues

THIRD AND FOURTH MARKETS THIRD MARKET:

•A name for a market where any trading of NYSE security is permittedtrading hours are not fixedtrading is not bound by NYSE trading

halts or circuit breakers

THIRD AND FOURTH MARKETS THE FOURTH MARKET:

•Direct trading in exchange-listed securities

•Between investors without the benefit of a broker

•Trading facilitated by an automated system: INSTINETgive quotations and executions

information immediately

OTHER METHODS OF ORDERING THE GROSSING SYSTEM PREFERENCING INTERNALIZATION

FOREIGN MARKETS

LONDON STOCK EXCHANGE:•Significantly changed by the “Big

Bang” of 1986:ending fixed commissionsintroduced SEAQ (Stock Exchange

Automated Quotations)attracted trading in non-UK stock

FOREIGN MARKETS

TOKYO STOCK EXCHANGE:•Has introduced major reforms:

introduced CORES (Computer-Assisted Order Routing and Execution System)

introduced FORES (Floor Order Routing and Execution System)

Saitori System of Trading follows IYATOSE Method at market open similar

to a call marekt– Zaraba used where orders are process continuously

FOREIGN MARKETS

TORONTO STOCK EXCHANGE:•Uses CATS (Computer-Assisted

Trading System)

•Similar to IYATOSE trading in Tokyo

INFORMATION- AND LIQUIDITY-MOTIVATED TRADERS THE DEALER’S DILEMMA: Adverse

Selection•Assume there are two types of

traders that a dealer may confront during the trading day:informed traders whose information and

identity are unknown to the dealeruninformed (liquidity) traders

INFORMATION- AND LIQUIDITY-MOTIVATED TRADERS THE DILEMMA: How to quote the

correct price and make a profit?•Solution:

set the bid-ask spread wide enough so that the gains from the uninformed traders offsets the mistaken price quotes to the informed traders.

REGULATION OF SECURITIES MARKETS THE FOUR PILLARS OF SECURITY

REGULATION:•The Securities Act of 1933

•The Securities Exchange Act of 1934

•The Investment Company Act of 1940

•The Investment Advisors Act of 1940

REGULATION OF SECURITIES MARKETS

•Provisions of the Securities Act of 1933known as the “truth in securities” lawrequires registration of new issuesdisclosure of relevant information by

issuerprohibits misrepresentation and fraud

REGULATION OF SECURITIES MARKETS

•Provisions of the Securities Exchange Act of 1934requires national exchanges, brokers, and d

ealers to be registeredmade possible creation of Self Regulatory Or

ganizations (SROs) to oversee the industryestablished the Securities Exchange Commis

sion (SEC)

REGULATION OF SECURITIES MARKETS

•Provisions of the Investment Company Act of 1940extends disclosure and registration

requirements to investment companies

REGULATION OF SECURITIES MARKETS

•Provisions of the Investment Advisors Act of 1940

required registration of those providing advice

END OF CHAPTER 3